|

시장보고서

상품코드

1836467

관성항법 시스템 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Inertial Navigation System (INS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

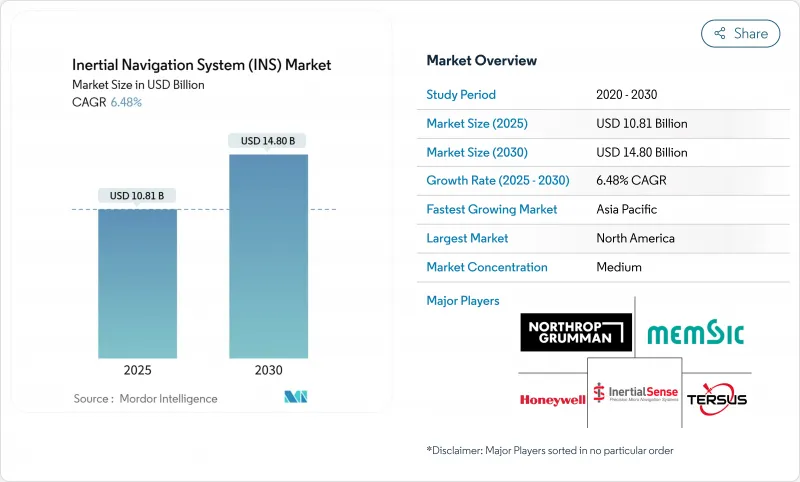

관성항법 시스템 시장 규모는 2025년에 108억 1,000만 달러에 달하고, 2030년에는 148억 달러에 이르며, CAGR 6.48%를 나타낼 것으로 예측됩니다.

미국 국방부의 1,410억 달러의 연구 예산이 GPS-Enterprise 구상에 15억 달러를 충당하는 등, 국방 배분 증가가 탄력성 있는 내비게이션 플랫폼 수요를 지지하고 있습니다. 미국 해군 연구소의 Continuous 3D-Cooled Atom Beam Interferometer와 같은 획기적인 기술은 GPS를 사용하지 않는 시나리오에서 성능을 제한하는 드리프트 한계를 해결합니다. 하니웰의 2억 유로(2억 2,600만 달러)를 투자한 Civitanavi Systems의 인수로 대표되는 전략적인수로 센서 노하우가 통합되어 세계 전개가 확대되고 있습니다. 비용 효율적인 MEMS 아키텍처는 방위 분야 이외의 채택을 확대하고, 광학 및 양자 기반 자이로스코프는 프리미엄 틈새 시장을 개척하고 있습니다. 상업우주비행, 자율주행차, 무인시스템은 각각 정부와 기업이 탄력성 있는 위치·항법·타이밍(PNT) 솔루션을 우선하고 있기 때문에 수년에 걸친 규모의 확대가 전망됩니다.

세계의 관성항법 시스템 시장 동향과 인사이트

군사 및 방위비 증가

방어의 근대화로 인해 관성항법 시스템 시장에는 전례없는 자금이 투입되고 있습니다. 미국의 RDT&E 배분액은 1,410억 달러로 고정밀 INS 페이로드와 원활하게 통합하는 GPS-Enterprise 프로그램에 15억 달러를 충당하고 있습니다. 유럽 계약자도 이 기세를 반영하고 있으며, 탈레스는 2024년 수주로 253억 유로(275억 달러)를 기록했으며, 여기에는 육해군 플랫폼을 위한 내비게이션 장비가 포함되어 있습니다. AN/WSN-7 Ring Laser Gyro Navigator와 같은 해군의 이니셔티브는 GPS에 의존하지 않는 작전에 대한 전술적 축족을 강조하는 것입니다. NATO의 표준화된 선박 관성항법 시스템의 채택은 전체 동맹의 조화를 강조합니다. 이러한 프로그램을 종합하면 방사선 내성과 전자전에 대한 내성을 갖춘 내비게이션 등급 센서 수요가 가속화되고 있습니다.

자율주행차에 채용 확대

자동차 OEM은 견고한 INS를 레벨 4-5의 자율성 전제조건으로 간주하고 관성항법 시스템 시장의 상당 부분을 자극하고 있습니다. 느슨하게 결합된 5G-IMU 퓨전 방식은 실행 시간의 95%로 14cm의 정밀도를 실증하고 있으며, 종래의 GPS만의 방식을 능가하고 있습니다. 이 분야의 CAGR 8.2%는 단순한 프리미엄 플릿뿐만 아니라 대중 시장 모델에서의 채용을 반영하고 있습니다. 실리콘 카바이드로 제조된 MEMS 자이로는 80°C에서 460만 Q 인자를 달성하고 0.5°*h-1 이하의 바이어스 불안정성을 유지합니다. 언센티드 칼만 필터를 사용한 센서 퓨전은 RMS 오차를 5m 이하로 줄여 차선 수준의 유도를 강화했습니다. 규제가 안전 기준에 수렴함에 따라 Tier One 공급업체는 이중 중복 IMU를 통합하여 INS를 선택 사양 애드온이 아닌 핵심 설계 요소로 전환합니다.

내비게이션 등급 시스템의 고비용

내비게이션 등급 어셈블리의 가격은 5만 달러에서 20만 달러이기 때문에 지금까지 비용에 민감한 분야에서의 보급은 제한적이었습니다. MEMS의 수율은 향상되고 있는 것, 전술 그레이드의 대체품에 비해 3배의 가격차가 있기 때문에 신흥 경제국에서의 채용은 여전히 억제되고 있습니다. 아네로 포토닉스가 개발한 칩 스케일 광자이로는 재료비를 억제하면서 100km의 거리 오차를 0.1%로 주장하고 있습니다. 병렬로 수행된 설문조사는 저비용 마이크로컨트롤러 기반 센서 퓨전이 수중에서 서브미터의 정확도를 달성했으며 알고리즘을 강화하여 하드웨어 가격을 부분적으로 상쇄할 수 있음을 입증했습니다. 공급업체는 패브라이트 모델과 라이선스 계약을 채택하여 1대당 교정 오버헤드를 줄이고 있지만, 저렴한 가격이 관성항법 시스템 시장 확대의 중기적인 발판이 되고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 무인 시스템(UAV, UGV, USV)에서의 수요 증가

- 정밀 유도탄을 가능하게 하는 소형화된 INS

- GNSS와 비교한 누적 드리프트 오류

부문 분석

IMU는 2024년 매출의 42.5%를 차지하며 관성항법 시스템 시장의 기초 구성요소로서의 역할을 강화했습니다. 3축 가속도계, 자이로스코프 및 선택적 지자기계의 견고한 단일 패키지 통합으로 배선, 무게, 교정 비용을 절감할 수 있습니다. 이 구성은 단위 경제성이 향상됨에 따라 유도 무기, 산업용 봇 및 소비자 드론으로 확대되고 있습니다. 이 분야는 웨이퍼 레벨 진공 패키징과 머신러닝 기반의 에러 모델링을 통해 앨런의 편차를 2자리 마진으로 줄일 수 있기 때문에 2030년까지의 CAGR은 7.4%를 나타낼 것으로 예측됩니다.

자율적인 창고 로봇과 과수원 로봇은 GNSS 수신이 실내와 밀림 아래에서 떨어지기 때문에 새로운 수요를 보여줍니다. GRU-Transformer 알고리즘은 기존 EKF에 비해 위치의 RMSE를 61.6% 줄이고 고급 필터링의 승수 효과를 강조합니다. 재고 로봇은 비전 지원 IMU를 채택하여 낮은 선반에서 95.8%의 상품 검출을 달성했습니다. 이러한 도입으로 IMU의 유비쿼터스화에 대한 궤도가 강화되어 관성항법 시스템 시장에서의 점유율이 확대되고 있는 것을 확인하였습니다.

MEMS 디바이스의 2024년 매출은 37.0%였지만, 이것은 주조 규모의 확대와 리소그래피의 성숙의 증거입니다. 저전력 및 내충격성으로 인해 MEMS 자이로는 스마트폰과 자동차용 ADAS를 위한 논리적 선택이 되었습니다. MEMS 배송의 CAGR은 8.6%를 나타낼 것으로 예측됩니다. 이것은 팹이 200mm 실리콘 카바이드로 전환하고 높은 종횡비 에칭을 도입하여 400만 개 이상의 Q 팩터를 실현하기 때문입니다.

고정밀 틈새 분야에서는 여전히 링 레이저와 광섬유 자이로에 의존하고 있지만, 광 도파관 온 실리콘 솔루션은 성능 격차를 줄이고 있습니다. 광학 자이로 온 칩은 1cm2 이하의 다이 면적에서 센티미터급의 위치 정밀도를 보고합니다. 동시에 INFN-Pisa의 링 레이저 연구원은 프린지 대비 안정성을 향상시키고 내비게이션 등급 단위의 MTBF를 연장할 수 있습니다. 이러한 혁신이 상업화됨에 따라 MEMS는 관성항법 시스템 시장의 양적 성장의 지점이 되고 있습니다.

관성항법 시스템 시장은 구성 요소별(가속도계, 자이로스코프, 기타), 기술별(메커니컬 자이로, 링 레이저 자이로, 광섬유 자이로, 기타), 성능 등급별(내비게이션 업그레이드, 택티컬그레이드, 인더스트리얼그레이드, 기타), 최종 사용자 산업별(항공우주 및 방위, 해양, 기타), 플랫폼별(항공기, 육상, 기타), 지역별로 구분됩니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역 분석

북미는 2024년 관성항법 시스템 시장의 31.4%를 차지했고 탄력적인 PNT를 우선하는 국방예산 사이클에 의해 활성화되었습니다. Northrop Grumman은 2025년 1분기에 915억 달러의 수주 잔여를 기록했으며, 생체와 미사일 내비게이션 업그레이드를 위한 장기적인 활주로를 강조했습니다. 수출관리규칙 개정 등 규제 합리화로 연간 약 90건의 라이선스 신청이 줄어들어 우주기술 납품이 가속화됩니다. 자율주행 차량의 조종사와 상업 발사 제공업체에 대한 민간 부문의 왕성한 자금 공급은 기술 갱신률을 유지하고 이 지역의 리더십을 강화합니다.

아시아태평양은 방위의 근대화, 반도체 제조 규모의 확대, 무인 항공기의 급속한 도입에 견인되어 2030년까지의 CAGR이 9.3%를 나타낼 것으로 예측됩니다. 일본과 한국은 ADAS와 초소형 이동성에 대한 자본 지출을 늘리고 인도는 국산 항법 별자리가 로켓과 미사일에 대한 국내 INS 통합을 추진합니다. 중국의 스마트폰 OEM은 실내 위치 추적를 향상시키기 위해 듀얼 IMU 셋업의 통합을 계속하고 있어 소비자의 인식을 프리미엄 내비게이션 기능으로 축발을 옮기는데 도움이 되고 있습니다.

유럽은 수직 통합 항공우주 분야의 패자와 협력하는 NATO 프로그램에서 이익을 얻고 있습니다. 하니웰의 시비타 네비 인수는 광섬유 자이로의 지역 공급 기반을 강화합니다. 탈레스는 신흥 시장으로부터의 수주가 49% 증가한 것을 지적하고 유럽 플랫폼의 수출 매력을 강조했습니다. 북해와 지중해의 에너지 탐사에서는 파이프라인 검사용 해저 INS 키트가 요구되고 있어 추가 상승을 가져옵니다. 중동 및 아프리카, 남미에서는 소규모이면서 꾸준히 수요가 늘고 있으며, 해양 시추, 채광, 국경 경비 프로그램 등, GPS에 의존하지 않는 내비게이션이 그 이유가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 군 및 방위비 증가

- 자율주행차의 채용 확대

- 무인 시스템(UAV, UGV, USV) 수요 증가

- 정밀 유도탄을 가능하게 하는 소형화 INS(비공개)

- 필드 로봇이나 스마트 농업을 위한 GNSS와의 통합(비공개)

- 방사선에 강한 INS에 대한 상업 우주 비행의 요구(비공개)

- 시장 성장 억제요인

- 내비게이션 등급 시스템의 고비용

- GNSS에 대한 누적 드리프트 오차

- 심우주 미션에서의 방사선 유발 오차(비공개)

- 신흥 시장에서의 채용을 제한하는 ITAR 수출규제(비공개)

- 가치/공급망 분석

- 규제 상황

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자/소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모와 성장 예측(금액)

- 구성 요소별

- 가속도계

- 자이로스코프

- 자력계

- 관성 측정 장치(IMU)

- 기타

- 기술별

- 기계식 자이로

- 링 레이저 자이로(RLG)

- 광섬유 자이로(FOG)

- 마이크로 전기 기계 시스템(MEMS)

- 반구형 공진기 자이로(HRG)

- 기타

- 성능 등급별

- 내비게이션 등급

- 전술 등급

- 산업용 등급

- 자동차 등급

- 소비자 등급

- 최종 사용자 산업별

- 항공우주 및 방위

- 해양

- 자동차

- 산업 및 제조

- 석유, 가스 및 에너지

- 농업, 광업 및 건설

- 기타

- 플랫폼별

- 항공

- 지상

- 해군

- 우주

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- ASEAN

- 아시아태평양의 기타 국가

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향 및 발전

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- Northrop Grumman Corp.

- Safran Electronics and Defense

- Thales Group

- Bosch Sensortec GmbH

- KVH Industries Inc.

- Trimble Inc.

- NovAtel Inc.(Hexagon)

- iXblue(Exail)

- VectorNav Technologies LLC

- MEMSIC Inc.

- Parker Hannifin-LORD MicroStrain

- Tersus GNSS Inc.

- Inertial Labs Inc.

- Oxford Technical Solutions Ltd.

- Inertial Sense LLC

- Aeron Systems Pvt. Ltd.

- STMicroelectronics NV

- Analog Devices Inc.

- Raytheon Technologies Corp.

제7장 시장 기회와 전망

KTH 25.10.27The inertial navigation system market size stands at USD 10.81 billion in 2025 and is projected to climb to USD 14.80 billion by 2030, advancing at a 6.48% CAGR.

Heightened defense allocations, including the U.S. Department of Defense's USD 141 billion research budget that earmarks USD 1.5 billion for GPS-Enterprise initiatives, are anchoring demand for resilient navigation platforms. Breakthroughs such as the U.S. Naval Research Laboratory's Continuous 3D-Cooled Atom Beam Interferometer are also addressing drift limitations that restrict performance in GPS-denied scenarios. Strategic acquisitions-exemplified by Honeywell's EUR 200 million (USD 226 million) purchase of Civitanavi Systems-are consolidating sensor know-how and extending global reach. Cost-efficient MEMS architectures broaden adoption beyond defense, while optical and quantum-based gyroscopes open premium niches. Commercial spaceflight, autonomous vehicles, and unmanned systems each offer a multiyear runway for scale as governments and enterprises prioritize resilient Positioning, Navigation, and Timing (PNT) solutions.

Global Inertial Navigation System (INS) Market Trends and Insights

Increased Military and Defense Spending

Defense modernization is funneling unprecedented capital toward the inertial navigation system market. The USD 141 billion U.S. RDT&E allocation dedicates USD 1.5 billion to GPS-Enterprise programs that integrate seamlessly with high-precision INS payloads. European contractors mirror this momentum; Thales recorded EUR 25.3 billion (USD 27.5 billion) in 2024 orders that included navigation equipment for land and naval platforms. Naval initiatives such as the AN/WSN-7 Ring Laser Gyro Navigator underscore a tactical pivot toward GPS-independent operations. NATO's adoption of standardized Ships Inertial Navigation Systems highlights alliance-wide harmonization. Collectively these programs accelerate demand for navigation-grade sensors with radiation tolerance and electronic-warfare resilience.

Growing Adoption in Autonomous Vehicles

Vehicle OEMs view robust INS as a prerequisite for Level 4-5 autonomy, catalyzing a sizable slice of the inertial navigation system market. Loosely coupled 5G-IMU fusion schemes have demonstrated 14 cm accuracy for 95% of run-time, eclipsing legacy GPS-only methods. The sector's 8.2% CAGR reflects adoption in mass-market models, not merely premium fleets. MEMS gyros fabricated with silicon-carbide achieve Q-factors of 4.6 million at 80 °C, sustaining bias instability below 0.5°*h-1-an outcome well suited to high-temperature automotive cabins. Sensor fusion using Unscented Kalman Filters has cut RMS errors to under 5 m, bolstering lane-level guidance. As regulation converges on safety standards, tier-one suppliers embed dual-redundant IMUs, turning INS into a core design element rather than an optional add-on.

High Cost of Navigation-Grade Systems

Navigation-grade assemblies priced between USD 50,000 and USD 200,000 have historically restricted penetration in cost-sensitive domains. Although MEMS yields are improving, the three-fold price gap versus tactical-grade alternatives still discourages adoption in emerging economies. Chip-scale optical gyros developed by Anello Photonics claim 0.1% distance error over 100 km while compressing bill-of-materials cost. Parallel research shows low-cost microcontroller-based sensor-fusion achieving sub-meter accuracy underwater, proving that algorithmic enhancements can partially offset hardware pricing. Suppliers are adopting fab-lite models and licensing arrangements to lower per-unit calibration overhead, yet affordability remains a mid-term drag on inertial navigation system market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand from Unmanned Systems (UAV, UGV, USV)

- Miniaturized INS Enabling Precision-Guided Munitions

- Cumulative Drift Error Versus GNSS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IMUs generated 42.5% of 2024 revenue, reinforcing their role as the foundational building block of the inertial navigation system market. Robust single-package integration of tri-axial accelerometers, gyroscopes, and optional magnetometers reduces wiring, weight, and calibration costs. This configuration is scaling into guided weapons, industrial bots, and consumer drones as unit economics improve. The segment is projected to post a 7.4% CAGR through 2030, fueled by wafer-level vacuum packaging and machine-learning-based error modeling that cut Allan variance by double-digit margins.

Autonomous warehouse and orchard robots illustrate emerging demand as GNSS reception degrades indoors or under dense foliage. A GRU-Transformer algorithm trimmed positional RMSE by 61.6% compared with traditional EKF, underscoring the multiplier effect of advanced filtering. Inventory robotics employ vision-aided IMUs to achieve 95.8% item detection on low shelves. These deployments reinforce IMUs' trajectory toward ubiquity and affirm their expanding share within the inertial navigation system market.

MEMS devices owned 37.0% revenue in 2024, a testament to foundry scale and maturing lithography. Lower power draw and shock resilience position MEMS gyros as logical choices for smartphones and automotive ADAS. Forecasts place an 8.6% CAGR on MEMS shipments as fabs switch to 200-mm silicon-carbide and deploy high-aspect ratio etching to realize Q-factors above 4 million.

High-precision niches still rely on ring laser or fiber-optic gyros, yet optical-waveguide-on-silicon solutions are narrowing the performance gap. An optical gyro-on-chip reports centimeter-grade positional accuracy while occupying less than 1 cm2 die area. Concurrently, ring laser researchers at INFN-Pisa improved fringe contrast stability, potentially extending MTBF for navigation-grade units. As these innovations commercialize, MEMS remains the fulcrum for volume growth in the inertial navigation system market.

Inertial Navigation System (INS) Market is Segmented by Component (Accelerometers, Gyroscopes, and More), Technology (Mechanical Gyro, Ring Laser Gyro, Fiber-Optic Gyro, and More), Performance Grade (Navigation Grade, Tactical Grade, Industrial Grade, and More), End-User Industry (Aerospace and Defense, Marine, and More), Platform (Airborne, Land, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 31.4% of the inertial navigation system market in 2024, energized by a defense budget cycle that prioritizes resilient PNT. Northrop Grumman closed 2025 Q1 with USD 91.5 billion backlog, emphasizing long-term runway for avionics and missile navigation upgrades. Regulatory streamlining, such as the Export Administration Regulations amendment, trims roughly 90 annual license applications and accelerates space technology deliveries. Robust private-sector funding for autonomous-vehicle pilots and commercial launch providers sustains technology refresh rates, reinforcing the region's leadership.

Asia-Pacific is projected to post a 9.3% CAGR through 2030, steered by defense modernization, semiconductor fabrication scale, and rapid adoption of unmanned aerial vehicles. Japan and South Korea are raising capital spend on ADAS and micro-mobility, while India's indigenous navigation constellation drives domestic INS integration in launch vehicles and missiles. Chinese smartphone OEMs continue to integrate dual-IMU set-ups to improve indoor positioning, helping pivot consumer perception toward premium navigation capabilities.

Europe benefits from vertically integrated aerospace champions and concerted NATO programs. Honeywell's purchase of Civitanavi bolsters the regional supply base for fiber-optic gyros. Thales noted a 49% upswing in orders from emerging markets, highlighting export attractiveness of European platforms thalesgroup.com. Energy exploration in the North Sea and Mediterranean demands subsea INS kits for pipeline inspection, offering incremental uplift. Smaller but steadily growing demand pockets in the Middle East, Africa, and South America stem from offshore drilling, mining, and border-security programs that all rely on GPS-independent navigation.

- Honeywell International Inc.

- Northrop Grumman Corp.

- Safran Electronics and Defense

- Thales Group

- Bosch Sensortec GmbH

- KVH Industries Inc.

- Trimble Inc.

- NovAtel Inc. (Hexagon)

- iXblue (Exail)

- VectorNav Technologies LLC

- MEMSIC Inc.

- Parker Hannifin - LORD MicroStrain

- Tersus GNSS Inc.

- Inertial Labs Inc.

- Oxford Technical Solutions Ltd.

- Inertial Sense LLC

- Aeron Systems Pvt. Ltd.

- STMicroelectronics NV

- Analog Devices Inc.

- Raytheon Technologies Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased military and defense spending

- 4.2.2 Growing adoption in autonomous vehicles

- 4.2.3 Rising demand from unmanned systems (UAV, UGV, USV)

- 4.2.4 Miniaturized INS enabling precision-guided munitions (under-the-radar)

- 4.2.5 Integration with GNSS for field robotics and smart farming (under-the-radar)

- 4.2.6 Commercial spaceflight need for radiation-hardened INS (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 High cost of navigation-grade systems

- 4.3.2 Cumulative drift error versus GNSS

- 4.3.3 Radiation-induced errors in deep-space missions (under-the-radar)

- 4.3.4 ITAR export controls limiting emerging-market adoption (under-the-radar)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Accelerometers

- 5.1.2 Gyroscopes

- 5.1.3 Magnetometers

- 5.1.4 Inertial Measurement Units (IMU)

- 5.1.5 Others

- 5.2 By Technology

- 5.2.1 Mechanical Gyro

- 5.2.2 Ring Laser Gyro (RLG)

- 5.2.3 Fiber-Optic Gyro (FOG)

- 5.2.4 Micro-Electro-Mechanical Systems (MEMS)

- 5.2.5 Hemispherical Resonator Gyro (HRG)

- 5.2.6 Others

- 5.3 By Performance Grade

- 5.3.1 Navigation Grade

- 5.3.2 Tactical Grade

- 5.3.3 Industrial Grade

- 5.3.4 Automotive Grade

- 5.3.5 Consumer Grade

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Marine

- 5.4.3 Automotive

- 5.4.4 Industrial and Manufacturing

- 5.4.5 Oil and Gas and Energy

- 5.4.6 Agriculture, Mining and Construction

- 5.4.7 Others

- 5.5 By Platform

- 5.5.1 Airborne

- 5.5.2 Land

- 5.5.3 Naval

- 5.5.4 Space

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 ASEAN

- 5.6.4.7 Rest of APAC

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of MEA

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 Northrop Grumman Corp.

- 6.4.3 Safran Electronics and Defense

- 6.4.4 Thales Group

- 6.4.5 Bosch Sensortec GmbH

- 6.4.6 KVH Industries Inc.

- 6.4.7 Trimble Inc.

- 6.4.8 NovAtel Inc. (Hexagon)

- 6.4.9 iXblue (Exail)

- 6.4.10 VectorNav Technologies LLC

- 6.4.11 MEMSIC Inc.

- 6.4.12 Parker Hannifin - LORD MicroStrain

- 6.4.13 Tersus GNSS Inc.

- 6.4.14 Inertial Labs Inc.

- 6.4.15 Oxford Technical Solutions Ltd.

- 6.4.16 Inertial Sense LLC

- 6.4.17 Aeron Systems Pvt. Ltd.

- 6.4.18 STMicroelectronics NV

- 6.4.19 Analog Devices Inc.

- 6.4.20 Raytheon Technologies Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment