|

시장보고서

상품코드

2011929

말초혈관 디바이스 시장 예측(-2031년) : 유형별, 최종사용자별Peripheral Vascular Devices Market by Type (Angioplasty Balloon & Angioplasty Stent, Catheters (IVUS/OCT), Plaque Modification, Vascular Closure Devices, Balloon Inflation Devices, Hemodynamic Flow Alteration), End User - Global Forecast to 2031 |

||||||

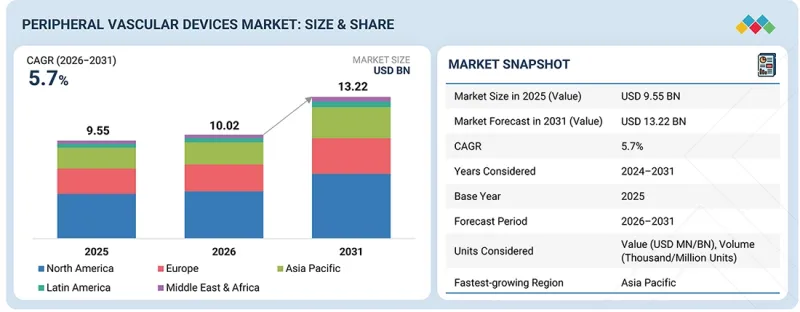

세계의 말초혈관 디바이스 시장 규모는 2026년 100억 2,000만 달러에서 2031년까지 132억 2,000만 달러에 달할 것으로 예측되며, 2026-2031년에 CAGR로 5.7%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러, 1,000/100만개 |

| 부문 | 유형, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

말초혈관기기 시장은 말초동맥질환(PAD) 및 기타 혈관질환의 유병률 증가로 인해 큰 폭의 성장세를 보이고 있습니다. 이러한 질병은 고령화, 당뇨병, 비만, 흡연율 증가와 밀접한 관련이 있습니다. 약물 코팅 풍선, 차세대 스텐트, 동맥절제술 시스템, 색전증 보호 장치 등 저침습적 혈관내 장치의 혁신으로 임상 결과가 크게 향상되고 치료 가능한 환자의 범위가 확대되고 있습니다. 또한 외래 및 외래 수술 센터에서의 수술에 대한 선호도가 높아짐에 따라 많은 지역에서 유리한 상환 정책이 지원되어 이러한 장치의 채택이 가속화되고 있습니다.

또한 조기 진단 및 치료에 대한 인식의 증가, 개발도상국의 의료 인프라 개선, 주요 제조업체의 혁신 및 임상 연구에 대한 지속적인 투자 등이 시장 성장에 기여하고 있습니다.

"혈관성형술용 풍선 시장에서 구식/표준 풍선 부문은 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

혈관성형술용 풍선 시장에서는 비용 효율성, 임상적 전문 지식의 보급, 말초혈관 및 관상동맥 중재시술에서의 범용성 등으로 인해 일반(표준) 풍선에 대한 수요가 증가하고 있습니다. 이러한 풍선은 특히 약제용출성 풍선이 필요하지 않거나 보험 적용이 되지 않는 경우, 병변의 전처리 및 확장 전후의 수술에 여전히 널리 사용되고 있습니다. 첨단 풍선 기술의 등장에도 불구하고 표준 풍선은 사용 편의성, 신뢰성, 다양한 스텐트 시스템과의 호환성으로 인해 요구 수준이 낮고 건수가 많은 시장, 특히 개발도상국에서 꾸준한 판매를 유지하고 있습니다.

"혈행동태적인 혈류 개선 장치 시장에서 색전증 보호 장치 부문은 예측 기간 중 가장 높은 CAGR로 성장할 것으로 예상됩니다. "

혈행동태적인 혈류 변경 장치 시장에서 색전증 보호 장치에 대한 수요가 증가할 것으로 예상됩니다. 이는 원위부 색전증의 위험이 눈에 띄게 높은 복잡한 혈관내 치료 및 구조적 심장질환 치료에서 그 사용이 증가하고 있기 때문입니다. 특히 경동맥, 말초혈관, 경피적 카테터 삽입술에서 뇌졸중 및 장기 허혈과 같은 수술 관련 합병증에 대한 인식이 높아지면서 임상 적용이 가속화되고 있습니다. 또한 포획 효율, 전달성, 혈관 적합성을 향상시키는 장치 설계의 개선이 시장 성장을 크게 촉진하고 있습니다. 이러한 추세는 확립된 가이드라인의 도입과 저침습적 혈관 수술의 확대로 더욱 강화되고 있습니다.

"최종사용자별로는 외래 수술 센터(ASC) 부문이 예측 기간 중 말초혈관기기 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다. "

말초혈관기기 시장은 외래수술센터(ASC)의 긍정적인 영향에 힘입어 큰 폭의 성장세를 보이고 있습니다. 이들 센터는 외래 진료의 편의성과 안전성을 우선시하는 최소침습 수술로의 전환을 추진하고 있습니다. ASC는 수술 비용 절감, 환자 회전율 향상, 입원 기간 단축, 업무 효율성 향상 등 다양한 이점을 제공함으로써 보험사, 의료진, 환자 모두에게 매력적인 선택이 되고 있습니다. 소형화된 이미징 시스템, 로우 프로파일 카테터, 풍선, 동맥절제술 장치와 같은 말초혈관 장치의 혁신으로 가장 복잡한 수술도 ASC 환경에서 시행할 수 있게 되었습니다. 또한 유리한 상환 정책, 의사 소유 모델, 당일 퇴원을 원하는 환자 증가, 말초동맥질환(PAD) 유병률 증가 등이 이 시장에서 ASC의 채택을 가속화하는 데 기여하고 있습니다.

세계의 말초혈관 디바이스 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 말초혈관 디바이스 시장 : 유형별

제10장 말초혈관 디바이스 시장 : 최종사용자별

제11장 말초혈관 디바이스 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

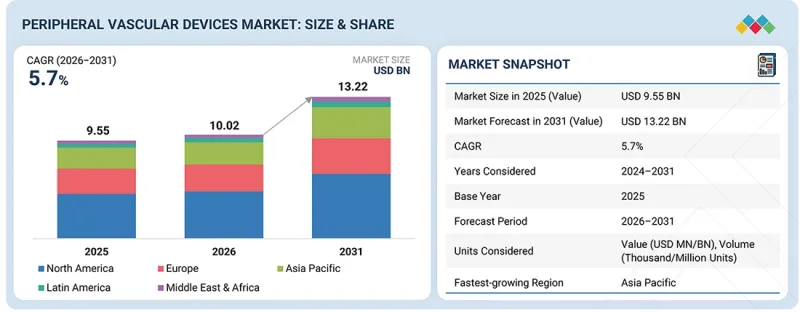

KSA 26.05.04The peripheral vascular devices market is projected to reach USD 13.22 billion by 2031 from USD 10.02 billion in 2026, at a CAGR of 5.7% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion), Volume (Thousand/Million Units) |

| Segments | Type, End user, and Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The peripheral vascular devices market is experiencing significant growth, driven by the rising prevalence of peripheral artery disease (PAD) and other vascular disorders. These conditions are largely linked to the aging population, along with rising rates of diabetes, obesity, and smoking. Innovations in minimally invasive endovascular devices, such as drug-coated balloons, next-generation stents, atherectomy systems, and embolic protection devices, are greatly improving clinical outcomes and expanding the range of patients who can be treated. Additionally, the growing preference for outpatient and ambulatory surgical center-based procedures, supported by favorable reimbursement policies in many regions, is accelerating the adoption of these devices.

Furthermore, increasing awareness of early diagnosis and treatment, improvements in healthcare infrastructure in developing countries, and ongoing investments by major manufacturers in innovation and clinical research are all contributing to market growth.

"The old/normal balloons segment is expected to grow at the highest CAGR in the angioplasty balloons market during the forecast period."

The angioplasty balloons market is experiencing increased demand for plain (standard) balloons due to their cost-effectiveness, availability of clinical expertise, and versatility across peripheral and coronary interventions. These balloons remain popular for lesion preparation, as well as for pre- and post-dilatation procedures, particularly when drug-coated options are either unnecessary or not covered by insurance. Despite the emergence of advanced balloon technologies, standard balloons continue to see strong sales in less demanding, high-volume markets, especially in developing countries, due to their ease of use, reliability, and compatibility with different stent systems.

"The embolic protection devices segment is expected to grow at the highest CAGR in the hemodynamic flow alteration devices market during the forecast period."

Embolic protection devices are expected to see increased demand in the hemodynamic flow alteration devices market. This is due to their growing use in complex endovascular and structural heart procedures, where the risk of distal embolization is notably high. The rising awareness of procedure-related complications, such as stroke and organ ischemia-especially during carotid, peripheral, and transcatheter interventions-has accelerated their clinical adoption. Additionally, improvements in device design, which enhance capture efficiency, deliverability, and vessel compatibility, have significantly supported market growth. This trend is further bolstered by the introduction of established guidelines and the expansion of minimally invasive vascular procedures.

"Based on end users, the ambulatory surgical centers segment is expected to grow at the highest CAGR in the peripheral vascular devices market during the forecast period."

The peripheral vascular devices market is experiencing significant growth, largely driven by the positive impact of ambulatory surgery centers (ASCs). These centers facilitate the shift toward minimally invasive procedures that prioritize the comfort and safety of outpatient care. ASCs offer numerous benefits, including lower procedural costs, faster patient turnover, shorter hospital stays, and improved operational efficiency, making them appealing to payers, providers, and patients alike. Innovations in peripheral vascular devices, such as miniaturized imaging systems, low-profile catheters, balloons, and atherectomy devices, have enabled even the most complex procedures to be performed in ASC settings. Additionally, favorable reimbursement policies, physician ownership models, increasing patient preference for same-day discharge, and the rising incidence of peripheral artery disease (PAD) are all contributing to the accelerated adoption of ASCs in this market.

"The Asia Pacific is estimated to register the highest CAGR during the forecast period."

The primary driver of the peripheral vascular devices market in the APAC region is the rapidly increasing incidence of peripheral artery disease (PAD) and diabetes. This trend is supported by a large aging population and a global shift towards healthier lifestyles. Countries like China, India, and Japan are leading the way in adopting these devices, driven by developing healthcare infrastructure, rising healthcare expenditures, and improved access to advanced endovascular procedures. Additionally, growing awareness of the benefits of minimally invasive interventions, an increasing number of skilled interventional specialists, and a gradual but steady expansion of reimbursement coverage in key markets are also contributing to market growth. Furthermore, low-cost manufacturing, the presence of local companies, and the strategic expansion of global medical device firms are significant drivers of this market's growth in the APAC region.

Key Players

Some of the major players in this market are Boston Scientific (US), Medtronic Plc (US), Abbott (US), Becton, Dickinson and Company (US), Terumo Corporation (Japan), B. Braun Melsungen AG (Germany), Merit Medical Systems (US), Penumbra, Inc. (US), Koninklijke Philips (Netherlands), Stryker (US), Cordis (US), W.L. Gore & Associates (US), Biotronik Stryker (US), Endologix LLC (US), and Cook Medical (US), among others.

Research Coverage

The report analyzes the peripheral vascular devices market, estimating market size and future growth potential across various segments. These segments include angioplasty stents, endovascular aneurysm repair stent grafts, inferior vena cava filters, catheters, angioplasty balloons, plaque modification devices, hemodynamic flow alteration devices, other devices, and end users. Additionally, the report includes a product portfolio matrix of various peripheral vascular devices available in the market. It also provides a competitive analysis of the key players in this market, detailing their company profiles, product offerings, and key market strategies.

Reasons to Buy the Report

This report will provide market leaders and new entrants with valuable revenue estimates for the overall peripheral vascular devices market and its subsegments. It will help stakeholders understand the competitive landscape, enabling them to better position their businesses and develop effective go-to-market strategies. Additionally, the report will offer insights into the current market dynamics, highlighting key drivers, restraints, challenges, and opportunities.

This report provides insights into the following pointers:

- Analysis of key drivers (rapid growth in geriatric population and resulting increase in disease prevalence and favorable reimbursement scenario for peripheral vascular procedures), restraints (availability of alternative treatment options and shortage of skilled professionals with expertise in peripheral vascular devices), opportunities (high growth potential in emerging markets and growing incidence of obesity & diabetes), and challenges (product failures and device recalls).

- Product Developments/Enhancements: Comprehensive details about new product launches and anticipated trends in the global peripheral vascular devices market.

- Product Innovation: Detailed insights on upcoming trends, research & development activities, and new product launches in the global peripheral vascular devices market.

- Market Development: Comprehensive information on the lucrative emerging markets by angioplasty stents, structural heart devices, catheters, angioplasty balloons, plaque modification devices, hemodynamic flow alteration devices, other devices, and end users.

- Market Diversification: Exhaustive information about new products and services or product and service enhancements, growing geographies, recent developments, and investments in the global peripheral vascular devices market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global peripheral vascular devices market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PERIPHERAL VASCULAR DEVICES MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 PERIPHERAL VASCULAR DEVICES MARKET OVERVIEW

- 3.2 ASIA PACIFIC: PERIPHERAL VASCULAR DEVICES MARKET, BY PRODUCT TYPE AND COUNTRY

- 3.3 PERIPHERAL VASCULAR DEVICES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 PERIPHERAL VASCULAR DEVICES MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid growth in geriatric population

- 4.2.1.2 Favorable reimbursement scenario for procedures

- 4.2.1.3 Increasing number of product approvals

- 4.2.1.4 Rising prevalence of diabetes

- 4.2.1.5 Growth in tobacco consumption

- 4.2.1.6 Rising obesity rates

- 4.2.2 RESTRAINTS

- 4.2.2.1 Increasing number of product failures and recalls

- 4.2.2.2 Regulatory complexity and approval delays

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 High growth potential in emerging markets

- 4.2.3.2 Increasing awareness and early diagnosis of PAD

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited availability of alternative treatments

- 4.2.4.2 Dearth of skilled professionals with expertise in peripheral vascular devices

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY KEY PLAYERS, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF PRODUCTS, BY REGION, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT DATA FOR HS CODE 901839

- 5.7.2 EXPORT DATA FOR HS CODE 901839

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 MEDTRONIC

- 5.11.2 TERUMO

- 5.11.3 BOSTON SCIENTIFIC CORPORATION

- 5.12 IMPACT OF 2025 US TARIFFS - PERIPHERAL VASCULAR DEVICES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

- 5.12.5.1 Hospitals

- 5.12.5.1.1 Large chain hospitals

- 5.12.5.1.2 Standalone hospital facilities

- 5.12.5.2 Ambulatory care settings

- 5.12.5.3 Cardiac care centers

- 5.12.5.4 Other end users

- 5.12.5.1 Hospitals

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 Drug-eluting stents

- 6.1.1.2 Atherectomy devices

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Intravascular ultrasound

- 6.1.2.2 Optical coherence tomography

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Remote patient monitoring

- 6.1.3.2 3D printing and patient-specific modeling

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 INSIGHTS ON PATENT PUBLICATION TRENDS, TOP APPLICANTS AND JURISDICTION FOR PERIPHERAL VASCULAR DEVICES MARKET, JANUARY 2015-DECEMBER 2025

- 6.3.2 LIST OF MAJOR PATENTS, 2023-2026

- 6.4 FUTURE APPLICATIONS

- 6.4.1 INTRAVASCULAR LITHOTRIPSY FOR CALCIFIED PAD LESIONS

- 6.4.2 ADVANCED IMAGE-GUIDED INTERVENTIONS

- 6.4.3 SMART SENSOR-INTEGRATED VASCULAR IMPLANTS

- 6.4.4 INTEGRATED MULTI-FUNCTION ENDOVASCULAR DEVICES

- 6.5 IMPACT OF AI ON PERIPHERAL VASCULAR DEVICES MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 Medical Device Quality Management Standard (ISO 13485)

- 7.1.2.2 Biological Evaluation and Biocompatibility of Medical Devices (ISO 10993)

- 7.1.2.3 Vascular Stent Performance Standard (ISO 25539-2)

- 7.1.2.4 Intravascular Access Device Standard (ISO 11070)

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE PACKAGING AND DIGITAL INSTRUCTIONS (BOSTON SCIENTIFIC CASE STUDY)

- 7.2.2 SUSTAINABLE PRODUCT LIFECYCLE MANAGEMENT (ABBOTT CASE STUDY)

- 7.2.3 PACKAGING WASTE REDUCTION INITIATIVE BY MEDTRONIC

- 7.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE SETTINGS

- 8.5 MARKET PROFITABILITY

- 8.5.1 SHIFT TOWARD HIGH-VALUE, DRUG-ELUTING, AND SPECIALTY DEVICES

- 8.5.2 PROCEDURE VOLUME GROWTH DRIVEN BY AGING POPULATION AND PAD PREVALENCE

- 8.5.3 COST OPTIMIZATION THROUGH SUPPLY CHAIN EFFICIENCY AND PORTFOLIO BREADTH

9 PERIPHERAL VASCULAR DEVICES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 ANGIOPLASTY STENTS MARKET, BY TYPE

- 9.2.1 VOLUME ANALYSIS: ANGIOPLASTY STENTS MARKET, BY TYPE

- 9.2.2 DRUG-ELUTING STENTS

- 9.2.2.1 Drug-eluting stents to witness higher adoption due to technological advancements leading to lower restenosis rate

- 9.2.3 BARE-METAL STENTS

- 9.2.3.1 Bare-metal stents, by delivery platform

- 9.2.3.1.1 Balloon-expandable stents

- 9.2.3.1.1.1 Better radial strength and ease of deployment to drive usage

- 9.2.3.1.2 Self-expandable stents

- 9.2.3.1.2.1 Flexibility, tolerance, and support for vessel movement and compression to propel market

- 9.2.3.1.1 Balloon-expandable stents

- 9.2.3.1 Bare-metal stents, by delivery platform

- 9.3 ENDOVASCULAR ANEURYSM REPAIR STENT GRAFTS MARKET, BY TYPE

- 9.3.1 ABDOMINAL AORTIC ANEURYSM STENT GRAFTS

- 9.3.1.1 Rising prevalence of AAA and need for less invasive treatment to drive market

- 9.3.2 THORACIC AORTIC ANEURYSM STENT GRAFTS

- 9.3.2.1 Increasing incidence of thoracic aortic aneurysms to propel adoption

- 9.3.1 ABDOMINAL AORTIC ANEURYSM STENT GRAFTS

- 9.4 CATHETERS MARKET, BY TYPE

- 9.4.1 ANGIOGRAPHY CATHETERS

- 9.4.1.1 Angiography catheters to dominate catheters market

- 9.4.2 GUIDING CATHETERS

- 9.4.2.1 Growing number of target procedures to drive demand for guiding catheters

- 9.4.3 IVUS/OCT CATHETERS

- 9.4.3.1 IVUS/OCT catheters segment to register highest growth

- 9.4.1 ANGIOGRAPHY CATHETERS

- 9.5 INFERIOR VENA CAVA FILTERS MARKET, BY TYPE

- 9.5.1 RETRIEVABLE FILTERS

- 9.5.1.1 Retrievable filters segment to register higher growth due to increase in use as temporary measure to block pulmonary embolism

- 9.5.2 PERMANENT FILTERS

- 9.5.2.1 Advances in other technologies and risks associated with permanent filters to hamper sales

- 9.5.1 RETRIEVABLE FILTERS

- 9.6 ANGIOPLASTY BALLOONS MARKET, BY TYPE

- 9.6.1 OLD/NORMAL BALLOONS

- 9.6.1.1 Old/normal balloons to dominate angioplasty balloons market as they remain effective and widely used

- 9.6.2 DRUG-ELUTING BALLOONS

- 9.6.2.1 Drug-eluting balloons to witness highest growth with increasing demand for angioplasty procedures and rising regulatory approvals for DEBs

- 9.6.3 CUTTING & SCORING BALLOONS

- 9.6.3.1 Preference for medication as primary treatment for atherosclerosis to restrain adoption

- 9.6.1 OLD/NORMAL BALLOONS

- 9.7 PLAQUE MODIFICATION DEVICES MARKET, BY TYPE

- 9.7.1 ATHERECTOMY DEVICES

- 9.7.1.1 Increase in incidence of atherosclerosis to drive market

- 9.7.2 THROMBECTOMY DEVICES

- 9.7.2.1 Growing DVT incidence to drive adoption of thrombectomy devices

- 9.7.1 ATHERECTOMY DEVICES

- 9.8 HEMODYNAMIC FLOW ALTERATION DEVICES MARKET, BY TYPE

- 9.8.1 EMBOLIC PROTECTION DEVICES

- 9.8.1.1 Investments in technological advancements and growing regulatory approvals to drive market

- 9.8.2 CHRONIC TOTAL OCCLUSION DEVICES

- 9.8.2.1 Rise in support for device development especially in addressing longstanding plaque buildup to drive market

- 9.8.1 EMBOLIC PROTECTION DEVICES

- 9.9 OTHER PERIPHERAL VASCULAR DEVICES MARKET, BY TYPE

- 9.9.1 GUIDEWIRES

- 9.9.1.1 Higher success rate during stenting and endovascular aneurysm repair contribute to largest market share

- 9.9.2 VASCULAR CLOSURE DEVICES

- 9.9.2.1 Technological advancements and minimized duration of hospital stay to support demand

- 9.9.3 INTRODUCER SHEATHS

- 9.9.3.1 Potential for reducing arterial damage during interventional procedures to drive adoption

- 9.9.4 BALLOON INFLATION DEVICES

- 9.9.4.1 Integrated technologies and rising number of target procedures to propel adoption

- 9.9.1 GUIDEWIRES

10 PERIPHERAL VASCULAR DEVICES MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOSPITALS

- 10.2.1 ADVANCED INFRASTRUCTURE AND SPECIALIZED EQUIPMENT TO DRIVE SEGMENT GROWTH

- 10.2.2 LARGE CHAIN HOSPITALS

- 10.2.2.1 Strong infrastructure and integrated networks driving dominance in complex peripheral vascular procedures

- 10.2.3 STANDALONE HOSPITAL FACILITIES

- 10.2.3.1 Expanding accessibility and cost-effective care to support peripheral vascular procedure volumes

- 10.3 AMBULATORY SURGICAL CENTERS

- 10.3.1 FASTER PROCEDURE TIME AND LOWER INFECTION RATES TO DRIVE SEGMENT GROWTH

- 10.4 OTHER END USERS

11 PERIPHERAL VASCULAR DEVICES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.2.2 NORTH AMERICA ANGIOPLASTY STENTS MARKET: VOLUME ANALYSIS, BY TYPE

- 11.2.3 US

- 11.2.3.1 Favorable reimbursement scenario to contribute to market growth

- 11.2.4 CANADA

- 11.2.4.1 Increasing cases of chronic conditions to fuel market

- 11.3 EUROPE

- 11.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.3.2 EUROPE ANGIOPLASTY STENTS MARKET: VOLUME ANALYSIS, BY TYPE

- 11.3.3 GERMANY

- 11.3.3.1 Statutory health insurance policy to support market growth

- 11.3.4 FRANCE

- 11.3.4.1 Growing geriatric population to drive market

- 11.3.5 UK

- 11.3.5.1 Increasing volume of coronary angioplasty procedures to sustain market growth

- 11.3.6 SPAIN

- 11.3.6.1 Growing cases of diabetes and obesity to boost market

- 11.3.7 ITALY

- 11.3.7.1 Increasing prevalence of atherosclerotic cardiovascular disease to spur market growth

- 11.3.8 REST OF EUROPE

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 ASIA PACIFIC ANGIOPLASTY STENTS MARKET: VOLUME ANALYSIS, BY TYPE

- 11.4.3 JAPAN

- 11.4.3.1 Large geriatric population to ensure sustained demand

- 11.4.4 CHINA

- 11.4.4.1 Growing incidence of lifestyle diseases to fuel market

- 11.4.5 INDIA

- 11.4.5.1 Rising prevalence of target diseases and growing healthcare expenditure to propel market

- 11.4.6 AUSTRALIA

- 11.4.6.1 High prevalence of cardiovascular and peripheral artery diseases to drive market

- 11.4.7 SOUTH KOREA

- 11.4.7.1 Rising rates of chronic diseases to boost market

- 11.4.8 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 LATIN AMERICA ANGIOPLASTY STENTS MARKET: VOLUME ANALYSIS, BY TYPE

- 11.5.3 BRAZIL

- 11.5.3.1 Rising healthcare expenditure to aid market growth

- 11.5.4 MEXICO

- 11.5.4.1 Increasing prevalence of cardiovascular diseases to spur market growth

- 11.5.5 COLOMBIA

- 11.5.5.1 Growing incidence of peripheral artery diseases to expedite market growth

- 11.5.6 ARGENTINA

- 11.5.6.1 Increasing prevalence of peripheral artery diseases to support market growth

- 11.5.7 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 11.6.2 MIDDLE EAST & AFRICA ANGIOPLASTY STENTS MARKET: VOLUME ANALYSIS, BY TYPE

- 11.6.3 GCC COUNTRIES

- 11.6.3.1 Kingdom of Saudi Arabia (KSA)

- 11.6.3.1.1 Rising diabetes prevalence and strong government healthcare investments to drive market

- 11.6.3.2 United Arab Emirates (UAE)

- 11.6.3.2.1 Advanced healthcare infrastructure and growing medical tourism to accelerate peripheral vascular devices adoption

- 11.6.3.1 Kingdom of Saudi Arabia (KSA)

- 11.6.4 REST OF GCC COUNTRIES

- 11.6.5 REST OF MIDDLE EAST & AFRICA

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.4.1 GLOBAL: PERIPHERAL VASCULAR DEVICES MARKET SHARE ANALYSIS, 2025

- 12.4.2 US: PERIPHERAL VASCULAR DEVICES MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 12.5.5.1 Company footprint

- 12.5.5.2 Regional footprint

- 12.5.5.3 Product type footprint

- 12.5.5.4 End user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 DYNAMIC COMPANIES

- 12.6.3 RESPONSIVE COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.7 BRAND/PRODUCT COMPARISON

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8.1 FINANCIAL METRICS

- 12.8.2 COMPANY VALUATION

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES AND APPROVALS

- 12.9.2 DEALS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 BOSTON SCIENTIFIC CORPORATION

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product approvals

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Other developments

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 BECTON, DICKINSON AND COMPANY

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches and approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.3.4 Other developments

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 ABBOTT LABORATORIES

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices made

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 CARDINAL HEALTH, INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 KONINKLIJKE PHILIPS N.V.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product approvals

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 TERUMO CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.7 MERIT MEDICAL SYSTEMS, INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches

- 13.1.7.3.2 Deals

- 13.1.8 B. BRAUN SE

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product approvals

- 13.1.9 MEDTRONIC

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches and approvals

- 13.1.9.3.2 Deals

- 13.1.10 PENUMBRA, INC.

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches and approvals

- 13.1.11 STRYKER CORPORATION

- 13.1.11.1 Business overview

- 13.1.11.2 Products offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Deals

- 13.1.12 CORDIS

- 13.1.12.1 Business overview

- 13.1.12.2 Products offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Product approvals

- 13.1.12.3.2 Deals

- 13.1.13 COOK

- 13.1.13.1 Business overview

- 13.1.13.2 Products offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Deals

- 13.1.14 W. L. GORE & ASSOCIATES, INC.

- 13.1.14.1 Business overview

- 13.1.14.2 Products offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product approvals

- 13.1.15 BIOSENSORS INTERNATIONAL GROUP, LTD.

- 13.1.15.1 Business overview

- 13.1.15.2 Products offered

- 13.1.16 IVASCULAR

- 13.1.16.1 Business overview

- 13.1.16.2 Products offered

- 13.1.17 BIOTRONIK

- 13.1.17.1 Business overview

- 13.1.17.2 Products offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Product launches

- 13.1.18 ENDOLOGIX

- 13.1.18.1 Business overview

- 13.1.18.2 Products offered

- 13.1.19 ENDOCOR GMBH & CO., KG

- 13.1.19.1 Business overview

- 13.1.19.2 Products offered

- 13.1.1 BOSTON SCIENTIFIC CORPORATION

- 13.2 OTHER PLAYERS

- 13.2.1 MERIL LIFE SCIENCES PVT. LTD.

- 13.2.2 ALVIMEDICA

- 13.2.3 CARDIONOVUM GMBH

- 13.2.4 SMT

- 13.2.5 MEDINOL

- 13.2.6 ANDRAMED GMBH

- 13.2.7 REX MEDICAL

- 13.2.8 QMD

- 13.2.9 BROSMED MEDICAL CO., LTD.

- 13.2.10 ELIXIR MEDICAL

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 Key industry insights

- 14.1.2.3 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.3 GROWTH FORECAST

- 14.3.1 KEY INDUSTRY INSIGHTS

- 14.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RISK ASSESSMENT

- 14.7 RESEARCH LIMITATIONS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.3.1 PRODUCT ANALYSIS

- 15.3.2 US: END-USER ANALYSIS

- 15.3.3 GEOGRAPHIC ANALYSIS

- 15.3.4 COMPANY INFORMATION

- 15.3.5 REGIONAL/COUNTRY-LEVEL MARKET SHARE ANALYSIS

- 15.3.6 COUNTRY-LEVEL VOLUME ANALYSIS BY PRODUCT TYPE

- 15.3.7 MARKET SHARE ANALYSIS, BY PRODUCT TYPE (TOP FIVE PLAYERS)

- 15.3.8 ANY CONSULTS/CUSTOM REQUIREMENTS AS PER CLIENT REQUEST

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS