|

시장보고서

상품코드

2021041

식재 장비 시장 예측(-2031년) : 유형별, 작물 유형별, 디자인별, 지역별Planting Equipment Market by Type (air seeders, seed drills, planters, others ), Design, Crop Type, and Region - Global Forecast to 2031 |

||||||

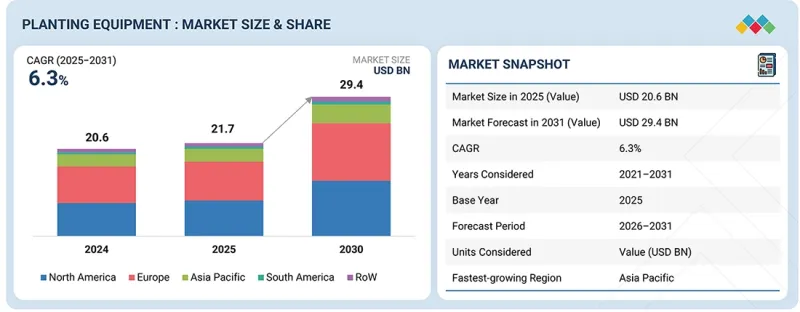

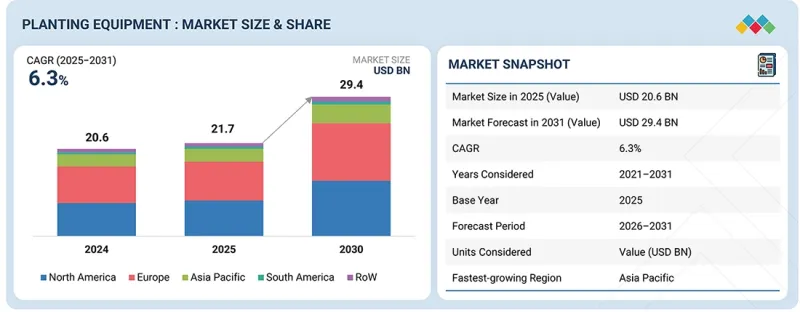

세계의 식재 장비 시장 규모는 2026년에 217억 4,000만 달러로 추계되고 있으며, 2026-2031년에 CAGR 6.3%로 추이하며, 2031년에는 294억 4,000만 달러에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러) 및 톤 |

| 부문 | 유형별, 작물 유형별, 디자인별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

디지털 농업 툴, 정밀 시비 시스템, 데이터베이스 영양 관리 플랫폼의 통합은 재배 장비 산업의 제품 개발 및 현장 성능을 혁신적으로 변화시키고 있습니다. 야라 인터내셔널(Yara International)과 같은 주요 기업은 디지털 농업 솔루션을 활용하여 권장 시비량을 최적화하고, 영양분 이용 효율(NUE)을 향상시키며, 작물 수확량을 향상시키고 있습니다. 이러한 제품 혁신은 정밀농업 및 제어된 영양분 공급 시스템의 발전과 함께 전 세계 재배 장비 시장에서 지속가능한 성장, 지속가능성 향상 및 고부가가치 작물 생산성을 실현하기 위한 토대를 마련하고 있습니다.

재배 장비 시장의 기회와 변화 - 이 분야는 정밀농업의 확대 추세와도 밀접한 관련이 있습니다. 식재 장비 시장은 농가와 제조업체 모두에게 큰 비즈니스 기회를 제공하고 있습니다. 이는 작물 수확량 증가, 품질 개선, 종자 및 노동력과 같은 자원의 보다 효율적인 활용에 대한 수요 증가에 힘입은 것입니다. 농가에 첨단 재배 장비의 도입은 특히 열대 작물 재배에서 종자를 정확하게 배치하고 자원을 효율적으로 사용할 수 있게 해줍니다. 기술적으로 진보된 기계에 대한 수요 증가는 제조업체들에게 제품 라인의 다양화, 작물에 특화된 파종 솔루션 개발, 자동화 및 디지털 통합에 대한 투자, 유통 및 서비스 네트워크 강화 등의 기회를 가져다줍니다. 동시에 디지털 농업 플랫폼의 보급, 밭 작업의 자동화, 보다 엄격한 지속가능성 기준, 그리고 자원 효율적인 농업 방식에 대한 관심이 높아짐에 따라 시장은 변화의 소용돌이에 휩싸였다. 이 모든 것이 경쟁 환경을 변화시키고 장기적인 성장을 형성하고 있습니다.

첨단 기술: 인공지능(AI)과 기계학습이 심기 장비 시장에 점점 더 많이 통합되어 농가가 종자 배치를 최적화하고, 파종 밀도를 조정하고, 토양 건강 및 기상 조건에 대한 의사결정을 개선할 수 있게 되었습니다. 이를 통해 농가는 묘목의 정착률과 생산성을 향상시킬 수 있습니다.

정밀 시비 시스템 - GPS 안내 시스템, 센서, IoT 장치, 실시간 모니터링 플랫폼의 통합으로 파종 과정의 정확도가 향상되었습니다. 이는 이러한 시스템이 투입물 사용을 최적화하고, 운영 비용을 절감하며, 균일한 종자 파종을 통해 수율 잠재력을 극대화하기 때문입니다.

기계식 식재 장비 부문은 설계 부문에서 큰 비중을 차지하고 있습니다. 비용 효율성이 뛰어나고 조작이 간단합니다. 또한 중소규모의 농가에서도 널리 이용되고 있습니다. 또한 비용 효율성과 사용 편의성이 중요한 고려사항인 개발도상국에서는 특히 높은 지지를 받고 있습니다. 자동 식재 장비가 보급되고 있는 가운데, 기계식 식재 장비는 신뢰성이 높고 다양한 조건에서 사용하기에 적합하므로 시장에서 큰 점유율을 유지하고 있습니다.

재배기는 식재 장비 중 가장 빠르게 성장하고 있는 분야 중 하나로 꼽히고 있습니다. 종자의 위치, 간격, 깊이를 정확하게 확보할 수 있는 능력으로 인해 그 활용이 확대되고 있습니다. 이들은 씨앗의 발아율과 식물의 전반적인 성장을 향상시키는 데 필수적인 요소로 간주됩니다. 화분은 옥수수, 콩, 면화 등 열대작물 재배에 널리 이용되고 있습니다. 특히 대규모의 현대식 농가를 중심으로 높은 지지를 받고 있습니다. 또한 효율성에 대한 관심이 높아진 것도 파종기 기술에 대한 수요 증가의 한 요인으로 작용하고 있습니다.

시장의 주요 기업으로는 Deere &Company(미국), AGCO Corporation(미국), CNH Industrial N.V.(영국), Vaderstad AB(스웨덴), Kinze Manufacturing(미국), Bourgault Industries Ltd.(캐나다), KUHN Group(프랑스), SeedMaster Manufacturing Ltd.(캐나다), HORSCH Maschinen GmbH(독일), MaterMacc S.p.A.(이탈리아), LEMKEN GmbH &Co. KG(독일), Maschio Gaspardo(이탈리아), Kubota Corporation(일본), Sfoggia Agriculture Division(이탈리아) 및 Yanmar(일본) 등을 들 수 있습니다.

조사 범위:

본 조사 보고서는 세계의 재배 장비 시장을 유형별(에어시더, 파종기, 파종기, 파종기(정밀파종기, 공압파종기, 무경운/보전파종기, 기타(이식기, 파종기, 특수파종기)), 설계별(기계식, 자동식), 작물별(곡물, 지방종자/두류, 과일/채소, 기타 작물), 지역별로 분류하여 조사했습니다. 과일/채소, 기타 작물) 및 지역별로 분류하고 있습니다. 이 보고서의 조사 범위에는 식재 장비 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 저해요인, 도전 과제, 기회 등)에 대한 자세한 정보가 포함되어 있습니다. 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 솔루션 및 서비스, 주요 전략, 계약, 파트너십, 합의 사항, 제품 및 서비스 출시, 인수합병, 최근 시장 관련 동향에 대한 인사이트를 제공합니다. 이 보고서에서는 식재 장비 시장 생태계의 신흥 스타트업 기업의 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 전체 식재 장비 시장과 각 하위 부문의 매출에 대한 가장 정확한 추정치에 대한 정보를 제공함으로써 시장 리더와 신규 진입자에게 도움이 될 것입니다. 이 보고서는 이해관계자들이 경쟁 상황을 이해하고, 비즈니스 포지셔닝을 개선하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 얻을 수 있도록 돕습니다.

이 보고서는 다음 사항에 대한 인사이트를 제공합니다. :

1. 신흥 시장에 초점을 맞춘 지역별 인사이트 - 이 보고서는 아시아태평양, 북미, 유럽, 남미 및 기타 지역(RoW)의 성장 기회를 강조하고 국가 및 지역 수준의 상세한 분석을 제공합니다. 지역별 수요 패턴, 규제 정책 및 정밀농업 투자 동향을 평가하여 사업 확장 및 현지화 구상을 위한 전략적 지침을 제공합니다.

2. 경쟁 정보 및 혁신 동향 - Deere &Company(미국), AGCO Corporation(미국), CNH Industrial N.V.(영국), Vaderstad AB(스웨덴), Kinze Manufacturing(미국) 등 주요 시장 진입 기업에 대한 자세한 프로필을 제공하고 있습니다. 이 보고서에서는 글로벌 식재 장비 시장의 경쟁 구도, 최근 제품 출시, 생산 능력 확대, 전략적 제휴 및 투자에 대해 다룹니다.

3. 데이터베이스 조사 기법에 기반한 수요 예측 - 2031년까지 시장 규모 및 성장 예측은 하향식 및 상향식 접근 방식을 결합하여 수립되었으며, 업계 전문가, 업계 단체 및 정부의 공식 데이터를 통해 검증되었습니다. 이러한 인사이트는 글로벌 시장에서의 투자 계획과 시장 기회 평가에 대한 신뢰할 수 있는 지침을 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 테크놀러지, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 식재 장비 시장(유형별)

제10장 식재 장비 시장(작물 유형별)

제11장 식재 장비 시장(디자인별)

제12장 식재 장비 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSA 26.05.13The global planting equipment market is estimated at USD 21.74 billion in 2026 and is projected to reach USD 29.44 billion by 2031, at a CAGR of 6.3% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD) and Volume (Metric Tons) |

| Segments | By Type, Crop Type, Design, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The integration of digital agronomy tools, precision fertigation systems, and data-driven nutrient management platforms is transforming product development and on-field performance in the planting equipment industry. Leading companies such as Yara International are leveraging digital farming solutions to optimize nutrient recommendations, enhance nutrient use efficiency (NUE), and improve crop yield outcomes. Such product innovations, combined with advancements in precision agriculture and controlled nutrient delivery systems, are positioning the planting equipment market for sustained growth, improved sustainability, and higher-value crop productivity worldwide.

Opportunities and disruptions in the planting equipment market: This sector is also linked to the growing trend of precision agriculture. The planting equipment market presents significant business opportunities for both farmers and manufacturers. This is driven by the increasing demand for higher crop yields, better crop quality, and more efficient use of resources like seeds and labor. For farmers, adopting advanced planting equipment allows for precise seed placement, leading to more efficient resource use, especially in row crops. For manufacturers, the rising demand for technologically advanced machinery offers chances to diversify product lines, develop crop-specific planting solutions, invest in automation and digital integration, and strengthen dealer and service networks. Simultaneously, the market is experiencing disruption due to the growing adoption of digital farming platforms, automation of field operations, stricter sustainability standards, and a rising preference for resource-efficient farming practices, all of which are transforming competition and shaping long-term growth.

Advanced formulation technologies: Artificial intelligence and machine learning are increasingly being incorporated into the planting equipment market, enabling farmers to optimize seed placement, adjust planting density, and improve decision-making regarding soil health and weather conditions. This enables farmers to improve seedling establishment and productivity.

Precision fertigation systems: With the integration of GPS guidance systems, sensors, IoT devices, and real-time monitoring platforms, the accuracy of the planting process is enhanced. This is because the systems help optimize input use, lower operating costs, and maximize yield potential through uniform seed distribution.

"Mechanical stood as the major design segment of the planting equipment market."

The mechanical planting equipment segment has a significant share of the design segment. It is cost-effective and easy to use. It is also popularly used by small and medium-scale farmers. In addition, it is highly preferred in developing countries where cost-effectiveness and ease of use are major considerations. Although automated planting equipment is becoming popular, mechanical planting equipment has a significant share of the market due to its reliability and suitability for use under different conditions.

Planters are considered one of the fastest-growing segments of planting equipment. Their increased use can be attributed to their ability to ensure accurate seed positioning, space, and depth. These are considered essential considerations for improving seed germination and overall plant growth. Planters are popularly used for row crops such as corn, soybeans, and cotton. They are highly preferred by large-scale and modern farmers. In addition, the increased focus on improving efficiency has also contributed to the increased demand for planter technologies.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the planting equipment market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include Deere & Company (United States), AGCO Corporation (United States), CNH Industrial N.V. (United Kingdom), Vaderstad AB (Sweden), Kinze Manufacturing (United States), Bourgault Industries Ltd. (Canada), KUHN Group (France), SeedMaster Manufacturing Ltd. (Canada), HORSCH Maschinen GmbH (Germany), MaterMacc S.p.A. (Italy), LEMKEN GmbH & Co. KG (Germany), Maschio Gaspardo (Italy), Kubota Corporation (Japan), Sfoggia Agriculture Division (Italy), and Yanmar Co., Ltd. (Japan).

Research Coverage:

This research report categorizes the global planting equipment market, by type (air seeders, seed drills, planters (precision planters, pneumatic planters, no-till/conservation planters), others (transplanters, broadcast seeders, specialized planters)), design (mechanical, automatic), crop type (cereals & grains, oilseeds & pulses, fruits & vegetables, other crop types), and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the planting equipment market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, agreements, product & service launches, mergers and acquisitions, and recent developments associated with the market. Competitive analysis of upcoming startups in the planting equipment market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue figures for the overall Planting equipment market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across Asia Pacific, North America, Europe, South America, and the RoW. It evaluates regional demand patterns, regulatory policies, and investment trends in precision agriculture, offering strategic guidance for expansion and localization initiatives.

2. Competitive Intelligence and Innovation Landscape: Leading market participants, such as Deere & Company (United States), AGCO Corporation (United States), CNH Industrial N.V. (United Kingdom), Vaderstad AB (Sweden), Kinze Manufacturing (United States), are profiled in detail. The report covers recent product launches, capacity expansions, strategic partnerships, and investments shaping the competitive dynamics of the global planting equipment market.

3. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the global sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN PLANTING EQUIPMENT MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN PLANTING EQUIPMENT MARKET

- 3.2 PLANTING EQUIPMENT MARKET, BY TYPE AND REGION

- 3.3 PLANTING EQUIPMENT MARKET, BY DESIGN

- 3.4 PLANTING EQUIPMENT MARKET, BY CROP TYPE

- 3.5 PLANTING EQUIPMENT MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising adoption of precision agriculture

- 4.2.1.2 Labor shortages in agriculture

- 4.2.1.3 Increasing demand for higher crop productivity

- 4.2.1.4 Government subsidies & farm mechanization programs

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial investment cost

- 4.2.2.2 Fragmented land holdings

- 4.2.2.3 Limited technical awareness & training

- 4.2.2.4 Dependence on seasonal demand & weather conditions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth of smart & autonomous planting equipment

- 4.2.3.2 Expansion in emerging markets

- 4.2.3.3 Equipment-as-a-Service (EaaS)/Custom hiring models

- 4.2.4 CHALLENGES

- 4.2.4.1 Integration with diverse farm conditions

- 4.2.4.2 High maintenance & after-sales service requirements

- 4.2.4.3 Price sensitivity in developing markets

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PLANTING EQUIPMENT MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 EXPANSION OF PRECISION AGRICULTURE DRIVING ADVANCED PLANTER ADOPTION

- 5.2.2 INCREASING FARM MECHANIZATION RATE DRIVING ADOPTION OF PLANTING EQUIPMENT

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 COMPONENT MANUFACTURING

- 5.3.3 EQUIPMENT ASSEMBLY & TECHNOLOGY INTEGRATION

- 5.3.4 DISTRIBUTION & DEALER NETWORKS

- 5.3.5 END-USER APPLICATION (FARMERS & AGRIBUSINESSES)

- 5.3.6 AFTER-SALES SERVICES & MAINTENANCE

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO OF HS CODE 843230

- 5.6.2 IMPORT SCENARIO OF HS CODE 843230

- 5.7 KEY CONFERENCES AND EVENTS, 2024-2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 DEERE & COMPANY INTRODUCES AI-DRIVEN PRECISION PLANTING OPTIMIZATION

- 5.9.2 AGCO CORPORATION DEPLOYS AI-ENABLED SMART PLANTING SYSTEMS

- 5.9.3 CNH INDUSTRIAL N.V. LAUNCHES AI-POWERED AUTONOMOUS PLANTING SOLUTIONS

- 5.10 IMPACT OF 2025 US TARIFFS - PLANTING EQUIPMENT MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 China (Asia Pacific)

- 5.10.4.2 Canada & Mexico (North America)

- 5.10.4.3 European Union (Europe)

- 5.10.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI-POWERED PRECISION PLANTING SYSTEMS

- 6.1.2 DIGITAL TWIN & FARM DATA PLATFORMS INTEGRATION

- 6.1.3 ROBOTICS & AUTONOMOUS PLANTING EQUIPMENT

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 IOT-ENABLED SENSOR NETWORKS

- 6.2.2 EDGE COMPUTING FOR REAL-TIME ANALYTICS

- 6.2.3 ADVANCED MACHINE VISION & IMAGING SYSTEMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 VARIABLE RATE FERTILIZATION SYSTEMS (VRF)

- 6.3.2 CROP MONITORING DRONES

- 6.3.3 SOIL HEALTH & MICROBIOME ANALYTICS PLATFORMS

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AUTONOMOUS AND ROBOTICS-ENABLED PLANTERS

- 6.5.2 AI-DRIVEN PRECISION PLANTING SYSTEMS

- 6.5.3 DIGITAL TWIN AND IOT-CONNECTED EQUIPMENT

- 6.5.4 VARIABLE-RATE AND CLIMATE-ADAPTIVE PLANTING TECHNOLOGY

- 6.5.5 SUSTAINABLE AND ECO-FRIENDLY EQUIPMENT DESIGNS

- 6.6 IMPACT OF GENERATIVE AI ON PLANTING EQUIPMENT MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 USE OF GENERATIVE AI ON PLANTING EQUIPMENT MARKET

- 6.6.3 TOP USE CASES AND MARKET POTENTIAL

- 6.6.4 BEST PRACTICES IN PLANTING EQUIPMENT INDUSTRY

- 6.6.5 CASE STUDIES OF AI IMPLEMENTATION IN PLANTING EQUIPMENT MARKET

- 6.6.6 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN PLANTING EQUIPMENT MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

- 7.4.1 REGION-WISE LABELING STANDARDS

- 7.4.1.1 North America

- 7.4.1.2 Europe

- 7.4.1.3 Asia Pacific

- 7.4.1.4 South America

- 7.4.1 REGION-WISE LABELING STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.2.3 ADOPTION BARRIER & INTERNAL CHALLENGES

- 8.2.4 UNMET NEEDS OF VARIOUS END-USER/END-USE INDUSTRY

- 8.2.4.1 Large-scale Commercial Farmers

- 8.2.4.2 Small and Medium-scale Farmers

- 8.2.4.3 Horticulture and Protected Farming Operators

- 8.2.4.4 Equipment Rental and Service Providers

- 8.2.5 MARKET PROFITABILITY

9 PLANTING EQUIPMENT MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 AIR SEEDERS

- 9.2.1 AIR SEEDERS DRIVING EFFICIENCY IN LARGE-SCALE FARMING

- 9.3 SEED DRILLS

- 9.3.1 SEED DRILLS ENHANCING UNIFORM CROP ESTABLISHMENT

- 9.4 PLANTERS

- 9.4.1 PLANTERS ADVANCING PRECISION FARMING AND SUSTAINABLE AGRICULTURE

- 9.4.1.1 High-Speed Planters

- 9.4.1.2 Precision Planters

- 9.4.1.3 Mechanical Planters

- 9.4.1.4 Other Specialized Planters

- 9.4.1 PLANTERS ADVANCING PRECISION FARMING AND SUSTAINABLE AGRICULTURE

- 9.5 OTHER TYPES

10 PLANTING EQUIPMENT MARKET BY CROP TYPE

- 10.1 INTRODUCTION

- 10.2 CEREALS & GRAINS

- 10.2.1 CEREALS & GRAINS DRIVING HIGH-VOLUME DEMAND FOR PLANTING EQUIPMENT

- 10.3 OILSEEDS & PULSES

- 10.3.1 OILSEEDS & PULSES SUPPORTING DIVERSIFICATION IN PLANTING EQUIPMENT DEMAND

- 10.4 FRUITS & VEGETABLES

- 10.4.1 FRUITS && VEGETABLES DRIVING DEMAND FOR PRECISION PLANTING EQUIPMENT

- 10.5 OTHER CROP TYPES

11 PLANTING EQUIPMENT MARKET, BY DESIGN

- 11.1 INTRODUCTION

- 11.2 MECHANICAL

- 11.2.1 MECHANICAL PLANTING EQUIPMENT ENSURING COST-EFFECTIVE AND RELIABLE FARM OPERATIONS

- 11.3 AUTOMATIC

- 11.3.1 AUTOMATIC PLANTING EQUIPMENT ADVANCING PRECISION AND SMART FARMING

12 PLANTING EQUIPMENT MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 CANADA

- 12.2.1.1 Driving large-scale mechanization and precision agriculture adoption

- 12.2.2 MEXICO

- 12.2.2.1 Enhancing mechanization through government support and smallholder accessibility

- 12.2.1 CANADA

- 12.3 EUROPE

- 12.3.1 GERMANY

- 12.3.1.1 Driving precision agriculture through digitalization and sustainable farming practices

- 12.3.2 FRANCE

- 12.3.2.1 Advance toward precision agriculture with increase in adoption of digital technologies in planting operations in France

- 12.3.3 POLAND

- 12.3.3.1 Accelerate efficiency with advanced planting solutions

- 12.3.4 UK

- 12.3.4.1 Enhancing productivity through precision agriculture and technology integration

- 12.3.5 ITALY

- 12.3.5.1 Promoting specialized mechanization and precision farming for high-value crops

- 12.3.6 SPAIN

- 12.3.6.1 Enhancing water efficiency and precision farming in water-scarce conditions

- 12.3.7 REST OF EUROPE

- 12.3.1 GERMANY

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Accelerating agricultural mechanization through policy support and technology adoption

- 12.4.2 INDIA

- 12.4.2.1 Driving mechanization through government initiatives and accessibility programs

- 12.4.3 JAPAN

- 12.4.3.1 Advancing smart agriculture through automation and high-precision technologies

- 12.4.4 AUSTRALIA & NEW ZEALAND

- 12.4.4.1 Enhancing farm efficiency through precision agriculture and large-scale mechanization

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.5.1.1 Driving large-scale mechanization and precision agriculture adoption

- 12.5.2 ARGENTINA

- 12.5.2.1 Advancing no-till farming and precision agriculture practices

- 12.5.3 REST OF SOUTH AMERICA

- 12.5.1 BRAZIL

- 12.6 REST OF THE WORLD (ROW)

- 12.6.1 AFRICA

- 12.6.1.1 Promoting mechanization and technology adoption

- 12.6.2 MIDDLE EAST

- 12.6.2.1 Driving mechanization through government initiatives and technology integration

- 12.6.1 AFRICA

13 COMPETITIVE LANDSCAPE

- 13.1 OVERVIEW

- 13.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN, 2020-2025

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 DEERE & COMPANY (US)

- 13.4.2 KUBOTA CORPORATION (JAPAN)

- 13.4.3 AGCO CORPORATION (US)

- 13.4.4 CNH INDUSTRIAL N.V. (UK)

- 13.4.5 KUHN GROUP (FRANCE)

- 13.5 PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Type footprint

- 13.6.5.3 Design footprint

- 13.6.5.4 Form footprint

- 13.7 COMPANY VALUATION AND FINANCIAL METRICS

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 KEY PLAYERS

- 14.1.1 DEERE & COMPANY

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 AGCO CORPORATION

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Product launches

- 14.1.2.3.2 Deals

- 14.1.2.3.3 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices made

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 CNH INDUSTRIAL N.V.

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.3.4 MnM view

- 14.1.3.4.1 Right to win

- 14.1.3.4.2 Strategic choices

- 14.1.3.4.3 Weaknesses and competitive threats

- 14.1.4 VADERSTAD AB

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.3.2 Deals

- 14.1.4.3.3 Expansions

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 KINZE MANUFACTURING

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches

- 14.1.5.3.2 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Right to win

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 BOURGAULT INDUSTRIES LTD.

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Product launches

- 14.1.6.4 MnM view

- 14.1.7 KUHN GROUP

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Expansions

- 14.1.7.4 MnM view

- 14.1.8 SEEDMASTER MANUFACTURING LTD.

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches

- 14.1.8.4 MnM view

- 14.1.9 HORSCH MASCHINEN GMBH

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Expansions

- 14.1.9.4 MnM view

- 14.1.10 MATERMACC S.P.A.

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 MnM view

- 14.1.11 LEMKEN GMBH & CO. KG

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Expansions

- 14.1.11.4 MnM view

- 14.1.12 MASCHIO GASPARDO

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.12.3 Recent developments

- 14.1.12.3.1 Product launches

- 14.1.12.3.2 Deals

- 14.1.12.4 MnM view

- 14.1.13 KUBOTA CORPORATION

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.13.3 Recent developments

- 14.1.13.3.1 Product launches

- 14.1.13.3.2 Deals

- 14.1.13.3.3 Expansions

- 14.1.13.4 MnM view

- 14.1.14 SFOGGIA AGRICULTURE DIVISION

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.14.3 Recent developments

- 14.1.14.3.1 Product launches

- 14.1.14.3.2 Expansions

- 14.1.14.4 MnM view

- 14.1.15 YANMAR CO., LTD.

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.15.3 Recent developments

- 14.1.15.3.1 Deals

- 14.1.15.3.2 Expansions

- 14.1.15.4 MnM view

- 14.1.16 AMAZONE

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Product launches

- 14.1.16.4 MnM view

- 14.1.17 ORTHMAN MANUFACTURING, INC

- 14.1.17.1 Business overview

- 14.1.17.2 Products offered

- 14.1.17.3 Recent developments

- 14.1.17.3.1 Product launches

- 14.1.17.4 MnM view

- 14.1.18 EQUALIZER PLANTERS

- 14.1.18.1 Business overview

- 14.1.18.2 Products offered

- 14.1.18.2.1 Product launches

- 14.1.18.3 MnM view

- 14.1.19 ZOOMLION HEAVY INDUSTRY SCIENCE & TECHNOLOGY CO., LTD.

- 14.1.19.1 Business overview

- 14.1.19.2 Products offered

- 14.1.19.3 MnM view

- 14.1.20 NOVAG

- 14.1.20.1 Business overview

- 14.1.20.2 Products offered

- 14.1.20.3 MnM view

- 14.1.21 AGRISEM INTERNATIONAL S.A.S

- 14.1.22 KOCKERLING

- 14.1.23 LANDOLL CORP

- 14.1.24 NARDI GROUP

- 14.1.25 NOVAG

- 14.1.1 DEERE & COMPANY

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of major secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 Breakdown of primaries

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.2.2.1 Approach to estimate market size using top-down analysis

- 15.3 DATA TRIANGULATION

- 15.4 RESEARCH ASSUMPTIONS

- 15.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS