|

시장보고서

상품코드

2022832

유제품 가공 장비 시장 예측(-2031년) : 유형별, 용도별, 가동 방식별, 공장 규모별, 지역별Dairy Processing Equipment Market by Type (Pasteurizers, Homogenizers, Mixers & Blenders, Separators, Evaporators, Dryers, Others), Mode of Operation (Automatic and Semi-automatic), Application, Plant Capacity, and Region - Global Forecast to 2031 |

||||||

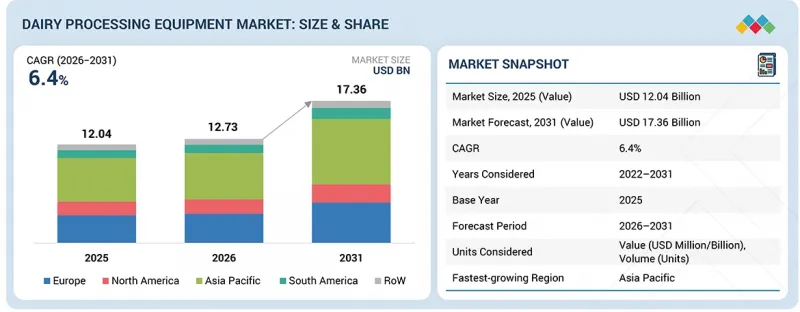

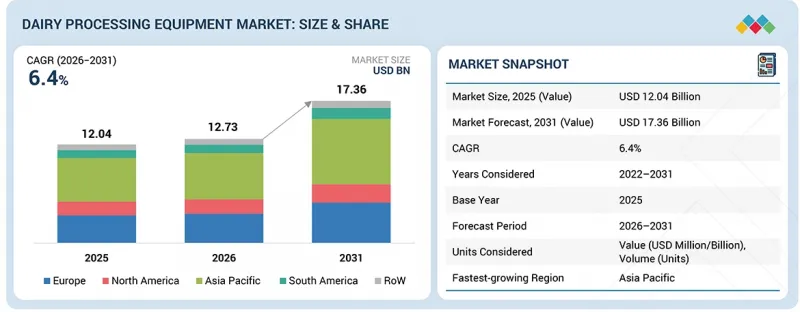

유제품 가공 장비 시장 규모는 2026년에 127억 3,000만 달러로 추계되고 있으며, 예측 기간 중 CAGR 6.4%로 확대하며, 2031년에는 173억 6,000만 달러에 달할 것으로 전망되고 있습니다.

시장 성장은 우유, 치즈, 요구르트, 버터, 우유 음료 등 유제품 가공품에 대한 수요 증가에 의해 주도되고 있습니다. 이러한 제품들은 안전성과 품질의 일관성을 유지하면서 대량 처리가 가능한 가공 시스템이 필요합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) 및 수량(단위) |

| 부문 | 유형별, 용도별, 가동 방식별, 공장 규모별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

저온 살균, 균질화, 막여과, 증발, 건조 등의 공정은 여전히 유제품 가공의 핵심입니다. 끊임없는 기술 발전과 더불어 자동화 및 디지털 모니터링 시스템의 통합을 통해 유제품 가공업체는 운영 효율성을 높이고 제품 품질 안정성을 유지하며 생산 비용을 절감할 수 있습니다. 분유와 단백질 기반 제품 등 유제품 원료에 대한 수요도 증가하고 있습니다. 이에 따라 특히 대규모 수출 지향적인 사업에서 고용량 및 에너지 효율이 높은 설비에 대한 투자가 이루어지고 있습니다. 동시에 개발도상국 시장에서는 조직적인 유제품 가공이 확대되고 있으며, 이는 이러한 설비의 보급을 촉진하고 있습니다. 전반적으로 시장은 효율성, 규모, 그리고 더 나은 공정 제어에 중점을 두고 보다 진보된 가공 시스템으로 전환하고 있습니다.

"모델별 카테고리의 증발기 부문은 예측 기간 중 상당한 CAGR을 기록할 것으로 추정됩니다. "

증발 공정은 원유와 유청에서 85%에서 90%의 수분을 제거하는 필수적인 중간 과정으로 작용합니다. 이 농축 과정을 통해 에너지 수요를 줄이는 동시에 운영 효율을 향상시킬 수 있습니다. 증발기가 제조 공정에서 필수적인 구성 요소로 사용되는 이유는 분말 생산 라인의 처리 능력을 결정하는 병목 현상으로 작용하기 때문입니다.

이 부문이 성장하고 있는 이유는 건조 능력의 증설에 의존하고 있기 때문입니다. 이는 대량의 분유 및 유청 유도체 생산이 필요한 수출 시장에 필수적인 요소입니다. 주요 유제품 가공업체들은 증기 사용량을 최적화하고 총 가공 비용의 상당 부분을 차지하는 에너지 비용을 절감하기 위해 다단식 증발기(MEE) 및 열 증기 재압축(TVR)/기계식 증기 재압축(MVR) 시스템에 대한 투자를 늘리고 있습니다. 연속 처리 시스템에 대한 업계 동향과 통합 플랜트 설계 시스템이 결합되어 산업 생산 수준에서 대량의 원료를 처리할 수 있는 자동 증발 시스템에 대한 수요가 증가하고 있습니다. 유청 단백질 농축액, 유청 단백질 분리물 및 유당 생산의 증가는 후속 분리 및 건조 공정에 필수적인 농축 공정을 제공하므로 증발 처리의 필요성을 증가시키고 있습니다. 증발 장치는 CIP 지원 시스템을 통해 사용자에게 안정적인 고형분 수준을 유지하면서 가동 중단을 최소화하고 더 나은 세척 결과를 달성할 수 있는 능력을 제공합니다. 유제품 가공업체들이 원료 생산량을 늘리면서 수율 향상과 에너지 사용량 감소를 위해 증발장치 시장은 가장 빠르게 성장할 것으로 보입니다.

증발 공정은 유제품 가공에서 중요한 단계입니다. 이 공정은 우유와 유청에서 다량의 수분을 제거하고 건조 및 기타 가공을 하기 전에 고형분 함량을 농축하는 과정입니다. 증발기는 분유 및 유청 원료 생산의 핵심 단계이기 때문에 증발기는 종종 전체 공장의 생산 능력과 효율의 속도를 결정하는 요인으로 작용합니다. 이 부문의 성장은 분유, 유청 단백질, 유당 및 기타 유제품에 대한 수요 증가, 특히 대량 생산이 필요한 수출 주도형 시장에서의 수요 증가에 힘입어 성장세를 보이고 있습니다. 많은 유제품 가공업체들은 에너지 사용량과 운영 비용을 관리하기 위해 다단식 증발기(MEE), 열/기계식 증기 재압축(TVR/MVR) 등 첨단 시스템에 투자하고 있습니다.

연속적이고 보다 통합된 가공 라인으로의 전환은 대규모 운영이 가능한 자동 증발 시스템의 도입을 촉진하고 있습니다. 최신 증발기는 안정적인 고형분 농도를 유지하고, 고정식 세척(CIP)을 지원하며, 다운타임을 줄일 수 있도록 설계되어 있습니다. 생산자들이 수율, 에너지 절약 및 전반적인 효율성에 점점 더 집중함에 따라 유제품 가공 장비 시장에서 증발기 부문이 성장할 것으로 예상됩니다.

분유 제조는 유제품 가공에서 설비 의존도가 높은 공정으로 살균, 균질화, 증발, 분무 건조 등의 기술 통합이 필수적입니다. 그 결과, 이 부문의 확대는 특히 증발기 및 건조기를 중심으로 한 주요 설비에 대한 설비 투자를 촉진하고 있습니다. 영유아용 영양식품, 기능성 우유 성분 및 단백질 강화 제품에 대한 수요 증가가 분유 생산능력 확대에 기여하고 있습니다. 가공업체는 규정된 입자 크기, 수분 함량, 용해도를 포함한 균일한 제품 품질을 유지하기 위해 첨단 대용량 시스템에 의존하고 있습니다. 특히 주요 유제품 생산 지역의 수출 수요 증가는 새로운 분유 가공 공장에 대한 투자를 촉진하고 있으며, 각 공장에는 포괄적이고 통합된 가공 라인이 필수적입니다. 그 결과, 분유 부문은 계속해서 설비 수요의 주요 원동력이 될 것이며, 유제품 가공 장비 시장에서 가장 빠르게 성장하는 응용 분야 중 하나가 될 것으로 예상됩니다.

북미 유제품 가공 장비 시장은 탄탄한 유제품 산업과 탄탄한 가공 인프라에 의해 지원되고 있습니다. 이 지역에는 자동화된 대용량 시스템을 통해 우유, 치즈, 버터, 유제품을 생산하는 대규모 유제품 사업체가 있습니다. SPX FLOW, Paul Mueller와 같은 주요 장비 공급업체의 존재는 열처리, 분리, 유체 처리의 기술 발전에 더욱 기여하고 있습니다. 부가가치 제품, 특히 치즈 및 단백질 기반 원료에 대한 수요가 증가함에 따라 분리기, 멤브레인 여과 시스템, 증발 및 건조 장치 등의 설비 이용이 확대되고 있습니다. 동시에 엄격한 규제 요건과 탄탄한 콜드 체인 네트워크는 신뢰할 수 있고 위생적이며 효율적인 가공 시스템에 대한 필요성을 높이고 있습니다. 또한 장비 공급업체와 유제품 가공업체와의 협력 관계는 공장 개선을 촉진하고 효율성을 향상시키며 지역 전체에서 혁신을 촉진하고 있습니다.

시장의 주요 기업 : Alfa Laval(스웨덴), SPX FLOW(미국), Andritz AG(오스트리아), Pentair PLC(영국/미국), Sulzer Ltd(스위스), Fristam Pumpen KG(독일), HRS Heat Exchangers Ltd(영국), Anderson Dahlen(미국), Anderson Dahlen Inc.(미국), Coperion GmbH(독일), Bucher Unipektin AG(스위스), Scherjon Equipment Holland B.V.(네덜란드), Fenco Food Machinery S.r.l.(이탈리아), Sealtech Engineers Pvt Ltd(인도), Tetra Pak(스위스), GEA Group AG(독일), Krones AG(독일), JBT Marel(미국/아이슬란드), Ziemann Holvrieka(독일), IDMC Limited(인도), Van den Heuvel Dairy &Food Equipment(네덜란드), Neologic Engineers Pvt Ltd(인도), SSP Pvt Ltd(인도), Goma Engineering Pvt Ltd(인도), GEMAK Group(튀르키예), TESSA I.E.C Group(이탈리아), IWAI Kikai Kogyo(일본) 및 Shanghai Jimei Food Machinery(중국)

기타 주요 기업으로는 Skylark Engineers(인도), Micro Dairy Designs Ltd(영국), INOXPA S.A.U.(스페인), CFT S.p.A.(이탈리아), Milkman Dairy Equipment(인도), Triowin Intelligent Machinery(중국), COMAT(이탈리아), REDA S.p.A.(이탈리아) 및 Kovalus Separation Solutions(미국) 등을 들 수 있습니다.

조사 범위

세계의 유제품 가공기기 시장을 제품 유형(살균기, 균질화기, 믹서-블렌더, 분리기, 증발기, 건조기, 멤브레인 여과장치, 기타), 용도(가공유, 원유, 버터-버터밀크, 치즈, 분유, 단백질 원료), 가동 모드(자동-반자동), 공장 규모(정성적)(소규모 유제품 공장, 중형 유제품 공장, 대규모 산업용 유제품 공장), 지역(북미, 유럽, 아시아태평양, 남미, 기타 지역)으로 분류하고 있습니다. 이 보고서의 조사 범위에는 유제품 가공 장비 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약요인, 과제 및 기회)에 대한 자세한 정보가 포함되어 있습니다. 이 보고서는 주요 업계 플레이어에 대한 상세한 분석을 통해 사업 개요, 솔루션, 서비스, 주요 전략, 계약, 파트너십 및 합의에 대한 인사이트를 제공합니다. 본 조사에서는 신제품 및 서비스 출시, 인수합병, 유제품 가공 장비 시장과 관련된 최근 동향을 조사했습니다. 또한 이 보고서에는 유제품 가공 장비 시장 생태계의 신생 스타트업 기업에 대한 경쟁 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 리더와 신규 진입자에게 전체 유제품 가공 장비 시장과 각 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 또한 이해관계자들이 경쟁 상황을 이해하고, 자신의 비즈니스를 더 나은 위치에 놓고, 적절한 시장 진입 전략을 수립하기 위한 인사이트를 얻을 수 있도록 돕습니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악할 수 있도록 주요 시장 촉진요인, 제약, 도전 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

Q1.유제품 가공 장비 시장에서 가장 큰 점유율을 차지하는 제품 유형은 무엇인가?

저온 살균기가 시장에서 가장 큰 점유율을 차지하고 있습니다. 이는 저온살균이 유제품 가공에 있으며, 필수적이고 필수적인 공정이기 때문입니다. 이러한 시스템은 제품의 안전성을 보장하고 유통기한을 연장하기 위해 가공유, 요구르트, 유음료 등의 용도에 널리 사용되고 있습니다.

Q2. 시장에서 가장 높은 성장률을 보일 것으로 예상되는 분야는 어디인가?

분유 및 유제품 생산에 대한 수요 증가를 배경으로 증발기 부문이 가장 높은 성장률을 보일 것으로 예상됩니다. 증발은 건조 전 농축 공정에서 중요한 역할을 하며, 대규모 유제품 생산에 필수적인 공정입니다.

Q3. 유제품 가공 장비 시장을 주도하는 지역은 어디인가?

아시아태평양은 높은 우유 생산량, 유제품 소비 확대, 현대식 유제품 가공 인프라에 대한 투자 증가로 인해 시장에서 가장 큰 점유율을 차지하고 있습니다. 중국, 인도 등의 국가들이 이 지역의 성장에 크게 기여하고 있습니다.

Q4. 유제품 가공 장비의 수요를 이끄는 주요 요인은 무엇인가?

주요 성장 요인으로는 가공유제품 및 고부가가치 유제품의 소비 증가, 분유 및 단백질 원료에 대한 수요 확대, 가공기술의 발전, 효율성과 제품 균일성 향상을 위한 자동화 도입 확대 등을 꼽을 수 있습니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 유제품 가공 장비 시장(유형별)

제10장 유제품 가공 장비 시장(용도별)

제11장 유제품 가공 장비 시장(가동 방식별)

제12장 유제품 가공 설비(공장 규모별)

제13장 유제품 가공 장비 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 인접 시장 및 관련 시장

제17장 조사 방법

제18장 부록

KSA 26.05.14The market for dairy processing equipment is estimated to be USD 12.73 billion in 2026 and is projected to reach USD 17.36 billion by 2031, at a CAGR of 6.4% during the forecast period. Market growth is driven by rising demand for processed dairy products such as milk, cheese, yogurt, butter, and dairy-based beverages. These products need processing systems that can handle volume while maintaining safety and consistency.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) and Volume (Units) |

| Segments | By Type, Application, Mode of Operation, Plant Capacity, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

Processes such as pasteurization, homogenization, membrane filtration, evaporation, and drying continue to be a core part of dairy processing. Continuous technological improvements, coupled with the integration of automation and digital monitoring systems, are enabling dairy processors to enhance operational efficiency, maintain product consistency, and reduce production costs. Demand for dairy ingredients such as milk powder and protein-based products is also increasing. This is leading to investment in high-capacity and energy-efficient equipment, especially in large-scale and export-focused operations. At the same time, organized dairy processing is expanding in developing markets, which is supporting wider use of such equipment. Overall, the market is moving toward more advanced processing systems, with a clear focus on efficiency, scale, and better process control.

"The evaporators segment within the type category is estimated to witness a significant CAGR during the forecast period."

The evaporation process serves as an essential intermediate step that removes 85% to 90% of water from raw milk or whey. This process reduction results in lower energy needs while it enhances operational effectiveness. The production process uses evaporators as essential components because they operate as bottleneck assets that determine the processing capabilities of powder production lines.

The segment experiences growth because it relies on increased drying capacity, which is essential for export markets that need to produce milk powder and whey derivatives at high volumes. Large dairy processors are increasingly investing in multi-effect evaporators (MEE) and thermal vapor recompression (TVR)/mechanical vapor recompression (MVR) systems to optimize steam usage and reduce energy costs, which can account for a significant share of total processing expenditure. The industry trend towards continuous processing systems, together with integrated plant design systems, has created a greater need for automated evaporation systems that can process high volumes of material at industrial production levels. The increasing production of whey protein concentrates, whey protein isolates, and lactose drives the need for evaporation because it provides essential concentration for subsequent separation and drying processes. Evaporators give users the ability to maintain steady solids levels while they experience fewer operational interruptions and achieve better cleaning results through CIP-compatible systems. The market for evaporators will experience its fastest growth because dairy processors aim to enhance yield and decrease energy use while increasing ingredient production.

Evaporation is an important step in dairy processing. It removes a large amount of water from milk or whey so the solids can be concentrated before drying or other processing. Since it is a core stage in producing milk powder and whey ingredients, the evaporator often sets the pace for overall plant capacity and efficiency. Growth in this segment is supported by rising demand for milk powder, whey proteins, lactose, and other dairy ingredients, particularly in export driven markets that need high volume production. To manage energy use and operating costs, many dairy processors are investing in advanced systems like multi effect evaporators (MEE) and thermal or mechanical vapor recompression (TVR/MVR).

The move toward continuous and more integrated processing lines is also driving the adoption of automated evaporation systems that can run at a large scale. Newer evaporators are built to maintain stable solids levels, support clean in place (CIP) cleaning, and reduce downtime. As producers focus more on yield, energy savings, and overall efficiency, the evaporator segment is expected to grow within the dairy processing equipment market.

"The milk powder segment within the application category is estimated to witness strong growth during the forecast period."

Milk powder production is a highly equipment-dependent process within dairy processing, necessitating the integration of technologies including pasteurization, homogenization, evaporation, and spray drying. The expansion of this sector is consequently fueling capital investments in essential equipment, with a particular emphasis on evaporators and dryers. The rising demand for infant nutrition, functional dairy ingredients, and protein-enriched products is contributing to the growth of milk powder production capacity. Processors depend on sophisticated, high-capacity systems to maintain uniform product quality, encompassing regulated particle size, moisture content, and solubility. The increasing demand for exports, particularly from major dairy-producing areas, is fueling investments in new powder processing plants, each necessitating comprehensive and integrated processing lines. Consequently, the milk powder sector continues to be a primary catalyst for equipment demand and is projected to be among the most rapidly expanding application domains within the dairy processing equipment market.

"North America is estimated to hold a significant share of the dairy processing equipment market."

The dairy processing equipment market in North America is supported by a well-established dairy industry and strong processing infrastructure. The region has large-scale dairy operations that use automated and high-capacity systems to produce milk, cheese, butter, and dairy ingredients. The presence of prominent equipment suppliers, including SPX FLOW and Paul Mueller, further contributes to advancements in thermal processing, separation, and fluid handling. The increasing demand for value-added products, particularly cheese and protein-based ingredients, is resulting in greater utilization of equipment such as separators, membrane filtration systems, and evaporation and drying units. Simultaneously, stringent regulatory mandates and a robust cold-chain network are fueling the necessity for dependable, sanitary, and efficient processing systems. Furthermore, the collaborative efforts between equipment suppliers and dairy processors are facilitating plant enhancements, boosting efficiency, and fostering innovation throughout the region.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the dairy processing equipment market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) - 10%

Prominent companies in the market include Alfa Laval (Sweden), SPX FLOW (US), Andritz AG (Austria), Pentair PLC (UK/US), Sulzer Ltd (Switzerland), Fristam Pumpen KG (Germany), HRS Heat Exchangers Ltd (UK), Anderson Dahlen (US), Anderson Dahlen Inc. (US), Coperion GmbH (Germany), Bucher Unipektin AG (Switzerland), Scherjon Equipment Holland B.V. (Netherlands), Fenco Food Machinery S.r.l. (Italy), Sealtech Engineers Pvt Ltd (India), Tetra Pak (Switzerland), GEA Group AG (Germany), Krones AG (Germany), JBT Marel (US/Iceland), Ziemann Holvrieka (Germany), IDMC Limited (India), Van den Heuvel Dairy & Food Equipment (Netherlands), Neologic Engineers Pvt Ltd (India), SSP Pvt Ltd (India), Goma Engineering Pvt Ltd (India), GEMAK Group (Turkey), TESSA I.E.C Group (Italy), IWAI Kikai Kogyo Co., Ltd. (Japan), and Shanghai Jimei Food Machinery Co., Ltd (China).

Other players include Skylark Engineers (India), Micro Dairy Designs Ltd (UK), INOXPA S.A.U. (Spain), CFT S.p.A. (Italy), Milkman Dairy Equipment (India), Triowin Intelligent Machinery Co., Ltd. (China), COMAT (Italy), REDA S.p.A. (Italy), and Kovalus Separation Solutions (US).

Research Coverage

This research report categorizes the dairy processing equipment market by product type (pasteurizers, homogenizers, mixers & blenders, separators, evaporators, dryers, membrane filtration equipment, and other types), application (processed milk, fresh dairy products, butter & buttermilk, cheese, milk powder, and protein ingredients), mode of operation (automatic and semi-automatic), plant capacity (qualitative) (small-scale dairy plants, medium-scale dairy plants, large industrial dairy plants), and region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the dairy processing equipment market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; Contracts, partnerships, and agreements. The study includes new product & service launches, mergers & acquisitions, and recent developments associated with the dairy processing equipment market. This report also includes a competitive analysis of emerging startups in the dairy processing equipment market ecosystem.

Reasons To Buy This Report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall dairy processing equipment and the subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

Q1. Which product type holds the largest share in the dairy processing equipment market?

Pasteurizers hold the largest share in the market, as pasteurization is a critical and mandatory step in dairy processing. These systems are widely used across applications such as processed milk, yogurt, and dairy beverages to ensure product safety and extend shelf life.

Q2. Which segment is expected to grow at the fastest rate in the market?

The evaporators segment is expected to register the highest growth rate, driven by increasing demand for milk powder and dairy ingredient production. Evaporation plays a key role in concentration processes prior to drying, making it essential for large-scale dairy operations.

Q3. Which region dominates the dairy processing equipment market?

Asia Pacific holds the largest share of the market due to its high milk production, growing consumption of dairy products, and increasing investments in modern dairy processing infrastructure. Countries such as China and India are key contributors to regional growth.

Q4. What are the key factors driving demand for dairy processing equipment?

Key growth drivers include rising consumption of processed and value-added dairy products, increasing demand for milk powder and protein ingredients, advancements in processing technologies, and growing adoption of automation to improve efficiency and product consistency.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 UNITS CONSIDERED

- 1.3.4.1 Currency unit

- 1.3.4.2 Volume unit

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DAIRY PROCESSING EQUIPMENT MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DAIRY PROCESSING EQUIPMENT MARKET

- 3.2 DAIRY PROCESSING EQUIPMENT MARKET, BY TYPE AND REGION

- 3.3 DAIRY PROCESSING EQUIPMENT MARKET: BY TOP FOUR TYPES

- 3.4 DAIRY PROCESSING EQUIPMENT MARKET, BY APPLICATION

- 3.5 DAIRY PROCESSING EQUIPMENT MARKET, BY MODE OF OPERATION

- 3.6 DAIRY PROCESSING EQUIPMENT MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rise in demand for functional and fortified dairy products

- 4.2.1.2 Growth in demand for dairy products with long shelf lives

- 4.2.1.3 Increase in adoption of automation and smart dairy plants in dairy processing facilities

- 4.2.1.4 Rise in demand for dairy ingredients in food industry

- 4.2.1.4.1 Growth in production of milk due to increase in consumption of dairy products

- 4.2.1.4.2 Increase in demand for protein-rich dairy ingredients such as whey and casein

- 4.2.1.4.3 Growth in demand for lactose-free and specialty dairy products, dairy powder, and infant nutrition products

- 4.2.1.5 Expansion of dairy processing capacity in emerging countries

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial investment and high maintenance, operational, and installation costs of dairy processing equipment

- 4.2.2.2 Complexity in integrating advanced automation systems in existing plants

- 4.2.2.3 Increase in energy costs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for membrane filtration technologies in dairy processing

- 4.2.3.2 Increase in investment in dairy cold chain infrastructure

- 4.2.3.3 Technological innovation in automated cleaning and sanitation systems

- 4.2.3.4 Higher demand for customized and modular dairy processing equipment

- 4.2.4 CHALLENGES

- 4.2.4.1 Strict food safety and hygiene regulations in dairy processing & compliance with international dairy quality standards

- 4.2.4.2 Equipment downtime affecting production efficiency

- 4.2.4.3 Increase in pressure to reduce energy consumption and carbon emissions

- 4.2.4.4 High costs associated with equipment upgrades and modernization

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DAIRY PROCESSING EQUIPMENT MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 MACROECONOMIC INDICATORS

- 5.2.2.1 Rising investment in cold chain and food logistics infrastructure

- 5.2.2.2 Government subsidies and financial support for dairy processing infrastructure

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL & COMPONENT SOURCING

- 5.3.2 PRODUCT DEVELOPMENT & MANUFACTURING

- 5.3.3 QUALITY, SAFETY & REGULATORY COMPLIANCE

- 5.3.4 INSTALLATION, CUSTOMIZATION & INTEGRATION

- 5.3.5 SALES, DISTRIBUTION, AND AFTER-SALES SERVICES

- 5.3.6 END USERS

- 5.4 ECOSYSTEM/MARKET MAP ANALYSES

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 INTRODUCTION

- 5.5.2 INDICATIVE PRICE TREND AMONG MARKET PLAYERS

- 5.5.3 INDICATIVE AVERAGE SELLING PRICE (ASP) TREND, BY REGION AND TYPE

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO OF HS CODE 843420

- 5.6.2 EXPORT SCENARIO OF HS CODE 843420

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 GEA GROUP: LAUNCH OF ENERGY-EFFICIENT DAIRY EVAPORATOR TECHNOLOGY

- 5.10.2 ALFA LAVAL: EXTEND TECHNOLOGY IMPROVING EFFICIENCY IN DAIRY PASTEURIZATION

- 5.10.3 GEA GROUP: SUPPORTING ARLA FOODS IN HIGH-QUALITY LACTOSE PRODUCTION FOR INFANT NUTRITION

- 5.10.4 TETRA PAK: COLLABORATED WITH DAIRY INGREDIENT MANUFACTURER CAYUGA MILK INGREDIENTS (CMI) TO EXPAND DAIRY PROCESSING FACILITY IN CAYUGA COUNTY, NEW YORK

- 5.11 IMPACT OF 2025 US TARIFF - DAIRY PROCESSING EQUIPMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRIES/REGIONS

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END-USE INDUSTRIES

- 5.12 MILK PRODUCTION DATA AND NUMBER OF DAIRY PROCESSING PLANTS

- 5.12.1 RAW MILK PRODUCTION

- 5.12.2 LIQUID MILK PRODUCTION

- 5.12.3 NUMBER OF DAIRY PROCESSING PLANTS, BY KEY COUNTRY

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY TECHNOLOGIES

- 6.1.1.1 Thermal processing technologies (pasteurization, UHT, sterilization)

- 6.1.1.2 Homogenization and Fat Standardization Technology

- 6.1.1.3 Membrane filtration technologies (UF, MF, RO)

- 6.1.2 COMPLEMENTARY ANALYSIS

- 6.1.2.1 Evaporation & drying technologies (spray drying, falling film evaporation)

- 6.1.2.2 Fermentation & culturing technologies

- 6.1.2.3 Enzyme-based cleaning-in-place (CIP) in dairy processing

- 6.1.2.4 Automation & process control systems (SCADA, PLC, IoT integration)

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Energy-efficient & sustainability-driven technologies (heat recovery, water recycling)

- 6.1.3.2 Smart monitoring & predictive maintenance systems

- 6.1.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.1.4.1 Short-Term | Foundation & Early Commercialization

- 6.1.4.2 Mid-Term | Smart Technologies & Sustainable Processing

- 6.1.4.3 Long-Term | Fully Integrated Smart Factories & Industry 4.0

- 6.1.1 KEY TECHNOLOGIES

- 6.2 PATENT ANALYSIS

- 6.3 FUTURE APPLICATIONS

- 6.3.1 IOT-BASED MACHINE LEARNING SYSTEM FOR DAIRY PRODUCTION QUALITY OPTIMIZATION

- 6.3.2 AI-BASED SENSOR SYSTEM FOR ANTIBIOTIC DETECTION IN MILK

- 6.3.3 AI-DRIVEN ECONOMIC MODEL PREDICTIVE CONTROL FOR DAIRY PASTEURIZATION UNITS

- 6.3.4 LED-BASED TECHNOLOGIES FOR DAIRY PROCESSING AND STERILIZATION

- 6.3.5 ADVANCED MEMBRANE SEPARATION TECHNOLOGY FOR NEXT-GENERATION DAIRY PROCESSING

- 6.4 IMPACT OF GENERATIVE AI ON DAIRY PROCESSING EQUIPMENT MARKET

- 6.4.1 INTRODUCTION

- 6.4.2 TOP USE CASES AND MARKET POTENTIAL

- 6.4.3 BEST PRACTICES IN DAIRY PROCESSING EQUIPMENT INDUSTRY

- 6.4.4 CASE STUDIES OF AI IMPLEMENTATION IN DAIRY PROCESSING EQUIPMENT MARKET

- 6.4.5 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.4.6 CLIENTS' READINESS TO ADOPT GENERATIVE AI FOR DAIRY PROCESSING EQUIPMENT

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.3 LABELING REQUIREMENTS AND CLAIMS

- 7.1.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.4.1 Stricter hygienic equipment design and sanitation standards

- 7.1.4.2 Global harmonization of food processing equipment safety standards

- 7.1.4.3 Enhanced food safety and preventive control regulations

- 7.1.4.4 Digital traceability, smart monitoring, and compliance automation

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE SOURCING

- 7.2.2 CARBON FOOTPRINT REDUCTION INITIATIVES

- 7.2.3 CIRCULAR ECONOMY APPROACHES

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS APPLICATION INDUSTRIES ACROSS SUPPLY CHAIN

- 8.5 MARKET PROFITABILITY

- 8.6 REVENUE POTENTIAL

- 8.6.1 COST DYNAMICS

- 8.6.2 MARGIN OPPORTUNITIES, BY TYPE

9 DAIRY PROCESSING EQUIPMENT MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 PASTEURIZERS

- 9.2.1 ENSURING DAIRY SAFETY AND SHELF LIFE THROUGH ADVANCED PASTEURIZATION SYSTEMS

- 9.3 HOMOGENIZERS

- 9.3.1 ENHANCING TEXTURE AND STABILITY FOR CONSISTENT, HIGH-QUALITY DAIRY PRODUCTS

- 9.4 MIXERS & BLENDERS

- 9.4.1 ENSURING UNIFORMITY AND TEXTURE IN DAIRY PRODUCTS THROUGH ADVANCED MIXING TECHNOLOGIES

- 9.5 SEPARATORS

- 9.5.1 ENABLING EFFICIENT MILK FRACTIONATION FOR VALUE-ADDED DAIRY PRODUCTION

- 9.6 EVAPORATORS

- 9.6.1 ENHANCING DAIRY CONCENTRATION WITH ENERGY-EFFICIENT EVAPORATION TECHNOLOGIES

- 9.7 DRYERS

- 9.7.1 ADVANCED DRYING TECHNOLOGIES FOR HIGH-QUALITY AND NUTRIENT-RICH DAIRY POWDERS

- 9.8 MEMBRANE FILTRATION EQUIPMENT

- 9.8.1 TRANSFORMING DAIRY PROCESSING THROUGH ADVANCED AND SUSTAINABLE FILTRATION SYSTEMS

- 9.9 OTHER TYPES

10 DAIRY PROCESSING EQUIPMENT MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 PROCESSED MILK

- 10.2.1 PROCESSED MILK DEMAND IS TRANSFORMING DAIRY PROCESSING FROM TRADITIONAL HANDLING TO TECHNOLOGY-DRIVEN, LARGE-SCALE PRECISION SYSTEMS

- 10.3 FRESH DAIRY PRODUCTS

- 10.3.1 SHIFT IN CONSUMER TRENDS TOWARD HEALTHIER DESSERTS AND GOURMET CUISINES

- 10.4 BUTTER & BUTTERMILK

- 10.4.1 STRONG GLOBAL BAKERY DEMAND DRIVES GROWTH IN BUTTER & BUTTERMILK PROCESSING EQUIPMENT

- 10.5 CHEESE

- 10.5.1 RISING GLOBAL CHEESE CONSUMPTION AND ITS EXPANDING ROLE IN PROCESSED FOODS TO DRIVE SUSTAINED DEMAND

- 10.6 MILK POWDER

- 10.6.1 RISING DEMAND FOR SHELF-STABLE DAIRY FUELS GROWTH IN MILK POWDER PROCESSING TECHNOLOGIES

- 10.7 PROTEIN INGREDIENTS

- 10.7.1 RISING DEMAND FOR WHEY PROTEIN INGREDIENTS DRIVES ADOPTION OF ADVANCED FILTRATION TECHNOLOGIES

11 DAIRY PROCESSING EQUIPMENT MARKET, BY MODE OF OPERATION

- 11.1 INTRODUCTION

- 11.2 AUTOMATIC

- 11.2.1 SMART AUTOMATION FOR SEAMLESS, EFFICIENT, AND HIGH-QUALITY DAIRY PROCESSING

- 11.3 SEMI-AUTOMATIC

- 11.3.1 FLEXIBLE AND COST-EFFECTIVE SOLUTIONS FOR CONTROLLED AND SCALABLE DAIRY PROCESSING

12 DAIRY PROCESSING EQUIPMENT, BY PLANT CAPACITY

- 12.1 INTRODUCTION

- 12.2 SMALL-SCALE DAIRY PLANTS

- 12.2.1 EMPOWER DECENTRALIZED MILK PROCESSING THROUGH COMPACT AND COST-EFFECTIVE EQUIPMENT SOLUTIONS

- 12.3 MEDIUM-SCALE DAIRY PLANTS

- 12.3.1 ACCELERATE MARKET GROWTH THROUGH SCALABLE CAPACITY AND ADVANCED PROCESSING INTEGRATION

- 12.4 LARGE INDUSTRIAL DAIRY PLANTS

- 12.4.1 INDUSTRIAL PRODUCTION THROUGH HIGH-CAPACITY AUTOMATION AND ADVANCED PROCESSING TECHNOLOGIES

13 DAIRY PROCESSING EQUIPMENT MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Strong dairy consumption and large-scale processing infrastructure to drive demand for advanced dairy processing equipment

- 13.2.2 CANADA

- 13.2.2.1 Expansion of dairy processing infrastructure and rising product value to fuel equipment demand

- 13.2.3 MEXICO

- 13.2.3.1 Rising dairy consumption and expanding processing base to support demand for dairy processing equipment

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Large-scale milk production and strong processing industry to fuel demand for advanced dairy processing equipment

- 13.3.2 FRANCE

- 13.3.2.1 Strong dairy production, high-value product demand, and export orientation to support processing equipment adoption

- 13.3.3 ITALY

- 13.3.3.1 Strong cheese-focused processing industry and export demand to fuel equipment adoption

- 13.3.4 UK

- 13.3.4.1 Strong dairy processing infrastructure and rising demand for value-added products to drive equipment adoption

- 13.3.5 NETHERLANDS

- 13.3.5.1 High-value dairy processing ecosystem to accelerate demand for advanced equipment

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Shifting demand toward high-value dairy products to accelerate need for advanced processing equipment

- 13.4.2 INDIA

- 13.4.2.1 Government-backed expansion of dairy processing infrastructure and modernization initiatives to significantly drive demand

- 13.4.3 JAPAN

- 13.4.3.1 High-quality dairy processing and rising demand for functional products to fuel equipment adoption

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Export-driven, high-efficiency dairy systems to fuel demand for advanced processing technologies

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Brazil's rising milk output and shift toward value-added dairy processing to accelerate demand

- 13.5.2 ARGENTINA

- 13.5.2.1 Argentina's rising dairy production & consumption and industrial processing shift to drive demand for advanced dairy equipment

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD (ROW)

- 13.6.1 MIDDLE EAST

- 13.6.1.1 Middle East's rising dairy demand and food security initiatives to drive investment in advanced dairy processing equipment

- 13.6.2 AFRICA

- 13.6.2.1 Increase in demand for processed dairy products, along with potential in structural gaps in local dairy infrastructure, to provide growth opportunities

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2022-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 EV/EBITDA

- 14.6 BRAND COMPARISON ANALYSIS

- 14.7 COMPANY EVALUATION MATRIX: OEM SECTOR (PROCESS INTEGRATORS), 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: OEM SECTOR (PROCESS INTEGRATORS), 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Regional footprint

- 14.7.5.3 Type footprint

- 14.7.5.4 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: MACHINERY/PROCESS EQUIPMENT SUPPLIERS, 2025

- 14.8.1 STARS

- 14.8.2 EMERGING LEADERS

- 14.8.3 PERVASIVE PLAYERS

- 14.8.4 PARTICIPANTS

- 14.8.5 COMPANY FOOTPRINT: MACHINERY/PROCESS EQUIPMENT SUPPLIERS, 2025

- 14.8.5.1 Company footprint

- 14.8.5.2 Regional footprint

- 14.8.5.3 Type footprint

- 14.8.5.4 Application footprint

- 14.8.6 COMPETITIVE BENCHMARKING: OEM SECTOR (PROCESS INTEGRATORS), 2025

- 14.8.6.1 Detailed list of original equipment manufacturer (OEM)

- 14.9 COMPETITIVE SCENARIO AND TRENDS

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 OEM SECTOR (PROCESS INTEGRATORS)

- 15.1.1 TETRA LAVAL GROUP

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Services/Solutions offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 GEA GROUP AKTIENGESELLSCHAFT

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Services/Solutions offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 KRONES AG

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Services/Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 JBT MAREL

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Services/Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 IDMC LIMITED

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Services/Solutions offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 VAN DEN HEUVEL DAIRY & FOOD EQUIPMENT

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Services/Solutions offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.7 NEOLOGIC ENGINEERS PRIVATE LIMITED

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Services/Solutions offered

- 15.1.7.3 Recent developments

- 15.1.7.4 MnM view

- 15.1.8 SSP PVT. LTD

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Services/Solutions offered

- 15.1.8.3 Recent developments

- 15.1.8.4 MnM view

- 15.1.9 GOMA

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Services/Solutions offered

- 15.1.9.3 Recent developments

- 15.1.9.4 MnM view

- 15.1.10 GEMAK

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Services/Solutions offered

- 15.1.10.3 Recent developments

- 15.1.10.4 MnM view

- 15.1.11 TESSA DAIRY MACHINERY

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Services/Solutions offered

- 15.1.11.3 Recent developments

- 15.1.11.4 MnM view

- 15.1.12 IWAI KIKAI KOGYO CO., LTD.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Services/Solutions offered

- 15.1.12.3 Recent developments

- 15.1.12.4 MnM view

- 15.1.13 JIMEI MACHINERY CO., LTD.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Services/Solutions offered

- 15.1.13.3 Recent developments

- 15.1.13.4 MnM view

- 15.1.14 PIERRE GUERIN

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Services/Solutions offered

- 15.1.14.3 Recent developments

- 15.1.14.4 MnM view

- 15.1.15 SM ENGINEERING

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Services/Solutions offered

- 15.1.15.3 Recent developments

- 15.1.15.4 MnM view

- 15.1.16 SHANGHAI TRIOWIN INTELLIGENT MACHINERY CO., LTD

- 15.1.17 SICCADANIA

- 15.1.18 REDA SPA

- 15.1.19 COMAT

- 15.1.20 KOVALUS SEPARATION SOLUTIONS

- 15.1.1 TETRA LAVAL GROUP

- 15.2 MACHINERY/PROCESS EQUIPMENT SUPPLIERS

- 15.2.1 ALFA LAVAL

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Services/Solutions offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Product launches

- 15.2.1.3.2 Deals

- 15.2.1.3.3 Expansions

- 15.2.1.3.4 Other developments

- 15.2.1.4 MnM view

- 15.2.1.4.1 Right to win

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses and competitive threats

- 15.2.2 SPX FLOW

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Services/Solutions offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches

- 15.2.2.3.2 Deals

- 15.2.2.3.3 Expansions

- 15.2.2.3.4 Other developments

- 15.2.2.4 MnM view

- 15.2.2.4.1 Right to win

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses and competitive threats

- 15.2.3 ANDRITZ AG

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Services/Solutions offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches

- 15.2.3.3.2 Expansions

- 15.2.3.3.3 Other developments

- 15.2.3.4 MnM view

- 15.2.3.4.1 Right to win

- 15.2.3.4.2 Strategic choices

- 15.2.3.4.3 Weaknesses and competitive threats

- 15.2.4 ANDERSON DAHLEN

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Services/Solutions offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches

- 15.2.4.3.2 Expansions

- 15.2.4.4 MnM view

- 15.2.4.4.1 Right to win

- 15.2.4.4.2 Strategic choices

- 15.2.4.4.3 Weaknesses and competitive threats

- 15.2.5 FRISTAM PUMPEN KG

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Services/Solutions offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches

- 15.2.5.3.2 Expansions

- 15.2.5.3.3 Other developments

- 15.2.5.4 MnM view

- 15.2.5.4.1 Right to win

- 15.2.5.4.2 Strategic choices

- 15.2.5.4.3 Weaknesses and competitive threats

- 15.2.6 PENTAIR PLC

- 15.2.6.1 Business overview

- 15.2.6.2 Products/Services/Solutions offered

- 15.2.6.3 Recent developments

- 15.2.6.3.1 Product launches

- 15.2.6.3.2 Deals

- 15.2.6.3.3 Expansions

- 15.2.6.4 MnM view

- 15.2.6.4.1 Right to win

- 15.2.6.4.2 Strategic choices

- 15.2.6.4.3 Weaknesses and competitive threats

- 15.2.7 SULZER LTD

- 15.2.7.1 Business overview

- 15.2.7.2 Products/Services/Solutions offered

- 15.2.7.3 Recent developments

- 15.2.7.4 MnM view

- 15.2.7.4.1 Right to win

- 15.2.7.4.2 Strategic choices

- 15.2.7.4.3 Weaknesses and competitive threats

- 15.2.8 HRS HEAT EXCHANGERS LTD

- 15.2.8.1 Business overview

- 15.2.8.2 Products/Services/Solutions offered

- 15.2.8.3 Recent developments

- 15.2.8.3.1 Product launches

- 15.2.8.3.2 Deals

- 15.2.8.3.3 Expansions

- 15.2.8.3.4 Other developments

- 15.2.8.4 MnM view

- 15.2.8.4.1 Right to win

- 15.2.8.4.2 Strategic choices

- 15.2.8.4.3 Weaknesses and competitive threats

- 15.2.9 ATS CORPORATION

- 15.2.9.1 Business overview

- 15.2.9.2 Products/Services/Solutions offered

- 15.2.9.3 Recent developments

- 15.2.9.3.1 Product launches

- 15.2.9.3.2 Deals

- 15.2.9.3.3 Other developments

- 15.2.9.4 MnM view

- 15.2.9.4.1 Right to win

- 15.2.9.4.2 Strategic choices

- 15.2.9.4.3 Weaknesses and competitive threats

- 15.2.10 COPERION GMBH

- 15.2.10.1 Business overview

- 15.2.10.2 Products/Services/Solutions offered

- 15.2.10.3 Recent developments

- 15.2.10.3.1 Deals

- 15.2.10.4 MnM view

- 15.2.11 BUCHER UNIPEKTIN AG

- 15.2.11.1 Business overview

- 15.2.11.2 Products/Services/Solutions offered

- 15.2.11.3 Recent developments

- 15.2.11.3.1 Product launches

- 15.2.11.4 MnM view

- 15.2.11.4.1 Right to win

- 15.2.12 SCHERJON EQUIPMENT HOLLAND B.V.

- 15.2.12.1 Business overview

- 15.2.12.2 Products/Services/Solutions offered

- 15.2.12.3 Recent developments

- 15.2.12.3.1 Product launches

- 15.2.12.3.2 Expansions

- 15.2.12.3.3 Other developments

- 15.2.12.4 MnM view

- 15.2.13 FENCO FOOD MACHINERY S.R.L.

- 15.2.13.1 Business overview

- 15.2.13.2 Products/Services/Solutions offered

- 15.2.13.3 Recent developments

- 15.2.13.4 MnM view

- 15.2.13.4.1 Right to win

- 15.2.14 SEALTECH ENGINEERS PVT LTD

- 15.2.14.1 Business overview

- 15.2.14.2 Products/Services/Solutions offered

- 15.2.14.3 Recent developments

- 15.2.14.4 MnM view

- 15.2.14.4.1 Right to win

- 15.2.15 MICROTHERMICS, INC.

- 15.2.15.1 Business overview

- 15.2.15.2 Products/Services/Solutions offered

- 15.2.15.3 Recent developments

- 15.2.15.3.1 Product launches

- 15.2.15.4 MnM view

- 15.2.15.4.1 Right to win

- 15.2.16 SKYLARK ENGINEERS

- 15.2.17 MICRO DAIRY DESIGNS LTD

- 15.2.18 INOXPA S.A.U.

- 15.2.19 HARVEST HI-TECH EQUIPMENTS (INDIA) PVT LTD

- 15.2.20 MILKMAN DAIRY EQUIPMENT

- 15.2.1 ALFA LAVAL

16 ADJACENT AND RELATED MARKETS

- 16.1 INTRODUCTION

- 16.2 RESEARCH LIMITATIONS

- 16.3 FOOD & BEVERAGE PROCESSING EQUIPMENT MARKET

- 16.3.1 MARKET DEFINITION

- 16.3.2 MARKET OVERVIEW

- 16.3.3 FOOD & BEVERAGE PROCESSING EQUIPMENT MARKET, BY TYPE

- 16.4 BAKERY PROCESSING EQUIPMENT MARKET

- 16.4.1 MARKET DEFINITION

- 16.4.2 MARKET OVERVIEW

- 16.4.3 BAKERY PROCESSING EQUIPMENT MARKET, BY TYPE

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Breakdown of primary profiles

- 17.1.2.3 Key insights from industry experts

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 TOP-DOWN APPROACH

- 17.2.1.1 Supply-side analysis

- 17.2.2 BOTTOM-UP APPROACH (DEMAND SIDE)

- 17.2.1 TOP-DOWN APPROACH

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH ASSUMPTIONS

- 17.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS