|

시장보고서

상품코드

2022834

염소화 폴리염화비닐(CPVC) 시장 예측(-2031년) : 형상별, 등급별, 생산 프로세스별, 판매 채널별, 용도별, 최종 용도 산업별, 지역별Chlorinated Polyvinyl Chloride Market By Form (Pellet, Powder), Grade (Injection, Extrusion), Production Process, Sales Channel (Direct Sales, Indirect Sales), Application, End-use Industry, and Region - Global Forecast to 2031 |

||||||

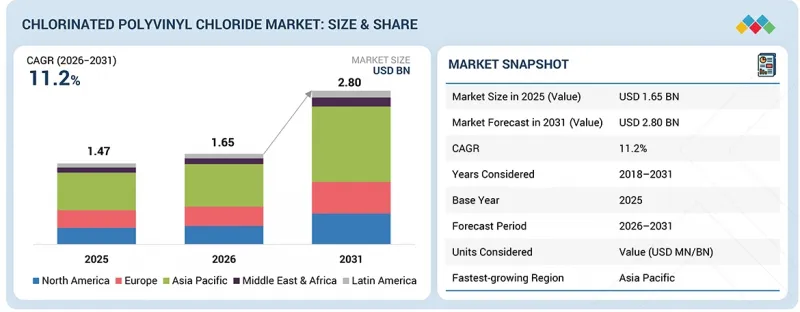

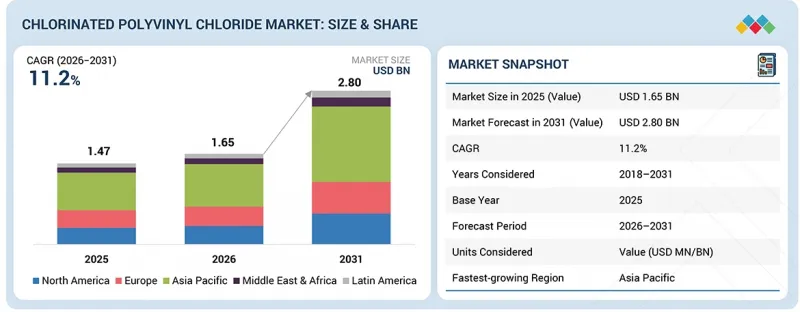

세계의 염소화 폴리염화비닐(CPVC) 시장 규모는 2026년에 추정 16억 5,000만 달러로, 2031년까지 28억 달러에 달할 것으로 예측되며, 예측 기간에 CAGR로 11.2%의 성장이 전망되고 있습니다.

첨단 가공 응용 분야의 수요 증가로 인해 펠릿 형태는 예측 기간 중 세계의 CPVC 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2018-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만/10억 달러 |

| 부문 | 형상, 등급, 생산 프로세스, 판매 채널, 용도, 최종 용도 산업 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

펠릿은 우수한 핸들링, 균일성 및 운송 용이성을 갖추고 있으며, 대규모 제조 작업에 매우 적합합니다. 맞춤형 배합에 대응하고 일관된 품질을 유지할 수 있다는 점이 파이프 및 피팅 제조업체의 채택을 더욱 촉진하고 있습니다. 또한 정밀 성형 부품 및 특수 산업 용도에 대한 수요 증가는 CPVC 펠릿의 사용 확대에 기여하고 있습니다. 압출 성형에 광범위하게 사용되어 분말 형태가 여전히 주류인 반면, 가공 효율성과 다용도로 인해 펠릿 부문이 인기를 끌고 있습니다.

"금액 기준으로는 사출성형 등급이 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. "

등급별로 보면 사출성형 등급 CPVC는 다양한 용도의 정밀 성형 부품에 대한 수요 증가로 인해 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 우수한 유동성, 열 안정성, 치수 정밀도는 피팅, 밸브와 같은 복잡한 부품 제조에 이상적입니다. 주거, 상업 및 산업 부문에서 고성능 및 맞춤형 부품에 대한 수요가 증가함에 따라 그 채택을 더욱 촉진하고 있습니다. 또한 사출성형 기술의 발전으로 생산 효율과 품질이 향상되고 있습니다. 파이프에 광범위하게 사용되는 압출 성형 등급은 여전히 시장을 독점하고 있지만, 사출성형 등급은 특수 용도에 대한 적합성으로 인해 인기를 얻고 있습니다.

"금액 기준으로는 고상법 부문이 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. "

생산 공정별로는 고상법이 제품의 성능과 효율성을 향상시키는 능력으로 인해 예측 기간 중 전 세계 CPVC 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 이 방법은 염소화 공정의 제어를 개선하고 최종 제품의 열 안정성, 기계적 강도 및 균일성을 향상시킵니다. 재료의 품질이 매우 중요한 고성능 응용 분야에서 이 방법이 점점 더 많이 채택되고 있습니다. 또한 이 공정은 기존 방식보다 에너지 효율이 높고 환경 친화적이라는 평가를 받고 있습니다. 물 현탁법이 여전히 주류 생산 공정이지만, 고상법은 기술적 우위와 첨단 응용 분야에 대한 적합성으로 인해 주목을 받고 있습니다.

"금액 기준으로는 북미가 예측 기간 중 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. "

인프라 개보수 및 현대화에 대한 투자가 증가함에 따라 북미는 예측 기간 중 세계 CPVC 시장에서 두 번째로 높은 CAGR을 기록할 것으로 예상됩니다. 이 지역에서는 배관 및 소방 시스템에서 CPVC에 대한 수요가 강세를 보이고 있으며, 특히 노후화된 금속 배관을 보다 내구성과 내식성이 뛰어난 소재로 대체하려는 움직임이 두드러집니다. 엄격한 건축 기준과 안전 규정도 주거 및 상업 부문에서 CPVC의 채택을 더욱 촉진하고 있습니다. 또한 지속가능하고 유지보수가 적은 배관 솔루션에 대한 관심이 높아지는 것도 시장 확대에 기여하고 있습니다. 기존 제조업체의 존재와 지속적인 기술 발전도 이 지역의 안정적인 성장을 지원하고 있습니다.

세계의 염화폴리염화비닐(CPVC) 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI의 채택에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 CPVC 시장 : 형상별

제10장 CPVC 시장 : 등급별

제11장 CPVC 시장 : 생산 프로세스별

제12장 CPVC 시장 : 판매 채널별

제13장 CPVC 시장 : 용도별

제14장 CPVC 시장 : 최종 용도 산업별

제15장 CPVC 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSA 26.05.14The CPVC market is estimated at USD 1.65 billion in 2026 and is projected to reach USD 2.80 billion by 2031, at a CAGR of 11.2% during the forecast period. Pellet form is expected to register the second-highest CAGR in the global CPVC market during the forecast period, driven by its growing preference in advanced processing applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2018-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Form, Grade, Production Process, Sales Channel, Application, End-use Industry |

| Regions covered | Europe, North America, Asia Pacific, the Middle East & Africa, and Latin America |

Pellets offer superior handling, uniformity, and ease of transportation, making them highly suitable for large-scale manufacturing operations. Their ability to support customized formulations and consistent product quality is further encouraging adoption among pipe and fitting manufacturers. Additionally, increasing demand for precision-molded components and specialized industrial applications is contributing to the rising use of CPVC pellets. While powder form continues to dominate due to its widespread use in extrusion, the pellet segment is gaining momentum owing to its processing efficiency and versatility.

"In terms of value, injection grade is expected to register the second-highest CAGR during the forecast period."

Based on grade, injection grade CPVC is expected to register the second-highest CAGR during the forecast period, driven by the increasing demand for precision-molded components across various applications. Its excellent flow properties, thermal stability, and dimensional accuracy make it ideal for manufacturing fittings, valves, and other complex parts. The growing need for high-performance and customized components in residential, commercial, and industrial sectors is further supporting its adoption. Additionally, advancements in injection molding technologies are enhancing production efficiency and product quality. While extrusion grade continues to dominate due to its extensive use in pipes, injection grade is gaining traction owing to its suitability for specialized applications.

"In terms of value, the solid phase method segment is expected to register the second-highest CAGR during the forecast period."

Based on production process, the solid phase method is expected to register the second-highest CAGR in the global CPVC market during the forecast period, driven by its ability to enhance product performance and efficiency. This method enables better control over the chlorination process, resulting in improved thermal stability, mechanical strength, and consistency of the final product. It is increasingly being adopted for high-performance applications where material quality is critical. Additionally, the process is considered relatively energy-efficient and environmentally favorable compared to conventional methods. While aqueous suspension remains the dominant production process, the solid-phase method is gaining traction due to its technological advantages and suitability for advanced applications.

"In terms of value, North America is expected to register the second-highest CAGR during the forecast period."

North America is expected to register the second-highest CAGR in the global CPVC market during the forecast period, driven by increasing investments in infrastructure renovation and modernization. The region is witnessing strong demand for CPVC in plumbing and fire protection systems, particularly for replacing aging metal piping with more durable and corrosion-resistant materials. Stringent building codes and safety regulations are further supporting the adoption of CPVC across residential and commercial sectors. Additionally, the growing focus on sustainable and low-maintenance piping solutions is contributing to market expansion. The presence of established manufacturers and continuous technological advancements also supports steady growth in the region.

This study has been validated through primary interviews with industry experts globally. The primary sources have been divided into the following three categories:

- By Company Type: Tier 1 - 60%, Tier 2 - 20%, and Tier 3 - 20%

- By Designation: C-level - 33%, Director-level - 33%, and Managers - 34%

- By Region: North America - 15%, Europe - 25%, Asia Pacific - 30%, the Middle East & Africa - 20%, and South America - 10%

The report provides a comprehensive analysis of the following companies:

Prominent companies in this market are The Lubrizol Corporation (US), Sekisui Chemical Co., Ltd. (Japan), Epigral Limited (India), Shandong Novista Chemicals Co., Ltd (Novista Group) (China), Shandong Pujie Rubber & Plastic Co., Ltd. (China), Kaneka Corporation (Japan), KEM ONE (France), DCW Limited (Mumbai), Sundow Polymers Co., Ltd. (China), Mitsui & Co. Ltd. (Japan), Shandong Yada New Material Co., Ltd. (China), Shandong Gaoxin Chemical Co., Ltd. (China), and Shandong Xuye New Materials Co., Ltd. (China).

Research Coverage

This research report categorizes the CPVC market by form (pellet, powder), grade (injection grade, extrusion grade), production process (aqueous suspension method, solvent method, solid phase method), sales channel (direct sales, indirect sales), application (plumbing systems, fire protection systems, chemical & industrial equipment, power cable, adhesives & coatings, and other applications), end-use industry (residential, commercial, industrial), and region (North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America). The scope of the report includes detailed information about the major factors influencing the growth of the CPVC market, such as drivers, restraints, challenges, and opportunities. A thorough examination of the key industry players has been conducted to provide insights into their business overview, solutions and services, key strategies, and recent developments in the CPVC market. This report includes a competitive analysis of upcoming startups in the CPVC market ecosystem.

Reasons to buy this report

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall CPVC market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Growth in construction and infrastructure development), restraints (Volatility of raw material cost), opportunities (Increasing adoption in industrial applications and chemical handling), and challenges (Environmental concerns and perception around chlorinated polymer standards) are influencing the growth of the CPVC market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the CPVC market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the CPVC market across varied regions

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the CPVC market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like The Lubrizol Corporation (US), Sekisui Chemical Co., Ltd. (Japan), Epigral Limited (India), Shandong Novista Chemicals Co., Ltd (Novista Group) (China), Shandong Pujie Rubber & Plastic Co., Ltd. (China), Kaneka Corporation (Japan), KEM ONE (France), DCW Limited (Mumbai), Sundow Polymers Co., Ltd. (China), Mitsui & Co. Ltd. (Japan), Shandong Yada New Material Co., Ltd. (China), Shandong Gaoxin Chemical Co., Ltd. (China), and Shandong Xuye New Materials Co., Ltd. (China).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CPVC MARKET

- 3.2 CPVC MARKET, BY APPLICATION AND REGION

- 3.3 CPVC MARKET, BY END-USE INDUSTRY

- 3.4 CPVC MARKET, BY GRADE

- 3.5 CPVC MARKET, BY FORM

- 3.6 CPVC MARKET, BY PRODUCTION PROCESS

- 3.7 CPVC MARKET, BY SALES CHANNEL

- 3.8 CPVC MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growth in construction and infrastructure development

- 4.2.1.2 Increasing investments in water supply and aging infrastructure replacement

- 4.2.1.3 Shift towards high-performance and cost-efficient materials

- 4.2.2 RESTRAINTS

- 4.2.2.1 Volatility of raw material cost

- 4.2.2.2 High competition from alternative piping materials

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing adoption in industrial applications and chemical handling

- 4.2.3.2 Shift toward sustainable and low-maintenance piping solutions

- 4.2.4 CHALLENGES

- 4.2.4.1 Environmental concerns and perception around chlorinated polymer standards

- 4.2.4.2 Susceptibility to counterfeit products and quality inconsistencies

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CPVC MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS: REGIONAL ANALYSIS

- 5.1.1.1 Asia Pacific

- 5.1.1.2 North America

- 5.1.1.3 Europe

- 5.1.1.4 Latin America

- 5.1.1.5 Middle East & Africa

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.1 THREAT OF NEW ENTRANTS: REGIONAL ANALYSIS

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN CONSTRUCTION INDUSTRY

- 5.2.4 TRENDS IN INDUSTRIAL SECTOR

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE, BY KEY PLAYERS

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 390410)

- 5.6.2 EXPORT SCENARIO (HS CODE 390410)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CPVC PIPING SOLUTION ENHANCES URBAN WATER INFRASTRUCTURE IN INDIA

- 5.10.2 CPVC ENABLES CORROSION-RESISTANT CHEMICAL PROCESSING SYSTEM IN EUROPE

- 5.10.3 CPVC FIRE SPRINKLER SYSTEM IMPROVES SAFETY IN COMMERCIAL BUILDINGS (NORTH AMERICA)

- 5.11 IMPACT OF 2025 US TARIFF ON CPVC MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCE CHLORINATION PROCESSES (FLUIDIZED BED & AQUEOUS SUSPENSION METHODS)

- 6.1.2 HIGH-PERFORMANCE ADDITIVES & STABILIZER SYSTEMS

- 6.1.3 EXTRUSION & INJECTION MOLDING ADVANCEMENTS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 SOLVENT CEMENT JOINING TECHNOLOGY

- 6.2.2 FIRE SPRINKLER SYSTEM TECHNOLOGY (BLAZEMASTER CPVC SYSTEMS)

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 METHODOLOGY

- 6.4.3 DOCUMENT TYPE

- 6.4.4 INSIGHTS

- 6.4.5 LEGAL STATUS OF PATENTS

- 6.4.6 JURISDICTION ANALYSIS

- 6.4.7 TOP APPLICANTS

- 6.4.8 LIST OF PATENTS BY SEKISUI CHEMICAL CO., LTD.

- 6.5 FUTURE APPLICATIONS

- 6.5.1 RESIDENTIAL & COMMERCIAL HOT/COLD WATER PLUMBING: INNOVATIVE CPVC-BASED SOLUTIONS

- 6.5.2 INDUSTRIAL PROCESSING PIPING SYSTEMS: EXPANDING USAGE IN CHEMICAL, PETROCHEMICAL, AND MANUFACTURING PLANTS

- 6.5.3 AUTOMATIC FIRE SPRINKLER SYSTEMS: ACCELERATING ADOPTION IN RESIDENTIAL, HIGH-RISE, AND LIGHT HAZARD COMMERCIAL BUILDINGS

- 6.5.4 UNDERGROUND CONDUIT & TRENCHLESS TECHNOLOGY: HIGH-STRENGTH CPVC CASING AND DUCTING FOR CRITICAL BURIED CABLE AND OPTIC FIBER INFRASTRUCTURE

- 6.5.5 ADVANCED BATTERY & ELECTRONICS PACKAGING: EMERGING CPVC FORMULATIONS FOR THERMALLY STABLE AND FLAME-RETARDANT COMPONENT AND BATTERY CELL CASINGS

- 6.6 IMPACT OF AI/GEN AI ON CPVC MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN CPVC PROCESSING

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN CPVC MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CPVC MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 DEVELOPMENT OF ENVIRONMENTALLY COMPLIANT MATERIALS

- 7.2.2 ENERGY-EFFICIENT MANUFACTURING & RESOURCE OPTIMIZATION

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITIBILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USES

9 CPVC MARKET, BY FORM

- 9.1 INTRODUCTION

- 9.2 POWDER

- 9.2.1 CHEMICAL RESISTANCE AND PRESSURE HANDLING CAPABILITIES TO DRIVE DEMAND

- 9.3 PELLET

- 9.3.1 BALANCED PERFORMANCE AND PROCESSABILITY TO SUPPORT MARKET GROWTH

10 CPVC MARKET, BY GRADE

- 10.1 INTRODUCTION

- 10.2 EXTRUSION GRADE

- 10.2.1 EXCELLENT THERMAL STABILITY AND SMOOTH PROCESSING TO INCREASE ADOPTION

- 10.3 INJECTION GRADE

- 10.3.1 LOW VISCOSITY AND IMPROVED MOLD FILLING TO DRIVE DEMAND

11 CPVC MARKET, BY PRODUCTION PROCESS

- 11.1 INTRODUCTION

- 11.2 AQUEOUS SUSPENSION METHOD

- 11.2.1 SUPERIOR CHEMICAL AND THERMAL STABILITY TO FUEL DEMAND

- 11.3 SOLVENT METHOD

- 11.3.1 IMPROVED PRODUCT UNIFORMITY TO DRIVE ADOPTION

- 11.4 SOLID PHASE METHOD

- 11.4.1 ENHANCED PRODUCT QUALITY AND SOLVENT-FREE ENVIRONMENT TO DRIVE MARKET GROWTH

12 CPVC MARKET, BY SALES CHANNEL

- 12.1 INTRODUCTION

- 12.2 DIRECT SALES

- 12.2.1 HIGHER MARGINS AND MARKET FEEDBACK TO FUEL DEMAND

- 12.3 INDIRECT SALES

- 12.3.1 EXPANSIVE MULTI-TIER DISTRIBUTION NETWORK TO SUPPORT MARKET GROWTH

13 CPVC MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 PLUMBING SYSTEMS

- 13.2.1 RESISTANCE TO CORROSION AND COST-EFFECTIVENESS TO FUEL DEMAND

- 13.3 FIRE PROTECTION

- 13.3.1 STRUCTURAL INTEGRITY AND LONGEVITY TO INCREASE ADOPTION

- 13.4 CHEMICAL & INDUSTRIAL EQUIPMENT

- 13.4.1 REDUCED MAINTENANCE COSTS TO PROPEL MARKET GROWTH

- 13.5 POWER CABLE CASING

- 13.5.1 ENHANCED SAFETY WITH FIRE RETARDANT PROPERTIES TO FUEL DEMAND

- 13.6 ADHESIVES & COATINGS

- 13.6.1 HIGH SOLUBILITY IN VARIOUS ORGANIC SOLVENTS TO DRIVE SEGMENTAL GROWTH

- 13.7 OTHER APPLICATIONS

14 CPVC MARKET, BY END-USE INDUSTRY

- 14.1 INTRODUCTION

- 14.2 RESIDENTIAL

- 14.2.1 STRONG HOUSING DEMAND AND SHIFT TOWARD DURABLE, LOW-MAINTENANCE PIPING SOLUTIONS DRIVING SEGMENTAL GROWTH

- 14.3 COMMERCIAL

- 14.3.1 RISING CONSTRUCTION OF COMMERCIAL INFRASTRUCTURE AND INCREASING FOCUS ON SAFETY DRIVING GROWTH

- 14.4 INDUSTRIAL

- 14.4.1 EXPANDING PROCESS INDUSTRIES AND RISING NEED FOR DURABLE FLUID HANDLING SYSTEMS FUELING GROWTH

15 CPVC MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: CPVC MARKET, BY FORM

- 15.2.2 NORTH AMERICA: CPVC MARKET, BY GRADE

- 15.2.3 NORTH AMERICA: CPVC MARKET, BY PRODUCTION PROCESS

- 15.2.4 NORTH AMERICA: CPVC MARKET, BY SALES CHANNEL

- 15.2.5 NORTH AMERICA: CPVC MARKET, BY APPLICATION

- 15.2.6 NORTH AMERICA: CPVC MARKET, BY END-USE INDUSTRY

- 15.2.7 NORTH AMERICA: CPVC MARKET, BY COUNTRY

- 15.2.7.1 US

- 15.2.7.1.1 Strong renovation activity and emphasis on high-performance building materials driving market growth

- 15.2.7.2 Canada

- 15.2.7.2.1 Growing infrastructure upgrades and increasing adoption of reliable piping materials supporting market growth

- 15.2.7.1 US

- 15.3 EUROPE

- 15.3.1 EUROPE: CPVC MARKET, BY FORM

- 15.3.2 EUROPE: CPVC MARKET, BY GRADE

- 15.3.3 EUROPE: CPVC MARKET, BY PRODUCTION PROCESS

- 15.3.4 EUROPE: CPVC MARKET, BY SALES CHANNEL

- 15.3.5 EUROPE: CPVC MARKET, BY APPLICATION

- 15.3.6 EUROPE: CPVC MARKET, BY END-USE INDUSTRY

- 15.3.7 EUROPE: CPVC MARKET, BY COUNTRY

- 15.3.7.1 Germany

- 15.3.7.1.1 Emphasis on engineering precision and compliance-led material adoption supporting market expansion

- 15.3.7.2 UK

- 15.3.7.2.1 Rising refurbishment activities and shift toward modern piping solutions supporting market growth

- 15.3.7.3 France

- 15.3.7.3.1 Strong regulatory framework and focus on sustainable building practices to drive demand

- 15.3.7.4 Italy

- 15.3.7.4.1 Renovation-driven construction landscape and demand for durable piping solutions to drive market

- 15.3.7.5 Spain

- 15.3.7.5.1 Growing infrastructure modernization and adoption of advanced building materials fueling demand

- 15.3.7.6 Rest of Europe

- 15.3.7.1 Germany

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: CPVC MARKET, BY FORM

- 15.4.2 ASIA PACIFIC: CPVC MARKET, BY GRADE

- 15.4.3 ASIA PACIFIC: CPVC MARKET, BY PRODUCTION PROCESS

- 15.4.4 ASIA PACIFIC: CPVC MARKET, BY SALES CHANNEL

- 15.4.5 ASIA PACIFIC: CPVC MARKET, BY APPLICATION

- 15.4.6 ASIA PACIFIC: CPVC MARKET, BY END-USE INDUSTRY

- 15.4.7 ASIA PACIFIC: CPVC MARKET, BY COUNTRY

- 15.4.7.1 China

- 15.4.7.1.1 Mega urban clusters and industrial corridor expansion driving sustained demand

- 15.4.7.2 India

- 15.4.7.2.1 Government-led housing push and water infrastructure programs fueling market growth

- 15.4.7.3 South Korea

- 15.4.7.3.1 Advanced construction practices and smart city initiatives supporting CPVC adoption

- 15.4.7.4 Japan

- 15.4.7.4.1 Urban redevelopment and resilience-focused infrastructure supporting market growth

- 15.4.7.5 Rest of Asia Pacific

- 15.4.7.1 China

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 MIDDLE EAST & AFRICA: CPVC MARKET, BY FORM

- 15.5.2 MIDDLE EAST & AFRICA: CPVC MARKET, BY GRADE

- 15.5.3 MIDDLE EAST & AFRICA: CPVC MARKET, BY PRODUCTION PROCESS

- 15.5.4 MIDDLE EAST & AFRICA: CPVC MARKET, BY SALES CHANNEL

- 15.5.5 MIDDLE EAST & AFRICA: CPVC MARKET, BY APPLICATION

- 15.5.6 MIDDLE EAST & AFRICA: CPVC MARKET, BY END-USE INDUSTRY

- 15.5.7 MIDDLE EAST & AFRICA: CPVC MARKET, BY COUNTRY

- 15.5.7.1 GCC countries

- 15.5.7.1.1 UAE

- 15.5.7.1.1.1 Implementation of smart city projects driving market growth

- 15.5.7.1.2 Saudi Arabia

- 15.5.7.1.2.1 Vision 2030 and mega urban developments accelerating market

- 15.5.7.1.3 Rest of GCC countries

- 15.5.7.1.1 UAE

- 15.5.7.2 South Africa

- 15.5.7.2.1 Market shaped by water scarcity and infrastructure rehabilitation needs

- 15.5.7.3 Rest of Middle East & Africa

- 15.5.7.1 GCC countries

- 15.6 LATIN AMERICA

- 15.6.1 LATIN AMERICA: CPVC MARKET, BY FORM

- 15.6.2 LATIN AMERICA: CPVC MARKET, BY GRADE

- 15.6.3 LATIN AMERICA: CPVC MARKET, BY PRODUCTION PROCESS

- 15.6.4 LATIN AMERICA: CPVC MARKET, BY SALES CHANNEL

- 15.6.5 LATIN AMERICA: CPVC MARKET, BY APPLICATION

- 15.6.6 LATIN AMERICA: CPVC MARKET, BY END-USE INDUSTRY

- 15.6.7 LATIN AMERICA: CPVC MARKET, BY COUNTRY

- 15.6.7.1 Mexico

- 15.6.7.1.1 Urban infrastructure, sanitation upgrades, and industrial construction projects to fuel growth

- 15.6.7.2 Brazil

- 15.6.7.2.1 Water infrastructure revamp projects to support market growth

- 15.6.7.3 Rest of Latin America

- 15.6.7.1 Mexico

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS

- 16.5 BRAND/PRODUCT COMPARISON

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6.5.1 Company footprint

- 16.6.5.2 Region footprint

- 16.6.5.3 Grade footprint

- 16.6.5.4 Form footprint

- 16.6.5.5 Production process footprint

- 16.6.5.6 Sales channel footprint

- 16.6.5.7 Application footprint

- 16.6.5.8 End-use industry footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPANY VALUATION AND FINANCIAL METRICS

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 EXPANSIONS

- 16.9.2 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 THE LUBRIZOL CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.3.2 Expansions

- 17.1.1.3.3 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 SEKISUI CHEMICAL CO., LTD.

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 MnM view

- 17.1.2.3.1 Right to win

- 17.1.2.3.2 Strategic choices

- 17.1.2.3.3 Weaknesses and competitive threats

- 17.1.3 EPIGRAL LIMITED

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Expansions

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 SHANGDONG NOVISTA CHEMICAL CO., LTD.

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 MnM view

- 17.1.4.3.1 Right to win

- 17.1.4.3.2 Strategic choices

- 17.1.4.3.3 Weaknesses and competitive threats

- 17.1.5 SHANDONG PUJIE RUBBER & PLASTIC CO., LTD.

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Right to win

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 KANEKA CORPORATION

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 MnM view

- 17.1.6.3.1 Right to win

- 17.1.6.3.2 Strategic choices

- 17.1.6.3.3 Weaknesses and competitive threats

- 17.1.7 SHANGDONG YADA NEW MATERIAL CO., LTD.

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 MnM view

- 17.1.7.3.1 Right to win

- 17.1.7.3.2 Strategic choices

- 17.1.7.3.3 Weaknesses and competitive threats

- 17.1.8 KEM ONE

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Other developments

- 17.1.8.4 MnM view

- 17.1.8.4.1 Right to win

- 17.1.8.4.2 Strategic choices

- 17.1.8.4.3 Weaknesses and competitive threats

- 17.1.9 SHANDONG XUYE NEW MATERIALS CO., LTD.

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 MnM view

- 17.1.9.3.1 Right to win

- 17.1.9.3.2 Strategic choices

- 17.1.9.3.3 Weaknesses and competitive threats

- 17.1.10 DCW LIMITED

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Expansions

- 17.1.10.4 MnM view

- 17.1.10.4.1 Right to win

- 17.1.10.4.2 Strategic choices

- 17.1.10.4.3 Weaknesses and competitive threats

- 17.1.11 SUNDOW POLYMERS CO., LTD.

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 MnM view

- 17.1.11.3.1 Right to win

- 17.1.11.3.2 Strategic choices

- 17.1.11.3.3 Weaknesses and competitive threats

- 17.1.12 MITSUI & CO., LTD.

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 MnM view

- 17.1.12.3.1 Right to win

- 17.1.12.3.2 Strategic choices

- 17.1.12.3.3 Weaknesses and competitive threats

- 17.1.13 SHANGHAI CHLOR-ALKALI CHEMICAL CO., LTD.

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Solutions/Services offered

- 17.1.13.3 MnM view

- 17.1.13.3.1 Right to win

- 17.1.13.3.2 Strategic choices

- 17.1.13.3.3 Weaknesses and competitive threats

- 17.1.1 THE LUBRIZOL CORPORATION

- 17.2 OTHER COMPANIES

- 17.2.1 SHANDONG GAOXIN CHEMICAL CO., LTD.

- 17.2.2 HANWHA SOLUTIONS

- 17.2.3 HANGZHOU ELECTROCHEMICAL GROUP CO., LTD.

- 17.2.4 EN-DOOR

- 17.2.5 WEIFANG YADA PLASTIC CO., LTD.

- 17.2.6 SHANDONG KETIAN CHEMICAL CO., LTD.

- 17.2.7 VIA CHEMICAL CO., LTD.

- 17.2.8 JIANGSU TIANTENG CHEMICAL CO., LTD.

- 17.2.9 AVIENT CORPORATION

- 17.2.10 KUNSHAN MAIJISEN COMPOSITE MATERIALS CO., LTD.

- 17.2.11 ZHONGTAI IMPORT & EXPORT CORPORATION

- 17.2.12 SHANDONG HONOR NEW MATERIAL CO., LTD.

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Key primary interview participants

- 18.1.2.3 Breakdown of primary interviews

- 18.1.2.4 Key industry insights

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.2.1 BOTTOM-UP APPROACH

- 18.2.2 TOP-DOWN APPROACH

- 18.3 BASE NUMBER CALCULATION

- 18.3.1 APPROACH 1: SUPPLY-SIDE ANALYSIS

- 18.3.2 APPROACH 2: DEMAND-SIDE ANALYSIS

- 18.4 MARKET FORECAST APPROACH

- 18.4.1 SUPPLY SIDE

- 18.4.2 DEMAND SIDE

- 18.5 DATA TRIANGULATION

- 18.6 FACTOR ANALYSIS

- 18.7 RESEARCH ASSUMPTIONS

- 18.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS