|

시장보고서

상품코드

2027004

유리 기판 시장 : 유형별, 최종 이용 산업별, 지역별 - 세계 예측(-2031년)Glass Substrate Market by Type (Borosilicate-based, Silicon-based, Ceramic-based, Other Types), End-use Industry (Electronics, Automotive, Medical, Aerospace & Defense, and Solar Power), and Region - Global Forecast To 2031 |

||||||

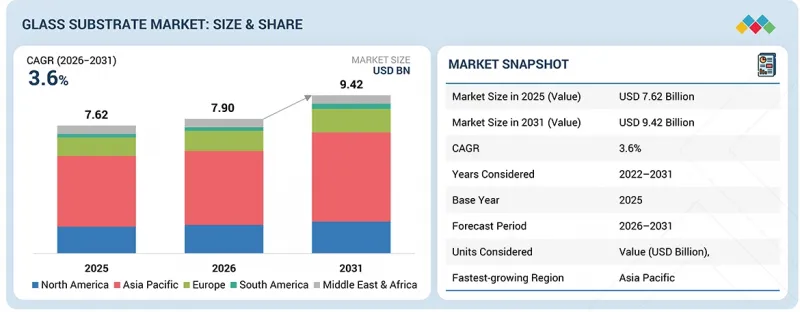

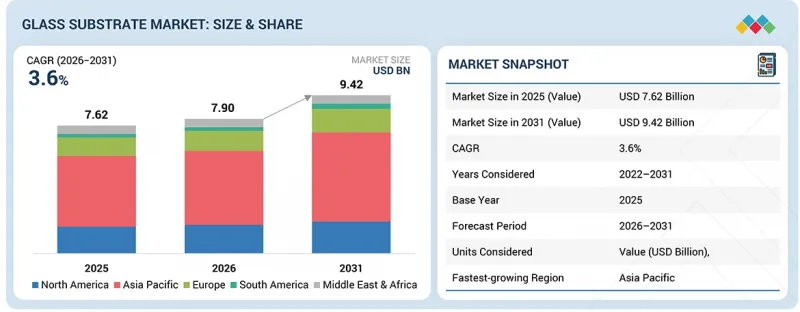

세계의 유리 기판 시장 규모는 2026년 79억 달러에서 2031년까지 94억 2,000만 달러에 달할 것으로 예측되며, 예측 기간 동안 CAGR로 3.6%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 100만 달러 |

| 부문 | 유형, 최종 이용 산업, 지역 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

유리 기판 시장은 반도체 및 전자 산업, 특히 HPC 및 첨단 패키징 응용 분야의 수요 증가로 인해 성장할 것으로 예상됩니다. 또한, OLED 디스플레이, AI, 5G 기술의 보급이 진행됨에 따라 수요는 더욱 확대되고 있습니다.

"붕규산 유리 기판 부문이 2031년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

붕규산 유리 기판 부문은 최고의 내열성과 낮은 열팽창률로 반도체 및 디스플레이 응용 분야에 적합하여 2031년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 높은 화학적 내구성과 치수 안정성으로 고온 환경 및 정밀 제조 공정에서 신뢰성을 보장합니다. 이러한 특성으로 인해 하이 레벨 패키징, OLED 디스플레이, 태양광발전 모듈에 최적입니다.

"전자 부문이 2031년에 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

전자 부문은 디스플레이, 반도체, 회로 부품에 유리 기판이 많이 사용되면서 2031년 가장 큰 시장 점유율을 기록할 것으로 예상됩니다. 스마트폰, 노트북, TV 등 가전제품의 급속한 성장이 수요를 촉진하고 있습니다. AI, 5G, HPC 등의 기술 발전이 첨단 기판에 대한 수요를 촉진하고 있습니다.

"아시아태평양의 보호 필름 시장은 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 예상됩니다."

아시아태평양의 유리 기판 시장은 반도체 및 전자기기 제조 산업을 중심으로 예측 기간 동안 가장 높은 CAGR을 보일 것으로 예상됩니다. 이 지역에는 많은 투자와 정부의 지원, 그리고 제조 시설의 확장이 진행되고 있습니다. 또한, 소비자 전자제품, 재생에너지, 자동차 전자제품에 대한 수요 증가가 성장을 견인하고 있습니다.

세계의 유리 기판 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대한 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI 채용에 의한 전략적 파괴

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 유리 기판 시장 : 유형별

제10장 유리 기판 시장 : 최종 이용 산업별

제11장 유리 기판 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

KSM 26.05.20The glass substrate market is projected to grow from USD 7.90 billion in 2026 to USD 9.42 billion in 2031, at a CAGR of 3.6% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million) |

| Segments | Type, End-use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The glass substrate market is expected to grow due to increased demand from the semiconductor and electronics industries, especially for high-performance computing and advanced packaging applications. The demand is also growing as OLED displays, AI, and 5G technologies become more widespread.

"The borosilicate-based glass substrate segment is projected to capture the largest market share in 2031."

The borosilicate-based glass substrate segment is expected to have the highest market share in 2031 because it offers the best thermal resistance and low thermal expansion, making it suitable for semiconductor and display applications. Its high chemical durability and dimensional stability ensure reliability in high-temperature and precision manufacturing processes. Its properties make it well-suited for high-level packaging, OLED displays, and photovoltaic modules.

"The electronics segment is projected to capture the largest market share in 2031."

The electronics segment will record the largest market share in 2031 due to the high usage of glass substrates in displays, semiconductors, and circuit components. The rapid growth of consumer electronics, such as smartphones, laptops, and TVs, is largely driving demand. Advances in technologies such as AI, 5G, and high-performance computing are driving the need for advanced substrates.

"Asia Pacific protective films market is projected to grow at the highest CAGR during the forecast period."

The Asia Pacific glass substrate market is expected to have the highest CAGR over the forecast period, as it has dominated the semiconductor and electronics manufacturing industry. The region has high investments, government encouragement, and growing manufacturing facilities. Growth is further propelled by increasing demand for consumer electronics, renewable energy, and automotive electronics.

By Company Type: Tier 1 - 52%, Tier 2 - 26%, and Tier 3 - 22%

By Designation: C-level Executives - 48%, Directors - 23%, and Others - 29%

By Region: North America - 20%, Europe - 10%, Asia Pacific - 40%, South America - 10%, and Middle East & Africa - 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 500 Million; Tier 2: USD 100 million-500 Million; and Tier 3: <USD 100 million

Companies Covered: AGC Inc. (Japan), Schott AG (Germany), Corning Incorporated (US), Nippon Sheet Glass Co., Ltd. (Japan), and HOYA Corporation (Japan), among other companies, are covered in the report.

The study includes an in-depth competitive analysis of these key players in the glass substrate market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the glass substrate market based on type (borosilicate-based glass substrate, silicon-based glass substrate, ceramic-based glass substrate, fused silica-/quartz- based glass substrate, and other types), end-use industry (electronics, automotive, medical, aerospace & defense, and solar power), and region (Asia Pacific, North America, Europe, South America, and the Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the glass substrate market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, products offered, and key strategies, including product launches, expansions, partnerships, and collaborations related to the glass substrate market. This report covers a competitive analysis of upcoming startups in the glass substrate market ecosystem.

Reasons to Buy the Report

The report will provide market leaders/new entrants with information on the closest approximations of revenue for the overall glass substrate market and its subsegments. This report will help stakeholders understand the competitive landscape, gain deeper insights into positioning their businesses, and plan suitable go-to-market strategies. The report will help stakeholders understand the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (Rapid semiconductor industry expansion), restraints (High technology development and manufacturing cost), opportunities (Rapid expansion of global solar installations), and challenges (LCD glass to meet strict quality requirements)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the glass substrate market

- Market Development: Comprehensive information about profitable markets-the report analyzes the glass substrate market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the glass substrate market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as AGC Inc. (Japan), Schott AG (Germany), Corning Incorporated (US), Nippon Sheet Glass Co., Ltd. (Japan), and HOYA Corporation (Japan).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 STAKEHOLDERS

- 1.4 SUMMARY OF STRATEGIC CHANGES IN MARKET

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING GLASS SUBSTRATE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN GLASS SUBSTRATE MARKET

- 3.2 GLASS SUBSTRATE MARKET, BY TYPE AND REGION

- 3.3 GLASS SUBSTRATE MARKET, BY END-USE INDUSTRY

- 3.4 GLASS SUBSTRATE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid semiconductor industry expansion

- 4.2.1.2 Rising demand for large-sized and high-resolution displays

- 4.2.1.3 Rapid expansion of 5G networks and IoT ecosystems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High technology development and manufacturing cost

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Innovations in display technologies

- 4.2.3.2 Rapid expansion of global solar installations

- 4.2.3.3 Emergence of glass core substrates as a next-gen solution

- 4.2.4 CHALLENGES

- 4.2.4.1 LCD glass to meet strict quality requirements

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN GLASS SUBSTRATE MARKET

- 4.3.1.1 Scalable, high-yield manufacturing of glass substrate for advanced packaging

- 4.3.1.2 Achieving cost competitiveness through process and material innovation

- 4.3.1.3 Standardization and ecosystem alignment with semiconductor manufacturing

- 4.3.1.4 Enhancing thermal-mechanical performance for advanced systems

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 High-frequency applications in 5G/6G, RF, and mmWave Systems

- 4.3.2.2 Photonics and co-packaged optics in data center and AI applications

- 4.3.2.3 Panel-level packaging (PLP) for cost and scale advantages

- 4.3.1 UNMET NEEDS IN GLASS SUBSTRATE MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING EXPANSION AND PRODUCT INNOVATION

- 4.5.1.1 Corning incorporated-capacity expansion in LCD glass substrates

- 4.5.1.2 Nippon electric glass co., Ltd.-product innovation in glass core substrates

- 4.5.1 TIER 1 PLAYERS: GLOBAL LEADERS DRIVING EXPANSION AND PRODUCT INNOVATION

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.2.3 TRENDS IN ELECTRONICS INDUSTRY

- 5.2.4 TRENDS IN AUTOMOTIVE INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 PRICING ANALYSIS BASED ON REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO (HS CODE 7005)

- 5.6.2 IMPORT SCENARIO (HS CODE 7005)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SAFE TRANSPORT CONTAINERS FOR SCHOTT TELESCOPE MIRROR SUBSTRATE

- 5.11 IMPACT OF US TARIFFS-GLASS SUBSTRATE MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Asia Pacific

- 5.11.4.3 Europe

- 5.11.5 END-USE INDUSTRY IMPACT

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ULTRA-THIN GLASS (UTG) TECHNOLOGY

- 6.1.2 LARGE-GENERATION DISPLAY GLASS (GEN 10.5+)

- 6.1.3 THROUGH GLASS VIA (TGV) TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 THIN FILM DEPOSITION

- 6.2.2 PHOTOLITHOGRAPHY & ETCHING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ADVANCED SEMICONDUCTOR PACKAGING (2.5D/3D INTEGRATION & CHIPLETS)

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & INTEGRATION

- 6.4.3 LONG-TERM (2030-2035+) | MATURITY & SUSTAINABLE ADVANCED MATERIAL SYSTEMS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 GLASS SUBSTRATE MARKET, PATENT ANALYSIS, 2016-2025

- 6.6 FUTURE APPLICATIONS

- 6.6.1 EXPANSION OF GLASS SUBSTRATES INTO NEXT-GENERATION SYSTEMS

- 6.7 IMPACT OF AI/GEN AI ON GLASS SUBSTRATE MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN GLASS SUBSTRATE

- 6.7.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN GLASS SUBSTRATE MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 CORNING ASTRA GLASS ENABLES HIGH-PERFORMANCE QUANTUM DOT DISPLAYS FOR NEXT-GENERATION TVS AND MONITORS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GLASS SUBSTRATE

- 7.2.1.1 Carbon Impact Reduction

- 7.2.1.2 Eco-Applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF GLASS SUBSTRATE

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.6 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 GLASS SUBSTRATE MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 BOROSILICATE-BASED GLASS SUBSTRATES

- 9.2.1 ADVANTAGEOUS PROPERTIES OF GLASS SUBSTRATES TO DRIVE DEMAND

- 9.3 SILICON-BASED GLASS SUBSTRATES

- 9.3.1 MECHANICAL SUPPORT FOR INTEGRATED CIRCUITS TO SUPPORT GROWTH

- 9.4 CERAMIC-BASED GLASS SUBSTRATES

- 9.4.1 ABILITY TO WITHSTAND THERMAL SHOCKS TO DRIVE DEMAND

- 9.5 FUSED SILICA-/QUARTZ-BASED GLASS SUBSTRATES

- 9.5.1 GOOD THERMAL SHOCK RESISTANCE TO DRIVE DEMAND

- 9.6 OTHER TYPES

10 GLASS SUBSTRATE MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 ELECTRONICS

- 10.2.1 INCREASING DEMAND FOR CONSUMER ELECTRONICS PRODUCTS TO DRIVE DEMAND

- 10.3 AUTOMOTIVE

- 10.3.1 RISING DEMAND FOR ELECTRIC VEHICLES TO DRIVE DEMAND

- 10.4 MEDICAL

- 10.4.1 GROWING MEDICAL DEVICE INDUSTRY TO DRIVE DEMAND

- 10.5 AEROSPACE & DEFENSE

- 10.5.1 HIGH OPTICAL CLARITY AND RESISTANCE TO ENVIRONMENTAL FACTORS TO DRIVE DEMAND

- 10.6 SOLAR POWER

- 10.6.1 RAPID GROWTH IN GLOBAL SOLAR INSTALLATIONS TO DRIVE DEMAND

11 GLASS SUBSTRATE MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 ASIA PACIFIC

- 11.2.1 CHINA

- 11.2.1.1 Dominance in display manufacturing to propel market

- 11.2.2 JAPAN

- 11.2.2.1 Semiconductor investment and advanced packaging technology development to drive market

- 11.2.3 INDIA

- 11.2.3.1 Rapid growth of electric vehicle industry to boost market

- 11.2.4 SOUTH KOREA

- 11.2.4.1 Semiconductor manufacturing leadership to augment market

- 11.2.5 TAIWAN

- 11.2.5.1 Expansion of AI chip development to boost market

- 11.2.6 REST OF ASIA PACIFIC

- 11.2.1 CHINA

- 11.3 NORTH AMERICA

- 11.3.1 US

- 11.3.1.1 Growth in electric vehicles to propel market

- 11.3.2 CANADA

- 11.3.2.1 Rising adoption of zero-emission vehicles to drive market

- 11.3.3 MEXICO

- 11.3.3.1 Expansion of automotive manufacturing to drive market

- 11.3.1 US

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Semiconductor expansion and advanced packaging demand to propel market

- 11.4.2 FRANCE

- 11.4.2.1 Expansion of solar energy and photovoltaic installations to drive market

- 11.4.3 UK

- 11.4.3.1 Growing electric vehicle adoption to augment market

- 11.4.4 ITALY

- 11.4.4.1 Rapid solar PV expansion and renewable energy targets to augment market

- 11.4.5 RUSSIA

- 11.4.5.1 Electronics localization and domestic production expansion to boost market

- 11.4.6 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Semiconductor ecosystem development to drive market

- 11.5.1.2 UAE

- 11.5.1.2.1 Rapid electric vehicle adoption and smart mobility initiatives to boost market

- 11.5.1.3 Rest of GCC countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Rapid expansion of solar energy to propel market

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Rapid expansion of distributed solar energy to propel market

- 11.6.2 ARGENTINA

- 11.6.2.1 Growing automotive industry to drive market

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES'S/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY VALUATION AND FINANCIAL METRICS

- 12.5.1 COMPANY VALUATION

- 12.5.2 FINANCIAL METRICS

- 12.6 BRAND COMPARISON

- 12.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.7.1 STARS

- 12.7.2 EMERGING LEADERS

- 12.7.3 PERVASIVE PLAYERS

- 12.7.4 PARTICIPANTS

- 12.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 12.7.5.1 Company footprint

- 12.7.5.2 Region footprint

- 12.7.5.3 Type footprint

- 12.7.5.4 End-use industry footprint

- 12.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.8.1 PROGRESSIVE COMPANIES

- 12.8.2 RESPONSIVE COMPANIES

- 12.8.3 DYNAMIC COMPANIES

- 12.8.4 STARTING BLOCKS

- 12.9 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.9.1 DETAILED LIST OF KEY STARTUPS/SMES

- 12.9.2 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 12.10 COMPETITIVE SCENARIO

- 12.10.1 PRODUCT LAUNCHES

- 12.10.2 DEALS

- 12.10.3 EXPANSIONS

- 12.10.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 AGC INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Solutions/Services offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Deals

- 13.1.1.3.2 Expansions

- 13.1.1.3.3 Others

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses and competitive threats

- 13.1.2 CORNING INCORPORATED

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Solutions/Services offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Expansions

- 13.1.2.3.2 Others

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses and competitive threats

- 13.1.3 SCHOTT AG

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Solutions/Services offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.3.4 Others

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 NIPPON SHEET GLASS CO., LTD.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Deals

- 13.1.4.3.2 Expansions

- 13.1.4.3.3 Others

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 PLAN OPTIK AG

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 HOYA CORPORATION

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 MnM view

- 13.1.7 OHARA INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 MnM view

- 13.1.8 TOPPAN INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Solutions/Services offered

- 13.1.8.3 MnM view

- 13.1.9 TUNGHSU GROUP CO. LTD.

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 MnM view

- 13.1.10 NIPPON ELECTRIC GLASS CO., LTD.

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 MnM view

- 13.1.1 AGC INC.

- 13.2 OTHER PLAYERS

- 13.2.1 SPECIALTY GLASS PRODUCTS

- 13.2.2 ABSOLICS INC.

- 13.2.3 BIOTAIN CRYSTAL CO., LIMITED

- 13.2.4 VALLEY DESIGN CORP.

- 13.2.5 AVANSTRATE INC.

- 13.2.6 KYODO INTERNATIONAL, INC.

- 13.2.7 TAIWAN GLASS IND. CORP.

- 13.2.8 GUARDIAN INDUSTRIES

- 13.2.9 TECNISCO, LTD.

- 13.2.10 ARRYAIT CORPORATION

- 13.2.11 PRAZISIONS GLAS & OPTIK GMBH

- 13.2.12 JIANGSU SUCHUAN TECHNOLOGY CO., LTD.

- 13.2.13 BUWON PRECISION SCIENCES CO., LTD.

- 13.2.14 VIRACON

- 13.2.15 3DGS

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 TOP-DOWN APPROACH

- 14.2.2 BOTTOM-UP APPROACH

- 14.3 BASE NUMBER CALCULATION

- 14.3.1 BASE NUMBER APPROACH 1

- 14.3.2 BASE NUMBER APPROACH 2

- 14.4 MARKET FORECAST APPROACH

- 14.4.1 SUPPLY SIDE

- 14.4.2 DEMAND SIDE

- 14.5 DATA TRIANGULATION

- 14.6 RESEARCH ASSUMPTIONS

- 14.7 RISK ASSESSMENT

- 14.8 GROWTH RATE ASSUMPTIONS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 CUSTOMIZATION OPTIONS

- 15.3 RELATED REPORTS

- 15.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.5 AUTHOR DETAILS