|

시장보고서

상품코드

2033993

X선 검출기 시장 예측(-2031년) : 기술별, 용도별X-ray Detectors Market by Technology, Application Global Forecast to 2031 |

||||||

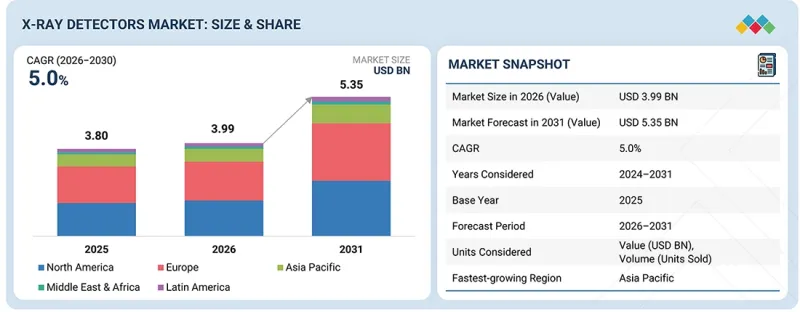

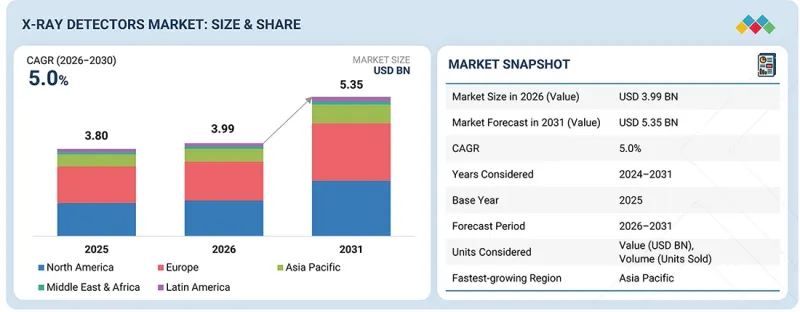

세계의 X선 검출기 시장 규모는 2025년 38억 달러에서 2031년까지 53억 5,000만 달러에 달할 것으로 예측되며, 2026-2031년에 CAGR로 5.0%의 성장이 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2025-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2025-2031년 |

| 단위 | 10억 달러 |

| 부문 | 기술, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

시장 촉진요인은 질병의 조기 및 정확한 진단에 대한 관심 증가와 환자 수 증가 및 만성질환의 증가로 진단용 영상에 대한 지속적인 수요를 촉진하고 있습니다. 이와 함께 의료 인프라 현대화를 위한 지속적인 투자와 디지털 이미징 생태계로의 전환은 첨단 엑스레이 검출기 기술의 채택을 가속화하고 있습니다.

여러 전문 분야에 걸쳐 영상에 대한 임상적 의존도가 높아짐에 따라 X선 검출기의 적용 범위가 계속 확대되고 있으며, 장기적인 시장 성장의 탄탄한 토대를 마련하고 있습니다. 시장에서는 혁신 주도형 채용으로 뚜렷한 전환을 볼 수 있습니다. 휴대용 현장 진료용 엑스레이 시스템의 보급이 확대되면서 응급, 외래, 원격의료 현장에서 영상 촬영에 대한 접근성이 향상되고 있습니다.

또한 AI를 영상 워크플로우에 통합함으로써 진단 정확도를 높이고, 영상 해석을 가속화하며, 임상적 의사결정을 최적화하고 있습니다. 검출기의 감도와 화질 향상으로 방사선 피폭을 줄이면서 진단의 신뢰도를 더욱 높이고 있습니다.

기술별로는 평판 검출기 부문이 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다.

X선 검출기 시장의 성장은 검출기 기술 중 가장 높은 성장률을 기록할 것으로 예상되는 FPD(Flat Panel Detector) 기술의 채택 확대에 의해 촉진되고 있습니다. 플랫 패널 검출기는 기존의 컴퓨터 방사선 촬영(CR) 시스템과 비교하여 더 높은 해상도, 더 빠른 이미지 획득, 실시간 이미징 기능 등 우수한 디지털 이미징 능력을 제공합니다. 이러한 장점은 진단 정확도 향상, 방사선과 워크플로우의 효율화, 환자의 방사선 피폭 감소에 기여하므로 현대 의료영상 환경에서 FPD를 강력히 권장하고 있습니다. 평판형 검출기의 확장을 지원하는 또 다른 중요한 추세는 병원과 영상센터 전체가 기존의 필름 기반 영상 시스템이나 CR 영상 시스템에서 완전 디지털 방사선 촬영 플랫폼으로 전환하고 있다는 점입니다.

휴대용 평판 검출기 부문은 2025년 휴대용 평판 검출기 부문에서 가장 높은 CAGR을 기록했습니다.

X선 검출기 시장에서는 휴대용 평판형 검출기(FPD)의 채택이 빠르게 진행되고 있으며, 검출기 형태 중 가장 빠른 성장이 예상되고 있습니다. 주로 다양한 의료 현장에서 유연한 POC(Point-of-Care) 이미징 솔루션에 대한 수요 증가가 이러한 성장을 주도하고 있습니다. 휴대용 FPD를 통해 임상의는 환자의 침대 옆, 특히 응급실, 중환자실, 원격지 및 자원이 제한된 환경에서 영상을 촬영할 수 있습니다. 이 기능은 워크플로우의 효율성을 높이고, 환자의 이동을 최소화하며, 시간적 제약이 있는 상황에서 신속한 임상적 판단을 돕습니다. 이 부문의 확장을 지원하는 중요한 추세는 높은 화질과 조작상의 기동성을 겸비한 경량 무선 디지털 검출기로의 전환입니다. 이러한 시스템은 신속하고 신뢰할 수 있는 영상 촬영이 필수적인 외상 및 응급의료 분야에서 특히 중요합니다. 또한 모바일 엑스레이 시스템의 보급 확대, 재택 의료 서비스의 확대, 신흥 시장의 의료 인프라의 지속적인 정비로 인해 휴대용 FPD에 대한 수요는 더욱 가속화되고 있습니다.

용도별로는 의료 응용 분야가 2025년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다.

X선 검출기 시장에서는 전 세계에서 고령화 및 만성질환의 유병률 증가로 인해 의료용 영상에 대한 수요가 증가하고 있습니다. 암, 심혈관 질환, 근골격계 질환 등의 질환에서는 조기 발견, 치료 계획 수립, 경과 관찰을 위해 잦은 영상 촬영이 필요합니다. 그 결과, 의료 서비스 제공자들은 정확하고 신속한 진단을 위해 고성능 검출기가 장착된 첨단 엑스레이 이미징 시스템에 대한 의존도가 높아지고 있으며, 이로 인해 의료용 애플리케이션 부문의 시장 지배력이 더욱 강화되고 있습니다.

세계의 X선 검출기 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 X선 검출기 시장 : 기술별

제8장 X선 검출기 시장 : 용도별

제9장 플랫 패널 검출기 시장

제10장 X선 검출기 시장 : 지역별

제11장 경쟁 구도

제12장 기업 개요

제13장 조사 방법

제14장 부록

KSA 26.05.26The global X-ray detectors market is projected to reach USD 5.35 billion by 2031 from USD 3.80 billion in 2025, at a CAGR of 5.0% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2025-2031 |

| Base Year | 2025 |

| Forecast Period | 2025-2031 |

| Units Considered | Value (USD billion) |

| Segments | Technology, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The market is driven by an increasing emphasis on early and accurate disease detection, coupled with a rising patient pool and a growing burden of chronic conditions, which is driving sustained demand for diagnostic imaging. In parallel, ongoing investments in healthcare infrastructure modernization and the transition toward digital imaging ecosystems are accelerating the adoption of advanced X-ray detector technologies.

The expanding clinical reliance on imaging across multiple specialties continues to broaden the application scope of X-ray detectors, establishing a strong foundation for long-term market growth. The market is witnessing a clear shift toward innovation-led adoption. The increasing deployment of portable and point-of-care X-ray systems is enhancing access to imaging in emergencies, outpatient, and remote care settings.

Additionally, integrating artificial intelligence (AI) into imaging workflows improves diagnostic accuracy, enabling faster image interpretation and optimizing clinical decision-making. Advancements in detector sensitivity and image quality are further strengthening diagnostic confidence while reducing radiation exposure.

By technology, the flat-panel detectors segment is expected to register the highest CAGR during the forecast period.

By technology, the X-ray detectors market is segmented into flat-panel detectors, computed radiography detectors, line scan detectors, charge-coupled device detectors, and photon-counting detectors . The growth of the X-ray detectors market is driven by the increasing adoption of flat-panel detectors (FPD) technology, which is expected to record the highest growth among detector technologies. Flat-panel detectors offer superior digital imaging capabilities, including higher image resolution, faster image acquisition, and real-time imaging functionality compared to traditional computed radiography (CR) systems. These advantages improve diagnostic accuracy, enhance workflow efficiency in radiology departments, and help reduce patient radiation exposure, making FPDs highly preferred in modern medical imaging environments. Another important trend supporting the expansion of flat-panel detectors is the ongoing transition from conventional film-based and CR imaging systems to fully digital radiography platforms across hospitals and diagnostic imaging centers.

By portability, the portable flat-panel detectors segment accounted for the highest CAGR of the market in 2025.

The X-ray detectors market is witnessing strong adoption of portable flat-panel detectors (FPDs), which are projected to grow the fastest among detector formats. The increasing need for flexible, point-of-care imaging solutions across diverse healthcare settings primarily drives this growth. Portable FPDs enable clinicians to conduct imaging at the patient's bedside, particularly in emergency departments, intensive care units, and remote or resource-constrained environments. This capability enhances workflow efficiency, minimizes patient movement, and supports faster clinical decision-making in time-sensitive scenarios. A key trend underpinning this segment's expansion is the shift toward lightweight, wireless digital detectors that combine high image quality with operational mobility. These systems are particularly critical in trauma and emergency care, where rapid and reliable imaging is essential. Additionally, the rising deployment of mobile X-ray systems, the expansion of home healthcare services, and ongoing healthcare infrastructure development in emerging markets are further accelerating demand for portable FPDs.

By application, the medical applications segment accounted for the highest market share in 2025.

The X-ray detectors market is experiencing an increasing demand for medical imaging driven by the rising prevalence of chronic diseases and the growing aging population worldwide. Conditions such as cancer, cardiovascular disorders, and musculoskeletal diseases require frequent diagnostic imaging for early detection, treatment planning, and disease monitoring. As a result, healthcare providers are increasingly relying on advanced X-ray imaging systems equipped with high-performance detectors to deliver accurate, rapid diagnoses, thereby strengthening the dominance of the medical application segment in the market.

Another important trend supporting this growth is the rapid adoption of digital radiography systems across hospitals and diagnostic imaging centers. Continuous investments in healthcare infrastructure, particularly in developed regions such as the United States, along with increasing funding for advanced medical imaging technologies, are further accelerating the demand for high-quality X-ray detectors. The ongoing modernization of radiology departments and the need for faster, more efficient diagnostic workflows are encouraging healthcare facilities to adopt advanced detector technologies, thereby reinforcing the medical segment as the largest application area in the global X-ray detectors market .

Asia Pacific is expected to register the highest growth rate in the market during the forecast period.

The rapid expansion of healthcare infrastructure across the Asia-Pacific region is driving growth in the X-ray detectors market. Countries such as China and India, along with several Southeast Asian nations, are experiencing rapid growth in healthcare facilities, rising healthcare expenditures, and increasing demand for advanced diagnostic imaging technologies. The region's large and growing population, coupled with the rising prevalence of chronic diseases and greater awareness of early disease diagnosis, is significantly increasing demand for modern digital X-ray systems equipped with high-performance detectors.

Another important trend supporting market growth is the rising level of government and private sector investment in healthcare infrastructure. The construction of new hospitals, expansion of diagnostic imaging centers, and increased funding for advanced medical technologies are accelerating the adoption of digital radiography systems across the region. In addition, the presence of local X-ray equipment manufacturers and the growing use of cost-effective digital imaging solutions are further strengthening the market. These factors collectively position Asia-Pacific as the fastest-growing region in the global X-ray detectors market.

A breakdown of the primary participants referred to for this report is provided below:

- By Company Type: Tier 1 (40%), Tier 2 (30%), and Tier 3 (30%)

- By Designation: C-level Executives (55%), Directors (27%), and Others (18%)

- By Region: North America (35%), Europe (32%), Asia Pacific (25%), Latin America (6%), and the Middle East & Africa (2%)

The prominent players in this market are Agfa-Gevaert Group (Belgium), Analogic Corporation (US), Canon Inc. (Japan), Carestream Health (US), Detection Technology Plc (Finland), DRTECH (South Korea), Fujifilm Holdings Corporation (Japan), Hamamatsu Photonics K.K. (Japan), iRay Group (China), Konica Minolta Inc. (Japan), New Medical Imaging Co., Ltd (China), Rigaku Holdings Corporation (Japan), Teledyne Technologies (US), Thales Group (France), Varex Imaging (US), among others.

Research Coverage

The X-ray detectors market is segmented by technology, application, end user, and region. Key factors influencing market growth include driving forces, restraints, opportunities, and challenges for stakeholders. The report also reviews the leading companies competing in the X-ray detectors market. A micro-level analysis can be conducted to examine trends, growth opportunities, and contributions to the market. Additionally, it highlights potential revenue growth opportunities across various market segments in five major regions.

Key Benefits of Buying the Report

The report is valuable for new entrants to the X-ray detectors market, as it provides comprehensive market information. This information is essential for understanding various investment opportunities. The report provides insights into both key and smaller players in the market, which can help create a solid basis for risk analysis when making investment decisions. It accurately segments the market by end users and regions, providing focused insights into specific market segments. Additionally, the report highlights key trends, challenges, growth drivers, and opportunities to support strategic decision-making through a thorough analysis.

The report provides insights into the following points:

- Key drivers (expanding applications of X-ray detectors, investments to advance healthcare facilities and digital imaging technologies), restraints (stringent regulatory requirements, health hazards of full-body scanning), opportunities (growing demand for portable and mobile imaging, development of advanced detector materials, technological advancements in detector technology), and challenges (lack of skilled radiologists and technicians, increasing adoption of refurbished X-ray units)

- Product Development/Innovation: Emerging technologies in space, R&D, recent product launches & approvals in the X-ray detectors market

- Market Growth: In-depth insights into remunerative markets report to analyze the X-ray detectors market across varied geographies

- Market Diversification: Detailed analysis of new products, unexplored geographies, latest trends, and investments in the X-ray detectors market

- Competitive Assessment: Detailed assessment of market share, service offerings, leading strategies of major players such as Canon Inc. (Japan), (South Korea), Fujifilm Holdings Corporation (Japan), Hamamatsu Photonics K.K. (Japan), iRay Group (China), Teledyne Technologies (US), Thales Group (France), Varex Imaging (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 RESEARCH LIMITATIONS

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 DISRUPTIVE TRENDS IN X-RAY DETECTORS MARKET

- 2.3 HIGH-GROWTH SEGMENTS

- 2.4 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 X-RAY DETECTORS MARKET OVERVIEW

- 3.2 NORTH AMERICA: X-RAY DETECTORS MARKET, BY TECHNOLOGY, 2025

- 3.3 GEOGRAPHIC SNAPSHOT OF X-RAY DETECTORS MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing target population

- 4.2.1.2 Expanding applications of X-ray detectors

- 4.2.1.3 Investments to advance healthcare facilities and digital imaging technologies

- 4.2.1.4 Rising prevalence of animal diseases and growing number of veterinary practitioners

- 4.2.1.5 Growing demand for cosmetic dentistry

- 4.2.1.6 Integration of AI and advanced imaging software

- 4.2.2 RESTRAINTS

- 4.2.2.1 Stringent regulatory requirements

- 4.2.2.2 Health hazards of full-body scanning

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for portable and mobile imaging

- 4.2.3.2 Development of advanced detector materials

- 4.2.3.3 Technological advancements in detector technology

- 4.2.3.4 Growing adoption of digital radiography systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of skilled radiologists and technicians

- 4.2.4.2 Increasing adoption of refurbished X-ray units

- 4.2.4.3 Budget constraints in hospitals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER1/2/3 PLAYERS

- 4.5.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN X-RAY DETECTORS MARKET

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF BUYERS

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 THREAT OF NEW ENTRANTS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL DIAGNOSTIC IMAGING INDUSTRY

- 5.2.4 TRENDS IN GLOBAL X-RAY DETECTORS INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL (SUPPLIERS)

- 5.3.2 MANUFACTURING

- 5.3.3 SALES & DISTRIBUTION

- 5.3.4 END USERS

- 5.4 VALUE CHAIN ANALYSIS

- 5.4.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.4.2 RAW MATERIAL PROCUREMENT

- 5.4.3 MANUFACTURING

- 5.4.4 DISTRIBUTION

- 5.4.5 MARKETING & SALES

- 5.4.6 POST-SALES SERVICES

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE, BY KEY PLAYER

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.7 TRADE ANALYSIS

- 5.8 KEY CONFERENCES AND EVENTS (2026-2027)

- 5.9 TRENDS IMPACTING CUSTOMER BUSINESS

- 5.9.1 RISING ADOPTION OF PORTABLE AND WIRELESS IMAGING SOLUTIONS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFF

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 KEY TARIFF RATES

- 5.12.4 PRICE IMPACT ANALYSIS

- 5.12.5 IMPACT ON COUNTRY/REGION

- 5.12.5.1 US

- 5.12.5.2 Europe

- 5.12.5.3 Asia Pacific

- 5.12.6 IMPACT ON END USERS

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 INTRODUCTION

- 6.2 DECISION-MAKING PROCESS

- 6.3 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 6.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 6.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 6.6 REGULATORY ANALYSIS

- 6.6.1 KEY REGULATORY BODIES AND GOVERNMENT AGENCIES

- 6.6.1.1 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.6.1.2 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.6.1.3 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.6.1.4 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.6.1.5 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES AND OTHER ORGANIZATIONS

- 6.6.1 KEY REGULATORY BODIES AND GOVERNMENT AGENCIES

- 6.7 KEY REGULATORY GUIDELINES

- 6.7.1 US

- 6.7.2 CANADA

- 6.7.3 UK

- 6.7.4 FRANCE

- 6.7.5 CHINA

- 6.7.6 INDIA

- 6.7.7 BRAZIL

- 6.7.8 UAE

- 6.8 REIMBURSEMENT SCENARIO

- 6.8.1 INDUSTRY STANDARDS

7 X-RAY DETECTORS MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.2 FLAT PANEL DETECTORS

- 7.2.1 RAPID ADVANCEMENTS IN FLAT-PANEL DETECTORS FOR X-RAY IMAGING AND IMPACT ON MEDICAL APPLICATIONS - KEY DRIVERS

- 7.3 COMPUTED RADIOGRAPHY DETECTORS

- 7.3.1 ENHANCED IMAGING QUALITY, STREAMLINED CASSETTE HANDLING, AND OPTIMIZED IMAGING PLATE COSTS TO BOOST ADOPTION

- 7.4 LINE-SCAN DETECTORS

- 7.4.1 SURGING TECHNOLOGICAL PROGRESS FUELS DEMAND IN CT APPLICATIONS

- 7.5 CHARGE-COUPLED DEVICE DETECTORS

- 7.5.1 SEGMENT DRIVEN BY ABILITY TO DETECT VERY WEAK LIGHT SIGNALS

- 7.6 PHOTON COUNTING DETECTORS

- 7.6.1 COST EFFICIENCY AND RAPID PROCESSING TIMES TO DRIVE INCREASED DEMAND

8 X-RAY DETECTORS MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- 8.2 MEDICAL APPLICATIONS

- 8.2.1 STATIC IMAGING

- 8.2.1.1 Chest imaging

- 8.2.1.1.1 Growing incidence of target diseases to drive market

- 8.2.1.2 ORTHOPEDICS

- 8.2.1.2.1 Rising incidence of orthopedic disorders to support market growth

- 8.2.1.3 Mammography

- 8.2.1.3.1 Rising breast cancer caseload and advancements in imaging technology to propel market growth

- 8.2.1.4 Oncology

- 8.2.1.4.1 Need for early diagnosis and treatment to foster market growth

- 8.2.1.5 Other static imaging applications

- 8.2.1.1 Chest imaging

- 8.2.2 DYNAMIC IMAGING

- 8.2.2.1 FLUOROSCOPY

- 8.2.2.1.1 Technological advancements and growing healthcare awareness to drive market

- 8.2.2.2 SURGICAL IMAGING

- 8.2.2.2.1 Potential side effects of radiation exposure may affect end-user adoption

- 8.2.2.3 Cardiovascular imaging

- 8.2.2.3.1 Need for early detection and efficient management of CVD to drive market

- 8.2.2.4 SPINAL IMAGING

- 8.2.2.4.1 Advancements in DR technologies to support market growth

- 8.2.2.1 FLUOROSCOPY

- 8.2.1 STATIC IMAGING

- 8.3 DENTAL APPLICATIONS

- 8.3.1 GROWING OCCURRENCE OF DENTAL CARIES AND PERIODONTAL DISEASES TO DRIVE MARKET

- 8.4 SECURITY/DEFENSE APPLICATIONS

- 8.4.1 IMPLEMENTATION OF NEW SECURITY SYSTEMS TO DRIVE MARKET

- 8.4.2 HOMELAND SECURITY

- 8.4.2.1 Wide applications in homeland security to drive the market

- 8.4.3 PUBLIC & PRIVATE ENTERPRISES

- 8.4.3.1 Rising developments related to X-ray detectors to enhance security systems and propel growth

- 8.4.4 DEFENSE

- 8.4.4.1 Growing demand for advanced X-ray detectors in security and military applications to drive market

- 8.5 VETERINARY APPLICATIONS

- 8.5.1 GROWING AWARENESS OF ANIMAL HEALTH AND RISING PET ADOPTION TO DRIVE DEMAND FOR PET MEDICAL CARE AND FAVOR MARKET GROWTH

- 8.6 INDUSTRIAL APPLICATIONS

- 8.6.1 RISING USE IN AVIATION AND TRANSPORTATION TO PROPEL MARKET GROWTH

- 8.6.2 NON-DESTRUCTIVE TESTING

- 8.6.3 ELECTRONIC INSPECTION

- 8.7 OTHER APPLICATIONS

9 FLAT-PANEL DETECTORS MARKET

- 9.1 INTRODUCTION

- 9.2 FLAT-PANEL MARKET DETECTORS BY TYPE

- 9.2.1 CESIUM IODIDE FLAT-PANEL DETECTORS

- 9.2.1.1 Rising number of radiography exams and growing awareness to propel market growth

- 9.2.2 GADOLINIUM OXYSULFIDE

- 9.2.2.1 Affordability and technological advancements to support market growth

- 9.2.3 AMORPHOUS SILICON

- 9.2.3.1 Growing awareness of advantages and need for precision in diagnostics to drive demand

- 9.2.4 AMORPHOUS SELENIUM

- 9.2.4.1 High sensitivity, durability, and longer lifespan to drive adoption

- 9.2.5 CMOS

- 9.2.5.1 Superior image quality, speed, and efficiency to boost adoption

- 9.2.6 OTHER FLAT-PANEL DETECTORS

- 9.2.1 CESIUM IODIDE FLAT-PANEL DETECTORS

- 9.3 FLAT-PANEL DETECTORS MARKET, BY PANEL TYPE

- 9.3.1 LARGE-AREA FLAT-PANEL DETECTORS

- 9.3.1.1 Technological advancements to drive market

- 9.3.2 MEDIUM-AREA FLAT-PANEL DETECTORS

- 9.3.2.1 Growing use in medical and industrial applications to support demand growth

- 9.3.3 SMALL-AREA FLAT-PANEL DETECTORS

- 9.3.3.1 High demand in ENT imaging and digital mammography to drive market

- 9.3.1 LARGE-AREA FLAT-PANEL DETECTORS

- 9.4 FLAT-PANEL DETECTORS MARKET, PORTABILITY

- 9.4.1 PORTABLE FLAT-PANEL DETECTORS

- 9.4.1.1 Lower radiation dose requirements and ease of use to support adoption

- 9.4.2 FIXED FLAT-PANEL DETECTORS

- 9.4.2.1 Limited space requirements constrain use in large hospitals

- 9.4.1 PORTABLE FLAT-PANEL DETECTORS

- 9.5 FLAT-PANEL DETECTORS MARKET, BY PLATFORM

- 9.5.1 DIGITAL FLAT-PANEL DETECTORS

- 9.5.1.1 Rising demand for new and latest capabilities to drive demand

- 9.5.2 RETROFIT FLAT-PANEL DETECTORS

- 9.5.2.1 High-quality images and cost-effectiveness to drive market

- 9.5.1 DIGITAL FLAT-PANEL DETECTORS

10 X-RAY DETECTORS MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 US

- 10.2.1.1 Surge in aging population and need for early detection and treatment of ailments to boost market

- 10.2.2 CANADA

- 10.2.2.1 Improved medical imaging access and need to address breast cancer challenges to drive market

- 10.2.1 US

- 10.3 EUROPE

- 10.3.1 GERMANY

- 10.3.1.1 Industrial and automotive sectors - key growth drivers

- 10.3.2 FRANCE

- 10.3.2.1 Increase in healthcare expenditure leads to market growth

- 10.3.3 UK

- 10.3.3.1 Strategic investment and technological advancements in healthcare to propel growth

- 10.3.4 ITALY

- 10.3.4.1 Increasing emphasis on security anticipated to boost utilization of advanced X-ray systems

- 10.3.5 SPAIN

- 10.3.5.1 Focus on cancer screening, aging population, and digital health initiatives - key market drivers

- 10.3.6 REST OF EUROPE

- 10.3.1 GERMANY

- 10.4 ASIA PACIFIC

- 10.4.1 JAPAN

- 10.4.1.1 Integration of AI in digital imaging - pivotal driver for growth

- 10.4.2 CHINA

- 10.4.2.1 Healthcare expansion and adoption of digital technology leads to market growth

- 10.4.3 INDIA

- 10.4.3.1 Government initiatives in healthcare system to drive market growth

- 10.4.4 AUSTRALIA

- 10.4.4.1 Adoption of mobile X-ray systems supports market growth

- 10.4.5 SOUTH KOREA

- 10.4.5.1 Government-led AI and digital health initiatives fuel demand

- 10.4.6 REST OF ASIA PACIFIC

- 10.4.1 JAPAN

- 10.5 LATIN AMERICA

- 10.5.1 BRAZIL

- 10.5.1.1 Rising disease burden and evolving healthcare landscape drive market

- 10.5.2 MEXICO

- 10.5.2.1 Increasing number of hospitals contributes to expansion of market

- 10.5.3 REST OF LATIN AMERICA

- 10.5.1 BRAZIL

- 10.6 MIDDLE EAST & AFRICA

- 10.6.1 COLLABORATIVE EFFORTS OF PUBLIC AND PRIVATE SECTORS TO ENHANCE MARKET GROWTH

- 10.6.2 GCC COUNTRIES

- 10.6.2.1 Increase in healthcare initiatives and investments to drive market

- 10.6.3 REST OF MIDDLE EAST & AFRICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES

- 11.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN X-RAY DETECTORS MARKET

- 11.3 REVENUE ANALYSIS

- 11.4 MARKET SHARE ANALYSIS

- 11.4.1 GLOBAL X-RAY DETECTORS MARKET SHARE, BY KEY PLAYER, 2025

- 11.5 VALUATION AND FINANCIAL METRICS OF X-RAY DETECTORS VENDORS

- 11.6 BRAND/PRODUCT COMPARATIVE ANALYSIS

- 11.6.1 BRAND/PRODUCT COMPARATIVE ANALYSIS, BY MODEL

- 11.7 COMPANY EVALUATION MATRIX

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.8 START-UP/SME EVALUATION MATRIX

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.9 COMPETITIVE BENCHMARKING

- 11.9.1 FOOTPRINT ANALYSIS

- 11.9.1.1 Region footprint

- 11.9.1.2 Technology footprint

- 11.9.1.3 Flat-panel detector type footprint

- 11.9.1.4 Panel type footprint

- 11.9.1.5 Portability footprint

- 11.9.1.6 Platform footprint

- 11.9.1.7 Application footprint

- 11.9.1 FOOTPRINT ANALYSIS

- 11.10 COMPETITIVE BENCHMARKING OF STARTUP/SME PLAYERS

- 11.11 COMPETITIVE SCENARIO AND TRENDS

- 11.11.1 PRODUCT LAUNCHES & APPROVALS, JANUARY 2022-MARCH 2026

- 11.11.2 DEALS, JANUARY 2022-MARCH 2026

- 11.11.3 EXPANSIONS, JANUARY 2022-MARCH 2026

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- 12.1.1 VAREX IMAGING

- 12.1.1.1 Business overview

- 12.1.1.2 Products offered

- 12.1.1.3 Recent developments

- 12.1.1.3.1 Product launches

- 12.1.1.4 MnM view

- 12.1.1.4.1 Right to win

- 12.1.1.4.2 Strategic choices

- 12.1.1.4.3 Weaknesses and competitive threats

- 12.1.2 THALES

- 12.1.2.1 Business overview

- 12.1.2.2 Products offered

- 12.1.2.3 Recent developments

- 12.1.2.3.1 Product launches

- 12.1.2.3.2 Other Developments

- 12.1.2.4 MnM view

- 12.1.2.4.1 Right to win

- 12.1.2.4.2 Strategic choices

- 12.1.2.4.3 Weaknesses and competitive threats

- 12.1.3 CANON INC.

- 12.1.3.1 Business overview

- 12.1.3.2 Products offered

- 12.1.3.3 Recent developments

- 12.1.3.3.1 Product launches

- 12.1.3.3.2 Deals

- 12.1.3.4 MnM view

- 12.1.3.4.1 Key strengths

- 12.1.3.4.2 Strategic choices

- 12.1.3.4.3 Weaknesses and competitive threats

- 12.1.4 KONICA MINOLTA, INC.

- 12.1.4.1 Business overview

- 12.1.4.2 Products offered

- 12.1.4.3 Recent developments

- 12.1.4.3.1 Product launches

- 12.1.4.3.2 Deals

- 12.1.4.3.3 Expansions

- 12.1.5 AGFA-GEVAERT GROUP

- 12.1.5.1 Business overview

- 12.1.5.2 Products offered

- 12.1.5.3 Recent developments

- 12.1.5.3.1 Product launches

- 12.1.5.3.2 Deals

- 12.1.6 CARESTREAM HEALTH

- 12.1.6.1 Business overview

- 12.1.6.2 Products offered

- 12.1.6.3 Recent developments

- 12.1.6.3.1 Product launches/approvals

- 12.1.7 FUJIFILM HOLDINGS CORPORATION

- 12.1.7.1 Business overview

- 12.1.7.2 Products offered

- 12.1.7.3 Recent developments

- 12.1.7.3.1 Product launches

- 12.1.7.3.2 Deals

- 12.1.8 TELEDYNE TECHNOLOGIES INCORPORATED

- 12.1.8.1 Business overview

- 12.1.8.2 Products offered

- 12.1.8.3 Recent developments

- 12.1.8.3.1 Product launches

- 12.1.9 ANALOGIC CORPORATION

- 12.1.9.1 Business overview

- 12.1.9.2 Products offered

- 12.1.9.3 Recent developments

- 12.1.9.3.1 Deals

- 12.1.10 HAMAMATSU PHOTONICS KK.

- 12.1.10.1 Business overview

- 12.1.10.2 Products offered

- 12.1.10.3 Recent developments

- 12.1.10.3.1 Expansions

- 12.1.11 RAYENCE

- 12.1.11.1 Business overview

- 12.1.11.2 Products offered

- 12.1.12 DRTECH

- 12.1.12.1 Business overview

- 12.1.12.2 Products offered

- 12.1.13 DETECTION TECHNOLOGY PLC.

- 12.1.13.1 Business overview

- 12.1.13.2 Products offered

- 12.1.13.3 Recent developments

- 12.1.13.3.1 Product launches

- 12.1.13.3.2 Expansions

- 12.1.14 RIGAKU CORPORATION

- 12.1.14.1 Business overview

- 12.1.14.2 Products offered

- 12.1.14.3 Recent developments

- 12.1.14.3.1 Product launches

- 12.1.14.3.2 Deals

- 12.1.15 ACTEON

- 12.1.15.1 Business overview

- 12.1.15.2 Products offered

- 12.1.1 VAREX IMAGING

- 12.2 OTHER PLAYERS

- 12.2.1 ASTEL

- 12.2.2 NEW MEDICAL IMAGING CO., LTD.

- 12.2.3 MOXTEK, INC.

- 12.2.4 JPI HEALTHCARE SOLUTIONS

- 12.2.5 IBIS S.R.L.

- 12.2.6 VIEWORKS CO., LTD.

- 12.2.7 KA IMAGING

- 12.2.8 IRAY TECHNOLOGY

- 12.2.9 DECTRIS

- 12.2.10 PEXRAYTECH

13 RESEARCH METHODOLOGY

- 13.1 RESEARCH DATA

- 13.1.1 SECONDARY RESEARCH

- 13.1.1.1 Key data from secondary sources

- 13.1.2 PRIMARY RESEARCH

- 13.1.2.1 Primary sources

- 13.1.2.2 Key industry insights

- 13.1.1 SECONDARY RESEARCH

- 13.2 MARKET SIZE ESTIMATION

- 13.2.1 APPROACH 1: COMPANY REVENUE ESTIMATION APPROACH

- 13.2.2 APPROACH 2: CUSTOMER-BASED MARKET ESTIMATION

- 13.3 MARKET FORECASTING APPROACH

- 13.4 DATA VALIDATION APPROACH

- 13.5 MARKET SHARE ASSESSMENT

- 13.6 RESEARCH ASSUMPTIONS

- 13.7 RESEARCH LIMITATIONS

- 13.8 RISK ANALYSIS

- 13.8.1 X-RAY DETECTORS MARKET: RISK ANALYSIS

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS