|

시장보고서

상품코드

2033994

임상시험수탁기관(CRO) 서비스 시장 : 유형별, 제공 모델별, 모달리티별, 치료 분야별, 최종사용자별, 지역별 - 세계 예측(-2031년)Contract Research Organization (CRO) Services Market by Type (Early Phase, Clinical, Lab, Consulting), Therapeutic Area, Modality, Model (FSO, FSP), End User, Competition - Global Forecast to 2031 |

||||||

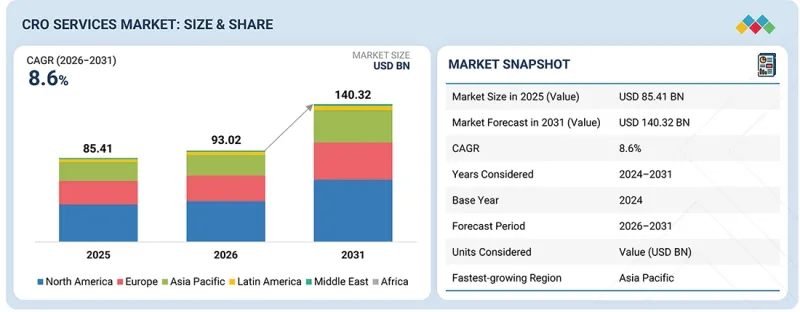

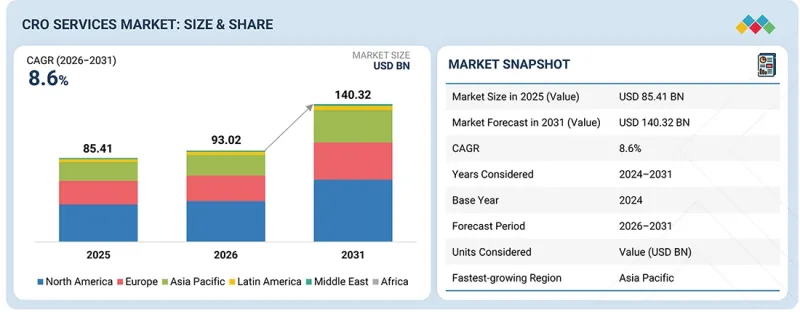

임상시험수탁기관(CRO) 서비스 시장 규모는 예측 기간 동안 CAGR 8.6%로 확대되어 2026년 930억 2,000만 달러에서 2031년에는 1,403억 2,000만 달러에 달할 것으로 전망됩니다.

시장 성장에 기여하는 주요 요인으로는 세포 및 유전자 치료제 파이프라인의 확대와 정밀의학에 대한 관심의 증가를 들 수 있습니다. 이러한 요인들로 인해 스폰서 기업들은 자체적으로 수행하기 어려운 복잡한 시험 설계, 유전체 스크리닝, 맞춤형 물류 및 필수적인 장기 추적 조사 능력을 갖춘 CRO 파트너를 찾을 것으로 예상됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 제공 모델별, 모달리티별, 치료 분야별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

정밀 프로그램은 환자 코호트를 세분화하고 피험자 등록 기간을 단축하기 위해 통합된 CRO-실험실 네트워크와 전 세계 시험기관 네트워크가 개발 일정과 데이터 품질 측면에서 결정적인 요소로 작용합니다. 규제 당국과 보험사가 강력한 실시간 증거를 요구하는 가운데, 스폰서들은 개발 리스크를 줄이기 위해 고급 실험실, 데이터 과학, RWE(Real World Data) 기능을 갖춘 임상 업무를 제공하는 CRO에 대한 의존도가 높아지고 있습니다.

서비스 유형별로는 초기 단계 개발 서비스 부문이 2025년 CRO 서비스 시장에서 두 번째로 큰 점유율을 차지했습니다.

서비스 유형별로 CRO 서비스 시장은 임상연구, 초기 단계 개발, 검사, 컨설팅, 데이터 관리 서비스 등으로 분류됩니다. 2025년 초기 개발 서비스 부문은 시장에서 두 번째로 큰 점유율을 차지했습니다. 현재 파이프라인은 특수 독성학, DMPK, 바이오 분석 및 안전성 약리학을 필요로 하는 신규 생물학적 제제, CGT 및 표적 치료제 개발에 중점을 두고 있으며, 많은 스폰서들이 IND(임상시험용 의약품) 단계에 더 빨리 도달하기 위해 이러한 업무를 아웃소싱하는 것을 선호하고 있습니다. 선호하고 있습니다.

최종사용자별로는 2025년 CRO 서비스 시장에서 제약 및 바이오제약 기업이 가장 큰 비중을 차지했습니다.

최종사용자별로 CRO 서비스 시장은 제약 및 바이오 제약 기업, 의료기기 기업, 학술 기관으로 분류됩니다. 2025년 제약 및 바이오 제약 기업 부문이 CRO 서비스 시장에서 가장 큰 점유율을 차지했습니다. 이 최종사용자 부문의 큰 점유율은 제약 및 생명공학 기업의 수많은 파이프라인 제품에 기인한다고 볼 수 있습니다. 또한, CRO는 속도, 규모, 유연한 비용 기반을 제공하여 최종사용자를 끌어들이고 있습니다.

지역별로는 2025년 북미가 가장 큰 시장 점유율을 차지했습니다.

2025년 북미는 세계 CRO 서비스 시장에서 가장 큰 점유율을 차지했습니다. 이는 기존 제약 및 생명공학 산업의 존재에 힘입은 바 크며, 이는 외부 위탁 연구개발 서비스에 대한 큰 수요를 창출하고 있습니다. 또한, 광범위한 임상시험 시설, 병원 및 전문 시설의 네트워크는 이 지역에서 대규모 임상시험을 수행하기에 이상적인 인프라를 제공합니다. 또한, 미국에서 디지털 헬스 솔루션과 분산형 임상시험 모델이 빠르게 확산되면서 CRO에 대한 수요가 증가하고 있으며, 스폰서들이 환자 모집과 유지를 개선할 수 있는 혁신적인 방법을 모색하면서 CRO에 대한 수요는 더욱 증가하고 있습니다.

본 보고서에서 다루고 있는 기업 프로파일 목록:

- IQVIA Inc. (미국) ICON plc (아일랜드) Thermo Fisher Scientific Inc. (미국) Laboratory Corporation of America Holdings (LabCorp) (미국) Fortrea, Inc. (미국) Syneos Health (미국) WuXi AppTec (중국) Charles River Laboratories (미국) PAREXEL International Corporation (미국) Pharmaron (중국) Medpace (미국) SGS SA (스위스), Frontage Labs (미국) Eurofins Scientific (룩셈부르크) BioAgile(인도) Firma Clinical Research(미국) Acculab Life Sciences(미국) Novotech(호주) KCR S.A.(미국) Linical(일본) Advanced Clinical(미국) Allucent(미국) Clinical Trial Service(네덜란드) Guires Inc. (Pepgra Healthcare Pvt. Ltd.)(영국) Worldwide Clinical Trials(미국) CTI Clinical Trial And Consulting(미국)

조사 범위

이 보고서는 CRO 서비스 시장을 유형별, 모달리티별, 제공 모델별, 최종사용자별, 지역별로 분류하고 있습니다. 이 보고서는 CRO 서비스 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약요인, 과제 및 기회 등)에 대한 자세한 정보를 다루고 있습니다. 주요 업계 플레이어에 대한 철저한 분석을 통해 각 회사의 사업 개요, 서비스, 주요 전략, 제휴, 파트너십 및 계약에 대한 인사이트를 제공합니다. 신제품 출시, 제휴, 파트너십 및 인수는 CRO 서비스 시장과 관련된 최근 동향입니다.

본 보고서 구매의 주요 이점

이 보고서는 CRO 서비스 시장 전체와 그 하위 부문의 수익에 대한 가장 정확한 추정치를 제공함으로써 시장 리더와 신규 진입자에게 도움을 줄 수 있습니다. 또한, 이해관계자들이 경쟁 상황을 더 깊이 이해하고, 비즈니스를 더 효과적으로 포지셔닝하고, 적절한 시장 진입 전략을 수립할 수 있는 인사이트를 얻을 수 있도록 돕습니다. 이 보고서를 통해 이해관계자들은 시장 동향을 파악하고 주요 시장 촉진요인, 기회 및 과제에 대한 정보를 얻을 수 있습니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 시장 성장에 영향을 미치는 주요 촉진요인(분산형 임상시험에 대한 관심 증가, 임상시험의 복잡성 및 수 증가, CRO가 제공하는 서비스의 유연성), 기회(환자층의 다양성에 대한 규제 당국의 관심), 과제(환자 유지에 대한 과제, 사이버 보안 및 지적재산권 관련 우려)에 대한 분석.

- 서비스 개발/혁신 : CRO 서비스 시장의 새로운 서비스에 대한 심층적인 인사이트

- 시장 개발 : 수익성 높은 시장에 대한 종합적인 정보 - 이 보고서는 다양한 지역의 시장을 분석합니다.

- 시장 다각화 : CRO 서비스 시장의 신규 서비스, 미개척 지역, 최근 동향 및 투자에 대한 종합적인 정보 제공

- 경쟁사 분석 : IQVIA Inc.(미국), ICON Plc(아일랜드), Medpace(미국), Laboratory Corporation of America Holdings(LabCorp)(미국), Thermo Fisher Scientific Inc.(미국), Fortrea, Inc.(미국)을 포함한 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가. CRO 서비스 시장의 주요 업체들을 상세히 분석했으며, 주요 업체들의 주요 전략, 서비스 출시, 인수, 인수합병, 제휴, 계약, 합작투자, 사업 확장, 기타 최근 동향, 투자 및 자금 조달 활동, 브랜드/서비스 비교 분석, 업체 평가 및 재무 지표에 대한 인사이트를 제공합니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 CRO 서비스 시장(유형별)

제10장 CRO 서비스 시장(제공 모델별)

제11장 CRO 서비스 시장(모달리티별)

제12장 CRO 서비스 시장(치료 분야별)

제13장 CRO 서비스 시장(최종사용자별)

제14장 CRO 서비스 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

KSM 26.05.27The contract research organization (CRO) services market is expected to reach USD 140.32 billion in 2031 from USD 93.02 billion in 2026, at a CAGR of 8.6% during the forecast period. The key factors contributing to market growth include the expanding pipeline of cell & gene therapies and the growing focus on precision medicine. These factors are expected to drive sponsors toward CRO partners that can handle complex designs, genomic screening, customizable logistics, and mandatory long-term follow-up capabilities that are challenging to implement in-house.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Type, Modality, Therapeutic Area, Delivery Model, and End User |

| Regions covered | North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa |

Precision programs fragment patient cohorts and shorten enrollment windows, making integrated CRO-lab networks and global site coverage decisive for timelines and data quality. As regulators and payers demand robust, real-time evidence, sponsors increasingly depend on CROs that offer clinical operations with advanced lab, data science, and RWE capabilities to de-risk development.

By service type, the early phase development services segment accounted for the second-largest share of the CRO services market in 2025.

Based on service type, the CRO services market is segmented into clinical research, early-phase development, laboratory, consulting, and data management services. In 2025, the early phase development services segment accounted for the second-largest share of the market. The current pipeline is focused on developing novel biologics, CGT, and targeted modalities that require specialized toxicology, DMPK, bioanalysis, and safety pharmacology, which several sponsors prefer to outsource to reach the IND (investigational new drug) stage faster.

By end user, the pharmaceutical & biopharmaceutical companies accounted for the largest share in the CRO services market in 2025.

Based on end user, the CRO services market is segmented into pharmaceutical & biopharmaceutical companies, medical device companies, and academic institutes. In 2025, the pharmaceutical & biopharmaceutical companies segment accounted for the largest share of the CRO services market. The large share of this end-user segment can be attributed to the large number of drug pipeline products of pharma and biotech companies. Moreover, CROs deliver speed, scale, and flexible cost bases, attracting end users.

By region, North America accounted for the largest share of the market in 2025.

In 2025, North America held the largest share of the global CRO services market, driven by the presence of well-established pharmaceutical and biotechnology industries, which drive significant demand for outsourced research and development services. Additionally, a vast network of clinical sites, hospitals, and specialized facilities provides an ideal infrastructure for conducting large-scale clinical trials in the region. Additionally, the rapid adoption of digital health solutions and decentralized trial models in the US, a significant contributor to the region's substantial share, is further boosting CRO demand, as sponsors seek innovative ways to improve patient recruitment and retention.

List of Companies Profiled in the Report:

- IQVIA Inc. (US)

- ICON plc (Ireland)

- Thermo Fisher Scientific Inc. (US)

- Laboratory Corporation of America Holdings (LabCorp) (US)

- Fortrea, Inc. (US)

- Syneos Health (US)

- WuXi AppTec (China)

- Charles River Laboratories (US)

- PAREXEL International Corporation (US)

- Pharmaron (China)

- Medpace (US)

- SGS SA (Switzerland), Frontage Labs (US)

- Eurofins Scientific (Luxembourg)

- BioAgile (India)

- Firma Clinical Research (US)

- Acculab Life Sciences (US)

- Novotech (Australia)

- KCR S.A. (US)

- Linical (Japan)

- Advanced Clinical (US)

- Allucent (US)

- Clinical Trial Service (Netherlands)

- Guires Inc. (Pepgra Healthcare Pvt. Ltd.) (UK)

- Worldwide Clinical Trials (US)

- CTI Clinical Trial And Consulting (US)

Research Coverage

This research report categorizes the CRO services market by type (clinical research services, early-phase development services, laboratory services, consulting services, and data management services), modality (small molecules, biologics, biosimilars, medical devices), delivery model (Full-service outsourcing (FSO) model, Functional service provider (FSP) model, Hybrid model), end user (pharmaceutical & biopharmaceutical companies, medical device companies, and academic institutes), and region (North America, Europe, the Asia Pacific, Latin America, the Middle East, and Africa). The report covers detailed information regarding the leading factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the CRO services market. A thorough analysis of the key industry players has provided insights into their business overview, services, key strategies, collaborations, partnerships, and agreements. New launches, collaborations, partnerships, and acquisitions are the recent developments associated with the CRO services market.

Key Benefits of Buying the Report

The report will help market leaders/new entrants by providing the closest approximations of the revenue numbers for the overall CRO services market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business more effectively and develop suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide information on key market drivers, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing focus on decentralized trials, rising complexity and volume of trials, service flexibility offered by CROs), opportunities (regulatory focus on patient pool diversity), and challenges (challenges of patient retention and cybersecurity/intellectual property concerns) influencing the growth of the market.

- Service Development/Innovation: Detailed insights on newly launched services of the CRO services market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the market across varied regions.

- Market Diversification: Exhaustive information about new services, untapped geographies, recent developments, and investments in the CRO services market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of key players, including IQVIA Inc. (US), ICON Plc (Ireland), Medpace (US), Laboratory Corporation of America Holdings (LabCorp) (US), Thermo Fisher Scientific Inc. (US), and Fortrea, Inc. (US). A detailed analysis of the key industry players has been conducted to provide insights into their key strategies, service launches, acquisitions, partnerships, agreements, collaborations, expansions, other recent developments, investment and funding activities, brand/service comparative analysis, and vendor valuation and financial metrics of the CRO services market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 GLOBAL CRO SERVICES MARKET SNAPSHOT

- 3.2 NORTH AMERICA: CRO SERVICES MARKET, BY MODALITY AND COUNTRY, 2024

- 3.3 CRO SERVICES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising trial volume and complexity

- 4.2.1.2 Growing focus on decentralized/patient-centric trials

- 4.2.1.3 Service flexibility offered by CROs

- 4.2.1.4 Technological integrations

- 4.2.1.5 Growing R&D investments and presence of a robust clinical pipeline

- 4.2.2 OPPORTUNITIES

- 4.2.2.1 Growing regulatory stringency on the diversity of the patient pool

- 4.2.2.2 Risk-based monitoring (RBM) and risk-based quality management as a service

- 4.2.2.3 Offering data analysis outcomes favoring clients' reimbursement and market access strategy

- 4.2.2.4 AI-powered clinical development and decentralized trial models

- 4.2.3 CHALLENGES

- 4.2.3.1 Patient retention

- 4.2.3.2 Cybersecurity or intellectual property challenges

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MARKET TRENDS

- 5.1.1 INTEGRATION OF HEOR AND RWE INTO CLINICAL TRIAL DESIGN

- 5.1.2 IN SILICO TRIALS

- 5.1.3 SPECIALIZED BIOANALYTICS FOR EMERGING MODALITIES (CGT)

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 BARGAINING POWER OF SUPPLIERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL CRO SERVICES MARKET

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING RANGE, BY SERVICE TYPE, 2025

- 5.6.2 INDICATIVE PRICING ANALYSIS, BY PHASE, 2025

- 5.6.3 INDICATIVE PRICING ANALYSIS, BY REGION, 2025

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 IMPACT OF 2025 US TARIFFS-CRO SERVICES MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 North America

- 5.10.4.1.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.4.1 North America

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.10.5.1 Pharmaceutical & biotech companies

- 5.10.5.2 Medical device companies

- 5.10.5.3 Academic institutes

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 AI-INTEGRATED CLINICAL TRIAL MANAGEMENT SYSTEM (CTMS) & ELECTRONIC TRIAL MASTER FILE (ETMF) PLATFORMS

- 6.1.2 RANDOMIZATION AND TRIAL SUPPLY MANAGEMENT (RTSM)

- 6.1.3 ELECTRONIC DATA CAPTURE (EDC) SYSTEM

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 DIGITAL BIOMARKERS, WEARABLES & ELECTRONIC PATIENT-REPORTED OUTCOME (EPRO) TOOLS

- 6.2.2 MODEL-INFORMED DRUG DEVELOPMENT (MIDD)

- 6.2.3 DATA MANAGEMENT AND INFORMATICS TECHNOLOGIES

- 6.2.4 REAL-WORLD EVIDENCE (RWE) & REAL-WORLD DATA (RWD) PLATFORMS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CLINICAL TRIAL SIMULATION TOOLS

- 6.4 TECHNOLOGY/SERVICE ROADMAP

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON CRO SERVICES MARKET

- 6.6.1 INTRODUCTION

- 6.6.2 MARKET POTENTIAL ACROSS DRUG DEVELOPMENT STAGES

- 6.6.3 AI USE CASES

- 6.6.4 FUTURE OF GENERATIVE AI IN DRUG DEVELOPMENT ECOSYSTEM

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Rest of the World

- 7.1.3 CERTIFICATIONS, LABELING, & ECO-STANDARDS

- 7.1.4 REGULATORY ANALYSIS

- 7.1.5 REGULATORY SCENARIO FOR DRUG APPROVALS AND CGMP PROCEDURES

- 7.2 SUSTAINABILITY INITIATIVES

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 CUSTOMER LANDSCAPE

- 8.3.1 BUDGET ALLOCATION TREND

- 8.3.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 CRO SERVICES MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 CLINICAL RESEARCH SERVICES

- 9.2.1 PHASE III

- 9.2.1.1 Large-scale testing ability to assess efficacy and safety of drugs to aid growth

- 9.2.2 PHASE II

- 9.2.2.1 Growing number of pipeline products in Phase II studies to drive market

- 9.2.3 PHASE I

- 9.2.3.1 Robust pipeline of pharmaceutical and biopharmaceutical products to support growth

- 9.2.4 PHASE IV

- 9.2.4.1 Stringent global regulations for drug safety monitoring to spur growth

- 9.2.1 PHASE III

- 9.3 EARLY-PHASE DEVELOPMENT SERVICES

- 9.3.1 CHEMISTRY, MANUFACTURING, AND CONTROLS SERVICES

- 9.3.1.1 Growing need to meet regulatory norms for drugs to fuel market

- 9.3.2 PRECLINICAL SERVICES

- 9.3.2.1 Pharmacokinetics/Pharmacodynamics

- 9.3.2.1.1 Rise in outsourcing services by pharmaceutical and biopharmaceutical companies to promote growth

- 9.3.2.2 Toxicology testing

- 9.3.2.2.1 Need to prevent late-stage failures to contribute to growth

- 9.3.2.3 Other preclinical services

- 9.3.2.1 Pharmacokinetics/Pharmacodynamics

- 9.3.3 DISCOVERY STUDIES

- 9.3.3.1 Increasing reliance on CRO services for target identification and validation to expedite growth

- 9.3.1 CHEMISTRY, MANUFACTURING, AND CONTROLS SERVICES

- 9.4 LABORATORY SERVICES

- 9.4.1 ANALYTICAL TESTING

- 9.4.1.1 Physical characterization

- 9.4.1.1.1 Ability to minimize product failure in late-phase development to favor growth

- 9.4.1.2 Raw material testing

- 9.4.1.2.1 Need to maintain quality of finished product to facilitate growth

- 9.4.1.3 Batch-release testing

- 9.4.1.3.1 Need to maintain batch-to-batch consistency of pharmaceutical dosage forms to advance growth

- 9.4.1.4 Stability testing

- 9.4.1.4.1 Ability to establish drug compatibility and formulation development to aid growth

- 9.4.1.5 Other analytical testing services

- 9.4.1.1 Physical characterization

- 9.4.2 BIOANALYTICAL TESTING

- 9.4.2.1 Increasing outsourcing of R&D activities to accelerate growth

- 9.4.1 ANALYTICAL TESTING

- 9.5 CONSULTING SERVICES

- 9.5.1 GROWING ADOPTION OF CONSULTING SERVICES FOR FASTER REGULATORY APPROVALS TO BOOST MARKET

- 9.6 DATA MANAGEMENT SERVICES

- 9.6.1 NEED TO TRACK PROGRESS OF EARLY DRUG DEVELOPMENT TO AUGMENT GROWTH

10 CRO SERVICES MARKET, BY DELIVERY MODEL

- 10.1 INTRODUCTION

- 10.2 FULL-SERVICE OUTSOURCING (FSO) MODEL

- 10.2.1 RISE IN NUMBER OF EMERGING BIOPHARMACEUTICAL COMPANIES TO DRIVE MARKET

- 10.3 FUNCTIONAL SERVICE PROVIDER (FSP) MODEL

- 10.3.1 GROWING ADOPTION OF FSP SERVICES BY LARGE PHARMACEUTICAL COMPANIES TO FUEL MARKET GROWTH

- 10.4 HYBRID MODEL

- 10.4.1 HIGH FLEXIBILITY OFFERED BY HYBRID MODEL TO SUPPORT MARKET GROWTH

11 CRO SERVICES MARKET, BY MODALITY

- 11.1 INTRODUCTION

- 11.2 SMALL MOLECULES

- 11.2.1 ONGOING SURGE IN PHARMACEUTICAL R&D INVESTMENTS TO SUPPORT GROWTH

- 11.3 BIOLOGICS

- 11.3.1 MONOCLONAL ANTIBODIES

- 11.3.1.1 Surging demand for targeted therapies across oncology, autoimmune disorders, and infectious diseases to drive market

- 11.3.2 CELL & GENE THERAPY

- 11.3.2.1 Robust pipeline and R&D initiatives to drive market

- 11.3.3 OTHER BIOLOGICS

- 11.3.1 MONOCLONAL ANTIBODIES

- 11.4 MEDICAL DEVICES

- 11.4.1 RAPID INNOVATIONS IN DIAGNOSTICS, IMPLANTABLES, AND DIGITAL HEALTH TECHNOLOGIES TO FOSTER GROWTH

- 11.5 BIOSIMILARS

- 11.5.1 MONOCLONAL ANTIBODY BIOSIMILARS

- 11.5.1.1 Rising demand for affordable therapeutic options to support growth

- 11.5.2 INSULIN

- 11.5.2.1 Increasing patent expirations to contribute to growth

- 11.5.3 COLONY-STIMULATING FACTORS

- 11.5.3.1 Increasing use of colony-stimulating factor during post-chemotherapy to aid growth

- 11.5.4 ERYTHROPOIETIN

- 11.5.4.1 Essential role of erythropoietin in treating anemia to stimulate growth

- 11.5.5 OTHER BIOSIMILARS

- 11.5.1 MONOCLONAL ANTIBODY BIOSIMILARS

12 CRO SERVICES MARKET, BY THERAPEUTIC AREA

- 12.1 INTRODUCTION

- 12.2 ONCOLOGY

- 12.2.1 GROWING INCIDENCE OF CANCER TO DRIVE MARKET

- 12.2.2 BREAST CANCER

- 12.2.2.1 Increasing cases and high spending on treating breast cancer to support growth

- 12.2.3 LUNG CANCER

- 12.2.3.1 Increasing focus on developing drugs against lung cancer to foster growth

- 12.2.4 COLORECTAL CANCER

- 12.2.4.1 Increasing drug discovery and development efforts against colorectal cancer to aid growth

- 12.2.5 PROSTATE CANCER

- 12.2.5.1 Growing clinical pipeline to propel market

- 12.2.6 OTHER CANCERS

- 12.3 INFECTIOUS DISEASES

- 12.3.1 INCREASING INCIDENCE OF CHRONIC INFECTIONS TO SUPPORT GROWTH

- 12.4 CARDIOVASCULAR SYSTEM DISORDERS

- 12.4.1 HIGH MORTALITY RATES OF CARDIOVASCULAR DISEASES TO FUEL MARKET

- 12.5 NEUROLOGY

- 12.5.1 GROWING INVESTMENTS IN NEUROLOGICAL DISORDER RESEARCH TO DRIVE MARKET

- 12.6 VACCINES

- 12.6.1 INCREASING FOCUS ON VACCINE DEVELOPMENT TO SPUR GROWTH

- 12.7 METABOLIC DISORDERS/ENDOCRINOLOGY

- 12.7.1 INCREASING GLOBAL DIABETES AND OBESITY POPULATION TO PROMOTE GROWTH

- 12.8 IMMUNOLOGICAL DISORDERS

- 12.8.1 GROWING CLINICAL RESEARCH FOR IMMUNOLOGICAL DISORDERS TO BOOST MARKET

- 12.9 PSYCHIATRY

- 12.9.1 RISING CASES OF PSYCHIATRIC DISORDERS AND DEPRESSION TO SUSTAIN GROWTH

- 12.10 RESPIRATORY DISORDERS

- 12.10.1 RISING INCIDENCE OF CHRONIC RESPIRATORY DISEASE TO FOSTER GROWTH

- 12.11 DERMATOLOGY

- 12.11.1 GROWING FOCUS ON DRUG DEVELOPMENT AGAINST VARIOUS SKIN CONDITIONS TO DRIVE MARKET

- 12.12 OPHTHALMOLOGY

- 12.12.1 GROWTH IN NUMBER OF OPHTHALMOLOGY PIPELINE DRUGS TO SUPPORT SEGMENT GROWTH

- 12.13 GASTROINTESTINAL DISEASES

- 12.13.1 RAPID LIFESTYLE AND DIETARY CHANGES TO AMPLIFY GROWTH

- 12.14 GENITOURINARY & WOMEN'S HEALTH

- 12.14.1 RISING AWARENESS ABOUT EARLY DISEASE DIAGNOSIS AND TREATMENT TO BOLSTER MARKET

- 12.15 HEMATOLOGY

- 12.15.1 INCREASING DRUG APPROVALS FOR DRUGS AGAINST NON-MALIGNANT HEMATOLOGICAL CONDITIONS TO SUPPORT GROWTH

- 12.16 OTHER THERAPEUTIC AREAS

13 CRO SERVICES MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 13.2.1 INCREASING OUTSOURCING AND PARTNERSHIPS TO ACCELERATE GROWTH

- 13.2.2 LARGE PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 13.2.2.1 Demand for therapeutic expertise and global reach to aid outsourcing to CROs

- 13.2.3 SMALL & MID-SIZE PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 13.2.3.1 Demand is driven by need to control fixed costs, access global development expertise, and accelerate timelines

- 13.3 MEDICAL DEVICE COMPANIES

- 13.3.1 INCREASING GROWTH INITIATIVES BY MEDTECH CROS TO DRIVE MARKET

- 13.4 ACADEMIC INSTITUTES

- 13.4.1 CONSISTENT COLLABORATIONS BETWEEN CROS AND ACADEMIA TO INTENSIFY GROWTH

14 CRO SERVICES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Increasing incidence of oncology indications to accelerate growth

- 14.2.2 CANADA

- 14.2.2.1 Favorable government initiatives and high investments to support growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Presence of strong pharmaceutical and biotechnology R&D infrastructure to spur growth

- 14.3.2 UK

- 14.3.2.1 Rising pharmaceutical R&D expenditure to expedite growth

- 14.3.3 FRANCE

- 14.3.3.1 Increasing technological advancements and faster drug discovery and development initiatives to aid growth

- 14.3.4 ITALY

- 14.3.4.1 Short timeline for drug approvals to encourage growth

- 14.3.5 SPAIN

- 14.3.5.1 Growing investment in pharmaceutical industry to boost market

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Continued efforts on improving the level of drug safety and supply to spur growth

- 14.4.2 INDIA

- 14.4.2.1 Large pool of patients and presence of highly skilled medical professionals to augment growth

- 14.4.3 JAPAN

- 14.4.3.1 Growing drug development activity to propel market

- 14.4.4 AUSTRALIA

- 14.4.4.1 Growing focus on funding opportunities to propel market

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Emerging clinical research hub to sustain growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Growing focus on enhancing pharmaceutical research and production to fuel market

- 14.5.2 MEXICO

- 14.5.2.1 Increasing investments in pharma R&D to promote growth

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.6.1.1 Kingdom of Saudi Arabia (KSA)

- 14.6.1.1.1 Expanding clinical trials ecosystem to contribute to growth

- 14.6.1.2 United Arab Emirates (UAE)

- 14.6.1.2.1 Growing clinical trials activity to drive market

- 14.6.1.3 Rest of GCC Countries

- 14.6.1.1 Kingdom of Saudi Arabia (KSA)

- 14.6.2 REST OF MIDDLE EAST

- 14.6.1 GCC COUNTRIES

- 14.7 AFRICA

- 14.7.1 BOOMING PHARMACEUTICAL INDUSTRY TO FACILITATE GROWTH

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN CRO SERVICES MARKET, JANUARY 2023-MARCH 2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Type footprint

- 15.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 RESPONSIVE COMPANIES

- 15.6.3 DYNAMIC COMPANIES

- 15.6.4 STARTING BLOCKS

- 15.6.5 COMPETITIVE BENCHMARKING

- 15.6.5.1 Detailed list of key startups/SMEs

- 15.6.5.2 Competitive benchmarking of startups/SMEs

- 15.7 COMPANY VALUATION & FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 SERVICE COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 SERVICE LAUNCHES & APPROVALS

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 IQVIA INC.

- 16.1.1.1 Business overview

- 16.1.1.2 Services/Solutions offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product & service launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/Right to win

- 16.1.1.4.2 Strategic choices made

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 ICON PLC

- 16.1.2.1 Business overview

- 16.1.2.2 Services/Solutions offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Service launches

- 16.1.2.3.2 Deals

- 16.1.2.3.3 Expansions

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/Right to win

- 16.1.2.4.2 Strategic choices made

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 THERMO FISHER SCIENTIFIC INC.

- 16.1.3.1 Business overview

- 16.1.3.2 Services/Solutions offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Service launches

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/Right to win

- 16.1.3.4.2 Strategic choices made

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 LABORATORY CORPORATION OF AMERICA HOLDINGS

- 16.1.4.1 Business overview

- 16.1.4.2 Services/Solutions offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Service launches

- 16.1.4.3.2 Deals

- 16.1.4.3.3 Expansions

- 16.1.4.3.4 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/Right to win

- 16.1.4.4.2 Strategic choices made

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 FORTREA, INC.

- 16.1.5.1 Company overview

- 16.1.5.2 Services/Solutions offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Service launches

- 16.1.5.3.2 Deals

- 16.1.5.3.3 Expansions

- 16.1.5.3.4 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/Right to win

- 16.1.5.4.2 Strategic choices made

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 SYNEOS HEALTH

- 16.1.6.1 Business overview

- 16.1.6.2 Services/Solutions offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Service launches

- 16.1.6.3.2 Deals

- 16.1.7 WUXI APPTEC

- 16.1.7.1 Business overview

- 16.1.7.2 Services/Solutions offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Expansions

- 16.1.7.3.2 Other developments

- 16.1.8 CHARLES RIVER LABORATORIES

- 16.1.8.1 Business overview

- 16.1.8.2 Services/Solutions offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Deals

- 16.1.9 PAREXEL INTERNATIONAL CORPORATION

- 16.1.9.1 Business overview

- 16.1.9.2 Services/Solutions offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Deals

- 16.1.9.3.2 Expansions

- 16.1.10 PHARMARON

- 16.1.10.1 Business overview

- 16.1.10.2 Services/Solutions offered

- 16.1.11 MEDPACE

- 16.1.11.1 Business overview

- 16.1.11.2 Services/Solutions offered

- 16.1.12 SGS SA

- 16.1.12.1 Business overview

- 16.1.12.2 Services/Solutions offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.13 FRONTAGE LABS

- 16.1.13.1 Business overview

- 16.1.13.2 Services/Solutions offered

- 16.1.13.3 Recent developments

- 16.1.13.3.1 Deals

- 16.1.13.3.2 Other developments

- 16.1.14 EUROFINS SCIENTIFIC

- 16.1.14.1 Business overview

- 16.1.14.2 Services/Solutions offered

- 16.1.15 TIGERMED

- 16.1.15.1 Business overview

- 16.1.15.2 Services offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Product/Service approvals

- 16.1.15.3.2 Deals

- 16.1.16 PSI CRO AG

- 16.1.16.1 Business overview

- 16.1.16.2 Services/Solutions offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Service launches

- 16.1.16.3.2 Deals

- 16.1.16.3.3 Expansions

- 16.1.17 BIOAGILE

- 16.1.17.1 Business overview

- 16.1.17.2 Services/Solutions offered

- 16.1.18 FIRMA CLINICAL RESEARCH

- 16.1.18.1 Business overview

- 16.1.18.2 Services/Solutions offered

- 16.1.19 ACCULAB LIFE SCIENCES

- 16.1.19.1 Business overview

- 16.1.19.2 Services/Solutions offered

- 16.1.20 NOVOTECH

- 16.1.20.1 Business overview

- 16.1.20.2 Services/Solutions offered

- 16.1.20.3 Recent developments

- 16.1.20.3.1 Deals

- 16.1.21 LINICAL

- 16.1.21.1 Business overview

- 16.1.21.2 Services/Solutions offered

- 16.1.21.3 Recent developments

- 16.1.21.3.1 Expansions

- 16.1.22 ADVANCED CLINICAL

- 16.1.22.1 Business overview

- 16.1.22.2 Services/Solutions offered

- 16.1.22.3 Recent developments

- 16.1.22.3.1 Deals

- 16.1.1 IQVIA INC.

- 16.2 OTHER PLAYERS

- 16.2.1 ALLUCENT

- 16.2.2 EMVENIO

- 16.2.3 GUIRES INC. (PEPGRA HEALTHCARE PVT. LTD.)

- 16.2.4 WORLDWIDE CLINICAL TRIALS

- 16.2.5 CTI CLINICAL TRIAL & CONSULTING

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH APPROACH

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key sources of secondary data

- 17.1.1.2 Key objectives of secondary research

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakdown of primaries

- 17.1.2.2 Key objectives of primary research

- 17.1.1 SECONDARY DATA

- 17.2 MARKET ESTIMATION METHODOLOGY

- 17.2.1 COMPANY REVENUE ANALYSIS (BOTTOM-UP APPROACH)

- 17.2.2 MNM REPOSITORY ANALYSIS AND PRIMARY RESEARCH

- 17.2.3 SEGMENTAL MARKET ASSESSMENT (TOP-DOWN APPROACH)

- 17.3 GROWTH RATE PROJECTIONS

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS