|

시장보고서

상품코드

2033995

EMI 차폐 시장 : 재료별, 방법별, 주파수별, 유형별 - 세계 예측(-2032년)EMI Shielding Market by Material, Method, Frequency, Type - Global Forecast to 2032 |

||||||

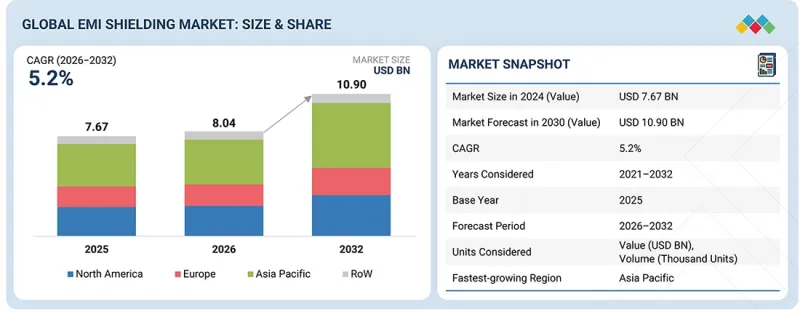

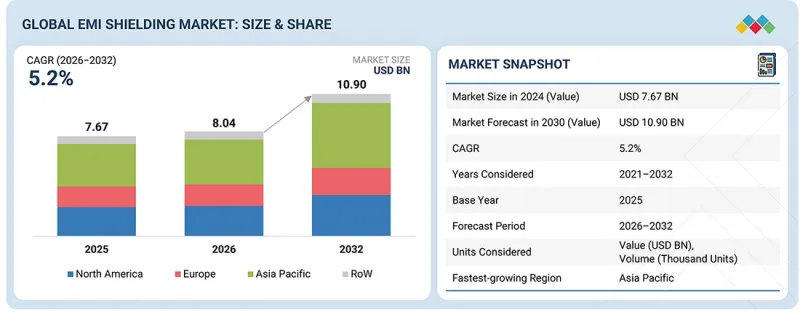

세계의 EMI 차폐 시장 규모는 2026년 80억 4,000만 달러에서 2032년까지 109억 달러에 달할 것으로 예측되며, CAGR로 5.2%의 성장이 전망됩니다.

현대의 시스템은 더 높은 주파수에서 작동하고 전자기 환경의 혼잡도도 증가함에 따라 무선 통신 기술의 급속한 보급에 따라 EMI 차폐에 대한 수요가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 10억 달러 |

| 부문 | 재료, 주파수, 유형, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

5G 기술의 확대와 더불어 Wi-Fi, 블루투스, IoT 기기의 보급으로 인해 신호 밀도가 크게 증가하여 부품 및 장치 간 전자기 간섭의 위험이 증가하고 있습니다. 이 간섭은 신호 품질 저하, 데이터 전송 효율 저하, 심지어 장치의 오작동을 유발할 수 있습니다. 그 결과, 제조업체들은 특히 소형 및 고속 전자 시스템에서 신호 무결성을 보장하고, 성능의 신뢰성을 유지하며, 엄격한 전자기 호환성(EMC) 규제를 충족하기 위해 첨단 EMI 차폐 솔루션을 도입하고 있습니다.

"방법론별로는 전도성 방식이 예측 기간 동안 가장 높은 CAGR을 기록할 것으로 예상됩니다."

방식별로는 직접 전기 경로를 통한 전자기 간섭의 효율적인 소산에 대한 요구가 증가함에 따라 EMI 차폐 시장의 전도성 방식 부문이 가장 빠르게 성장할 것으로 예상됩니다. 전도성 방식에 의한 차폐는 금속, 코팅, 개스킷과 같은 전도성 물질을 통해 불필요한 전자기에너지를 섬세한 부품으로부터 멀리 떨어뜨림으로써 작동하기 때문에 소형, 고밀도 전자 시스템에서 매우 효과적입니다. 5G 기술, EV용 전자기기, 첨단 PCB에 의한 고속 응용이 증가함에 따라 발생원에서의 간섭 관리가 매우 중요해지고 있습니다. 또한, 전도성 방식은 신뢰성, 비용 효율성, 최신 디바이스 아키텍처에 쉽게 통합할 수 있는 장점이 있어 소비자 가전, 자동차, 산업용 애플리케이션에 대한 채택이 더욱 가속화되고 있습니다.

"용도별로는 PCB 레벨의 차폐가 예측 기간 동안 EMI 차폐 시장을 지배할 것으로 예상됩니다."

전자기기의 소형화 및 복잡성 증가, 간섭을 발생원에서 직접 제어할 필요성이 높아짐에 따라 예측 기간 동안 PCB 레벨의 차폐가 시장을 지배할 것으로 예상됩니다. PCB에 컴포넌트가 밀집되어 구현됨에 따라 칩과 회로 간 전자기 간섭의 위험이 크게 증가하여 시스템 수준의 접근 방식보다 국부적 차폐가 더 효과적일 수 있습니다. 차폐 캔, 전도성 코팅, 접지면과 같은 PCB 차폐 솔루션은 기판의 특정 영역 내에서 노이즈를 봉쇄하고 격리하여 신호의 무결성과 안정적인 성능을 보장합니다. 5G 네트워크, IoT 기기, 첨단 자동차 전장품의 고속 애플리케이션이 확대됨에 따라 PCB 레벨의 차폐는 컴팩트하고 비용 효율적이며 확장 가능한 솔루션을 제공하여 업계 전반의 채택을 주도하고 있습니다.

"중국이 2025년 아시아태평양 EMI 차폐 시장에서 가장 큰 점유율을 차지했습니다."

중국은 전자기기 제조, 반도체 생산, 통신 인프라 개발에서 압도적인 우위를 바탕으로 아시아태평양의 EMI 차폐 시장에서 가장 큰 점유율을 차지했습니다. 중국은 효과적인 EMI 차폐 솔루션을 필요로 하는 스마트폰, 노트북, 네트워크 장비의 대규모 생산으로 소비자 전자제품의 세계 허브 역할을 하고 있습니다. 또한, 중국 내 5G 기술의 급속한 보급과 전기자동차 생태계의 성장은 첨단 차폐 재료에 대한 수요를 더욱 촉진하고 있습니다. 정부의 지원, 탄탄한 공급망, 주요 OEM 및 부품 제조업체의 존재로 인해 중국의 시장 입지가 강화되고 있으며, 중국은 이 지역에서 리더십을 유지하고 있습니다.

세계의 EMI 차폐 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 최신 EMI 차폐 기술과 유효성 시험

제10장 EMI 차폐 형성

제11장 EMI 차폐 시장 : 유형별

제12장 EMI 차폐 시장 : 재료별

제13장 EMI 차폐 시장 : 방법별

제14장 EMI 차폐 시장 : 주파수별

제15장 EMI 차폐 시장 : 용도별

제16장 EMI 차폐 시장 : 업계별

제17장 EMI 차폐 시장 : 지역별

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

KSM 26.05.27The global EMI shielding market is projected to grow from USD 8.04 billion in 2026 to USD 10.90 billion by 2032, registering a CAGR of 5.2%. The demand for EMI shielding is increasing with the rapid proliferation of wireless communication technologies because modern systems operate at higher frequencies and in increasingly crowded electromagnetic environments.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Material, Frequency, Type and Region |

| Regions covered | North America, Europe, APAC, RoW |

The expansion of 5G technology, along with Wi-Fi, Bluetooth, and IoT devices, has significantly increased signal density, leading to greater risks of electromagnetic interference between components and devices. This interference can degrade signal quality, reduce data transmission efficiency, and cause device malfunction. As a result, manufacturers are integrating advanced EMI shielding solutions to ensure signal integrity, maintain performance reliability, and meet stringent electromagnetic compatibility (EMC) regulations, especially in compact and high-speed electronic systems.

"Conduction, by method, is expected to record the highest CAGR during the forecast period."

The conduction segment in the EMI shielding market, by method, is likely to be the fastest-growing segment due to the increasing need for efficient dissipation of electromagnetic interference through direct electrical pathways. Conduction-based shielding works by transferring unwanted electromagnetic energy away from sensitive components through conductive materials such as metals, coatings, and gaskets, making it highly effective for compact, high-density electronic systems. With the rise of high-speed applications driven by 5G technology, EV electronics, and advanced PCBs, managing interference at the source has become critical. Additionally, conduction methods offer better reliability, cost efficiency, and ease of integration into modern device architectures, further accelerating their adoption across consumer electronics, automotive, and industrial applications.

"PCB-level shielding is expected to dominate the EMI shielding market, by application, throughout the forecast period"

PCB-level shielding is expected to dominate the market throughout the forecast period due to the increasing miniaturization and complexity of electronic devices, where interference needs to be controlled directly at the source. As components are densely packed onto printed circuit boards, the risk of electromagnetic interference between chips and circuits rises significantly, making localized shielding more effective than system-level approaches. PCB shielding solutions, such as shielding cans, conductive coatings, and ground planes, help contain and isolate noise within specific sections of the board, ensuring signal integrity and reliable performance. With the expansion of high-speed applications driven by 5G networks, IoT devices, and advanced automotive electronics, PCB-level shielding offers a compact, cost-efficient, and scalable solution, leading to its dominant adoption across industries.

"China secured the largest share of the Asia Pacific EMI shielding market in 2025."

China secured the largest share of the Asia Pacific EMI shielding market due to its strong dominance in electronics manufacturing, semiconductor production, and telecom infrastructure development. The country serves as a global hub for consumer electronics, with large-scale production of smartphones, laptops, and networking equipment that require effective EMI shielding solutions. Additionally, China's rapid deployment of 5G technology and the growth of its electric vehicle ecosystem further drive demand for advanced shielding materials. Government support, robust supply chains, and the presence of major OEMs and component manufacturers strengthen its market position, enabling China to maintain leadership in the region.

- By Company Type: Tier 1 - 30%, Tier 2 - 50%, and Tier 3 - 20%

- By Designation: Directors - 40%, C-level Executives - 30%, and Others - 30%

- By Region: North America - 22%, Europe - 22%, Asia Pacific - 45%, and RoW - 11%

Prominent players profiled in this report include PARKER HANNIFIN CORP (US), PPG Industries, Inc. (US), 3M (US), Hankel AG & CO KGAA (Germany), Qnity Electronics Inc (US), Leader Tech Inc (US), MG Chemicals (Canada), Nolato AB (Sweden), Tech Etch Inc (US), and RTP Company (US).

Research Coverage:

The report defines, describes, and forecasts the EMI shielding market based on type (narrowband EMI, broadband EMI), method (radiation, conduction), material (conductive coatings & paints (silver-based conductive coatings, copper-based conductive coatings, nickel-based conductive coatings, carbon-based conductive coatings (printed carbon ink, graphene-based conductive coatings)), conductive polymers (conductive elastomers (silicone and fluorosilicone, Ethylene Propylene Diene Monomer (EPDM)), conductive plastics)), metal shielding, EMI/EMC filters (EMI/EMC filters, by load type (AC filters (single-phase, three-phase), DC filters)), EMI/EMC filters (by insertion loss (differential mode, common mode), and EMI shielding tapes & laminates), frequency (low-frequency Shielding (below 100 MHz), high-frequency shielding (100 MHz-1 GHz)), application (PCB-level shielding, cable shielding, enclosure shielding, connector shielding, antenna shielding), industry (consumer electronics, telecommunications, automotive, healthcare, aerospace, energy & power, industrial, transportation), and region (North America, Europe, Asia Pacific, and RoW). It provides detailed information regarding drivers, restraints, opportunities, and challenges influencing the market's growth. It also analyzes competitive developments, including acquisitions, product launches, expansions, and actions taken by key players to grow in the market.

Reasons to Buy This Report:

The report will help market leaders/new entrants with information on the closest approximations of the revenue for the overall EMI shielding market and its subsegments. The report will help stakeholders understand the competitive landscape and gain more insight to position their business better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market's pulse and provides information on key drivers, restraints, opportunities, and challenges.

The report will provide insights into the following points:

- Analysis of Key Drivers (Rising demand for high-speed and high-frequency devices, Enforcement of stringent regulations to prevent electronic equipment malfunctions), restraints (Environmental hazards and high costs of EMI shielding metals, Low effectiveness of traditional EMI shielding materials), opportunities (Growing adoption of digital healthcare solutions, Rising consumer awareness of effects of EMI shielding), and challenges (Reducing electromagnetic interference in miniaturized devices, Thermal management trade-offs) of the EMI shielding market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the EMI shielding market

- Market Development: Comprehensive information about lucrative markets (The report analyzes the EMI shielding market across various regions.)

- Market Diversification: Exhaustive information about new products launched, untapped geographies, recent developments, and investments in the EMI shielding market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and offerings of leading players, including PARKER HANNIFIN CORP (US), PPG Industries, Inc. (US), 3M (US), Hankel AG & CO KGAA (Germany), Qnity Electronics Inc (US), in the EMI shielding market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN EMI SHIELDING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS OPERATING IN EMI SHIELDING MARKET

- 3.2 EMI SHIELDING MARKET, BY TYPE

- 3.3 EMI SHIELDING MARKET SHARE, BY MATERIAL

- 3.4 EMI SHIELDING MARKET IN NORTH AMERICA, BY INDUSTRY AND COUNTRY

- 3.5 EMI SHIELDING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing electronic content in devices

- 4.2.1.2 Stringent regulatory standards for electromagnetic compatibility across industries

- 4.2.1.3 Rising demand for high-speed and high-frequency devices

- 4.2.1.4 Increasing proliferation of wireless communication technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 High material and manufacturing cost

- 4.2.2.2 Design complexity in compact electronic devices

- 4.2.2.3 Environmental hazards and high costs of EMI shielding metals

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growth of EVs, 5G infrastructure, and high-frequency electronics

- 4.2.3.2 Development of lightweight and flexible shielding materials

- 4.2.3.3 Growing adoption of digital healthcare solutions

- 4.2.3.4 Rising consumer awareness of effects of EMI shielding

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing shielding effectiveness with thermal management

- 4.2.4.2 High complexity in reducing electromagnetic interference in miniaturized devices

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 BARGAINING POWER OF SUPPLIERS

- 5.2.2 BARGAINING POWER OF BUYERS

- 5.2.3 THREAT OF NEW ENTRANTS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL CONSUMER ELECTRONICS INDUSTRY

- 5.3.4 TRENDS IN GLOBAL TELECOMMUNICATIONS INDUSTRY

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING OF KEY PLAYERS, BY MATERIAL, 2025

- 5.6.2 INDICATIVE PRICING OF CONDUCTIVE COATINGS & PAINTS, BY TYPE, 2025

- 5.6.3 AVERAGE SELLING PRICE TREND OF EMI SHIELDING, BY MATERIAL, 2021-2025

- 5.6.4 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (852859)

- 5.7.2 EXPORT SCENARIO (852859)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 MILITARY GROUND RADAR SYSTEM RECEIVES CUSTOM DUAL-FUNCTION EMI VENT

- 5.11.2 AUTOMOTIVE TIER-1 RESOLVES EMI AND THERMAL CHALLENGES IN COMPACT INFOTAINMENT CONTROLLER

- 5.11.3 MOUNT SINAI HOSPITAL ELIMINATES SUBWAY-INDUCED MRI INTERFERENCE USING ACTIVE MAGNETIC COMPENSATION

- 5.11.4 AUTOMOTIVE OEMS ACHIEVE DUAL EMI AND THERMAL PROTECTION IN ADAS MODULES WITH SINGLE SILICONE-FREE GAP PAD

- 5.11.5 GPU MANUFACTURER ELIMINATES BOARD-LEVEL EMI IN COMPACT SEMICONDUCTOR DESIGN WITH ULTRA-THIN FERRITE SHEETS

- 5.12 IMPACT OF 2025 US TARIFF - EMI SHIELDING MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ELECTROMAGNETIC REFLECTION

- 6.1.2 MULTIPLE REFLECTION ATTENUATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GROUNDING AND BONDING ENGINEERING

- 6.2.2 SIGNAL INTEGRITY ENGINEERING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 DIFFERENTIAL SIGNALING TECHNOLOGY

- 6.3.2 ELECTROSTATIC DISCHARGE (ESD) CONTROL TECHNOLOGY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 IMPACT OF AI/GEN AI ON EMI SHIELDING MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES FOLLOWED BY OEMS IN EMI SHIELDING MARKET

- 6.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN EMI SHIELDING MARKET

- 6.6.4 INTERCONNECTED/ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED EMI SHIELDING

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1.1 Industry standards

- 7.1.1.2 Regulations

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS INDUSTRIES

9 LATEST EMI SHIELDING TECHNOLOGIES AND EFFECTIVENESS TESTS

- 9.1 LATEST EMI SHIELDING TECHNOLOGIES

- 9.1.1 TRANSPARENT EMI SHIELDING MATERIALS

- 9.2 EMI SHIELDING EFFECTIVENESS TESTS

- 9.2.1 SHIELDED BOX TESTS

- 9.2.2 SHIELDED ROOM TESTS

- 9.2.3 OPEN FIELD TESTS

- 9.2.4 COAXIAL TRANSMISSION LINE TESTS

10 FORMATIONS OF EMI SHIELDING

- 10.1 INTRODUCTION

- 10.2 EMI SHIELDING GASKETS AND O-RINGS

- 10.2.1 EMI SHIELDING GASKETS

- 10.2.2 EMI SHIELDING O-RINGS

- 10.3 SOLID ENCLOSURES

- 10.4 WIRE MESH & SCREENS

- 10.5 CABLE SHIELDING

- 10.6 COATINGS

11 EMI SHIELDING MARKET, BY TYPE

- 11.1 INTRODUCTION

- 11.1.1 NARROWBAND EMI

- 11.1.1.1 Increasing complexity of electronic architecture to accelerate demand for targeted EMI shielding

- 11.1.2 BROADBAND EMI

- 11.1.2.1 Expansion of high-speed connectivity infrastructure to drive demand for wide-spectrum shielding solutions

- 11.1.1 NARROWBAND EMI

12 EMI SHIELDING MARKET, BY MATERIAL

- 12.1 INTRODUCTION

- 12.2 CONDUCTIVE COATINGS & PAINTS

- 12.2.1 SILVER-BASED

- 12.2.1.1 Superior electrical conductivity to drive demand for high-performance EMI shielding

- 12.2.2 COPPER-BASED

- 12.2.2.1 Cost-effective conductivity to support adoption across high-volume electronics

- 12.2.3 NICKEL-BASED

- 12.2.3.1 Strong corrosion resistance to increase adoption in harsh operating environments

- 12.2.4 CARBON-BASED

- 12.2.4.1 Printed carbon ink

- 12.2.4.1.1 Increasing adoption of printed electronics to drive demand for carbon ink shielding solutions

- 12.2.4.2 Graphene-based conductive coatings

- 12.2.4.2.1 Superior conductivity-to-weight ratio to accelerate adoption

- 12.2.4.1 Printed carbon ink

- 12.2.5 OTHER TYPES

- 12.2.1 SILVER-BASED

- 12.3 CONDUCTIVE POLYMERS

- 12.3.1 CONDUCTIVE ELASTOMERS

- 12.3.1.1 Silicone and fluorosilicone

- 12.3.1.1.1 Increasing use of high-temperature electronics in aerospace and defense to drive demand

- 12.3.1.2 EPDM

- 12.3.1.2.1 Expansion of high-speed internet networks to boost demand

- 12.3.1.1 Silicone and fluorosilicone

- 12.3.2 CONDUCTIVE PLASTICS

- 12.3.2.1 Increasing demand for lightweight and versatile conductive plastics to augment market growth

- 12.3.1 CONDUCTIVE ELASTOMERS

- 12.4 METAL SHIELDING

- 12.4.1 INCREASING DEPLOYMENT OF 5G BASE STATIONS TO DRIVE DEMAND FOR HIGH-PERFORMANCE METAL SHIELDING MATERIALS

- 12.5 EMI/EMC FILTERS

- 12.5.1 EMI/EMC FILTERS, BY LOAD TYPE

- 12.5.1.1 AC filters

- 12.5.1.1.1 Single-phase

- 12.5.1.1.1.1 Increasing adoption of consumer electronics and low-power equipment to drive demand

- 12.5.1.1.2 Three-phase

- 12.5.1.1.2.1 Increasing industrial automation and motor drive adoption to propel demand

- 12.5.1.1.1 Single-phase

- 12.5.1.2 DC filters

- 12.5.1.2.1 Expansion of EV charging and renewable energy systems to accelerate demand for DC EMI filters

- 12.5.1.1 AC filters

- 12.5.2 EMI/EMC FILTERS, BY INSERTION LOSS

- 12.5.2.1 Common-mode

- 12.5.2.1.1 Increasing density of high-speed electronics to drive demand

- 12.5.2.2 Differential-mode

- 12.5.2.2.1 Rising use of power electronics to accelerate demand

- 12.5.2.1 Common-mode

- 12.5.1 EMI/EMC FILTERS, BY LOAD TYPE

- 12.6 EMI SHIELDING TAPES & LAMINATES

- 12.6.1 INCREASING DEMAND FOR EMI SHIELDING IN 5G INFRASTRUCTURE TO AUGMENT MARKET GROWTH

13 EMI SHIELDING MARKET, BY METHOD

- 13.1 INTRODUCTION

- 13.2 RADIATION

- 13.2.1 ADVANCEMENTS IN LIGHTWEIGHT SHIELDING MATERIALS TO DRIVE ADOPTION IN HIGH-PERFORMANCE ELECTRONIC APPLICATIONS

- 13.3 CONDUCTION

- 13.3.1 GROWTH IN CONNECTED ELECTRONICS ACROSS AUTOMOTIVE AND CONSUMER SEGMENTS TO INCREASE DEMAND

14 EMI SHIELDING MARKET, BY FREQUENCY

- 14.1 INTRODUCTION

- 14.2 BELOW 100 MHZ

- 14.2.1 INCREASING ADOPTION OF POWER ELECTRONICS TO DRIVE DEMAND FOR LOW-FREQUENCY EMI SHIELDING

- 14.3 ABOVE 100 MHZ

- 14.3.1 NEED FOR SEAMLESS CONNECTIVITY AND ADHERENCE TO STRINGENT REGULATORY STANDARDS TO DRIVE MARKET

15 EMI SHIELDING MARKET, BY APPLICATION

- 15.1 INTRODUCTION

- 15.2 PCB-LEVEL SHIELDING

- 15.2.1 INCREASING CIRCUIT DENSITY IN COMPACT ELECTRONICS TO DRIVE DEMAND

- 15.3 CABLE SHIELDING

- 15.3.1 RISING COMPLEXITY OF CONNECTED SYSTEMS TO ACCELERATE DEMAND

- 15.4 ENCLOSURE SHIELDING

- 15.4.1 INCREASING ADOPTION OF HIGH-FREQUENCY ELECTRONICS TO DRIVE MARKET

- 15.5 CONNECTOR SHIELDING

- 15.5.1 GROWTH IN HIGH-SPEED DATA TRANSMISSION TO INCREASE DEMAND

- 15.6 ANTENNA SHIELDING

- 15.6.1 EXPANSION OF MULTI-BAND WIRELESS DEVICES TO DRIVE MARKET

16 EMI SHIELDING MARKET, BY INDUSTRY

- 16.1 INTRODUCTION

- 16.2 CONSUMER ELECTRONICS

- 16.2.1 STRINGENT REGULATORY REQUIREMENTS FOR ELECTROMAGNETIC COMPATIBILITY TO FUEL MARKET GROWTH

- 16.2.2 SMARTPHONES

- 16.2.3 LAPTOPS AND COMPUTERS

- 16.2.4 SMART HOME DEVICES

- 16.2.5 GAMING CONSOLES

- 16.3 TELECOMMUNICATIONS

- 16.3.1 GOVERNMENT-BACKED 5G INVESTMENTS TO ACCELERATE DEMAND FOR EMI SHIELDING SOLUTIONS

- 16.3.2 BASE STATIONS AND SMALL CELLS

- 16.3.3 STORAGE DEVICES

- 16.3.4 OPTICAL TRANSCEIVERS

- 16.4 AUTOMOTIVE

- 16.4.1 INCREASING INVESTMENTS IN EV INFRASTRUCTURE AND ADVANCED VEHICLE ELECTRONICS TO DRIVE DEMAND FOR EMI SHIELDING

- 16.4.2 ADVANCED DRIVER ASSISTANCE SYSTEMS (ADAS)

- 16.4.3 INFOTAINMENT AND COMMUNICATION SYSTEMS

- 16.4.4 ENGINE CONTROL UNITS (ECUS)

- 16.5 HEALTHCARE

- 16.5.1 MINIATURIZATION OF MEDICAL DEVICES TO DRIVE MARKET GROWTH

- 16.5.2 MEDICAL DEVICES

- 16.5.3 DIAGNOSTIC EQUIPMENT

- 16.6 AEROSPACE

- 16.6.1 INCREASING ADOPTION OF ADVANCED AVIONICS AND RADAR SYSTEMS TO DRIVE DEMAND FOR EMI SHIELDING SOLUTIONS

- 16.6.2 NAVIGATION AND COMMUNICATION SYSTEMS

- 16.6.3 RADAR AND SURVEILLANCE SYSTEMS

- 16.7 ENERGY & POWER

- 16.7.1 INCREASING INVESTMENTS IN RENEWABLE ENERGY INFRASTRUCTURE TO DRIVE DEMAND FOR EMI SHIELDING SOLUTIONS

- 16.7.2 POWER DISTRIBUTION SYSTEMS

- 16.8 INDUSTRIAL

- 16.8.1 INCREASING DEMAND FOR ADVANCED ROBOTICS AND AUTOMATION SYSTEMS TO AUGMENT MARKET GROWTH

- 16.8.2 LOGIC CONTROLLERS

- 16.8.3 ROBOTICS

- 16.8.4 INDUSTRIAL IOT DEVICES

- 16.9 TRANSPORTATION

- 16.9.1 INCREASING INVESTMENTS IN RAIL ELECTRIFICATION AND HIGH-SPEED RAIL INFRASTRUCTURE TO DRIVE DEMAND

- 16.9.2 TRAIN CONTROL AND PROPULSION

17 EMI SHIELDING MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Increase in semiconductor manufacturing investments to drive market

- 17.2.2 CANADA

- 17.2.2.1 Increasing investments in semiconductor and advanced electronics manufacturing to propel market

- 17.2.3 MEXICO

- 17.2.3.1 Growth in electronics manufacturing and semiconductor assembly to drive market

- 17.2.1 US

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Strong automotive electronics innovation to drive demand for EMI shielding solutions

- 17.3.2 UK

- 17.3.2.1 Growing demand for sophisticated electronic devices in healthcare industry to drive market

- 17.3.3 FRANCE

- 17.3.3.1 Adoption of advanced technologies in aerospace and defense to increase demand

- 17.3.4 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 ASIA PACIFIC

- 17.4.1 CHINA

- 17.4.1.1 Telecom infrastructure expansion to support market growth

- 17.4.2 JAPAN

- 17.4.2.1 Surging developments in various industries to stimulate market growth

- 17.4.3 INDIA

- 17.4.3.1 Expanding automotive, telecom, and defense electronics sectors to drive demand

- 17.4.4 REST OF ASIA PACIFIC

- 17.4.1 CHINA

- 17.5 ROW

- 17.5.1 MIDDLE EAST

- 17.5.1.1 Saudi Arabia

- 17.5.1.1.1 Telecom, automotive electrification, smart infrastructure, and digital transformation to drive growth

- 17.5.1.2 UAE

- 17.5.1.2.1 Increasing investments in manufacturing sector to drive market

- 17.5.1.3 Rest of Middle East

- 17.5.1.1 Saudi Arabia

- 17.5.2 AFRICA

- 17.5.2.1 Increased adoption of telecommunications networks, digital infrastructure, and electronics to propel market

- 17.5.3 SOUTH AMERICA

- 17.5.3.1 Brazil

- 17.5.3.1.1 Growing automotive industry to boost demand

- 17.5.3.2 Argentina

- 17.5.3.2.1 Modernization of manufacturing sector to drive market

- 17.5.3.3 Rest of South America

- 17.5.3.1 Brazil

- 17.5.1 MIDDLE EAST

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 18.3 REVENUE ANALYSIS, 2021-2025

- 18.4 MARKET SHARE ANALYSIS, 2O25

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND COMPARISON

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Material footprint

- 18.7.5.4 Method footprint

- 18.7.5.5 Industry footprint

- 18.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 18.8.5.1 Detailed list of key startups/SMEs

- 18.8.5.2 Competitive benchmarking of key startups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 PARKER HANNIFIN CORP

- 19.1.1.1 Business overview

- 19.1.1.2 Products/Solutions/Services offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches

- 19.1.1.4 MnM view

- 19.1.1.4.1 Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 PPG INDUSTRIES, INC.

- 19.1.2.1 Business overview

- 19.1.2.2 Products/Solutions/Services offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Expansions

- 19.1.2.3.4 Other developments

- 19.1.2.4 MnM view

- 19.1.2.4.1 Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 3M

- 19.1.3.1 Business overview

- 19.1.3.2 Products/Solutions/Services offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Expansions

- 19.1.3.4 MnM view

- 19.1.3.4.1 Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 HENKEL AG & CO. KGAA

- 19.1.4.1 Business overview

- 19.1.4.2 Products/Solutions/Services offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches

- 19.1.4.3.2 Other developments

- 19.1.4.4 MnM view

- 19.1.4.4.1 Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 QNITY ELECTRONICS, INC.

- 19.1.5.1 Business overview

- 19.1.5.2 Products/Solutions/Services offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches

- 19.1.5.3.2 Other developments

- 19.1.5.4 MnM view

- 19.1.5.4.1 Right to win

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses and competitive threats

- 19.1.6 LEADER TECH INC.

- 19.1.6.1 Business overview

- 19.1.6.2 Products/Solutions/Services offered

- 19.1.7 MG CHEMICALS

- 19.1.7.1 Business overview

- 19.1.7.2 Products/Solutions/Services offered

- 19.1.8 NOLATO AB

- 19.1.8.1 Business overview

- 19.1.8.2 Products/Solutions/Services offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Deals

- 19.1.9 TECH ETCH, INC.

- 19.1.9.1 Business overview

- 19.1.9.2 Products/Solutions/Services offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches

- 19.1.9.3.2 Deals

- 19.1.10 RTP COMPANY

- 19.1.10.1 Business overview

- 19.1.10.2 Products/Solutions/Services offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Deals

- 19.1.11 TE CONNECTIVITY

- 19.1.11.1 Business overview

- 19.1.11.2 Products/Solutions/Services offered

- 19.1.12 KITAGAWA INDUSTRIES AMERICA, INC.

- 19.1.12.1 Business overview

- 19.1.12.2 Products/Solutions/Services offered

- 19.1.13 ETS-LINDGREN

- 19.1.13.1 Business overview

- 19.1.13.2 Products/Solutions/Services offered

- 19.1.14 SEAL SCIENCE, INC.

- 19.1.14.1 Business overview

- 19.1.14.2 Products/Solutions/Services offered

- 19.1.1 PARKER HANNIFIN CORP

- 19.2 OTHER PLAYERS

- 19.2.1 E-SONG EMC CO., LTD

- 19.2.2 EAST COAST SHIELDING

- 19.2.3 EFFECTIVE SHIELDING CO. INC.

- 19.2.4 ATLANTA METAL COATING, INC.

- 19.2.5 HOLLAND SHIELDING SYSTEMS BV

- 19.2.6 ICOTEK

- 19.2.7 INTEGRATED POLYMER SOLUTIONS

- 19.2.8 INTERSTATE SPECIALTY PRODUCTS

- 19.2.9 MARIAN, INC.

- 19.2.10 NTRIUM INC.

- 19.2.11 OMEGA SHIELDING PRODUCTS

- 19.2.12 SPIRA MANUFACTURING

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH APPROACH

- 20.1.1 SECONDARY AND PRIMARY RESEARCH

- 20.1.2 SECONDARY DATA

- 20.1.2.1 List of major secondary sources

- 20.1.2.2 Key data from secondary sources

- 20.1.3 PRIMARY DATA

- 20.1.3.1 Breakdown of primaries

- 20.1.3.2 Key data from primary sources

- 20.1.3.3 Key primary participants

- 20.1.3.4 Key industry insights

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.2 TOP-DOWN APPROACH

- 20.2.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 20.3 MARKET FORECAST APPROACH

- 20.3.1 SUPPLY SIDE

- 20.3.2 DEMAND SIDE

- 20.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 20.5 RESEARCH ASSUMPTIONS

- 20.6 RISK ASSESSMENT

21 APPENDIX

- 21.1 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.2 CUSTOMIZATION OPTIONS

- 21.3 RELATED REPORTS

- 21.4 AUTHOR DETAILS