|

시장보고서

상품코드

2062069

전자파(EMI) 차폐 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Electromagnetic Interference (EMI) Shielding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

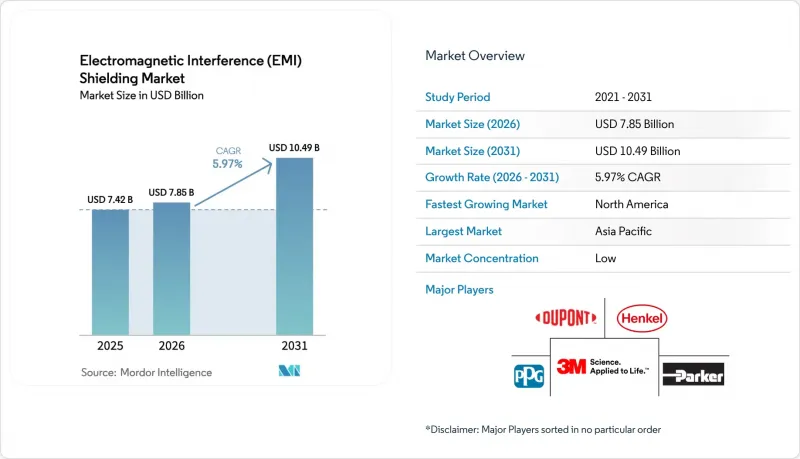

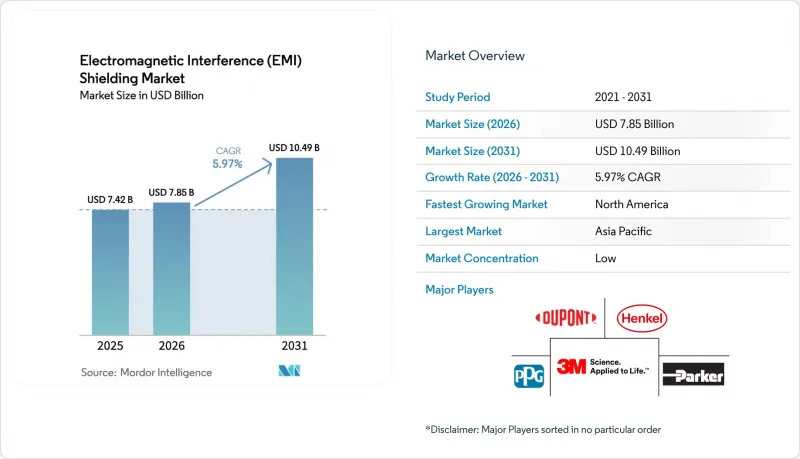

Mordor Intelligence에 의하면, 전자파(EMI) 차폐 시장 규모는 2025년에 74억 2,000만 달러로 평가되었고, 2026년 78억 5,000만 달러로 평가되었고, 2031년까지 104억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.97%를 나타낼 전망입니다.

본 보고서는 소재 유형별(금속 차폐, 기타), 차폐 방법별(컨포멀 코팅, 개스킷 차폐, 기타), 용도별(가전 및 웨어러블 기기, 기타), 형태별(시트 및 폼, 기타), 지역별(아시아태평양, 북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 전자파(EMI) 차폐 시장 동향 및 분석

가전제품과 웨어러블 기기의 보급 확대

스마트폰, 스마트 워치, 이어폰은 소형화가 진행되고 있기 때문에 엔지니어들은 현재 2.4-6GHz 대역에서 60 dB 이상의 감쇠 성능을 유지하면서 두께 10μm 이하의 차폐층을 지정하고 있습니다. MXene 기반 직물은 단층 구조에서 42dB, 3층 적층 구조에서 69dB의 감쇠 성능을 달성하며, 500회 이상의 굽힘에도 견딜 수 있어 곡면이 있는 웨어러블 기기의 표면에 최적입니다. 폴더블 스마트폰의 힌지는 20만 회 이상 접어도 견딜 수 있습니다. 은 나노와이어 잉크는 50%의 변형 하에서도 31,000 S/cm의 전도성을 유지하며, RF 누설 채널을 방지합니다. 투명하고 신축성이 있으며 세탁이 가능한 필름 시장이 성숙해짐에 따라, 롤 투 롤 코팅 라인을 보유한 공급업체들이 기존 금속 캔 제조업체들을 앞지를 것으로 예측됩니다.

5G/mm파 인프라의 급속한 확산

26GHz 및 39GHz mm파 기지국의 경우, 저손실 폴리테트라플루오로에틸렌(PTFE)이나 액정 폴리머 기판이 방사 방출을 증폭시키기 때문에 80 dB 이상의 정격치를 갖는 기판 수준의 차폐가 필요합니다. 연방통신위원회(FCC)의 Part 15와 유럽전기통신표준화기구(ETSI)의 EN 301 489가 2024년에 강화됨에 따라, OEM(원래 장비 제조업체)은 현재 열 비아와 EMI 개스킷을 결합한 성형 어셈블리를 구매하여 제조 공정을 줄이고 있습니다. 북미의 스몰셀 수는 2028년까지 100만 대를 넘어설 것으로 예상되며, 워싱턴 D.C. 인근의 데이터센터 운영업체들은 그래픽 처리 장치(GPU) 메모리 오류 사고를 계기로 이미 랙에 60-80dB 수준의 방음 패널을 추가로 설치하고 있습니다.

고성능 차폐 재료 및 공정의 높은 비용

나노 소재 필름은 1kg당 200달러를 넘기도 하며, 이는 니켈 코팅 탄소섬유의 10배에 달하는 가격입니다. 진공 스퍼터링 장비는 50만 달러 이상이며 30-60분 주기로 가동되는 반면, 초음파 코팅 장비는 설비 투자 비용이 약 5만 달러로 저렴하지만 잉크 배합의 복잡성은 더 커집니다. 인증 획득에는 개발 예산의 15-20%가 추가로 소요되기 때문에 사내에 전자기적 호환성(EMC) 시험실을 갖추지 못한 중소기업들은 제품 출시 지연에 직면하고 있습니다.

부문별 분석

2025년에는 전도성 코팅 및 도료가 매출의 32.70%를 차지했습니다. 이는 스프레이, 브러시, 침지 코팅과 같은 공정과의 호환성에 기반을 두고 있으며, 막대한 설비 투자가 필요한 장비 변경 없이도 기존 생산 라인에 원활하게 통합할 수 있기 때문입니다. 금속 차폐는 80dB 이상의 감쇠가 필요한 항공 전자 장비 베이 등, 높은 내구성이 요구되는 용도에서 여전히 주류를 이루고 있습니다.

전도성 폴리머 및 복합재료 시장은 2031년까지 연평균 성장률(CAGR) 6.12%를 나타낼 것으로 예측되며, 선박 및 실외 통신 장비의 외장재에 내식성을 요구하는 설계자들의 관심을 끌 것으로 보입니다. 폴리아닐린/니켈 페라이트 복합재료는 주로 흡수 메커니즘을 통해 K 대역에서 78.07 dB의 차폐 효과를 달성하였으며, 그린 지수도 1.0을 초과합니다. 이는 EU의 REACH 규정에 따라 금지된 6가 크롬 표면 처리와 비교할 때 환경적 측면에서 우월함을 보여줍니다. 하이브리드 TPU 복합 소재는 현재 312 S/cm의 전도성을 보이고 있으며, 다양한 소재 포트폴리오를 제공하는 공급업체는 축소되는 공급업체 목록 속에서 교차 판매가 가능해집니다.

개스킷을 이용한 차폐 기술은 2025년에 53.15%의 시장 점유율을 차지한 것으로 평가되었으며, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR)은 6.23%를 나타낼 것으로 보입니다. 이는 10만 회의 도어 개폐 사이클을 통해 1Ω 이하의 접촉 저항을 유지하고, 125°C에 달하는 보닛 내부 온도를 견딜 수 있는 전도성 엘라스토머 및 폼 상부 천 코팅 개스킷을 지정하는 자동차 OEM 업체들에 의해 주도되고 있습니다. 기판 레벨 차폐는 스마트폰 및 IoT 모듈 수요를 흡수하고 있지만, 모듈 공급업체들이 기판 제조 시 통합 성형 차폐로 전환함에 따라 이 부문은 이익률 압박에 직면해 있습니다.

컨포멀 코팅은 비용 효율성을 중시하는 소비자용 용도, 셋톱박스, 스마트 스피커에 제공되며, 스프레이로 도포된 은 또는 니켈 도료를 통해 금형 투자 없이도 FCC Part 15 Class B 규정을 충족하는 30-50 dB의 감쇠 성능을 실현합니다. 케이블 차폐 및 인클로저, 통풍구 차폐는 인프라 시장에 대응하고 있습니다. 수냉식 AI 랙을 설치하는 데이터센터 사업자는 열 스로틀링을 방지하기 위해 200 CFM 이상의 기류를 유지하면서도, 1-6GHz 대역에서 60-80 dB의 감쇠 성능을 구현하는 허니컴 메쉬가 적용된 RF 차폐 통풍 패널이 필요합니다.

지역별 분석

2025년에는 아시아태평양이 매출의 41.40%를 차지했습니다. 이는 심천과 동관의 클러스터가 세계 스마트폰 및 웨어러블 기기의 60% 이상을 조립하고 있는 중국의 전자기기 제조 거점, 그리고 배터리 관리 시스템(BMS)의 실드 수요를 끌어모으고 있는 인도의 확대되는 전기차용 배터리 셀 생산 능력에 힘입은 결과입니다. 일본은 2-6GHz 모듈용 고성능 페라이트 코어 시장에서 약 9억 달러 시장 규모를 기록했습니다. 한국 5G 시장의 선도적 입지와 삼성의 투자가 치플렛(Chiplet) 실드 수요를 끌어올리고 있는 반면, 싱가포르와 자카르타의 데이터센터에서는 벤트 패널 수요가 급증하고 있습니다.

2031년까지 연평균 성장률(CAGR) 6.55%로 가장 빠른 성장이 예상되는 북미는 하이퍼스케일 데이터센터의 확장과 5G 인프라 투자의 혜택을 누리고 있습니다. 2025년에는 사업자들이 GPU 클러스터와 엣지 노드를 동일한 시설 내에 함께 배치하는 추세가 확산되면서, 북버지니아주에서만 해당 지역의 EMI 차폐 통풍 패널 소비량의 30% 이상을 차지했습니다.

유럽은 2025년에 큰 시장 점유율을 차지할 것으로 보이며, 독일의 자동차 및 산업 기반에 더해, 6가 크롬산염 코팅을 전도성 폴리머로 대체하는 것을 가속화하는 EU의 REACH 규제가 이를 주도하고 있습니다. 프랑스의 항공우주 및 방위 부문에서는 낙뢰 내성 인증을 획득한 케이블 실드나 MIL-STD-461G 규격을 준수하는 케이스가 요구되고 있는 반면, 영국에서는 5G 구축과 스마트 그리드에 대한 투자가 통신 및 산업 자동화 부문을 뒷받침하고 있습니다. 남미, 중동 및 아프리카는 여전히 신흥 시장이며, 브라질의 항공우주 클러스터나 아랍에미리트의 스마트 시티 프로젝트가 틈새 시장 기회를 제공하고 있지만, 현지 생산이 제한적이고 수입 의존도가 높기 때문에 이미 성숙한 지역에 비해 성장이 제약을 받고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the electromagnetic interference shielding market size was valued at USD 7.42 billion in 2025 and is estimated to grow from USD 7.85 billion in 2026 to reach USD 10.49 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031).

This report is Segmented by Material Type (Metal Shielding, and More), Shielding Method (Conformal Coating, Gasket Shielding, and More), Application (Consumer Electronics and Wearables, and More), Form Factor (Sheets and Foams and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Electromagnetic Interference (EMI) Shielding Market Trends and Insights

Surging Adoption of Consumer Electronics and Wearables

Smartphones, smartwatches, and earbuds are shrinking, so engineers now specify shielding layers thinner than 10 μm that still deliver over 60 dB attenuation from 2.4-6 GHz. MXene-based fabrics achieve 42 dB in a single layer and 69 dB in triple stacks while enduring more than 500 bends, making them ideal for curved wearable surfaces. Foldable-phone hinges flex over 200,000 times; silver-nanowire inks keep 31,000 S/cm conductivity even under 50% strain, preventing RF leakage paths. As transparent, stretchable, and washable films mature, suppliers with roll-to-roll coating lines will outpace traditional metal-can vendors.

Rapid 5G/mm-Wave Infrastructure Rollout

Millimeter-wave base stations at 26 GHz and 39 GHz need board-level shields rated above 80 dB because low-loss polytetrafluoroethylene (PTFE) and liquid-crystal-polymer substrates amplify radiated emissions. Federal Communications Commission (FCC) Part 15 and European Telecommunications Standards Institute (ETSI) EN 301 489 tightened in 2024, so OEMs (Original Equipment Manufacturers) now buy molded assemblies that combine thermal vias and EMI gaskets, cutting production steps. North American small-cell counts are on track to top 1 million by 2028, and data-center operators near Washington D.C. already retrofit racks with 60-80 dB panels after graphics processing unit (GPU) memory-error incidents.

High Cost of Advanced Shielding Materials and Processes

Nanomaterial films can exceed USD 200 per kg, ten times the price of nickel-coated carbon fibers. Vacuum sputtering tools cost above USD 500,000 and run 30-60 minute cycles, while ultrasonic coaters have lower capital needs, at roughly USD 50,000, but add ink-formulation complexity. Certification adds 15-20% to development budgets, so small firms without in-house Electromagnetic Compatibility (EMC) labs face delayed launches.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Global EMC Regulations in Auto, Medical and Aero Sectors

- Chiplet and SiP Compartment-Level Shielding in Advanced Packaging

- Copper-Price Volatility Elevating BOM Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conductive coatings and paints controlled 32.70% of revenue in 2025, sustained by their compatibility with spray, brush, and dip-coating processes that integrate seamlessly into existing production lines without capital-intensive tooling changes. Metal shielding still dominates high-robustness roles such as avionics bays that need more than 80 dB attenuation.

Conductive polymers and composites will grow at 6.12% CAGR to 2031, attract designers seeking corrosion immunity in marine and outdoor telecom enclosures; polyaniline/nickel-ferrite composites achieved 78.07 dB shielding effectiveness in K-band with absorption-dominant mechanisms and Green Index above 1.0, signaling environmental advantages over hexavalent-chromate surface treatments banned under EU REACH. Hybrid TPU composites now post 312 S/cm conductivity, so suppliers offering multi-material portfolios can cross-sell within shrinking vendor lists.

Gasket Shielding held 53.15% method share in 2025 and will grow at 6.23% CAGR during the forecast period (2026-2031), propelled by automotive OEMs specifying conductive-elastomer and fabric-over-foam gaskets that maintain less than 1 Ω contact resistance across 100,000 door-open cycles and withstand underhood temperatures reaching 125°C. Board-Level Shielding captures smartphone and IoT-module demand, yet this segment faces margin pressure as module vendors shift to molded shielding integrated during substrate fabrication.

Conformal Coating serves cost-sensitive consumer applications, set-top boxes, and smart speakers, where spray-applied silver or nickel paints deliver 30-50 dB attenuation sufficient for FCC Part 15 Class B compliance without tooling investment. Cable Shielding and Enclosure and Vent Shielding address infrastructure markets: data-center operators installing liquid-cooled AI racks require RF-shielded ventilation panels with honeycomb mesh that attenuates 60-80 dB at 1-6 GHz while sustaining airflow above 200 CFM to prevent thermal throttling.

Geography Analysis

Asia-Pacific commanded 41.40% of revenue in 2025, anchored by China's electronics-manufacturing base, where Shenzhen and Dongguan clusters assemble over 60% of global smartphones and wearables, and India's expanding EV cell-production capacity, which is attracting battery-management-system shielding demand. Japan logged about USD 900 million on advanced ferrite cores for 2-6 GHz modules. South Korea's 5G leadership and Samsung investments uplift chiplet shielding, while Singapore and Jakarta data centers spike vent-panel demand.

North America, forecast to grow fastest at 6.55% CAGR through 2031, benefits from hyperscale data-center expansion and 5G infrastructure investment; Northern Virginia alone accounted for over 30% of regional EMI-shielding ventilation-panel consumption in 2025 as operators co-locate GPU clusters and edge nodes within the same facilities.

Europe held a significant share in 2025, driven by Germany's automotive and industrial base and stringent EU REACH regulations that accelerate the substitution of hexavalent-chromate coatings with conductive polymers. France's aerospace and defense sectors demand lightning-strike-certified cable shields and MIL-STD-461G enclosures, while the United Kingdom's 5G rollout and smart-grid investments support telecom and industrial-automation segments. South America and Middle East and Africa remain emerging markets, with Brazil's aerospace clusters and UAE's smart-city projects providing niche opportunities, yet limited local manufacturing and reliance on imports constrain growth relative to established regions.

- 3M

- Changzhou National Radio-Products Factory

- DuPont

- ETS-Lindgren

- Henkel AG & Co. KGaA

- Holland Shielding Systems BV

- Kitagawa Industries Co., Ltd.

- Leader Tech Inc.

- MG Chemicals

- Mobix Labs

- Nolato AB

- Parker Hannifin Corp

- PPG Industries Inc.

- RTP Company

- Schaffner Holding AG

- Sekisui Chemical Co., Ltd.

- Shin-Etsu Polymer Co., Ltd.

- Sidus Space

- TDK Corporation

- Tech-Etch Inc.

- W. L. Gore & Associates Inc.

- YShield GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of consumer electronics and wearables

- 4.2.2 Rapid 5G/mm-Wave infrastructure rollout

- 4.2.3 Stricter global EMC regulations in auto, medical and aero sectors

- 4.2.4 Vertical-specific satellite constellations driving on-board shielding demand

- 4.2.5 Chiplet and SiP compartment-level shielding in advanced packaging

- 4.3 Market Restraints

- 4.3.1 High cost of advanced shielding materials and processes

- 4.3.2 Form-factor constraints in ultra-compact and foldable devices

- 4.3.3 Copper-price volatility elevating BOM risk in large-volume programs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Conductive Coatings and Paints

- 5.1.2 Metal Shielding

- 5.1.3 Conductive Polymers and Composites

- 5.1.4 EMI/EMC Filters

- 5.1.5 Tapes and Laminates

- 5.1.6 Carbon-based Foams and Nanomaterial Films

- 5.2 By Shielding Method

- 5.2.1 Conformal Coating

- 5.2.2 Gasket Shielding

- 5.2.3 Board-Level Shielding

- 5.2.4 Cable Shielding

- 5.2.5 Enclosure and Vent Shielding

- 5.3 By Application

- 5.3.1 Consumer Electronics and Wearables

- 5.3.2 Automotive and Electric Vehicles

- 5.3.3 Telecommunications and 5G/6G Infrastructure

- 5.3.4 Aerospace, Defense and eVTOL

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Industrial Equipment and Automation

- 5.3.7 Renewable Energy and Smart Grid

- 5.3.8 Data Centers and Cloud Infrastructure

- 5.4 By Form Factor

- 5.4.1 Films and Coatings

- 5.4.2 Gaskets and O-Rings

- 5.4.3 Sheets and Foams

- 5.4.4 Fabric/Flexible Textiles

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Asia-Pacific

- 5.5.5.1 China

- 5.5.5.2 India

- 5.5.5.3 Japan

- 5.5.5.4 South Korea

- 5.5.5.5 Rest of Asia-Pacific

- 5.5.6 Middle-East and Africa

- 5.5.6.1 South Africa

- 5.5.6.2 United Arab Emirates

- 5.5.6.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Changzhou National Radio-Products Factory

- 6.4.3 DuPont

- 6.4.4 ETS-Lindgren

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 Holland Shielding Systems BV

- 6.4.7 Kitagawa Industries Co., Ltd.

- 6.4.8 Leader Tech Inc.

- 6.4.9 MG Chemicals

- 6.4.10 Mobix Labs

- 6.4.11 Nolato AB

- 6.4.12 Parker Hannifin Corp

- 6.4.13 PPG Industries Inc.

- 6.4.14 RTP Company

- 6.4.15 Schaffner Holding AG

- 6.4.16 Sekisui Chemical Co., Ltd.

- 6.4.17 Shin-Etsu Polymer Co., Ltd.

- 6.4.18 Sidus Space

- 6.4.19 TDK Corporation

- 6.4.20 Tech-Etch Inc.

- 6.4.21 W. L. Gore & Associates Inc.

- 6.4.22 YShield GmbH & Co. KG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment