|

시장보고서

상품코드

2033996

치과용 소모품 시장 : 제품별, 최종사용자별, 지역별 - 세계 예측(-2031년)Dental Consumables Market by Product, By End User - Global Forecast to 2031 |

||||||

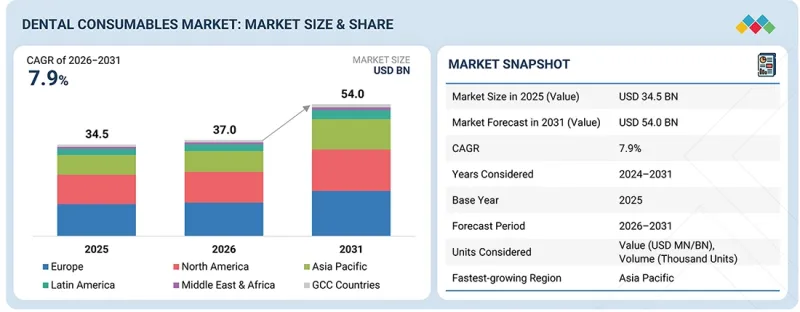

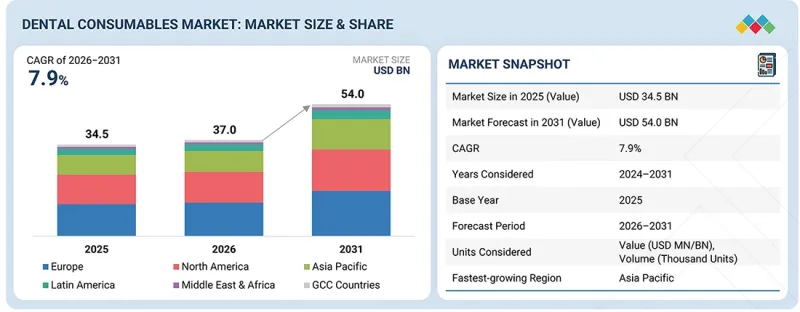

세계의 치과용 소모품 시장 규모는 예측 기간 동안 CAGR 7.9%로 확대되어 2026년 370억 달러에서 2031년에는 540억 달러에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

치과용 소모품 시장은 인구통계학적 변화, 임상적 요구, 기술 발전의 영향을 받아 빠르게 성장할 것으로 예상됩니다. 치과 질환을 앓고 있는 사람들이 증가하고, 특히 수복 및 보철 치료를 필요로 하는 노년층이 증가함에 따라 전 세계 수요는 계속 증가하고 있습니다. 치과용 재료의 개선과 디지털 덴티스트리, 생체적합성 복합재료, CAD/CAM 시스템 등의 혁신적인 기술로 치료 결과가 크게 향상되어 제품 보급이 촉진되고 있습니다. 또한 구강 위생에 대한 관심 증가, 치과 의료에 대한 접근성 향상, 미용치과의 인기 확대도 시장 성장에 기여하고 있습니다. 이러한 추세는 향후 몇 년 동안 선진국과 신흥 지역 모두에서 강세를 유지할 것으로 예상됩니다.

제품 유형별로는 치과 수복물 부문이 치과용 소모품 시장을 주도하고 있습니다.

치과용 소모품 시장은 제품 유형에 따라 치과 수복, 교정, 교정, 치주 치료, 감염 관리, 신경치료, 미백 제품, 마감 및 연마 제품, 기타로 분류됩니다.

이 중 치과 수복 부문은 충치, 치아 상실과 같은 질환의 유병률이 높고 충전, 크라운, 브릿지 등의 시술이 필요하기 때문에 치과용 소모품 시장을 주도했습니다. 심미치과에 대한 수요 증가도 외관과 내구성이 향상된 첨단 수복 재료의 사용을 촉진하고 있습니다. 또한, 재료와 디지털 치과의 기술 발전으로 치료 결과와 효율성이 향상되었습니다. 구강 위생에 대한 인식이 높아지고 치과 의료에 대한 접근성이 향상되면서 이 부문의 지속적인 수요에 더욱 기여하고 있습니다.

최종사용자별로는 치과 병원 및 클리닉 부문이 치과용 소모품 시장에서 가장 큰 점유율을 차지했습니다.

치과용 소모품 시장은 치과 병원 및 클리닉, 치과 기공소, 치과 서비스 조직(DSO), 치과 교육 및 연구 기관, 법치의학을 포함한 기타 최종사용자로 구분됩니다. 2025년 기준, 치과 병원 및 클리닉은 환자 수, 제공되는 치료 방법의 다양성, 최신 치과 기술의 가용성을 바탕으로 치과 소모품 시장에서 가장 큰 점유율을 차지했습니다. 이들 기관은 신경치료, 수복치료, 외과적 수술을 많이 하는 경향이 있어 소모품에 대한 수요가 높은 편이며, 이에 따라 소모품에 대한 수요가 높습니다. 또한, 경험이 풍부한 치과의사의 존재와 공공 및 민간 클리닉의 인프라에 대한 투자 증가는 이 부문의 우위를 더욱 강화시키고 있습니다. 클리닉에서 심미치과와 예방치과에 대한 관심이 높아진 것도 시장에서의 선도적 지위를 뒷받침하고 있습니다.

아시아태평양은 예측 기간 동안 치과용 소모품 시장에서 가장 높은 CAGR을 기록할 것으로 예상됩니다.

아시아태평양은 신흥국의 치과 의료 접근성 향상과 빠르게 확대되는 의료 인프라를 바탕으로 예측 기간 동안 치과용 소모품 시장에서 가장 높은 성장률을 보일 것으로 예상됩니다. 구강 위생에 대한 인식이 높아지고 충치 및 치주질환과 같은 질병의 유병률이 증가함에 따라 예방 및 수복 치과 치료에 대한 수요가 증가하고 있습니다. 또한 가처분 소득의 증가, 중산층의 확대, 라이프스타일의 변화로 인해 필수적인 치과 치료뿐만 아니라 심미적인 치과 치료에 대한 지출도 증가하고 있습니다. 구강 의료에 대한 접근성을 개선하기 위한 정부의 노력과 더불어 민간 기업의 투자 증가는 시장 확대를 더욱 촉진하고 있습니다. 또한, 디지털 영상 진단, CAD/CAM 시스템 등 첨단 기술의 도입이 진행되면서 치료의 효율성과 성과가 향상되어 고품질 치과용 소모품에 대한 수요가 증가하고 있습니다.

치과용 소모품 시장의 주요 기업으로는 Institut Straumann AG(스위스), Envista(미국), Dentsply Sirona(미국), ZimVie Inc.(미국), Solventum(미국), Henry Schein, Inc.(미국), Kuraray(일본), Mitsui Chemicals, Inc.(일본), Geistlich Pharma AG(스위스), Ivoclar Vivadent(리히텐슈타인), GC Corporation(일본), Keystone Dental Inc.(미국), BEGO GmbH & Co. KG(독일), Septodont Holding(프랑스), Ultradent Products(미국), VOCO GmbH(독일), COLTENE Group(스위스), SDI Limited(호주), Young Innovations, Inc.(미국), DMG Chemisch-Pharmazeutische Fabrik(독일), Brasseler USA(미국), SHOFU INC.(일본), Glidewell(미국), BISCO, Inc.(미국), Dental Technologies Inc.(미국) 등이 있습니다.

조사 범위

이 보고서는 치과용 소모품 시장에 대한 분석을 제공하며, 제품 유형, 지역, 최종사용자를 포함한 각 부문의 시장 규모로 추정치 및 향후 성장 가능성에 초점을 맞추고 있습니다. 또한, 본 보고서에서는 시장 주요 기업에 대한 경쟁 분석을 통해 각 기업의 기업 개요, 제품 및 서비스 제공 내용, 최근 동향, 주요 시장 전략에 대해 상세히 기술하고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 치과용 소모품 업계의 시장 리더와 신규 진입자 모두에게 유용한 인사이트를 제공하며, 전체 시장과 하위 부문의 대략적인 매출 규모를 제시합니다. 이를 통해 이해관계자들은 경쟁 상황을 이해하고, 자신의 비즈니스를 더 나은 위치에 놓을 수 있으며, 효과적인 시장 진입 전략을 수립할 수 있습니다. 또한, 이 보고서는 주요 시장 촉진요인, 억제요인, 도전 과제, 기회 요인을 파악하여 이해관계자들이 시장 현황을 파악하는 데 도움이 될 것입니다.

본 보고서에서는 다음과 같은 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(충치 사례 증가에 따른 치아 수복 치료 증가, 고도화된 심미 치과 치료에 대한 수요 증가, 신흥국에서의 치과 관광 시장 확대, 그리고 첨단 솔루션 개발), 제약요인(부족한 보험 급여 및 높은 치과 서비스 비용), 기회(CAD/CAM 기술에 대한 투자 확대, 신흥 시장에 대한 관심 증가 및 가처분 소득 증가, 당일 치과 치료에 대한 수요 증가), 그리고 과제(주요 시장 진입 기업이 직면한 가격 압박 및 숙련된 실험실 전문가 부족)

- 시장 침투 : 이 보고서는 세계 치과용 소모품 시장의 주요 기업들이 제공하는 제품 포트폴리오에 대한 자세한 정보를 제공합니다. 이 보고서는 제품 유형, 최종사용자, 지역 등 다양한 부문을 다루고 있습니다.

- 제품 강화 및 혁신 : 세계 치과용 소모품 시장의 신제품 출시 및 예측 동향에 대한 종합적인 세부 정보.

- 시장 개발 : 제품 유형, 최종사용자, 지역별로 수익성 높은 성장 시장에 대한 철저한 지식과 분석을 제공합니다.

- 시장 다각화 : 세계 치과용 소모품 시장의 신제품 및 서비스 출시, 시장 확대, 현재 진행 상황 및 투자에 대한 종합적인 정보를 제공합니다.

- 경쟁 분석 : 세계 치과용 소모품 시장에서 주요 경쟁사의 시장 점유율, 성장 계획, 제품 및 서비스 제공, 생산능력에 대한 철저한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 치과용 소모품 시장(제품별)

제10장 치과용 소모품 시장(최종사용자별)

제11장 치과용 소모품 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

KSM 26.05.27The global dental consumables market is projected to reach USD 54.0 billion by 2031, up from USD 37.0 billion in 2026, at a CAGR of 7.9% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa |

The market for dental consumables is set to grow quickly, influenced by demographic shifts, clinical needs, and technological advancements. As more people experience dental issues and the aging population increases, especially those requiring restorative and prosthetic care, global demand continues to rise. Improvements in dental materials and innovative technologies like digital dentistry, biocompatible composites, and CAD/CAM systems have significantly improved treatment results, encouraging more widespread product use. Additionally, greater attention to oral health, easier access to dental care, and the growing popularity of cosmetic dentistry are all contributing to market growth. These trends are expected to sustain positive momentum in both developed and emerging regions in the years ahead.

By product type, the dental restoration segment dominated the dental consumables market.

The dental consumables market is segmented by product type into dental restoration, orthodontics, periodontics, infection control, endodontics, whitening products, finishing & polishing products, and others.

Among these, the dental restoration segment dominated the dental consumables market due to the high prevalence of conditions such as dental caries and tooth loss, which require procedures such as fillings, crowns, and bridges. Increasing demand for aesthetic dentistry has also driven the use of advanced restorative materials that offer improved appearance and durability. Moreover, technological advancements in materials and digital dentistry have enhanced treatment outcomes and efficiency. Rising awareness of oral health and greater access to dental care have further contributed to sustained demand in this segment.

Based on end user, the dental hospitals and clinics segment accounted for the largest share of the dental consumables market.

The dental consumables market is segmented into dental hospitals and clinics, dental laboratories, dental service organizations (DSOs), and other end users, including dental academic & research institutes and forensic dentistry. Dental hospitals and clinics accounted for the largest share of the dental consumables market in 2025 based on their high inflow of patients, extensive assortment of procedures offered, and availability of the latest dental technology. These institutions tend to manage a large volume of endodontic, restorative, and surgical cases, necessitating the high demand for consumables. Also, the presence of experienced dental practitioners and increasing investments in infrastructure at public and private clinics have augmented segment dominance further. The growing focus on cosmetic and preventive dental care in clinics supports their market leadership.

Asia Pacific is expected to register the highest CAGR in the dental consumables market during the forecast period.

The Asia Pacific is projected to experience the highest growth rate in the dental consumables market over the forecast period, driven by improving access to dental care and rapidly expanding healthcare infrastructure in emerging economies. Rising awareness of oral health, coupled with the increasing prevalence of conditions such as dental caries and periodontal diseases, is driving demand for both preventive and restorative dental treatments. Additionally, growing disposable incomes, a rising middle-class population, and changing lifestyle habits are encouraging higher spending on essential as well as cosmetic dental procedures. Government initiatives to improve oral healthcare access, along with increasing investments from private players, are further supporting market expansion. Furthermore, the growing adoption of advanced technologies, such as digital imaging and CAD/CAM systems, is enhancing treatment efficiency and outcomes, boosting demand for high-quality dental consumables.

A breakdown of the primary participants (supply side) for the dental consumables market referred to in this report is provided below:

- By Company Type: Tier 1 (30%), Tier 2 (35%), and Tier 3 (35%)

- By Designation: C-level Executives (20%), Directors (35%), and Others (45%)

- By Region: North America (30%), Europe (25%), Asia Pacific (20%), Latin America (20%), Middle East & Africa (2%), GCC Countries (3%)

Prominent players in the dental consumables market include Institut Straumann AG (Switzerland), Envista (US), Dentsply Sirona (US), ZimVie Inc. (US), Solventum (US), Henry Schein, Inc. (US), Kuraray Co., Ltd. (Japan), Mitsui Chemicals, Inc. (Japan), Geistlich Pharma AG (Switzerland), Ivoclar Vivadent (Liechtenstein), GC Corporation (Japan), Keystone Dental Inc. (US), BEGO GmbH & Co. KG (Germany), Septodont Holding (France), Ultradent Products (US), VOCO GmbH (Germany), COLTENE Group (Switzerland), SDI Limited (Australia), Young Innovations, Inc. (US), DMG Chemisch-Pharmazeutische Fabrik (Germany), Brasseler USA (US), SHOFU INC. (Japan), Glidewell (US), BISCO, Inc. (US), and Dental Technologies Inc. (US).

Research Coverage

The report provides an analysis of the dental consumables market, focusing on estimating market size and potential future growth across segments, including product types, regions, and end users. Additionally, the report features a competitive analysis of the key players in the market, detailing their company profiles, product & service offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report provides valuable insights for both market leaders and new entrants in the dental consumables industry, offering approximate revenue figures for the overall market and its subsegments. It helps stakeholders understand the competitive landscape, enabling them to better position their businesses and develop effective go-to-market strategies. Additionally, the report highlights key market drivers, restraints, challenges, and opportunities, helping stakeholders gauge the current state of the market.

This report provides insights into the following points:

- Analysis of key drivers (rising cases of dental caries and subsequent increase in tooth repair procedures, rising demand for advanced cosmetic dental procedures, growing market for dental tourism in emerging countries, and development of advanced solutions), restraints (inadequate reimbursement and high cost of dental services), opportunities (increasing investments in CAD/CAM technologies, growing focus on emerging markets and rising disposable income levels, and increasing demand for same-day dentistry) and challenges (pricing pressure faced by prominent market players, and dearth of skilled lab professionals)

- Market Penetration: It provides detailed information on the product portfolios offered by major players in the global dental consumables market. The report covers various segments, including product types, end users, and regions.

- Product Enhancement/Innovation: Comprehensive details about new product launches and anticipated trends in the global dental consumables market.

- Market Development: Thorough knowledge and analysis of the profitable rising markets by product types, end users, and regions.

- Market Diversification: Comprehensive information about newly launched products and services, expanding markets, current advancements, and investments in the global dental consumables market.

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings of products and services, and capacities of the major competitors in the global dental consumables market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY MARKET PARTICIPANTS: INSIGHTS & DEVELOPMENTS

- 2.2 DISRUPTIVE TRENDS SHAPING MARKET GROWTH

- 2.3 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.4 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DENTAL CONSUMABLES MARKET OVERVIEW

- 3.2 EUROPE: DENTAL CONSUMABLES MARKET, BY END USER AND COUNTRY

- 3.3 DENTAL CONSUMABLES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 DENTAL CONSUMABLES MARKET, BY REGION

- 3.5 DENTAL CONSUMABLES MARKET: DEVELOPED VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing prevalence of dental caries leading to higher demand for tooth restoration procedures

- 4.2.1.2 Growing preference for advanced cosmetic dental treatments

- 4.2.1.3 Expanding dental tourism market in developing nations

- 4.2.1.4 Introduction of innovative and advanced dental solutions

- 4.2.2 RESTRAINTS

- 4.2.2.1 Limited reimbursement policies and high cost associated with dental treatments

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rising funding and adoption of CAD/CAM dental technologies

- 4.2.3.2 Expanding opportunities in emerging markets supported by rising disposable incomes

- 4.2.3.3 Growing popularity of same-day dental treatment services

- 4.2.4 CHALLENGES

- 4.2.4.1 Intense pricing competition among leading market players

- 4.2.4.2 Shortage of qualified and experienced dental laboratory professionals

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER- 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN DENTAL CONSUMABLES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF DENTAL CONSUMABLES, BY TYPE, 2023-2025

- 5.6.2 AVERAGE SELLING PRICE TREND OF DENTAL IMPLANTS, BY COUNTRY, 2023-2025

- 5.7 TRADE ANALYSIS

- 5.8 KEY CONFERENCES & EVENTS, 2026

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFFS ON DENTAL CONSUMABLES MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON REGION

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USER INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 CAD/CAM TECHNOLOGY

- 6.1.2 CARIES DETECTION TECHNOLOGY

- 6.1.3 COMPLEMENTARY TECHNOLOGIES

- 6.1.3.1 Robot dentists and AI

- 6.1.4 ADJACENT TECHNOLOGIES

- 6.1.4.1 Novel biocompatible materials

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.2.1 SHORT-TERM |RECENT TECHNOLOGIES| FOUNDATION & EARLY COMMERCIALIZATION

- 6.2.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.2.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.3 PATENT ANALYSIS

- 6.3.1 PATENT PUBLICATION TRENDS FOR DENTAL CONSUMABLES

- 6.3.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.3.3 TOP APPLICANTS & OWNERS (COMPANIES/INSTITUTIONS) FOR DENTAL CONSUMABLES PATENTS (JANUARY 2015-DECEMBER 2025)

- 6.3.4 TOP APPLICANT COUNTRIES/REGIONS PATENTS FOR DENTAL CONSUMABLES (JANUARY 2015-DECEMBER 2025)

- 6.4 IMPACT OF AI/GEN AI ON DENTAL CONSUMABLES MARKET

- 6.4.1 TOP USE CASES & MARKET POTENTIAL

- 6.4.2 INTERCONNECTED ADJACENT ECOSYSTEMS & IMPACT ON MARKET PLAYERS

- 6.4.3 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN DENTAL CONSUMABLES MARKET

- 6.5 SUCCESS STORIES & REAL-WORLD APPLICATIONS

- 6.5.1 INSTITUT STRAUMANN: AI-DRIVEN DIGITAL WORKFLOW & SMILE DESIGN

- 6.5.2 DENTSPLY SIRONA: AI-POWERED CAD/CAM & SINGLE-VISIT DENTISTRY

- 6.5.3 ENVISTA: AI-ENABLED IMAGE ANALYSIS & DIGITAL WORKFLOW INTEGRATION

7 REGULATORY LANDSCAPE

- 7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 INDUSTRY STANDARDS

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 China

- 7.1.1.3.2 Japan

- 7.1.1.4 Latin America

- 7.1.1.4.1 Brazil

- 7.1.1.4.2 Mexico

- 7.1.1.5 Middle East

- 7.1.1.6 Africa

- 7.1.1.1 North America

- 7.1.1 INDUSTRY STANDARDS

- 7.2 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 INFLUENCE OF KEY STAKEHOLDERS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

9 DENTAL CONSUMABLES MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 DENTAL IMPLANTS

- 9.2.1 TITANIUM IMPLANTS

- 9.2.1.1 High biocompatibility and cost-effectiveness to drive usage in implants

- 9.2.2 ZIRCONIUM IMPLANTS

- 9.2.2.1 Superior esthetics to drive preference for zirconium over titanium implants

- 9.2.1 TITANIUM IMPLANTS

- 9.3 DENTAL RESTORATIONS

- 9.3.1 DIRECT RESTORATIVE MATERIALS

- 9.3.1.1 Amalgams

- 9.3.1.1.1 Presence of mercury in amalgams to restrain market growth

- 9.3.1.2 Composites

- 9.3.1.2.1 Need for minimal tooth preparation and effective bonding to propel growth

- 9.3.1.3 Glass ionomers

- 9.3.1.3.1 Low load-bearing strength to restrain growth

- 9.3.1.4 Other direct restorative materials

- 9.3.1.1 Amalgams

- 9.3.2 INDIRECT RESTORATIVE MATERIALS

- 9.3.2.1 Metals

- 9.3.2.1.1 High durability and fracture resistance to drive demand

- 9.3.2.2 Ceramics

- 9.3.2.2.1 Appeal and translucency to propel adoption

- 9.3.2.3 Other indirect restorative materials

- 9.3.2.1 Metals

- 9.3.3 DENTAL BIOMATERIALS

- 9.3.3.1 Dental bone grafts & substitutes

- 9.3.3.1.1 Growing number of dental implant procedures to drive market

- 9.3.3.2 Dental membranes

- 9.3.3.2.1 Growing procedural volumes to drive market

- 9.3.3.3 Tissue regenerative materials

- 9.3.3.3.1 Rising number of cosmetic dentistry procedures to support segment growth

- 9.3.3.1 Dental bone grafts & substitutes

- 9.3.1 DIRECT RESTORATIVE MATERIALS

- 9.4 ORTHODONTICS

- 9.4.1 CLEAR ALIGNERS/REMOVABLE BRACES

- 9.4.1.1 Esthetic concerns among teens and adults to drive adoption

- 9.4.2 FIXED BRACES

- 9.4.2.1 Brackets

- 9.4.2.1.1 Advancements in orthodontic brackets to support market growth

- 9.4.2.2 Archwires

- 9.4.2.2.1 Increasing number of orthodontic procedures to drive growth

- 9.4.2.3 Anchorage appliances

- 9.4.2.3.1 Huge patient population base with malocclusions and jaw diseases to propel market growth

- 9.4.2.4 Ligatures

- 9.4.2.4.1 Advantages such as low cost, ease of use, and comfort to increased adoption of ligatures

- 9.4.2.1 Brackets

- 9.4.3 ACCESSORIES

- 9.4.3.1 Increasing number of orthodontic procedures to support demand for accessories

- 9.4.1 CLEAR ALIGNERS/REMOVABLE BRACES

- 9.5 PERIODONTICS

- 9.5.1 DENTAL ANESTHETICS

- 9.5.1.1 Injectable anesthetics

- 9.5.1.1.1 Safety and efficacy to drive the market

- 9.5.1.2 Topical anesthetics

- 9.5.1.2.1 Rising volume of pediatric dental procedures to boost usage

- 9.5.1.1 Injectable anesthetics

- 9.5.2 DENTAL HEMOSTATS

- 9.5.2.1 Oxidized regenerated cellulose-based hemostats

- 9.5.2.1.1 Superior hemostasis and bactericidal effectiveness during surgical procedures to propel demand

- 9.5.2.2 Gelatin-based hemostats

- 9.5.2.2.1 Innovations in gelatin-based hemostats to support market growth

- 9.5.2.3 Collagen-based hemostats

- 9.5.2.3.1 Reduced blood loss and effectiveness to support adoption

- 9.5.2.1 Oxidized regenerated cellulose-based hemostats

- 9.5.3 DENTAL SUTURES

- 9.5.3.1 Non-absorbable dental sutures

- 9.5.3.1.1 Possibility of discomfort during removal to restrain adoption

- 9.5.3.2 Absorbable dental sutures

- 9.5.3.2.1 Great tensile strength and high comfort for patients to promote growth

- 9.5.3.1 Non-absorbable dental sutures

- 9.5.1 DENTAL ANESTHETICS

- 9.6 INFECTION CONTROL PRODUCTS

- 9.6.1 SANITIZING GELS

- 9.6.1.1 Sanitizing gels to hold largest market share

- 9.6.2 PERSONAL PROTECTIVE WEAR

- 9.6.2.1 Government mandates for using personal protective wear to support segment growth

- 9.6.3 DISINFECTANTS

- 9.6.3.1 Emphasis on environmental disinfection in dental settings to support growth

- 9.6.1 SANITIZING GELS

- 9.7 ENDODONTICS

- 9.7.1 SHAPING & CLEANING CONSUMABLES

- 9.7.1.1 Importance of shaping & cleaning consumables in root canal treatment to propel adoption

- 9.7.2 OBTURATION CONSUMABLES

- 9.7.2.1 Increasing root canal procedures to drive demand

- 9.7.3 ACCESS PREPARATION CONSUMABLES

- 9.7.3.1 Growing demand for access preparation consumables in endodontic treatment to drive market

- 9.7.1 SHAPING & CLEANING CONSUMABLES

- 9.8 WHITENING PRODUCTS

- 9.8.1 IN-OFFICE WHITENING CONSUMABLES

- 9.8.1.1 Gels

- 9.8.1.1.1 Safety and effectiveness of gels to drive market growth

- 9.8.1.2 Resin barriers

- 9.8.1.2.1 Easy application and no patient discomfort to propel usage

- 9.8.1.3 Other in-office whitening consumables

- 9.8.1.1 Gels

- 9.8.2 TAKE-HOME WHITENING CONSUMABLES

- 9.8.2.1 Whitening trays

- 9.8.2.1.1 Lower effectiveness than other modes to restrain market growth

- 9.8.2.2 Pens

- 9.8.2.2.1 Convenience to support adoption

- 9.8.2.3 Pocket trays

- 9.8.2.3.1 Regular intake of tobacco and tannin-containing products to boost adoption

- 9.8.2.4 Other take-home whitening consumables

- 9.8.2.1 Whitening trays

- 9.8.1 IN-OFFICE WHITENING CONSUMABLES

- 9.9 FINISHING & POLISHING PRODUCTS

- 9.9.1 PROPHYLAXIS PRODUCTS

- 9.9.1.1 Pastes

- 9.9.1.1.1 High dental polishing procedure volumes to drive demand for pastes

- 9.9.1.2 Disposable agents

- 9.9.1.2.1 Greater flexibility in polishing and finishing to boost usage

- 9.9.1.3 Cups

- 9.9.1.3.1 High flexibility and stability to drive adoption

- 9.9.1.4 Brushes

- 9.9.1.4.1 Durability and ease of use to propel market

- 9.9.1.1 Pastes

- 9.9.2 FLUORIDES

- 9.9.2.1 Varnishes

- 9.9.2.1.1 Effective protection against tooth decay to boost adoption

- 9.9.2.2 Rinses

- 9.9.2.2.1 Product development efforts to drive launch of innovative offerings

- 9.9.2.3 Topical gels/oral solutions

- 9.9.2.3.1 Highly acidic nature of fluoride gels to hinder growth

- 9.9.2.4 Foams

- 9.9.2.4.1 Reduced risk of dulling and etching of restorations to propel growth

- 9.9.2.5 Trays

- 9.9.2.5.1 Rising awareness on reducing risk of caries to drive market

- 9.9.2.1 Varnishes

- 9.9.1 PROPHYLAXIS PRODUCTS

- 9.10 OTHER DENTAL CONSUMABLES

- 9.10.1 DENTAL SPLINTS

- 9.10.1.1 Rising treatment of occlusion-related disorders to propel market

- 9.10.2 DENTAL SEALANTS

- 9.10.2.1 Growing popularity and usage to support segment growth

- 9.10.3 DENTAL IMPRESSION MATERIALS

- 9.10.3.1 Frequent, repetitive usage in dental hospitals & clinics to ensure sustained demand

- 9.10.4 BONDING AGENTS/ADHESIVES

- 9.10.4.1 Applications in bonding direct and indirect restorative materials to drive market

- 9.10.5 OTHER CONSUMABLES

- 9.10.1 DENTAL SPLINTS

10 DENTAL CONSUMABLES MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 DENTAL HOSPITALS & CLINICS

- 10.2.1 RISING NUMBER OF DENTAL HOSPITALS & CLINICS IN EMERGING MARKETS TO DRIVE MARKET GROWTH

- 10.3 DENTAL LABORATORIES

- 10.3.1 INCREASING INTEREST IN COSMETIC DENTISTRY TO PROPEL MARKET GROWTH

- 10.4 DENTAL SERVICE ORGANIZATIONS

- 10.5 OTHER END USERS

11 DENTAL CONSUMABLES MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 EUROPE

- 11.2.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 11.2.2 GERMANY

- 11.2.2.1 Favorable government policies to drive demand for dental consumables

- 11.2.3 ITALY

- 11.2.3.1 Low-cost treatment and growing penetration of dental products to drive market

- 11.2.4 SPAIN

- 11.2.4.1 Increasing demand for cosmetic dentistry and growing medical tourism drive demand

- 11.2.5 FRANCE

- 11.2.5.1 Favorable government healthcare strategies to fuel market growth

- 11.2.6 UK

- 11.2.6.1 Increasing incidence of dental disorders to drive demand for dental consumables

- 11.2.7 REST OF EUROPE

- 11.3 NORTH AMERICA

- 11.3.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 11.3.2 US

- 11.3.2.1 US to dominate North American dental consumables market

- 11.3.3 CANADA

- 11.3.3.1 Rising incidence of dental caries to drive demand for dental consumables

- 11.4 ASIA PACIFIC

- 11.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 11.4.2 JAPAN

- 11.4.2.1 Rising geriatric population and favorable reimbursement to support market growth

- 11.4.3 AUSTRALIA

- 11.4.3.1 Increasing incidence of dental disorders to drive demand for dental consumables

- 11.4.4 SOUTH KOREA

- 11.4.4.1 High penetration of dental implants to drive market in South Korea

- 11.4.5 CHINA

- 11.4.5.1 Growing prevalence of dental diseases to drive market

- 11.4.6 INDIA

- 11.4.6.1 India to offer lucrative growth opportunities for market players

- 11.4.7 REST OF ASIA PACIFIC

- 11.5 LATIN AMERICA

- 11.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 11.5.2 BRAZIL

- 11.5.2.1 Rising investments in R&D and growing popularity of 3D dental printing to promote market growth

- 11.5.3 MEXICO

- 11.5.3.1 Focus on improving healthcare infrastructure and availability of skilled dentists to drive the market

- 11.5.4 ARGENTINA

- 11.5.4.1 Growing demand for personalized dentistry to drive market

- 11.5.5 REST OF LATIN AMERICA

- 11.6 MIDDLE EAST & AFRICA

- 11.6.1 GROWING AWARENESS ABOUT DENTAL HYGIENE TO DRIVE MARKET GROWTH

- 11.6.2 MACROECONOMIC OUTLOOK FOR THE MIDDLE EAST & AFRICA

- 11.7 GCC COUNTRIES

- 11.7.1 RISING NUMBER OF CONFERENCES, SUMMITS AND TRAINING COURSES

- 11.7.2 MACROECONOMIC OUTLOOK FOR GCC COUNTRIES

12 COMPETITIVE LANDSCAPE

- 12.1 INTRODUCTION

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.2.1 OVERVIEW OF MAJOR STRATEGIES ADOPTED BY KEY PLAYERS IN DENTAL CONSUMABLES MARKET

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product footprint

- 12.5.5.4 End-user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 COMPANY VALUATION & FINANCIAL METRICS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 R&D EXPENDITURE OF KEY PLAYERS

- 12.10 COMPETITIVE SCENARIO

- 12.10.1 PRODUCT LAUNCHES

- 12.10.2 DEALS

- 12.10.3 EXPANSIONS

- 12.10.4 OTHER DEVELOPMENTS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 INSTITUT STRAUMANN AG

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 ENVISTA

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches & approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 DENTSPLY SIRONA

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 SOLVENTUM

- 13.1.4.1 Business overview

- 13.1.4.2 Products offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 ZIMVIE INC.

- 13.1.5.1 Business overview

- 13.1.5.2 Products offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.6 HENRY SCHEIN

- 13.1.6.1 Business overview

- 13.1.6.2 Products offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.3.4 Other developments

- 13.1.7 KURARAY CO., LTD.

- 13.1.7.1 Business overview

- 13.1.7.2 Products offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.3.2 Expansions

- 13.1.8 MITSUI CHEMICALS, INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 DEALS

- 13.1.9 SHOFU

- 13.1.9.1 Business overview

- 13.1.9.2 Products offered

- 13.1.10 IVOCLAR VIVADENT AG

- 13.1.10.1 Business overview

- 13.1.10.2 Products offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Product launches

- 13.1.10.3.2 Deals

- 13.1.1 INSTITUT STRAUMANN AG

- 13.2 OTHER PLAYERS

- 13.2.1 GC CORPORATION

- 13.2.2 KEYSTONE DENTAL GROUP

- 13.2.3 BEGO GMBH & CO. KG

- 13.2.4 SEPTODONT HOLDING

- 13.2.5 ULTRADENT PRODUCTS

- 13.2.6 VOCO GMBH

- 13.2.7 COLTENE GROUP

- 13.2.8 SDI LIMITED

- 13.2.9 YOUNG INNOVATIONS, INC.

- 13.2.10 DMG CHEMISCH-PHARMAZEUTISCHE FABRIK GMBH

- 13.2.11 BRASSELER USA

- 13.2.12 GEISTLICH PHARMA AG

- 13.2.13 GLIDEWELL

- 13.2.14 BISCO INC.

- 13.2.15 DENTAL TECHNOLOGIES INC.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 14.4 MARKET SHARE ESTIMATION

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RESEARCH LIMITATIONS

- 14.6.1 SCOPE-RELATED LIMITATIONS

- 14.6.2 METHODOLOGY-RELATED LIMITATIONS

- 14.7 RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS