|

시장보고서

상품코드

2033998

ADAS 시장 : PC/LCV/HCV 시스템 유형별, 제공 유형별, 자율주행 레벨별, 안전 용도별, EV 유형별, 지역별 - 세계 예측(-2033년)ADAS market by PC, LCV, HCV System Type (ACC, AEB, LDW, BSD), Offering Type [Hardware (Camera, Radar, LiDAR) and Software], LOA (L1, L2, L3, L4, L5), Safety Application (OCS, DashCam), EV Type, and Region - Global Forecast to 2033 |

||||||

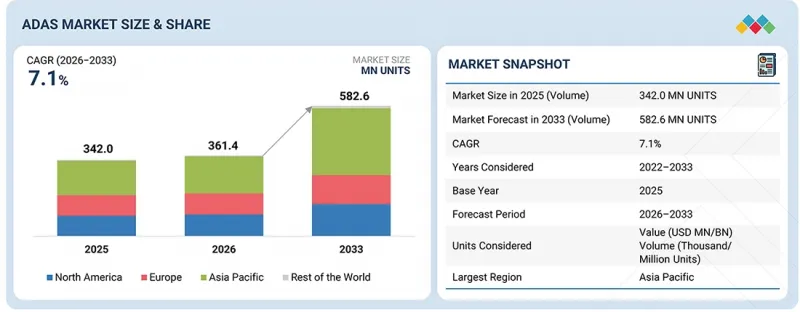

세계의 ADAS 시장 규모는 2026년 3억 6,140만 대에서 2033년까지 5억 8,260만 대에 달할 것으로 예측되며, CAGR로 7.1%의 성장이 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 1,000대, 100만 달러 |

| 부문 | 자동차 시스템, 제공 유형, LOA, 안전 용도, EV 유형, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 기타 지역 |

ADAS 시장은 사용자 친화적인 인터페이스, OTA 업데이트, 데이터 분석에 중점을 두고 장기적으로 시스템 성능을 향상시키기 위해 소프트웨어 중심의 혁신으로 전환하고 있습니다. 엣지 컴퓨팅의 발전으로 카메라와 센서가 로컬에서 데이터를 처리할 수 있게 되면서 통신 환경이 불안정한 지역에서도 보다 빠른 의사결정과 안정적인 작동이 가능해졌습니다. 또한 AI, 머신러닝, IoT, 빅데이터 등 기술의 통합으로 보다 지능적이고 적응력이 높은 시스템 개발이 촉진되고 있습니다. 안전 규제 강화와 안전한 운송 수단에 대한 수요 증가에 따라 ADAS가 운전자의 안전성 향상과 사고 감소에 기여함에 따라 상용차 부문도 성장이 예상됩니다.

2033년

2033년초음파 센서가 예측 기간 동안 ADAS 시장을 주도할 것으로 예상됩니다.

초음파 센서는 기본적인 주차 보조에서 사각지대감지, 차선 변경 지원, 운전자 모니터링 등 보다 복잡한 기능으로 진화하고 있습니다. 이러한 발전은 센서의 정확도 향상, 소형화, 다른 차량 시스템과의 통합을 통해 현대 자동차의 안전 기능을 강화할 수 있도록 지원하고 있습니다. 이 센서는 일반적으로 앞뒤 범퍼에 장착되어 주변 차량과 장애물을 감지하고 최대 3미터 범위 내에서 효과적으로 작동할 수 있습니다. 단, 비스듬히 위치한 물체 감지 및 신호 간섭의 영향으로 성능에 한계가 발생할 수 있습니다. 이러한 문제에도 불구하고 초음파 센서는 모든 기상 조건에서 안정적으로 작동합니다. Robert Bosch GmbH, Denso Corporation, Valeo 등의 기업이 주요 OEM에 초음파 센서를 공급하고 있습니다. 예를 들어, Robert Bosch GmbH는 BMW AG의 2026 M2/M3 모델에 초음파 센서를 공급하고, Denso Corporation은 Toyota Corporation의 2026 Land Cruiser 300, Prius, Sienta 모델에 초음파 센서를 공급했습니다.

배터리 전기자동차(BEV)가 예측 기간 동안 ADAS 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.

배터리 전기자동차(BEV)는 중앙집중식 소프트웨어 정의 전기/전자(E/E) 아키텍처를 기반으로 구축되어 첨단 ADAS 기능과 고속 통신 네트워크의 원활한 통합을 가능하게 합니다. 자동차 제조사들은 BEV를 기술 중심의 차량으로 포지셔닝하고 있으며, AEB, ACC, 하이웨이 어시스트와 같은 ADAS 기능을 표준 또는 구독 기반 기능으로 제공하는 경우가 많습니다. 이들 차량은 센서 융합과 실시간 처리를 지원하는 고성능 컴퓨팅 플랫폼과 도메인/존 컨트롤러를 채택하고 있습니다. BEV는 ICE 차량과 달리 기존의 설계 제약이 없기 때문에 카메라, 레이더, LiDAR를 포함한 확장 가능한 센서 구성을 쉽게 통합할 수 있습니다. 또한, BEV는 OTA 업데이트 친화성이 높아 차량 판매 이후에도 ADAS 기능을 지속적으로 개선할 수 있습니다. 차량 안전에 대한 규제 당국의 관심 증가와 지능형 커넥티드 자동차에 대한 소비자 수요 증가는 BEV의 ADAS 채택을 더욱 촉진하고 있습니다. 또한, 레이더 및 LiDAR와 결합된 딥러닝 기반 비전 시스템을 채택하여 AEB와 같은 ADAS 기능의 정확도와 전반적인 성능을 향상시키고 있습니다. BMW, BYD, Mercedes-Benz, Audi 등의 OEM은 첨단 안전기능과 운전지원 기능을 갖춘 전기자동차를 출시하고 있습니다. 예를 들어, 2026년 4월, Chery는 Exeed EX7을 출시했습니다. 이 모델에는 지능형 주행에 사용되는 장거리 고정밀 LiDAR 및 밀리미터파 레이더를 포함한 27개의 고성능 센서와 Nvidia Orin-Y 칩이 탑재되어 있습니다. 앞서 언급한 모든 요인들이 BEV의 ADAS 채택을 촉진하고 있습니다.

세계의 ADAS 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 승용차용 ADAS 시장 : 시스템 유형별

제10장 소형 상용차용 ADAS 시장 : 시스템 유형별

제11장 대형 상용차용 ADAS 시장 : 시스템 유형별

제12장 ADAS 시장 : 전기자동차 유형별

제13장 ADAS 시장 : 자율주행 레벨별

제14장 ADAS 시장, 제공 유형

제15장 ADAS 시장 : 안전 용도별

제16장 ADAS 시장 : 지역별

제17장 경쟁 구도

제18장 기업 개요

제19장 조사 방법

제20장 부록

KSMThe ADAS market is projected to grow from 361.4 million units in 2026 to 582.6 million units by 2033, at a CAGR of 7.1%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Volume (Thousand Units) and Value (USD Million) |

| Segments | Car Sysytem, Offering Type, LOA, Safety Application, EV Type, and Region |

| Regions covered | Asia Pacific, Europe, North America, and Rest of the World |

The ADAS market is shifting toward software-driven innovation, with a focus on user-friendly interfaces, over-the-air updates, and data analytics to improve system performance over time. Advancements in edge computing enable cameras and sensors to process data locally, allowing faster decision-making and reliable operation even in low-connectivity areas. In addition, the integration of technologies such as AI, machine learning, IoT, and big data is supporting the development of more intelligent and adaptive systems. With stricter safety regulations and increasing demand for safer transportation, the commercial vehicle segment is also expected to grow, as ADAS helps improve driver safety and reduce accidents.

Ultrasonic sensors are projected to lead the ADAS market during the forecast period.

![ADAS market by PC, LCV, HCV System Type (ACC, AEB, LDW, BSD), Offering Type [Hardware (Camera, Radar, LiDAR) and Software], LOA (L1, L2, L3, L4, L5), Safety Application (OCS, DashCam), EV Type, and Region - Global Forecast to 2033](https://www.giiresearch.com/sample/img/MAMA2033998-f1.webp)

Ultrasonic sensors have advanced from basic parking assistance to more complex functions such as blind spot detection, lane change assistance, and driver monitoring. This development is supported by improvements in sensor accuracy, miniaturization, and integration with other vehicle systems, enabling enhanced safety features in modern vehicles. These sensors are typically installed in the front and rear bumpers to detect nearby vehicles or obstacles and perform effectively within a range of up to 3 meters. However, they may face limitations when detecting angled objects or due to signal interference. Despite these challenges, ultrasonic sensors function reliably in all weather conditions. Companies such as Robert Bosch GmbH, Denso Corporation, and Valeo supply ultrasonic sensors to major OEMs. For instance, Robert Bosch GmbH supplied ultrasonic sensors to BMW AG for its 2026 M2 and M3 models, while Denso Corporation supplied them to Toyota Corporation for its 2026 Land Cruiser 300, Prius, and Sienta models.

The battery electric vehicle (BEV) is projected to hold the largest share of the ADAS market during the forecast period.

Battery electric vehicles (BEVs) are built on centralized and software-defined electrical/electronic (E/E) architectures, which enable seamless integration of advanced ADAS features and high-speed communication networks. Automakers position BEVs as technology-focused vehicles, often offering ADAS functions such as AEB, ACC, and highway assist as standard or subscription-based features. These vehicles use high-performance computing platforms and domain or zonal controllers that support sensor fusion and real-time processing. Unlike ICE vehicles, BEVs do not have legacy design constraints, allowing easier integration of scalable sensor setups, including cameras, radar, and LiDAR. In addition, BEVs are well aligned with OTA updates, enabling continuous improvement of ADAS features after the vehicle is sold. The growing regulatory focus on vehicle safety and increasing consumer demand for intelligent and connected vehicles are further driving ADAS adoption in BEVs. Moreover, the use of deep learning-based vision systems combined with radar and LiDAR is improving the accuracy and overall performance of ADAS functions such as AEB. OEMs such as BMW, BYD, Mercedes-Benz, and Audi are introducing electric vehicles with advanced safety and driver-assistance features. For instance, in April 2026, Chery launched the Exeed EX7, which is equipped with 27 high-performance sensors and an Nvidia Orin-Y chip, including long-range high-precision LiDAR and millimeter-wave radar for intelligent driving. All the aforementioned factors are driving the adoption of ADAS in BEVs.

"Europe is expected to have a significant market share in the ADAS market during the forecast period."

Europe is expected to hold a significant share of the ADAS market during the forecast period. Strict emission regulations and zero-emission targets are influencing manufacturers of both passenger and commercial vehicles. Market growth is supported by advancements in driver assistance features such as traffic jam assist and blind spot detection with rear cross-traffic alert. From July 7, 2024, the second phase of the EU General Safety Regulation II (GSR II) requires all new vehicles to comply with stricter safety standards. This includes mandatory systems such as Advanced Emergency Braking System (AEBS), Emergency Lane Keeping System (ELKS), Emergency Stop Signal (ESS), Intelligent Speed Assistance (ISA), Driver Drowsiness and Attention Warning (DDAW), Reversing Detection (REV), and Event Data Recorder (EDR). For buses and heavy commercial vehicles, additional systems such as Blind Spot Information System (BSIS), Moving Off Information System (MOIS), and Tire Pressure Monitoring System (TPMS) are also required. In addition, the increasing shift toward electric vehicles, along with rising road safety concerns and greater consumer awareness, is expected to further drive the demand for ADAS in the region.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: Tier I - 24%, Tier II - 67%, and Tier III - 9%

- By Designation: C-Level - 33%, Managers - 52%, and Executives - 15%

- By Region: North America - 26%, Europe - 30%, Asia Pacific - 35%, and RoW - 9%

The ADAS market is dominated by major players, including Robert Bosch GmbH (Germany), Aumovio SE (Germany), ZF Friedrichshafen AG (Germany), Denso Corporation (Japan), and Magna International Inc. (Canada). These companies offer advanced, integrated ADAS solutions that enhance vehicle safety, enable higher levels of automation, and meet evolving regulatory and consumer demands.

Research Coverage:

The report covers the ADAS market in terms of PC, LCV, HCV system type (ACC, AEB, LDW, BSD & Others), offering type [hardware (camera, radar, LiDAR & others) and software], LOA (L1, L2, L3, L4, L5), safety application (OCS, DashCam), EV type, and Region. It covers the competitive landscape and company profiles of the major ADAS market ecosystem players.

The study also includes an in-depth competitive analysis of the key market players, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall ADAS market and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies.

- The report will help stakeholders understand the market pulse and provide information on key market drivers, restraints, challenges, and opportunities.

- The report will also help stakeholders understand the current and future pricing trends of the ADAS market.

The report provides insights into the following pointers:

- Analysis of key drivers (rising demand for enhanced vehicle safety and driving comfort through ADAS, increasing regulatory mandates and safety standard compliance), restraints (infrastructure gaps limiting effective deployment of ADAS and autonomous systems, consumer trust and acceptance challenges for autonomous vehicle technologies), opportunities (advancements in autonomous driving technologies enabling next-generation ADAS capabilities, EV-driven innovation accelerating enhanced safety and user experience integration), and challenges (high integration costs and system complexity limiting ADAS adoption, sensor reliability and performance constraints impacting ADAS effectiveness)

- Product Development/Innovation: Detailed insights into upcoming technologies and research & development activities in the ADAS market

- Market Development: Comprehensive information about lucrative markets (the report analyzes the ADAS market across varied regions)

- Market Diversification: Exhaustive information about untapped geographies, recent developments, and investments in the ADAS market

- Competitive Assessment: In-depth assessment of market share, growth strategies, and product offerings of leading players like Robert Bosch GmbH (Germany), Aumovio SE (Germany), ZF Friedrichshafen AG (Germany), Denso Corporation (Japan), Magna International Inc. (Canada), among others, in the ADAS market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS & MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING ADAS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ADAS MARKET

- 3.2 ADAS MARKET, BY LEVEL OF AUTONOMY

- 3.3 ADAS MARKET, BY PASSENGER CAR SYSTEM TYPE

- 3.4 ADAS MARKET, BY LIGHT COMMERCIAL VEHICLE SYSTEM TYPE

- 3.5 ADAS MARKET, BY HEAVY COMMERCIAL VEHICLE SYSTEM TYPE

- 3.6 ADAS MARKET, BY ELECTRIC VEHICLE TYPE

- 3.7 ADAS MARKET, BY OFFERING TYPE

- 3.8 ADAS MARKET, BY SAFETY APPLICATION

- 3.9 ADAS MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising demand for enhanced vehicle safety and driving comfort through ADAS

- 4.2.1.2 Increasing regulatory mandates and safety standard compliance

- 4.2.2 RESTRAINTS

- 4.2.2.1 Infrastructure gaps limiting effective deployment of ADAS and autonomous systems

- 4.2.2.2 Consumer trust and acceptance challenges for autonomous vehicle technologies

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Advancements in autonomous driving technologies enabling next-generation ADAS capabilities

- 4.2.3.2 EV-driven innovation accelerating enhanced safety and user experience integration

- 4.2.4 CHALLENGES

- 4.2.4.1 High integration costs and system complexity limiting ADAS adoption

- 4.2.4.2 Sensor reliability and performance constraints impacting ADAS effectiveness

- 4.2.5 IMPACT ANALYSIS OF MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ADAS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL ADAS MARKET

- 5.1.3 TRENDS IN GLOBAL AUTONOMOUS VEHICLE INDUSTRY

- 5.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3 PRICING ANALYSIS

- 5.3.1 AVERAGE SELLING PRICE TREND OF CAMERA UNITS, BY REGION, 2023-2025

- 5.3.2 AVERAGE SELLING PRICE TREND OF LIDARS, BY REGION, 2023-2025

- 5.3.3 AVERAGE SELLING PRICE TREND OF RADAR SENSORS, BY REGION, 2023-2025

- 5.3.4 AVERAGE SELLING PRICE TREND OF ULTRASONIC SENSORS, BY REGION, 2023-2025

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 OEMS

- 5.4.2 TIER 1 SUPPLIERS

- 5.4.3 AUTONOMOUS VEHICLE DEVELOPERS

- 5.4.4 SOFTWARE AND SYSTEMS PROVIDERS

- 5.4.5 LIDAR SYSTEM PROVIDERS

- 5.4.6 RADAR SYSTEM PROVIDERS

- 5.4.7 CAMERA SUPPLIERS

- 5.4.8 PROCESSOR (SOC) MANUFACTURERS

- 5.4.9 SENSOR COMPONENT SUPPLIERS

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.6 CASE STUDY ANALYSIS

- 5.6.1 ACCELERATING AUTONOMOUS DRIVING WITH ADVANCED ADAS SOLUTIONS

- 5.6.2 ACCELERATING SAFE AND SCALABLE ADAS DEVELOPMENT WITH EDGE-CENTRIC DATA MANAGEMENT

- 5.6.3 SCENARIO-BASED TESTING VALIDATION FOR ADS/ADAS

- 5.6.4 KONRAD TECHNOLOGIES TO CONDUCT ADAS SENSOR PACKAGE AND RELIABILITY TEST

- 5.6.5 NVIDIA TO PROVIDE OPEN AV DEVELOPMENT PLATFORM FOR AUTONOMOUS VEHICLES

- 5.6.6 ZF TO RELEASE NEW AI-BASED SERVICES FOR ADAS

- 5.6.7 RENESAS TO BOOST DEEP LEARNING DEVELOPMENT FOR ADAS AND AUTOMATED DRIVING APPLICATIONS

- 5.6.8 MERCEDES-BENZ USED ANSYS OPTISLANG FOR ADAS VALIDATION THROUGH RELIABLE ANALYSIS

- 5.7 INVESTMENT AND FUNDING SCENARIO

- 5.8 SUPPLIER ANALYSIS

- 5.8.1 ADAS SUPPLIERS, BY KEY OEMS

- 5.8.2 RADAR (MILLIMETER WAVE RADAR, LIDAR, AND OTHERS), BY KEY OEMS

- 5.8.3 CAMERA, BY KEY OEMS

- 5.8.4 PARKING ASSIST, BY KEY OEMS

- 5.8.5 VEHICLE-APPROACH NOTICE CONTROL UNIT, BY KEY OEMS

- 5.8.6 CRUISE CONTROL, BY KEY OEMS

- 5.8.7 DRIVER MONITORING SYSTEM, BY KEY OEMS

- 5.8.8 HIGH-DEFINITION MAP, BY KEY OEMS

- 5.8.9 LANE DEPARTURE WARNING SYSTEM, BY KEY OEMS

- 5.8.10 TIRE PRESSURE MONITORING SYSTEM, BY KEY OEMS

- 5.8.11 ADAS OFFERINGS BY KEY PLAYERS

- 5.8.11.1 Tesla

- 5.8.11.2 Toyota Motor Corporation

- 5.8.11.2.1 Corolla

- 5.8.11.2.2 Camry

- 5.8.11.2.3 RAV4

- 5.8.11.2.4 Tundra

- 5.8.11.3 Nissan Motor Co., Ltd.

- 5.8.11.3.1 Versa

- 5.8.11.3.2 Altima

- 5.8.11.3.3 Nissan Leaf

- 5.8.11.4 Mercedes-Benz

- 5.8.11.4.1 S-Class Sedan

- 5.8.11.4.2 C-Class Sedan

- 5.8.11.4.3 E-Class Sedan

- 5.8.11.5 Audi

- 5.8.11.5.1 A3 Sedan

- 5.8.11.5.2 A6 Sedan

- 5.9 SEMIAUTONOMOUS AND AUTONOMOUS VEHICLE DEVELOPMENT AND DEPLOYMENT

- 5.9.1 LEVEL 3

- 5.9.2 LEVEL 4 AND LEVEL 5

- 5.9.2.1 Global ADAS and autonomous driving deployments by key regions

- 5.9.2.2 Baidu

- 5.9.2.3 DiDi

- 5.9.2.4 Pony.ai and Hyundai

- 5.9.2.5 Waymo

- 5.9.2.6 Volvo

- 5.9.2.7 Einride

- 5.9.3 KEY DISTINCTIONS BETWEEN LEVEL 2/LEVEL 3 AND LEVEL 4 AUTONOMOUS DRIVING STACKS

- 5.9.4 ADVANCEMENT TO LEVEL 4 IN MOBILITY & TRUCKING

- 5.10 TRADE ANALYSIS

- 5.10.1 IMPORT DATA

- 5.10.2 EXPORT DATA

- 5.11 UNLOCKING NEW REVENUE STREAMS: SUBSCRIPTION-DRIVEN ADAS SERVICES IN SOFTWARE-DEFINED VEHICLES

- 5.12 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.13 MNM INSIGHTS INTO HIGH-PERFORMANCE CHIPS POWERING NEXT-GEN ADAS AND AUTONOMY

- 5.14 IMPACT OF ISRAEL-IRAN WAR

- 5.14.1 INTRODUCTION

- 5.14.2 ENERGY MARKET DISRUPTION

- 5.14.3 OPERATING COST IMPACT

- 5.14.4 MARKET DEMAND SHIFT

- 5.14.5 SUPPLY CHAIN AND LOCALIZATION IMPACT

- 5.14.6 STRATEGIC MARKET OUTLOOK

- 5.15 EU-INDIA TRADE DEAL IMPACT ANALYSIS

- 5.15.1 INTRODUCTION

- 5.15.2 EU TARIFFS

- 5.15.3 IMPORTS TO INDIA

- 5.15.4 EXPORTS FROM INDIA

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 PATENT ANALYSIS

- 6.2 TECHNOLOGY ANALYSIS

- 6.2.1 INTRODUCTION

- 6.2.2 KEY TECHNOLOGIES

- 6.2.2.1 Cockpit-ADAS integration platform for centralized vehicle computing

- 6.2.2.2 Precision localization system for assisted and automated driving

- 6.2.2.3 Software-based video perception system for driving and parking automation

- 6.2.3 COMPLEMENTARY TECHNOLOGIES

- 6.2.3.1 Cooperative adaptive cruise control

- 6.2.3.2 Autonomous vehicles: Cybersecurity and data privacy

- 6.2.3.3 Vehicle-to-Everything (V2X) Communication

- 6.2.3.3.1 Vehicle-to-cloud (V2C)

- 6.2.3.3.2 Vehicle-to-pedestrian (V2P)

- 6.2.3.3.3 Vehicle-to-infrastructure (V2I)

- 6.2.3.3.4 Vehicle-to-vehicle (V2V)

- 6.2.3.3.5 Cellular V2X

- 6.2.3.3.5.1 LTE-V2X

- 6.2.3.3.5.2 5G-V2X

- 6.2.4 ADJACENT TECHNOLOGIES

- 6.2.4.1 Automated vehicles are reshaping ride-hailing

- 6.2.4.1.1 Impact of automation L2 on ride-hailing

- 6.2.4.1.2 Impact of automation L3 on ride-hailing

- 6.2.4.1.3 Impact of automation L4/L5 on ride-hailing

- 6.2.4.1 Automated vehicles are reshaping ride-hailing

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2026-2027): FOUNDATION AND EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2030): EXPANSION AND STANDARDIZATION

- 6.3.3 LONG-TERM (2031-2035+): MASS COMMERCIALIZATION AND DISRUPTION

- 6.4 IMPACT OF AI/GENERATIVE AI

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.1.1 AI and Generative AI capabilities

- 6.4.1.2 AI for ADAS in practice

- 6.4.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS

- 6.4.2.1 Safety standards & validation

- 6.4.2.2 Regulatory compliance

- 6.4.2.3 Data governance & privacy

- 6.4.2.4 Compute architecture & deployment

- 6.4.2.5 Over-the-air updates

- 6.4.3 CASE STUDIES RELATED TO AI IMPLEMENTATION

- 6.4.3.1 Accelerating ADAS safety validation using Generative AI and simulation

- 6.4.3.2 Scalable and cost-efficient ADAS deployment with AI-driven Gen6 platform

- 6.4.3.3 Accelerating ADAS deployment with a pre-integrated AI and SoC platform

- 6.4.3.4 Scaling advanced ADAS in India with a single-chip AI platform

- 6.4.4 INTERCONNECTED ECOSYSTEM AND IMPACT OF MARKET PLAYERS

- 6.4.5 CLIENTS' READINESS TO ADOPT AI

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1.1 North America

- 7.1.1.2 Europe

- 7.1.1.3 Asia Pacific

- 7.1.2 KEY REGULATIONS

- 7.1.2.1 ADAS Regulations and Initiatives

- 7.1.2.2 NCAP Regulations

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS

- 7.2.1.1 Lifecycle vs. operation

- 7.2.1.2 Eco applications

- 7.2.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.2.2.1 European Union

- 7.2.2.2 US

- 7.2.2.3 China

- 7.2.2.4 India

- 7.2.3 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

- 7.2.3.1 Type I Ecolabels (ISO 14024)

- 7.2.3.2 Product Carbon Footprint (ISO 14067)

- 7.2.3.3 EcoDesign and Material Standards (IEC 62430)

- 7.2.3.4 Hazardous Substance Restrictions (RoHS/REACH)

- 7.2.3.5 Circular Economy & Recycling Certification

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

9 PASSENGER CAR ADAS MARKET, BY SYSTEM TYPE

- 9.1 INTRODUCTION

- 9.2 ADAPTIVE CRUISE CONTROL (ACC)

- 9.2.1 OEMS BUNDLING ACC WITH LANE-CENTERING FEATURES TO DRIVE GROWTH

- 9.3 ADAPTIVE FRONT LIGHTS (AFL)

- 9.3.1 RISING ADOPTION OF LED AND MATRIX LIGHTING SYSTEMS TO DRIVE GROWTH

- 9.4 AUTOMATIC EMERGENCY BRAKING (AEB)

- 9.4.1 REGULATORY MANDATES FOR AEB ACROSS MAJOR COUNTRIES TO DRIVE GROWTH

- 9.5 BLIND SPOT DETECTION (BSD)

- 9.5.1 HIGH TWO-WHEELER AND MIXED-TRAFFIC DENSITY IN URBAN ENVIRONMENTS TO DRIVE GROWTH

- 9.6 CROSS TRAFFIC ALERT (CTA)

- 9.6.1 LIMITED REAR VISIBILITY IN SUVS AND CROSSOVERS TO DRIVE GROWTH

- 9.7 DRIVER MONITORING SYSTEM (DMS)

- 9.7.1 REGULATORY REQUIREMENTS TO INCLUDE DMS IN NEW VEHICLES TO DRIVE GROWTH

- 9.8 FORWARD COLLISION WARNING (FCW)

- 9.8.1 OEM'S STANDARDIZATION OF FCW ACROSS ENTRY- AND MID-LEVEL VEHICLES TO DRIVE GROWTH

- 9.9 INTELLIGENT PARK ASSIST (IPA)

- 9.9.1 INCREASING URBAN PARKING CONSTRAINTS IN DENSE CITIES TO DRIVE GROWTH

- 9.10 LANE DEPARTURE WARNING SYSTEM (LDW)

- 9.10.1 MAJOR OEMS OFFERING LDW AS STANDARD FEATURE ACROSS NEW VEHICLES TO DRIVE GROWTH

- 9.11 NIGHT VISION SYSTEM (NVS)

- 9.11.1 HIGHER INCIDENCE OF NIGHTTIME ACCIDENTS ON HIGHWAYS AND RURAL ROADS TO DRIVE GROWTH

- 9.12 ROAD SIGN RECOGNITION (RSR)

- 9.12.1 GROWING INTEGRATION WITH ADAPTIVE CRUISE CONTROL AND SPEED-LIMITING SYSTEMS TO DRIVE GROWTH

- 9.13 TIRE PRESSURE MONITORING SYSTEM (TPMS)

- 9.13.1 REGULATORY MANDATES IN MAJOR REGIONS TO DRIVE GROWTH

- 9.14 TRAFFIC JAM ASSIST (TJA)

- 9.14.1 INCREASING URBAN CONGESTION IN MEGACITIES TO DRIVE GROWTH

- 9.15 KEY PRIMARY INSIGHTS

10 LIGHT COMMERCIAL VEHICLE ADAS MARKET, BY SYSTEM TYPE

- 10.1 INTRODUCTION

- 10.2 ADAPTIVE CRUISE CONTROL (ACC)

- 10.2.1 GROWING NEED FOR EFFICIENCY AND DRIVER COMFORT TO DRIVE MARKET

- 10.3 ADAPTIVE FRONT LIGHT (AFL)

- 10.3.1 NEED TO IMPROVE VISIBILITY AND OPERATIONAL SAFETY IN VARIED DRIVING ENVIRONMENTS TO DRIVE GROWTH

- 10.4 AUTOMATIC EMERGENCY BRAKING (AEB)

- 10.4.1 RISING PRESSURE TO IMPROVE FLEET SAFETY TO DRIVE GROWTH

- 10.5 BLIND SPOT DETECTION (BSD)

- 10.5.1 NEED TO REDUCE SIDE-COLLISION INCIDENTS AND LIABILITY COSTS TO DRIVE GROWTH

- 10.6 CROSS TRAFFIC ALERT (CTA)

- 10.6.1 RISING COMPLEXITY OF URBAN DELIVERY ENVIRONMENTS TO DRIVE GROWTH

- 10.7 DRIVER MONITORING SYSTEM (DMS)

- 10.7.1 INCREASING FOCUS ON DRIVER ACCOUNTABILITY AND FATIGUE MANAGEMENT TO DRIVE GROWTH

- 10.8 FORWARD COLLISION WARNING (FCW)

- 10.8.1 RISING EXPOSURE TO FRONT-END COLLISION RISKS IN URBAN DELIVERY CYCLES TO DRIVE GROWTH

- 10.9 INTELLIGENT PARK ASSIST (IPA)

- 10.9.1 GROWING OPERATIONAL CHALLENGES IN URBAN LOGISTICS TO DRIVE GROWTH

- 10.10 LANE DEPARTURE WARNING (LDW)

- 10.10.1 INCREASING EMPHASIS ON HIGHWAY SAFETY AND DRIVER COMPLIANCE TO DRIVE GROWTH

- 10.11 NIGHT VISION SYSTEM (NVS)

- 10.11.1 NEED TO IMPROVE VISIBILITY DURING OVERNIGHT LOGISTICS AND INTERCITY FREIGHT MOVEMENT TO DRIVE GROWTH

- 10.12 ROAD SIGN RECOGNITION (RSR)

- 10.12.1 INCREASING ENFORCEMENT OF SPEED COMPLIANCE AND ROUTE DISCIPLINE IN FLEET OPERATIONS TO DRIVE GROWTH

- 10.13 TIRE PRESSURE MONITORING SYSTEM (TPMS)

- 10.13.1 RISING FOCUS ON VEHICLE UPTIME AND OPERATING COST CONTROL TO DRIVE GROWTH

- 10.14 TRAFFIC JAM ASSIST (TJA)

- 10.14.1 RISING CONGESTION IN URBAN DELIVERY CORRIDORS TO DRIVE GROWTH

- 10.15 KEY PRIMARY INSIGHTS

11 HEAVY COMMERCIAL VEHICLE ADAS MARKET, BY SYSTEM TYPE

- 11.1 INTRODUCTION

- 11.2 ADAPTIVE CRUISE CONTROL (ACC)

- 11.2.1 NEED TO IMPROVE EFFICIENCY AND CONSISTENCY IN LONG-HAUL FREIGHT OPERATIONS TO DRIVE GROWTH

- 11.3 AUTOMATIC EMERGENCY BRAKING (AEB)

- 11.3.1 GLOBAL SAFETY REGULATIONS ARE PUSHING OEMS TO STANDARDIZE AEB ACROSS NEW HEAVY-DUTY PLATFORMS

- 11.4 BLIND SPOT DETECTION (BSD)

- 11.4.1 INCREASING EXPOSURE TO SIDE-SWIPE INCIDENTS IN HIGH-TRAFFIC FREIGHT CORRIDORS TO DRIVE GROWTH

- 11.5 FORWARD COLLISION WARNING (FCW)

- 11.5.1 NEED FOR EARLY HAZARD DETECTION IN HIGH-SPEED FREIGHT OPERATIONS TO DRIVE GROWTH

- 11.6 INTELLIGENT PARK ASSIST (IPA)

- 11.6.1 NEED FOR FREQUENT DOCKING AND MANEUVERING IN CONFINED LOGISTICS ENVIRONMENTS TO DRIVE GROWTH

- 11.7 LANE DEPARTURE WARNING (LDW)

- 11.7.1 GROWING EMPHASIS ON MAINTAINING LANE DISCIPLINE IN LONG-HAUL FREIGHT OPERATIONS TO DRIVE GROWTH

- 11.8 TRAFFIC JAM ASSIST (TJA)

- 11.8.1 FREQUENT CONGESTION NEAR PORTS, INDUSTRIAL ZONES, AND URBAN FREIGHT CORRIDORS TO DRIVE GROWTH

- 11.9 KEY PRIMARY INSIGHTS

12 ADAS MARKET, BY ELECTRIC VEHICLE TYPE

- 12.1 INTRODUCTION

- 12.2 BATTERY ELECTRIC VEHICLE (BEV)

- 12.2.1 INCREASING LEVEL 2+ ADAS ADOPTION IN BEVS TO DRIVE GROWTH

- 12.3 HYBRID ELECTRIC VEHICLE (HEV)

- 12.3.1 EXPANSION OF HYBRID VEHICLES WITH LEVEL 1 & LEVEL 2 ADAS TO DRIVE GROWTH

- 12.4 PLUG-IN HYBRID ELECTRIC VEHICLE (PHEV)

- 12.4.1 EXPANSION OF PHEVS WITH ENHANCED SAFETY SYSTEMS TO DRIVE GROWTH

- 12.5 FUEL CELL ELECTRIC VEHICLE (FCEV)

- 12.6 PRIMARY INSIGHTS

13 ADAS MARKET, BY LEVEL OF AUTONOMY

- 13.1 INTRODUCTION

- 13.2 L1

- 13.2.1 INCREASING ADOPTION WITHIN MID-SIZED VEHICLE SEGMENT TO DRIVE GROWTH

- 13.3 L2

- 13.3.1 ESCALATING DEMAND FOR PREMIUM VEHICLES TO DRIVE GROWTH

- 13.4 L3

- 13.4.1 ADVANCEMENT IN AUTONOMOUS VEHICLE TECHNOLOGY TO DRIVE GROWTH

- 13.5 L4

- 13.6 L5

- 13.7 KEY PRIMARY INSIGHTS

14 ADAS MARKET, OFFERING TYPE

- 14.1 INTRODUCTION

- 14.2 HARDWARE OFFERING

- 14.2.1 INTRODUCTION

- 14.2.1.1 ADAS functions supported by ADAS sensors

- 14.2.1.2 Top hardware providers, 2026

- 14.2.2 CAMERA UNIT

- 14.2.2.1 Rising adoption of Level 2+ driver-assist packages in mid-range vehicles to drive growth

- 14.2.3 LIDAR

- 14.2.3.1 Increasing adoption of autonomous driving systems to drive growth

- 14.2.3.1.1 Installation of LiDAR systems in passenger cars, height vs. volume

- 14.2.3.1 Increasing adoption of autonomous driving systems to drive growth

- 14.2.4 RADAR SENSOR

- 14.2.4.1 Advancements in 4D imaging radar technology to drive growth

- 14.2.5 ULTRASONIC SENSOR

- 14.2.5.1 Continuous improvements in sensor accuracy and miniaturization to drive growth

- 14.2.6 ECU

- 14.2.6.1 Rising compute demand and centralized architectures to drive growth

- 14.2.1 INTRODUCTION

- 14.3 SOFTWARE OFFERING

- 14.3.1 INTRODUCTION

- 14.3.2 OEM OFFERINGS, BY SOFTWARE

- 14.3.3 MIDDLEWARE

- 14.3.3.1 Growing need for scalable and standardized software integration to drive growth

- 14.3.4 APPLICATION SOFTWARE

- 14.3.4.1 Increasing demand for advanced perception, AI-driven features, and continuous OTA feature updates to drive growth

- 14.3.5 OPERATING SYSTEMS

- 14.3.5.1 Rising need for real-time, safety-certified platforms to manage centralized ADAS workloads to drive growth

- 14.4 KEY INDUSTRY INSIGHTS

15 ADAS MARKET, BY SAFETY APPLICATION

- 15.1 INTRODUCTION

- 15.2 OCCUPANT CLASSIFICATION SYSTEM

- 15.2.1 GROWING COMPLEXITY OF IN-CABIN SAFETY SYSTEMS TO DRIVE GROWTH

- 15.2.2 CHILD PRESENCE DETECTION

- 15.3 DASHCAM

- 15.3.1 RISING NEED FOR VERIFIABLE INCIDENT DATA TO DRIVE GROWTH

- 15.4 INTRUSION DETECTION

- 15.5 KEY PRIMARY INSIGHTS

16 ADAS MARKET, BY REGION

- 16.1 INTRODUCTION

- 16.2 ASIA PACIFIC

- 16.2.1 CHINA

- 16.2.1.1 Strong policy framework and ADAS innovation to drive market

- 16.2.2 INDIA

- 16.2.2.1 Mandatory inclusion of ADAS in vehicles to drive market

- 16.2.3 JAPAN

- 16.2.3.1 Advanced ADAS integration and policy support to drive market

- 16.2.4 SOUTH KOREA

- 16.2.4.1 Substantial investments by automakers and tech providers to enhance performance of ADAS solutions to drive market

- 16.2.5 THAILAND

- 16.2.5.1 Government mandates to include ADAS features in BEVs and HEVs to drive market

- 16.2.6 INDONESIA

- 16.2.6.1 Active involvement of private sector in ADAS technological development to drive market

- 16.2.7 REST OF ASIA PACIFIC

- 16.2.1 CHINA

- 16.3 EUROPE

- 16.3.1 GERMANY

- 16.3.1.1 Increasing sales of luxury vehicles equipped with advanced safety features to drive market

- 16.3.2 FRANCE

- 16.3.2.1 Mandating safety requirements to drive market

- 16.3.3 ITALY

- 16.3.3.1 Innovation in automobile industry to drive market

- 16.3.4 SPAIN

- 16.3.4.1 Legislative support for autonomous vehicle development and trials to drive market

- 16.3.5 RUSSIA

- 16.3.5.1 Increasing integration of advanced safety features in new vehicle models to drive market

- 16.3.6 UK

- 16.3.6.1 Rising inclusion of ADAS features in mid-tier automobiles to drive market

- 16.3.7 TURKEY

- 16.3.7.1 Advancements aimed at improving driving comfort in compact cars to drive growth

- 16.3.8 REST OF EUROPE

- 16.3.1 GERMANY

- 16.4 NORTH AMERICA

- 16.4.1 US

- 16.4.1.1 Substantial investments by OEMs in autonomous driving to drive market

- 16.4.2 CANADA

- 16.4.2.1 Rising safety awareness and demand for efficient driving to drive market

- 16.4.3 MEXICO

- 16.4.3.1 Growing awareness about crash-prevention technologies to drive market

- 16.4.1 US

- 16.5 REST OF THE WORLD

- 16.5.1 BRAZIL

- 16.5.1.1 Safety regulations and OEM investments to drive market

- 16.5.2 SOUTH AFRICA

- 16.5.2.1 Development of ADAS for integration into vehicles to drive market

- 16.5.3 IRAN

- 16.5.1 BRAZIL

17 COMPETITIVE LANDSCAPE

- 17.1 OVERVIEW

- 17.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 17.3 MARKET SHARE ANALYSIS FOR KEY PLAYERS, 2025

- 17.4 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS, 2025

- 17.5 COMPANY VALUATION AND FINANCIAL METRICS

- 17.5.1 COMPANY VALUATION

- 17.5.2 FINANCIAL METRICS

- 17.6 BRAND/ PRODUCT COMPARISON

- 17.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 17.7.1 STARS

- 17.7.2 EMERGING LEADERS

- 17.7.3 PERVASIVE PLAYERS

- 17.7.4 PARTICIPANTS

- 17.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 17.7.5.1 Company footprint

- 17.7.5.2 Region footprint

- 17.7.5.3 Hardware offering footprint

- 17.7.5.4 Software offering footprint

- 17.7.5.5 Vehicle type footprint

- 17.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 17.8.1 PROGRESSIVE COMPANIES

- 17.8.2 RESPONSIVE COMPANIES

- 17.8.3 DYNAMIC COMPANIES

- 17.8.4 STARTING BLOCKS

- 17.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 17.8.5.1 List of startups/SMEs

- 17.8.5.2 Competitive benchmarking of startups/SMEs

- 17.9 COMPETITIVE SCENARIO

- 17.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 17.9.2 DEALS

- 17.9.3 EXPANSIONS

- 17.9.4 OTHER DEVELOPMENTS

18 COMPANY PROFILES

- 18.1 KEY PLAYERS

- 18.1.1 ROBERT BOSCH GMBH

- 18.1.1.1 Business overview

- 18.1.1.2 Products offered

- 18.1.1.3 Recent developments

- 18.1.1.3.1 Product launches/developments

- 18.1.1.3.2 Deals

- 18.1.1.3.3 Expansions

- 18.1.1.3.4 Other developments

- 18.1.1.4 MnM view

- 18.1.1.4.1 Key strengths

- 18.1.1.4.2 Strategic choices

- 18.1.1.4.3 Weaknesses and competitive threats

- 18.1.2 AUMOVIO SE

- 18.1.2.1 Business overview

- 18.1.2.2 Products offered

- 18.1.2.3 Recent developments

- 18.1.2.3.1 Product launches/developments

- 18.1.2.3.2 Deals

- 18.1.2.3.3 Expansions

- 18.1.2.3.4 Other developments

- 18.1.2.4 MnM view

- 18.1.2.4.1 Key strengths

- 18.1.2.4.2 Strategic choices

- 18.1.2.4.3 Weaknesses and competitive threats

- 18.1.3 ZF FRIEDRICHSHAFEN AG

- 18.1.3.1 Business overview

- 18.1.3.2 Products offered

- 18.1.3.3 Recent developments

- 18.1.3.3.1 Product developments

- 18.1.3.3.2 Deals

- 18.1.3.3.3 Expansions

- 18.1.3.3.4 Other developments

- 18.1.3.4 MnM view

- 18.1.3.4.1 Key strengths

- 18.1.3.4.2 Strategic choices

- 18.1.3.4.3 Weaknesses and competitive threats

- 18.1.4 DENSO CORPORATION

- 18.1.4.1 Business overview

- 18.1.4.2 Products offered

- 18.1.4.3 Recent developments

- 18.1.4.3.1 Product launches

- 18.1.4.3.2 Deals

- 18.1.4.3.3 Other developments

- 18.1.4.4 MnM view

- 18.1.4.4.1 Key strengths

- 18.1.4.4.2 Strategic choices

- 18.1.4.4.3 Weaknesses and competitive threats

- 18.1.5 MAGNA INTERNATIONAL INC.

- 18.1.5.1 Business overview

- 18.1.5.2 Products offered

- 18.1.5.3 Recent developments

- 18.1.5.3.1 Product launches

- 18.1.5.3.2 Deals

- 18.1.5.3.3 Expansions

- 18.1.5.3.4 Other developments

- 18.1.5.4 MnM view

- 18.1.5.4.1 Key strengths

- 18.1.5.4.2 Strategic choices

- 18.1.5.4.3 Weaknesses and competitive threats

- 18.1.6 MOBILEYE

- 18.1.6.1 Business overview

- 18.1.6.2 Products offered

- 18.1.6.3 Recent developments

- 18.1.6.3.1 Product launches

- 18.1.6.3.2 Deals

- 18.1.6.3.3 Contracts

- 18.1.6.3.4 Other developments

- 18.1.7 APTIV

- 18.1.7.1 Business overview

- 18.1.7.2 Products offered

- 18.1.7.3 Recent developments

- 18.1.7.3.1 Product launches

- 18.1.7.3.2 Deals

- 18.1.7.3.3 Expansions

- 18.1.7.3.4 Contracts

- 18.1.7.3.5 Other developments

- 18.1.8 VALEO

- 18.1.8.1 Business overview

- 18.1.8.2 Products offered

- 18.1.8.3 Recent developments

- 18.1.8.3.1 Deals

- 18.1.8.3.2 Expansions

- 18.1.8.3.3 Contracts

- 18.1.8.3.4 Other developments

- 18.1.9 HYUNDAI MOBIS

- 18.1.9.1 Business overview

- 18.1.9.2 Products offered

- 18.1.9.3 Recent developments

- 18.1.9.3.1 Product launches/developments

- 18.1.9.3.2 Deals

- 18.1.9.3.3 Other developments

- 18.1.10 NVIDIA CORPORATION

- 18.1.10.1 Business Overview

- 18.1.10.2 Products offered

- 18.1.10.3 Recent developments

- 18.1.10.3.1 Product launches

- 18.1.10.3.2 Deals

- 18.1.10.3.3 Contracts

- 18.1.11 NXP SEMICONDUCTORS

- 18.1.11.1 Business overview

- 18.1.11.2 Products offered

- 18.1.11.3 Recent developments

- 18.1.11.3.1 Product launches/developments

- 18.1.11.3.2 Deals

- 18.1.11.3.3 Other developments

- 18.1.12 AUTOLIV

- 18.1.12.1 Business overview

- 18.1.12.2 Products offered

- 18.1.12.3 Recent developments

- 18.1.12.3.1 Deals

- 18.1.13 ASTEMO LTD.

- 18.1.13.1 Business overview

- 18.1.13.2 Products offered

- 18.1.13.3 Recent developments

- 18.1.13.3.1 Product launches/developments

- 18.1.13.3.2 Deals

- 18.1.14 HORIZON ROBOTICS INC.

- 18.1.14.1 Business overview

- 18.1.14.2 Products offered

- 18.1.14.3 Recent developments

- 18.1.14.3.1 Product launches/developments

- 18.1.14.3.2 Deals

- 18.1.15 ADVANCED MICRO DEVICES, INC.

- 18.1.15.1 Business overview

- 18.1.15.2 Products offered

- 18.1.15.3 Recent developments

- 18.1.15.3.1 Product launches/developments

- 18.1.15.3.2 Deals

- 18.1.16 FICOSA INTERNACIONAL SA

- 18.1.16.1 Business overview

- 18.1.16.2 Products offered

- 18.1.16.3 Recent developments

- 18.1.16.3.1 Other developments

- 18.1.1 ROBERT BOSCH GMBH

- 18.2 OTHER KEY PLAYERS

- 18.2.1 AISIN CORPORATION

- 18.2.2 RENESAS ELECTRONICS CORPORATION

- 18.2.3 INFINEON TECHNOLOGIES AG

- 18.2.4 HELLA GMBH & CO. KGAA

- 18.2.5 TEXAS INSTRUMENTS INCORPORATED

- 18.2.6 SAMSUNG

- 18.2.7 GENTEX CORPORATION

- 18.2.8 BLACKBERRY LIMITED

- 18.2.9 MICROCHIP TECHNOLOGY INC.

- 18.2.10 VEONEER US SAFETY SYSTEMS, LLC.

- 18.2.11 PANASONIC AUTOMOTIVE SYSTEMS CO., LTD.

19 RESEARCH METHODOLOGY

- 19.1 RESEARCH DATA

- 19.1.1 SECONDARY DATA

- 19.1.1.1 Key secondary sources

- 19.1.1.2 Key data from secondary sources

- 19.1.2 PRIMARY DATA

- 19.1.2.1 Primary interviewees from demand and supply sides

- 19.1.2.2 Key industry insights and breakdown of primary interviews

- 19.1.2.3 List of primary interview participants

- 19.1.1 SECONDARY DATA

- 19.2 MARKET SIZE ESTIMATION

- 19.2.1 BOTTOM-UP APPROACH

- 19.2.2 TOP-DOWN APPROACH

- 19.3 DATA TRIANGULATION

- 19.4 FACTOR ANALYSIS

- 19.4.1 DEMAND AND SUPPLY-SIDE FACTOR ANALYSIS

- 19.5 RESEARCH ASSUMPTIONS

- 19.6 RESEARCH LIMITATIONS

- 19.7 RISK ASSESSMENT

20 APPENDIX

- 20.1 DISCUSSION GUIDE

- 20.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 20.3 CUSTOMIZATION OPTIONS

- 20.3.1 EV ADAS MARKET, BY REGION

- 20.3.2 ADAS MARKET BY VEHICLE TYPE AT COUNTRY LEVEL

- 20.3.3 COMPANY INFORMATION:

- 20.3.3.1 Profiling of additional market players (up to 5)

- 20.4 RELATED REPORTS

- 20.5 AUTHOR DETAILS