|

시장보고서

상품코드

2034859

의료 분야 디지털 트윈 시장(-2031년) : 컴포넌트(소프트웨어 및 서비스), 용도(맞춤형 의료, Drug Discovery, 의료 교육, 워크플로우 최적화), 최종사용자(의료 제공업체, 연구 및 학술기관, 보험자), 지역별Digital Twins in Healthcare Market By Component (Software, Services), Application (Personalized Medicine, Drug Discovery, Medical Education, Workflow Optimization), End User (Providers, Research & Academia, Payers), and Region - Global Forecast to 2031 |

||||||

세계의 의료 분야 디지털 트윈 시장은 의료 분야에서의 디지털 트윈 도입 확대나, 민관에 의한 투자 증가를 배경으로 2025년에 현저한 성장을 이루고 있습니다.

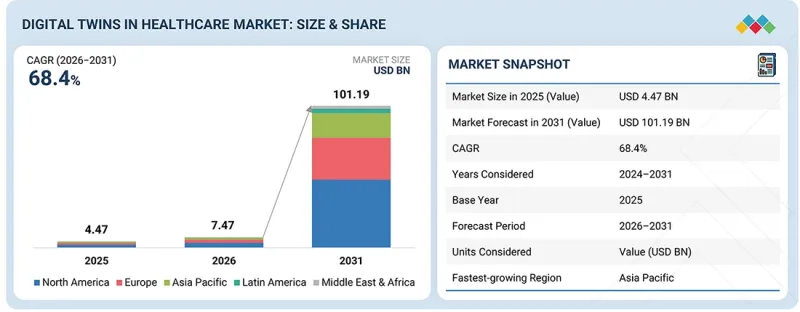

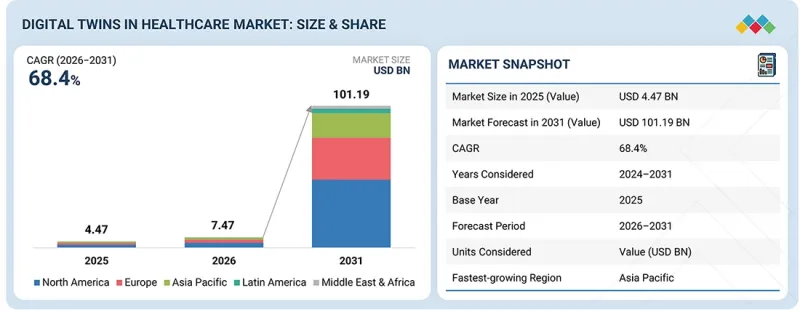

시장 규모는 2026년 74억 7,000만 달러에서 예측 기간 동안 CAGR 68.4%로 확대되어 2031년에는 1,011억 9,000만 달러에 달할 것으로 예측됩니다. 디지털 트윈의 혁신적 가능성으로 인해, 민관 모두 디지털 트윈에 대한 투자가 활발히 이루어지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 금액(달러) |

| 부문 | 컴포넌트, 유형, 용도, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

발렌시아에 본사를 둔 Quibim은 정밀의료에서 이미지 바이오마커의 활용을 추진하고 있습니다. Quibim은 미국 시장에서의 발판을 마련하기 위해 시리즈 A 투자 라운드의 일환으로 5,060만 달러의 자금 조달에 성공했다고 발표했습니다. 회사 측에 따르면, 이는 인간 디지털 트윈 개발의 획기적인 사건이라고 합니다. 이는 사람의 건강 상태를 모니터링하는 동시에 의약품을 효율적으로 개발할 수 있는 역동적인 모델입니다.

"용도별로는 수술 계획 및 의료 교육 부문이 예측 기간 동안 두 번째로 큰 점유율을 차지할 것으로 예측됩니다."

디지털 트윈은 가상현실(VR) 용도과 연동하여 레지던트들이 환자별 해부학적, 생리적 특성에 맞는 수술 과정을 시뮬레이션하고 훈련할 수 있기 때문에 이 시장의 성장에 기여하고 있습니다. 실제 임상 현장의 성능을 재현할 수 있어 수술 중 지표 평가가 용이해집니다. 많은 기업들이 헌체에 대한 의존도를 낮추기 위해 인체 해부학적 구조와 수술 과정을 시뮬레이션하고 있습니다.

"구성요소별로는 소프트웨어가 예측 기간 동안 가장 빠른 성장세를 기록할 것으로 예상"

이 부문의 성장 배경에는 실시간 시뮬레이션 및 예측 분석을 제공하기 위해 디지털 트윈 플랫폼의 도입이 증가하고 있다는 점을 들 수 있습니다. 의료기관과 연구기관은 영상진단 기술, 전자의무기록, 웨어러블 커넥티드 디바이스를 통해 수집된 정보를 기반으로 환자, 장기, 의료시설의 가상 모델을 개발하기 위해 소프트웨어 디지털 트윈 솔루션에 대한 의존도를 높이고 있습니다. 소프트웨어 디지털 트윈 솔루션은 지속적인 모니터링뿐만 아니라 질병 진행 예측 및 맞춤 치료 계획 수립을 가능하게 합니다. 디지털 트윈 기술 및 소프트웨어 솔루션에 대한 관심이 높아진 것은 AI 및 클라우드 컴퓨팅 기반 플랫폼의 채택이 확대되고 있기 때문으로 풀이됩니다. 또한, 가치 기반 의료와 정밀의료의 강화 추세도 디지털 트윈 소프트웨어 솔루션 수요를 촉진할 것으로 예측됩니다. 또한, 디지털 헬스 솔루션에 대한 지속적인 투자와 병원의 IT 인프라와 연동 가능한 상호운용성 있는 시스템 구축의 필요성도 이러한 성장에 기여하고 있습니다.

"아시아태평양이 예측 기간 동안 가장 높은 성장률을 나타낼 것으로 예상"

아시아태평양 시장은 임상 연구 활동의 활성화와 의료 서비스 제공업체의 디지털 기술 도입으로 빠르게 성장하고 있습니다. 이 지역은 연구 활동의 주요 거점 중 하나로 부상하고 있으며, 인도, 일본, 한국, 호주 등의 국가들은 규제 환경의 개선과 비용 구조의 감소로 그 존재감을 강화하고 있습니다. 제약 및 생명공학 기업들은 데이터와 시뮬레이션을 활용한 R&D 이니셔티브에 더욱 적극적으로 참여하고 있으며, 이는 디지털 트윈 기술의 도입을 더욱 촉진하고 있습니다. 동시에 디지털 트윈 기술 구현에 필수적인 AI, 클라우드 컴퓨팅, 헬스 IT 시스템 등 디지털 헬스 인프라 개발을 위해 많은 투자가 이루어지고 있습니다. 또한, 아시아태평양의 각국 정부는 의료 산업의 디지털화를 통해 효율성과 성과를 개선하기 위해 노력하고 있습니다. 이와 관련하여 최근 몇 가지 진전을 보이고 있습니다. 예를 들어, 일본의 후지쯔(Fujitsu Limited)는 맞춤형 의료 및 임상 프로세스의 의사결정을 위해 AI 기반 시뮬레이션 플랫폼을 활용한 의료 분야용 디지털 트윈 기술을 개발했습니다.

세계의 의료 분야 디지털 트윈(Digital Twin) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다. 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술, 특허, 디지털 기술, AI도입에 의한 전략적 파괴적 변화

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 의료 분야 디지털 트윈 시장 : 컴포넌트별

제10장 의료 분야 디지털 트윈 시장 : 유형별

제11장 의료 분야 디지털 트윈 시장 : 용도별

제12장 의료 분야 디지털 트윈 시장 : 최종사용자별

제13장 의료 분야 디지털 트윈 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

LSH 26.06.01The global digital twin healthcare market is experiencing significant growth in 2025, driven by the increasing adoption of digital twins in healthcare and rising investments by public & private entities. The market is projected to reach USD 101.19 billion by 2031 from USD 7.47 billion in 2026, at a CAGR of 68.4% during the forecast period. There have been many investments in digital twins by both public and private organizations due to their innovation potential.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Component, Type, Application, and End user. |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. |

For instance, Quibim, based in Valencia, is developing the use of imaging biomarkers in precision medicine. Quibim has made an announcement on its successful raising of funds amounting to USD 50.6 million as part of its series A investment round to establish a footprint in the USA market. According to Quibim, this will be a milestone in developing human digital twins. These are dynamic models that will make it possible to monitor the well-being of people while ensuring that drugs are developed efficiently.

"Surgical planning & medical education segment accounted for the second-largest share of the market during the forecast period, by application."

In 2025, the surgical planning & medical education segment accounted for the second-largest share of the digital twin in the healthcare market. The growth in this market was driven by the ability of digital twins to work with virtual reality applications that enable the residents to train by simulating surgical processes for the specific anatomical and physiological profile of the patients. This helps in generating a real-life performance depiction and facilitates the evaluation of the intraoperative metrics. Many companies have simulated human anatomy and surgery processes in order to reduce reliance on cadavers.

"By component, software accounted for the fastest growth during the forecast period."

Based on component, software is projected to witness the fastest growth in the digital twins in healthcare market during the forecast period. The reason behind such growth is associated with the rising number of adoptions of digital twin platforms in order to offer real-time simulation and predictive analytics. In particular, healthcare organizations and research institutions will start relying on software digital twin solutions to develop virtual models of patients, organs, and healthcare facilities based on information collected via imaging techniques, electronic health records, and wearable connected devices. Software digital twin solutions enable not only continuous monitoring but also predicting disease progression and creating personalized treatment plans. Rising interest in digital twin technology and software solutions is also explained by the growing adoption of platforms based on AI and cloud computing. In addition, the rising trend towards value-based care and precision medicine is anticipated to boost demand for digital twin software solutions. Furthermore, the ongoing investments in digital health solutions and the necessity of building interoperable systems capable of interacting with the IT infrastructures of hospitals contribute to such growth.

"Asia Pacific to witness the highest growth rate during the forecast period."

The market for digital twins in healthcare in the Asia Pacific region is growing at a fast pace, owing to increased clinical research activities and the adoption of digital technologies by healthcare providers. Asia Pacific has emerged as one of the major hubs for research activities, where countries like India, Japan, South Korea, and Australia have become prominent owing to improved regulation and lower cost structure. Pharmaceutical and biotechnology companies are increasingly engaging in research initiatives through the use of data and simulations, which is further driving the adoption of digital twin technologies. At the same time, significant investment is being made towards the development of digital health infrastructure in the form of artificial intelligence, cloud computing, and health IT systems, which are vital for the implementation of digital twin technologies. Furthermore, governments in the Asia Pacific region are working towards the digitalization of the healthcare industry to improve efficiency and performance. There have been recent developments in this regard. For example, the Japanese company Fujitsu Limited has developed digital twin technology in the healthcare sector using artificial intelligence-based simulation platforms for personalized medicine and decision-making in clinical processes.

The breakdown of primary participants is as follows:

- By Company Type - Tier 1: 45%, Tier 2: 30%, and Tier 3: 25%

- By Designation - C-level: 42%, Director-level: 31%, and Others: 27%

- By Region - North America: 45%, Europe: 30%, Asia Pacific: 20%, Latin America: 3%, and Middle East & Africa: 2%.

The key players operating in the digital twin in healthcare market include Microsoft Corporation (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Amazon Web Services, Inc. (US), Dassault Systemes (France), GE Healthcare (US), IBM (US), NVIDIA Corporation (US), Oracle Corporation (US), PTC (US), SAP (Germany), Atos SE (France), ANSYS, Inc. (US), Faststream Technologies (US), Rescale, Inc. (US), Twin Health (US), NUREA (France), Predictiv (US), Verto (Canada), Qbio (US), Virtonomy GmbH (Germany), Unlearn.ai, Inc. (US), ThoughtWire (Canada), Sim and Cure (France), and PrediSurge (France).

- The study includes an in-depth competitive analysis of these key players in the digital twin in healthcare market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report analyzes the digital twins in healthcare market and aims to estimate the market size and future growth potential of various market segments, based on components, application, end user, and region. The report also provides a competitive analysis of the key players operating in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to buy this report

This report will enrich established firms as well as new entrants/smaller firms to gauge the pulse of the market, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers (increasing Investments in digital twins in developed as well as emerging technology adoption, rising demand for personalized medicine, increasing funding and investments in digital twin startups), restraints (accuracy and privacy issues with digital twin systems and high implementation costs), opportunities (growing importance of digital twin Iin emerging market, increasing focus on cutting edge real-time data analytics), and challenges (lack of technical expertise & data management issues) influencing the growth of the digital twin market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product & service launches in the digital twins in healthcare market

- Market Development: Comprehensive information on the lucrative emerging markets, components, applications, end users, and regions

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the digital twins in healthcare market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players in the digital twins in healthcare market like Microsoft Corporation (US), Siemens Healthineers AG (Germany), Koninklijke Philips N.V. (Netherlands), Amazon Web Services, Inc. (US), Dassault Systemes (France), GE Healthcare (US), IBM (US), NVIDIA Corporation (US), Oracle Corporation (US), PTC (US), SAP (Germany), Atos SE (France), ANSYS, Inc. (US), Faststream Technologies (US), Rescale, Inc. (US), Twin Health (US), NUREA (France), Predictiv (US), Verto (Canada), Qbio (US), Virtonomy GmbH (Germany), Unlearn.ai, Inc. (US), ThoughtWire (Canada), Sim and Cure (France), and PrediSurge (France)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 DIGITAL TWINS IN HEALTHCARE MARKET OVERVIEW

- 3.2 DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT & REGION

- 3.3 DIGITAL TWINS IN HEALTHCARE MARKET: REGIONAL SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing investments by public and private entities

- 4.2.1.2 Growing applications of digital twins

- 4.2.1.3 Technological advancements

- 4.2.1.4 Growing funding and investments in digital twin startups

- 4.2.2 RESTRAINTS

- 4.2.2.1 Managing data quality, privacy issues, and high implementation costs

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing focus on cutting-edge real-time data analytics

- 4.2.3.2 Growing importance of digital twins in emerging economies

- 4.2.4 CHALLENGES

- 4.2.4.1 Lack of skilled professionals

- 4.2.4.2 Integration with existing systems and outdated digital infrastructure

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY (HIGH)

- 5.1.2 BARGAINING POWER OF SUPPLIERS (LOW)

- 5.1.3 BARGAINING POWER OF BUYERS (HIGH)

- 5.1.4 THREAT OF NEW ENTRANTS (LOW)

- 5.1.5 THREAT OF SUBSTITUTES (LOW)

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RESEARCH & PRODUCT DEVELOPMENT

- 5.3.2 TECHNOLOGY INPUTS AND INFRASTRUCTURE

- 5.3.3 PLATFORM DEVELOPMENT AND INTEGRATION

- 5.3.4 DISTRIBUTION

- 5.3.5 MARKETING AND SALES

- 5.3.6 POST-SALE SERVICES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY TYPE (2025)

- 5.5.2 INDICATIVE PRICE FOR DIGITAL TWIN IN HEALTHCARE MARKET, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - DIGITAL TWIN IN HEALTHCARE MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END USERS

- 5.10.5.1 Pharma & biopharma companies

- 5.10.5.2 Research & academia

- 5.10.5.3 Healthcare providers

- 5.10.5.4 Medical device companies

- 5.10.5.5 Other end users

6 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI/ML AND SIMULATION MODELS

- 6.1.2 CLOUD COMPUTING AND HIGH-PERFORMANCE COMPUTING

- 6.1.3 DATA INTEGRATION PLATFORMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 INTERNET OF MEDICAL THINGS (IOMT) AND CONNECTED DEVICES

- 6.2.2 MEDICAL IMAGING AND IMAGING AI

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CLINICAL DECISION SUPPORT SYSTEMS

- 6.3.2 AR/VR FOR SURGICAL SIMULATION AND TRAINING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR DIGITAL TWIN IN HEALTHCARE MARKET

- 6.5.2 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE MODELING AND CLINICAL DECISION SUPPORT

- 6.6.2 VIRTUAL THERAPEUTIC SIMULATION AND PERSONALIZED INTERVENTIONS

- 6.6.3 VIRTUAL CLINICAL TRIALS AND HEALTH SYSTEM OPTIMIZATION

- 6.6.4 POPULATION HEALTH MANAGEMENT AND PANDEMIC RESPONSE MODELING

- 6.7 IMPACT OF AI/GEN AI ON DIGITAL TWIN IN HEALTHCARE MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN DIGITAL TWIN IN HEALTHCARE MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 AI-driven cardiac digital twin for personalized treatment planning

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Digital twin analytics & AI-driven simulation platforms

- 6.7.4.2 Digital twin platform integration & regulatory infrastructure

- 6.7.4.3 Clinical care, virtual monitoring & personalized therapeutics

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Pharma & biopharma companies

- 6.7.5.1.2 User B: Research & academia

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Pharma & biopharma companies

- 6.7.5.2.2 User B: Research & academia

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 DIGITAL TWINS IN HEALTHCARE MARKET, BY COMPONENT

- 9.1 INTRODUCTION

- 9.2 SERVICES

- 9.2.1 INTRODUCTION OF COMPLEX SOFTWARE TO DRIVE DEMAND FOR SERVICES

- 9.3 SOFTWARE

- 9.3.1 SHIFT TO WEB/CLOUD-BASED MODELS TO SUPPORT GROWTH

10 DIGITAL TWINS IN HEALTHCARE MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 PROCESS TWINS

- 10.2.1 RISING DEMAND FOR HEALTHCARE WORKFLOWS AND OPERATIONAL PROCESSES TO BOOST ADOPTION

- 10.3 SYSTEM TWINS

- 10.3.1 INCREASED DEMAND FOR OPERATIONAL EFFICIENCY IN HOSPITALS TO BOOST SEGMENT

- 10.4 WHOLE BODY TWINS

- 10.4.1 ADVANCEMENTS IN AI AND ML TECHNOLOGIES TO BOOST MARKET

- 10.5 BODY PART TWINS

- 10.5.1 RISING DEMAND FOR PERSONALIZED & PRECISION MEDICINE TO FUEL MARKET GROWTH

11 DIGITAL TWINS IN HEALTHCARE MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 DRUG DISCOVERY & DEVELOPMENT

- 11.2.1 ABILITY OF DIGITAL TWINS TO ENHANCE DRUG DISCOVERY & DEVELOPMENT TO BOOST MARKET

- 11.3 PERSONALIZED MEDICINE

- 11.3.1 QUICK AND COST-EFFECTIVE DEVELOPMENT AND TESTING OF PERSONALIZED DIAGNOSTICS TO SUPPORT MARKET

- 11.4 SURGICAL PLANNING & MEDICAL EDUCATION

- 11.4.1 ABILITY TO ENHANCE SURGICAL TRAINING AND SIMULATE SURGICAL PROCEDURES TO BOOST ADOPTION

- 11.5 MEDICAL DEVICE DESIGN & TESTING

- 11.5.1 POTENTIAL OF DIGITAL TWINS TO STREAMLINE OPERATIONS, MINIMIZE RISK, AND REDUCE DOWNTIME TO PROMOTE USE

- 11.6 HEALTHCARE WORKFLOW OPTIMIZATION & ASSET MANAGEMENT

- 11.6.1 IMPROVED EFFICIENCY AND VALUABLE INSIGHTS TO SUPPORT DEMAND

- 11.7 OTHER APPLICATIONS

12 DIGITAL TWINS IN HEALTHCARE MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 PHARMA & BIOPHARMA COMPANIES

- 12.2.1 RISING DEMAND TO REDUCE TIME AND COST OF DRUG DEVELOPMENT TO BOOST ADOPTION

- 12.3 RESEARCH & ACADEMIA

- 12.3.1 INTERACTIVE AND IMMERSIVE LEARNING EXPERIENCES OFFERED BY DIGITAL TWINS TO BOOST ADOPTION

- 12.4 HEALTHCARE PROVIDERS

- 12.4.1 LOWER COSTS AND BETTER PATIENT TREATMENT TO FAVOR MARKET GROWTH

- 12.5 MEDICAL DEVICE COMPANIES

- 12.5.1 GROWING USE OF DIGITAL TWINS FOR SOFTWARE OPTIMIZATION OF MEDICAL DEVICES TO FUEL GROWTH

- 12.6 OTHER END USERS

13 DIGITAL TWINS IN HEALTHCARE MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 13.2.2 US

- 13.2.2.1 Expanding applications of digital twins in healthcare to bolster market growth

- 13.2.3 CANADA

- 13.2.3.1 National digital health strategy and AI-driven clinical research accelerating adoption

- 13.3 EUROPE

- 13.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Hospital digitalization mandates and engineering-healthcare convergence drive market

- 13.3.3 UK

- 13.3.3.1 NHS digital transformation and in silico trial leadership advances digital twin market

- 13.3.4 FRANCE

- 13.3.4.1 National AI health strategy and clinical research infrastructure support digital twin integration

- 13.3.5 ITALY

- 13.3.5.1 National recovery plan investments and clinical research modernization drive adoption

- 13.3.6 SPAIN

- 13.3.6.1 Health system digital transformation and biomedical research network enables digital twin growth

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 13.4.2 JAPAN

- 13.4.2.1 National Digital Health Mission and pharma innovation ecosystem emerging as digital twin growth frontier

- 13.4.3 CHINA

- 13.4.3.1 National AI strategy and smart hospital infrastructure to drive large-scale digital twin deployment

- 13.4.4 INDIA

- 13.4.4.1 Improvement in healthcare infrastructure to support market growth

- 13.4.5 AUSTRALIA

- 13.4.5.1 National Digital Health Strategy 2023-2028 and Medical Research Future Fund advance digital twin adoption

- 13.4.6 SOUTH KOREA

- 13.4.6.1 Smart Hospital Policy and deep tech industrial ecosystem position country as regional leader

- 13.4.7 REST OF ASIA PACIFIC

- 13.5 LATIN AMERICA

- 13.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 13.5.2 BRAZIL

- 13.5.2.1 Country to dominate regional market

- 13.5.3 MEXICO

- 13.5.3.1 Favorable government strategies to drive market growth

- 13.5.4 REST OF LATIN AMERICA

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 13.6.2 GCC COUNTRIES

- 13.6.2.1 Increasing healthcare infrastructure development and investment to support market growth

- 13.6.2.2 Saudi Arabia

- 13.6.2.2.1 Government-led digital transformation and strong investments in AI-driven healthcare

- 13.6.2.3 UAE

- 13.6.2.3.1 Advancing digital health innovation and strategic collaborations to drive digital biomarkers adoption

- 13.6.2.4 Other GCC countries

- 13.6.2.4.1 Regulatory initiatives, national health visions, and digital health infrastructure driving digital biomarkers adoption

- 13.6.3 SOUTH AFRICA

- 13.6.3.1 Rising healthcare demand and need for cost-efficient, data-driven care delivery drive adoption

- 13.6.4 REST OF MIDDLE EAST & AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL TWINS IN HEALTHCARE MARKET

- 14.3 REVENUE SHARE ANALYSIS OF TOP MARKET PLAYERS

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 VALUATION & FINANCIAL METRICS

- 14.6.1 FINANCIAL METRICS

- 14.6.2 COMPANY VALUATION

- 14.7 COMPANY EVALUATION QUADRANT: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Component footprint

- 14.7.5.4 Type footprint

- 14.7.5.5 Application footprint

- 14.7.5.6 End user footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SME players

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT/SERVICE LAUNCHES, ENHANCEMENTS, AND APPROVALS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 MICROSOFT

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 SIEMENS HEALTHINEERS AG

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 KONINKLIJKE PHILIPS N.V.

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 DASSAULT SYSTEMES

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product/Service launches & enhancements

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 AMAZON WEB SERVICES, INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product/Service launches & enhancements

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 GE HEALTHCARE

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 ORACLE

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Deals

- 15.1.8 IBM

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 PTC

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.10 SAP

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.3.2 Other developments

- 15.1.11 ATOS SE

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.12 NVIDIA CORPORATION

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product/Service launches & enhancements

- 15.1.12.3.2 Deals

- 15.1.13 ANSYS INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product/Service launches & enhancements

- 15.1.13.3.2 Deals

- 15.1.14 FASTSTREAM TECHNOLOGIES

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Services offered

- 15.1.15 RESCALE, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Services offered

- 15.1.15.2.1 Other developments

- 15.1.1 MICROSOFT

- 15.2 OTHER PLAYERS

- 15.2.1 TWIN HEALTH

- 15.2.2 VERTO HEALTH

- 15.2.3 QBIO

- 15.2.4 THOUGHTWIRE

- 15.2.5 SIM&CURE

- 15.2.6 OWKIN, INC

- 15.2.7 NUREA

- 15.2.8 UNLEARN.AI, INC.

- 15.2.9 VIRTONOMY GMBH

- 15.2.10 PREDISURGE

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH APPROACH

- 16.1.1 SECONDARY RESEARCH

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY RESEARCH

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primaries

- 16.1.2.3 Insights from primary experts

- 16.1.1 SECONDARY RESEARCH

- 16.2 RESEARCH METHODOLOGY DESIGN

- 16.3 MARKET SIZE ESTIMATION

- 16.4 MARKET BREAKDOWN DATA TRIANGULATION

- 16.5 MARKET SHARE ESTIMATION

- 16.6 STUDY ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS

- 16.7.1 METHODOLOGY-RELATED LIMITATIONS

- 16.7.2 SCOPE-RELATED LIMITATIONS

- 16.8 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS