|

시장보고서

상품코드

2034865

의료용 피부 접착제 시장(-2030년) : 제품(아크릴, 실리콘, 고무), 기재, 유형, 용도, 최종사용자(병원 및 진료소, 홈케어), 주요 이해관계자 및 구입 기준, 미충족 요구Medical Stick-to-Skin Adhesives Market by Product (Acrylic, Silicone, Rubber), Backing Material, Type, Application, End User (Hospital, Clinic, Home Care), Key Stakeholder & Buying Criteria, Unmet Need - Forecast to 2030 |

||||||

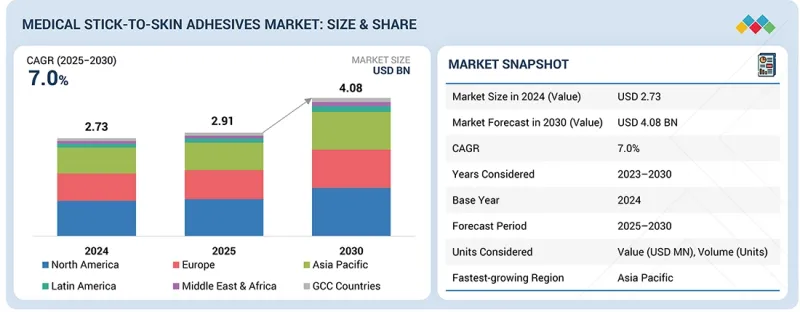

의료용 피부 접착제 시장 규모는 2025년 29억 1,000만 달러에서 2030년에는 40억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 중 연평균 복합 성장률(CAGR)은 7.0%를 나타낼 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2023년-2030년 |

| 기준 연도 | 2024년 |

| 예측 기간 | 2025-2030년 |

| 단위 | 금액(달러) |

| 부문 | 제품, 기재, 유형, 용도, 최종사용자, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

의료용 피부 접착제 시장은 수술 건수 증가, 웨어러블 의료기기의 보급 확대, 만성 상처 및 고령화 사회를 위한 저자극성, 장기 착용 가능한 드레싱재에 대한 수요 증가에 의해 주도되고 있습니다. 실리콘, 아크릴, 하이브리드 접착 기술의 발전은 그 보급을 더욱 가속화하고 있습니다. 한편, 병원 입찰에서의 가격 압박과 개인 브랜드와의 경쟁은 시장 성장을 억제하고 있습니다. 재택치료에서의 활용 확대, 웨어러블 건강 모니터링, 신흥 시장에서의 보급이 향후 성장 기회로 꼽힙니다.

용도별로는 수술 분야가 가장 큰 시장 점유율을 차지하고 있습니다. 수술 후 상처 보호, 절개창 관리, 의료기기의 고정에는 점착성 드레싱, 테이프, 고정 제품의 사용이 필수적이기 때문입니다. 특히 정형외과, 심혈관외과, 일반외과에서 수술 건수가 많기 때문에 신뢰성이 높고 멸균되어 장기간 착용할 수 있는 접착제에 대한 지속적인 수요가 증가하고 있습니다. 병원은 합병증을 최소화하고 빠른 회복을 위해 고성능 제품을 선호하고 있으며, 이는 수술 분야를 주요 응용 분야로 확고히 자리매김하고 있습니다.

최종 사용자별로는 병원 및 클리닉이 가장 큰 시장 점유율을 차지하고 있습니다. 이는 의료용 테이프, 점착성 드레싱, 고정 제품을 필요로 하는 수술, 상처 치료, 의료기기 고정이 가장 많이 이루어지고 있기 때문입니다. 임상적으로 검증된 고품질 솔루션에 대한 선호도가 안정적인 수요를 창출하고 있습니다. 구급, 수술, 입원 현장에서 자주 사용되어 대규모 조달 물량이 확보되어 있습니다. 표준화된 프로토콜과 상환제도의 지원도 병원의 압도적인 점유율을 더욱 공고히 하고 있습니다.

북미는 선진화된 의료 인프라, 높은 수술 건수, 고품질 드레싱 및 웨어러블 의료기기의 보급으로 인해 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. 이 지역은 잘 정립된 임상 가이드라인, 풍부한 보험급여 제도, 그리고 당뇨병 관리, 원격 모니터링, 수술 후 관리에서 장기 부착형 접착제를 광범위하게 사용하는 혜택을 누리고 있습니다. 주요 제조업체의 존재, 광범위한 유통망, 높은 환자 인지도는 북미의 지배적 지위를 더욱 공고히 하고 있습니다.

세계의 의료용 피부 접착제 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술 및 특허 동향, 법 및 규제 환경, 사례 분석, 시장 규모 추이와 예측, 각종 부문별/지역별/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 의료용 피부 접착제 시장 : 용도별

제10장 의료용 피부 접착제 시장 : 최종사용자별

제11장 의료용 피부 접착제 시장 : 기재별

제12장 의료용 피부 접착제 시장 : 제품별

제13장 의료용 피부 접착제 시장 : 유형별

제14장 의료용 피부 접착제 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

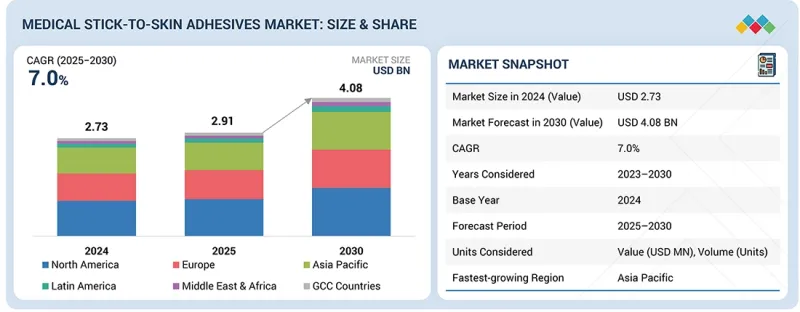

LSH 26.06.01The medical stick-to-skin adhesives market is projected to reach USD 4.08 billion by 2030 from USD 2.91 billion in 2025, at a CAGR of 7.0% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD billion) |

| Segments | By product, backing material, type, application, end user, and region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries |

The medical stick-to-skin adhesives market is driven by rising surgical volumes, growing adoption of wearable medical devices, and increasing demand for gentle, extended-wear dressings for chronic wounds and aging populations. Advancements in silicone, acrylic, and hybrid adhesive technologies further accelerate adoption. However, pricing pressure from hospital tenders and private-label competition restrains market growth. Expanding home care usage, wearable health monitoring, and emerging-market adoption present strong opportunities for future growth.

Based on application, surgery holds the largest market share because postoperative wound protection, incision management, and device fixation require extensive use of adhesive dressings, tapes, and securement products. High surgical volumes, particularly in orthopedics, cardiovascular surgery, and general surgery, drive a continuous demand for reliable, sterile, and long-wearing adhesives. Hospitals prioritize high-performance products to minimize complications and support faster recovery, reinforcing surgery as the leading application segment.

Based on end user, hospitals & clinics hold the largest market share because they perform the highest volume of surgeries, wound treatments, and device fixations requiring medical tapes, adhesive dressings, and securement products. Their preference for clinically validated, high-quality solutions drives consistent demand. Frequent use across emergency, surgical, and inpatient settings ensures large procurement volumes. Standardized protocols and reimbursement support further reinforce hospitals' dominant share.

North America is expected to hold the largest market share due to its advanced healthcare infrastructure, high surgical volumes, and strong adoption of premium wound care dressings and wearable medical devices. The region benefits from well-established clinical guidelines, strong reimbursement pathways, and widespread use of long-wear adhesives in diabetes management, remote monitoring, and post-operative care. The presence of leading manufacturers, extensive distribution networks, and high patient awareness further reinforce North America's dominant position in the medical stick-to-skin adhesives market.

A breakdown of the primary participants (supply side) for the medical stick-to-skin adhesives market referred to in this report is provided below:

- By Company Type: Tier 1 (45%), Tier 2 (30%), and Tier 3 (25%)

- By Designation: C-level Executives (42%), Director-level Executives (29%), and Others (29%)

- By Region: North America (29%), Europe (24%), Asia Pacific (29%), Latin America (10%), the Middle East & Africa (5%), and GCC Countries (3%)

Prominent players in the medical stick-to-skin adhesives market are Solventum (US), Coloplast Group (Denmark), Johnson & Johnson (US), Avery Dennison Corporation (US), Smith & Nephew Plc (UK), Nitto Denko Corporation (Japan), Henkel AG & Co. KGaA (Germany), DuPont (US), Molnlycke Health Care AB (Sweden), Advanced Medical Solutions Group plc (UK), Nichiban Co., Ltd. (Japan), B. Braun Melgungen AG (Germany), and HB Fuller (US), among others.

Research Coverage

The report evaluates the medical stick-to-skin adhesives market and estimates the market size and future growth potential of this market based on various segments, including backing material, type, product, application, end user, and region. The report also includes a competitive analysis of the major players in this market, along with company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will assist market leaders and new entrants with data on the nearest approximations of revenue numbers for the overall medical stick-to-skin adhesives market and its subsegments. The report will help stakeholders understand the competitive landscape and gain further insights into better positioning their businesses and developing effective go-to-market strategies. The report helps stakeholders understand the market pulse and provides them with data on influential drivers, hindrances, obstacles, and opportunities in the market.

This report provides insights into the following points:

- Analysis of key drivers (increasing demand for minimally invasive surgical procedures, advancements in wearable medical devices, growing prevalence of chronic diseases, increasing aging population, rising demand for neonatal care solutions, expanding applications in medicine, and technological innovations in adhesive materials), restraints (regulatory compliance and safety concerns and high cost of advanced adhesive products), opportunities (expanding healthcare infrastructure in emerging economies, expansion of home healthcare services, and increasing adoption of telemedicine and remote patient monitoring), and challenges (need to balance functionality with skin-friendliness and maintaining long-term adhesion)

- Product Enhancement/Innovation: Comprehensive details about product launches and anticipated trends in the global medical stick-to-skin adhesives market

- Market Development: Thorough knowledge and analysis of the profitable rising markets by type, backing material, application, product, end user, and region

- Market Diversification: Comprehensive information about newly launched products, expanding markets, current advancements, and investments in the global medical stick-to-skin adhesives market

- Competitive Assessment: Thorough evaluation of the market shares, growth plans, offerings, and capacities of the major competitors in the global medical stick-to-skin adhesives market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 LIMITATIONS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 MEDICAL STICK-TO-SKIN ADHESIVES MARKET OVERVIEW

- 3.2 NORTH AMERICA: MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY PRODUCT AND COUNTRY

- 3.3 MEDICAL STICK-TO-SKIN ADHESIVES MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY REGION

- 3.5 MEDICAL STICK-TO-SKIN ADHESIVES MARKET: DEVELOPED MARKETS VS. EMERGING ECONOMIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing demand for minimally invasive surgical procedures

- 4.2.1.2 Advancements in wearable medical devices

- 4.2.1.3 Growing prevalence of chronic diseases

- 4.2.1.4 Increasing aging population

- 4.2.1.5 Rising demand for neonatal care solutions

- 4.2.1.6 Expanding applications in medicine

- 4.2.1.7 Technological innovations in adhesive materials

- 4.2.2 RESTRAINTS

- 4.2.2.1 Regulatory compliance and safety concerns

- 4.2.2.2 High cost of advanced adhesive products

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding healthcare infrastructure in emerging economies

- 4.2.3.2 Expansion of home healthcare services

- 4.2.3.3 Increasing adoption of telemedicine and remote patient monitoring

- 4.2.4 CHALLENGES

- 4.2.4.1 Need to balance functionality with skin-friendliness

- 4.2.4.2 Maintaining long-term adhesion

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MEDICAL STICK-TO-SKIN ADHESIVES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT FROM NEW ENTRANTS

- 5.1.2 THREAT FROM SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL MEDICAL STICK-TO-SKIN ADHESIVE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL WOUND CARE & MEDICAL DEVICE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF MEDICAL STICK-TO-SKIN ADHESIVES, BY KEY PLAYER

- 5.6.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 391990)

- 5.7.2 EXPORT SCENARIO (HS CODE 391990)

- 5.8 KEY CONFERENCES & EVENTS, 2026

- 5.9 TRENDS & DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF 2025 US TARIFF

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON REGIONS

- 5.12.4.1 North America

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END-USE INDUSTRY

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED SILICONE-BASED ADHESIVES

- 6.1.2 HYDROCOLLOID AND HYDROGEL ADHESIVE TECHNOLOGIES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIOMATERIALS & ADHESIVE FORMULATION TECHNOLOGIES

- 6.2.2 WEARABLE INTEGRATION & SKIN INTERFACE TECHNOLOGIES

- 6.3 TECHNOLOGY/PRODUCT ROADMAP

- 6.3.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.3.2 MID-TERM (2028-2030) | EXPANSION & STANDARDIZATION

- 6.3.3 LONG-TERM (2031-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.4 PATENT ANALYSIS

- 6.4.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 AI-ENABLED WEARABLES & SMART DEVICE INTEGRATION

- 6.5.2 NON-INVASIVE DRUG DELIVERY & THERAPEUTIC PATCHES

- 6.5.3 ADVANCED WOUND CARE & SKIN-SAFE ADHESION SYSTEMS

- 6.6 IMPACT OF AI/GEN AI ON MEDICAL STICK-TO-SKIN ADHESIVES MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 CASE STUDIES OF AI IMPLEMENTATION IN MEDICAL STICK-TO-SKIN ADHESIVES MARKET

- 6.6.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN MEDICAL STICK-TO-SKIN ADHESIVES MARKET

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 SURGERY

- 9.2.1 SHIFT TOWARD ADHESIVE-BASED WOUND CLOSURE IN SURGERIES TO DRIVE MARKET

- 9.3 WOUND DRESSINGS

- 9.3.1 INCREASING PREVALENCE OF CHRONIC WOUNDS TO DRIVE DEMAND

- 9.4 OSTOMY SEALS

- 9.4.1 ADOPTION OF MEDICAL ADHESIVES IN OSTOMY CARE TO SUPPORT MARKET GROWTH

- 9.5 OTHER APPLICATIONS

10 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 HOSPITALS & CLINICS

- 10.2.1 RISING PATIENT POPULATION AND PREVALENCE OF CHRONIC DISEASES TO DRIVE MARKET

- 10.3 HOME CARE SETTINGS

- 10.3.1 GROWING INTEREST IN HOME-BASED HEALTHCARE TO FAVOR MARKET GROWTH

- 10.4 OTHER END USERS

11 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY BACKING MATERIAL

- 11.1 INTRODUCTION

- 11.2 PAPER

- 11.2.1 FOCUS ON IMPROVED BREATHABILITY TO DRIVE MARKET

- 11.3 FABRIC

- 11.3.1 GROWING DEMAND FOR FLEXIBLE AND COMFORTABLE WOUND CARE SOLUTIONS TO DRIVE MARKET

- 11.4 PLASTIC

- 11.4.1 DEVELOPMENT OF THINNER AND MORE DISCREET PLASTIC-BACKED DRESSINGS TO DRIVE DEMAND

- 11.5 OTHER MATERIALS

12 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY PRODUCT

- 12.1 INTRODUCTION

- 12.2 ACRYLIC-BASED ADHESIVES

- 12.2.1 STRONG BONDING PROPERTIES, DURABILITY, AND BIOCOMPATIBILITY TO DRIVE MARKET

- 12.3 SILICONE-BASED ADHESIVES

- 12.3.1 ATRAUMATIC REMOVAL AND SKIN-FRIENDLY CHARACTERISTICS TO DRIVE MARKET

- 12.4 WATER-BASED ADHESIVES

- 12.4.1 GROWING DEMAND FOR ADVANCED WOUND CARE SOLUTIONS TO SUPPORT MARKET GROWTH

- 12.5 RUBBER-BASED ADHESIVES

- 12.5.1 EASE OF MANUFACTURING AND COST-EFFECTIVENESS TO BOOST ADOPTION

- 12.6 OTHER ADHESIVES

13 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY TYPE

- 13.1 INTRODUCTION

- 13.2 SPECIALIZED ADHESIVES

- 13.2.1 DEMAND FOR ADVANCED SOLUTIONS TO SUPPORT GROWTH

- 13.3 ELECTRODE ADHESIVES

- 13.3.1 INCREASING PREVALENCE OF CHRONIC DISEASES TO SUPPORT MARKET GROWTH

- 13.4 TRANSDERMAL DRUG DELIVERY ADHESIVES

- 13.4.1 CONVENIENCE AND IMPROVED PATIENT COMPLIANCE TO DRIVE MARKET

14 MEDICAL STICK-TO-SKIN ADHESIVES MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Growing demand for minimally invasive surgeries to drive demand

- 14.2.2 CANADA

- 14.2.2.1 Growing emphasis on patient-centered care to support market growth

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Rising demand for advanced wound care solutions to support growth

- 14.3.2 UK

- 14.3.2.1 Rising incidence of chronic diseases to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Growing chronic wound prevalence to propel market growth

- 14.3.4 ITALY

- 14.3.4.1 Increasing popularity of home healthcare to favor market growth

- 14.3.5 SPAIN

- 14.3.5.1 Growing number of healthcare clinics to drive demand

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Rising prevalence of chronic diseases to drive market

- 14.4.2 JAPAN

- 14.4.2.1 Demand for innovative healthcare solutions to favor market growth

- 14.4.3 INDIA

- 14.4.3.1 Growing emphasis on telehealth solutions and remote patient monitoring to support market growth

- 14.4.4 AUSTRALIA

- 14.4.4.1 Rising per capita spending on healthcare to support market growth

- 14.4.5 SOUTH KOREA

- 14.4.5.1 Advanced healthcare infrastructure and tech-savvy population to support market growth

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 LATIN AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Growing demand for advanced wound care solutions to drive market

- 14.5.2 MEXICO

- 14.5.2.1 Growing chronic disease prevalence to drive demand

- 14.5.3 REST OF LATIN AMERICA

- 14.5.1 BRAZIL

- 14.6 MIDDLE EAST & AFRICA

- 14.6.1 AVAILABILITY OF FUNDS TO PROMOTE HEALTHCARE TO SUPPORT MARKET GROWTH

- 14.7 GCC COUNTRIES

- 14.7.1 STRONG GOVERNMENT FUNDING & HEALTHCARE INVESTMENTS TO DRIVE MARKET EXPANSION

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS

- 15.4 MARKET SHARE ANALYSIS

- 15.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 15.5.1 STARS

- 15.5.2 EMERGING LEADERS

- 15.5.3 PERVASIVE PLAYERS

- 15.5.4 PARTICIPANTS

- 15.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 15.5.5.1 Company footprint

- 15.5.5.2 Region footprint

- 15.5.5.3 Product footprint

- 15.5.5.4 Application footprint

- 15.5.5.5 End user footprint

- 15.6 COMPETITIVE EVALUATION MATRIX: STARTUPS/SMES, 2024

- 15.6.1 PROGRESSIVE COMPANIES

- 15.6.2 DYNAMIC COMPANIES

- 15.6.3 STARTING BLOCKS

- 15.6.4 RESPONSIVE COMPANIES

- 15.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7.1 FINANCIAL METRICS

- 15.7.2 COMPANY VALUATION

- 15.8 BRAND/PRODUCT COMPARISON

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES & APPROVALS

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 SOLVENTUM

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches & approvals

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses & competitive threats

- 16.1.2 JOHNSON & JOHNSON PRIVATE LIMITED

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 MnM view

- 16.1.2.3.1 Right to win

- 16.1.2.3.2 Strategic choices

- 16.1.2.3.3 Weaknesses & competitive threats

- 16.1.3 AVERY DENNISON CORPORATION

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses & competitive threats

- 16.1.4 DUPONT

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses & competitive threats

- 16.1.5 COLOPLAST GROUP

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses & competitive threats

- 16.1.6 ADVANCED MEDICAL SOLUTIONS GROUP PLC

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.7 MOLNLYCKE AB

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.8 HENKEL AG & CO. KGAA

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches & approvals

- 16.1.9 H.B. FULLER COMPANY

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.10 SMITH+NEPHEW

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.11 B. BRAUN SE

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.12 NICHIBAN CO., LTD.

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.13 NITTO DENKO CORPORATION

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.14 LOHMANN & RAUSCHER

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.15 POLYMER SCIENCE, INC.

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.1 SOLVENTUM

- 16.2 OTHER PLAYERS

- 16.2.1 ADGEZION BIOMEDICAL, LLC

- 16.2.2 MBK TAPE SOLUTIONS

- 16.2.3 TAPECON, INC.

- 16.2.4 CHEMENCE

- 16.2.5 PARAFIX TAPES & CONVERSIONS LTD

- 16.2.6 DERMAMED COATINGS COMPANY, LLC

- 16.2.7 PAUL HARTMANN AG

- 16.2.8 MACTAC

- 16.2.9 SEKISUI KASEI CO., LTD.

- 16.2.10 SHURTAPE TECHNOLOGIES, LLC.

- 16.2.11 ADHESIVES RESEARCH INC.

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key industry insights

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.3 MARKET BREAKDOWN & DATA TRIANGULATION

- 17.4 MARKET RANKING ANALYSIS

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RISK ASSESSMENT

- 17.7 LIMITATIONS

- 17.7.1 METHODOLOGY-RELATED LIMITATIONS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS