|

시장보고서

상품코드

2037093

직접 칩 냉각(D2C) 시장 예측(-2032년) : 유형, 냉각액 유형, 최종사용자, 지역별Data Center Direct-to-chip Cooling Market by Type, Coolant Type, End User, and Region - Global Forecast to 2032 |

||||||

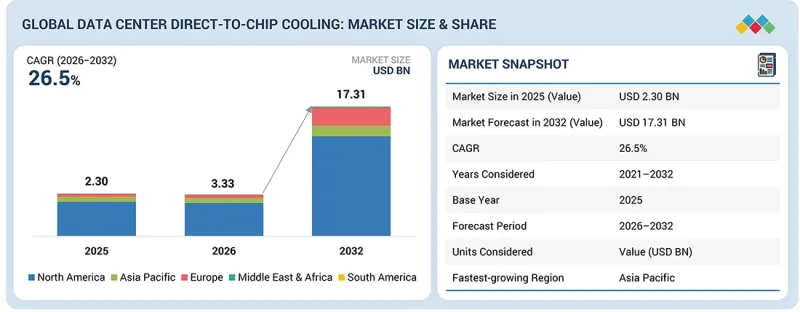

직접 칩 냉각(D2C) 시장 규모는 2026년 33억 3,000만 달러에서 2032년에는 173억 1,000만 달러로 성장하며, 예측 기간 중 CAGR은 26.5%에 달할 것으로 전망되고 있습니다.

세계의 직접 칩 냉각(D2C) 냉각 시장은 첨단 컴퓨팅 시스템에서 열적 정밀도와 컴포넌트 레벨의 열 관리에 대한 요구가 증가함에 따라 주도하고 있습니다. 현대의 프로세서는 소형화 설계와 고성능화가 진행됨에 따라 특정 부위에서 발열이 발생하여 기존의 방 단위나 랙 단위의 냉각 시스템으로는 일정한 온도 제어가 어려워지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(달러) |

| 부문 | 유형, 냉각액 유형, 최종사용자, 지역 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

직접 칩 냉각(D2C)은 발열 부품에 직접 냉각수를 공급함으로써 이러한 문제를 해결하고, 온도 제어를 개선하는 동시에 성능 및 하드웨어 수명에 악영향을 미치는 열적 핫스팟을 줄여줍니다. 데이터센터 운영자는 사업 운영에 있으며, 다운타임을 최소화하고 지속적인 서비스 유지가 필요하므로 신뢰할 수 있는 온도 제어를 제공하는 첨단 냉각 시스템을 채택하고 있습니다. 엣지 컴퓨팅 및 지연에 민감한 애플리케이션의 확대는 수요를 더욱 증가시키고 있으며, 소규모 분산형 데이터센터에서는 한정된 공간과 인프라의 제약 속에서 운영할 수 있는 효율적인 냉각 솔루션이 요구되고 있습니다. 이 두 가지 요인에 더해 처리 효율과 시스템 안정성 향상에 대한 요구로 인해 전 세계 데이터센터에서는 직접 칩 냉각(D2C) 솔루션의 도입이 증가하고 있습니다.

"유형별로는 금액 기준으로 단상 부문이 가장 큰 비중을 차지"

이는 단상 시스템이 널리 보급되어 신뢰성이 입증되었고, 현재 데이터센터 시스템과의 궁합이 좋기 때문입니다. 단상 냉각 시스템은 현재 가장 상업적으로 성숙하고 널리 도입된 솔루션으로, 하이퍼스케일 사업자와 액체 냉각으로 전환하는 기업 데이터센터 모두에게 선호되는 선택이 되고 있습니다. 이러한 제품의 채택률이 증가하는 이유는 설치가 간단하고 유지보수가 용이할 뿐만 아니라, 구성 부품이 작동하기 위해 상변화가 필요하지 않기 때문입니다. 이러한 시스템은 큰 설계 변경 없이 기존 서버 아키텍처 및 시설 설계에 통합할 수 있으므로 사업자는 도입 규모를 유연하게 확장할 수 있습니다. 표준화된 구성 요소, 기존 공급망, 그리고 이러한 제품에 대한 경험을 가진 데이터센터 엔지니어의 존재로 인해 시장에서의 우위를 더욱 공고히 하고 있습니다. 단상 시스템은 데이터센터가 시스템을 운영하는 데 필요한 기본적인 요구사항만 충족하는 반면, 단상 시스템은 기본적인 운영 요구사항만 충족합니다.

"냉각액 유형별로는 물-글리콜계 부문이 금액 기준 가장 큰 점유율을 보일 것으로 예상"

물 및 글리콜 기반 냉각수 부문은 업계에서 폭넓은 수용성, 비용 효율성, 다양한 데이터센터 환경에서의 높은 운영 안정성으로 인해 금액 기준으로 가장 큰 점유율을 차지할 것으로 추정됩니다. 기존 액체 냉각 시스템 및 HVAC 시스템에서 이러한 냉각액을 사용했던 경험은 사업자들이 직접 칩간 냉각으로 전환할 때 신뢰할 수 있고 안전한 선택임을 입증했으며, 이는 운영 측면에서 빠른 채택으로 이어지고 있습니다. 물과 글리콜 혼합물은 최적의 열전도율과 시스템 보호 기능을 결합하여 내식성, 동결 방지, 다양한 작동 조건에서 성능 안정성과 같은 이점을 제공합니다. 이를 통해 장기적인 안정적 운영과 안정적인 성능이 모두 요구되는 대규모 데이터센터 도입에 적합합니다. 제품 취급의 용이성, 기존 공급망 네트워크, 기존 시스템 인프라와의 호환성은 도입시 어려움을 줄이고 총 비용 절감 및 시장 리더십 강화에 기여하고 있습니다. 성능 및 운영 실적이 우수한 물 및 글리콜 냉각수는 확장 가능하고 검증된 냉각 시스템에 대한 데이터센터 수요에 힘입어 예측 기간 중 시장 리더의 지위를 유지할 것으로 예상됩니다.

"최종사용자별로는 하이퍼스케일 부문이 금액 기준으로 가장 큰 비중을 차지할 것으로 전망"

하이퍼스케일 부문은 막대한 투자 규모와 전 세계에서 사업을 확장하고 있는 주요 클라우드 기술 기업의 지속적인 확장으로 인해 금액 기준으로 가장 큰 점유율을 차지할 것으로 추정됩니다. 하이퍼스케일 데이터센터 운영 사업자들은 단일 시설 내에 수천 대의 고성능 서버를 도입하고 있으며, 효율적인 열 관리를 위해 첨단 직접 칩 냉각(D2C) 시스템을 필요로 하는 매우 높은 발열량을 발생시키고 있습니다. 이들 사업자들은 성능 최적화, 에너지 효율성, 대규모의 장기적인 비용 절감을 우선시하므로 액체 냉각 기술 채택의 선두에 서 있습니다. 하이퍼스케일 기업은 차세대 냉각 시스템에 대규모 투자를 할 수 있는 충분한 자금력을 보유하고 있으며, 단계적인 시스템 강화가 아닌 향후 시설에 달할 도입할 계획입니다. 클라우드 컴퓨팅, AI, 머신러닝, 데이터 집약적 애플리케이션에 대한 수요 증가로 인해 하이퍼스케일 시설의 확장이 진행되고 있으며, 이는 고성능 냉각 시스템에 대한 수요를 증가시키고 있습니다. 하이퍼스케일 사업자들은 에너지 소비를 줄이고 지속가능성 성과를 개선하기 위해 보다 효율적인 냉각 기술을 도입하고 있으며, 이는 DTC 솔루션이 도움이 될 수 있습니다. 하이퍼스케일 부문은 대규모 시스템 도입과 막대한 자금 투자, 첨단 기술 활용으로 인해 예측 기간 중 가장 큰 시장 규모에 도달할 것으로 예상됩니다.

세계의 직접 칩 냉각(D2C) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이와 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요, 주요 기업 개요 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 주요 기술의 진보, AI에 의한 영향, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 데이터센터용 직접 칩 냉각(D2C) 시장 : 냉각액 유형별

제10장 데이터센터용 직접 칩 냉각(D2C) 시장 : 유형별

제11장 데이터센터용 직접 칩 냉각(D2C) 시장 : 최종사용자별

제12장 데이터센터용 직접 칩 냉각(D2C) 시장 : 지역별

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

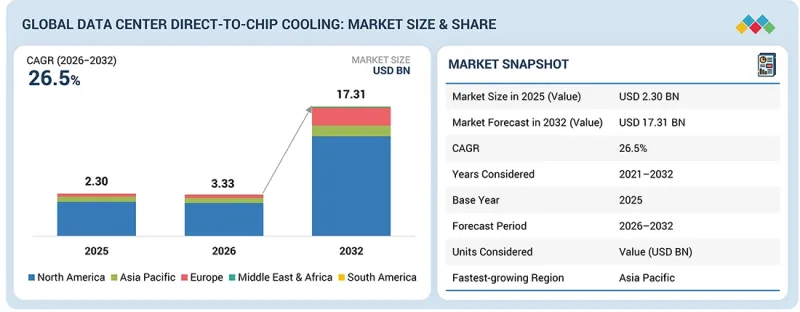

KSA 26.05.29The data center direct-to-chip cooling market is projected to grow from USD 3.33 billion in 2026 to USD 17.31 billion by 2032, at a CAGR of 26.5% over the forecast period. The global data center direct-to-chip cooling market is also being driven by the increasing need for thermal precision and component-level heat management in advanced computing systems. The compact design of modern processors, together with their increased processing power, results in heat generation at specific points, which prevents traditional room-sized or rack-sized cooling systems from achieving constant temperature control.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Type, Coolant Type, End User, and Region |

| Regions covered | Asia Pacific, Europe, North America, the Middle East & Africa, and South America |

Direct-to-chip cooling addresses this challenge by delivering coolant directly to heat-generating components, allowing for better temperature control while reducing thermal hotspots that adversely affect performance and hardware lifespan. Data center operators are adopting advanced cooling systems that provide dependable temperature control because their business operations require them to minimize downtime and maintain continuous service. The expansion of edge computing and latency-sensitive applications is further contributing to demand, as smaller and distributed data centers require efficient cooling solutions that can operate within limited space and infrastructure constraints. The combination of these two factors, together with the current need for higher processing efficiency and system reliability, is driving data centers worldwide to implement direct-to-chip cooling solutions.

"By type, the single phase segment is estimated to hold the largest share, in terms of value."

The data center direct-to-chip cooling market will see its largest share from single-phase systems because they have become widely used, proven reliable, and work well with current data center systems. Single-phase cooling systems are currently the most commercially mature and widely deployed solutions, making them the preferred choice for both hyperscale operators and enterprise data centers transitioning toward liquid cooling. The adoption rate of these products has increased because their design enables simpler installation and easier maintenance, and their components do not require phase changes to function. The systems permit operators to scale their deployments because they can be integrated into existing server architectures and facility designs without major design changes. Their market dominance is further strengthened by standardized components, existing supply chains, and data center engineers who have experience with these products. Single-phase systems now provide computing power, except that they only use basic operational needs, while their single-phase systems provide the basic operational requirements that data centers need to operate their systems.

"By coolant type, the water-glycol-based coolants segment is estimated to hold the largest share, in terms of value."

The water glycol-based coolants segment is estimated to hold the largest share, in terms of value, in the data center direct-to-chip cooling market due to its widespread industry acceptance, cost-effectiveness, and strong operational reliability across diverse data center environments. The existing use of these coolants in traditional liquid cooling and HVAC systems establishes them as a safe option that operators can trust when they switch to direct-to-chip cooling, leading to rapid adoption in operations. Water glycol mixtures deliver optimal thermal conductivity together with system protection, resulting in benefits that include corrosion resistance, freeze protection, and performance stability across different operating conditions. This makes them suitable for large data center deployments that require both stable operations and dependable performance over extended periods. The product's handling simplicity, existing supply chain networks, and compatibility with current system infrastructure all contribute to reduced implementation challenges, which lower total expenses and enhance their market leadership position. Data centers that need expandable cooling systems that have already proven their effectiveness will encourage operators to select coolant solutions that deliver both performance benefits and operational knowledge, resulting in water glycol coolants maintaining their position as the market leader during the forecast period.

"By end user, the hyperscale segment is estimated to hold the largest share, in terms of value."

The hyperscale segment is estimated to hold the largest share, in terms of value, in the data center direct to chip cooling market due to the massive scale of investments and the continuous expansion of large cloud and technology companies operating globally. Hyperscale data center operators deploy thousands of high-performance servers within a single facility, producing extreme heat levels that require advanced direct to chip cooling systems for efficient heat management. These operators are at the forefront of adopting liquid cooling technologies as they prioritize performance optimization, energy efficiency, and long-term cost savings at scale. Hyperscale companies possess sufficient financial resources to make substantial investments in next-generation cooling systems, which they will implement in their upcoming facilities instead of utilizing gradual system enhancements. The growing need for cloud computing, artificial intelligence, machine learning, and data-intensive applications has resulted in the expansion of hyperscale facilities, which drives up requirements for premium cooling systems. Hyperscale operators are implementing more efficient cooling technologies to lower energy consumption and enhance their sustainability performance, making direct to chip solutions beneficial. The hyperscale segment reaches its highest market value during the forecast period because it combines extensive system deployments with significant financial investments and the use of cutting-edge technologies.

Break-up of primary participants for the report:

- By Company Type: Tier 1 - 20%, Tier 2 - 40%, and Tier 3 - 40%

- By Designation: C-Level Executives- 10%, Directors- 70%, and Others - 20%

- By Region: North America - 45%, Asia Pacific - 25%, Europe - 20%, Middle East & Africa - 5%, and South America - 5%

Vertiv Group Corp. (US), Super Micro Computer, Inc. (US), Modine Manufacturing Company (US), DCX Liquid Cooling Systems (Poland), and Schneider Electric (France) are the key players in the data center direct-to-chip cooling market. These players have adopted various strategies, including agreements, joint ventures, and expansions, to increase their market share and business revenue.

Research Coverage:

The report defines, segments, and projects the size of the data center direct-to-chip cooling market by type, coolant type, end user, and region. It strategically profiles the key players and comprehensively analyzes their market share and core competencies. It also tracks and analyzes competitive developments, such as expansions, agreements, and acquisitions undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help market leaders/new entrants by providing the closest approximations of revenue for the data center direct-to-chip cooling market and its segments. This report is also expected to help stakeholders gain a deeper understanding of the market's competitive landscape, acquire valuable insights to enhance their business positions, and develop effective go-to-market strategies. It also enables stakeholders to understand the market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (Increasing Heat Density from AI & HPC Workloads, Superior Thermal Efficiency Compared to Air Cooling, Growing Demand for Energy-efficient Data Centers, Increasing Rack Power Density in Hyperscale Data Centers), restraints (High Initial Capital Investment, Complex Integration with Existing Infrastructure, Limited Standardization Across Vendors), opportunities (Rapid Growth of AI, Generative AI, and GPU-based Computing, Expansion of Edge Data Centers with High Compute Density, Integration with Waste Heat Recovery Systems), and challenges (Skill Gap in Installation and Maintenance, Infrastructure Complexity and Space Constraints, Reliability and Long-term Maintenance Concerns) influencing the growth of the data center direct-to-chip cooling market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities in the data center direct-to-chip cooling market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the data center direct-to-chip cooling market across varied regions

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the data center direct-to-chip cooling market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Vertiv Group Corp. (US), Super Micro Computer, Inc. (US), Modine Manufacturing Company (US), DCX Liquid Cooling Systems (Poland), Schneider Electric (France), and others are the key players in the data center direct-to-chip cooling market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN DATA CENTER DIRECT-TO-CHIP COOLING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN DATA CENTER DIRECT-TO- CHIP COOLING MARKET

- 3.2 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY END USER

- 3.3 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY TYPE

- 3.4 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY REGION

- 3.5 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising AI, HPC, and hyperscale workloads

- 4.2.1.2 Increasing rack power density

- 4.2.1.3 Energy efficiency and sustainability goals

- 4.2.2 RESTRAINTS

- 4.2.2.1 High initial capital investment

- 4.2.2.2 Integration complexity in existing data centers

- 4.2.2.3 Lack of standardization

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expansion of edge and modular data centers

- 4.2.3.2 Innovation in coolant technologies and microfluidics

- 4.2.3.3 High-density computing and chip innovation

- 4.2.4 CHALLENGES

- 4.2.4.1 Leakage and reliability risks

- 4.2.4.2 Cooling of non-chip components

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN DATA CENTER DIRECT-TO-CHIP COOLING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 DATA CENTER INDUSTRY

- 5.2.4 TRENDS IN GLOBAL DATA CENTER COOLING INDUSTRY

- 5.2.5 MANUFACTURING INDUSTRY

- 5.2.6 TRENDS IN GLOBAL HYPERSCALE AND AI DATA CENTER INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 ENERGY SUSTAINABILITY FOR DATA CENTERS

- 5.5.1 SUSTAINABLE DATA CENTERS USING DIRECT-TO-CHIP COOLING

- 5.5.2 ISSUES IN DEVELOPING COUNTRIES

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CASE STUDY 1: PERFORMANCE EVALUATION OF TWO-PHASE DIRECT-TO-CHIP LIQUID COOLING COMBINED WITH AIR COOLING FOR DATA CENTERS

- 5.9.2 CASE STUDY 2: A PATH TO COMMISSIONING OF DIRECT-TO-CHIP LIQUID COOLING FOR HYPERSCALE DATA CENTERS USING EXPERIMENTAL AND CFD TECHNIQUES

6 KEY TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 TWO-PHASE DIRECT-TO-CHIP COOLING

- 6.1.2 ADVANCED COLD PLATE DESIGN

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 MICROCHANNEL LIQUID COOLING

- 6.2.2 MICROCONVECTIVE LIQUID COOLING

- 6.3 FUTURE APPLICATIONS

- 6.3.1 AI-OPTIMIZED HYPERSCALE DATA CENTERS

- 6.3.2 EDGE & DISTRIBUTED DATA CENTERS

- 6.3.3 HYBRID COOLING IN EXISTING DATA CENTERS

- 6.3.4 HIGH-PERFORMANCE COMPUTING (HPC) & AI CLUSTERS

- 6.3.5 SUSTAINABLE & ENERGY-EFFICIENT DATA CENTERS

- 6.4 IMPACT OF AI/GEN AI ON DATA CENTER DIRECT-TO-CHIP COOLING MARKET

- 6.4.1 TOP USE CASES AND MARKET POTENTIAL

- 6.4.2 BEST MARKET PRACTICES

- 6.4.3 CASE STUDIES OF AI IMPLEMENTATION IN DATA CENTER DIRECT-TO-CHIP COOLING MARKET

- 6.4.4 READINESS OF COMPANIES TO ADOPT GENERATIVE AI IN DATA CENTER DIRECT-TO-CHIP COOLING MARKET

- 6.5 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.5.1 VERTIV: AI-READY LIQUID COOLING INFRASTRUCTURE DEPLOYMENT

- 6.5.2 SCHNEIDER ELECTRIC: END-TO-END LIQUID COOLING ECOSYSTEM

- 6.5.3 COMPUDYNAMICS: COMPLEX LIQUID COOLING FOR HIGH DENSITY RACKS AT A HYPERSCALE DATA CENTER IN NC

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 US

- 7.1.3 EUROPE

- 7.1.4 CHINA

- 7.1.5 JAPAN

- 7.1.6 INDIA

- 7.1.7 SINGAPORE

- 7.1.8 OPEN COMPUTE PROJECT (OCP): A STANDARD FOR DATA CENTER BUILDINGS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO APPLICATIONS OF PROPYLENE OXIDE

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY COOLANT TYPE

- 9.1 INTRODUCTION

- 9.2 WATER-GLYCOL-BASED COOLANTS

- 9.2.1 INCREASING DEMAND FOR SCALABLE AND EASY-TO-MAINTAIN COOLING SOLUTIONS TO INCREASE DEMAND

- 9.3 DIELECTRIC FLUID

- 9.3.1 RISING NEED FOR SAFE AND HIGH-PERFORMANCE COOLING IN ADVANCED DATA CENTERS TO BOOST MARKET

- 9.4 REFRIGERANTS

- 9.4.1 GROWING FOCUS ON ADVANCED COOLING TECHNOLOGIES FOR HIGH-DENSITY WORKLOADS TO INCREASE DEMAND

10 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 SINGLE-PHASE

- 10.2.1 GROWING PREFERENCE FOR SIMPLER AND COST-EFFECTIVE LIQUID COOLING SOLUTIONS TO BOOST MARKET GROWTH

- 10.3 TWO-PHASE

- 10.3.1 RISING NEED FOR HIGH-EFFICIENCY COOLING IN HIGH-DENSITY COMPUTING ENVIRONMENTS TO SUPPORT MARKET EXPANSION

11 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.2 HYPERSCALE DATA CENTERS

- 11.2.1 RAPID EXPANSION OF LARGE-SCALE CLOUD INFRASTRUCTURE AND HIGH-DENSITY COMPUTING TO FUEL MARKET GROWTH

- 11.3 COLOCATION PROVIDERS

- 11.3.1 RISING DEMAND FOR SCALABLE AND HIGH-PERFORMANCE SHARED DATA CENTER FACILITIES TO SUPPORT MARKET GROWTH

- 11.4 ENTERPRISES

- 11.4.1 INCREASING DIGITAL TRANSFORMATION AND ADOPTION OF HIGH-PERFORMANCE IT INFRASTRUCTURE TO INCREASE DEMAND

12 DATA CENTER DIRECT-TO-CHIP COOLING MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.3 US

- 12.3.1 RAPID AI INFRASTRUCTURE EXPANSION TO SUPPORT MARKET GROWTH

- 12.4 CANADA

- 12.4.1 SUSTAINABLE DATA CENTER DEVELOPMENT AND COLD CLIMATE ADVANTAGE DRIVING LIQUID COOLING ADOPTION

- 12.5 MEXICO

- 12.5.1 RISING HYPERSCALE INVESTMENTS AND WATER-EFFICIENT COOLING REQUIREMENTS TO BOOST MARKET

- 12.6 ASIA PACIFIC

- 12.7 CHINA

- 12.7.1 RAPID AI INFRASTRUCTURE EXPANSION AND DOMESTIC SEMICONDUCTOR ECOSYSTEM INTEGRATION TO DRIVE MARKET

- 12.8 JAPAN

- 12.8.1 HIGH DENSITY URBAN DATA CENTER DEPLOYMENTS AND ENERGY EFFICIENCY MANDATES TO DRIVE DEMAND

- 12.9 INDIA

- 12.9.1 EXTREME CLIMATIC CONDITIONS AND LARGE-SCALE HYPERSCALE INVESTMENTS TO INCREASE DEMAND

- 12.10 SOUTH KOREA

- 12.10.1 HYPERSCALE AI DATA CENTER INVESTMENTS AND SEMICONDUCTOR-DRIVEN COMPUTE INTENSITY TO SUPPORT MARKET GROWTH

- 12.11 MALAYSIA

- 12.11.1 RISING HYPERSCALE INVESTMENTS AND TROPICAL CLIMATE-DRIVEN COOLING REQUIREMENTS TO BOOST MARKET

- 12.12 SINGAPORE

- 12.12.1 HYPERSCALE EXPANSION AND STRONG SUSTAINABILITY MANDATES TO FUEL ADOPTION

- 12.13 AUSTRALIA

- 12.13.1 STRONG AI INFRASTRUCTURE GROWTH AND STRICT SUSTAINABILITY REGULATIONS TO SUPPORT MARKET GROWTH

- 12.14 REST OF ASIA PACIFIC

- 12.15 EUROPE

- 12.16 GERMANY

- 12.16.1 STRINGENT ENERGY EFFICIENCY REGULATIONS AND WASTE HEAT REUSE MANDATES DRIVING ADVANCED COOLING ADOPTION

- 12.17 FRANCE

- 12.17.1 STRONG HYPERSCALE INVESTMENTS AND SUSTAINABILITY-DRIVEN DATA CENTER EXPANSION TO BOOST MARKET EXPANSION

- 12.18 UK

- 12.18.1 AI INFRASTRUCTURE DEVELOPMENT AND GOVERNMENT SUPPORT FOR ENERGY-EFFICIENT DATA CENTERS TO INCREASE ADOPTION

- 12.19 REST OF EUROPE

- 12.20 MIDDLE EAST & AFRICA

- 12.20.1 GCC COUNTRIES

- 12.21 SAUDI ARABIA

- 12.21.1 AI INFRASTRUCTURE INVESTMENTS AND EXTREME CLIMATE DRIVING ADOPTION OF ADVANCED COOLING TECHNOLOGIES

- 12.22 REST OF GCC COUNTRIES

- 12.22.1 GROWING DIGITAL INFRASTRUCTURE DEVELOPMENT AND RISING NEED FOR ENERGY-EFFICIENT COOLING TO BOOST MARKET

- 12.23 SOUTH AFRICA

- 12.23.1 RISING HYPERSCALE INVESTMENTS, AI INFRASTRUCTURE EXPANSION, AND FOCUS ON ENERGY AND WATER-EFFICIENT COOLING TO BOOST MARKET

- 12.24 REST OF MIDDLE EAST & AFRICA

- 12.25 SOUTH AMERICA

- 12.26 BRAZIL

- 12.26.1 LARGE-SCALE HYPERSCALE INVESTMENTS AND RENEWABLE ENERGY-DRIVEN DATA CENTER EXPANSION TO BOOST MARKET

- 12.27 REST OF SOUTH AMERICA

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 13.3 REVENUE ANALYSIS

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.4.1 RANKING OF KEY MARKET PLAYERS, 2025

- 13.4.2 MARKET SHARE ANALYSIS, 2025

- 13.4.2.1 Vertiv Group Corp. (US)

- 13.4.2.2 Super Micro Computer, Inc. (US)

- 13.4.2.3 Modine Manufacturing Company (US)

- 13.4.2.4 DCX Liquid Cooling Systems (Poland)

- 13.4.2.5 Schneider Electric (France)

- 13.5 BRAND/PRODUCT COMPARISON

- 13.5.1 VERTIV

- 13.5.2 SUPERMICRO

- 13.5.3 MODINE

- 13.5.4 DCX

- 13.5.5 SCHNEIDER ELECTRIC

- 13.6 COMPANY VALUATION AND FINANCIAL METRICS

- 13.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.7.1 STARS

- 13.7.2 EMERGING LEADERS

- 13.7.3 PERVASIVE PLAYERS

- 13.7.4 PARTICIPANTS

- 13.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.7.5.1 Company footprint

- 13.7.6 REGION FOOTPRINT

- 13.7.7 TYPE FOOTPRINT

- 13.7.8 COOLANT TYPE FOOTPRINT

- 13.7.9 END USER FOOTPRINT

- 13.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 13.8.1 PROGRESSIVE COMPANIES

- 13.8.2 RESPONSIVE COMPANIES

- 13.8.3 DYNAMIC COMPANIES

- 13.8.4 STARTING BLOCKS

- 13.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.8.5.1 Detailed list of key startups/SMEs

- 13.8.5.2 Competitive benchmarking of key startups/SMEs

- 13.9 COMPETITIVE SCENARIO

- 13.9.1 PRODUCT LAUNCHES

- 13.9.2 DEALS

- 13.9.3 EXPANSIONS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 VERTIV GROUP CORP.

- 14.1.1.1 Business overview

- 14.1.1.2 Products offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Product launches

- 14.1.1.3.2 Deals

- 14.1.1.3.3 Expansions

- 14.1.1.4 MnM view

- 14.1.1.4.1 Key strengths

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 SUPER MICRO COMPUTER, INC.

- 14.1.2.1 Business overview

- 14.1.2.2 Products offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Deals

- 14.1.2.3.2 Expansions

- 14.1.2.4 MnM view

- 14.1.2.4.1 Key strengths

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 MODINE MANUFACTURING COMPANY

- 14.1.3.1 Business overview

- 14.1.3.2 Products offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches

- 14.1.3.3.2 Deals

- 14.1.3.3.3 Expansions

- 14.1.4 DCX LIQUID COOLING SYSTEMS

- 14.1.4.1 Business overview

- 14.1.4.2 Products offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches

- 14.1.4.4 MnM view

- 14.1.4.4.1 Key strengths

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 SCHNEIDER ELECTRIC

- 14.1.5.1 Business overview

- 14.1.5.2 Products offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Deals

- 14.1.5.3.2 Expansions

- 14.1.5.4 MnM view

- 14.1.5.4.1 Key strengths

- 14.1.5.4.2 Strategic choices

- 14.1.5.4.3 Weaknesses and competitive threats

- 14.1.6 FLEX LTD.

- 14.1.6.1 Business overview

- 14.1.6.2 Products offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.7 COOLIT SYSTEMS

- 14.1.7.1 Business overview

- 14.1.7.2 Products offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches

- 14.1.7.3.2 Deals

- 14.1.7.3.3 Expansions

- 14.1.8 NVENT

- 14.1.8.1 Business overview

- 14.1.8.2 Products offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Deals

- 14.1.8.3.2 Expansions

- 14.1.9 KAORI HEAT TREATMENT CO., LTD.

- 14.1.9.1 Business overview

- 14.1.9.2 Products offered

- 14.1.10 ZUTACORE, INC.

- 14.1.10.1 Business overview

- 14.1.10.2 Products offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches

- 14.1.10.3.2 Deals

- 14.1.11 ICEOTOPE PRECISION LIQUID COOLING

- 14.1.11.1 Business overview

- 14.1.11.2 Products offered

- 14.1.11.3 Recent developments

- 14.1.11.3.1 Product launches

- 14.1.11.3.2 Deals

- 14.1.11.3.3 Expansions

- 14.1.12 BOYD

- 14.1.12.1 Business overview

- 14.1.12.2 Products offered

- 14.1.13 TAISOL ELECTRONICS CO., LTD.

- 14.1.13.1 Business overview

- 14.1.13.2 Products offered

- 14.1.14 WIWYNN CORPORATION

- 14.1.14.1 Business overview

- 14.1.14.2 Products offered

- 14.1.15 INSPUR CO., LTD.

- 14.1.15.1 Business overview

- 14.1.15.2 Products offered

- 14.1.16 LENOVO

- 14.1.16.1 Business overview

- 14.1.16.2 Products offered

- 14.1.16.3 Recent developments

- 14.1.16.3.1 Product launches

- 14.1.16.3.2 Deals

- 14.1.17 ACCELSIUS LLC

- 14.1.17.1 Business overview

- 14.1.17.2 Recent developments

- 14.1.17.2.1 Product launches

- 14.1.18 STULZ GMBH

- 14.1.18.1 Business overview

- 14.1.18.2 Products offered

- 14.1.18.3 Recent developments

- 14.1.18.3.1 Product launches

- 14.1.19 RITTAL GMBH & CO. KG (FRIEDHELM LOH GROUP)

- 14.1.19.1 Business overview

- 14.1.19.2 Products offered

- 14.1.19.3 Recent developments

- 14.1.19.3.1 Product launches

- 14.1.19.3.2 Deals

- 14.1.20 DELTA POWER SOLUTIONS

- 14.1.20.1 Business overview

- 14.1.20.2 Products offered

- 14.1.20.3 Recent developments

- 14.1.20.3.1 Deals

- 14.1.21 LIQUIDSTACK HOLDING B.V. (TRANE TECHNOLOGIES)

- 14.1.21.1 Business overview

- 14.1.21.2 Products/Solutions/Services offered

- 14.1.21.3 Recent developments

- 14.1.21.3.1 Product launches

- 14.1.21.3.2 Deals

- 14.1.21.3.3 Expansions

- 14.1.21.3.4 Other developments

- 14.1.22 CHILLDYNE, INC.

- 14.1.22.1 Business overview

- 14.1.22.2 Products/Solutions/Services offered

- 14.1.22.3 Recent developments

- 14.1.22.3.1 Product launches

- 14.1.22.3.2 Deals

- 14.1.23 MALICO INC.

- 14.1.23.1 Business overview

- 14.1.23.2 Products/Solutions/Services offered

- 14.1.1 VERTIV GROUP CORP.

- 14.2 OTHER PLAYERS

- 14.2.1 KOOLANCE, INC.

- 14.2.2 GIGA-BYTE TECHNOLOGY CO., LTD.

- 14.2.3 OPTICOOL TECHNOLOGIES

- 14.2.4 SEGUENTE INC.

- 14.2.5 COOLCENTRIC

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 List of key secondary sources

- 15.1.1.2 Key data from secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Key data from primary sources

- 15.1.2.2 Key industry insights

- 15.1.2.3 List of primary participants

- 15.1.2.4 Breakdown of primary interviews

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.2.1 BOTTOM-UP APPROACH

- 15.2.2 TOP-DOWN APPROACH

- 15.3 DEMAND-SIDE ANALYSIS

- 15.4 SUPPLY-SIDE ANALYSIS

- 15.4.1 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 15.5 GROWTH FORECAST

- 15.6 DATA TRIANGULATION

- 15.7 RESEARCH ASSUMPTIONS

- 15.8 RESEARCH LIMITATIONS

- 15.9 RISK ASSESSMENT

- 15.10 FACTOR ANALYSIS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS