|

시장보고서

상품코드

2037096

환경 DNA 시장 예측(-2031년) : 솔루션(서비스, 제품, 기기 및 플랫폼, 소프트웨어, 데이터 분석), 샘플 유형(물, 토양, 퇴적물, 대기, 생물 유래 폐기물), 검출 방법, 용도, 지역별Environmental DNA Market by Type of Solution (Services, Products, Instruments & Platforms, Software & Data Analytics), Sample Type (Water, Soil, Sediment, Air, Biological Waste), Detection method, Application, and Region - Global Forecast to 2031 |

||||||

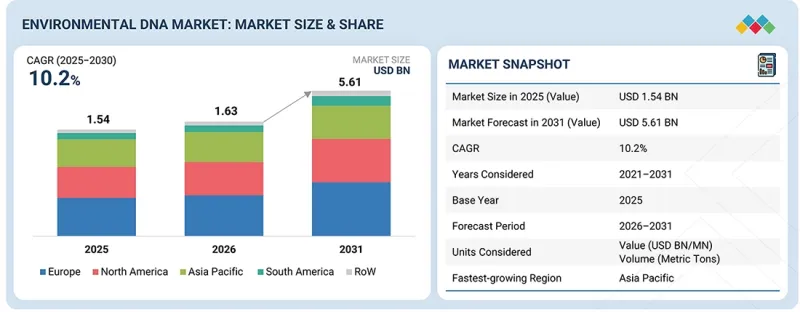

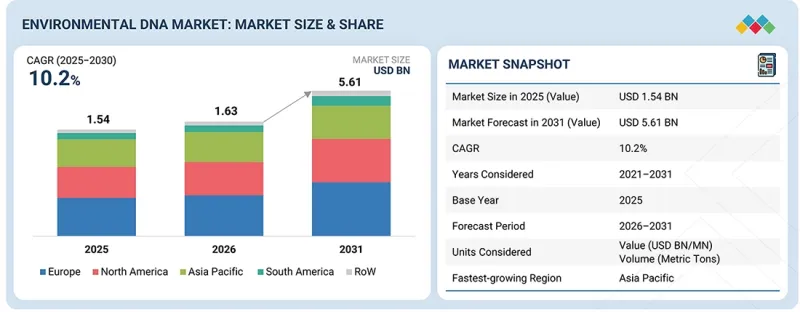

환경 DNA 시장 규모는 2026년 16억 3,000만 달러에서 2031년에는 56억 1,000만 달러에 달할 것으로 예측되고 있으며, CAGR은 10.2%에 달할 전망입니다. 새로운 검사 기법을 통해 생물종을 포획하거나 직접 관찰하지 않고도 검출할 수 있게된 것을 배경으로 시장이 성장하고 있습니다.

이 방법은 물, 토양, 공기 중에 존재하는 유전 물질을 활용하므로 자연 서식지에 미치는 영향을 최소화하면서 생물다양성을 보다 빠르게 추적할 수 있습니다. 따라서 이러한 기술은 연구 활동과 규제 모니터링 모두에서 실용적인 기술입니다. 조직이 생태계 건강성을 추적하고 외래종 식별을 위해 신뢰할 수 있는 데이터를 필요로 하므로 수요가 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(달러) , 톤 |

| 부문 | 솔루션 유형, 샘플 유형, 검출 방법, 용도, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

환경 모니터링에 대한 정부 규제도 강화되고 있으며, 이것이 도입에 힘을 실어주고 있습니다. 많은 프로젝트가 공공 자금과 학술연구에 의해 지원되는 한편, 민간 연구소도 검사 규모 확대에 기여하고 있습니다. 특히 DNA 농도가 매우 낮은 샘플의 경우, 시퀀싱 툴, 검사 정확도, 데이터 분석의 정확도가 향상되는 등 기술적으로도 발전이 이루어지고 있습니다. 동시에 방법론의 표준화를 위한 노력도 활발히 진행되고 있습니다. 표준화의 진전과 이해관계자와의 협력이 심화되는 가운데, 환경 DNA 시장은 현대 환경 관리의 혁신적인 툴로 계속 진화하고 있습니다.

"용도별로는 기후변화 영향 평가 부문이 두드러진 CAGR을 기록할 것으로 전망"

조직들이 기후변화가 생태계에 미치는 장기적인 영향을 측정하는 것을 중요시하는 가운데, 이 분야는 점점 더 많은 추진력을 얻고 있습니다. 종의 서식지, 서식지 상태, 전반적인 생물다양성의 변화를 일관된 방식으로 추적할 필요성이 높아지고 있습니다. 이에 따라 여러 장소에서 반복적으로 모니터링할 수 있는 방법의 활용이 증가하고 있습니다. 환경 DNA는 물, 토양, 퇴적물에서 대규모 현장 조사 없이도 시료 채취가 가능하므로 더 자주 활용되고 있습니다. 이를 통해 정기적인 조사 실시 및 장기적으로 비교 가능한 데이터세트 구축이 용이해집니다. 이는 기존 방법으로는 반드시 가시화할 수 없는 점진적인 환경 변화를 파악하는 데 특히 유용합니다. 정부기관, 연구기관, 자연보호단체들은 기후 관련 프로그램을 강화하고 있으며, 그 평가에서 생물다양성 추적이 중요한 부분을 차지하고 있습니다. 이러한 노력은 특히 취약한 생태계를 중심으로 지역 전체로 확산되고 있습니다. 검사 방법이 더욱 신뢰성이 높아지고, 대규모로 쉽게 배포할 수 있게 됨에 따라 도입은 더욱 늘어날 것으로 예상됩니다.

"샘플 유형별로는 대기 샘플 부문이 견고한 성장세를 유지"

이 부문의 성장은 생물다양성 모니터링에서 대기 샘플링의 보급에 의해 주도되고 있습니다. 이 방법은 비침습적이며, 도입이 용이합니다. 물과 토양 샘플링은 여전히 표준적인 접근 방식이지만, 대기 샘플링은 식물, 동물, 미생물의 DNA를 동시에 수집할 수 있으므로 현재 주목을 받고 있습니다. 대기 샘플링은 현장 조사가 어렵거나 비용이 많이 드는 지역에서 특히 유용합니다. 넓은 범위를 커버하기 위해 필요한 샘플링 지점이 적습니다. 따라서 이 방법은 장기적이고 반복적인 모니터링 프로젝트에 적합합니다. 현재 자연 환경과 도시 환경 모두에서 테스트가 진행 중입니다. 대학, 연구기관, 환경 보호 기관은 성능과 재현성을 검증하기 위한 파일럿 프로그램을 확대하고 있습니다. 이러한 연구는 데이터의 품질과 일관성에 초점을 맞추고 있습니다. 초기 결과는 유망하며, 이 기법의 추가 활용과 개선에 박차를 가하고 있습니다. 운영 절차가 명확해지고 시험 결과가 향상됨에 따라 대기 유래 DNA 데이터에 대한 신뢰도가 높아질 것으로 예상됩니다.

"북미는 환경 DNA에 있으며, 유망한 시장"

북미는 지속적인 연구 활동과 첨단 검사 기술의 조기 도입에 힘입어 환경 DNA 시장의 큰 비중을 차지하고 있습니다. 이 지역은 성숙한 실험실 기반의 혜택을 누리고 있으며, 이러한 방법을 대규모로 적용하는 것이 가능합니다. 환경 모니터링에 대한 투자는 특히 생물다양성 조사, 수질 분석, 외래종 모니터링에 환경 DNA를 활용하는 정부기관과 연구기관들 사이에서 이미 정착되어 있습니다. 미국과 캐나다 양국에서 환경 DNA는 시험적 활용 단계를 넘어 현재 다양한 보전 및 모니터링 프로그램에 통합되고 있습니다. 이러한 변화는 명확한 규제 체계와 생태학 연구에 대한 지속적인 자금 지원으로 지원되고 있습니다. 전문 서비스 제공업체와 기술 기업의 강력한 입지가 시장을 더욱 지원하여 효율적인 처리와 신뢰할 수 있는 분석 결과를 보장하는 데 기여하고 있습니다. 대학, 환경 당국, 비상장 기업 간의 지속적인 협력도 이 분야의 발전에 중요한 역할을 하고 있습니다. 이러한 파트너십은 검사 방법의 개선과 검사 관행의 통일화에 기여하고 있습니다. 그 결과, 담수, 해양, 육상 각 분야에서 프로젝트 활동이 안정적으로 지속되고 있습니다.

세계의 환경 DNA 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술, 특허, 디지털 기술, AI 도입에 의한 전략적 디스럽션

제8장 지속가능성과 규제 상황

제9장 환경 DNA 시장 : 용도별

제10장 환경 DNA 시장 : 검출 방법별

제11장 환경 DNA 시장 : 샘플 유형별

제12장 환경 DNA 시장 : 솔루션 유형별

제13장 환경 DNA 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 인접 시장 및 관련 시장

제18장 부록

KSA 26.05.29The environmental DNA market is projected to reach USD 5.61 billion by 2031, from USD 1.63 billion in 2026, with a CAGR of 10.2%. The market is growing as newer testing methods make it simpler to detect species without having to capture or directly observe them. These approaches rely on genetic material present in water, soil, and air, allowing teams to track biodiversity more quickly and with less disruption to natural habitats. This makes them practical for both research activities and regulatory monitoring. Demand is rising because organizations need reliable data to track ecosystem health and identify invasive species.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD BN), Volume (Metric Tons) |

| Segments | By Type of Solution, Sample Type, Detection Method, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

Government regulations around environmental monitoring are also becoming stricter, which is supporting adoption. Many projects are backed by public funding and academic research, while private labs are helping scale testing. Technology is also improving; sequencing tools, testing accuracy, and data analysis are getting better, especially for samples with very low DNA levels. At the same time, efforts to standardize methods are increasing. As the process of standardization advances and collaborations with stakeholders increase, the environmental DNA market remains evolving as an innovative tool for contemporary environmental management.

"The climate change impact assessment segment within the application category is expected to record a notable CAGR."

The segment is gaining traction as organizations place more focus on measuring how climate change is affecting ecosystems over time. There is a growing need to track shifts in species presence, habitat conditions, and overall biodiversity in a consistent manner. This has increased the use of methods that allow repeat monitoring across locations. Environmental DNA is being used more frequently as it allows sample collection from water, soil, and sediment without intensive fieldwork. This makes it easier to run periodic studies and build comparable datasets over time. It is particularly useful in identifying gradual environmental changes that are not always visible through traditional methods. Government bodies, research institutions, and conservation groups are strengthening climate-related programs, where biodiversity tracking forms an important part of assessment. These efforts are expanding across regions, especially in sensitive ecosystems. As testing methods become more dependable and easier to deploy at scale, adoption is expected to increase.

"The air sample segment within the sample type category maintains strong growth."

Growth in this segment is driven by wider use of air sampling for biodiversity monitoring. The method is non-invasive and easier to deploy. Water and soil samples are still the standard approach, but air sampling is now drawing interest because it can collect DNA from plants, animals, and microorganisms at the same time. Air-based sampling is especially useful in areas where fieldwork is difficult or expensive. Fewer sampling points are needed to cover large areas. This makes the method practical for long-term and repeat monitoring projects. Both natural and urban locations are now part of ongoing trials. Universities, research centers, and environmental agencies are increasing pilot programs to test performance and repeatability. These studies focus on data quality and consistency. Early results have been promising and are encouraging further use and refinement of the approach. As operating procedures become clearer and test results improve, confidence in air-derived DNA data is expected to rise.

"North America is a lucrative market for eDNA."

North America represents a large portion of the environmental DNA market, driven by sustained research activity and early uptake of advanced testing techniques. The region also benefits from a mature laboratory base, which allows these methods to be applied at scale. Investment in environmental monitoring is well established, particularly among government agencies and research organizations that use environmental DNA for biodiversity studies, water quality analysis, and invasive species monitoring. In both the US and Canada, environmental DNA has moved beyond trial use and is now embedded in a range of conservation and monitoring programs. This shift is supported by defined regulatory structures and continued funding for ecological research. A strong presence of specialized service providers and technology firms further supports the market, helping ensure efficient processing and dependable analytical output. Ongoing collaboration between universities, environmental authorities, and private companies plays an important role in advancing the field. These partnerships contribute to method refinement and greater alignment in testing practices. As a result, project activity remains consistent across freshwater, marine, and terrestrial applications.

In-depth interviews were conducted with CEOs, directors, and other executives from various key organizations operating in the environmental DNA market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World -10%

Prominent companies in the market include Thermo Fisher Scientific Inc. (US), QIAGEN (Netherlands), Illumina, Inc. (US), Eurofins Scientific (Luxembourg), SGS Societe Generale de Surveillance SA (Switzerland), NatureMetrics (UK), EnviroDNA (Australia), EDNAtec (Canada), SPYGEN (France), ID-GENE ecodiagnostics Ltd. (France), Takara Bio Inc. (Japan), Stantec (Canada), Applied Genomics (UK), AllGenetics (Spain), and Jonah Ventures (US).

Other players include Cramer Fish Sciences (US), StarSEQ (Germany), Sinsoma GmbH (Germany), eDNA Metagenomics Inc. (US), eDNANature Ltd. (UK), Wilderlab NZ Ltd. (New Zealand), SimplexDNA (US), Biome Makers Inc. (US), Metagen (US), and Biomeme (US).

Research Coverage:

This research report categorizes the environmental DNA market by Type of Solution {Services [Sample Collection & Field Services, Laboratory Analysis, Sequencing services, Bioinformatics & Data Interpretation, End-to-End Project Studies], Products [Sampling Kits, DNA Extraction Kits, PCR Reagents (qPCR, ddPCR), Library Preparation Kits], Instruments & Platforms [PCR Systems (qPCR, ddPCR), Sequencing Platforms (NGS), Sample Processing Instruments], Software & Data Analytics [Bioinformatics Pipelines, Species Identification Databases, Monitoring & Reporting Platforms]}, Sample Type (Water, Soil, Sediment, Air, Biological waste), Detection Method [qPCR (quantitative Polymerase Chain Reaction), ddPCR (digital droplet PCR), Metabarcoding, Metagenomics, CRISPR-based Detection, Hybrid Methods (e.g., qPCR + NGS)], Application (Biodiversity Monitoring, Invasive Species Detection, Conservation Biology, Aquaculture & Fisheries, Water Quality Assessment, Climate Change Impact Assessment, Forensics & Compliance), and Region (North America, Europe, Asia Pacific, South America, Rest of the World). The report's scope encompasses detailed information on the major factors, including drivers, restraints, challenges, and opportunities, that influence the growth of the environmental DNA market. A detailed analysis of key industry players has been conducted to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, and agreements. New product & service launches, mergers & acquisitions, and recent developments associated with the environmental DNA market have been included. This report also covers the competitive analysis of upcoming start-ups in the environmental DNA ecosystem.

Reasons to buy this report:

The report will help market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall environmental DNA and subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

1. In-depth Segmentation across Type of Solution, Sample Type, Detection method, and Application: This report offers an in-depth analysis of the environmental DNA market, categorizing by Type of Solution {Services [Sample Collection & Field Services, Laboratory Analysis, Sequencing services, Bioinformatics & Data Interpretation, End-to-End Project Studies], Products [Sampling Kits, DNA Extraction Kits, PCR Reagents (qPCR, ddPCR), Library Preparation Kits], Instruments & Platforms [PCR Systems (qPCR, ddPCR), Sequencing Platforms (NGS), Sample Processing Instruments], Software & Data Analytics [Bioinformatics Pipelines, Species Identification Databases, Monitoring & Reporting Platforms]}, Sample Type (Water, Soil, Sediment, Air, Biological waste), Detection Method [qPCR (quantitative Polymerase Chain Reaction), ddPCR (digital droplet PCR), Metabarcoding, Metagenomics, CRISPR-based Detection, Hybrid Methods (e.g., qPCR + NGS)], Application (Biodiversity Monitoring, Invasive Species Detection, Conservation Biology, Aquaculture & Fisheries, Water Quality Assessment, Climate Change Impact Assessment, Forensics & Compliance). Such detailed segmentation enables stakeholders to pinpoint high-growth areas, optimize product development, and strategically position offerings along the supply chain.

2. Region-specific Insights with Focus on Emerging Markets: The report provides country- and region-specific analysis, emphasizing opportunities in rapidly growing markets such as Asia Pacific, North America, Europe, and South America. It explores regional regulatory frameworks, key demand drivers, and investment trends, serving as a critical guide for companies pursuing expansion or localization strategies.

3. Competitive Intelligence and Innovation Landscape: Leading market participants, including Thermo Fisher Scientific Inc. (US), QIAGEN (Netherlands), Illumina, Inc. (US), Eurofins Scientific (Luxembourg), SGS Societe Generale de Surveillance SA (Switzerland), NatureMetrics (UK), EnviroDNA (Australia), EDNAtec (Canada), SPYGEN (France), ID-GENE ecodiagnostics Ltd. (France), Takara Bio Inc. (Japan), Stantec (Canada), Applied Genomics (UK), AllGenetics (Spain), and Jonah Ventures (US) are profiled in detail. The report covers recent developments such as new product launches, mergers & acquisitions, facility expansions, and R&D initiatives, helping users benchmark competitors and monitor emerging innovation trends.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the environmental DNA sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 VOLUME UNIT CONSIDERED

- 1.7 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN ENVIRONMENTAL DNA MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ENVIRONMENTAL DNA MARKET

- 3.2 ENVIRONMENTAL DNA MARKET, BY SAMPLE TYPE AND REGION

- 3.3 ENVIRONMENTAL DNA MARKET, BY TYPE OF SOLUTION

- 3.4 ENVIRONMENTAL DNA MARKET, BY SAMPLE TYPE

- 3.5 ENVIRONMENTAL DNA MARKET, BY DETECTION METHOD

- 3.6 ENVIRONMENTAL DNA MARKET, BY APPLICATION

- 3.7 ENVIRONMENTAL DNA MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising Focus on Biodiversity Conservation

- 4.2.1.2 Growing Demand for Non-invasive Monitoring Techniques

- 4.2.1.3 Technological Advancements in Sequencing and Molecular Biology

- 4.2.2 RESTRAINTS

- 4.2.2.1 High Initial Cost and Infrastructure Requirements

- 4.2.2.2 Lack of Standardization and Protocol Variability

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration into Environmental Regulations and Compliance Frameworks

- 4.2.3.2 Adoption in Biodiversity Credits and Natural Capital Markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Fragmented Regulatory and Data-governance Landscape

- 4.2.4.2 Limited Awareness and Technical Understanding Among End Users

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN ENVIRONMENTAL DNA MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 ENVIRONMENTAL DNA MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.2.2 THREAT OF NEW ENTRANTS

- 5.2.3 THREAT OF SUBSTITUTES

- 5.2.4 BARGAINING POWER OF SUPPLIERS

- 5.2.5 BARGAINING POWER OF BUYERS

- 5.2.6 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC INDICATORS

- 5.3.1 WATER STRESS & FRESHWATER AVAILABILITY

- 5.4 BIODIVERSITY LOSS & ECOSYSTEM DEGRADATION

- 5.5 SUPPLY CHAIN ANALYSIS

- 5.5.1 RESEARCH & ASSAY DEVELOPMENT

- 5.5.2 SOURCING & INPUT SUPPLY

- 5.5.3 SAMPLE COLLECTION & PRE-PROCESSING

- 5.5.4 LABORATORY PROCESSING & SEQUENCING

- 5.5.5 BIOINFORMATICS & DATA ANALYSIS

- 5.5.6 DISTRIBUTION & END CONSUMER

- 5.6 VALUE CHAIN ANALYSIS

- 5.6.1 RESEARCH & ASSAY DEVELOPMENT

- 5.6.2 SOURCING & INPUT SUPPLY

- 5.6.3 SAMPLE COLLECTION & PRE-PROCESSING

- 5.6.4 LABORATORY PROCESSING & SEQUENCING

- 5.6.5 BIOINFORMATICS & DATA ANALYSIS

- 5.6.6 DISTRIBUTION & END CONSUMER

- 5.7 ECOSYSTEM ANALYSIS

- 5.7.1 TECHNOLOGY PROVIDERS

- 5.7.2 EDNA SERVICE PROVIDERS

- 5.7.3 REGULATORY BODIES

- 5.7.4 END USERS

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TYPE OF SOLUTION (2022-2026)

- 5.8.2 AVERAGE SELLING PRICE TREND, BY TYPE

- 5.8.3 AVERAGE SELLING PRICE TREND, BY REGION

- 5.9 TRADE ANALYSIS

- 5.9.1 TRADE ANALYSIS OF HS CODE 382219: DIAGNOSTIC OR LABORATORY REAGENTS ON A BACKING, PREPARED DIAGNOSTIC OR LABORATORY REAGENTS, WHETHER OR NOT ON A BACKING, WHETHER OR NOT PUT UP IN THE FORM OF KITS (EXCLUDING CERTAIN SPECIFIED CATEGORIES)

- 5.9.1.1 Export Trends of Environmental DNA under HS Code 382219 (2022-2025)

- 5.9.1.2 Import Trends of Environmental DNA under HS Code 382219 (2022-2025)

- 5.9.1 TRADE ANALYSIS OF HS CODE 382219: DIAGNOSTIC OR LABORATORY REAGENTS ON A BACKING, PREPARED DIAGNOSTIC OR LABORATORY REAGENTS, WHETHER OR NOT ON A BACKING, WHETHER OR NOT PUT UP IN THE FORM OF KITS (EXCLUDING CERTAIN SPECIFIED CATEGORIES)

- 5.10 KEY CONFERENCES & EVENTS

- 5.11 TRENDS IMPACTING CUSTOMERS' BUSINESSES

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 CASE STUDY ANALYSIS

- 5.13.1 REFORESTATION MONITORING USING EDNA (LAND LIFE X NATUREMETRICS, 2024)

- 5.13.2 EDNA SURFACE SAMPLING FOR FISHERIES MANAGEMENT (OCEAN DIAGNOSTICS X NWIFC, 2023-2024)

- 5.14 IMPACT OF 2025 US TARIFF - ENVIRONMENTAL DNA MARKET

- 5.14.1 INTRODUCTION

- 5.14.2 PRICE IMPACT ANALYSIS

- 5.14.3 IMPACT ON COUNTRY/REGION

- 5.14.3.1 North America (US, Canada, Mexico)

- 5.14.3.2 Europe

- 5.14.3.3 Asia Pacific

- 5.14.3.4 South America

- 5.14.3.5 Middle East & Africa

- 5.14.4 IMPACT ON END-USE INDUSTRIES

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 INTRODUCTION

- 6.2 DECISION-MAKING PROCESS

- 6.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.3.2 BUYING CRITERIA

- 6.4 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.5 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

- 6.6 MARKET PROFITABILITY

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 7.1 INTRODUCTION

- 7.2 KEY EMERGING TECHNOLOGIES

- 7.2.1 NEXT-GENERATION SEQUENCING (NGS) & METABARCODING

- 7.2.2 QUANTITATIVE PCR (QPCR) AND DIGITAL PCR (DDPCR)

- 7.2.3 CRISPR-BASED DETECTION TECHNOLOGIES

- 7.3 COMPLEMENTARY TECHNOLOGIES

- 7.3.1 GEOGRAPHIC INFORMATION SYSTEMS (GIS) AND SPATIAL ANALYTICS

- 7.3.2 REMOTE SENSING TECHNOLOGIES

- 7.3.3 AUTOMATED SAMPLING AND FILTRATION SYSTEMS

- 7.3.4 IOT-ENABLED ENVIRONMENTAL SENSORS

- 7.3.5 CLOUD COMPUTING AND DATA MANAGEMENT PLATFORMS

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.4.1 SHORT-TERM | WORKFLOW STANDARDIZATION AND DETECTION RELIABILITY

- 7.4.2 MID-TERM | AUTOMATION, INTEGRATION, AND FIELD-DEPLOYABLE SOLUTIONS

- 7.4.3 LONG-TERM | REAL-TIME MONITORING AND DATA-DRIVEN ECOSYSTEMS

- 7.5 PATENT ANALYSIS

- 7.5.1 LIST OF MAJOR PATENTS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 ON-SITE, REAL-TIME ENVIRONMENTAL DNA MONITORING SYSTEMS

- 7.6.2 AIRBORNE ENVIRONMENTAL DNA FOR TERRESTRIAL BIODIVERSITY MONITORING

- 7.6.3 LONG-TERM ENVIRONMENTAL DNA-BASED ECOSYSTEM MONITORING SYSTEMS

- 7.6.4 GLOBAL ENVIRONMENTAL DNA DATA PLATFORMS FOR BIODIVERSITY GOVERNANCE AND POLICY INTEGRATION

- 7.6.5 INTELLIGENT ENVIRONMENTAL DNA ANALYTICS AND PREDICTIVE MONITORING SYSTEMS

- 7.7 IMPACT OF GENERATIVE AI ON ENVIRONMENTAL DNA MARKET

- 7.7.1 INTRODUCTION

- 7.7.2 USE OF GENERATIVE AI IN ENVIRONMENTAL DNA MARKET

- 7.7.3 TOP USE CASES AND MARKET POTENTIAL

- 7.7.4 BEST PRACTICES IN ENVIRONMENTAL DNA INDUSTRY

- 7.7.5 CASE STUDIES OF AI IMPLEMENTATION IN ENVIRONMENTAL DNA MARKET

- 7.7.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 7.7.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN ENVIRONMENTAL DNA MARKET

- 7.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

8 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 8.1 INTRODUCTION

- 8.2 REGIONAL REGULATIONS AND COMPLIANCE

- 8.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.2.2 INDUSTRY STANDARDS

- 8.2.3 LABELING REQUIREMENTS AND CLAIMS

- 8.2.4 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 8.2.4.1 Standardization and Method Validation Regulations

- 8.2.4.2 Data Reporting, Transparency, and Digital Integration Requirements

- 8.2.4.3 Environmental Monitoring and Biodiversity Policy Integration

- 8.2.4.4 Sustainability and Laboratory Environmental Compliance

- 8.3 SUSTAINABILITY INITIATIVES

- 8.3.1 SUSTAINABLE SAMPLING AND FIELD PRACTICES

- 8.3.2 LABORATORY RESOURCE AND ENERGY EFFICIENCY

- 8.3.3 WASTE REDUCTION AND MATERIAL MANAGEMENT

- 8.3.4 DATA EFFICIENCY AND DIGITAL SUSTAINABILITY

- 8.3.5 SUPPORT FOR BIODIVERSITY AND CONSERVATION GOALS

- 8.4 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 8.5 CERTIFICATIONS, LABELING, ECO-STANDARDS

9 ENVIRONMENTAL DNA MARKET, BY APPLICATION

- 9.1 INTRODUCTION

- 9.2 BIODIVERSITY MONITORING

- 9.2.1 INCREASING NEED FOR LARGE-SCALE BIODIVERSITY MONITORING AND ECOSYSTEM ASSESSMENT TO DRIVE EDNA MARKET

- 9.3 INVASIVE SPECIES DETECTION

- 9.3.1 NEED FOR EARLY DETECTION AND SCALABLE MONITORING OF INVASIVE SPECIES DRIVING EDNA ADOPTION

- 9.4 CONSERVATION BIOLOGY

- 9.4.1 INCREASING FOCUS ON SPECIES PROTECTION AND HABITAT CONSERVATION TO DRIVE MARKET

- 9.5 AQUACULTURE & FISHERIES

- 9.5.1 INCREASING FOCUS ON ACCURATE FISH STOCK ASSESSMENT AND SPECIES-LEVEL MONITORING TO DRIVE MARKET

- 9.6 WATER QUALITY ASSESSMENT

- 9.6.1 GROWING NEED FOR BIOLOGICAL AND ECOSYSTEM-LEVEL WATER QUALITY MONITORING TO DRIVE MARKET

- 9.7 CLIMATE CHANGE IMPACT ASSESSMENT

- 9.7.1 INCREASING NEED TO TRACK CLIMATE-DRIVEN CHANGES IN SPECIES DISTRIBUTION AND ECOSYSTEMS TO DRIVE MARKET

- 9.8 FORENSICS & COMPLIANCE

- 9.8.1 INCREASING DEMAND FOR VERIFIABLE SPECIES DETECTION IN ENVIRONMENTAL ENFORCEMENT AND COMPLIANCE TO DRIVE MARKET

10 ENVIRONMENTAL DNA MARKET, BY DETECTION METHOD

- 10.1 INTRODUCTION

- 10.2 QPCR (QUANTITATIVE POLYMERASE CHAIN REACTION)

- 10.2.1 HIGH SENSITIVITY IN DETECTING LOW-CONCENTRATION DNA FOR EARLY AND RELIABLE SPECIES DETECTION TO DRIVE MARKET

- 10.3 DDPCR (DIGITAL DROPLET PCR)

- 10.3.1 INCREASING NEED FOR HIGHLY RELIABLE DETECTION OF LOW-ABUNDANCE DNA USING DDPCR TO DRIVE MARKET

- 10.4 METABARCODING

- 10.4.1 INCREASING NEED FOR COMPREHENSIVE MULTI-SPECIES BIODIVERSITY DETECTION TO DRIVE MARKET

- 10.5 METAGENOMIC

- 10.5.1 NEED FOR HIGH RESOLUTION AND FUNCTIONAL BIODIVERSITY INSIGHTS TO DRIVE MARKET

- 10.6 CRISPR-BASED DETECTION

- 10.6.1 ABILITY TO ENABLE RAPID AND FIELD-BASED DNA DETECTION USING CRISPR TO DRIVE MARKET

- 10.7 HYBRID METHODS

- 10.7.1 NEED TO CAPTURE BOTH SPECIES-SPECIFIC AND BROAD BIODIVERSITY SIGNALS TO DRIVE MULTI-METHOD EDNA DETECTION

11 ENVIRONMENTAL DNA MARKET, BY SAMPLE TYPE

- 11.1 INTRODU3CTION

- 11.2 WATER

- 11.2.1 HIGH BIODIVERSITY CONCENTRATION IN AQUATIC ECOSYSTEMS REQUIRING SENSITIVE AND SCALABLE DETECTION TO DRIVE MARKET

- 11.3 SOIL

- 11.3.1 INCREASING NEED FOR SOIL BIODIVERSITY DETECTION TO DRIVE EDNA ADOPTION

- 11.4 SEDIMENT

- 11.4.1 ENHANCED BIODIVERSITY DETECTION AND BROADER TAXONOMIC COVERAGE IN SEDIMENT SAMPLES TO DRIVE EDNA ADOPTION

- 11.5 AIR

- 11.5.1 INCREASING NEED TO TRACK DISPERSED AND AIRBORNE SPECIES ACROSS OPEN ENVIRONMENTS TO DRIVE MARKET

- 11.6 BIOLOGICAL WASTE

- 11.6.1 ABILITY TO DETERMINE SPECIES DIET AND TROPHIC INTERACTIONS USING BIOLOGICAL WASTE SAMPLES TO DRIVE MARKET

12 ENVIRONMENTAL DNA MARKET, BY TYPE OF SOLUTION

- 12.1 INTRODUCTION

- 12.2 SERVICES

- 12.2.1 LIMITATIONS OF FRAGMENTED WORKFLOWS AND LACK OF IN-HOUSE EXPERTISE DRIVING RELIANCE ON END-TO-END ENVIRONMENTAL DNA SERVICE MODELS

- 12.2.2 SAMPLE COLLECTION & FIELD SERVICES

- 12.2.3 LABORATORY ANALYSIS SERVICES

- 12.2.4 SEQUENCING SERVICES

- 12.2.5 BIOINFORMATICS & DATA INTERPRETATION SERVICES

- 12.2.6 END-TO-END PROJECT STUDIES

- 12.3 CONSUMABLES & REAGENTS

- 12.3.1 RISING ADOPTION OF STANDARDIZED SAMPLING, EXTRACTION, AND AMPLIFICATION WORKFLOWS TO DRIVE ENVIRONMENTAL DNA MARKET

- 12.3.2 SAMPLING CONSUMABLES

- 12.3.3 DNA EXTRACTION & LIBRARY PREPARATION

- 12.3.4 PCR & DETECTION REAGENTS

- 12.4 INSTRUMENTS & HARDWARE

- 12.4.1 RISING DEMAND FOR HIGH-THROUGHPUT, AUTOMATED, AND REAL-TIME ENVIRONMENTAL DNA ANALYSIS WORKFLOWS TO DRIVE MARKET

- 12.4.2 SAMPLE PROCESSING EQUIPMENT

- 12.4.3 PCR SYSTEMS

- 12.4.4 SEQUENCING PLATFORMS

13 ENVIRONMENTAL DNA MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Expanding federal aquatic biodiversity surveillance programs and invasive species monitoring initiatives to drive market

- 13.2.2 CANADA

- 13.2.2.1 Expanding freshwater biodiversity monitoring and invasive aquatic species surveillance programs to drive environmental DNA adoption across Canada

- 13.2.3 MEXICO

- 13.2.3.1 Expanding marine biodiversity conservation and protected coastal ecosystem monitoring programs to drive environmental DNA adoption across Mexico

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Advancement of national-scale biodiversity surveillance and airborne environmental DNA monitoring to drive market growth in UK

- 13.3.2 GERMANY

- 13.3.2.1 Expansion of standardized biodiversity monitoring programs and high-frequency ecological surveillance initiatives to drive environmental DNA adoption across Germany

- 13.3.3 FRANCE

- 13.3.3.1 Standardization of aquatic biodiversity monitoring and species conservation programs to drive environmental DNA adoption across France

- 13.3.4 ITALY

- 13.3.4.1 Growing use of eDNA metabarcoding for Mediterranean marine biodiversity assessment and ecosystem monitoring to support market growth in Italy

- 13.3.5 SPAIN

- 13.3.5.1 Increasing integration of eDNA-based ecological assessment within estuarine monitoring and freshwater restoration programs to drive market growth in Spain

- 13.3.6 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 China's growing adoption of eDNA for biodiversity monitoring driving environmental DNA market growth

- 13.4.2 INDIA

- 13.4.2.1 India's increasing adoption of eDNA technologies for biodiversity and wildlife monitoring driving growth in environmental DNA market

- 13.4.3 JAPAN

- 13.4.3.1 Japan Emerging as Key Hub for eDNA-based Aquatic Biodiversity Monitoring and Conservation

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Australia & New Zealand Accelerating eDNA Market Growth Through Advanced Biodiversity Conservation Initiatives

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Use of eDNA for freshwater biodiversity surveillance to drive environmental DNA market growth in Brazil

- 13.5.2 ARGENTINA

- 13.5.2.1 Rising adoption of eDNA technologies for marine ecosystem assessment and conservation research to support environmental DNA market growth in Argentina

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD (ROW)

- 13.6.1 MIDDLE EAST

- 13.6.1.1 Water Sustainability & Marine Ecosystem Monitoring Growth

- 13.6.2 AFRICA

- 13.6.2.1 Biodiversity Conservation & Freshwater Monitoring Expansion

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2026

- 14.3 BRAND/PRODUCT COMPARISON

- 14.3.1 THERMO FISHER SCIENTIFIC INC. (US)

- 14.3.2 ILLUMINA, INC. (US)

- 14.3.3 QIAGEN (NETHERLANDS)

- 14.3.4 SGS SOCIETE GENERALE DE SURVEILLANCE SA (SWITZERLAND)

- 14.3.5 EUROFINS SCIENTIFIC (LUXEMBOURG)

- 14.4 REVENUE ANALYSIS, 2023-2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 EV/EBITDA

- 14.6 MARKET SHARE ANALYSIS, 2026

- 14.7 ENVIRONMENTAL DNA COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Type of solution footprint

- 14.7.5.4 Sample type footprint

- 14.7.5.5 Detection footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 Key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 ILLUMINA, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 QIAGEN

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 SGS SOCIETE GENERALE DE SURVEILLANCE SA

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Expansions

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 EUROFINS SCIENTIFIC

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Expansions

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 STANTEC

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.6.4.1 Right to win

- 15.1.6.4.2 Strategic choices

- 15.1.6.4.3 Weaknesses and competitive threats

- 15.1.7 NATUREMETRICS

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches

- 15.1.7.3.2 Deals

- 15.1.7.3.3 Expansions

- 15.1.7.3.4 Other developments

- 15.1.7.4 MnM view

- 15.1.7.4.1 Right to win

- 15.1.7.4.2 Strategic choices

- 15.1.7.4.3 Weaknesses and competitive threats

- 15.1.8 ENVIRODNA

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches

- 15.1.8.3.2 Deals

- 15.1.8.3.3 Other developments

- 15.1.8.4 MnM view

- 15.1.8.4.1 Right to win

- 15.1.8.4.2 Strategic choices

- 15.1.8.4.3 Weaknesses and competitive threats

- 15.1.9 EDNATEC

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.4 MnM view

- 15.1.9.4.1 Right to win

- 15.1.9.4.2 Strategic choices

- 15.1.9.4.3 Weaknesses and competitive threats

- 15.1.10 SPYGEN

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Deals

- 15.1.10.4 MnM view

- 15.1.10.4.1 Right to win

- 15.1.10.4.2 Strategic choices

- 15.1.10.4.3 Weaknesses and competitive threats

- 15.1.11 ID-GENE ECODIAGNOSTICS LTD.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.4 MnM view

- 15.1.11.4.1 Right to win

- 15.1.11.4.2 Strategic choices

- 15.1.11.4.3 Weaknesses and competitive threats

- 15.1.12 TAKARA BIO INC.

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.4 MnM view

- 15.1.12.4.1 Right to win

- 15.1.12.4.2 Strategic choices

- 15.1.12.4.3 Weaknesses and competitive threats

- 15.1.13 APPLIED GENOMICS

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.13.3.2 Expansions

- 15.1.13.4 MnM view

- 15.1.13.4.1 Right to win

- 15.1.13.4.2 Strategic choices

- 15.1.13.4.3 Weaknesses and competitive threats

- 15.1.14 ALLGENETICS

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.4 MnM view

- 15.1.14.4.1 Right to win

- 15.1.14.4.2 Strategic choices

- 15.1.14.4.3 Weaknesses and competitive threats

- 15.1.15 JONAH VENTURES

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches

- 15.1.15.3.2 Deals

- 15.1.15.3.3 Other developments

- 15.1.15.4 MnM view

- 15.1.15.4.1 Right to win

- 15.1.15.4.2 Strategic choices

- 15.1.15.4.3 Weaknesses and competitive threats

- 15.1.1 THERMO FISHER SCIENTIFIC INC.

- 15.2 OTHER PLAYERS

- 15.2.1 CRAMER FISH SCIENCES

- 15.2.1.1 Business overview

- 15.2.1.2 Products offered

- 15.2.1.3 Recent developments

- 15.2.1.4 MnM view

- 15.2.2 STARSEQ

- 15.2.2.1 Business overview

- 15.2.2.2 Products offered

- 15.2.2.3 Recent developments

- 15.2.2.4 MnM view

- 15.2.3 SINSOMA GMBH

- 15.2.3.1 Business overview

- 15.2.3.2 Products offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Deals

- 15.2.3.3.2 Other developments

- 15.2.3.4 MnM view

- 15.2.4 EDNA METAGENOMICS INC.

- 15.2.4.1 Business overview

- 15.2.4.2 Products offered

- 15.2.4.3 Recent developments

- 15.2.4.4 MnM view

- 15.2.5 EDNATURE LTD.

- 15.2.5.1 Business overview

- 15.2.5.2 Products offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Other developments

- 15.2.5.4 MnM view

- 15.2.6 WILDERLAB NZ LTD.

- 15.2.7 SIMPLEXDNA

- 15.2.8 BIOME MAKERS INC.

- 15.2.9 METAGEN

- 15.2.10 BIOMEME

- 15.2.1 CRAMER FISH SCIENCES

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primary profiles

- 16.1.2.3 Key insights from industry experts

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOP-DOWN APPROACH

- 16.2.2 SUPPLY-SIDE ANALYSIS

- 16.2.3 BOTTOM-UP APPROACH (DEMAND SIDE)

- 16.3 DATA TRIANGULATION AND MARKET BREAKUP

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 ADJACENT & RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 LIMITATIONS

- 17.3 ENVIRONMENTAL MONITORING MARKET

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.4 ENVIRONMENTAL TESTING MARKET

- 17.4.1 MARKET DEFINITION

- 17.4.2 MARKET OVERVIEW

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS