|

시장보고서

상품코드

2037097

고전단 믹서 시장 : 시스템 유형별, 구성별, 혼합 용도별, 용도별, 지역별 - 세계 예측(-2031년)High Shear Mixers Market by System Type (Batch Mixers, Inline Mixers), Configuration, Mixing Application, Application (Dairy, Cheese, Ice Cream, Food Products, Dairy Alternatives, Beverages, Other Food Products), and Region - Forecast to 2031 |

||||||

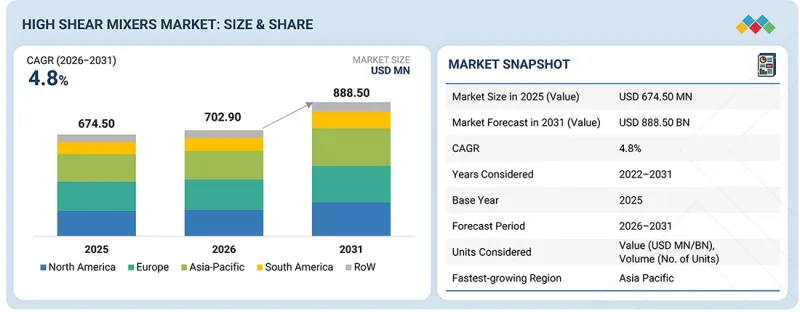

세계의 고전단 믹서 시장 규모는 2026년 7억 290만 달러에서 2031년까지 8억 8,850만 달러에 달할 것으로 예측되며, CAGR로 4.8%의 성장이 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러, 받침대 |

| 부문 | 시스템 유형, 구성, 혼합 용도, 용도, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

이러한 성장은 식품, 유제품, 음료, 식물성 제품, 기타 가공식품 부문 등 다양한 산업 분야에서 가공 솔루션에 대한 수요 증가에 의해 촉진되고 있습니다. 제조업체들은 제품 배합의 균일성, 가공 시간 단축, 광범위한 배합에서 성분의 더 나은 통합을 목표로 하고 있으며, 이 모든 것이 시장 확대에 기여하고 있습니다.

이러한 수요에 대응하기 위해 각 제조업체들은 첨단 고전단 로터 및 고정자 시스템, 다단 믹서, 임베디드 가열 및 냉각 모듈을 개발하고 있습니다. 이러한 혁신은 혼합 공정을 가속화하고 입자 크기를 더욱 미세화할 수 있도록 설계되었습니다. GEA Group Aktiengesellschaft(독일), SPX FLOW, Inc.(미국), Tetra Laval Group(스위스), IDEX Corporation(미국), Buhler Holding AG(스위스), EBARA Corporation(일본), Silverson Machines Ltd.(영국) 등 주요 기업들은 고전단 혼합, 고압 균질화, 첨단 여과 시스템을 결합한 보다 진보된 장비 라인업을 구축하기 위해 연구개발에 많은 투자를 하고 있습니다. 다른 기업들도 가열, 냉각, 진공 기능을 갖춘 혼합기를 제공하고 있습니다.

공장 건설 및 운영에 따른 높은 비용, 생산 관리에 필요한 전문 지식, 그리고 중소 제조업체가 직면하는 추가적인 어려움 등 여러 가지 문제가 시장 성장을 저해할 수 있습니다. 또한, 지역마다 다른 가공 수요의 차이로 인해 통합이 복잡해지고, 지역별로 다양한 식습관에 따른 커스터마이징이 필수적입니다. 이러한 도전과제가 있는 반면, 가공식품 및 간편식에 대한 수요 증가, 세계 식품 공급망 확대, 식물성 식품의 인기 상승, 기능성 식품에 대한 관심 증가로 인해 큰 시장 기회가 창출되고 있습니다.

"시스템 유형별로는 인라인 부문이 예측 기간 동안 가장 빠르게 성장할 것으로 예상됩니다."

고전단 믹서 시장에서 인라인 믹싱 시스템의 채택이 확대됨에 따라 배치 믹서에 비해 큰 이점이 있습니다. 인라인 믹서에서는 재료가 시스템에 지속적으로 공급되고, 혼합되고, 동시에 배출됩니다. 이 프로세스는 작업 속도를 높이고, 생산 속도를 크게 높이며, 전체 가공 시간을 단축합니다. 인라인 믹서는 로터/스테이터 시스템을 이용하여 높은 전단력을 발생시켜 빠른 분산, 유화, 균질화를 가능하게 합니다. 특히 고점도 제품 가공에 적합하며, 기존 가공 라인에 쉽게 통합할 수 있습니다. 이 연속 운전은 공정의 제어와 유연성을 향상시키는 동시에 전체 공정을 단순화합니다. 또한, 연속 혼합을 통해 제품의 편차를 최소화하고 규모 확대가 용이합니다. 배치 믹서는 여전히 가장 큰 시장 점유율을 차지하며 고점도 제품 혼합이 필요한 많은 응용 분야를 지원하는 기둥이지만, 그 이점이 널리 인식됨에 따라 인라인 연속 시스템이 현대의 고처리량 플랜트에서 점점 더 인기를 얻고 있습니다.

"용도별로는 식품 부문이 예측 기간 동안 고전단 믹서 시장에서 큰 점유율을 차지할 것으로 예상됩니다."

식품은 고전단 믹서의 응용 분야에서 가장 큰 시장 점유율을 차지하고 있습니다. 주요 응용 분야에는 이유식, 유아용 조제분유, 수프, 소스, 반죽, 커피 크리머, 커스터드, 딥, 마요네즈, 의료용 식품, 특수 식품, 스포츠 영양 식품, 식품 대체품, 애완동물 사료 등이 포함되며, 이 모든 분야에서 각 특정 용도의 요구 사항을 충족시키기 위해 위해 고전단 믹서가 사용되고 있습니다.

세계의 고전단 믹서 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 중요한 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 고전단 믹서 시장 : 시스템 유형별

제10장 고전단 믹서 시장 : 용도별

제11장 고전단 믹서 시장 : 구성별

제12장 고전단 믹서 시장 : 혼합 용도별

제13장 고전단 믹서 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 인접 시장과 관련 시장

제18장 부록

KSM 26.05.29The global high shear mixers market is projected to grow from USD 702.9 million in 2026 to USD 888.5 million by 2031, at a CAGR of 4.8%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) and Volume (Units) |

| Segments | By System Type, Configuration, Mixing Application, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

This growth is driven by increasing demand for processing solutions across industries such as food, dairy, beverages, plant-based products, and other processed food sectors. Manufacturers aim for consistency in product formulation, reduced processing times, and better integration of ingredients across a wide range of formulations, all of which contribute to market expansion.

To meet these demands, manufacturers are developing advanced high shear rotor-stator systems, multi-stage mixers, and integrated heating and cooling modules. These innovations are designed to accelerate mixing processes and achieve smaller particle sizes. Major companies, such as GEA Group Aktiengesellschaft (Germany), SPX FLOW, Inc. (US), Tetra Laval Group (Switzerland), IDEX Corporation (US), Buhler Holding AG (Switzerland), EBARA Corporation (Japan), and Silverson Machines Ltd. (UK), are investing significantly in research and development to create a more advanced lineup of equipment that combines high-shear mixing, high-pressure homogenizing, and advanced filtration systems. Other companies also provide mixing equipment that includes heating, cooling, and vacuum features.

Several challenges could hinder market growth, including high costs associated with building and operating these plants, the need for specialized knowledge to manage production, and additional difficulties faced by small and medium-sized manufacturers. Furthermore, varying processing needs across different regions complicate integration, and diverse regional food preferences necessitate customization. Despite these challenges, there are significant market opportunities driven by rising demand for processed and convenient foods, the expansion of global food supply chains, the growing popularity of plant-based foods, and the increasing interest in functional foods.

"By system type, the inline segment is expected to be the fastest-growing segment during the forecast period."

The growing adoption of inline mixing systems in the high shear mixers market offers significant advantages over batch mixers. In inline mixers, materials are continuously fed into the system, mixed, and simultaneously discharged. This process enables quick operations, significantly accelerating production and reducing overall processing time. Inline mixers utilize rotor-stator systems to generate high shear forces, enabling rapid dispersion, emulsification, and homogenization. They are particularly well-suited for processing high-viscosity products and can be easily integrated into existing processing lines. This continuous operation enhances process control and flexibility while simplifying the overall process. Additionally, continuous mixing minimizes product variability and facilitates easier scale-up. While batch mixers still hold the largest market share and serve as the backbone for many applications requiring high-viscosity product mixing, inline and continuous systems are increasingly gaining popularity in modern high-throughput plants as their benefits become more widely recognized.

"By application, the food products segment is expected to account for a significant share of the high shear mixers market during the forecast period."

Food products hold the largest market share in the high shear mixer applications segment. Major application areas include baby food, infant formula, soups, sauces, batters, coffee creamers, custards, dips, mayonnaise, medical foods, special dietary products, sports nutrition, meal replacements, and pet foods, among others, all of which use high shear mixers to meet their specific application requirements. High shear mixing systems are increasingly used to process complex formulations that often require blending multiple ingredients, dispersing fine particles, and adjusting viscosity. Many of these processes involve multi-phase systems, such as oil-in-water emulsions and solid-liquid suspensions, where preventing phase separation is crucial. This segment is expected to grow further as the popularity of functional and fortified food products rises, where precision blending is vital to product efficacy and performance. Additionally, the increasing demand for convenience and ready-to-eat food products is likely to benefit the segment, as high shear mixers offer excellent performance at scale, ensuring high efficiency and productivity.

"By mixing application, the emulsification segment is expected to account for a significant share of the high shear mixers market."

Emulsification is the leading application segment in the high shear mixers market, as it is essential for creating stable emulsions of two immiscible liquids, such as oil and water. High shear mixers are specifically designed to generate the high shear conditions necessary for producing fine and stable emulsions. These emulsifiers are used across various sectors of the food & beverage industry, including dairy products (such as yogurt, enriched milk, recombined milk, and fortified milk), beverages (such as carbonated soft drinks and coffee drinks), sauces, ice creams, and salad dressings. Achieving a stable emulsion is critically important for enhancing texture and mouthfeel, as well as for preserving products that often contain added functional ingredients. Growing consumer demand for higher-quality, more visually appealing, and shelf-stable products is driving the use of high shear mixers in the emulsification segment. High shear technology simplifies processing, reduces the need for stabilizers, and improves formulation performance. As food manufacturing companies continue to innovate and optimize multi-phase recipes, the emulsification segment is expected to maintain a significant share of the high shear mixers market.

In-depth interviews have been conducted with chief executive officers (CEOs), directors, and other executives from key organizations operating in the high shear mixers market.

- By Company Type: Tier 1 (30%), Tier 2 (25%), and Tier 3 (45%)

- By Designation: CXOs (25%), Managers (35%), Others (40%)

- By Region: North America (20%), Europe (30%), Asia Pacific (35%), South America (10%), and the Rest of the World (5%)

Research Coverage

This research report categorizes the high shear mixers market by system type (batch mixers, inline mixers), configuration (batch mixing systems, recirculation mixing systems, continuous mixing systems, hybrid systems), mixing application (emulsification, homogenization, dispersion, particle size reduction), application (dairy, cheese, ice cream, food products, dairy alternatives, beverages, other food products), and region (North America, Europe, Asia Pacific, South America, and the Rest of the World).

The report provides comprehensive insights into the high shear mixers industry, highlighting key factors such as drivers, restraints, challenges, and opportunities that impact its growth. It includes an in-depth analysis of the major industry players, detailing their business activities, services, key strategies, contracts, partnerships, agreements, product launches, mergers and acquisitions and recent developments in the high shear mixers market.

Additionally, the report includes a competitive analysis of emerging startups in the high shear mixers market ecosystem. It also addresses industry-specific trends, including technology analysis, ecosystem and market mapping, and the patent and regulatory landscape, among other topics.

Reasons to Buy This Report

The report provides market leaders/new entrants with information on the closest approximations of revenue numbers for the overall High Shear Mixers and its subsegments. It will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (increasing demand for processed and convenience foods boosts the demand for high shear mixers), restraints (high capital cost of advanced high shear mixing systems), opportunities (adoption of continuous and inline mixing technologies), and challenges (handling complex multi-phase formulations) influencing the growth of the high shear mixers market

- Product Development/Innovation: Detailed insights into research & development activities and new product launches in the high shear mixers market

- Market Development: Comprehensive information about the market analysis of high shear mixers across varied regions

- Market Diversification: Exhaustive information about new product sources, untapped geographies, recent developments, and investments in the high shear mixers market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, brand/product comparison, and product footprints of leading players such as GEA Group Aktiengesellschaft (Germany), SPX FLOW, Inc. (US), Tetra Laval Group (Switzerland), IDEX Corporation (US), Buhler Holding AG (Switzerland), EBARA Corporation (Japan), Silverson Machines Ltd. (UK), IKA-Werke GmbH & Co. KG (Germany), Charles Ross & Son Company (US), Admix, Inc. (US), ystral GmbH Maschinenbau + Prozesstechnik (Germany), ProXES GmbH (Germany), INOXPA S.A.U. (Spain), Schold Manufacturing, LLC (US), ARDE-Barinco Inc. (US), and other players in the high shear mixers market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.5.1 CURRENCY UNIT

- 1.5.2 VOLUME UNIT

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HIGH SHEAR MIXERS MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN HIGH SHEAR MIXERS MARKET

- 3.2 HIGH SHEAR MIXERS MARKET, BY MIXING APPLICATION AND REGION

- 3.3 HIGH SHEAR MIXERS MARKET, BY SYSTEM TYPE

- 3.4 HIGH SHEAR MIXERS MARKET, BY APPLICATION

- 3.5 HIGH SHEAR MIXERS MARKET, BY CONFIGURATION

- 3.6 HIGH SHEAR MIXERS MARKET, BY MIXING APPLICATION

- 3.7 HIGH SHEAR MIXERS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Stringent food safety regulations and preventive control requirements

- 4.2.1.2 Growing demand for operational efficiency and reduced processing time

- 4.2.1.3 Advancement in rotor-stator technology and automation integration

- 4.2.1.4 Rising adoption in pharmaceutical and biologics manufacturing

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital expenditure and maintenance cost requirements

- 4.2.2.2 Technical complexity and skilled labor requirements

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of advanced control systems and digital monitoring capabilities

- 4.2.3.2 Geographic expansion into Southeast Asian manufacturing markets

- 4.2.4 CHALLENGES

- 4.2.4.1 Limited product differentiation

- 4.2.4.2 Intense price competition

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN HIGH SHEAR MIXERS MARKET

- 4.3.1.1 Process consistency and real-time quality monitoring

- 4.3.1.2 Cost-effective and scalable solutions for emerging markets

- 4.3.1.3 Digital integration and smart manufacturing compatibility

- 4.3.1.4 Energy efficiency and maintenance optimization

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Smart and sensor-integrated mixing systems

- 4.3.2.2 Flexible commercial deployment models

- 4.3.2.3 Integrated continuous processing solutions

- 4.3.2.4 Digitally connected and automated mixing ecosystems

- 4.3.1 UNMET NEEDS IN HIGH SHEAR MIXERS MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMICS OUTLOOK

- 5.2.1 RISING GLOBAL POPULATION AND INCREASING FOOD DEMAND

- 5.2.2 COST PRESSURES & INFLATION

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.3.1 UPSTREAM (RAW MATERIALS & COMPONENT SUPPLIERS)

- 5.3.2 COMPONENT MANUFACTURING & SUBASSEMBLY

- 5.3.3 EQUIPMENT MANUFACTURING (CORE STAGE)

- 5.3.4 DISTRIBUTION & INSTALLATION

- 5.3.5 END USERS

- 5.3.6 SUPPORTING ECOSYSTEM

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE SELLING PRICE OF KEY PLAYERS, BY SYSTEM TYPE

- 5.5.2 AVERAGE SELLING PRICE, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 847982)

- 5.6.2 EXPORT SCENARIO (HS CODE 847982)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.11 IMPACT OF 2025 US TARIFFS - HIGH SHEAR MIXERS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.6 TRUMP TARIFF UPDATE (2026) AND LEGAL DEVELOPMENTS

6 TECHNOLOGY ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ROTOR-STATOR TECHNOLOGY

- 6.1.2 SOLID-LIQUID INJECTION MANIFOLD (SLIM) AND POWDER INDUCTION TECHNOLOGY

- 6.1.3 VARIABLE FREQUENCY DRIVE (VFD) AND PRECISION SPEED CONTROL TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CLEAN-IN-PLACE (CIP) AND STERILIZE-IN-PLACE (SIP) SYSTEMS

- 6.2.2 PROCESS ANALYTICAL TECHNOLOGY (PAT) AND INLINE SENSING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 HIGH-PRESSURE HOMOGENIZATION (HPH)

- 6.3.2 ULTRASONIC HOMOGENIZATION TECHNOLOGY

- 6.4 PATENT ANALYSIS

- 6.4.1 INTRODUCTION

- 6.4.2 LIST OF MAJOR PATENTS, JANUARY 2016-DECEMBER 2025

- 6.5 FUTURE APPLICATIONS

- 6.5.1 LIPID NANOPARTICLE (LNP) & M-RNA THERAPEUTICS MANUFACTURING

- 6.5.2 ALTERNATIVE PROTEIN & PLANT-BASED FOOD MANUFACTURING

- 6.5.3 BATTERY ELECTRODE SLURRY MANUFACTURING

- 6.5.4 CONTINUOUS PHARMACEUTICAL MANUFACTURING (CPM)

- 6.5.5 GREEN HYDROGEN, CARBON CAPTURE & ENERGY APPLICATIONS

- 6.6 IMPACT OF AI/GEN AI ON HIGH SHEAR MIXERS SERVICE INDUSTRY

- 6.6.1 TOP USE CASES AND MARKET POTENTIALS

- 6.6.2 BEST PRACTICES IN HIGH SHEAR MIXERS INDUSTRY

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN HIGH SHEAR MIXERS MARKET

- 6.6.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 READINESS TO ADOPT GENERATIVE AI IN HIGH SHEAR MIXERS MARKET

- 6.7 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.7.1 GEA GROUP: PIONEERING AI-DRIVEN DIGITAL TRANSFORMATION IN MIXING & PROCESSING

- 6.7.2 SPX FLOW X SIEMENS: DIGITAL TWIN AND AI FOR MIXING AT MXD INNOVATION HUB

- 6.7.3 GEA GROUP: AI FOR NEW FOOD & ALTERNATIVE PROTEIN MIXING OPTIMIZATION

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY FRAMEWORK

- 7.1.1.1 North America

- 7.1.1.1.1 US

- 7.1.1.1.2 Canada

- 7.1.1.1.3 Mexico

- 7.1.1.2 Europe

- 7.1.1.2.1 Germany

- 7.1.1.2.2 UK

- 7.1.1.2.3 France

- 7.1.1.2.4 Italy

- 7.1.1.2.5 Rest of Europe

- 7.1.1.3 Asia Pacific

- 7.1.1.3.1 China

- 7.1.1.3.2 India

- 7.1.1.3.3 Japan

- 7.1.1.3.4 Australia and New Zealand

- 7.1.1.3.5 Rest of Asia Pacific

- 7.1.1.4 South America

- 7.1.1.4.1 Brazil

- 7.1.1.4.2 Argentina

- 7.1.1.5 RoW

- 7.1.1.5.1 Middle East

- 7.1.1.5.2 Africa Region

- 7.1.1.1 North America

- 7.1.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.3 INDUSTRY STANDARDS

- 7.1.4 DOCUMENTATION REQUIREMENTS

- 7.1.5 ANTICIPATED REGULATORY CHANGES IN NEXT 5-10 YEARS

- 7.1.1 REGULATORY FRAMEWORK

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.3.1 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY SYSTEM TYPE

9 HIGH SHEAR MIXERS MARKET, BY SYSTEM TYPE

- 9.1 INTRODUCTION

- 9.2 BATCH MIXERS

- 9.3 INLINE MIXERS

10 HIGH SHEAR MIXERS MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 DAIRY

- 10.2.1 EXPANDING GLOBAL DAIRY PROCESSING TO DRIVE HIGH-SHEAR MIXER DEMAND

- 10.3 CHEESE

- 10.3.1 GROWING PROCESSED AND ANALOGUE CHEESE PRODUCTION TO DRIVE HIGH-SHEAR MIXER ADOPTION

- 10.4 ICE CREAM

- 10.4.1 RISING INDUSTRIAL ICE CREAM PRODUCTION AND CONSUMPTION TO DRIVE HIGH-SHEAR MIXER DEMAND

- 10.5 FOOD PRODUCTS

- 10.5.1 RISING GLOBAL DEMAND FOR PROCESSED AND FUNCTIONAL FOODS TO DRIVE HIGH-SHEAR MIXER ADOPTION

- 10.6 DAIRY ALTERNATIVES

- 10.6.1 RAPID EXPANSION OF PLANT-BASED FOOD AND BEVERAGE PRODUCTION TO ACCELERATE HIGH-SHEAR MIXER DEMAND

- 10.7 BEVERAGES

- 10.7.1 RISE IN GLOBAL BEVERAGE PRODUCTION AND PROCESSING INTENSITY TO DRIVE HIGH SHEAR MIXER DEMAND

- 10.7.2 ALCOHOLIC BEVERAGES

- 10.7.3 NON-ALCOHOLIC BEVERAGES

- 10.8 OTHER FOOD PRODUCTS

11 HIGH SHEAR MIXERS MARKET, BY CONFIGURATION

- 11.1 INTRODUCTION

- 11.2 BATCH MIXING SYSTEMS

- 11.2.1 COMPLEX FORMULATIONS AND CONTROLLED HIGH SHEAR PROCESSING TO DRIVE BATCH SYSTEM DOMINANCE

- 11.3 RECIRCULATION MIXING SYSTEMS

- 11.3.1 ENHANCED DISPERSION EFFICIENCY AND MULTI-PASS SHEAR PROCESSING TO DRIVE RECIRCULATION SYSTEM ADOPTION

- 11.4 CONTINUOUS MIXING SYSTEMS

- 11.4.1 SHIFT TOWARD CONTINUOUS FOOD PROCESSING TO ACCELERATE INLINE HIGH SHEAR MIXING ADOPTION

- 11.5 HYBRID SYSTEMS

- 11.5.1 NEED FOR FLEXIBLE PROCESSING COMBINING BATCH CONTROL AND CONTINUOUS EFFICIENCY TO DRIVE HYBRID HSM ADOPTION

12 HIGH SHEAR MIXERS MARKET, BY MIXING APPLICATION

- 12.1 INTRODUCTION

- 12.2 EMULSIFICATION

- 12.2.1 DOMINANT APPLICATION DRIVEN BY DEMAND FOR STABLE LIQUID-LIQUID SYSTEMS

- 12.3 HOMOGENIZATION

- 12.3.1 ENSURING PRODUCT UNIFORMITY ACROSS LARGE-SCALE FOOD AND BEVERAGE PROCESSING

- 12.4 DISPERSION

- 12.4.1 INCREASING USE OF POWDERED INGREDIENTS TO DRIVE HIGH SHEAR DISPERSION APPLICATIONS

- 12.5 PARTICLE SIZE REDUCTION

- 12.5.1 DEMAND FOR TEXTURE CONTROL AND PRODUCT STABILITY TO DRIVE PARTICLE SIZE REDUCTION

13 HIGH SHEAR MIXERS, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Large-scale, multi-stage food processing industry driving demand for high-performance mixing technologies

- 13.2.2 CANADA

- 13.2.2.1 Strong focus on value-added and export-oriented food production supporting advanced mixing adoption

- 13.2.3 MEXICO

- 13.2.3.1 Expanding food manufacturing base and export integration driving demand for industrial mixing systems

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Advanced food processing automation and engineering capabilities driving high shear mixer adoption

- 13.3.2 FRANCE

- 13.3.2.1 Strong dairy and value-added food production supporting demand for precision mixing technologies

- 13.3.3 UK

- 13.3.3.1 Growing demand for processed and plant-based foods driving mixing technology adoption

- 13.3.4 ITALY

- 13.3.4.1 Strong presence in processed food, sauces, and dairy driving demand for batch mixing systems

- 13.3.5 SPAIN

- 13.3.5.1 Expanding processed food and beverage sector driving adoption of efficient mixing technologies

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Large-scale industrial food processing and dairy expansion driving dominant HSM demand

- 13.4.2 INDIA

- 13.4.2.1 Rapid growth in dairy processing and government-led food processing expansion driving HSM adoption

- 13.4.3 JAPAN

- 13.4.3.1 High-value, precision-driven food processing industry supporting advanced HSM adoption

- 13.4.4 AUSTRALIA & NEW ZEALAND

- 13.4.4.1 Export-oriented dairy processing and premium product focus driving HSM demand

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Largest food processing and agricultural economy in the region, driving strong HSM demand

- 13.5.2 ARGENTINA

- 13.5.2.1 Export-driven dairy and processed food sector supporting adoption of precision mixing technologies

- 13.5.3 REST OF SOUTH AMERICA

- 13.5.1 BRAZIL

- 13.6 REST OF THE WORLD (ROW)

- 13.6.1 MIDDLE EAST

- 13.6.1.1 High dependence on dairy and food imports driving demand for reconstitution and mixing technologies

- 13.6.2 AFRICA

- 13.6.2.1 Expanding food processing capacity and rising dairy consumption driving gradual high shear mixer adoption

- 13.6.1 MIDDLE EAST

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2020-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY VALUATION AND FINANCIAL METRICS

- 14.5.1 COMPANY VALUATION

- 14.5.2 EV/EBITDA

- 14.6 BRAND COMPARISON ANALYSIS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Regional footprint

- 14.7.5.3 System type footprint

- 14.7.5.4 Application footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: KEY STARTUPS/SMES, 2025

- 14.8.5.1 Detailed list of key startups/SMEs

- 14.8.5.2 Competitive benchmarking of key startups/SMEs

- 14.9 COMPETITIVE SCENARIO AND TRENDS

- 14.9.1 PRODUCT LAUNCHES

- 14.9.2 DEALS

- 14.9.3 EXPANSIONS

- 14.9.4 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 GEA GROUP AKTIENGESELLSCHAFT

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.3.2 Expansions

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 SPX FLOW, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Deals

- 15.1.2.3.2 Expansions

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 TETRA LAVAL GROUP

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Expansions

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 IDEX CORPORATION

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 BUHLER HOLDING AG

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 SILVERSON MACHINES

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.4 MnM view

- 15.1.7 IKA-WERKE GMBH & CO. KG

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.7.4 MnM view

- 15.1.8 CHARLES ROSS & SON COMPANY

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.4 MnM view

- 15.1.9 ADMIX, INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches

- 15.1.9.3.2 Deals

- 15.1.9.4 MnM view

- 15.1.10 YSTRAL GMBH MASCHINENBAU + PROCESSTECHNIK

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Expansions

- 15.1.10.4 MnM view

- 15.1.11 PROXES GMBH

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Expansions

- 15.1.11.4 MnM view

- 15.1.12 INOXPA S.A.U.

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches

- 15.1.12.3.2 Expansions

- 15.1.12.4 MnM view

- 15.1.13 SCHOLD MANUFACTURING, LLC

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.13.4 MnM view

- 15.1.14 EBARA CORPORATION

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product Launch

- 15.1.14.4 MnM view

- 15.1.15 ARDE-BARINCO, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.4 MnM view

- 15.1.1 GEA GROUP AKTIENGESELLSCHAFT

- 15.2 STARTUPS/SMES

- 15.2.1 PRIMIX CORPORATION

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.4 MnM view

- 15.2.2 MXD PROCESS

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Deals

- 15.2.2.4 MnM view

- 15.2.3 PERMIX TEC CO., LTD.

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.4 MnM view

- 15.2.4 LEE INDUSTRIES

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.4 MnM view

- 15.2.5 JINHU GINHONG MACHINERY CO., LTD.

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.4 MnM view

- 15.2.6 HOCKMEYER EQUIPMENT CORPORATION

- 15.2.7 MAELSTROM ADVANCED PROCESS TECHNOLOGIES LIMITED

- 15.2.8 WAHAL ENGINEERS PVT. LTD.

- 15.2.9 FLUKO EQUIPMENT SHANGHAI CO., LTD.

- 15.2.10 SPM PROCESS SYSTEMS

- 15.2.1 PRIMIX CORPORATION

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Breakdown of primary profiles

- 16.1.2.3 Key insights from industry experts

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH (BASED ON APPLICATION, BY REGION)

- 16.2.2 TOP-DOWN APPROACH (BASED ON GLOBAL MARKET)

- 16.2.3 SUPPLY SIDE

- 16.2.4 DEMAND SIDE

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

17 ADJACENT AND RELATED MARKETS

- 17.1 INTRODUCTION

- 17.2 RESEARCH LIMITATIONS

- 17.3 FOOD & BEVERAGE PROCESSING EQUIPMENT MARKET

- 17.3.1 MARKET DEFINITION

- 17.3.2 MARKET OVERVIEW

- 17.3.3 FOOD & BEVERAGE PROCESSING EQUIPMENT MARKET, BY TYPE

- 17.4 BAKERY PROCESSING EQUIPMENT MARKET

- 17.4.1 MARKET DEFINITION

- 17.4.2 MARKET OVERVIEW

- 17.4.3 BAKERY PROCESSING EQUIPMENT MARKET, BY TYPE

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS