|

시장보고서

상품코드

2037802

항공기 시트 시장 예측(-2031년) : 시트 유형별, 시트 클래스별, 컴포넌트별, 플랫폼별, 재료별, 최종사용자별, 지역별Aircraft Seating Market by Seat Type, Seat Class, Component, Platform, Material, End User, Region - Global Forecast to 2031 |

||||||

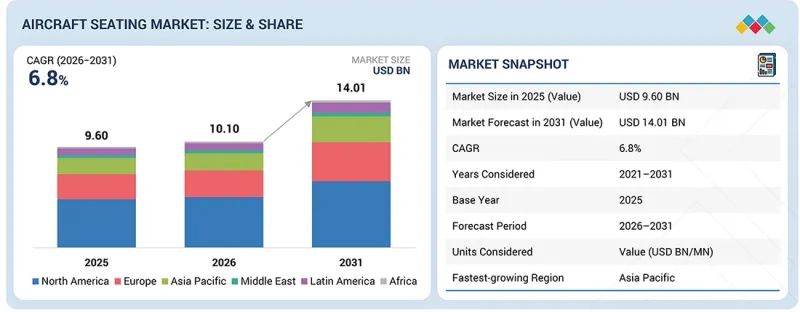

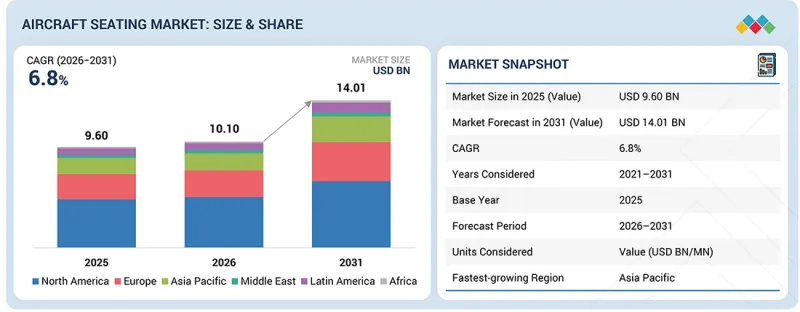

세계의 항공기 시트 시장 규모는 2026년 101억 달러에서 2031년까지 140억 1,000만 달러에 달할 것으로 예측되며, CAGR로 6.8%의 성장이 전망되고 있습니다.

항공 승객 수의 증가가 이 시장의 주요 성장 요인으로 작용하고 있습니다. 또한 항공사의 항공기 보유량도 확대되고 있으며, 새로운 항공기에 대한 강한 수요를 창출하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 단위 | 10억 달러 |

| 부문 | 시트 유형, 컴포넌트, 최종사용자, 지역 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

또한 항공사는 인체공학적 개선과 새로운 기능을 통해 승객의 편안함과 전반적인 여행 경험에 더 많은 관심을 기울이고 있습니다. 경량 소재의 사용이 증가하고 있으며, 모듈식 시트도 보편화되고 있습니다. 이러한 추세는 연료 효율 개선과 운항 실적 향상에 기여하고 있습니다.

가전제품은 예측 기간 중 가장 빠르게 성장하는 부품이 될 것으로 예상됩니다.

항공사가 기내 좌석내 전력 시스템, 조명, 커넥티비티 기능을 채택함에 따라 전기 기기 부문이 빠르게 성장하고 있습니다. 항공사는 USB 포트, 충전 포인트, 내장형 엔터테인먼트 시스템을 추가하여 승객 경험을 향상시키고 있습니다. 항공기 시스템의 전기화로의 전환도 첨단 가전제품에 대한 수요를 촉진하고 있습니다. 정기적인 객실 업그레이드와 리노베이션도 이 부문의 성장을 더욱 촉진하고 있습니다.

프리미엄 이코노미 클래스는 예측 기간 중 가장 높은 CAGR을 기록할 것으로 예상됩니다.

비즈니스석보다 저렴한 가격에 더 높은 편안함을 원하는 승객이 증가함에 따라 프리미엄 이코노미 부문이 성장하고 있습니다. 항공사는 더 높은 가성비를 원하는 레저 고객과 비즈니스 고객을 모두 끌어들이기 위해 프리미엄 이코노미의 선택 폭을 넓히고 있습니다. 또한 이 부문은 이코노미 부문보다 이익률이 높기 때문에 항공사는 프리미엄 좌석을 늘리고 있습니다. 또한 장거리 여행의 증가는 이 카테고리에서 더 편안한 좌석에 대한 수요를 지원하고 있습니다.

북미가 예측 기간 중 가장 큰 지역 시장이 될 것으로 예상됩니다.

북미가 주도적인 위치를 차지하는 주요 원인은 주요 항공기 제조업체와 항공사의 존재에 있습니다. 또한 승객 수가 많고 항공기 납품이 진행 중이기 때문에 새로운 좌석 시스템에 대한 수요는 안정적입니다. 또한 항공사들은 승객의 경험을 향상시키기 위해 객실 업그레이드 및 리노베이션 프로그램에 투자하고 있습니다. 첨단 시트 기술의 조기 도입과 강력한 애프터마켓 지원으로 시장 성장을 더욱 촉진하고 있습니다.

세계의 항공기 시트 시장에 대해 조사 분석했으며, 주요 촉진요인 및 저해요인, 제품 개발 및 혁신, 경쟁 구도 등의 정보를 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 항공기 시트 시장 : 항공기별

제10장 항공기 시트 시장 : 재료별

제11장 항공기 시트 시장 : 시트 유형별

제12장 항공기 시트 시장 : 최종사용자별

제13장 항공기 시트 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.06.01The aircraft seating market is expected to reach USD 14.01 billion by 2031, from USD 10.10 billion in 2026, with a CAGR of 6.8%. Rising air passenger traffic is a key driver of this market. Airline fleets are also expanding, creating strong demand for new aircraft.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Seat Type, Component, End User and Region |

| Regions covered | North America, Europe, APAC, RoW |

Additionally, airlines are placing greater emphasis on passenger comfort and the overall travel experience, achieved through improved ergonomics and new features. The use of lightweight materials is increasing, and modular seating is becoming common. These trends help improve fuel efficiency and support better operational performance.

Electrical fittings are expected to be the fastest-growing component during th e forecast period.

The electrical fittings segment is growing quickly as airlines increasingly adopt in-seat power systems, lighting, and connectivity features in aircraft cabins. Airlines are enhancing the passenger experience by adding USB ports, charging points, and built-in entertainment systems. The shift toward more electric aircraft systems is also driving demand for advanced electrical parts. Routine cabin upgrades and retrofitting are further fueling this segment's growth.

The premium economy seat class is expected to record the highest CAGR during the forecast period.

The premium economy segment is growing as more passengers seek greater comfort at a lower price than business class. Airlines are adding more premium economy options to attract both leisure and business travelers seeking better value. This segment also offers higher margins than the economy segment, so airlines are increasing the number of premium seats. Additionally, growth in long-haul travel is supporting demand for better seating in this category.

North America is expected to be the largest regional market during the forecast period.

North America's dominance is mainly due to the presence of leading aircraft manufacturers and major airline operators. Additionally, passenger traffic is high, and aircraft deliveries are ongoing, keeping demand for new seating systems steady. Airlines are also investing in cabin upgrades and retrofitting programs to improve the passenger experience. Early adoption of advanced seating technologies and strong aftermarket support are driving further market growth.

The breakdown of profiles for primary participants in the aircraft seating market is provided below:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 25%, Europe - 15%, Asia Pacific - 45%, Middle East - 10%, and Rest of the World - 5%

Research Coverage:

This market study examines the aircraft seating market across segments and subsegments. It aims to estimate the market's size and growth potential across regions. The study also provides a detailed competitive analysis of key market players, including their company profiles, product offerings, recent developments, and strategic market initiatives.

Reasons to buy this report:

The report will assist market leaders and new entrants by providing revenue estimates for the overall aircraft seating market. It will also enable stakeholders to better understand the competitive landscape, gain insights to position their businesses more effectively, and develop appropriate go-to-market strategies. Additionally, the report will help stakeholders understand market dynamics and provide insights into key drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market Drivers (Focus on enhancing passenger experience and cabin differentiation), Restraints (High cost of advanced seating systems and integration), Opportunities (Integration of smart and connected seating technologies), and Challenges (Managing long lead times and program delays in seat production and installation)

- Market Penetration: Comprehensive information on aircraft seating offered by the top market players

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the aircraft seating market.

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the aircraft seating market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the aircraft seating market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AIRCRAFT SEATING MARKET

- 2.4 HIGH GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AIRCRAFT SEATING MARKET

- 3.2 AIRCRAFT SEATING MARKET, BY SEAT TYPE

- 3.3 AIRCRAFT SEATING MARKET, BY SEAT CLASS

- 3.4 AIRCRAFT SEATING MARKET, BY END USER

- 3.5 AIRCRAFT SEATING MARKET, BY AIRCRAFT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing focus on enhancing passenger experience and cabin differentiation

- 4.2.1.2 Increasing emphasis on lightweight seating for fuel efficiency and cost optimization

- 4.2.1.3 Rising adoption of premium seating and ancillary revenue models

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of advanced seating systems and integration

- 4.2.2.2 Stringent regulatory and certification requirements

- 4.2.2.3 Limited cabin space and design constraints

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Integration of smart and connected seating technologies

- 4.2.3.2 Increasing demand for sustainable and eco-friendly seating solutions

- 4.2.3.3 Growth in low-cost carriers and high-density seating demand

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing long lead times and program delays in seat production and installation

- 4.2.4.2 Managing aftermarket maintenance and lifecycle support for seating systems

- 4.2.4.3 Managing passenger comfort expectations across diverse travel segments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 CONVERGENCE WITH AIRCRAFT MRO, LEASING, AND AFTERMARKET ECOSYSTEMS

- 4.4.2 INTEGRATION WITH AIRLINE REVENUE MANAGEMENT AND CABIN MONETIZATION STRATEGIES

- 4.4.3 CONVERGENCE WITH AIRPORT OPERATIONS AND PASSENGER-FLOW MANAGEMENT SYSTEMS

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 GDP TRENDS AND FORECAST

- 5.2.2 TRENDS IN GLOBAL AVIATION INDUSTRY

- 5.2.3 TRENDS IN GLOBAL AIRCRAFT SEATING INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 R&D ENGINEERS (~30%)

- 5.3.2 RAW MATERIAL SUPPLIERS (10~%)

- 5.3.3 COMPONENT AND PRODUCT MANUFACTURERS (~10%)

- 5.3.4 ASSEMBLERS AND INTEGRATORS (~30%)

- 5.3.5 END USERS (~20%)

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 MANUFACTURERS

- 5.4.2 SOLUTION AND SERVICE PROVIDERS

- 5.4.3 END USERS

- 5.5 INVESTMENT AND FUNDING SCENARIO

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING ANALYSIS, BY PLATFORM

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 9401)

- 5.7.2 EXPORT SCENARIO (HS CODE 9401)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 SAFRAN - LIGHTWEIGHT SEATING SOLUTIONS

- 5.10.2 RECARO - MODULAR AND PASSENGER-CENTRIC SEATING SOLUTIONS

- 5.10.3 ZIM AIRCRAFT SEATING - HIGH-DENSITY AND COST-EFFICIENT CABIN DESIGN

- 5.10.4 EXPLISEAT - ULTRA-LIGHTWEIGHT SEATING FOR EFFICIENCY

- 5.11 IMPACT OF 2025 US TARIFFS

- 5.11.1 KEY TARIFF RATES

- 5.11.2 PRICE IMPACT ANALYSIS

- 5.11.3 IMPACT ON COUNTRY/REGION

- 5.11.3.1 US

- 5.11.3.2 Europe

- 5.11.3.3 Asia Pacific

- 5.11.4 IMPACT ON END USERS

- 5.11.4.1 Commercial

- 5.11.4.2 Government & military

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 LIGHTWEIGHT COMPOSITE-BASED SEATING STRUCTURES

- 6.1.2 SMART SEATING WITH CONNECTIVITY AND INTEGRATED ELECTRONICS

- 6.1.3 MODULAR AND FLEXIBLE SEATING ARCHITECTURES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ADVANCED MATERIAL COATINGS AND ANTIMICROBIAL SURFACES

- 6.2.2 DIGITAL CABIN MANAGEMENT AND CONNECTED ECOSYSTEMS

- 6.2.3 ADDITIVE MANUFACTURING (3D PRINTING) FOR COMPONENT PRODUCTION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ADVANCED CABIN CONFIGURATION AND SPACE OPTIMIZATION SOLUTIONS

- 6.3.2 IN-FLIGHT ENTERTAINMENT AND DIGITAL EXPERIENCE PLATFORMS

- 6.3.3 CABIN LIGHTING AND ENVIRONMENTAL CONTROL SYSTEMS

- 6.3.4 CABIN HEALTH MONITORING AND AIR QUALITY MANAGEMENT SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GENERATIVE AI

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL IN AIRCRAFT SEATING MARKET

- 6.7.2 CASE STUDIES OF AI IMPLEMENTATION

- 6.7.3 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF AIRCRAFT SEATING

- 7.2.2 ECO-APPLICATIONS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3.1 SUSTAINABILITY IMPACT ON AIRCRAFT SEATING MARKET

- 7.3.2 REGULATORY POLICIES DRIVING AIRCRAFT SEATING

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END USERS

- 8.4.1 NEED FOR LIGHTWEIGHT AND FUEL-EFFICIENT SEATING SOLUTIONS

- 8.4.2 NEED FOR ENHANCED PASSENGER COMFORT AND DIFFERENTIATION

- 8.4.3 NEED FOR MODULAR AND RAPID RETROFIT SOLUTIONS

9 AIRCRAFT SEATING MARKET, BY AIRCRAFT (MARKET SIZE & FORECAST TO 2031 - USD MILLION & UNITS)

- 9.1 INTRODUCTION

- 9.2 NARROW-BODY AIRCRAFT

- 9.2.1 HIGH FLEET UTILIZATION AND LOW-COST CARRIER EXPANSION TO DRIVE GROWTH

- 9.2.1.1 Use case: BL3710 economy class seat by Recaro Aircraft Seating in narrow-body aircraft

- 9.2.1 HIGH FLEET UTILIZATION AND LOW-COST CARRIER EXPANSION TO DRIVE GROWTH

- 9.3 WIDE-BODY AIRCRAFT

- 9.3.1 INCREASING LONG-HAUL TRAVEL DEMAND AND PREMIUM CABIN EXPANSION TO DRIVE GROWTH

- 9.3.1.1 Use case: Elevation business class seat by Safran Seats in wide-body aircraft

- 9.3.1 INCREASING LONG-HAUL TRAVEL DEMAND AND PREMIUM CABIN EXPANSION TO DRIVE GROWTH

- 9.4 REGIONAL TRANSPORT AIRCRAFT

- 9.4.1 INCREASING REGIONAL CONNECTIVITY AND COST-EFFICIENT SEATING SOLUTIONS TO DRIVE GROWTH

- 9.4.1.1 Use case: Meridian economy class seat by Collins Aerospace in regional transport aircraft

- 9.4.1 INCREASING REGIONAL CONNECTIVITY AND COST-EFFICIENT SEATING SOLUTIONS TO DRIVE GROWTH

- 9.5 BUSINESS JETS

- 9.5.1 RISING DEMAND FOR LUXURY TRAVEL AND CUSTOMIZED CABIN SOLUTIONS TO DRIVE GROWTH

- 9.5.1.1 Use case: Nuage business class seat by Collins Aerospace in business jets

- 9.5.1 RISING DEMAND FOR LUXURY TRAVEL AND CUSTOMIZED CABIN SOLUTIONS TO DRIVE GROWTH

- 9.6 COMMERCIAL HELICOPTERS

- 9.6.1 INCREASING OFFSHORE OPERATIONS AND URBAN AIR MOBILITY DEMAND TO DRIVE GROWTH

- 9.6.1.1 Use case: Energy-absorbing helicopter seat by Collins Aerospace in commercial helicopters

- 9.6.1 INCREASING OFFSHORE OPERATIONS AND URBAN AIR MOBILITY DEMAND TO DRIVE GROWTH

- 9.7 LIGHT & ULTRALIGHT AIRCRAFT

- 9.7.1 GROWING RECREATIONAL AVIATION AND PILOT TRAINING ACTIVITIES TO DRIVE GROWTH

- 9.7.1.1 Use case: Lightweight pilot seat by Recaro Aircraft Seating in light & ultralight aircraft

- 9.7.1 GROWING RECREATIONAL AVIATION AND PILOT TRAINING ACTIVITIES TO DRIVE GROWTH

- 9.8 URBAN AIR MOBILITY (UAM)

- 9.8.1 ADVANCEMENTS IN EVTOL AIRCRAFT AND DEMAND FOR SPACE-EFFICIENT SEATING TO DRIVE GROWTH

- 9.8.1.1 Use case: Lightweight modular passenger seats by Joby Aviation in urban air mobility

- 9.8.1 ADVANCEMENTS IN EVTOL AIRCRAFT AND DEMAND FOR SPACE-EFFICIENT SEATING TO DRIVE GROWTH

10 AIRCRAFT SEATING MARKET, BY MATERIAL (MARKET SIZE & FORECAST TO 2031-USD MILLION)

- 10.1 INTRODUCTION

- 10.2 ROADMAP TO SEATING MATERIAL ADVANCEMENTS IN AIRCRAFT SEATING INDUSTRY

- 10.3 CUSHION MATERIAL

- 10.3.1 POLYURETHANE

- 10.3.1.1 Advancements in high-performance foam technologies to drive growth

- 10.3.1.2 Use case: Advanced polyurethane foam cushion by Recaro Aircraft Seating

- 10.3.2 POLYETHYLENE

- 10.3.2.1 Increasing demand for lightweight and impact-resistant cushioning solutions to drive growth

- 10.3.2.2 Use case: Polyethylene foam cushion by Safran Seats

- 10.3.3 NEOPRENE

- 10.3.3.1 Growing demand for moisture-resistant and high-durability cushioning materials to drive growth

- 10.3.3.2 Use case: Neoprene-based cushion layer by Collins Aerospace

- 10.3.4 OTHERS

- 10.3.4.1 Use case: Hybrid memory foam and gel cushion by Safran Seats

- 10.3.1 POLYURETHANE

- 10.4 STRUCTURE MATERIAL

- 10.4.1 ALUMINUM

- 10.4.1.1 Cost-effectiveness and proven structural performance to drive growth

- 10.4.1.2 Use case: Aluminum seat frame by Safran Seats

- 10.4.2 CARBON FIBER

- 10.4.2.1 Increasing adoption of advanced composites for weight reduction and performance enhancement to drive growth

- 10.4.2.2 Use case: Carbon-fiber seat frame by Recaro Aircraft Seating

- 10.4.3 FIBERGLASS

- 10.4.3.1 Increasing adoption of cost-effective composite materials to drive growth

- 10.4.3.2 Use case: Fiberglass seat shell by Collins Aerospace

- 10.4.4 OTHERS

- 10.4.4.1 Use case: Titanium-reinforced seat structure by Safran Seats

- 10.4.1 ALUMINUM

- 10.5 UPHOLSTERY & SEAT COVER

- 10.5.1 FABRIC

- 10.5.1.1 Increasing demand for cost-efficient, breathable, and durable seating materials to drive growth

- 10.5.1.2 Use case: Performance fabric seat cover by Recaro Aircraft Seating

- 10.5.2 LEATHER

- 10.5.2.1 Growing demand for premium aesthetics and enhanced passenger comfort to drive growth

- 10.5.2.2 Use case: Premium leather seat cover by Safran Seats

- 10.5.3 VINYL

- 10.5.3.1 Increasing adoption of cost-efficient and low-maintenance materials to drive growth

- 10.5.3.2 Use case: Advanced vinyl seat cover by Collins Aerospace

- 10.5.1 FABRIC

11 AIRCRAFT SEATING MARKET, BY SEAT TYPE (MARKET SIZE & FORECAST TO 2031-USD MILLION & UNITS)

- 11.1 INTRODUCTION

- 11.2 PASSENGER SEATS

- 11.2.1 INCREASING DEMAND FOR DIFFERENTIATED CABIN OFFERINGS AND PASSENGER EXPERIENCE TO DRIVE GROWTH

- 11.2.2 FIRST-CLASS SEATS

- 11.2.2.1 By component

- 11.2.2.1.1 Structures

- 11.2.2.1.2 Foams

- 11.2.2.1.3 Actuators

- 11.2.2.1.4 Electrical fittings

- 11.2.2.1.5 Others

- 11.2.2.2 By material

- 11.2.2.2.1 Cushion materials

- 11.2.2.2.2 Structure materials

- 11.2.2.2.3 Upholsteries & seat covers

- 11.2.2.1 By component

- 11.2.3 BUSINESS CLASS SEATS

- 11.2.3.1 By component

- 11.2.3.1.1 Structures

- 11.2.3.1.2 Foams

- 11.2.3.1.3 Actuators

- 11.2.3.1.4 Electrical fittings

- 11.2.3.1.5 Others

- 11.2.3.2 By material

- 11.2.3.2.1 Cushion materials

- 11.2.3.2.2 Structure materials

- 11.2.3.2.3 Upholsteries & seat covers

- 11.2.3.1 By component

- 11.2.4 PREMIUM ECONOMY SEATS

- 11.2.4.1 By component

- 11.2.4.1.1 Structures

- 11.2.4.1.2 Foams

- 11.2.4.1.3 Actuators

- 11.2.4.1.4 Electrical fittings

- 11.2.4.1.5 Others

- 11.2.4.2 By material

- 11.2.4.2.1 Cushion materials

- 11.2.4.2.2 Structure materials

- 11.2.4.2.3 Upholsteries & seat covers

- 11.2.4.1 By component

- 11.2.5 ECONOMY SEATS

- 11.2.5.1 By component

- 11.2.5.1.1 Structures

- 11.2.5.1.2 Foams

- 11.2.5.1.3 Others

- 11.2.5.2 By material

- 11.2.5.2.1 Cushion materials

- 11.2.5.2.2 Structure materials

- 11.2.5.2.3 Upholsteries & seat covers

- 11.2.5.1 By component

- 11.3 PILOT & CREW SEATS

- 11.3.1 INCREASING EMPHASIS ON SAFETY, ERGONOMICS, AND REGULATORY COMPLIANCE TO DRIVE GROWTH

- 11.3.2 PILOT SEATS

- 11.3.2.1 By component

- 11.3.2.1.1 Structures

- 11.3.2.1.2 Foams

- 11.3.2.1.3 Actuators

- 11.3.2.1.4 Electrical fittings

- 11.3.2.1.5 Others

- 11.3.2.2 By material

- 11.3.2.2.1 Cushion materials

- 11.3.2.2.2 Structure materials

- 11.3.2.2.3 Upholsteries & seat covers

- 11.3.2.1 By component

- 11.3.3 CREW SEATS

- 11.3.3.1 By component

- 11.3.3.1.1 Structures

- 11.3.3.1.2 Foams

- 11.3.3.1.3 Actuators

- 11.3.3.1.4 Electrical fittings

- 11.3.3.1.5 Others

- 11.3.3.2 By material

- 11.3.3.2.1 Cushion materials

- 11.3.3.2.2 Structure materials

- 11.3.3.2.3 Upholsteries & seat covers

- 11.3.3.1 By component

12 AIRCRAFT SEATING MARKET, BY END USER (MARKET SIZE & FORECAST TO 2031-USD MILLION & UNITS)

- 12.1 INTRODUCTION

- 12.2 OEM

- 12.2.1 INCREASING AIRCRAFT PRODUCTION AND LINE-FIT SEAT INSTALLATIONS TO DRIVE GROWTH

- 12.2.1.1 Use case: Line-fit seating integration by Collins Aerospace in OEM programs

- 12.2.1 INCREASING AIRCRAFT PRODUCTION AND LINE-FIT SEAT INSTALLATIONS TO DRIVE GROWTH

- 12.3 MRO

- 12.3.1 INCREASING RETROFIT DEMAND AND CABIN REFURBISHMENT ACTIVITIES TO DRIVE GROWTH

- 12.3.1.1 Use case: Cabin seat retrofit program by Lufthansa Technik

- 12.3.1 INCREASING RETROFIT DEMAND AND CABIN REFURBISHMENT ACTIVITIES TO DRIVE GROWTH

- 12.4 AFTERMARKET

- 12.4.1 INCREASING DEMAND FOR SPARE PARTS, UPGRADES, AND CUSTOMIZATION TO DRIVE GROWTH

- 12.4.1.1 Use case: Seat component replacement program by Safran Seats

- 12.4.1 INCREASING DEMAND FOR SPARE PARTS, UPGRADES, AND CUSTOMIZATION TO DRIVE GROWTH

13 AIRCRAFT SEATING MARKET, BY REGION (MARKET SIZE & FORECAST TO 2031 - USD MILLION & UNITS)

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 Increasing aircraft retrofit programs and premium cabin demand to drive market

- 13.2.2 CANADA

- 13.2.2.1 Growing emphasis on premium economy and business class seating to drive market

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 UK

- 13.3.1.1 Premium cabin upgrades and sustainability-driven seating innovations to drive market

- 13.3.2 GERMANY

- 13.3.2.1 Advancements in lightweight seating technologies and strong OEM ecosystem to drive market

- 13.3.3 FRANCE

- 13.3.3.1 Increasing investments in premium seating and cabin innovation to drive market

- 13.3.4 ITALY

- 13.3.4.1 Growing investments in fleet modernization and cabin upgrades to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Increasing demand for modular seating solutions to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 UK

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Continuous fleet expansion by major carriers to drive market

- 13.4.2 INDIA

- 13.4.2.1 Focus on high-density seating configurations for short-haul routes to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Increasing investments in premium cabin seating to drive market

- 13.4.4 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 MIDDLE EAST

- 13.5.1 GCC

- 13.5.1.1 UAE

- 13.5.1.1.1 Increasing adoption of lightweight and modular seating designs to drive market

- 13.5.1.2 Saudi Arabia

- 13.5.1.2.1 Large aircraft order volumes to drive market

- 13.5.1.1 UAE

- 13.5.2 REST OF MIDDLE EAST

- 13.5.1 GCC

- 13.6 LATIN AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 Expansion of low-cost and hybrid carriers to drive market

- 13.6.2 MEXICO

- 13.6.2.1 Growth of low-cost carriers to drive market

- 13.6.3 REST OF LATIN AMERICA

- 13.6.1 BRAZIL

- 13.7 AFRICA

- 13.7.1 SOUTH AFRICA

- 13.7.1.1 Fleet modernization and regional connectivity expansion to drive market

- 13.7.2 NIGERIA

- 13.7.2.1 Increasing investments in new aircraft acquisitions to drive market

- 13.7.3 REST OF AFRICA

- 13.7.1 SOUTH AFRICA

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, JANUARY 2021-MARCH 2026

- 14.3 REVENUE ANALYSIS, 2021-2024

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 OEM ECONOMY AIRCRAFT SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.4.2 AFTERMARKET ECONOMY AIRCRAFT ECONOMY SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.4.3 OEM BUSINESS CLASS AIRCRAFT SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.4.4 AFTERMARKET BUSINESS CLASS AIRCRAFT SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.4.5 OEM FIRST-CLASS AIRCRAFT SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.4.6 AFTERMARKET FIRST-CLASS AIRCRAFT SEATING MARKET SHARE FOR TOP 5 COMPANIES (2025), USD MILLION

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT, KEY PLAYERS, 2025

- 14.7.5.1 Company footprint

- 14.7.5.2 Region footprint

- 14.7.5.3 Aircraft footprint

- 14.7.5.4 Material footprint

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.8.5.1 List of startups/SMEs

- 14.8.5.2 Competitive benchmarking of startups/SMEs

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 RTX

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches/developments

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 SAFRAN

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches/developments

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 RECARO AIRCRAFT SEATING GMBH & CO. KG

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches/developments

- 15.1.3.3.2 Deals

- 15.1.3.3.3 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 STELIA AEROSPACE

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches/developments

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Other developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 ZIM AIRCRAFT SEATING GMBH

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches/developments

- 15.1.5.3.2 Deals

- 15.1.5.3.3 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 IPECO HOLDINGS LTD.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product launches/developments

- 15.1.6.3.2 Deals

- 15.1.7 GEVEN SPA

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches/developments

- 15.1.7.3.2 Deals

- 15.1.8 MARTIN-BAKER AIRCRAFT CO. LTD

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Product launches/developments

- 15.1.8.3.2 Other developments

- 15.1.9 EXPLISEAT

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches/developments

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Other developments

- 15.1.10 ADIENT PLC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches/developments

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Other developments

- 15.1.11 ACRO AIRCRAFT SEATING LTD

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Product launches/developments

- 15.1.11.3.2 Other developments

- 15.1.12 THOMPSON AERO

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches/developments

- 15.1.12.3.2 Deals

- 15.1.12.3.3 Other developments

- 15.1.13 UNUM

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Product launches

- 15.1.13.3.2 Deals

- 15.1.13.3.3 Other developments

- 15.1.14 MIRUS AIRCRAFT SEATING

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches/developments

- 15.1.14.3.2 Deals

- 15.1.15 ST ENGINEERING

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Deals

- 15.1.15.3.2 Other developments

- 15.1.16 JAMCO CORPORATION

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions offered

- 15.1.16.3 Recent developments

- 15.1.16.3.1 Product launches

- 15.1.16.3.2 Deals

- 15.1.16.3.3 Other developments

- 15.1.1 RTX

- 15.2 OTHER PLAYERS

- 15.2.1 AVIOINTERIORS S.P.A.

- 15.2.2 OPTIMARES SPA

- 15.2.3 AIRGO DESIGN

- 15.2.4 JHAS

- 15.2.5 MOBIUS PROTECTION SYSTEMS LTD.

- 15.2.6 ALICEBLUAERO

- 15.2.7 TIMETOOTH TECHNOLOGIES

- 15.2.8 BUTTERFLY FLEXIBLE SEATING SOLUTIONS

- 15.2.9 STARLING AEROSPACE

- 15.2.10 MOLON LABE SEATING

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Primary interview participants

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.2.3 BASE NUMBER CALCULATION

- 16.3 DATA TRIANGULATION

- 16.4 FACTOR ANALYSIS

- 16.4.1 SUPPLY-SIDE INDICATORS

- 16.4.2 DEMAND-SIDE INDICATORS

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 ANNEXURE

- 17.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.4 CUSTOMIZATION OPTIONS

- 17.5 RELATED REPORTS

- 17.6 AUTHOR DETAILS