|

시장보고서

상품코드

2037808

자동차용 HUD 시장 예측(-2033년) : HUD 유형별, 기술별, 승용차 클래스별, 차종별, 추진 유형별, EV 유형별, 자율주행 레벨별, 제공별, 판매 채널별, 지역별Automotive HUD Market by HUD Type (Windshield, Combiner HUD), Technology (2D, AR, 3D), Passenger Car Class, Vehicle Type, Propulsion Type, EV Type, Level of Autonomy, Offering, Sales Channel, and Region - Global Forecast to 2033 |

||||||

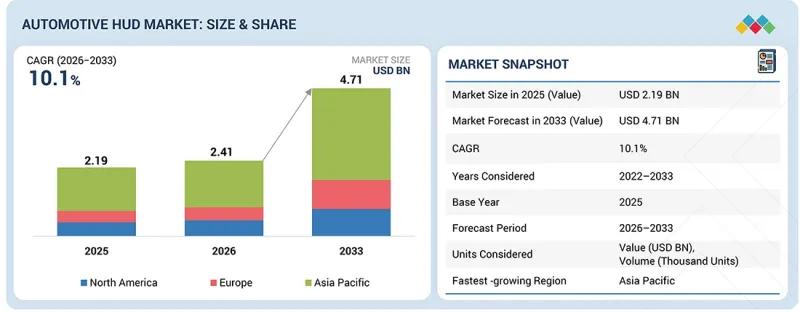

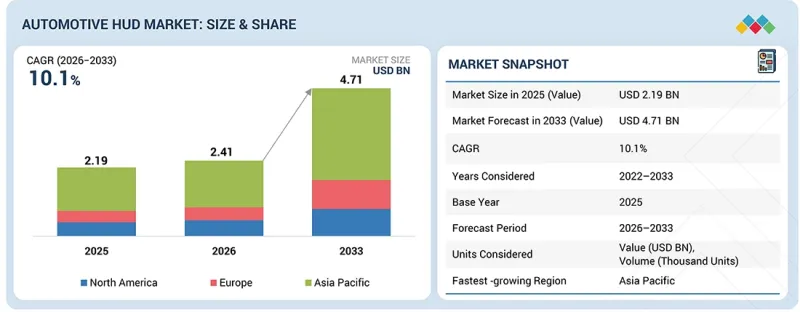

세계의 자동차용 HUD 시장 규모는 2026년 24억 1,000만 달러에서 2033년까지 47억 1,000만 달러에 달할 것으로 예측되며, CAGR로 10.1%의 성장이 예측됩니다.

시장 확대는 운전자의 안전과 주의 산만 감소에 대한 관심 증가, 운전자의 시야에 중요한 운전 정보를 실시간으로 투사하는 것에 대한 수요 증가, 승용차 전반의 첨단 자동차 디스플레이 기술 채택 확대에 기인합니다. 커넥티드 카 생태계에 대한 선호도 증가와 더불어 내비게이션 오버레이, 운전 보조 경고, 차량 진단 기능의 통합이 진행됨에 따라 HUD 시스템에 대한 수요가 더욱 증가하고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 단위 | 수량(1,000대), 금액(10억 달러) |

| 부문 | HUD 유형, 기술, 차종, 자율주행 레벨, 지역 |

| 대상 지역 | 아시아태평양, 북미, 유럽 |

프로젝션 기술, 광학 부품, 디스플레이 해상도의 발전으로 시스템 성능이 향상되는 동시에 비용 최적화가 가능해져 중급 차량에서 HUD 시스템의 가용성이 향상되고 있습니다. 디지털 콕핏 플랫폼 및 커넥티드 인터페이스와의 통합이 진행됨에 따라 사용자 경험과 기능이 향상되고 있으며, Robert Bosch GmbH, Nippon Seiki와 같은 기업은 첨단 제품을 통해 채택을 적극적으로 추진하고 있습니다.

"ICE 차량의 커넥티비티와 디지털화가 시장을 주도합니다. "

현대의 ICE 차량 아키텍처는 점점 더 많은 커넥티비티 기능과 첨단운전자보조시스템(ADAS)을 탑재하고 있으며, 기존 전자 프레임워크에 자동차 HUD 시스템을 원활하게 통합할 수 있게 되었습니다. 이 통합을 통해 HUD는 충돌 경고, 차선이탈 경고, 어댑티브 크루즈 컨트롤(ACC) 데이터와 같은 중요한 주행 정보를 운전자의 시야에 직접 투사하여 상황 인식 능력을 향상시키고 운전자의 주의 산만함을 줄일 수 있습니다. ICE 차량에 첨단 전자 기능과 안전 기능이 탑재되면서 HUD 시스템은 실시간 정보를 안전하고 효율적으로 제공하는 필수적인 인터페이스로 자리 잡고 있습니다. 특히 판매량이 많은 지역에서의 확고한 ICE 자동차 시장의 존재감이 HUD 시스템의 보급을 더욱 촉진하고 있습니다.

"운전의 안전과 편의성 향상에 대한 관심 증가가 시장 주도"

HUD는 투명한 표면(보통 앞 유리)에 정보를 투사하는 장치로, 사용자는 일반적인 시선에서 눈을 돌리지 않고도 데이터를 확인할 수 있습니다. 일반적으로 속도, 내비게이션 안내, 기타 관련 데이터를 운전자의 시야에 표시하여 운전 중 안전과 편의성을 높입니다. 하드웨어는 자동차 2D HUD의 주요 구성 요소이며, 이러한 HUD는 많은 소프트웨어 없이도 사용할 수 있는 기본적인 디스플레이 기능을 제공합니다. 하지만 AR과 ADAS를 지원하는 HUD에서는 소프트웨어의 필요성이 높아집니다. HUD 시장의 85% 이상을 2D HUD가 차지하고 있으며, HUD 비용의 대부분은 하드웨어가 차지하고 있습니다. 자동차 HUD에 사용되는 하드웨어는 앞유리, 프로젝터 유닛, 배터리, 블루투스, 기타 전자 부품으로 구성되어 있습니다. Aumovio(독일), Nippon Seiki(일본), Panasonic Automotive(일본), Foryou Corporation(중국), DENSO Corporation(일본)이 최종사용자에게 자동차 HUD 하드웨어를 제공하고 있습니다. 이들 기업은 Audi, Volkswagen, BMW, Mercedes-Benz 등의 OEM에 HUD 하드웨어를 공급하고 있습니다.

"유럽 자동차용 HUD 시장 성장 촉진, 고급차 제조업체의 강력한 존재감과 엄격한 안전 규제"

유럽 시장은 독일, 프랑스, 영국, 스페인, 이탈리아 등 주요 국가에 걸쳐 있는 탄탄한 자동차 생태계에 의해 주도되고 있습니다. Continental AG, WayRay AG, Envisics와 같은 기존 HUD 기술 제공업체의 존재는 혁신을 가속화하고 시장 성장을 촉진하고 있습니다.

세계의 자동차용 HUD 시장에 대해 조사 분석했으며, 주요 촉진요인과 저해요인, 제품 개발 및 혁신, 경쟁 구도에 대해 조사 분석하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 중요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 규제 상황

제8장 기술의 진보, AI에 의한 영향, 특허, 혁신, 향후 용도

제9장 자동차용 HUD 시장 : 컴바이너 HUD 디스플레이 사이즈별

제10장 자동차용 HUD 시장 : EV 유형별

제11장 자동차용 HUD 시장 : HUD 유형별

제12장 자동차용 HUD 시장 : 자율주행 레벨별

제13장 자동차용 HUD 시장 : 제공별

제14장 자동차용 HUD 시장 : 추진 유형별

제15장 자동차용 HUD 시장 : 판매 채널별

제16장 자동차용 HUD 시장 : 기술별

제17장 자동차용 HUD 시장 : 차량 클래스별

제18장 자동차용 HUD 시장 : 차종별

제19장 자동차용 HUD 시장 : 지역별

제20장 경쟁 구도

제21장 기업 개요

제22장 조사 방법

제23장 부록

KSA 26.06.04The automotive HUD market is projected to grow from USD 2.41 billion in 2026 to USD 4.71 billion by 2033, at a CAGR of 10.1%. The market is expanding due to the increasing focus on driver safety and reduced distraction, rising demand for real-time projection of critical driving information within the driver's line of sight, and growing adoption of advanced in-vehicle display technologies across passenger vehicles. Increasing preference for connected vehicle ecosystems, along with integration of navigation overlays, driver assistance alerts, and vehicle diagnostics, is further supporting the demand for HUD systems.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Volume (Thousand Units), Value (USD Billion) |

| Segments | by HUD Type, Technology, Vehicle Type, Level of Autonomy and Region |

| Regions covered | Asia Pacific, North America, and Europe |

Advancements in projection technologies, optical components, and display resolution are improving system performance while enabling cost optimization, making HUD systems more accessible across mid-segment vehicles. Increasing integration with digital cockpit platforms and connected interfaces is enhancing user experience and functionality, with companies such as Robert Bosch GmbH and Nippon Seiki Co., Ltd. actively driving adoption through advanced product offerings.

"Growing connectivity and digitalization in ICE vehicles to drive market"

Modern ICE vehicle architectures are increasingly equipped with connected features and advanced driver assistance systems (ADAS), enabling seamless integration of automotive HUD systems within existing electronic frameworks. This integration allows HUDs to project critical driving information, such as collision warnings, lane departure alerts, and adaptive cruise control data directly into the driver's line of sight, improving situational awareness and reducing driver distraction. As ICE vehicles continue to incorporate higher levels of electronic and safety functionalities, HUD systems are becoming an essential interface for delivering real-time information safely and efficiently. The presence of well-established ICE vehicle markets, particularly in high-volume regions, is further strengthening the adoption of HUD systems.

"Increasing focus on enhanced driving safety and convenience to drive market"

A HUD is a device that projects information onto a transparent surface, typically a windshield, allowing the user to view data without looking away from their usual viewpoint. It commonly displays information, such as speed, navigation directions, and other relevant data in the driver's line of sight, enhancing safety and convenience while driving. Hardware is a major component of automotive 2D HUDs, with such HUDs providing basic indicators that are generally available without the need for much software. However, the need for software increases in AR or ADAS-enabled HUDs. With 2D HUDs holding over 85% of the HUD market, Hardware is the major contributor to HUD cost. Hardware used in automotive HUDs consists of a windscreen, a projector unit, a battery, Bluetooth, and other electronic components. Aumovio (Germany), Nippon Seiki Co., Ltd. (Japan), Panasonic Automotive (Japan), Foryou Corporation (China), and DENSO Corporation (Japan) offer automotive HUD hardware for end users. They provide HUD hardware to OEMS such as Audi, Volkswagen, BMW, and Mercedes-Benz, among others.

"Strong presence of premium automotive OEMs and stringent safety regulations driving automotive HUD market growth in Europe"

The Europe market is driven by the region's robust automotive ecosystem across key countries, including Germany, France, the UK, Spain, and Italy. The presence of established HUD technology providers such as Continental AG, WayRay AG, and Envisics is accelerating innovation and strengthening market growth. Europe's strong foothold in the premium passenger vehicle segment (C segment and above), where HUD integration is more prominent, further supports adoption due to rising demand for advanced in-vehicle technologies and enhanced driving experiences. Market expansion is further reinforced by stringent European Union safety regulations and the increasing standardization of advanced driver assistance systems (ADAS). HUDs play a critical role in improving driver awareness by projecting essential information within the driver's line of sight, aligning with regulatory objectives to enhance road safety and reduce driver distraction. This regulatory framework, combined with growing consumer preference for safety and convenience features, continues to drive widespread HUD adoption.

The market is also supported by strong demand from leading automotive OEMs, including BMW, Audi, Mercedes-Benz, Porsche, Renault, Peugeot, Nissan, Bentley, Rolls-Royce, and Volkswagen AG. These OEMs are increasingly integrating HUD systems as standard or optional features in premium models, supported by collaborations with key suppliers such as Nippon Seiki, Bosch, Panasonic, and LG Electronics, thereby strengthening the value chain and accelerating market penetration.

Advancements in automotive electronics, display technologies, and human-machine interface (HMI) systems are further enhancing HUD functionality through real-time data visualization and improved system integration. These developments are elevating driver situational awareness, safety, and overall driving experience. As technological innovation continues alongside regulatory support, the European automotive HUD market is expected to maintain steady growth momentum.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: HUD Manufacturers - 50%, OEMs - 40%, Others - 10%

- By Designation: CXOs - 20%, Directors - 30%, Others - 50%

- By Country: Asia Pacific - 40%, North America - 20%, Europe - 30%

On the OEM side, manufacturers are increasingly integrating HUD systems with advanced driver assistance systems (ADAS) and digital cockpit platforms, particularly in premium vehicles, where features such as augmented reality HUDs are being deployed to enhance safety and user experience. Tier 1 suppliers are supporting this integration through continuous innovation in display technologies and scalable system architectures, enabling broader adoption across vehicle segments.

In the aftermarket and broader market context, decreasing costs of display technologies are making HUD systems more accessible beyond premium vehicles, supporting penetration into mid-range segments. Despite the economic slowdown observed in recent years, factors such as technological advancements, economies of scale, and the growing shift toward electric vehicles are expected to sustain demand. The increasing production of semi-autonomous vehicles, coupled with rising consumer preference for enhanced safety and driving experience, continues to act as a catalyst for automotive HUD adoption across North America.

Research Coverage:

The report covers the automotive HUD market by HUD type (Windshield HUD, Combiner HUD), technology type (2D HUD, AR HUD, 3D HUD), passenger car class (Economy, Mid-Segment, Luxury), vehicle type (Passenger Vehicles, Commercial Vehicles), propulsion type (ICE Vehicles, Electric Vehicles), EV type (BEV, PHEV), level of autonomy (Non-Autonomous Cars, Semi-Autonomous Cars, Autonomous Cars), offering (Hardware, Software) sales channel (OE, Aftermarket), combiner HUD display size (< 6 Inch, > 6 Inch), Region (Asia Pacific, Europe, North America), and Region (Asia Pacific, Europe and North America). It covers the competitive landscape and company profiles of the major players in the automotive HUD market ecosystem.

The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report:

- This report will help market leaders/new entrants in this market with information on the closest approximations of revenue numbers for the automotive HUD market ecosystem and its subsegments.

- This report will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies.

- This report will also help stakeholders understand the market's pulse and provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insight into the following pointers:

- Analysis of key drivers (Growing regulatory and consumer focus on driver safety and distraction reduction, growing inclination toward enhanced in-vehicle experience, rising adoption of premium and mid-segment vehicles integrating advanced cockpit technologies), restraints (Space constraints in automotive cockpits, lack of luminance and high power consumption), opportunities (Increasing demand for SDV and semi-autonomous vehicles, growth in EV adoption supporting greater integration of HUDs in modern vehicle systems, expansion of AR-HUD applications for navigation, hazard detection, and real-time data overlay) and challenges (Optical challenges, complex integration process)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the automotive HUD market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the automotive HUD market

- Competitive Assessment: In-depth assessment of market ranking, growth strategies, and service offerings of leading players like Robert Bosch GmbH (Germany), Denso (Japan), Nippon Seiki (Japan), Aumovio (Germany), and Panasonic Automotive (Germany) in the automotive HUD market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN AUTOMOTIVE HUD MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AUTOMOTIVE HUD MARKET

- 3.2 AUTOMOTIVE HUD MARKET, BY HUD TYPE

- 3.3 AUTOMOTIVE HUD MARKET, BY TECHNOLOGY

- 3.4 AUTOMOTIVE HUD MARKET, BY EV TYPE

- 3.5 AUTOMOTIVE HUD MARKET, BY VEHICLE TYPE

- 3.6 AUTOMOTIVE HUD MARKET, BY LEVEL OF AUTONOMY

- 3.7 AUTOMOTIVE HUD MARKET, BY PROPULSION TYPE

- 3.8 AUTOMOTIVE HUD MARKET, BY VEHICLE CLASS

- 3.9 AUTOMOTIVE HUD MARKET, BY OFFERING

- 3.10 AUTOMOTIVE HUD MARKET, BY SALES CHANNEL

- 3.11 AUTOMOTIVE HUD MARKET, BY COMBINER HUD DISPLAY SIZE

- 3.12 AUTOMOTIVE HUD MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing regulatory and consumer focus on driver safety

- 4.2.1.2 HUDs Driving the Evolution of Digital Cockpit Experience

- 4.2.1.3 Rising adoption of premium and mid-segment vehicles integrating advanced cockpit technologies

- 4.2.2 RESTRAINTS

- 4.2.2.1 Space constraints in automotive cockpits

- 4.2.2.2 Lack of luminance and high-power consumption

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing demand for SDV and semi-autonomous vehicles

- 4.2.3.2 Growth in EV adoption supporting greater integration of HUDs in modern vehicle systems

- 4.2.3.3 Expansion of AR-HUD applications for navigation, hazard detection, and real-time data overlay

- 4.2.4 CHALLENGES

- 4.2.4.1 Image Clarity issues due to mis-alignment

- 4.2.4.2 Complex integration process

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY KEY PLAYERS IN AUTOMOTIVE HUD MARKET

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 INTRODUCTION

- 5.1.2 GDP TRENDS AND FORECAST

- 5.1.3 TRENDS IN GLOBAL AUTOMOTIVE HUD MARKET

- 5.1.4 TRENDS IN GLOBAL AUTOMOTIVE & TRANSPORTATION INDUSTRY

- 5.2 ECOSYSTEM ANALYSIS

- 5.2.1 OEMS

- 5.2.2 HUD PROVIDERS

- 5.2.3 HUD COMPONENT PROVIDERS

- 5.2.4 HUD SOFTWARE PROVIDERS

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 BILL OF MATERIALS (BOM) ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF AUTOMOTIVE HUD TECHNOLOGIES, BY KEY PLAYER

- 5.5.2 AVERAGE SELLING PRICE TREND, BY TECHNOLOGY

- 5.5.3 AVERAGE SELLING PRICE TREND, BY REGION, BY TECHNOLOGY

- 5.6 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 INVESTMENT & FUNDING SCENARIO

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRADE ANALYSIS

- 5.9.1 IMPORT SCENARIO (HS CODE 852691)

- 5.9.2 EXPORT SCENARIO (HS CODE 852691)

- 5.10 OEM ANALYSIS BY VEHICLE MODEL

- 5.10.1 BMW

- 5.10.2 MERCEDES-BENZ

- 5.10.3 HYUNDAI, GENESIS & KIA

- 5.10.4 BYD

- 5.10.5 NISSAN

- 5.10.6 VOLKSWAGEN

- 5.10.7 LEXUS & TOYOTA

- 5.10.8 VOLVO & POLESTAR

- 5.10.9 OTHER KEY OEMS

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 IMPROVED DATA MONITORING CAPABILITIES WITH HUD DEMONSTRATOR

- 5.11.2 DRIVERLESS AUTOMATED VALET PARKING SYSTEM AND AR-HUD TECHNOLOGY FOR AUTOMOTIVE SAFETY AND COMFORT

- 5.11.3 BETTER HUD VISUAL QUALITY USING PROMETRIC IMAGING SYSTEMS AND TT-HUD SOFTWARE PLATFORM

- 5.11.4 ADVANCED AUGMENTED REALITY HUD DEVELOPMENT FOR NEXT-GENERATION DRIVER ASSISTANCE

- 5.11.5 HIGH-EFFICIENCY HUD CONTROL SYSTEM USING AI-DRIVEN DATA PROCESSING

- 5.11.6 COMPACT HUD MODULE DESIGN FOR ELECTRIC VEHICLE ARCHITECTURES

- 5.12 IMPACT OF 2026 EU-INDIA TRADE DEAL

- 5.12.1 INTRODUCTION

- 5.12.2 INDIA-EU FREE TRADE AGREEMENT

- 5.12.3 PRICE IMPACT ANALYSIS OF INDIA-EU FTA

- 5.12.4 SUPPLY CHAIN AND LOCALIZATION IMPACT

- 5.12.5 STRATEGIC MARKET OUTLOOK

6 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 KEY STAKEHOLDERS

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.3.1 STRUCTURAL ADOPTION CONSTRAINTS AND OPERATIONAL LIMITATIONS

- 6.3.2 DATA GOVERNANCE AND TRACEABILITY INTEGRATION COMPLEXITY

- 6.3.3 STANDARDIZATION LIMITATIONS AND CROSS-PLANT DEPLOYMENT VARIABILITY

- 6.4 UNMET NEEDS OF VARIOUS END USERS/END-USE INDUSTRIES

- 6.4.1 REAL-TIME INTEGRATION WITH SOFTWARE-DEFINED VEHICLE ARCHITECTURES

- 6.4.2 LOW TOTAL COST OF OWNERSHIP (TCO) AND REDUCED SYSTEM COMPLEXITY

- 6.4.3 DISPLAY CAPABILITY FOR INCREASINGLY COMPLEX COCKPIT ARCHITECTURES

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

8 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 8.1 KEY EMERGING TECHNOLOGIES

- 8.1.1 3D HUD

- 8.1.2 3D AR HUD

- 8.2 COMPLEMENTARY TECHNOLOGIES

- 8.2.1 ADVANCED SENSORS

- 8.2.1.1 Radar

- 8.2.1.2 LiDAR

- 8.2.1.3 Image sensors

- 8.2.2 LIGHT-EMITTING DIODE TECHNOLOGY

- 8.2.3 LASER BEAM SCANNING

- 8.2.4 BIOMETRIC DRIVER MONITORING

- 8.2.1 ADVANCED SENSORS

- 8.3 TECHNOLOGY/PRODUCT ROADMAP

- 8.4 PATENT ANALYSIS

- 8.4.1 INTRODUCTION

- 8.4.1.1 List of patents granted

- 8.4.1 INTRODUCTION

- 8.5 FUTURE APPLICATIONS

- 8.5.1 ON-DEMAND PERFORMANCE AND VISUAL VALIDATION IN AUTOMOTIVE HUD SYSTEMS

- 8.5.2 FLEET AND SPECIALTY VEHICLE HUD UTILIZATION

- 8.5.3 AI-ASSISTED HUD PERFORMANCE AND ADAPTIVE DISPLAY SYSTEMS

- 8.6 IMPACT OF AI ON AUTOMOTIVE HEAD-UP DISPLAY (HUD) MARKET

- 8.6.1 TOP USE CASES AND MARKET POTENTIAL

- 8.6.2 BEST PRACTICES FOLLOWED BY HEAD-UP DISPLAY MANUFACTURERS

- 8.6.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN AUTOMOTIVE HEAD-UP DISPLAY

- 8.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 8.6.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED AUTOMOTIVE HUD SYSTEMS

9 AUTOMOTIVE HUD MARKET, BY COMBINER HUD DISPLAY SIZE

- 9.1 INTRODUCTION

- 9.2 < 6 INCHES

- 9.2.1 COST-TO-PERFORMANCE BALANCE TO DRIVE ADOPTION IN MID-TIER VEHICLES

- 9.3 > 6 INCHES

- 9.3.1 COST-TO-PERFORMANCE BALANCE TO DRIVE ADOPTION IN MID-TIER VEHICLES

- 9.4 KEY INDUSTRY INSIGHTS

10 AUTOMOTIVE HUD MARKET, BY EV TYPE

- 10.1 INTRODUCTION

- 10.2 BEV

- 10.2.1 INCREASING INTEGRATION OF DIGITAL COCKPIT TECHNOLOGIES IN BEVS TO DRIVE MARKET

- 10.3 PHEV

- 10.3.1 TRANSITION TOWARD PREMIUM FEATURE PARITY WITH BEVS TO DRIVE MARKET

- 10.4 KEY INDUSTRY INSIGHTS

11 AUTOMOTIVE HUD MARKET, BY HUD TYPE

- 11.1 INTRODUCTION

- 11.2 WINDSHIELD HUD

- 11.2.1 GROWING DEMAND FOR ENHANCED DRIVER AWARENESS AND REAL-TIME SAFETY VISUALIZATION TO ACCELERATE WINDSHIELD HUD INTEGRATION

- 11.3 COMBINER HUD

- 11.3.1 HIGH UPTAKE OF PLUG-AND-PLAY DISPLAY SOLUTIONS IN AFTERMARKET TO DRIVE DEMAND

- 11.4 KEY INDUSTRY INSIGHTS

12 AUTOMOTIVE HUD MARKET, BY LEVEL OF AUTONOMY

- 12.1 INTRODUCTION

- 12.2 NON-AUTONOMOUS CAR

- 12.2.1 LEVEL 0

- 12.2.1.1 Rising production of cars in Asia Pacific to drive market

- 12.2.1 LEVEL 0

- 12.3 SEMI-AUTONOMOUS CAR

- 12.3.1 L1

- 12.3.1.1 Increasing adoption of basic autonomy at moderate cost to drive adoption

- 12.3.2 L2

- 12.3.2.1 Growing integration of automatic emergency braking, cross-traffic alert, and blind spot detection to drive market

- 12.3.3 L2+

- 12.3.3.1 Growing Demand for Advanced Driver Assistance and Intelligent Cockpit Experiences

- 12.3.4 L3

- 12.3.4.1 Growing shift to self-driving vehicles and driver support systems to drive market

- 12.3.1 L1

- 12.4 AUTONOMOUS CAR

- 12.4.1 L4

- 12.4.1.1 Growing inclination toward autonomous mobility solutions to drive market

- 12.4.2 L5

- 12.4.2.1 Rising demand for reduced manual control to drive market

- 12.4.1 L4

- 12.5 KEY INDUSTRY INSIGHTS

13 AUTOMOTIVE HUD MARKET, BY OFFERING

- 13.1 INTRODUCTION

- 13.2 HARDWARE

- 13.2.1 INCREASING FOCUS ON ENHANCED DRIVING SAFETY AND CONVENIENCE TO DRIVE MARKET

- 13.3 SOFTWARE

- 13.3.1 RISING ADOPTION OF ADAS-EQUIPPED VEHICLES TO DRIVE MARKET

- 13.4 KEY INDUSTRY INSIGHTS

14 AUTOMOTIVE HUD MARKET, BY PROPULSION TYPE

- 14.1 INTRODUCTION

- 14.2 ICE VEHICLE

- 14.2.1 RISING ADOPTION OF ADAS IN ICE VEHICLES TO DRIVE MARKET

- 14.3 ELECTRIC VEHICLE

- 14.3.1 GROWING FOCUS ON STRICT VEHICLE EMISSIONS TO DRIVE MARKET

- 14.4 KEY INDUSTRY INSIGHTS

15 AUTOMOTIVE HUD MARKET, BY SALES CHANNEL

- 15.1 INTRODUCTION

- 15.2 ORIGINAL EQUIPMENT (OE)

- 15.2.1 INCREASING INTEGRATION OF HUD WITH DIGITAL COCKPIT AND ADAS SYSTEMS TO DRIVE GROWTH

- 15.3 AFTERMARKET

- 15.3.1 DEMAND FOR COST-EFFECTIVE UPGRADE SOLUTIONS TO SUPPORT STEADY ADOPTION

- 15.4 KEY INDUSTRY INSIGHTS

16 AUTOMOTIVE HUD MARKET, BY TECHNOLOGY

- 16.1 INTRODUCTION

- 16.2 2D HUD

- 16.2.1 GROWING DEMAND FOR LUXURY VEHICLES TO DRIVE DEMAND

- 16.3 AR HUD

- 16.3.1 INTEGRATION OF SMART CONNECTED AND ADAS FEATURES TO HUD OUTPUT TO DRIVE DEMAND

- 16.4 3D HUD

- 16.4.1 DEMAND FOR FEATURING MULTIPLE OUTPUTS IN WINDSHIELD TO BOOST GROWTH

- 16.5 KEY INDUSTRY INSIGHTS

17 AUTOMOTIVE HUD MARKET, BY VEHICLE CLASS

- 17.1 INTRODUCTION

- 17.2 ECONOMY CAR

- 17.2.1 INCREASING ADOPTION OF HUDS IN SELECT ECONOMY VEHICLES TO DRIVE DEMAND

- 17.3 MID-SEGMENT CAR

- 17.3.1 GROWING ADOPTION OF HUDS IN TOP TRIMS OF MID-SEGMENT VEHICLES TO BOOST DEMAND

- 17.4 LUXURY CAR

- 17.4.1 NEED FOR ENHANCED SAFETY FEATURES TO DRIVE DEMAND

- 17.5 KEY INDUSTRY INSIGHTS

18 AUTOMOTIVE HUD MARKET, BY VEHICLE TYPE

- 18.1 INTRODUCTION

- 18.2 PASSENGER CAR

- 18.2.1 OEM STRATEGY TO PROVIDE HUDS IN SELECT TRIMS OF MID-SEGMENT PASSENGER CARS TO DRIVE DEMAND

- 18.3 COMMERCIAL VEHICLE

- 18.3.1 EXPANDING E-COMMERCE AND LAST-MILE DELIVERY SERVICES TO DRIVE MARKET

- 18.4 KEY INDUSTRY INSIGHTS

19 AUTOMOTIVE HUD MARKET, BY REGION

- 19.1 INTRODUCTION

- 19.2 NORTH AMERICA

- 19.2.1 CANADA

- 19.2.1.1 Focus on high trim vehicle assembly to support inclusion of HUD features

- 19.2.2 MEXICO

- 19.2.2.1 Rising vehicle production, export strength, and adoption of advanced features to drive market

- 19.2.3 US

- 19.2.3.1 Increased production of SUVs to drive market

- 19.2.1 CANADA

- 19.3 ASIA PACIFIC

- 19.3.1 CHINA

- 19.3.1.1 Demand for luxury vehicles to drive demand

- 19.3.2 INDIA

- 19.3.2.1 Growing demand for vehicles and improving consumer lifestyles to drive market growth

- 19.3.3 JAPAN

- 19.3.3.1 Growing demand for connected vehicles and ease of driving to drive growth

- 19.3.4 SOUTH KOREA

- 19.3.4.1 Strong AR HUD adoption push in mid-segment vehicles to drive market in South Korea

- 19.3.1 CHINA

- 19.4 EUROPE

- 19.4.1 FRANCE

- 19.4.1.1 HUDs' adoption in top trims of mid-segment vehicles to drive market

- 19.4.2 GERMANY

- 19.4.2.1 Premium OEMs accelerating shift toward AR HUD to drive market

- 19.4.3 SPAIN

- 19.4.3.1 Export-driven production integrating HUD into vehicles to drive market

- 19.4.4 UK

- 19.4.4.1 Export-oriented premium vehicle production, embedding HUD to drive market

- 19.4.5 ITALY

- 19.4.5.1 Growing production of luxury vehicles to drive market

- 19.4.1 FRANCE

- 19.5 REST OF THE WORLD

- 19.5.1 SAUDI ARABIA

- 19.5.2 SOUTH AFRICA

- 19.5.3 UAE

20 COMPETITIVE LANDSCAPE

- 20.1 OVERVIEW

- 20.2 KEY PLAYER STRATEGIES, 2023-2026

- 20.3 MARKET SHARE ANALYSIS, 2025

- 20.4 REVENUE ANALYSIS OF TOP PLAYERS

- 20.5 COMPANY VALUATION AND FINANCIAL METRICS

- 20.5.1 COMPANY VALUATION

- 20.5.2 FINANCIAL METRICS

- 20.6 BRAND/PRODUCT COMPARISON

- 20.7 COMPANY EVALUATION MATRIX: KEY PLAYERS

- 20.7.1 STARS

- 20.7.2 EMERGING LEADERS

- 20.7.3 PERVASIVE PLAYERS

- 20.7.4 PARTICIPANTS

- 20.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES

- 20.8.1 PROGRESSIVE COMPANIES

- 20.8.2 RESPONSIVE COMPANIES

- 20.8.3 DYNAMIC COMPANIES

- 20.8.4 STARTING BLOCKS

- 20.8.5 COMPETITIVE BENCHMARKING

- 20.9 COMPETITIVE SCENARIO

- 20.9.1 PRODUCT LAUNCHES

- 20.9.2 DEALS

- 20.9.3 EXPANSIONS

- 20.9.4 OTHER DEVELOPMENTS

21 COMPANY PROFILES

- 21.1 KEY PLAYERS

- 21.1.1 NIPPON SEIKI CO., LTD.

- 21.1.1.1 Business overview

- 21.1.1.2 Products offered

- 21.1.1.3 Recent developments

- 21.1.1.4 MnM view

- 21.1.1.4.1 Key strengths

- 21.1.1.4.2 Strategic choices

- 21.1.1.4.3 Weaknesses and competitive threats

- 21.1.2 AUMOVIO SE

- 21.1.2.1 Business overview

- 21.1.2.2 Products offered

- 21.1.2.3 Recent developments

- 21.1.2.4 MnM view

- 21.1.2.4.1 Key strengths

- 21.1.2.4.2 Strategic choices

- 21.1.2.4.3 Weaknesses and competitive threats

- 21.1.3 DENSO CORPORATION

- 21.1.3.1 Business overview

- 21.1.3.2 Products offered

- 21.1.3.3 Recent developments

- 21.1.3.4 MnM view

- 21.1.3.4.1 Key strengths

- 21.1.3.4.2 Strategic choices

- 21.1.3.4.3 Weaknesses and competitive threats

- 21.1.4 PANASONIC AUTOMOTIVE SYSTEMS CO., LTD.

- 21.1.4.1 Business overview

- 21.1.4.2 Products offered

- 21.1.4.3 Recent developments

- 21.1.4.4 MnM view

- 21.1.4.4.1 Key strengths

- 21.1.4.4.2 Strategic choices

- 21.1.4.4.3 Weaknesses and competitive threats

- 21.1.5 ROBERT BOSCH GMBH

- 21.1.5.1 Business overview

- 21.1.5.2 Products offered

- 21.1.5.3 Recent developments

- 21.1.5.4 MnM view

- 21.1.5.4.1 Key strengths

- 21.1.5.4.2 Strategic choices

- 21.1.5.4.3 Weaknesses and competitive threats

- 21.1.6 JIANGSU ZEJING AUTOMOTIVE ELECTRONICS CO., LTD.

- 21.1.6.1 Business overview

- 21.1.6.2 Products offered

- 21.1.6.3 MnM view

- 21.1.6.3.1 Key strengths

- 21.1.6.3.2 Strategic choices

- 21.1.6.3.3 Weaknesses and competitive threats

- 21.1.7 FORYOU CORPORATION

- 21.1.7.1 Business overview

- 21.1.7.2 Products Offered

- 21.1.7.3 Recent developments

- 21.1.8 YAZAKI CORPORATION

- 21.1.8.1 Business overview

- 21.1.8.2 Products offered

- 21.1.9 VISTEON CORPORATION

- 21.1.9.1 Business overview

- 21.1.9.2 Products offered

- 21.1.9.3 Recent developments

- 21.1.10 HUAWEI TECHNOLOGIES CO., LTD.

- 21.1.10.1 Business overview

- 21.1.10.2 Products offered

- 21.1.10.3 Recent developments

- 21.1.11 HYUNDAI MOBIS

- 21.1.11.1 Business overview

- 21.1.11.2 Products offered

- 21.1.11.3 Recent developments

- 21.1.12 LG ELECTRONICS

- 21.1.12.1 Business overview

- 21.1.12.2 Products offered

- 21.1.12.3 Recent developments

- 21.1.1 NIPPON SEIKI CO., LTD.

- 21.2 OTHER PLAYERS

- 21.2.1 HARMAN INTERNATIONAL

- 21.2.2 FUTURUS LLC

- 21.2.3 HUDWAY, LLC

- 21.2.4 HUDLY

- 21.2.5 CY VISION

- 21.2.6 ENVISICS

- 21.2.7 ZHEJIANG CRYSTAL-OPTECH CO., LTD.

- 21.2.8 YILI ELECTRONICS CO., LTD.

- 21.2.9 MAXWELL ENGINEERING SOLUTIONS LTD.

- 21.2.10 MAXWELL ENGINEERING SOLUTIONS LTD.: COMPANY OVERVIEW

- 21.2.11 NEUSOFT CORPORATION

- 21.2.12 LUMINIT, INC

- 21.2.13 E-LEAD ELECTRONIC CO., LTD.

- 21.2.14 SHENZHEN SUNWAY INDUSTRY CO., LTD.

22 RESEARCH METHODOLOGY

- 22.1 RESEARCH DATA

- 22.1.1 SECONDARY DATA

- 22.1.1.1 Secondary sources

- 22.1.1.2 Key data from secondary sources

- 22.1.2 PRIMARY DATA

- 22.1.2.1 Primary interviews: Demand and supply sides

- 22.1.2.2 Key industry insights

- 22.1.2.3 Breakdown of primary interviews

- 22.1.2.4 List of primary participants

- 22.1.1 SECONDARY DATA

- 22.2 MARKET SIZE ESTIMATION

- 22.2.1 BOTTOM-UP APPROACH

- 22.2.2 TOP-DOWN APPROACH

- 22.3 DATA TRIANGULATION

- 22.4 FACTOR ANALYSIS

- 22.5 RESEARCH LIMITATIONS

- 22.6 RISK ASSESSMENT

23 APPENDIX

- 23.1 KEY INSIGHTS FROM INDUSTRY EXPERTS

- 23.2 DISCUSSION GUIDE

- 23.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.4 CUSTOMIZATION OPTIONS

- 23.5 RELATED REPORTS

- 23.6 AUTHOR DETAILS