|

시장보고서

상품코드

2041524

보안 정보 및 이벤트 관리(SIEM) 시장 : 유형별(고도 SIEM, 차세대 SIEM), 용도별(위협 탐지, 조사, 대응(TDIR), 보안 모니터링 및 가시화, 컴플라이언스, 보안 분석) - 세계 예측(-2031년)Security Information and Event Management (SIEM) Market by Type (Advanced SIEM, Next-Gen SIEM), Application (Threat Detection, Investigation, & Response (TDIR), Security Monitoring & Visibility, Compliance, Security Analytics) - Global Forecast to 2031 |

||||||

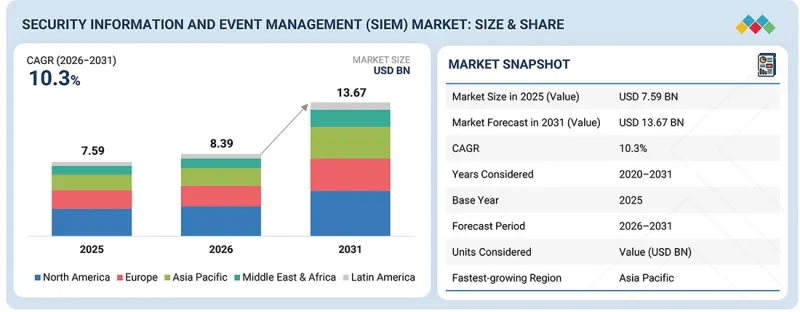

세계의 보안 정보 및 이벤트 관리(SIEM) 시장 규모는 2026년 83억 9,000만 달러에서 2031년에는 136억 7,000만 달러로 성장하여 예측 기간 동안 CAGR은 10.3%에 달할 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2035년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2035년 |

| 단위 | 금액(달러) |

| 부문 | 유형·제공·용도·도입 모드·기업 규모·산업·지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

사이버 위협의 증가와 고도화, 그리고 AI 기반 및 에이전트 기반의 차세대 SIEM의 등장으로 보다 신속한 탐지 및 대응이 가능해지면서 시장 성장이 가속화되고 있습니다. 기업들은 이벤트를 자율적으로 상관관계 분석하여 경보 피로를 줄이고 위협 가시성을 향상시킬 수 있는 지능형 SIEM 플랫폼을 도입하고 있습니다. 이러한 변화는 운영 효율성을 높이고 복잡한 공격 패턴에 대응할 수 있게 해주기 때문에 기업 전체가 고급 SIEM 기능에 대한 투자를 확대하고 있습니다.

"산업별로는 헬스케어 및 생명과학 분야가 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 전망"

의료 분야는 전자의무기록, 커넥티드 디바이스, 클라우드 기반 임상 시스템 등 디지털 헬스 생태계의 급속한 확장으로 공격 대상 영역이 크게 확대되면서 SIEM 시장에서 가장 빠르게 성장하고 있습니다. 환자 데이터의 높은 기밀성과 가치로 인해 의료 기관은 사이버 공격의 주요 표적이 되고 있으며, 이에 따라 고급 모니터링 및 위협 탐지 솔루션의 필요성이 더욱 커지고 있습니다. 또한, 엄격한 규제 요건과 지속적인 컴플라이언스의 필요성은 실시간 가시성과 감사 대응력을 보장할 수 있는 SIEM 플랫폼의 도입을 촉진하고 있습니다. 또한, 매니지드 SIEM 및 SOC 서비스에 대한 의존도 확대도 사내 사이버 보안 인력 부족을 보완하는 형태로 도입을 촉진하고 있습니다.

"조직 규모별로는 중소기업 부문이 예측 기간 동안 가장 높은 CAGR로 성장할 것으로 전망"

중소기업 부문은 사이버 위협에 대한 노출이 증가하고 사내 사이버 보안 역량이 제한적이기 때문에 SIEM 시장에서 괄목할 만한 성장세를 보이고 있습니다. 보안 체계가 취약하고 예산의 제약으로 인해 이들 조직은 공격에 더 취약하며, 사이버 공격의 상당 부분이 중소기업을 표적으로 삼고 있습니다. 이러한 위험은 클라우드 애플리케이션과 디지털 툴의 급속한 도입으로 공격 대상 영역이 확대되면서 더욱 증폭되고 있습니다. 이러한 문제를 해결하기 위해 중소기업들은 확장성, 도입 간소화, 비용 효율성을 제공하는 클라우드 기반 관리형 SIEM 솔루션을 점점 더 많이 채택하고 있습니다. 이러한 솔루션은 고도의 사내 전문 지식 없이도 중앙 집중식 모니터링, 기본적인 위협 탐지 및 컴플라이언스 대응이 가능하기 때문에 이 분야 전반에 걸쳐 SIEM 도입이 가속화되고 있습니다.

"용도별로는 위협 탐지, 조사 및 대응(TDIR) 부문이 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예상됩니다."

TDIR 부문은 엔드-투-엔드 보안 운영을 실현하는 데 있어 매우 중요한 역할을 하기 때문에 SIEM 시장에서 가장 큰 시장 점유율을 차지하고 있습니다. 조직은 통합된 프레임워크 내에서 지속적인 모니터링, 상세한 위협 분석, 조정된 대응 조치를 제공하는 TDIR 기능을 우선시하고 있습니다. 이러한 통합적 접근 방식은 복잡한 IT 환경 전반에 대한 가시성을 향상시켜 위협이 심각한 피해를 입히기 전에 위협을 보다 신속하게 식별하고 완화할 수 있도록 돕습니다. 또한, 자동화와 고도화된 분석에 힘입어 사후 대응형에서 사전 예방형으로 보안 운영이 전환되고 있는 것도 수요를 촉진하고 있습니다. 기업들이 위협 잠복 시간 단축, 사고 대응 효율성 향상, 비즈니스 영향 최소화 등에 집중하고 있는 가운데, TDIR은 SIEM 도입을 주도하고 있습니다.

세계의 보안 정보 및 이벤트 관리(SIEM) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술·특허 동향, 법·규제 환경, 사례 분석, 시장 규모 추정과 예측, 각종 부문별·지역별·주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다. 프로파일 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 소비자 상황과 구매 행동

제9장 보안 정보 및 이벤트 관리(SIEM) 시장 : 유형별

제10장 보안 정보 및 이벤트 관리(SIEM) 시장 : 제공별

제11장 보안 정보 및 이벤트 관리(SIEM) 시장 : 용도별

제12장 보안 정보 및 이벤트 관리(SIEM) 시장 : 도입 모드별

제13장 보안 정보 및 이벤트 관리(SIEM) 시장 : 조직 규모별

제14장 보안 정보 및 이벤트 관리(SIEM) 시장 : 산업별

제15장 보안 정보 및 이벤트 관리(SIEM) 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSM 26.06.04The global security information and event management (SIEM) market is projected to grow from USD 8.39 billion in 2026 to USD 13.67 billion by 2031, at a CAGR of 10.3% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By Output, Ship Type, System and Region |

| Regions covered | North America, Europe, APAC, RoW |

The growing volume and sophistication of cyber threats, combined with the emergence of AI-driven and agentic next-gen SIEM, is accelerating market growth by enabling faster detection and response. Organizations are increasingly adopting intelligent SIEM platforms that can autonomously correlate events, reduce alert fatigue, and improve threat visibility. This shift enhances operational efficiency and addresses complex attack patterns, thereby driving greater investments in advanced SIEM capabilities across enterprises.

"By vertical, the healthcare & life sciences segment is expected to grow at the highest CAGR during the forecast period."

The healthcare segment is witnessing the fastest growth in the SIEM market due to the rapid expansion of digital health ecosystems, including electronic medical records, connected devices, and cloud-based clinical systems, which significantly increase the attack surface. The high sensitivity and value of patient data make healthcare institutions prime targets for cyberattacks, further accelerating the need for advanced monitoring and threat detection solutions. Additionally, stringent regulatory requirements and the need for continuous compliance are driving the adoption of SIEM platforms for real-time visibility and audit readiness. The increasing reliance on managed SIEM and SOC services also supports adoption by addressing limited in-house cybersecurity expertise.

"By organization size, the SMEs segment is expected to grow at the highest CAGR during the forecast period."

The small and medium-sized enterprise segment is growing at a significant rate in the SIEM market due to increasing exposure to cyber threats and limited in-house cybersecurity capabilities. A substantial share of cyberattacks targets SMEs, as weaker security postures and budget constraints make these organizations more vulnerable. This risk is further amplified by the rapid adoption of cloud applications and digital tools, expanding the attack surface. To address these challenges, SMEs are increasingly adopting cloud-based and managed SIEM solutions that offer scalability, simplified deployment, and cost efficiency. These solutions enable centralized monitoring, basic threat detection, and compliance support without requiring extensive internal expertise, thereby accelerating SIEM adoption across this segment.

"By application, the threat detection, investigation, & response (TDIR) segment is expected to account for the largest market share during the forecast period."

The threat detection, investigation, and response (TDIR) segment holds the largest market share in the SIEM market due to its critical role in enabling end-to-end security operations. Organizations prioritize TDIR capabilities as they provide continuous monitoring, in-depth threat analysis, and coordinated response actions within a unified framework. This integrated approach enhances visibility across complex IT environments and enables faster identification and mitigation of threats before they cause significant damage. Additionally, the shift from reactive to proactive security operations, supported by automation and advanced analytics, is strengthening demand. As enterprises focus on reducing dwell time, improving incident response efficiency, and minimizing business disruption, TDIR continues to dominate SIEM adoption.

Breakdown of primaries

The study contains insights from various industry experts, including component suppliers, Tier 1 companies, and OEMs. The breakup of the primaries is as follows:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-Level Executives - 40% and Managerial & Other Levels - 60%

- By Region: North America - 35%, Europe - 20%, Asia Pacific - 20%, Middle East & Africa - 20%, and Latin America - 5%

Major vendors in the global SIEM market include Splunk (Cisco) (US), Microsoft (US), IBM (US), CrowdStrike (US), Palo Alto Networks (US), Google (US), Fortinet (US), Elastic (US), Rapid7 (US), Seceon (US), OpenText (Canada), ManageEngine (US), Huawei (China), Datadog (US), QAX (China), NetWitness (US), SolarWinds (US), Exabeam (US), Sumo Logic (US), Securonix (US), Gurucul (US), Graylog (US), Devo (US), Logsign (Netherlands), Hunters (Israel), UTMStack (US), Panther (US), and Huntsman Security (Australia).

The study includes an in-depth competitive analysis of the key players in the SIEM market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the SIEM market and forecasts its size by type (basic SIEM, advanced SIEM, next-gen SIEM), offering (platform/solutions, services), application (threat detection, investigation, & response (TDIR), security monitoring & visibility, compliance management & reporting, security analytics & risk prioritization, data management), deployment mode (on-premises, cloud, hybrid), organization size (large enterprises and SMEs), vertical (BFSI, IT & ITeS, government, aerospace & defense, healthcare & life sciences, retail & eCommerce, manufacturing, energy & utilities, telecommunications, media & entertainment, and others).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall SIEM market and its subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (growing volume and sophistication of cyber threats, increasing shift toward cloud-native architectures, stringent regulatory frameworks), restraints (high data ingestion and storage costs, deployment and integration complexity across diverse environments, shortage of skilled SOC analysts and detection engineers), opportunities (emergence of AI-driven and agentic next-gen SIEM, converged and open next-gen SIEM platforms, monetization of detection engineering and threat hunting, expansion of managed SIEM and SOC-as-a-Service models), and challenges (managing alert fatigue and false positives at scale, competitive pressure from XDR and next-generation SOC platforms)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the SIEM market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the SIEM market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the SIEM market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the SIEM market, including Splunk (Cisco) (US), Microsoft (US), IBM (US), CrowdStrike (US), and Palo Alto Networks (US).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE AND SEGMENTATION

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 3.2 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY TYPE

- 3.3 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY OFFERING

- 3.4 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY APPLICATION

- 3.5 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY VERTICAL

- 3.6 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing volume and sophistication of cyber threats

- 4.2.1.2 Increasing shift toward cloud-native architectures

- 4.2.1.3 Stringent regulatory frameworks

- 4.2.2 RESTRAINTS

- 4.2.2.1 High data ingestion and storage costs

- 4.2.2.2 Deployment and integration complexity across diverse environments

- 4.2.2.3 Shortage of skilled SOC analysts and detection engineers

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of AI-driven and agentic next-gen SIEM

- 4.2.3.2 Converged and open next-gen SIEM platforms

- 4.2.3.3 Monetization of detection engineering and threat hunting

- 4.2.3.4 Expansion of managed SIEM and SOC-as-a-Service models

- 4.2.4 CHALLENGES

- 4.2.4.1 Managing alert fatigue and false positives at scale

- 4.2.4.2 Competitive pressure from XDR and next-generation SOC platforms

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.5.1 CROSS-TIER STRATEGIC PATTERNS

- 4.5.2 STRATEGIC TRENDS

- 4.5.2.1 AI-driven threat detection and predictive analytics

- 4.5.2.2 Convergence of SIEM with XDR and unified security platforms

- 4.5.2.3 Expansion of cloud-native and data-centric SIEM architectures

- 4.5.2.4 Growth of automation and detection engineering capabilities

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL ICT INDUSTRY

- 5.2.4 TRENDS IN GLOBAL CYBERSECURITY INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF SIEM SERVICES, BY ORGANIZATION SIZE, 2025

- 5.5.2 INDICATIVE PRICING ANALYSIS, BY VENDOR, 2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 8523)

- 5.6.2 EXPORT SCENARIO (HS CODE 8523)

- 5.7 KEY CONFERENCES AND EVENTS IN 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 UNIVERSITY OF SAN FRANCISCO ENHANCES SECURITY VISIBILITY AND INCIDENT RESPONSE WITH SPLUNK CLOUD SIEM

- 5.10.2 IBM ENABLES UNITED FAMILY HEALTHCARE TO STRENGTHEN DATA PROTECTION AND SECURITY MONITORING

- 5.10.3 LUMEN TECHNOLOGIES IMPROVES THREAT DETECTION AND OPERATIONAL EFFICIENCY USING CROWDSTRIKE PLATFORM

- 5.10.4 PALO ALTO NETWORKS DEPLOYS AI-DRIVEN SECURITY OPERATIONS FOR LOUISIANA

- 5.10.5 RAKBANK ACCELERATES THREAT DETECTION AND INVESTIGATION WITH SECURONIX UNIFIED SIEM

- 5.11 IMPACT OF 2025 US TARIFF - SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 TECHNOLOGY ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 AI-driven behavioral analytics & risk-based detection

- 6.1.1.2 Generative AI for SOC operations

- 6.1.1.3 Cloud-native, data lake-driven SIEM architecture

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 SOAR (security orchestration, automation, and response)

- 6.1.2.2 Threat intelligence & XDR-driven context enrichment

- 6.1.2.3 Security data pipelines & observability integration

- 6.1.2.4 Identity & access management (IAM) integration

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Unified security platforms (XDR + CNAPP convergence)

- 6.1.3.2 Security analytics platforms (data lake & observability convergence)

- 6.1.3.3 Digital forensics & incident response (DFIR) platforms

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY ROADMAP

- 6.2.1 SHORT-TERM (2026-2027) | AI-ENABLED DETECTION & CLOUD-NATIVE FOUNDATION

- 6.2.2 MID-TERM (2027-2030) | UNIFIED ANALYTICS, AUTOMATION, & PLATFORM CONVERGENCE

- 6.2.3 LONG-TERM (2030-2035+) | AUTONOMOUS, PREDICTIVE, & ADAPTIVE SIEM ECOSYSTEM

- 6.3 PATENT ANALYSIS

- 6.4 FUTURE APPLICATIONS

- 6.4.1 AI-DRIVEN AUTONOMOUS THREAT DETECTION & RESPONSE PLATFORMS

- 6.4.2 PREDICTIVE SECURITY ANALYTICS & PROACTIVE THREAT HUNTING

- 6.4.3 UNIFIED CROSS-DOMAIN SECURITY VISIBILITY (XDR-INTEGRATED SIEM)

- 6.4.4 REAL-TIME RISK-BASED SECURITY OPERATIONS & DECISIONING

- 6.4.5 CLOUD-NATIVE, DATA LAKE-DRIVEN SECURITY ANALYTICS AT SCALE

- 6.5 IMPACT OF AI/GEN AI ON SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES IN SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 6.5.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 6.5.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.6.1 GURUCUL: AI-DRIVEN RISK ANALYTICS FOR GLOBAL INSURANCE AND RISK PROVIDER

- 6.6.2 SPLUNK: REAL-TIME SECURITY MONITORING FOR GLOBAL BUILDING MATERIALS ENTERPRISE

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CONSUMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

9 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.1.1 TYPE: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 9.2 BASIC SIEM

- 9.2.1 PROVIDING FOUNDATIONAL VISIBILITY ACROSS SECURITY OPERATIONS AND AUDIT FUNCTIONS

- 9.2.1.1 Log Management

- 9.2.1.2 Rule-Based Correlation

- 9.2.1 PROVIDING FOUNDATIONAL VISIBILITY ACROSS SECURITY OPERATIONS AND AUDIT FUNCTIONS

- 9.3 ADVANCED SIEM

- 9.3.1 ENABLING CONTEXT-AWARE DETECTION THROUGH BEHAVIORAL AND THREAT INTELLIGENCE CAPABILITIES

- 9.3.1.1 UEBA

- 9.3.1.2 Threat Intelligence Integration

- 9.3.1 ENABLING CONTEXT-AWARE DETECTION THROUGH BEHAVIORAL AND THREAT INTELLIGENCE CAPABILITIES

- 9.4 NEXT-GEN SIEM

- 9.4.1 ADVANCING SECURITY OPERATIONS THROUGH AI-DRIVEN ANALYTICS AND AUTOMATION

10 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.1.1 OFFERING: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 10.2 PLATFORMS/SOLUTIONS

- 10.2.1 COMPOSABLE AND CLOUD-NATIVE ARCHITECTURES RESHAPING SIEM PLATFORMS

- 10.3 SERVICES

- 10.3.1 PROFESSIONAL SERVICES

- 10.3.1.1 Advanced consulting and deployment services to strengthen SIEM implementation success

- 10.3.1.2 Design, consulting, & implementation

- 10.3.1.3 Training & education

- 10.3.1.4 Support & maintenance

- 10.3.2 MANAGED SERVICES

- 10.3.2.1 Shift toward scalable, outcome-based security models to fuel SIEM adoption

- 10.3.1 PROFESSIONAL SERVICES

11 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.1.1 APPLICATION: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 11.2 THREAT DETECTION, INVESTIGATION, & RESPONSE (TDIR)

- 11.2.1 RISING DEMAND FOR PROACTIVE THREAT DETECTION AND AUTOMATED RESPONSE TO DRIVE ADOPTION

- 11.3 SECURITY MONITORING & VISIBILITY

- 11.3.1 EXPANDING NEED FOR REAL-TIME VISIBILITY AND CENTRALIZED MONITORING TO DRIVE ADOPTION

- 11.4 COMPLIANCE MANAGEMENT & REPORTING

- 11.4.1 INCREASING REGULATORY PRESSURE AND AUDIT COMPLEXITY TO DRIVE MARKET

- 11.5 SECURITY ANALYTICS & RISK PRIORITIZATION

- 11.5.1 INCREASING FOCUS ON CONTEXTUAL RISK SCORING AND ADVANCED ANALYTICS TO DRIVE ADOPTION

- 11.6 DATA MANAGEMENT

- 11.6.1 ENHANCING LOG AGGREGATION, STORAGE OPTIMIZATION, AND COMPLIANCE READINESS

12 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY DEPLOYMENT MODE

- 12.1 INTRODUCTION

- 12.1.1 DEPLOYMENT MODE: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 12.2 CLOUD

- 12.2.1 INCREASING ADOPTION OF SCALABLE CLOUD-BASED SIEM PLATFORMS TO DRIVE MARKET

- 12.3 ON-PREMISES

- 12.3.1 INCREASING NEED FOR DATA SOVEREIGNTY AND INFRASTRUCTURE CONTROL TO DRIVE MARKET

- 12.4 HYBRID

- 12.4.1 INCREASING DEMAND FOR FLEXIBLE AND INTEGRATED SECURITY ARCHITECTURES TO DRIVE MARKET

13 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY ORGANIZATION SIZE

- 13.1 INTRODUCTION

- 13.1.1 ORGANIZATION SIZE: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 13.2 LARGE ENTERPRISES

- 13.2.1 INCREASING SECURITY DATA SCALE AND ADVANCED THREAT EXPOSURE IN LARGE ENTERPRISES TO DRIVE MARKET

- 13.3 SMALL & MEDIUM-SIZED ENTERPRISES

- 13.3.1 INCREASING ADOPTION OF SCALABLE AND COST-EFFECTIVE SIEM SOLUTIONS AMONG SMES TO DRIVE MARKET

14 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY VERTICAL

- 14.1 INTRODUCTION

- 14.1.1 VERTICAL: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 14.2 BANKING, FINANCIAL SERVICES, AND INSURANCE (BFSI)

- 14.2.1 RISING DIGITAL TRANSACTION VOLUMES AND SURGE IN FRAUD LOSSES TO DRIVE SIEM ADOPTION

- 14.3 IT & ITES

- 14.3.1 RISING VOLUME OF SECURITY TELEMETRY AND NEED FOR REAL-TIME MONITORING TO DRIVE SIEM ADOPTION

- 14.4 GOVERNMENT

- 14.4.1 ESCALATING NATION-STATE THREATS AND MULTI-AGENCY VISIBILITY REQUIREMENTS TO ACCELERATE SIEM ADOPTION

- 14.5 AEROSPACE & DEFENSE

- 14.5.1 HEIGHTENED PROTECTION OF CRITICAL DEFENSE SYSTEMS AND MISSION DATA TO DRIVE SIEM ADOPTION

- 14.6 HEALTHCARE & LIFE SCIENCES

- 14.6.1 PROTECTING PATIENT DATA AND ENSURING REGULATORY COMPLIANCE TO ACCELERATE SIEM ADOPTION

- 14.7 RETAIL & E-COMMERCE

- 14.7.1 SURGE IN DIGITAL COMMERCE AND PAYMENT FRAUD RISKS TO ACCELERATE SIEM ADOPTION

- 14.8 MANUFACTURING

- 14.8.1 STRENGTHENING OPERATIONAL RESILIENCE AND SECURING CONNECTED PRODUCTION ENVIRONMENTS TO DRIVE SIEM ADOPTION

- 14.9 ENERGY & UTILITIES

- 14.9.1 GRID MODERNIZATION AND CRITICAL INFRASTRUCTURE PROTECTION TO FUEL SIEM ADOPTION

- 14.10 TELECOMMUNICATIONS

- 14.10.1 RISING COMPLEXITY OF MOBILE NETWORKS AND 5G INFRASTRUCTURE TO DRIVE SIEM ADOPTION

- 14.11 TRANSPORTATION & LOGISTICS

- 14.11.1 DIGITIZATION OF TRANSPORT NETWORKS AND NEED FOR OPERATIONAL VISIBILITY TO ACCELERATE SIEM ADOPTION

- 14.12 MEDIA & ENTERTAINMENT

- 14.12.1 ESCALATING CONTENT PIRACY AND PLATFORM SECURITY CHALLENGES TO DRIVE SIEM ADOPTION

- 14.13 OTHER VERTICALS

15 SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 15.2.2 US

- 15.2.2.1 Strong regulatory push and AI-driven innovation to fuel market

- 15.2.3 CANADA

- 15.2.3.1 Regulatory guidance, enterprise demand, and service ecosystem to drive market

- 15.3 EUROPE

- 15.3.1 EUROPE: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 15.3.2 UK

- 15.3.2.1 Advanced managed security services and AI-driven partnerships to drive market

- 15.3.3 GERMANY

- 15.3.3.1 Strong Industry 4.0 adoption and rising cybersecurity requirements for industrial infrastructure to drive market

- 15.3.4 FRANCE

- 15.3.4.1 Rising cyber threat incidents and enterprise SIEM modernization to drive market

- 15.3.5 ITALY

- 15.3.5.1 Escalating cyber threat landscape and AI-enabled security transformation to drive market

- 15.3.6 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 15.4.2 CHINA

- 15.4.2.1 Centralized cyber control and evolving data security regulations to drive market

- 15.4.3 JAPAN

- 15.4.3.1 AI-enabled security transformation to accelerate SIEM adoption

- 15.4.4 INDIA

- 15.4.4.1 Rising investments and partnerships to accelerate market growth

- 15.4.5 AUSTRALIA & NEW ZEALAND

- 15.4.5.1 Automation-led security operations to fuel SIEM adoption

- 15.4.6 REST OF ASIA PACIFIC

- 15.5 MIDDLE EAST & AFRICA

- 15.5.1 MIDDLE EAST & AFRICA: SECURITY INFORMATION AND EVENT MANAGEMENT (SIEM) MARKET DRIVERS

- 15.5.2 MIDDLE EAST

- 15.5.2.1 GCC

- 15.5.2.1.1 UAE

- 15.5.2.1.1.1 Regulatory compliance and managed SIEM services to drive market

- 15.5.2.1.2 KSA

- 15.5.2.1.2.1 Strategic partnerships and Vision 2030 initiatives to drive market

- 15.5.2.1.3 Rest of GCC

- 15.5.2.1.1 UAE

- 15.5.2.2 Rest of Middle East

- 15.5.2.1 GCC

- 15.5.3 AFRICA

- 15.5.3.1 Partnerships, AI models, and managed security services to drive market

- 15.6 LATIN AMERICA

- 15.6.1 LATIN AMERICA: SECURITY INFORMATION AND EVENT MANAGEMENT MARKET DRIVERS

- 15.6.2 BRAZIL

- 15.6.2.1 Increasing focus on strengthening security operations with advanced SIEM and threat intelligence to drive market

- 15.6.3 MEXICO

- 15.6.3.1 AI-driven cyber threats and national cybersecurity reforms to drive market

- 15.6.4 REST OF LATIN AMERICA

16 COMPETITIVE LANDSCAPE

- 16.1 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2026

- 16.2 REVENUE ANALYSIS, 2020-2025

- 16.3 MARKET SHARE ANALYSIS, 2025

- 16.4 PRODUCT/BRAND COMPARISON

- 16.5 COMPANY VALUATION AND FINANCIAL METRICS

- 16.5.1 COMPANY VALUATION

- 16.5.2 FINANCIAL METRICS USING EV/EBITDA

- 16.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- 16.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.6.5.1 Company footprint

- 16.6.5.2 Regional footprint

- 16.6.5.3 Offering footprint

- 16.6.5.4 Deployment mode footprint

- 16.6.5.5 Vertical footprint

- 16.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.7.1 PROGRESSIVE COMPANIES

- 16.7.2 RESPONSIVE COMPANIES

- 16.7.3 DYNAMIC COMPANIES

- 16.7.4 STARTING BLOCKS

- 16.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.7.5.1 Detailed list of key startups/SMEs

- 16.7.5.2 Competitive benchmarking of key startups/SMEs

- 16.8 COMPETITIVE SCENARIO

- 16.8.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 16.8.2 DEALS

17 COMPANY PROFILE

- 17.1 KEY PLAYERS

- 17.1.1 SPLUNK

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches/enhancements

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 MICROSOFT

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches/enhancements

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 IBM

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Solutions/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches/enhancements

- 17.1.3.4 MnM view

- 17.1.3.4.1 Key strengths

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses and competitive threats

- 17.1.4 CROWDSTRIKE

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches/enhancements

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Other developments

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 PALO ALTO NETWORKS

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Solutions/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches/enhancements

- 17.1.5.3.2 Deals

- 17.1.5.4 MnM view

- 17.1.5.4.1 Key strengths

- 17.1.5.4.2 Strategic choices

- 17.1.5.4.3 Weaknesses and competitive threats

- 17.1.6 ELASTIC

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions/Services offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Product launches/enhancements

- 17.1.6.3.2 Deals

- 17.1.7 GOOGLE

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Solutions/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches/enhancements

- 17.1.7.3.2 Deals

- 17.1.7.3.3 Other developments

- 17.1.8 FORTINET

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Solutions/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches/enhancements

- 17.1.9 RAPID7

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Solutions/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches/enhancements

- 17.1.9.3.2 Deals

- 17.1.10 SECEON

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Solutions/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches/enhancements

- 17.1.10.3.2 Deals

- 17.1.11 OPENTEXT

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Solutions/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Product launches/enhancements

- 17.1.12 MANAGEENGINE

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Solutions/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product launches/enhancements

- 17.1.13 HUAWEI

- 17.1.14 DATADOG

- 17.1.15 QAX

- 17.1.16 NETWITNESS

- 17.1.17 SOLARWINDS

- 17.1.1 SPLUNK

- 17.2 OTHER PLAYERS

- 17.2.1 EXABEAM

- 17.2.2 SUMO LOGIC

- 17.2.3 SECURONIX

- 17.2.4 GURUCUL

- 17.2.5 GRAYLOG

- 17.2.6 DEVO

- 17.2.7 LOGSIGN

- 17.2.8 HUNTERS

- 17.2.9 UTMSTACK

- 17.2.10 PANTHER

- 17.2.11 HUNTSMAN SECURITY

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Breakup of primary profiles

- 18.1.2.2 Key insights from industry experts

- 18.2 DATA TRIANGULATION

- 18.3 MARKET SIZE ESTIMATION

- 18.3.1 TOP-DOWN APPROACH

- 18.3.2 BOTTOM-UP APPROACH

- 18.4 MARKET FORECAST

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS