|

시장보고서

상품코드

2066527

보안 정보 및 이벤트 관리(SIEM) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Security Information And Event Management (SIEM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

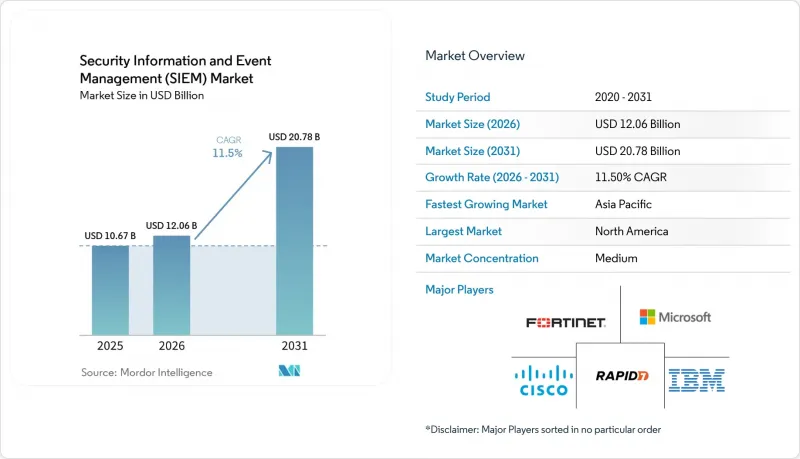

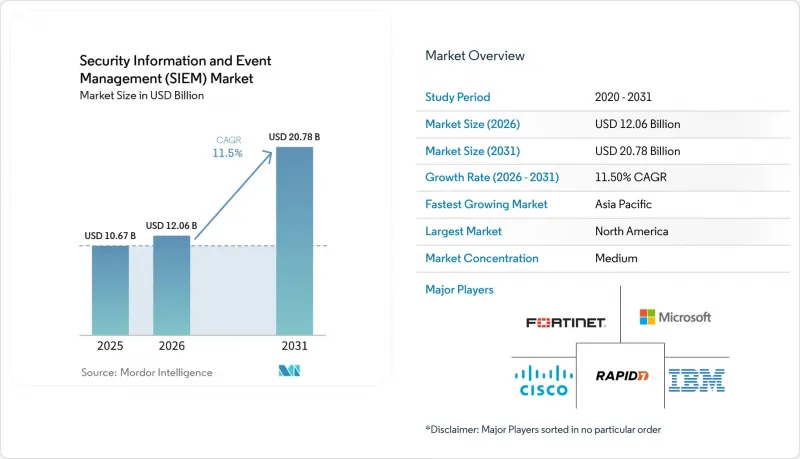

Mordor Intelligence에 의하면, 보안 정보 및 이벤트 관리(SIEM) 시장 규모는 2025년에 106억 7,000만 달러로 평가되었습니다. 2026년 120억 6,000만 달러에서 2031년까지 207억 8,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 11.5%를 나타낼 전망입니다.

본 보고서는 배포 형태(On-Premise, 클라우드, 하이브리드), 아키텍처(레거시, 클라우드 네이티브, 오픈소스), 구성 요소(플랫폼, 서비스 등), 조직 규모(중소기업, 대기업), 최종 사용자(은행, 금융서비스 및 보험(BFSI), 소매 등), 용도(위협 감지, 규정 준수 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 보안 정보 및 이벤트 관리(SIEM) 시장 동향 및 인사이트

보안 텔레메트리 데이터량의 기하급수적인 증가

직원 수가 1만 명 이상인 조직에서는 엔드포인트, 멀티클라우드 서비스, SaaS 도구 및 운영 기술(OT) 네트워크에 걸쳐 현재 하루에 10테라바이트 이상의 로그 데이터를 수집하고 있습니다. 마이크로소프트의 보고서에 따르면, 2025년에 Sentinel을 통해 처리된 이벤트 수는 전년 대비 150% 급증했으며, 로그의 각 행이 색인화됨에 따라 스토리지 예산에 큰 부담이 가해지고 있는 실정이 드러났습니다. 비용을 절감하기 위한 표준적인 설계 기법으로, 계층형 저장, 핫·웜·콜드 스토리지, 그리고 스트리밍 분석 파이프라인이 주목받고 있습니다. 재택근무로 인해 데이터의 홍수는 더욱 심화되고 있으며, 2024년부터 2025년에 걸쳐 VPN 인증 건수는 5배로 증가하여, 고정된 경계에 맞추어 조정되었던 감지 로직을 재구축할 수밖에 없는 상황에 처했습니다. 이 방대한 데이터를 효율적으로 압축, 정규화, 선별할 수 있는 벤더가 우위를 점하며, 보안 정보 및 이벤트 관리(SIEM) 시장의 성장을 가속화하고 있습니다.

규제에 따른 벌칙 및 감사 빈도의 강화

유럽의 NIS2 지침은 2024년 10월에 시행되었으며, 사고 기록이 불충분할 경우 전 세계 매출액의 최대 2%에 해당하는 벌금이 부과될 수 있습니다. 또한, ‘디지털 운영 복원력법’에 따라 유럽의 금융기관은 2025년 1월부터 분기별로 SIEM을 활용한 플레이북 테스트를 실시했습니다. 미국에서는 2023년 하반기에 발효된 SEC 규정에 따라 상장 기업은 중대한 사이버 보안 사고를 4영업일 이내에 공시해야 할 의무가 있습니다. 이러한 규제 체계의 통합에 따라, 변조 방지 기능과 검색 기능을 갖춘 이벤트 스토어 및 실시간 상관 분석이 요구되고 있으며, 규제가 엄격한 업계와 관련 업계 모두에서 도입이 가속화되고 있습니다.

높은 총소유비용(TCO)과 라이선싱의 복잡성

'사용량 기반 라이선싱' 방식에서는 클라우드, IoT 또는 SaaS 소스가 가동되면 비용이 급증하여 재무 부서를 당황하게 만듭니다. 2024년에 하루 500GB의 예산을 책정했던 기업조차 2025년까지 사용량이 2TB를 넘어섰고, 연간 지출이 4배로 급증했습니다. 수년에 걸친 데이터 보존으로 인해 페타바이트 규모의 스토리지 비용이 발생하며, 규칙 조정을 위한 전문 서비스 비용이 총 지출의 4분의 1을 추가로 차지합니다. 각 벤더사는 스토리지와 컴퓨팅을 분리함으로써 이에 대응하고 있으며, 고객은 원시 데이터를 저렴한 오브젝트 저장소에 저장하고, 쿼리나 감지가 실행될 때만 요금을 지불할 수 있습니다. 그러나 이러한 전환에는 스키마 설계 및 즉석 쿼리와 관련된 새로운 기술이 요구됩니다.

부문별 분석

클라우드 도입은 2031년까지 연평균 성장률(CAGR) 12.84%로 확대되고 있으며, 이는 보안 정보 및 이벤트 관리(SIEM) 시장 전체의 성장률인 11.50%를 상회하고 있습니다. 사용량 기반 과금제의 유연성과 하드웨어 업데이트 주기의 해소는 재무 부서에게 매력적인 요소이며, 한편 직접적인 API 통합을 통해 기존 에이전트로는 측정할 수 없었던 서버리스 함수, 컨테이너 오케스트레이터, SaaS 테넌트에서 발생하는 텔레메트리 데이터를 수집할 수 있게 됩니다. 2025년에도 On-Premise 시스템은 이미 이루어진 투자와 에어갭 방식의 방어 네트워크에 힘입어 여전히 55.27%의 점유율을 차지했습니다. 하이브리드 모델을 통해 규제 대상인 은행 및 의료 서비스 제공업체는 기밀성이 높은 로그를 국내에 보관하면서, 정교한 분석을 위해 클라우드 컴퓨팅 성능의 급격한 증가를 활용할 수 있습니다.

기업들이 On-Premise 클러스터의 패치 적용, 확장, 튜닝에 필요한 인건비를 인식하게 될수록, 클라우드의 운영 비용 측면에서의 우위는 더욱 커집니다. 퍼블릭 클라우드 제공업체가 인프라 관리 업무를 맡음으로써, 사내 팀은 디스크 프로비저닝 대신 위협 감지에 집중할 수 있게 됩니다. 데이터 현지화 법에 따라 획일적인 전략은 어려워졌으며, 지역별 인스턴스가 상호 연관된 경보를 전 세계 뷰로 전달하는 연합형 설계가 요구되고 있습니다. 이러한 아키텍처의 유연성 덕분에 중견 기업에서의 도입이 확대되면서 보안 정보 및 이벤트 관리(SIEM) 시장이 강화되고 있습니다.

클라우드 네이티브 및 차세대 스택은 2031년까지 연평균 11.95%의 성장률을 보일 것으로 예상되며, 2025년에는 레거시 관계형 데이터베이스 플랫폼이 차지했던 48.12%의 시장 점유율을 추월했습니다. 스토리지와 컴퓨팅을 분리하는 설계 덕분에, 팀은 원시 로그를 저렴한 오브젝트 스토리지에 저장하고, 조사 시에만 쿼리를 실행할 수 있게 됩니다. 2025년 벤더 벤치마크에 따르면, 이를 통해 인프라 비용을 최대 60%까지 절감할 수 있다고 합니다. Wazuh나 Graylog와 같은 오픈소스 대체 솔루션은 코드 투명성이 필요한 예산이 제한된 기관에 매력적이지만, 커넥터를 직접 개발해야 하며 24시간 유지보수가 필요합니다.

기업들이 맞춤형 상관 관계 규칙이나 분석가 교육에 수백만을 투자하고 있기 때문에 전환 비용이 마이그레이션을 가로막는 걸림돌이 되고 있습니다. 그럼에도 불구하고, 2024년 3월 시스코가 스플렁크를 280억 달러에 인수한 것은 기존 고객들의 신뢰를 흔들었고, 새로운 공급업체와의 시범 프로그램 시작으로 이어졌습니다. 클라우드 네이티브 제공업체들은 신속한 도입, AI를 활용한 트리아지, 종량제 요금제를 통해 차별화를 꾀하고 있습니다. 기존 벤더들은 관리형 도입 서비스나 데이터베이스 플랫폼 마이그레이션을 통해 대응하고 있지만, 탄력적인 확장을 전제로 구축된 아키텍처에 대한 수요가 증가함에 따라 최신 솔루션을 위한 보안 정보 및 이벤트 관리(SIEM) 시장 규모가 확대되고 있습니다.

지역별 분석

북미는 2025년 매출의 41.39%를 차지했으며, 이는 거의 실시간으로 침해를 감지하고 4일 이내에 침해 사실을 보고하도록 의무화한 SEC의 공시 요건에 힘입은 결과입니다. 상장 기업들은 SaaS 및 인프라 로그와 대규모로 통합되는 클라우드 네이티브 서비스로의 전환을 우선시하며, On-Premise 환경의 폐지를 가속화했습니다. 사이버 보안 스타트업에 대한 벤처 투자와 중요 인프라 보호를 위한 정부 지출 역시 이 지역의 경쟁력을 더욱 강화하고 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정), NIS2, DORA가 중첩되는 영향으로 상당한 수요가 예상됩니다. 2024년 말까지 16만 개가 넘는 추가 사업체가 NIS2의 적용 대상이 되며, 중견 기업들은 예산 제약이 있음에도 불구하고 통합 로그 관리 시스템 도입을 피할 수 없게 되었습니다. 금융 기관들은 분기별 복원력 테스트를 자동화하고 있으며, 제조업 수출 기업들은 엄격한 보안 정보 및 이벤트 관리(SIEM) 시장에서 고객을 대상으로 공급망 보안을 입증하기 위해 SIEM 분석을 활용하고 있습니다.

아시아태평양은 인도, 인도네시아, 베트남이 결제 디지털화와 데이터 현지화를 추진하고 있어 연평균 성장률(CAGR) 12.72%로 성장을 주도하고 있습니다. 중국의 규제에 따라 로그가 국내에 보관되게 되었으며, 모니터링 대시보드와 연동되는 지역별 SIEM 노드가 설치되어 있습니다. 싱가포르는 사이버 보안 허브로서의 입지를 다져가고 있는 반면, 호주에서는 주목을 받은 정보 유출 사건을 계기로 중요 인프라 관련 법규가 강화되고 있습니다. 남미와 중동에서는 텔레메트리 활용을 확대하는 스마트시티 및 전자정부 프로그램에 대한 투자가 꾸준히 진행되고 있지만, 환율 변동과 인력 부족이라는 과제에 직면해 있습니다. 아프리카는 남아프리카공화국, 나이지리아, 이집트를 중심으로 한 신흥 시장으로서의 잠재력을 지니고 있으며, 이들 국가에서는 통신 및 은행 부문이 조기 도입을 주도하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the security information and event management market size was valued at USD 10.67 billion in 2025 and is estimated to grow from USD 12.06 billion in 2026 to reach USD 20.78 billion by 2031, at a CAGR of 11.5% during the forecast period (2026-2031).

This report is Segmented by Deployment (On-Premise, Cloud, and Hybrid), Architecture (Legacy, Cloud-Native, and Open-Source), Component (Platform, Services, and More), Organization Size (SME, and Large Enterprises), End-User (BFSI, Retail, and More), Application (Threat Detection, Compliance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Security Information And Event Management (SIEM) Market Trends and Insights

Exponential Growth of Security Telemetry Volumes

Organizations with more than 10,000 employees now ingest over 10 terabytes of log data each day, spanning endpoints, multi-cloud services, SaaS tools, and operational-technology networks. Microsoft reported that events processed by Sentinel surged 150% year-over-year during 2025, underscoring the strain on storage budgets when every log line is indexed. Tiered retention, hot-warm-cold storage, and streaming analytics pipelines are emerging as default design choices to keep costs in check. Remote work further amplifies the data flood, VPN authentications quintupled between 2024 and 2025, reshaping detection logic calibrated for fixed perimeters. Vendors that efficiently compress, normalize, and triage this torrent gain an edge, accelerating the security information and event management (SIEM) market.

Escalating Regulatory Penalties and Audit Frequency

Europe's NIS2 directive became enforceable in October 2024 and allows fines of up to 2% of global revenue for inadequate incident logging. The Digital Operational Resilience Act obliges European financial entities to test SIEM-driven playbooks every quarter starting January 2025. In the United States, SEC rules that took effect in late 2023 require public companies to disclose material cybersecurity incidents within four business days. These converging frameworks demand immutable, searchable event stores and real-time correlation, propelling procurement among both heavily regulated and adjacent sectors.

High Total Cost of Ownership and Licensing Complexity

Pay-by-ingest licensing means costs spike when cloud, IoT, or SaaS sources are activated, blindsiding finance teams. Enterprises that budgeted for 500 GB per day in 2024 saw usage balloon past 2 TB by 2025, quadrupling annual spend. Multi-year retention adds petabyte storage bills, and professional services for rule-tuning consume another quarter of total outlay. Vendors are countering with decoupled storage and compute, letting customers push raw data into cheap object repositories and pay only when queries or detections run, but that shift demands new skills in schema design and ad-hoc querying.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Cloud and Hybrid Adoption of Enterprise Workloads

- AI/ML-Infused Analytics Improve Signal-to-Noise Ratios

- Shortage of Skilled SOC Analysts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments are expanding at a 12.84% CAGR through 2031, eclipsing the 11.50% trajectory of the overall Security Information and Event Management market. The elasticity of pay-per-use pricing and the elimination of hardware refresh cycles appeal to finance teams, while direct API integrations pull telemetry from serverless functions, container orchestrators, and SaaS tenants that legacy agents cannot instrument. On-premises systems still held 55.27% share in 2025, anchored by sunk investments and air-gapped defense networks. Hybrid models let regulated banks and healthcare providers keep sensitive logs in-country yet harness cloud compute bursts for advanced analytics.

The operating-expense advantage of cloud grows when enterprises recognize the staff hours required to patch, scale, and tune on-premises clusters. Public-cloud providers absorb infrastructure chores, letting internal teams focus on threat-hunting rather than disk provisioning. Data-localization laws complicate one-size-fits-all strategies, prompting federated designs where regional instances forward correlated alerts to a global view. This architectural flexibility is widening adoption among mid-size organizations, reinforcing the security information and event management (SIEM) market.

Cloud-native and next-generation stacks are projected to grow at 11.95% through 2031, challenging the 48.12% foothold that legacy relational-database platforms enjoyed in 2025. Decoupled storage-compute designs let teams park raw logs in cheap object stores and spin up queries only during investigations, slicing infrastructure spend by as much as 60% according to 2025 vendor benchmarks. Open-source alternatives like Wazuh and Graylog appeal to budget-constrained agencies that need code transparency, but they require DIY connectors and round-the-clock maintenance.

Switching costs slow migration because enterprises have millions invested in custom correlation rules and analyst training. Nonetheless, Cisco's USD 28 billion purchase of Splunk in March 2024 rattled installed-base confidence and triggered pilot programs with newer vendors. Cloud-native providers differentiate on rapid onboarding, AI-assisted triage, and consumption pricing. Legacy vendors are countering through managed deployment offerings and database re-platforming, but the momentum favours architectures built for elastic scale, lifting the security information and event management (SIEM) market size for modern solutions.

Geography Analysis

North America generated 41.39% of 2025 revenue, propelled by SEC disclosure mandates that force near-real-time detection and four-day breach reporting. Public corporations accelerated decommissioning of on-premises stacks in favour of cloud-native services that integrate with SaaS and infrastructure logs at massive scale. Venture investment in cybersecurity startups and government spending on critical-infrastructure protection also reinforce the region's primacy.

Europe commands sizable demand thanks to the overlapping weight of GDPR, NIS2, and DORA. More than 160,000 additional entities fell under NIS2 by late 2024, compelling mid-tier operators to adopt centralized log management despite budget constraints. Financial houses are automating quarterly resilience tests, and manufacturing exporters rely on SIEM analytics to certify supply-chain security for customers in strict security information and event management (SIEM) markets.

Asia Pacific leads growth at 12.72% CAGR as India, Indonesia, and Vietnam digitize payments and enforce data-localization. Chinese mandates keep logs onshore, prompting regional SIEM nodes that federate to a supervisory dashboard. Singapore is positioning as a cybersecurity hub, while Australia tightens critical-infrastructure laws after high-profile breaches. South America and the Middle East invest steadily in smart-city and e-government programs that expand telemetry but face currency volatility and skills gaps. Africa remains an emerging opportunity centered on South Africa, Nigeria, and Egypt, where telecom and banking sectors shoulder early adoption.

- Cisco Systems, Inc.

- International Business Machines Corporation

- Microsoft Corporation

- Google LLC

- Fortinet, Inc.

- LogRhythm, Inc.

- Exabeam, Inc.

- Rapid7, Inc.

- Open Text Corporation

- RSA Security LLC

- Securonix, Inc.

- CrowdStrike, Inc.

- Elastic N.V.

- AT&T Inc.

- SolarWinds Worldwide, LLC

- Graylog, Inc.

- Logpoint A/S

- Zoho Corporation Pvt. Ltd.

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exponential Growth of Security Telemetry Volumes

- 4.2.2 Escalating Regulatory Penalties and Audit Frequency

- 4.2.3 Accelerated Cloud and Hybrid Adoption of Enterprise Workloads

- 4.2.4 AI/ML-Infused Analytics Improve Signal-to-Noise Ratios

- 4.2.5 Emergence of Security-Data-Pipeline Layer Reduces SIEM TCO

- 4.2.6 Vendor Mega-Deals Trigger Refresh Cycles

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership and Licensing Complexity

- 4.3.2 Shortage of Skilled SOC Analysts

- 4.3.3 Data-Sovereignty Barriers to Central Log Aggregation

- 4.3.4 Overlap with XDR/SOAR Platforms Delays Budget Approval

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By SIEM Architecture

- 5.2.1 Legacy / Traditional SIEM

- 5.2.2 Cloud-Native / Next-Gen SIEM

- 5.2.3 Open-Source SIEM

- 5.3 By Component

- 5.3.1 Platform / Software

- 5.3.2 Professional Services

- 5.3.3 Managed SIEM Services (MSSP)

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services and Insurance

- 5.5.2 Retail and E-Commerce

- 5.5.3 Government and Defense

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Manufacturing

- 5.5.6 Energy and Utilities

- 5.5.7 Telecom and IT

- 5.5.8 Other End-User Industries

- 5.6 By Application

- 5.6.1 Threat Detection and Analytics

- 5.6.2 Compliance and Audit Management

- 5.6.3 Incident Response and Forensics

- 5.6.4 Log Management and Reporting

- 5.6.5 Cloud-Workload Security Monitoring

- 5.6.6 IoT / OT Security Monitoring

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 Germany

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Nordics

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 Australia

- 5.7.3.5 Rest of Asia Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Nigeria

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 International Business Machines Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Google LLC

- 6.4.5 Fortinet, Inc.

- 6.4.6 LogRhythm, Inc.

- 6.4.7 Exabeam, Inc.

- 6.4.8 Rapid7, Inc.

- 6.4.9 Open Text Corporation

- 6.4.10 RSA Security LLC

- 6.4.11 Securonix, Inc.

- 6.4.12 CrowdStrike, Inc.

- 6.4.13 Elastic N.V.

- 6.4.14 AT&T Inc.

- 6.4.15 SolarWinds Worldwide, LLC

- 6.4.16 Graylog, Inc.

- 6.4.17 Logpoint A/S

- 6.4.18 Zoho Corporation Pvt. Ltd.

- 6.4.19 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment