|

시장보고서

상품코드

2043694

헬스케어 클라우드 컴퓨팅 시장 예측(-2031년) : 제품별, 오퍼링별, 도입 형태별, 가격 모델별, 서비스 모델별, 최종사용자별, 지역별Healthcare Cloud Computing Market by Product (EHR, VNA, RIS, LIS, RCM, Telehealth), Deployment (Private, Public), Offering (Software), Pricing (Subs), Service Model (SaaS, IaaS, PaaS), End User (Hospital, ASC, Imaging Centers) - Global Forecast to 2031 |

||||||

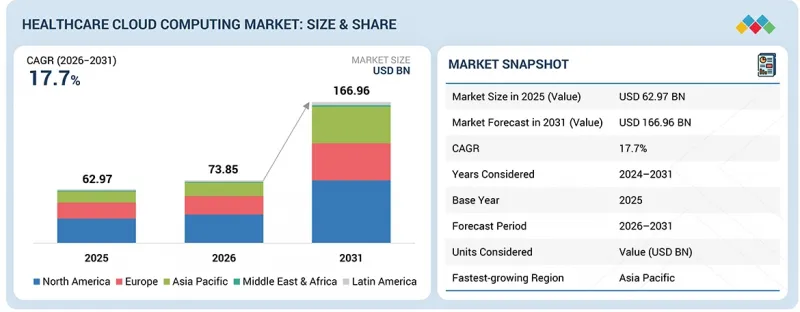

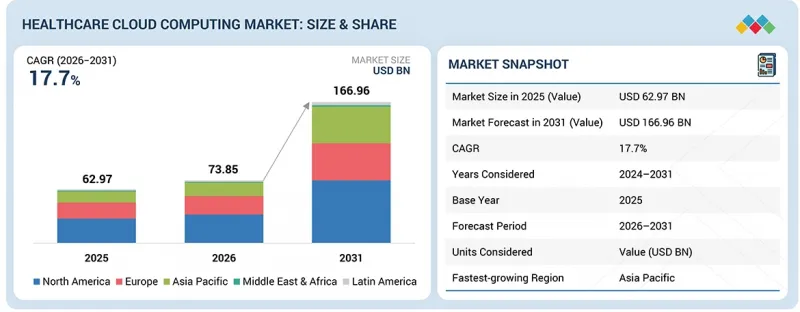

세계의 헬스케어 클라우드 컴퓨팅 시장 규모는 2026년 738억 5,000만 달러에서 2031년까지 1,669억 6,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간 중 CAGR 17.7%라는 높은 신장률을 보일 것으로 전망되고 있습니다.

이 시장의 성장은 전자건강기록(EHR), 전자처방전, 원격의료, 모바일 헬스(mHealth) 솔루션의 도입 확대에 힘입어 성장세를 보이고 있습니다. 정부의 디지털 전환(Digital Transformation, DX) 프로그램으로 인해 의료 산업에서 클라우드 기술의 활용이 점점 더 촉진되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제품별, 오퍼링별, 도입 형태별, 가격 모델별, 서비스 모델별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

2026년 2월, 오라클은 메디케어-메디케이드 서비스 센터(CMS)와 다년 계약을 체결하고 청구 처리 및 수급 자격 심사 시스템 등 의료 분야의 중요한 워크로드를 클라우드 환경에서 관리하기로 했습니다. 기존 컴퓨팅 인프라에서 보다 안전하고 유연한 클라우드 컴퓨팅 인프라로의 전환은 공공 부문의 디지털 전환 노력이 의료 분야의 클라우드 기술 도입에 미치는 영향을 보여줍니다.

"2025년 제품별로는 의료 서비스 제공자 솔루션이 헬스케어 클라우드 컴퓨팅 시장에서 가장 큰 부문을 차지했습니다. "

2025년 제품별로는 의료 서비스 제공자 솔루션 부문이 헬스케어 클라우드 컴퓨팅 시장에서 가장 큰 점유율을 차지했습니다. 이러한 성장은 주로 코로나 사태를 계기로 전자의무기록(EHR), 전자처방전, 원격의료, 모바일 헬스 등 다양한 의료 IT 솔루션의 도입이 확대된 것이 주요 원인으로 분석됩니다. 병원, 진료소, 전문 의료 센터는 전자건강기록(EHR), 의료 영상, 실시간 환자 모니터링 데이터 등 방대한 양의 민감한 환자 데이터를 관리하고 있으며, 이 모든 데이터는 견고하고 확장 가능하며 안전한 저장 및 처리 능력을 필요로 합니다. 클라우드 컴퓨팅은 이러한 의료기관에 향상된 데이터 스토리지, 정보 접근성, 이종 시스템 간의 상호운용성 향상, 고급 분석 기능을 제공합니다.

"2025년 서비스 모델별로는 SaaS(Software-as-a-Service) 부문이 가장 큰 시장점유율을 차지했습니다. "

2025년 서비스 모델별로는 서비스형 소프트웨어(SaaS) 부문이 헬스케어 클라우드 컴퓨팅 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 부문은 비용 효율성, 확장성, 도입의 용이성 등으로 인해 성장세를 보이고 있습니다. SaaS는 필요한 인프라 구축에 많은 투자를 필요로 하지 않기 때문에 의료기관은 SaaS를 통해 전자의무기록(EHR), 원격의료 툴, 기타 각종 애플리케이션을 활용할 수 있습니다. 또한 서로 다른 기기와 애플리케이션 간의 원격 액세스 및 실시간 연동 수요가 증가함에 따라 SaaS는 의료 기관들 사이에서 큰 인기를 얻고 있습니다. 예를 들어 오라클은 '오라클 헬스(Oracle Health)', '서너(Cerner)'와 같은 클라우드 기반 솔루션을 SaaS 방식으로 제공하고 있으며, 세일즈포스는 '세일즈포스 헬스 클라우드(Salesforce Health Cloud)'를 제공하고 있습니다.

"2025년 북미는 헬스케어 클라우드 컴퓨팅 시장에서 가장 큰 지역 시장으로 부상했습니다. "

2025년 북미는 첨단 의료 시스템, 디지털 헬스 솔루션의 높은 보급률, Amazon Web Services, Google, Oracle과 같은 주요 기업의 존재 등의 요인으로 인해 헬스케어 클라우드 컴퓨팅 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 차지했습니다. 헬스케어 클라우드 서비스 도입률이 증가한 주요 이유 중 하나는 HITECH법 등 정부의 노력을 통해 추진된 광범위한 전자건강기록(EHR) 및 전자처방전 시스템의 존재가 주요 원인 중 하나입니다. 미국 보건복지부에 따르면 국내 병원의 96%가 EHR 도입을 추진하고 있습니다. 또한 이 지역에서 사업을 운영하는 Amazon Web Services, Google과 같은 기업도 도입을 촉진하는 데 한 몫을 했습니다.

헬스케어 클라우드 컴퓨팅 시장의 주요 기업

헬스케어·클라우드 컴퓨팅 시장에서 사업을 운영하는 주요 기업으로는 Amazon Web Services, Inc.(미국), Microsoft Corporation(미국), Google, Inc.(미국), athenahealth, Inc.(미국), CareCloud, Inc.(미국), Siemens Healthineers AG(독일), eClinicalWorks(미국), Koninklijke Philips N.V.(네덜란드) 등을 들 수 있습니다.

조사 범위:

이 보고서는 헬스케어 클라우드 컴퓨팅 시장을 분석합니다. 제품, 오퍼링, 서비스 모델, 가격 모델, 도입 모델, 최종사용자 및 지역을 기반으로 각 시장 부문 시장 규모와 미래 성장 잠재력을 추정하는 것을 목표로 합니다. 또한 이 시장의 주요 기업에 대한 경쟁 분석과 함께 각 기업의 기업 개요, 제품 라인업, 최근 동향, 주요 시장 전략에 대해서도 조사하여 전해드립니다.

이 보고서를 구매해야 하는 이유

이 보고서는 기존 기업 및 신규 진입 기업, 중소기업이 시장 동향을 파악하여 시장 점유율 확대에 도움이 될 것입니다. 이 보고서를 구매한 기업은 다음 전략 중 하나 또는 두 가지를 조합하여 시장에서의 입지를 강화할 수 있습니다.

이 보고서는 다음과 같은 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인 분석:(만성질환 유병률 증가와 이에 따른 전자건강기록(EHR) 및 전자처방전 시스템 도입 확대, 의료 분야 빅데이터 분석, 웨어러블 기기, 사물인터넷(IoT) 도입 확대, 스토리지 및 확장성 기능 강화, 새로운 지불 모델 확산과 클라우드의 비용 효율성), 제약 요인(데이터 보안 및 프라이버시 문제, 엄격한 규제 및 컴플라이언스 요건, IT 인프라 관련 제약), 기회(텔레클라우드 및 원격의료 상담의 부상, 헬스케어 클라우드의 블록체인, 하이브리드 클라우드의 효과, ACO의 효율성) ACO의 성장 가능성), 도전과제(상호운용성 및 이식성 관련 과제, 신흥 국가의 기술 전문성 부족) 등 헬스케어 클라우드 컴퓨팅 시장의 성장에 영향을 미치는 요인을 분석하고 있습니다.

- 제품 개발/혁신: 헬스케어 클라우드 컴퓨팅 시장의 미래 기술, 연구개발 활동, 제품 및 서비스 출시에 대한 심층적인 인사이트를 제공합니다.

- 시장 개발: 수익성 높은 신흥 시장, 제품 및 서비스, 용도, 최종사용자 및 지역에 대한 포괄적인 정보를 제공합니다.

- 시장 다각화: 헬스케어 클라우드 컴퓨팅 시장의 제품 포트폴리오, 성장 지역, 최근 동향 및 투자에 대한 포괄적인 정보를 제공합니다.

- 경쟁 분석 : Amazon Web Services, Inc.(미국), Microsoft Corporation(미국), Google, Inc.(미국), athenahealth. Inc.(미국), CareCloud, Inc.(미국), Siemens Healthineers AG(독일), eClinicalWorks(미국), Koninklijke Philips N.V.(네덜란드) 등 헬스케어 클라우드 컴퓨팅 시장 주요 기업의 시장 점유율, 성장 전략, 제품 라인업 및 능력에 관한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 헬스케어 클라우드 컴퓨팅 시장(제품별)

제10장 헬스케어 클라우드 컴퓨팅 시장(오퍼링별)

제11장 헬스케어 클라우드 컴퓨팅 시장(도입 형태별)

제12장 헬스케어 클라우드 컴퓨팅 시장(가격 모델별)

제13장 헬스케어 클라우드 컴퓨팅 시장(서비스 모델별)

제14장 헬스케어 클라우드 컴퓨팅 시장(최종사용자별)

제15장 헬스케어 클라우드 컴퓨팅 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

KSA 26.06.05The global healthcare cloud computing market is projected to reach USD 166.96 billion by 2031 from USD 73.85 billion in 2026, at a high CAGR of 17.7% during the forecast period. The market's growth is boosted by an increasing adoption of Electronic Health Records (EHR), e-prescribing, telehealth, and mobile health (mHealth) solutions. Digital transformation programs being implemented by governments are increasingly driving the use of cloud technologies within the healthcare industry.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, Deployment Model, Service Model, Pricing Model, Offering, End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America and Middle East and Africa |

In February 2026, Oracle signed a multi-year agreement with the Centers for Medicare & Medicaid Services (CMS), wherein it will manage critical workloads in healthcare, such as claims processing and eligibility systems, in the company's cloud environment. This transition from conventional computing infrastructure to a more secure and flexible cloud computing infrastructure demonstrates the impact of digital transformation efforts within the public sector on cloud technology adoption within the healthcare space.

"In 2025, healthcare provider solutions constituted the largest segment in the healthcare cloud computing market, by product."

In 2025, the healthcare provider solutions segment represented the largest share of the healthcare cloud computing market, by product. This growth is primarily driven by the increased adoption of various health IT solutions, including EHR, e-prescribing, telehealth, and mHealth, spurred by the pandemic. Hospitals, clinics, and specialty care centers manage vast amounts of sensitive patient data, including electronic health records (EHRs), medical imaging, and real-time patient monitoring data, all of which demand robust, scalable, and secure storage and processing capabilities. Cloud computing offers these providers enhanced data storage, easier access to information, improved interoperability among disparate systems, and advanced analytics capabilities.

"In 2025, the software-as-a-service segment accounted for the largest market share among service models."

In 2025, the software-as-a-service segment captured the largest share of the healthcare cloud computing market, by service model. This segment is driven by its cost-effectiveness, scalability, and ease of deployment. Since SaaS does not require large amounts of investments in building the required infrastructure, healthcare organizations can utilize various applications like EHRs, telemedicine tools, and other tools via SaaS. Moreover, there is an increasing demand for remote access and real-time interaction between different devices and applications, making SaaS very popular among healthcare organizations. For example, Oracle Corporation provides its cloud-based solutions, such as Oracle Health and Cerner, in SaaS mode, whereas Salesforce, Inc. provides Salesforce Health Cloud.

"In 2025, North America was the largest regional market for healthcare cloud computing market."

In 2025, North America accounted for the largest share of the healthcare cloud computing market, owing to factors like advanced healthcare systems, higher adoption of digital health solutions, and the presence of key players such as Amazon Web Services, Google, Oracle, and others. One of the key reasons for the growth in the adoption rate of healthcare cloud services was the presence of an extensive electronic health record and e-prescription system in the region that has been encouraged through governmental efforts, such as the HITECH Act. According to the US Department of Health & Human Services, 96% of hospitals in the country have adopted the use of EHR. Moreover, companies like Amazon Web Services and Google operating in this region also helped in fueling adoption.

The breakdown of primary participants is as mentioned below:

- By Company Type - Tier 1: 34%, Tier 2: 46%, and Tier 3: 20%

- By Designation - C Level: 35%, Director Level: 25%, and Others: 40%

- By Region - North America: 30%, Europe: 45%, Asia Pacific: 20%, Latin America: 3%, Middle East & Africa: 2%,

Key Players in the Healthcare Cloud Computing Market

Key players operating in the healthcare cloud computing market include Amazon Web Services, Inc. (US), Microsoft Corporation (US), Google, Inc. (US), athenahealth. Inc. (US), CareCloud, Inc. (US), Siemens Healthineers AG (Germany), eClinicalWorks (US), Koninklijke Philips N.V. (Netherlands), and others.

Research Coverage:

The report analyses the healthcare cloud computing market. It aims to estimate the market size and future growth potential of various market segments based on product, offering, service model, pricing model, deployment model, end user, and region. The report also provides a competitive analysis of the key players in this market, along with their company profiles, product offerings, recent developments, and key market strategies.

Reasons to Buy the Report

This report will help established firms and new entrants/smaller firms to gauge the market's pulse, which, in turn, would help them garner a greater share of the market. Firms purchasing the report could use one or a combination of the following strategies to strengthen their positions in the market.

This report provides insights into:

- Analysis of key drivers: (Rising prevalence of chronic diseases and subsequent adoption of EHR & e-prescription systems; increasing adoption of big data analytics, wearable devices, and IoT in healthcare; enhanced storage and scalability features; proliferation of new payment models and cost-efficiency of cloud), restraints (Data security and privacy concerns, stringent regulatory & compliance requirements, constraints associated with IT infrastructure), opportunities (Emergence of telecloud & telehealth consultations, blockchain in health cloud, efficacy of hybrid cloud, growth potential of ACOs), and challenges (challenges associated with interoperability and portability, limited technical expertise in emerging economies) influencing the growth of the healthcare cloud computing market.

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the healthcare cloud computing market.

- Market Development: Comprehensive information on the lucrative emerging markets, products & services, applications, end users, and regions.

- Market Diversification: Exhaustive information about the product portfolios, growing geographies, recent developments, and investments in the healthcare cloud computing market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, product offerings, and capabilities of the leading players, such as Amazon Web Services, Inc. (US), Microsoft Corporation (US), Google, Inc. (US), athenahealth. Inc. (US), CareCloud, Inc. (US), Siemens Healthineers AG (Germany), eClinicalWorks (US), Koninklijke Philips N.V. (Netherlands), and others, in the healthcare cloud computing market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 HEALTHCARE CLOUD COMPUTING MARKET OVERVIEW

- 3.2 HEALTHCARE CLOUD COMPUTING MARKET, BY PRODUCT & REGION

- 3.3 HEALTHCARE CLOUD COMPUTING MARKET: GEOGRAPHIC SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising prevalence of chronic diseases and subsequent adoption of EHR & e-prescription systems

- 4.2.1.2 Increasing adoption of big data analytics, wearable devices, and IoT in healthcare

- 4.2.1.3 Enhanced storage and scalability features

- 4.2.1.4 Proliferation of new payment models and cost-efficiency of cloud

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data security and privacy concerns

- 4.2.2.2 Stringent regulatory & compliance requirements

- 4.2.2.3 Constraints associated with IT infrastructure

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Emergence of telecloud & telehealth consultations

- 4.2.3.2 Blockchain in health cloud

- 4.2.3.3 Efficacy of hybrid cloud

- 4.2.3.4 Growth potential of ACOs

- 4.2.4 CHALLENGES

- 4.2.4.1 Challenges associated with interoperability & portability

- 4.2.4.2 Limited technical expertise in emerging economies

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE OF HEALTHCARE CLOUD COMPUTING, BY KEY PLAYER (2025)

- 5.5.2 INDICATIVE PRICE OF HEALTHCARE CLOUD COMPUTING, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 TRANSFORMING DIAGNOSTIC IMAGING WITH VISAGE 7 ON AWS FOR ALLINA HEALTH

- 5.9.2 OPTIMIZING HEALTHCARE INFRASTRUCTURE WITH APEX HEALTH SOLUTIONS

- 5.9.3 CENTRALIZING PATIENT INFORMATION MANAGEMENT WITH CLOUD-BASED ECM SOLUTIONS

- 5.10 IMPACT OF US TARIFFS-HEALTHCARE CLOUD COMPUTING MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.10.5.1 Hospitals

- 5.10.5.2 Pharmacies

- 5.10.5.3 Public Payers

- 5.10.5.4 Private Payers

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 BIG DATA ANALYTICS

- 6.1.2 INTERNET OF THINGS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 ARTIFICIAL INTELLIGENCE (AI) & MACHINE LEARNING (ML)

- 6.2.2 EDGE COMPUTING AND IOT INTEGRATION

- 6.2.3 5G NETWORKS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 CYBERSECURITY & DATA ENCRYPTION

- 6.3.2 BLOCKCHAIN

- 6.3.3 EHR SYSTEMS

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 PATENT PUBLICATION TRENDS FOR HEALTHCARE CLOUD COMPUTING

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-DRIVEN PREDICTIVE ENGAGEMENT

- 6.6.2 REMOTE PATIENT MONITORING & TELEHEALTH

- 6.6.3 INTEROPERABILITY & DATA EXCHANGE

- 6.7 IMPACT OF AI/GEN AI ON HEALTHCARE CLOUD COMPUTING MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 MARKET POTENTIAL OF AI/GEN AI IN HEALTHCARE CLOUD COMPUTING MARKET

- 6.7.3 CASE STUDIES RELATED TO AI/GEN AI IMPLEMENTATION

- 6.7.3.1 Deploying Generative AI to Modernize Healthcare Operations

- 6.7.4 IMPACT OF AI/GEN AI ON INTERCONNECTED AND ADJACENT ECOSYSTEMS

- 6.7.4.1 Clinical information system

- 6.7.4.2 Population health management solutions

- 6.7.4.3 Cloud infrastructure & platform (SaaS, PaaS, IaaS)

- 6.7.5 USER READINESS AND IMPACT ASSESSMENT

- 6.7.5.1 User readiness

- 6.7.5.1.1 User A: Healthcare providers

- 6.7.5.1.2 User B: Healthcare payers

- 6.7.5.2 Impact assessment

- 6.7.5.2.1 User A: Healthcare providers

- 6.7.5.2.1.1 Implementation

- 6.7.5.2.1.2 Impact

- 6.7.5.2.2 User B: Healthcare payers

- 6.7.5.2.2.1 Implementation

- 6.7.5.2.2.2 Impact

- 6.7.5.2.1 User A: Healthcare providers

- 6.7.5.1 User readiness

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.2.1 North America

- 7.1.2.2 Europe

- 7.1.2.3 Asia Pacific

- 7.1.2.4 Latin America

- 7.1.2.5 Middle East & Africa

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END-USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 HEALTHCARE CLOUD COMPUTING MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 HEALTHCARE PROVIDER SOLUTIONS

- 9.2.1 CLINICAL INFORMATION SYSTEMS

- 9.2.1.1 EHR/EMR

- 9.2.1.1.1 Convenient access & transfer of patient information to drive market

- 9.2.1.2 PACS & VNA

- 9.2.1.2.1 Broad applications for image generation to boost demand

- 9.2.1.3 PHM solutions

- 9.2.1.3.1 Ability to identify high-risk patient populations and ensure targeted healthcare delivery to drive market

- 9.2.1.4 Telehealth solutions

- 9.2.1.4.1 Remote access and shortage of healthcare professionals to fuel uptake

- 9.2.1.5 Radiology information systems

- 9.2.1.5.1 Integration with HIS to enable automation and streamlining of patient workflows

- 9.2.1.6 Laboratory information systems

- 9.2.1.6.1 Cloud-based LIS offers high efficiency, scalability, and cost-efficiency

- 9.2.1.7 Pharmacy information systems

- 9.2.1.7.1 Growing trend of e-prescriptions to support market growth

- 9.2.1.8 Other clinical information systems

- 9.2.1.1 EHR/EMR

- 9.2.2 NON-CLINICAL INFORMATION SYSTEMS

- 9.2.2.1 RCM solutions

- 9.2.2.1.1 Ability to accelerate revenue cycles and automate processes to drive market

- 9.2.2.2 Financial management solutions

- 9.2.2.2.1 Simplification of labor-intensive healthcare financial management functions to support market growth

- 9.2.2.3 HIE solutions

- 9.2.2.3.1 Rising need for real-time sharing to boost demand

- 9.2.2.4 SCM solutions

- 9.2.2.4.1 Execution of transactions with minimal operational & administrative expenses to drive market

- 9.2.2.5 Billing & account management solutions

- 9.2.2.5.1 Implementation of cloud-based billing for enhanced customer convenience

- 9.2.2.6 Other non-clinical information systems

- 9.2.2.1 RCM solutions

- 9.2.1 CLINICAL INFORMATION SYSTEMS

- 9.3 HEALTHCARE PAYER SOLUTIONS

- 9.3.1 CLAIMS MANAGEMENT SOLUTIONS

- 9.3.1.1 Frequent need for software upgrades to drive the market

- 9.3.2 PAYMENT MANAGEMENT SOLUTIONS

- 9.3.2.1 Connection on a uniform integrated network to boost demand

- 9.3.3 CRM SOLUTIONS

- 9.3.3.1 Broad uptake of CSS and TES applications to propel market

- 9.3.4 PRM SOLUTIONS

- 9.3.4.1 Ability to provide flexibility for implementation of network strategies to support market growth

- 9.3.5 FRAUD MANAGEMENT SOLUTIONS

- 9.3.5.1 Increasing cases of fraudulent claims to support market growth

- 9.3.1 CLAIMS MANAGEMENT SOLUTIONS

10 HEALTHCARE CLOUD COMPUTING MARKET, BY OFFERING

- 10.1 INTRODUCTION

- 10.2 SERVICES

- 10.2.1 CONSULTING SERVICES

- 10.2.1.1 High demand in emerging economies to boost the market

- 10.2.2 IMPLEMENTATION SERVICES & IT SUPPORT

- 10.2.2.1 Growing demand for integration solutions and technical assistance to drive market

- 10.2.3 TRAINING & EDUCATION SERVICES

- 10.2.3.1 Rising awareness initiatives on technical assistance to fuel market

- 10.2.4 POST-SALES & MAINTENANCE SERVICES

- 10.2.4.1 Ability to rectify interoperability issues to support market growth

- 10.2.1 CONSULTING SERVICES

- 10.3 SOFTWARE

- 10.3.1 AUTOMATION TREND AND REDUCTION OF HEALTHCARE EXPENDITURE TO BOOST DEMAND

11 HEALTHCARE CLOUD COMPUTING MARKET, BY DEPLOYMENT MODEL

- 11.1 INTRODUCTION

- 11.2 PRIVATE CLOUD

- 11.2.1 ON-DEMAND INFRASTRUCTURE TO DRIVE MARKET

- 11.3 HYBRID CLOUD

- 11.3.1 HIGH SECURITY AND FLEXIBILITY TO PROPEL THE MARKET

- 11.4 PUBLIC CLOUD

- 11.4.1 DATA SECURITY & PRIVACY CONCERNS TO LIMIT MARKET ADOPTION

12 HEALTHCARE CLOUD COMPUTING MARKET, BY PRICING MODEL

- 12.1 INTRODUCTION

- 12.2 PAY-AS-YOU-GO PRICING MODEL

- 12.2.1 MINIMAL OPERATIONAL COSTS TO PROPEL MARKET

- 12.3 SUBSCRIPTION-BASED PRICING MODEL

- 12.3.1 UNLIMITED SERVICES TO BOOST DEMAND

13 HEALTHCARE CLOUD COMPUTING MARKET, BY SERVICE MODEL

- 13.1 INTRODUCTION

- 13.2 SOFTWARE-AS-A-SERVICE

- 13.2.1 INCREASING DEPLOYMENT OF MULTIPLE CLOUD-BASED APPLICATIONS TO DRIVE MARKET

- 13.3 INFRASTRUCTURE-AS-A-SERVICE

- 13.3.1 USAGE-BASED PRICING AND FLEXIBLE SCALABILITY TO BOOST DEMAND

- 13.4 PLATFORM-AS-A-SERVICE

- 13.4.1 SIMPLIFIED APPLICATION DEVELOPMENT WITH LOW CAPITAL EXPENSES TO PROPEL MARKET

14 HEALTHCARE CLOUD COMPUTING MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 HEALTHCARE PROVIDERS

- 14.2.1 HOSPITALS

- 14.2.1.1 Ability to streamline clinical workflows and manage patient volumes to boost demand

- 14.2.2 PHARMACIES

- 14.2.2.1 Convenient prescription management with cloud computing to augment market growth

- 14.2.3 DIAGNOSTIC IMAGING CENTERS

- 14.2.3.1 Management of imaging data to fuel the market

- 14.2.4 AMBULATORY SURGERY CENTERS

- 14.2.4.1 Rising adoption of telehealth consultations to support market growth

- 14.2.1 HOSPITALS

- 14.3 HEALTHCARE PAYERS

- 14.3.1 PUBLIC PAYERS

- 14.3.1.1 Supportive government initiatives for healthcare coverage to propel market

- 14.3.2 PRIVATE PAYERS

- 14.3.2.1 High uptake of claims & revenue cycle management solutions to drive market

- 14.3.1 PUBLIC PAYERS

15 HEALTHCARE CLOUD COMPUTING MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 15.2.2 US

- 15.2.2.1 Federal policy and hyperscaler partnerships establish cloud as the backbone of US HCIT

- 15.2.3 CANADA

- 15.2.3.1 Pan-Canadian interoperability roadmap and cloud PACS migration drive federal digital health investment

- 15.3 EUROPE

- 15.3.1 EUROPE: MACROECONOMIC OUTLOOK

- 15.3.2 GERMANY

- 15.3.2.1 KHZG cloud mandate and ePA rollout catalyze hospital cloud infrastructure adoption

- 15.3.3 UK

- 15.3.3.1 NHS multi-cloud strategy and Microsoft partnership anchor the largest public healthcare cloud transformation

- 15.3.4 FRANCE

- 15.3.4.1 HDS Sovereign Cloud Certification and Segur imaging compliance drive cloud infrastructure investment

- 15.3.5 ITALY

- 15.3.5.1 Introduction of National eHealth Pact to support market growth

- 15.3.6 SPAIN

- 15.3.6.1 National digital health strategy and PNRR-backed cloud investment modernize SNS imaging infrastructure

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 15.4.2 JAPAN

- 15.4.2.1 Rising potential of wireless technologies to boost demand

- 15.4.3 CHINA

- 15.4.3.1 Rising incidence of infectious diseases and growing adoption of telehealth consultations to fuel market growth

- 15.4.4 INDIA

- 15.4.4.1 Growth in healthcare sector and increasing target patient population to drive market

- 15.4.5 AUSTRALIA

- 15.4.5.1 Favorable initiatives for EMR/EHR uptake to fuel market

- 15.4.6 SINGAPORE

- 15.4.6.1 Improvements in cloud infrastructure to support market growth

- 15.4.7 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 15.5.2 BRAZIL

- 15.5.2.1 Uptake of medical device connectivity solutions to drive market

- 15.5.3 MEXICO

- 15.5.3.1 Favorable initiatives for cloud migration to support market growth

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 Introduction of Health Cloud project to boost demand

- 15.6.3 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.3 REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS

- 16.4.1 AMAZON WEB SERVICES, INC. (US)

- 16.4.2 MICROSOFT (US)

- 16.4.3 GOOGLE, INC. (US)

- 16.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- 16.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.5.5.1 Company footprint

- 16.5.5.2 Region footprint

- 16.5.5.3 Product footprint

- 16.5.5.4 Component footprint

- 16.5.5.5 End-user footprint

- 16.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.6.1 PROGRESSIVE COMPANIES

- 16.6.2 RESPONSIVE COMPANIES

- 16.6.3 DYNAMIC COMPANIES

- 16.6.4 STARTING BLOCKS

- 16.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.7 COMPANY VALUATION & FINANCIAL METRICS

- 16.7.1 FINANCIAL METRICS

- 16.7.2 COMPANY VALUATION

- 16.8 BRAND/PRODUCT COMPARISON

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT/SERVICE LAUNCHES

- 16.9.1.1 Deals

- 16.9.1 PRODUCT/SERVICE LAUNCHES

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 AMAZON WEB SERVICES, INC.

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Services offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product/Service launches

- 17.1.1.3.2 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 MICROSOFT

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Services offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product/Service launches

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 GOOGLE LLC (ALPHABET, INC.)

- 17.1.3.1 Business overview

- 17.1.3.2 Products/Services offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product/Service launches

- 17.1.3.4 Recent developments

- 17.1.3.4.1 Deals

- 17.1.3.5 MnM view

- 17.1.3.5.1 Key strategies

- 17.1.3.5.2 Strategic choices

- 17.1.3.5.3 Weaknesses and competitive threats

- 17.1.4 ATHENAHEALTH, INC.

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Services offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product/Service launches

- 17.1.4.3.2 Deals

- 17.1.5 CARECLOUD, INC.

- 17.1.5.1 Business overview

- 17.1.5.2 Products/Services offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product/Service launches & enhancements

- 17.1.5.3.2 Deals

- 17.1.6 SIEMENS HEALTHINEERS AG

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Services offered

- 17.1.7 ECLINICALWORKS

- 17.1.7.1 Business overview

- 17.1.7.2 Products/Services offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Deals

- 17.1.8 KONINKLIJKE PHILIPS N.V.

- 17.1.8.1 Business overview

- 17.1.8.2 Products/Services offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches & upgrades

- 17.1.8.3.2 Deals

- 17.1.9 VERADIGM LLC

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product/Service launches

- 17.1.9.3.2 Deals

- 17.1.10 NTT DATA GROUP CORPORATION

- 17.1.10.1 Business overview

- 17.1.10.2 Products/Services offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Deals

- 17.1.11 SECTRA AB

- 17.1.11.1 Business overview

- 17.1.11.2 Products/Services offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 GE HEALTHCARE

- 17.1.12.1 Business overview

- 17.1.12.2 Products/Services offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Deals

- 17.1.13 DXC TECHNOLOGY COMPANY

- 17.1.13.1 Business overview

- 17.1.13.2 Products/Services offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Deals

- 17.1.14 SALESFORCE, INC.

- 17.1.14.1 Business overview

- 17.1.14.2 Products/Services offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product/Service launches

- 17.1.14.3.2 Deals

- 17.1.15 FUJIFILM HOLDINGS CORPORATION

- 17.1.15.1 Business overview

- 17.1.15.2 Products/Services offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product/Service launches

- 17.1.15.3.2 Deals

- 17.1.16 DELL INC.

- 17.1.16.1 Business overview

- 17.1.16.2 Products/Services offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Deals

- 17.1.17 ORACLE

- 17.1.17.1 Business overview

- 17.1.17.2 Products/Services offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Product/Service enhancements

- 17.1.17.3.2 Deals

- 17.1.18 ENSOFTEK, INC.

- 17.1.18.1 Business overview

- 17.1.18.2 Products/Services offered

- 17.1.18.3 Recent developments

- 17.1.18.3.1 Product/Service enhancements

- 17.1.18.3.2 Deals

- 17.1.1 AMAZON WEB SERVICES, INC.

- 17.2 STARTUP/SME PLAYERS

- 17.2.1 IRON MOUNTAIN, INC.

- 17.2.2 CLEARDATA

- 17.2.3 VMWARE, INC. (BROADCOM)

- 17.2.4 INFINITT HEALTHCARE CO., LTD.

- 17.2.5 HYLAND SOFTWARE, INC.

- 17.2.6 VEPRO AG

- 17.2.7 NXGN MANAGEMENT, LLC. (THOMA BRAVO COMPANY): COMPANY OVERVIEW

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Insights from primary experts

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 18.4 MARKET SHARE ESTIMATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 LIMITATIONS

- 18.6.1 METHODOLOGY-RELATED LIMITATIONS

- 18.6.2 SCOPE-RELATED LIMITATIONS

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS