|

시장보고서

상품코드

2066381

의료 클라우드 컴퓨팅 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Healthcare Cloud Computing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

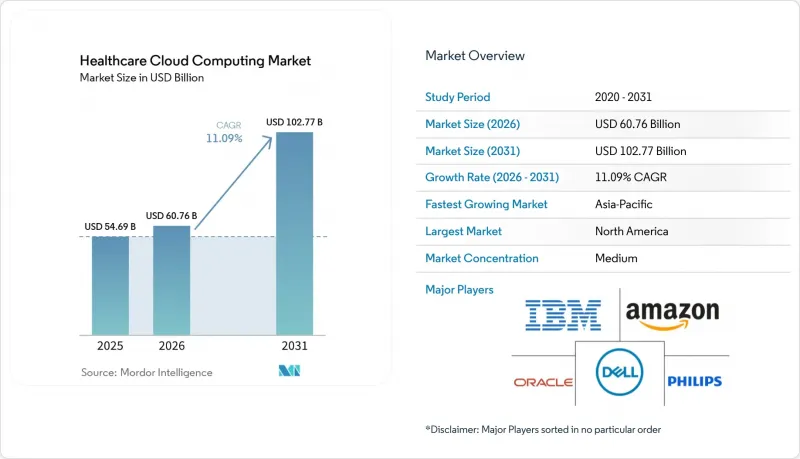

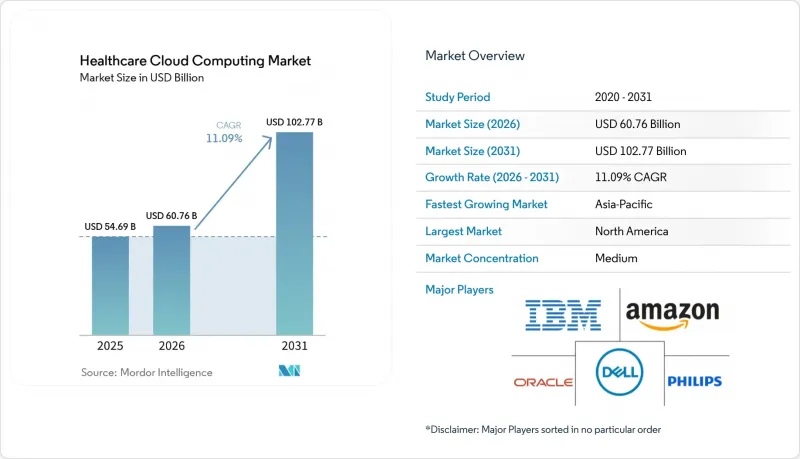

Mordor Intelligence에 의하면, 의료 클라우드 컴퓨팅 시장 규모는 2025년 546억 9,000만 달러, 2026년 607억 6,000만 달러에서 2031년까지 1,027억 7,000만 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 11.09%를 나타낼 전망입니다.

본 보고서는 용도(임상 정보 시스템, 비임상 정보 시스템), 배포 방식(프라이빗 클라우드, 퍼블릭 클라우드, 하이브리드 클라우드), 서비스(SaaS(Software-As-A-Service) 등), 최종 사용자(의료 제공업체, 의료 보험자), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 의료 클라우드 컴퓨팅 시장 동향과 인사이트

의료 현장에서의 IT 도입 확대

병원, 진료소, 진단 네트워크에서는 디지털 전환을 단순한 위기 대응 수단이 아닌 핵심적인 전략적 수단으로 인식하고 있습니다. 최신 클라우드 플랫폼은 노후화된 On-Premise 데이터센터를 대체하며, 소규모 의료 기관의 IT 팀으로는 대응하기 어려웠던 내장형 중복성, 즉시 프로비저닝, 자동 패치 적용 기능을 제공합니다. 팬데믹 기간 동안 이루어진 원격의료에 대한 투자는 클라우드에서 작동하는 확장 가능한 비디오, 스토리지, AI 트리아지에 기반을 둔 본격적인 가상 의료 생태계로 발전했습니다. 의료 시스템에서는 실시간 대시보드, IoMT(의료 사물인터넷) 기기의 피드, 그리고 병상에서 패혈증이나 상태 악화를 경고하는 예측 모델을 중심으로 임상 워크플로우의 재구성이 진행되고 있습니다. 소규모 지방 병원에서는 멀티테넌트형 SaaS 전자건강기록(EHR)을 활용하여, 과거에는 대학병원 수준의 예산이 필요했던 의사결정 지원 도구를 이용할 수 있게 되었습니다. 통합 의료 네트워크에서는 시설 간 상담 시 임상의가 통일된 경과 기록을 확인할 수 있도록 공통 데이터 패브릭 구축이 진행되고 있으며, 이를 통해 의료 업계의 클라우드 컴퓨팅 기반이 강화되고 있습니다.

클라우드 비용 절감과 확장성의 이점

자본 집약적인 하드웨어 교체 주기를 없애고 종량제 컴퓨팅으로 전환함으로써, 미국 병원들이 이익률 감소에 직면해 있는 시기에도 예산에 가해지는 부담을 줄일 수 있습니다. 주요 하이퍼스케일 제공업체들은 2024년에 아웃바운드 요금을 폐지함으로써 멀티클라우드에서 전환하는 데 따르는 장벽을 낮추는 동시에 CIO의 협상력을 강화했습니다. 탄력적인 인프라를 통해 대규모 백신 접종 캠페인이나 보험 청구 제출이 정점에 달했을 때 발생하는 트래픽 급증을, 과도한 리소스 할당 없이도 원활하게 처리할 수 있습니다. 패치 적용, 백업, 고가용성 아키텍처의 외주화를 통해 사내 직원들은 부가가치가 더 높은 데이터 사이언스 업무에 전념할 수 있게 됩니다. 클라우드 네이티브 규칙 엔진이 1분당 수만 건의 청구를 처리함으로써, 보험 지급 기관은 심사 처리 시간을 단축하고 가입자에 대한 환급을 신속하게 처리할 수 있습니다. 클라우드를 통한 비용 절감은 에너지 소비 감소와 데이터센터 부동산 매각에서도 나타나고 있으며, 이는 의료 서비스 제공업체의 지속가능성 목표와 부합하여 의료 클라우드 컴퓨팅 시장의 성장을 가속화할 것입니다.

데이터 보안 및 무결성에 대한 우려

병원을 대상으로 한 사이버 공격이 급증하고 있으며, 랜섬웨어 공격 그룹들은 설정 오류가 있는 오브젝트 스토리지나 패치가 적용되지 않은 API를 표적으로 삼고 있습니다. 정보 유출이 발생하면 HIPAA에 따른 과징금, 집단 소송, 이사회 차원의 철저한 조사가 뒤따르기 때문에 클라우드 전환 승인을 앞두고 보안 감사가 실시되고 있습니다. CIO는 ‘책임 분담 모델’로 인해 어려움을 겪고 있으며, 신원 관리, 로그 기록, 암호화 강화에 있어 자신의 역할을 과소평가하는 경우도 있습니다. 대규모 정보 유출 사고가 발생하면 보험료가 급등하고, 개혁 예산에 숨겨진 비용이 추가로 발생합니다. 규제 당국은 감사 기록 및 사고 보고 기한을 엄격히 적용함으로써 이에 대응하고 있으며, 전담 사이버 보안 인력이 부족한 소규모 지역 의료 기관의 경우 규정 준수에 따른 부담이 커지고 있습니다.

부문별 분석

임상 정보 시스템은 2025년 총 지출의 거의 절반을 차지하고 있으며, 이는 EHR, PACS 및 방사선과 워크플로가 환자 안전에 있어 매우 중요하다는 점을 반영하고 있습니다. 임상 업무 부하를 위한 의료 클라우드 컴퓨팅 시장 규모는 인증된 EHR 기술의 도입을 의무화하고 품질 보고 기준을 설정한 연방 정부의 경기 부양책의 혜택을 받았습니다. 클라우드에서 호스팅되는 EHR은 즉각적인 업그레이드와 통합된 임상 의사결정 플러그인을 제공함으로써 의사의 만족도 점수를 높이고 있습니다. 영상진단 부문에서는 CT 및 MR 검사 데이터를 클라우드 AI 서비스로 전송하여 중요한 소견에 표시를 붙임으로써, 결과 보고까지 걸리는 시간을 단축하고 있습니다.

재무 부서가 청구 기각률을 낮추기 위한 클라우드 기반 수익 주기 분석을 요구함에 따라, 비임상 분야에서의 적용 범위도 확대되고 있습니다. 의료 시스템에서는 SaaS형 청구 플랫폼을 도입하고, 가입 접수 기간 중에 시스템을 확장함으로써 가입자 수 증가에 맞추어 청구 심사가 원활하게 진행될 수 있도록 하고 있습니다. 인사팀은 클라우드 기반 일정 관리 및 급여 계산 엔진을 활용하여, 지오펜스를 통한 규정 준수를 바탕으로 출장 간호사 및 원격지의 코더를 관리하고 있습니다. 의료 클라우드 컴퓨팅 시장 예측형 공급망 대시보드는 의약품 부족을 예측하고, 적시 재고 관리를 최적화함으로써 임상 프로그램에 투입할 자금을 확보하고 있습니다.

많은 서비스 제공업체들이 PHI를 많이 사용하는 워크로드를 하드웨어 수준에서 분리된 싱글 테넌트 환경에 배치하고 있기 때문에 프라이빗 클라우드가 과반수의 점유율을 유지하고 있습니다. 유전체 연구 클러스터나 집중 치료 원격 모니터링 시스템을 운영하는 기관들은 데이터 주권에 관한 규정을 준수하기 위해 전용 인프라를 선택하고 있습니다. 사용자 정의가 가능한 방화벽과 On-Premise 보조 노드를 통해 CISO는 세밀한 정책을 적용할 수 있습니다.

퍼블릭 클라우드는 서비스 제공업체들이 하이퍼스케일러가 제공하는 HITRUST, GDPR(EU 개인정보보호규정), HDS 인증을 신뢰하게 되면 가장 빠르게 보급될 것입니다. 아웃바운드 통신 요금 폐지 및 기밀 계산용 칩셋의 등장으로 인해 벤더 종속성에 대한 우려도 완화될 것입니다. 많은 통합 의료 네트워크(IDN)는 하이브리드형 모델을 채택하고 있습니다. 구체적으로 말하면, 수술 영상과 텔레메트리 데이터는 저지연을 실현하기 위해 로컬 프라이빗 클라우드로 스트리밍되는 반면, 익명화된 조사 데이터 세트는 AI 모델 훈련을 위해 퍼블릭 클라우드로 복제됩니다. 이러한 균형 잡힌 접근 방식을 통해 중요한 워크로드를 가까이 두면서도, 부차적인 분석에는 하이퍼스케일의 비용 효율성을 활용함으로써 의료 업계의 클라우드 컴퓨팅을 강화하고 있습니다.

지역별 분석

북미 시장 점유율 48.30%는 수년에 걸친 전자건강기록(EHR) 의무화와 의료 분야에 특화된 규정 준수 툴킷을 갖춘 주요 하이퍼스케일러 기업들이 모두 진출해 있음을 반영하고 있습니다. 미국의 의료 시스템에서는 재해 복구 업무를 클라우드로 이전하는 움직임이 가속화되고 있어, On-Premise 공간을 수익을 창출하는 임상 부서에 할당할 수 있게 되었습니다. 캐나다의 각 주에서는 광활한 지역에 걸친 원격 방사선 진단을 지원하기 위해, 독자적인 하이퍼스케일러의 리전에 통합된 영상 아카이브를 구축하고 있습니다.

유럽에서는 ‘유럽 건강 데이터 공간 규정(European Health Data Space Regulation)’이 상호 운용 가능한 표준 규격과 환자의 접근권을 규정하고 있어, 이것이 긍정적인 요인으로 작용하고 있습니다. 이에 따라 클라우드 제공업체는 C5 및 GDPR(EU 개인정보보호규정) 기준을 준수하는 EU 내 가용성 구역을 추가로 개설했으며, 이를 통해 병원은 거주지 관련 법률을 위반하지 않으면서도 분산된 데이터를 통합할 수 있게 되었습니다. 독일의 민관 컨소시엄은 프라이빗 클라우드에서 호스팅되며 각 주(Lander) 간에 연계되는 FHIR 기반의 암 등록 시스템 시범 운영을 진행 중이며, 이를 통해 조사 데이터의 심도 있는 분석을 강화하고 있습니다. 스칸디나비아 국가들의 시스템에서는 재생에너지 비중이 높은 전력망을 활용하여, 각국의 기후 목표에 부합하는 탄소 중립형 클라우드 데이터센터를 운영하고 있습니다.

아시아태평양에서는 의료비 증가와 스마트폰 보급률 상승에 힘입어 18.88%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 인도의 국가 ABDM 디지털 헬스 스택은 국내 클라우드 익스체인지(Cloud Exchange)를 활용하고 있으며, 이를 통해 소규모 진료소에서도 상호 운용이 가능한 전자 건강 기록을 발급할 수 있게 되었습니다. 동남아시아에서는 민간 병원 체인이 퍼블릭 클라우드 기반 원격 진료 엔진을 활용한 ‘버추얼 퍼스트’형 보험 상품을 선보이고 있습니다. 호주의 ‘My Health Record’는 클라우드 기반 FHIR 서비스를 통해 검사 결과와 영상 진단 결과를 통합함으로써, 데이터의 무결성과 환자의 참여도를 높이고 있습니다. 다만, 인도네시아 농촌 지역의 대역폭 제약과 중국의 데이터 현지화 규제로 인해 지역별로 고유한 도입 토폴로지가 형성되고 있어, 지역 간 격차는 여전히 남아 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the healthcare cloud computing market size is projected to expand from USD 54.69 billion in 2025 and USD 60.76 billion in 2026 to USD 102.77 billion by 2031, registering a CAGR of 11.09% between 2026 to 2031.

This report is Segmented by Application (Clinical Information Systems, Non-Clinical Information Systems), Deployment (Private Cloud, Public Cloud, and Hybrid Cloud), Service (Software-As-A-Service (SaaS), and More), End User (Healthcare Providers and Healthcare Payers), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Cloud Computing Market Trends and Insights

Increased Adoption of IT Across Healthcare Settings

Hospitals, clinics, and diagnostic networks now treat digital transformation as a core strategic lever rather than a crisis response. Modern cloud platforms replace aging on-premise data centers, bringing built-in redundancy, instant provisioning, and automated patching that small provider IT teams could rarely support. Pandemic-era investments in telehealth evolved into full-scale virtual-care ecosystems that depend on scalable video, storage, and AI triage running in the cloud. Health systems restructure clinical workflows around real-time dashboards, IoMT device feeds, and predictive models that surface sepsis or deterioration alerts at the bedside. Smaller rural hospitals use multitenant SaaS EHRs to access decision-support tools that once required academic-center budgets. Integrated delivery networks pursue common data fabrics so that clinicians see unified longitudinal records during cross-facility consults, strengthening the cloud computing in healthcare industry.

Cost-Saving and Scalability Advantages of Cloud

Removing capital-intensive hardware refresh cycles and shifting to pay-as-you-go compute reduces budget pressure in a period of margin contraction for US hospitals. The major hyperscale providers canceled egress fees in 2024, lowering multicloud exit barriers and giving CIOs stronger negotiating leverage. Elastic infrastructure absorbs traffic spikes during mass vaccination drives or claims-submission peaks without overprovisioning. Outsourced patching, backup, and high-availability architecture free internal staff for higher-value data-science work. Payers cut adjudication turnaround when cloud-native rules engines process tens of thousands of claims per minute, leading to faster member reimbursements. Cloud cost savings also manifest in energy reduction and data-center real-estate divestments, which align with provider sustainability objectives and accelerate the healthcare cloud computing market.

Data-Security and Integrity Concerns

Cyberattacks against hospitals surged, with ransomware crews targeting misconfigured object storage and unpatched APIs. Breaches trigger HIPAA fines, class-action lawsuits, and board-level scrutiny, prompting security audits before cloud migration approvals. CIOs wrestle with the shared-responsibility model and sometimes underestimate their role in hardening identity management, logging, and encryption. Insurance premiums spike after large breaches, adding hidden costs to transformation budgets. Regulators respond with tighter audit trails and incident-reporting timelines, increasing compliance overhead for smaller community providers that lack dedicated cybersecurity talent.

Other drivers and restraints analyzed in the detailed report include:

- Easier Access to Advanced Analytics and ML Tools

- FHIR-Based API Push Enabling Cloud-Native Interoperability

- Lack of Interoperability and Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Information Systems represented nearly half of total 2025 spending, reflecting the centrality of EHR, PACS, and radiology workflows to patient safety. The Healthcare Cloud Computing market size for clinical workloads benefited from federal stimulus that required certified EHR technology and set quality-reporting thresholds. Cloud-hosted EHRs provide instant upgrades and integrated clinical-decision plugins, improving physician satisfaction scores. Imaging departments route CT and MR studies to cloud AI services that flag critical findings, cutting turnaround times.

Non-clinical applications expand as finance departments seek cloud-based revenue-cycle analytics that cut denial rates. Health systems deploy SaaS billing platforms that scale during open enrollment, ensuring claims adjudication keeps pace with member growth. HR teams use cloud scheduling and payroll engines to manage traveling nurses and remote coders with geofenced compliance. Predictive supply-chain dashboards in the Healthcare Cloud Computing market forecast drug shortages and optimize just-in-time inventory, freeing cash for clinical programs.

Private Cloud maintains majority share because many providers place PHI-heavy workloads in single-tenant environments with hardware-level isolation. Institutions running genomic research clusters or intensive care telemetry choose dedicated infrastructure to meet sovereign-data rules. Customizable firewalls and on-premise adjunct nodes let CISOs enforce granular policies.

Public Cloud accelerates fastest after providers grow confident in HITRUST, GDPR, and HDS certifications offered by hyperscalers. The removal of egress fees and arrival of confidential-computing chipsets ease vendor-lock concerns. Many IDNs adopt a hybrid pattern: surgical video and telemetry stream into local private clouds for low latency, while anonymized research datasets replicate to public clouds for AI model training. This balanced approach keeps critical workloads close while exploiting hyperscale economics for secondary analytics, strengthening the cloud computing in healthcare industry.

Geography Analysis

North America's 48.30% share reflects long-standing EHR mandates and the presence of all top hyperscalers with healthcare-focused compliance toolkits. US health systems increasingly shift disaster-recovery to the cloud, freeing on-premise floor space for revenue-generating clinical units. Canadian provinces deploy centralized imaging archives on sovereign hyperscale regions to support teleradiology across vast distances.

Europe benefits from the European Health Data Space Regulation, which prescribes interoperable standards and patient access rights. Cloud providers respond by opening additional EU-based availability zones certified to C5 and GDPR codes, allowing hospitals to consolidate silos without breaching residency laws. German public-private consortiums pilot FHIR-based cancer registries hosted in private clouds that federate across Lander, improving research data depth. Scandinavian systems leverage high renewable-energy grids to power carbon-neutral cloud data centers that align with national climate targets.

Asia-Pacific registers the fastest 18.88% CAGR due to rising healthcare spend and smartphone penetration. India's national ABDM digital-health stack rides on domestic cloud exchanges that enable small clinics to issue interoperable electronic health records. In Southeast Asia, private hospital chains launch virtual-first insurance plans that rely on public cloud tele-consult engines. Australia's My Health Record integrates lab and imaging results via cloud FHIR services, raising data completeness and patient engagement. Regional unevenness persists though, as bandwidth constraints in rural Indonesia and data-localization rules in China shape bespoke deployment topologies.

- Amazon Web Services (AWS)

- Microsoft

- IBM

- Google Cloud

- Oracle

- Dell Technologies

- Siemens Healthineers

- Koninklijke Philips

- ClearDATA

- athenahealth

- CareCloud

- ZYMR

- OSP Labs

- Euris

- Google Cloud (Alphabet)

- Salesforce

- SAP

- Cisco Systems

- Medidata Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Adoption Of IT Across Healthcare Settings

- 4.2.2 Cost-Saving & Scalability Advantages Of Cloud

- 4.2.3 Easier Access To Advanced Analytics & ML Tools

- 4.2.4 FHIR-Based API Push Enabling Cloud-Native Interoperability

- 4.2.5 Real-Time Clinical-Genomics Analytics Workloads

- 4.3 Market Restraints

- 4.3.1 Data-Security & Integrity Concerns

- 4.3.2 Lack Of Interoperability & Standards

- 4.3.3 High Egress Fees & Vendor Lock-In Risks

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Clinical Information Systems (CIS)

- 5.1.1.1 Electronic Health Record (EHR)

- 5.1.1.2 Picture Archiving & Communication System (PACS)

- 5.1.1.3 Radiology Information System (RIS)

- 5.1.1.4 Computerized Physician Order Entry (CPOE)

- 5.1.1.5 Other CIS Applications

- 5.1.2 Non-clinical Information Systems (NCIS)

- 5.1.2.1 Revenue Cycle Management (RCM)

- 5.1.2.2 Automatic Patient Billing (APB)

- 5.1.2.3 Payroll Management System

- 5.1.2.4 Other NCIS

- 5.1.1 Clinical Information Systems (CIS)

- 5.2 By Deployment

- 5.2.1 Private Cloud

- 5.2.2 Public Cloud

- 5.2.3 Hybrid Cloud

- 5.3 By Service

- 5.3.1 Software-as-a-Service (SaaS)

- 5.3.2 Infrastructure-as-a-Service (IaaS)

- 5.3.3 Platform-as-a-Service (PaaS)

- 5.4 By End User

- 5.4.1 Healthcare Providers

- 5.4.2 Healthcare Payers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amazon Web Services (AWS)

- 6.3.2 Microsoft

- 6.3.3 IBM Corporation

- 6.3.4 Google Cloud

- 6.3.5 Oracle

- 6.3.6 Dell Technologies

- 6.3.7 Siemens Healthineers

- 6.3.8 Koninklijke Philips N.V.

- 6.3.9 ClearDATA

- 6.3.10 athenahealth

- 6.3.11 CareCloud

- 6.3.12 ZYMR

- 6.3.13 OSP Labs

- 6.3.14 Euris

- 6.3.15 Google Cloud (Alphabet)

- 6.3.16 Salesforce

- 6.3.17 SAP SE

- 6.3.18 Cisco Systems

- 6.3.19 Medidata Solutions

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment