|

시장보고서

상품코드

2043695

암 바이오마커 시장 예측(-2032년) : 프로파일링 기술(오믹스, 이미징), 암 유형(폐암, 유방암, 백혈병, 흑색종), 제품(기기, 소모품), 용도(진단, 연구개발), 최종사용자(진단 실험실), 지역별Cancer Biomarkers Market by Profiling Technology (Omics, Imaging), Cancer (Lung, Breast, Leukemia, Melanoma), Product (Instruments, Consumables), Application (Diagnostics, R&D), End User (Diagnostic Laboratories), And Region - Global Forecast to 2032 |

||||||

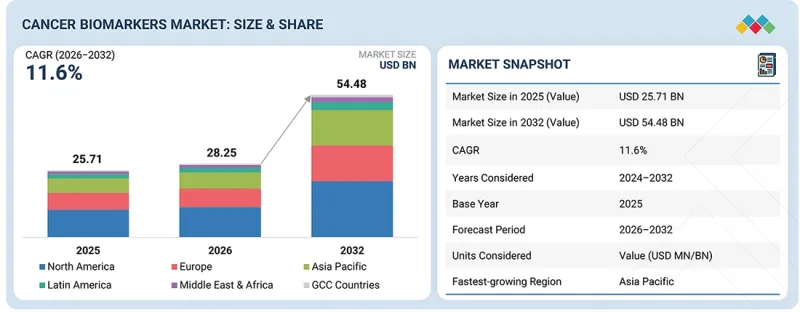

암 바이오마커 시장 규모는 2026년에 약 282억 5,000만 달러로 평가되어 11.6%의 성장률로 추이하며, 2032년에는 544억 8,000만 달러에 달할 것으로 예측됩니다.

이 시장은 꾸준히 성장하고 있으며, 병원과 진단 연구소는 환자의 치료 결과를 개선하기 위해 질병의 조기 발견과 정확한 진단에 초점을 맞추고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(달러) |

| 부문 | 프로파일링 기술, 암 유형, 제품, 용도, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카, GCC 국가 |

급속한 기술 발전과 전 세계 암 발병률 증가 등의 요인이 이 시장의 성장을 촉진하고 있습니다. 그러나 한편으로는 암 바이오마커 검증의 어려움과 전문 인력 부족이 성장의 걸림돌로 작용하고 있습니다.

"오믹스 기술 부문이 예측 기간 중 가장 높은 CAGR을 보일 것으로 예상"

프로파일링 기술별로는 오믹스 기술이 2025년 가장 높은 CAGR을 기록했습니다. 이는 신약개발 및 신약개발에 있으며, 단백질체학 및 유전체학의 활용 확대와 암 진단 기술의 향상에 기인합니다.

"암종별로 보면 유방암 부문이 예측 기간 중 가장 높은 성장률을 보였습니다. "

2025년 암 바이오마커 시장에서는 유방암 카테고리가 가장 높은 성장률을 보였습니다. 기술 발전, 전 세계 암 유병률 증가, 암 바이오마커 개발은 이 부문의 성장을 이끄는 두 가지 중요한 요인입니다.

"최종사용자별로는 진단 연구소 부문이 가장 큰 점유율을 차지"

진단 실험실 부문은 2025년에 더 큰 점유율을 차지했습니다. 전 세계에서 암 바이오마커를 기반으로 한 진단 검사를 수행하는 임상 검사 기관의 수가 증가하고, 악성 종양의 유병률이 증가함에 따라 이 최종사용자 부문의 큰 점유율을 차지할 수 있는 요인이 되었습니다.

"지역별로는 아시아태평양이 가장 높은 성장률을 기록할 것으로 전망"

이 지역은 의료 인프라 확충, 의료비 증가, 병원 및 진단 시설의 현대화 등 몇 가지 주요 요인으로 인해 빠르게 성장하고 있습니다. 또한 암 환자 수의 증가와 암 바이오마커 개발의 기술 발전이 아시아태평양의 암 바이오마커 시장 성장을 촉진하고 있습니다.

세계의 암 바이오마커(Cancer Biomarker) 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 고객 상황과 구매 행동

제8장 암 바이오마커 시장 : 기술별

제9장 암 바이오마커 시장 : 암 유형별

제10장 암 바이오마커 시장 : 제품별

제11장 암 바이오마커 시장 : 용도별

제12장 암 바이오마커 시장 : 최종사용자별

제13장 암 바이오마커 시장 : 지역별

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSA 26.06.05The market for cancer biomarkers is valued at around USD 28.25 billion in 2026 and is forecast to reach USD 54.48 billion by 2032, representing a growth of 11.6%. The market is growing steadily, and hospitals and diagnostic laboratories are focusing on the early detection and accurate diagnosis of diseases to improve patient outcomes.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD billion) |

| Segments | Profiling Technology, Cancer Type, Product, Application, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa, and GCC Countries |

Factors such as rapid technological advances and the global rise in cancer incidence propel market expansion in the development of cancer biomarkers. However, the main obstacles to this market's expansion are the difficulties in validating cancer biomarkers and the lack of qualified workers.

"The omics technology segment is predicted to showcase the highest CAGR during the forecast period."

The market for cancer biomarkers has been divided into two segments based on profiling methods: omics technologies and imaging technologies. Omics technology had the highest compound annual growth rate (CAGR) in 2025. This is explained by the growing use of proteomics and genomics in drug discovery and development, as well as by improved cancer diagnostics.

"The breast cancer segment accounted for the highest growth rate in the cancer biomarkers market, by cancer type, during the forecast period."

The market for cancer biomarkers is divided into categories according to the type of cancer, including non-Hodgkin's lymphoma, kidney cancer, bladder cancer, thyroid cancer, colorectal cancer, prostate cancer, melanoma, leukemia, and other cancer types. In the market for cancer biomarkers in 2025, the breast cancer category had the fastest growth rate. Advances in technology, the rising global prevalence of cancer, and the development of cancer biomarkers are two important factors driving this segment's growth.

"The diagnostic laboratories segment accounted for the highest share."

Based on end user, the cancer biomarkers market is segmented into diagnostic laboratories, biopharmaceutical companies & CROs, research and academic institutes, and other end-users. In 2025, the diagnostic laboratories segment accounted for a larger share of the cancer biomarkers market. The growing number of clinical laboratories worldwide performing cancer biomarker-based diagnostic tests and the rising prevalence of malignancies are responsible for this end-user segment's sizable share.

"Asia Pacific is expected to register the fastest growth rate in the cancer biomarkers market, by region."

The region is witnessing a growth spurt due to several key factors, including expanded healthcare infrastructure, increased healthcare expenditure, and greater modernization of hospital and diagnostic facilities. In addition, rising cancer cases and technological advancements in cancer biomarker development are driving growth in the cancer biomarker market in the Asia Pacific region.

The break-up of profiles of primary participants in the cancer biomarkers market:

- By Company Type: Tier 1 - 26%, Tier 2 - 44%, and Tier - 30%

- By Designation: C-level - 30%, D-level - 34%, and Others - 36%

- By Region: North America - 51%, Europe - 21%, Asia Pacific - 18%, Latin America -5 %, Middle East & Africa- 4%, GCC Countries- 1%

The key players in the cancer biomarkers market are Roche (Switzerland), Thermo Fisher (US), Illumina (US), Agilent Technologies (US), QIAGEN (Netherlands), Bio-Rad Laboratories, Inc. (US), Abbott Laboratories (US), bioMerieux SA (US), Becton, Dickinson and Company (US), and Merck Millipore (US).

Research Coverage:

This research report categorizes the cancer biomarkers market by profiling technology (omics technologies, imaging technologies), cancer type (breast, lung, colorectal, prostate, melanoma, leukemia, thyroid, bladder, non-Hodgkin's lymphoma (NHL), kidney, and other cancers), product type (consumables, instruments, and bioinformatics software), application (diagnostics, research & development, prognostics, risk assessment), end user (diagnostic laboratories, biopharmaceutical companies & CROs, research and academic institutes), and region (North America, Europe, Asia Pacific, Latin America, the Middle East & Africa, and GCC Countries). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, opportunities, and challenges influencing the growth of the cancer biomarkers market. A detailed analysis of the key industry players has been conducted to provide insights into their business overviews, solutions, key strategies such as partnerships, collaborations, expansions, agreements, new product launches, and recent developments in the cancer biomarkers market. This report covers a competitive analysis of upcoming startups in the cancer biomarker market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall cancer biomarkers market and the subsegments. It will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (Technological advancements in cancer biomarkers, increasing incidence of cancer, growing adoption of cancer biomarkers in drug discovery and development, increasing investments in research and development for biomarker innovation, growing adoption of non-invasive diagnostics (liquid biopsy), supportive government initiatives and cancer awareness programs), restraints (High capital requirements and long development timelines for biomarker commercialization, unfavorable regulatory frameworks and reimbursement limitations, high cost of biomarker-based diagnostic tests), opportunities (Expanding role of personalized and precision medicine, increasing applications of companion diagnostics in oncology, growth potential in emerging economies, integration of AI and multi-omics approaches in biomarker discovery and analysis), and challenges (Technical challenges related to sample collection, handling, and storage, complexities associated with biomarker validation and standardization, shortage of skilled professionals and technical expertise) influencing the growth of the cancer biomarkers market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and product launches in the cancer biomarkers market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the cancer biomarker market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the cancer biomarkers market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players like Roche (Switzerland), Thermo Fisher (US), Illumina (US), Agilent Technologies (US), and QIAGEN (Netherlands)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 CANCER BIOMARKERS MARKET OVERVIEW

- 3.2 CANCER BIOMARKERS MARKET, BY PROFILING TECHNOLOGY

- 3.3 CANCER BIOMARKERS MARKET, BY CANCER TYPE

- 3.4 CANCER BIOMARKERS MARKET, BY PRODUCT

- 3.5 CANCER BIOMARKERS MARKET, BY APPLICATION

- 3.6 CANCER BIOMARKERS MARKET, BY END USER

- 3.7 CANCER BIOMARKERS MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Technological Advancements in Cancer Biomarkers

- 4.2.1.2 Increasing incidence of cancer

- 4.2.1.3 Growing adoption of cancer biomarkers in drug discovery and development

- 4.2.1.4 Increasing investments in research and development for biomarker innovation

- 4.2.1.5 Growing Adoption of Non-Invasive Diagnostics (Liquid Biopsy)

- 4.2.1.6 Supportive Government Initiatives and Cancer Awareness Programs

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital requirements and long development timelines for biomarker commercialization

- 4.2.2.2 Unfavorable regulatory frameworks and reimbursement limitations

- 4.2.2.3 High Cost of Biomarker-Based Diagnostic Tests

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding role of personalized and precision medicine

- 4.2.3.2 Increasing applications of companion diagnostics in oncology

- 4.2.3.3 Growth potential in emerging economies

- 4.2.3.4 Integration of AI and Multi-Omics Approaches in Biomarker Discovery and Analysis

- 4.2.4 CHALLENGES

- 4.2.4.1 Technical challenges related to sample collection, handling, and storage

- 4.2.4.2 Complexities associated with biomarker validation and standardization

- 4.2.4.3 Shortage of skilled professionals and technical expertise

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CANCER BIOMARKERS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.5.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 SINTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF CANCER BIOMARKERS, BY KEY PLAYER, 2024-2026

- 5.6.2 AVERAGE SELLING PRICE OF CANCER BIOMARKERS PRODUCTS, BY REGION, 2024-2026

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 382200)

- 5.7.2 EXPORT SCENARIO (HS CODE 382200)

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 IMPACT OF 2025 US TARIFF ON CANCER BIOMARKERS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON REGION

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 Diagnostic Laboratories

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 NEXT-GENERATION SEQUENCING

- 6.1.2 POLYMERASE CHAIN REACTION

- 6.1.3 IMMUNOASSAYS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIOINFORMATICS PLATFORMS

- 6.2.2 MASS SPECTROMETRY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 LIQUID BIOPSY TECHNOLOGIES

- 6.3.2 MICROARRAY TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 LIST OF KEY PATENTS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GENERATIVE AI ON CANCER BIOMARKERS MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 TOP USE CASES AND MARKET POTENTIAL

- 6.7.3 KEY COMPANIES IMPLEMENTING AI

- 6.7.4 FUTURE OF AI

7 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 7.1 DECISION-MAKING PROCESS

- 7.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 7.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 7.2.2 BUYING CRITERIA

- 7.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 7.4 UNMET NEEDS IN VARIOUS END-USE INDUSTRIES

- 7.5 MARKET PROFITABILITY

- 7.5.1 REVENUE POTENTIAL

- 7.5.2 COST DYNAMICS

- 7.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

8 CANCER BIOMARKERS MARKET, BY TECHNOLOGY

- 8.1 INTRODUCTION

- 8.2 OMICS TECHNOLOGIES

- 8.2.1 PROTEOMICS

- 8.2.1.1 Immunoassays

- 8.2.1.1.1 Facilitate diagnosis of cancer at early stage

- 8.2.1.2 Mass spectrometry

- 8.2.1.2.1 High specificity of mass spectroscopy to drive adoption

- 8.2.1.3 2D gel electrophoresis

- 8.2.1.3.1 Increasing demand for gel electrophoresis in proteomics research and personalized medicine to drive segment

- 8.2.1.4 Protein microarrays

- 8.2.1.4.1 Increasing demand for gel electrophoresis in proteomics research and personalized medicine to drive growth

- 8.2.1.5 Other proteomic technologies

- 8.2.1.1 Immunoassays

- 8.2.2 GENOMICS

- 8.2.2.1 Next-generation sequencing

- 8.2.2.1.1 Development of advanced NGS platforms by leading players to drive growth

- 8.2.2.2 Polymerase chain reaction

- 8.2.2.2.1 Cost-effectiveness and easy availability of PCR tests to propel market

- 8.2.2.3 In situ hybridization

- 8.2.2.3.1 ISH-based diagnostic tests help identify specific biomarkers in clinical trials

- 8.2.2.1 Next-generation sequencing

- 8.2.3 OTHER OMICS TECHNOLOGIES

- 8.2.1 PROTEOMICS

- 8.3 IMAGING TECHNOLOGIES

- 8.3.1 ULTRASOUND IMAGING

- 8.3.1.1 Use of ultrasound for biomarker research in understanding disease onset & progression to drive growth

- 8.3.2 COMPUTED TOMOGRAPHY

- 8.3.2.1 Technological advancements to drive adoption

- 8.3.3 MAGNETIC RESONANCE IMAGING

- 8.3.3.1 Growing preference for open MRIs to support market growth

- 8.3.4 POSITRON EMISSION TOMOGRAPHY

- 8.3.4.1 Development of lab-on-chip-based multiplex assays to propel market

- 8.3.5 MAMMOGRAPHY

- 8.3.5.1 Advanced technologies like 3D mammography to support market growth

- 8.3.1 ULTRASOUND IMAGING

9 CANCER BIOMARKERS MARKET, BY CANCER TYPE

- 9.1 INTRODUCTION

- 9.2 BREAST CANCER

- 9.2.1 INCREASING PREVALENCE OF BREAST CANCER TO DRIVE MARKET

- 9.3 LUNG CANCER

- 9.3.1 INCREASING FOCUS ON DEVELOPMENT OF LUNG CANCER BIOMARKERS TO SUPPORT MARKET GROWTH

- 9.4 COLORECTAL CANCER

- 9.4.1 RISING DEMAND FOR BIOMARKERS IN EARLY DIAGNOSIS & PROGNOSIS OF COLORECTAL CANCER TO DRIVE MARKET

- 9.5 PROSTATE CANCER

- 9.5.1 ADVANCEMENTS IN GENOMIC TECHNOLOGIES TO PROPEL MARKET

- 9.6 MELANOMA

- 9.6.1 INCREASING UTILIZATION OF DIAGNOSTICS IN BRAF INHIBITOR THERAPY TO DRIVE MARKET

- 9.7 LEUKEMIA

- 9.7.1 INCREASING NUMBER OF RESEARCH STUDIES FOR DEVELOPMENT OF ACCURATE DIAGNOSTIC METHODS FOR LEUKEMIA TO DRIVE MARKET

- 9.8 THYROID CANCER

- 9.8.1 INCREASING RESEARCH FOR IDENTIFICATION OF NEW BIOMARKERS FOR THYROID NODULES TO SUPPORT MARKET GROWTH

- 9.9 BLADDER CANCER

- 9.9.1 INCREASING APPROVALS OF URINARY BIOMARKERS FOR DETECTION OF BLADDER CANCER TO PROPEL MARKET

- 9.10 NON-HODGKIN'S LYMPHOMA

- 9.10.1 INCREASING RESEARCH ACTIVITIES ON NHL TO DRIVE MARKET

- 9.11 KIDNEY CANCER

- 9.11.1 DEVELOPMENT OF NEW TARGETED THERAPIES FOR TREATMENT OF KIDNEY CANCER TO DRIVE MARKET

- 9.12 OTHER CANCERS

10 CANCER BIOMARKERS MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 CONSUMABLES

- 10.2.1 KITS & REAGENTS

- 10.2.1.1 Ease of use to support adoption

- 10.2.2 ANTIBODIES

- 10.2.2.1 Increasing approvals for therapeutic antibodies by regulatory authorities to drive market

- 10.2.3 PROBES

- 10.2.3.1 Need for probes in assay tests for cancer detection to support market growth

- 10.2.1 KITS & REAGENTS

- 10.3 INSTRUMENTS

- 10.3.1 IMAGING INSTRUMENTS

- 10.3.1.1 Technological advancements in imaging instruments to drive growth

- 10.3.2 PATHOLOGY-BASED INSTRUMENTS

- 10.3.2.1 Rising demand for cancer diagnosis to drive market

- 10.3.3 BIOPSY INSTRUMENTS

- 10.3.3.1 Increasing prevalence of cancer to drive growth

- 10.3.1 IMAGING INSTRUMENTS

- 10.4 BIOINFORMATICS SOFTWARE

- 10.4.1 TECHNOLOGICAL ADVANCEMENTS AND GROWING INFORMATION TECHNOLOGY SECTOR TO DRIVE MARKET

11 CANCER BIOMARKERS MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 DIAGNOSTICS

- 11.2.1 INCREASED AWARENESS & ACCEPTANCE OF TECHNOLOGICALLY ADVANCED BIOMARKER PRODUCTS TO PROPEL MARKET

- 11.3 RESEARCH & DEVELOPMENT

- 11.3.1 INCREASING FOCUS OF PHARMACEUTICAL COMPANIES ON USE OF BIOMARKERS IN DRUG DISCOVERY AND DEVELOPMENT TO DRIVE MARKET

- 11.4 PROGNOSTICS

- 11.4.1 GROWING ADOPTION OF SPECIFIC AND SENSITIVE BIOMARKER TESTS TO SUPPORT MARKET GROWTH

- 11.5 RISK ASSESSMENT

- 11.5.1 USED FOR DETECTING MUTATIONS OR VARIANTS IN GERMLINE DNA OF INDIVIDUALS

- 11.6 OTHER APPLICATIONS

12 CANCER BIOMARKERS MARKET, BY END USER

- 12.1 INTRODUCTION

- 12.2 DIAGNOSTIC LABORATORIES

- 12.2.1 INCREASING INCIDENCE OF CANCER TO DRIVE GROWTH

- 12.3 BIOPHARMACEUTICAL COMPANIES AND CROS

- 12.3.1 RISING FOCUS ON DRUG DISCOVERY IN BIOPHARMACEUTICAL AND BIOTECHNOLOGY COMPANIES TO DRIVE MARKET

- 12.4 RESEARCH AND ACADEMIC INSTITUTES

- 12.4.1 INCREASING RESEARCH FUNDING FOR EARLY DIAGNOSIS TO AUGMENT MARKET

- 12.5 OTHER END USERS

13 CANCER BIOMARKERS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 US

- 13.2.1.1 High adoption of precision oncology and biomarker-driven therapies to drive market growth

- 13.2.2 CANADA

- 13.2.2.1 Government Initiatives Driving Biomarker Growth

- 13.2.1 US

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 High Healthcare Spending Driving Biomarker Adoption

- 13.3.2 UK

- 13.3.2.1 Rising Cancer Incidence Driving Biomarker Adoption

- 13.3.3 FRANCE

- 13.3.3.1 Government Funding Supporting Biomarker Market Growth

- 13.3.4 ITALY

- 13.3.4.1 Growing geriatric population to support market growth

- 13.3.5 SPAIN

- 13.3.5.1 Rising emphasis on personalized medicine to drive market growth

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 ASIA PACIFIC

- 13.4.1 CHINA

- 13.4.1.1 Rising cancer burden and strong government support to drive market growth

- 13.4.2 JAPAN

- 13.4.2.1 Strong healthcare investment to drive market growth

- 13.4.3 INDIA

- 13.4.3.1 Rising cancer burden and expanding healthcare investments to drive market growth

- 13.4.4 AUSTRALIA

- 13.4.4.1 Rising cancer burden and strong government investments to drive market growth

- 13.4.5 REST OF ASIA PACIFIC

- 13.4.1 CHINA

- 13.5 LATIN AMERICA

- 13.5.1 BRAZIL

- 13.5.1.1 Rising cancer incidence to drive market growth

- 13.5.2 MEXICO

- 13.5.2.1 Expanding healthcare access and rising cancer burden to drive market growth

- 13.5.3 REST OF LATIN AMERICA

- 13.5.1 BRAZIL

- 13.6 MIDDLE EAST & AFRICA

- 13.6.1 EMERGING PRECISION MEDICINE INITIATIVES TO DRIVE MARKET GROWTH

- 13.7 GCC COUNTRIES

- 13.7.1 EXPANDING HEALTHCARE INFRASTRUCTURE TO DRIVE MARKET GROWTH

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.2.1 OVERVIEW OF STRATEGIES DEPLOYED BY PLAYERS IN CANCER BIOMARKERS MARKET

- 14.3 REVENUE ANALYSIS, 2023-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 GLOBAL MARKET SHARE ANALYSIS, 2025

- 14.4.2 US: MARKET SHARE ANALYSIS, 2025

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.5.5.1 Company footprint

- 14.5.5.2 Regional footprint

- 14.5.5.3 Product footprint

- 14.5.5.4 Profiling Technology footprint

- 14.5.5.5 Application footprint

- 14.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- 14.6.5 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.6.5.1 Detailed list of key startups/SMEs

- 14.6.5.2 Competitive benchmarking of startups/SMEs (1/2)

- 14.6.5.3 Competitive benchmarking of startups/SMEs (2/2)

- 14.7 COMPANY VALUATION & FINANCIAL METRICS

- 14.7.1 FINANCIAL METRICS

- 14.7.2 COMPANY VALUATION

- 14.8 BRAND/PRODUCT COMPARISON

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES & APPROVALS

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 F. HOFFMANN-LA ROCHE AG

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches & approvals

- 15.1.1.3.2 Deals

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 THERMO FISHER SCIENTIFIC

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches & approvals

- 15.1.2.3.2 Deals

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 ILLUMINA, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products & services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Product launches & approvals

- 15.1.3.3.2 Deals

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 AGILENT TECHNOLOGIES, INC.

- 15.1.4.1 Business overview

- 15.1.4.2 Products & services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches & approvals

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 QIAGEN

- 15.1.5.1 Business overview

- 15.1.5.2 Products & services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Product launches & approvals

- 15.1.5.3.2 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 BIO-RAD LABORATORIES, INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products & services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Deals

- 15.1.7 DANAHER CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.8 ABBOTT LABORATORIES

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.9 BIOMERIEUX

- 15.1.9.1 Business overview

- 15.1.9.2 Products & services offered

- 15.1.10 MERCK KGAA

- 15.1.10.1 Business overview

- 15.1.10.2 Products & services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches & approvals

- 15.1.11 SIEMENS HEALTHINEERS AG

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.12 BECTON, DICKINSON AND COMPANY

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.1 F. HOFFMANN-LA ROCHE AG

- 15.2 OTHER PLAYERS

- 15.2.1 MYRIAD GENETICS

- 15.2.2 SYSMEX CORPORATION

- 15.2.3 HOLOGIC, INC.

- 15.2.4 QUEST DIAGNOSTICS

- 15.2.5 CENTOGENE N.V.

- 15.2.6 BIOGENEX

- 15.2.7 R&D SYSTEMS, INC.

- 15.2.8 BIOVISION INC.

- 15.2.9 OLINK

- 15.2.10 ASURAGEN, INC.

- 15.2.11 MESO SCALE DIAGNOSTICS, LLC

- 15.2.12 INVIVOSCRIBE, INC.

- 15.2.13 INOVIQ LTD.

- 15.2.14 NANTOMICS

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 List of primary sources

- 16.1.2.2 Key data from primary sources

- 16.1.2.3 Key industry insights

- 16.1.2.4 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 TOTAL MARKET SIZE: CANCER BIOMARKERS MARKET

- 16.2.2 BOTTOM-UP APPROACH

- 16.2.2.1 Approach 1: Revenue estimation of key players

- 16.2.2.2 Approach 2: Study of annual reports and investor presentations

- 16.2.2.3 Approach 3: Primary interviews

- 16.2.2.4 Growth forecast

- 16.2.2.5 CAGR projections

- 16.2.3 TOP-DOWN APPROACH

- 16.3 DATA TRIANGULATION

- 16.4 RESEARCH ASSUMPTIONS

- 16.4.1 STUDY-RELATED ASSUMPTIONS

- 16.5 STUDY ASSUMPTIONS

- 16.5.1 PARAMETRIC ASSUMPTIONS

- 16.5.2 GROWTH RATE ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

- 16.7 RISK ASSESSMENT

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS