|

시장보고서

상품코드

2055606

암 바이오마커 시장(제3판) : 바이오마커 유형별, 암 유형별, 지역별 - 동향과 예측(-2035년)Cancer Biomarkers Market (3rd Edition) by Type of Biomarker, Type of Cancer and Geographical Regions - Trends and Forecasts Till 2035 |

||||||

암 바이오마커 시장 : 개요

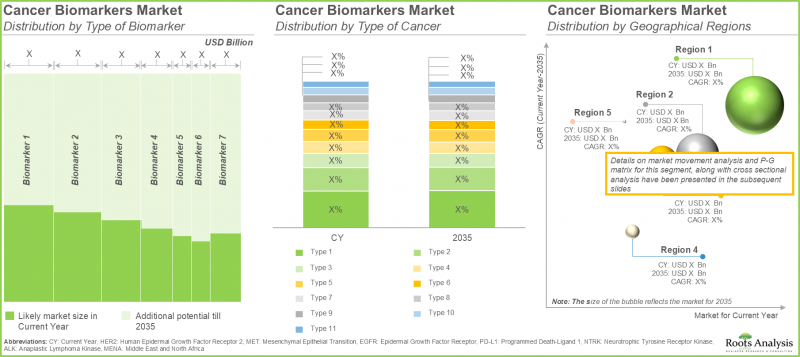

세계의 암 바이오마커 시장 규모는 2035년까지 연평균 복합 성장률(CAGR) 4.3%로 확대되어 현재 259억 달러에서 2035년에는 378억 달러에 이를 것으로 추정되고 있습니다.

암 바이오마커 시장 : 성장 및 동향

지난 20년 동안 연구자들과 바이오의약품 기업들은 표적 치료, 면역 치료, 치료용 암 백신 등 선진적이고 매우 효과적인 암 치료법을 다수 도입해 왔습니다. 이러한 진전에도 불구하고, 종양학 연구는 여전히 전신성 치료 관련 독성, 높은 임상시험 중도 탈락률, 그리고 다양한 약리학적 및 치료법 고유의 제약과 같은 중대한 과제에 직면해 있습니다. 이러한 뿌리 깊은 문제들은 치료 실패로 인한 경제적 영향을 최소화하면서도 환자의 예후를 개선할 수 있는 보다 정확하고 신뢰할 수 있는 진단 체계에 대한 필요성이 커지고 있음을 여실히 보여주고 있습니다.

이러한 중요한 미충족 의료 수요에 대응하기 위해, 의료계에서는 현대 종양학 진단의 기반으로 암 바이오마커의 도입이 점점 더 확대되고 있습니다. 이러한 바이오마커에 대한 수요는 주로 암의 분자적 이질성에 의해 주도되고 있습니다. 같은 암 유형이나 병기로 진단받은 환자라 하더라도 종종 서로 다른 분자 및 유전적 프로파일을 보이며, 그 결과 유전자 재조합 의약품이나 생물학적 제제에 대한 반응에 차이가 발생합니다. 이에 따라 제약 개발자와 의료 제공업체들은 점차 정밀 종양학(Precision Oncology) 접근 방식으로 전환하고 있습니다. 질환 특이적 분자 표지자를 규명함으로써, 임상의들은 이제 기존의 ‘일률적인’ 치료 모델을 넘어 개별 환자에게 맞춘 치료 전략을 수립할 수 있게 되었습니다.

PD-L1, BRAF, EGFR 등과 같은 단일 분석 대상 바이오마커는 종양학 진단에서 여전히 기초적인 역할을 수행하고 있지만, 복잡한 유전체 환경이나 장기적인 치료 효과라는 관점에서는 그 예측 능력이 종종 제한적입니다. 그 결과, 고처리량 기술, 특히 차세대 염기서열 분석(NGS)의 발전으로 인해 종양 돌연변이 부하(TMB) 및 미세위성 불안정성(MSI)을 포함한 보다 종합적인 바이오마커의 개발과 검증이 촉진되었습니다. 이러한 첨단 바이오마커는 유전체 불안정성과 종양 생물학에 대한 더 깊은 이해를 제공하며, 보다 정밀한 환자 분류와 치료법 선택을 가능하게 합니다.

임상적으로 검증된 바이오마커 파이프라인의 확대는 여전히 시장 성장의 주요 원동력으로 작용하고 있습니다. 주요 제약사 및 생명공학 기업들의 멀티오믹스 및 정밀의학 분야에 대한 막대한 투자를 바탕으로, 암 바이오마커 시장은 크게 성장할 것으로 전망되며, 데이터 기반의 통합 진단이 향후 암 치료의 표준을 재정의할 것으로 기대됩니다.

성장 촉진요인 - 시장 확대를 위한 전략적 촉진요인

고령화, 생활 방식의 변화, 환경적 위험 요인에 대한 노출 증가로 인해 전 세계적으로 암 부담이 커짐에 따라, 정밀한 종양 진단 및 표적 치료 접근법에 대한 수요가 지속적으로 증가하고 있습니다. 이러한 질환 유병률 증가에 대응하여, 의료계에서는 치료 방침이 개별 종양의 생물학적 특성이나 분자 프로파일링을 바탕으로 결정되는 ‘정밀 종양학’ 및 ‘맞춤형 의료’로의 대대적인 전환이 진행되고 있습니다. 이러한 전환은 차세대 염기서열 분석(NGS), 액체 생검 플랫폼, 멀티오믹스 기술, 생물정보학 및 인공지능(AI)을 활용한 진단 기술의 급속한 발전에 힘입어 강력하게 추진되고 있으며, 이 모든 요소가 바이오마커의 발견, 검증 및 임상 도입을 효율화하고 있습니다.

이러한 혁신을 통해 임상의들은 환자 고유의 분자적 특징을 파악할 수 있게 되었으며, 이로 인해 치료법 선택이 개선되고 치료에 따른 부작용이 줄어들었으며, 여러 암 적응증에서 생존율이 향상되고 있습니다. 시장 확장을 더욱 촉진하고 있는 요인은 로슈와 노바티스를 비롯한 주요 제약 및 바이오기술 기업들이 표적 면역종양학 치료를 지원하기 위해 바이오마커 중심의 임상시험 및 동반진단제 개발에 적극적으로 투자하고 있다는 점입니다. 이와 더불어 동반진단제의 승인 건수 증가와 면역요법의 적응증 확대가 시장의 상승세를 더욱 강화하고 있으며, 암 바이오마커는 차세대 암 의료의 중요한 구성 요소로서의 입지를 확고히 다져가고 있습니다.

시장의 과제 - 발전을 가로막는 중대한 장벽

암 바이오마커 시장은 강력한 성장 잠재력을 지니고 있지만, 운영, 기술, 규제 측면의 여러 과제가 여전히 광범위한 도입과 상용화를 가로막고 있습니다. 주요 장애물 중 하나는 바이오마커 연구 개발에 수반되는 막대한 비용과 장기화되는 과정입니다. 기업은 임상 도입에 이르기까지 발견, 검증, 규제 당국의 승인 절차에 막대한 자금을 투자해야 합니다. 이러한 재정적·운영상의 부담은 특히 중소 바이오기술 기업들 시장 진입을 제한하는 요인이 되며, 동시에 혁신적인 진단 솔루션의 도입을 지연시키고 있습니다. 또한, 검체 채취, 취급 및 보존과 관련된 기술적 제약도 여전히 심각한 우려 사항입니다. 부적절한 처리는 바이오마커의 열화, 오염, 검사 결과의 불일치를 초래하여, 결국 진단 정확도를 저하시켜 바이오마커 기반 검사에 대한 임상적 신뢰도를 떨어뜨릴 우려가 있습니다.

또한, 많은 신흥 바이오마커는 다양한 환자 집단에서 일관된 임상적 유용성을 아직 입증하지 못했기 때문에 시장은 대규모 임상 검증의 부족과 표준화된 데이터 프레임워크의 부재와 관련된 과제에도 직면해 있습니다. 검사 방법, 보고 기준, 데이터 형식이 검사실마다 다르기 때문에 데이터 통합, 비교 분석 및 종양학 진료에의 일상적인 도입이 더욱 복잡해지고 있습니다. 또한, 미국 식품의약국(FDA)이나 유럽의약품청(EMA) 등의 기관에 의해 감독되는 바이오마커 기반 진단법 및 동반 진단 검사에 관한 지역별 규제 상황은 지속적으로 변화하고 있어, 시장 진출기업들에게 불확실성을 야기하고 있습니다. 이로 인해 규정 준수 요건이 증가하고, 승인까지 걸리는 기간이 길어지며, 전반적인 상업화 비용이 상승하고 있습니다.

암 바이오마커 시장 : 주요 인사이트

본 보고서는 암 바이오마커 시장의 현황을 상세하게 분석하고, 업계 내 잠재적인 성장 기회를 파악하고 있습니다. 보고서의 주요 조사 결과는 다음과 같습니다.

- 생명공학의 발전으로 수많은 암 바이오마커 검사 솔루션이 개발되었으며, 이들은 현재 진단, 임상 연구 및 치료 관련 의사 결정 지원 등 다양한 목적으로 활용되고 있습니다.

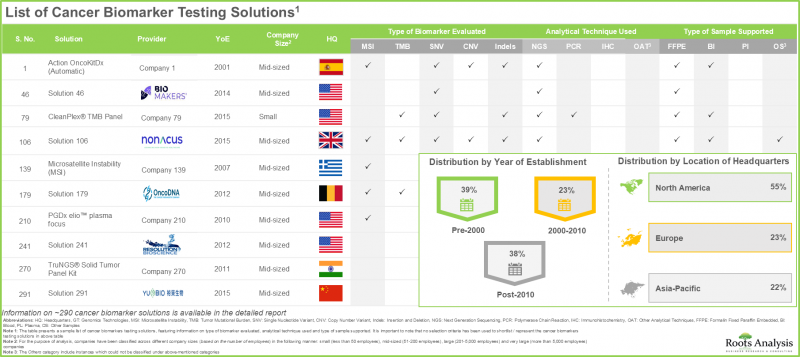

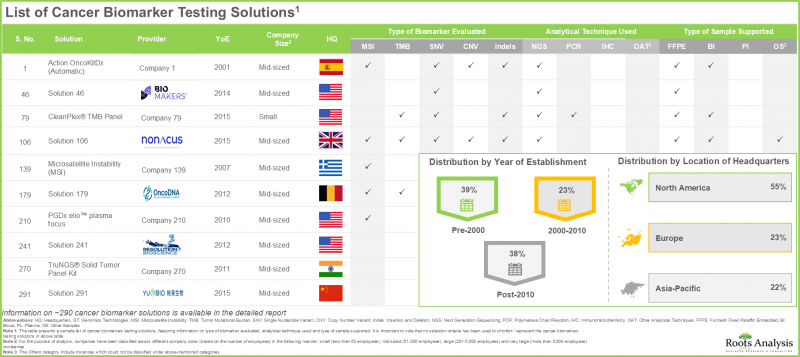

- 현재 시장에는 290개 이상의 바이오마커 솔루션이 존재하며, 그중 약 85%가 암 바이오마커 평가에 차세대 염기서열 분석(NGS)을 활용하고 있습니다.

- 암 바이오마커 검사 솔루션의 대부분(68%)은 인델(indel) 평가를 지원하며, 검사 솔루션의 85%는 암 바이오마커 평가에 차세대 염기서열 분석(NGS)을 활용하고 있습니다.

- 여러 업계 관계자 및 비업계 관계자들이 새로운 표적 치료제를 개발하기 위해 바이오마커별 계층화 임상시험을 실시하고 있으며, 환자의 대부분은 중국 내 여러 의료기관에서 등록되었습니다.

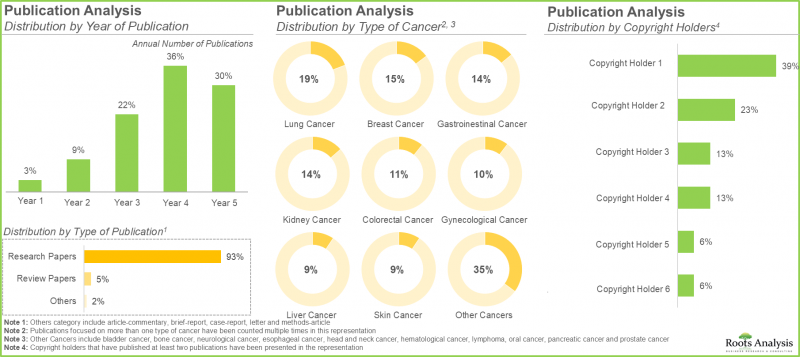

- 암 바이오마커 분야에서는 연구가 크게 증가하고 있으며, 다양한 연구자들이 470편 이상의 논문을 발표하고 있어, 이 분야에 대한 업계 및 학계 관계자들의 관심이 높아지고 있음을 보여주고 있습니다.

- 암 바이오마커 시장은 예측 기간 동안 연평균 4.3%의 성장률을 보일 것으로 예측됩니다. 특히, 유방암용 바이오마커 검사 솔루션이 현재 시장 점유율의 대부분을 차지할 것으로 예측됩니다.

- 미국 내 맞춤형 의료의 확산에 힘입어, 암 바이오마커 시장은 예측 기간 동안 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 전망됩니다.

- 암 발병률 증가와 임상 및 연구 현장에서 정확하고 바이오마커에 기반한 진단에 대한 수요가 높아지고 있는 점을 고려할 때, 암 바이오마커 시장은 꾸준한 성장이 예상됩니다.

암 바이오마커 시장

시장 규모 및 기회 분석은 다음 매개변수를 기준으로 세분화되어 있습니다.

바이오마커 유형별

- HER2

- MET

- EGFR

- PD-L1

- NTRK

- ALK

- 기타 바이오마커

암 유형별

- 유방암

- 대장암

- 폐암

- 전립선암

- 갑상선암

- 방광암

- 악성 흑색종

- 비호지킨 림프종

- 자궁내막암

- 신장암

- 백혈병

지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 북아프리카

암 바이오마커 시장 : 주요 부문

암 바이오마커 시장에서 어떤 유형의 바이오마커 검사가 가장 큰 점유율을 차지하고 있는가?

올해 HER2 바이오마커 검사 솔루션은 암 바이오마커 시장에서 가장 높은 점유율(21.1%)을 차지할 것으로 예측됩니다. 이러한 우위는 주로 유방암 및 위암의 진단, 예후, 치료 관리에 있어 HER2 검사의 광범위한 임상적 검증에 기인합니다. 이 부문의 강력한 시장 입지는 트라스투주맙 및 펠투주맙을 비롯한 여러 고부가가치 표적 치료제와의 직접적인 연관성을 통해 더욱 공고해지고 있으며, 이러한 치료제들은 HER2 기반 동반진단에 대한 전 세계적 수요를 지속적으로 견인하고 있습니다.

반면, EGFR 바이오마커 검사 부문은 예측 기간 동안 비교적 빠른 성장세를 보일 것으로 예측됩니다. 이러한 성장은 주로 전 세계 폐암 유병률 증가와 더불어, 정밀 종양학 및 표적 치료 접근법의 도입 확대에 힘입어 이루어지고 있습니다. 특히 오시멜티닙과 같은 EGFR 억제제의 임상적 활용이 확대됨에 따라, 비소세포폐암(NSCLC) 환자의 계층화 및 치료법 선택을 지원하기 위한 EGFR 변이 검사 수요가 크게 증가하고 있습니다.

지역별 분석 : 암 바이오마커 검사 분야에서 어느 지역이 가장 빠른 성장세를 보이고 있는가?

북미: 세계 시장을 주도

북미는 암 바이오마커 시장을 주도할 것으로 예상되며, 올해 전체 시장 매출의 52.1%를 차지할 전망입니다. 이 지역의 선도적인 위상은 암 발병률 증가, 확립된 의료 인프라, 그리고 맞춤형 의료 및 정밀 종양학의 확산에 기인한 것으로 보입니다. 또한, 바이오마커 연구에 대한 적극적인 투자, 첨단 진단 기술의 광범위한 활용 가능성, 그리고 유리한 규제 환경과 보험 급여 환경이 해당 지역 전체 시장 성장을 지속적으로 뒷받침하고 있습니다.

시장에서 점유율이 가장 높은 암 유형은?

현재 시장 추정 및 전망에 따르면, 유방암 바이오마커 검사는 전체 암 바이오마커 시장 매출에서 가장 큰 비중(25.1%)을 차지할 것으로 예측됩니다. 이는 유방암이 여성 암 관련 사망의 주요 원인 중 하나로 전 세계적으로 높은 발병률을 보이고 있기 때문입니다. 그 결과, 조기 발견, 예후 평가, 위험도 분류 및 맞춤형 치료를 지원하는 바이오마커를 활용한 진단법에 대한 수요가 높아지고 있습니다.

향후 흑색종 바이오마커 검사 부문은 비교적 빠른 속도로 성장할 것으로 예상되며, 예측 기간 동안 연평균 성장률(CAGR)은 4.5%를 나타낼 것으로 전망됩니다. 이러한 성장은 주로 전 세계 흑색종 발병률 증가, 표적 치료법의 지속적인 발전, 그리고 정밀 진단 방식의 확대에 힘입은 것입니다. 특히, BRAF 및 MEK 억제제의 임상 도입과 더불어, BRAF 변이 검사 및 액체 생검에 기반한 바이오마커 검사의 활용 확대가 이 부문의 성장에 크게 기여할 것으로 예측됩니다.

암 바이오마커 시장의 주요 기업 사례

- ARUP Laboratories

- Asper Biogene

- BioReference

- Caris Life Sciences

- CeGaT

- Foundation Medicine

- Genekor Medical

- Guardant Health

- IQVIA Laborateries

- Labcorp

- MedGenome

- NeoGenomics Laboratories

- Nonacus

- OncoDNA

- Quest Diagnostics

- Oxford Gene Technology

- Personal Genome Diagnostics

- PhenoPath

- Positive Biosciences

- Tempus

- Thermo Fisher Scientific

- YuceBio

1차 조사 개요

본 조사에서 제시된 견해와 인사이트은 여러 이해관계자들과의 논의를 바탕으로 합니다. 본 조사 보고서에는 다음 업계 관계자들과의 인터뷰 내용이 상세하게 수록되어 있습니다.

- 미국 중소기업, 최고기술책임자(CTO) 겸 전임 전임상 개발 및 전략적 제휴 담당 이사

- 독일의 중견 기업, 비즈니스 매니저

- 미국 대기업 전 최고과학책임자

암 바이오마커 시장 : 조사 범위

- 시장 규모 및 기회 분석 : 본 보고서에서는 암 바이오마커 시장에 대해(A) 바이오마커 유형,(B) 암 유형,(C) 지역과 같은 주요 시장 부문에 초점을 맞추어 상세하게 분석했습니다.

- 시장 동향 : 신규 암 바이오마커 검사 솔루션에 대해,(A)평가 대상 바이오마커 유형,(B)사용되는 분석 기법 유형,(C) 결과 보고까지 소요되는 시간,(D) 대응 샘플 유형,(E) 검사 대상이 되는 핵산 유형,(F) 암 유형,(G) 적용 분야, 그리고(H) 최종 사용자 등 다양한 매개변수를 고려한 종합적인 평가를 실시했습니다. 또한, 신규 암 바이오마커 검사 솔루션을 제공하는 개발 기업의 상세 목록 외에도(I) 설립 연도,(J) 기업 규모(직원 수 기준),(K) 본사 소재지 등 다양한 매개변수를 기반으로 한 분석도 포함되어 있습니다.

- 제품 경쟁력 분석 : 신규 암 바이오마커 검사 솔루션에 대한 종합적인 경쟁 분석으로, 제품의 범용성 및 경쟁력 등의 요인을 검증하고 있습니다.

- 기업 프로파일: 새로운 암 바이오마커 검사 솔루션을 제공하는 주요 기업의 상세한 프로파일입니다.(A) 기업 개요,(B) 재무 정보,(C) 암 바이오마커 검사 솔루션 포트폴리오,(D) 최근 동향, 그리고(E) 정보에 기반한 미래 전망에 초점을 맞추었습니다.

- 사례 연구: 종양성 질환 치료제 평가를 목적으로 한 바이오마커 기반 임상시험의 수행과 관련된 혁신적인 시험 설계에 대한 일반적인 고찰입니다. 각 시험 설계의 구조에 대한 세부 사항을 포함하고 있으며, 각각의 장점과 과제를 강조하고 있습니다.

- 임상시험 분석 :(A)시험 등록 연도,(B)시험 현황,(C)시험 단계,(D)등록 환자 수,(E)후원사/협력 기관 유형,(F)가장 활발한 기업(등록된 시험 수 기준),(G)시험 설계,(H)대상 치료 분야,(I)주요 지리적 지역과 같은 매개변수를 바탕으로, 각종 신규 암 바이오마커와 관련된 완료된, 진행 중인, 계획 중인 임상시험을 검증합니다.

- 출판물 분석 : 새로운 암 바이오마커와 관련된 진행 중인 연구의 주요 중점 분야를 파악하기 위해, 630건 이상의 공개된 논문을 상세하게 분석합니다. 본 분석에서는(A)출판 연도,(B)출판물 유형,(C)암 유형,(D)저작권자,(E)새로운 중점 분야,(F)가장 활발한 출판사(출판 건수 기준),(G) 주요 학술지(저널 임팩트 팩터 및 게재 논문 수 기준)를 바탕으로 일반적인 동향을 밝히고 있습니다.

- 대형 제약사 분석 : 주요 제약사별로 진행 중인 암 바이오마커에 초점을 맞춘 다양한 활동에 대한 종합적인 조사입니다. 이 분석에는 주요 제약사의 분포를 보여주는 히트맵을 통한 시각화뿐만 아니라, 여러 관련 지표를 바탕으로 각사의 노력을 비교하는 스파이더 웹 다이어그램이 포함되어 있습니다.

- 사례 연구 1 - 동반 진단 산업의 밸류체인 분석 : 동반 진단 생산과 관련된 다양한 단계를 탐구하는 종합적인 밸류체인 분석입니다. 여기에는 연구개발(R&D), 제품의 임상 평가, 제조 및 조립, 지불 주체와의 협상 및 마케팅 활동, 그리고 앞서 언급한 각 단계에서의 비용 배분에 대한 고찰이 포함됩니다.

- 사례 연구 2 - 향후 성장 기회: 이 분야의 암 바이오마커 검사 솔루션 제공업체에게 단·중기 및 중·장기적으로 시장 변화에 영향을 미칠 수 있는 향후 기회에 대해 상세하게 다루고 있습니다.

- 시장 영향 분석 : 본 보고서에서는 시장 성장에 영향을 미치는 촉진요인, 억제요인, 기회, 과제 등 다양한 요인을 분석했습니다.

목차

제1장 서문

제2장 조사 방법

제3장 경제적 및 기타 프로젝트 고유 고려사항

제4장 거시경제 지표

제5장 주요 요약

제6장 서론

제7장 시장 구도

제8장 제품 경쟁력 분석

제9장 기업 개요 : 암 바이오마커 검사 솔루션 제공업체

제10장 바이오마커에 근거한 임상시험을 위한 혁신적인 연구 디자인

제11장 임상시험 분석

제12장 출판물 분석

제13장 대형 제약 기업 : 벤치마크 분석

제14장 사례 연구 : 동반진단 업계 밸류체인 분석

제15장 사례 연구 : 암 바이오마커 산업 향후 성장 기회

제16장 세계의 암 바이오마커 시장

제17장 암 바이오마커 시장(바이오마커 유형별)

제18장 암 바이오마커 시장(암 유형별)

제19장 암 바이오마커 시장(지역별)

제20장 결론

제21장 경영 임원 인사이트

제22장 부록 1 : 표 형식 데이터

제23장 부록 2 : 기업 및 조직 리스트

LSH 26.06.19Cancer Biomarkers Market: Overview

As per Roots Analysis, the global cancer biomarkers market is estimated to grow from USD 25.9 billion in the current year to USD 37.8 billion by 2035, at a CAGR of 4.3% during the forecast period, till 2035.

Cancer Biomarkers Market: Growth and Trends

Over the past two decades, researchers and biopharmaceutical companies have introduced several advanced and highly effective cancer treatment modalities, including targeted therapies, immunotherapies, and therapeutic cancer vaccines. Despite these advancements, oncology research continues to encounter significant challenges, including systemic treatment-related toxicities, high clinical trial attrition rates, and various pharmacological and therapy-specific limitations. These persistent challenges underscore the growing need for more precise and reliable diagnostic frameworks capable of improving patient outcomes while minimizing the economic impact associated with therapeutic failure.

To address this critical unmet need, the healthcare industry has increasingly adopted cancer biomarkers as a cornerstone of modern oncology diagnostics. The demand for such biomarkers is primarily driven by the molecular heterogeneity of cancer, wherein patients diagnosed with the same cancer type and disease stage often exhibit distinct molecular and genetic profiles, resulting in variable responses to recombinant drugs and biologic therapies. In response, pharmaceutical developers and healthcare providers have progressively shifted toward precision oncology approaches. Through the identification of disease-specific molecular signatures, clinicians are now able to customize treatment strategies for individual patients, moving beyond the conventional "one-size-fits-all" therapeutic model.

Although single-analyte biomarkers, such as PD-L1, BRAF, and EGFR, continue to play a foundational role in oncology diagnostics, their predictive capabilities are often limited in the context of complex genomic landscapes and long-term treatment efficacy. As a result, advancements in high-throughput technologies, particularly next-generation sequencing (NGS), have facilitated the development and validation of more comprehensive biomarkers, including tumor mutational burden (TMB) and microsatellite instability (MSI). These advanced biomarkers offer deeper understanding of genomic instability and tumor biology, enabling more precise patient stratification and treatment selection.

The expanding pipeline of clinically validated biomarkers remains a key driver of market growth. Supported by substantial investments from leading pharmaceutical and biotechnology companies in multi-omics and precision medicine initiatives, the cancer biomarkers market is positioned for significant expansion, with data-driven diagnostic integration expected to redefine the future standard of oncology care.

Growth Drivers: Strategic Enablers of Market Expansion

The growing global burden of cancer, driven by aging populations, changing lifestyles, and increasing exposure to environmental risk factors, continues to accelerate the demand for advanced oncology diagnostics and targeted treatment approaches. In response to this rising disease prevalence, the healthcare industry is witnessing a significant shift toward precision oncology and personalized medicine, wherein treatment decisions are increasingly guided by individual tumor biology and molecular profiling. This transition has been strongly supported by rapid technological advancements in next-generation sequencing (NGS), liquid biopsy platforms, multi-omics technologies, bioinformatics, and artificial intelligence-enabled diagnostics, all of which have streamlined biomarker discovery, validation, and clinical implementation.

These innovations enable clinicians to identify patient-specific molecular signatures, improving therapeutic selection, reducing treatment-related toxicities, and enhancing survival outcomes across multiple cancer indications. Further strengthening market expansion, leading pharmaceutical and biotechnology companies, including Roche and Novartis, are actively investing in biomarker-driven clinical trials and companion diagnostic development to support targeted immuno-oncology therapies. In parallel, increasing regulatory approvals for companion diagnostics and expanded indications for immunotherapies are reinforcing the market's upward trajectory, positioning cancer biomarkers as a critical component of next-generation oncology care.

Market Challenges: Critical Barriers Impeding Progress

Despite the strong growth potential of the cancer biomarkers market, several operational, technical, and regulatory challenges continue to hinder widespread adoption and commercialization. One of the primary barriers is the high cost and extended timeline associated with biomarker research and development, as companies are required to invest substantial capital in discovery, validation, and regulatory approval processes before achieving clinical adoption. These financial and operational demands often restrict market participation, particularly among small and mid-sized biotechnology firms, while simultaneously delaying the introduction of innovative diagnostic solutions. In addition, technical limitations associated with sample collection, handling, and storage remain a significant concern. Improper processing can result in biomarker degradation, contamination, and inconsistent test results, ultimately compromising diagnostic accuracy and reducing clinical confidence in biomarker-based assays.

The market also faces challenges associated with limited large-scale clinical validation and the absence of standardized data frameworks, as many emerging biomarkers are yet to demonstrate consistent clinical utility across diverse patient populations. Variability in assay methodologies, reporting standards, and data formats across laboratories further complicates data integration, comparative analyses, and routine implementation in oncology practice. Moreover, the evolving and region-specific regulatory landscape for biomarker-based diagnostics and companion tests, overseen by agencies such as the U.S. Food and Drug Administration and the European Medicines Agency, continues to create uncertainty for market participants. It increases compliance requirements, prolongs approval timelines, and raises overall commercialization costs.

Cancer Biomarkers Market: Key Insights

The report delves into the current state of the cancer biomarkers market and identifies potential growth opportunities within industry. Some key findings from the report include:

- Advancements in biotechnology have led to the identification of several cancer biomarker testing solutions, which are presently being used for a variety of purposes, including diagnosis, clinical research and to facilitate therapy-related decision-making.

- Currently, more than 290 biomarker solutions are available in the market; around 85% of these solutions use next generation sequencing for the assessment of cancer biomarkers.

- Majority (68%) of the cancer biomarker testing solutions assist in the evaluation of indels; 85% of the testing solutions utilize next generation sequencing (NGS) for the assessment of cancer biomarkers.

- Several industry and non-industry players are conducting biomarker-stratified clinical trials to develop new targeted therapies; most of the patients were enrolled across multiple sites in China.

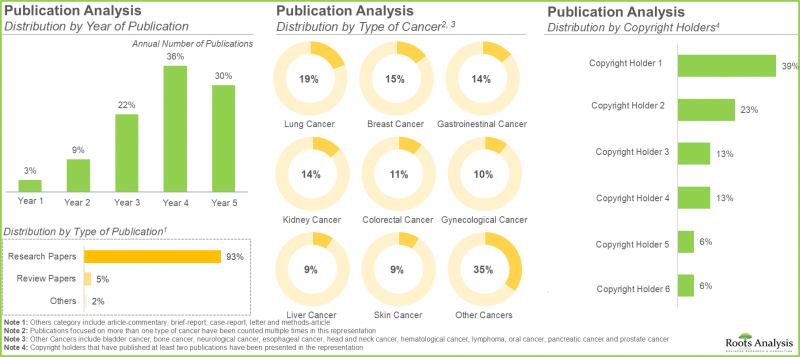

- The field of cancer biomarkers has seen a significant rise in research, with over 470 articles published by various researchers, underscoring the growing focus of several industry players and academic players in this domain.

- The cancer biomarkers market is expected to witness an annualized growth rate of 4.3% during the forecast period; notably, biomarker testing solutions for breast cancer are expected to capture the majority current market share.

- Driven by the growing adoption of personalized medicine in the US, the cancer biomarkers market is poised to grow at a higher CAGR during the forecast period.

- Given the rising prevalence of cancer, and the intensifying demand for precise, biomarker-driven diagnostics across clinical and research settings, the cancer biomarkers market is positioned for steady growth.

Cancer Biomarkers Market

The market sizing and opportunity analysis has been segmented across the following parameters:

By Type of Biomarker

- HER2

- MET

- EGFR

- PD-L1

- NTRK

- ALK

- Other Biomarkers

By Type of Cancer

- Breast Cancer

- Colorectum Cancer

- Lung Cancer

- Prostate Cancer

- Thyroid Cancer

- Bladder Cancer

- Melanoma

- Non-Hodgkin Lymphoma

- Endometrial Cancer

- Kidney Cancer

- Leukemia

By Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and North Africa

Cancer Biomarkers Market: Key Segments

Which Type of Biomarker Testing Accounts for the Largest Share in the Cancer Biomarkers Market?

In the current year, HER2 biomarker testing solutions are expected to account for the largest share (21.1%) of the cancer biomarkers market. This dominance is primarily attributed to the extensive clinical validation of HER2 testing in the diagnosis, prognosis, and therapeutic management of breast and gastric cancers. The segment's strong market position is further reinforced by its direct association with several high-value targeted therapies, including Trastuzumab and Pertuzumab, which continue to drive sustained global demand for HER2-based companion diagnostics.

In contrast, the EGFR biomarker testing segment is anticipated to witness comparatively faster growth during the forecast period. This growth is primarily driven by the increasing global prevalence of lung cancer, along with the rising adoption of precision oncology and targeted treatment approaches. In particular, the growing clinical utilization of EGFR inhibitors, such as Osimertinib, has significantly increased the demand for EGFR mutation testing to support patient stratification and treatment selection in non-small cell lung cancer (NSCLC).

Regional Analysis: Which Regions are Showing the Fastest Growth in the Cancer Biomarkers Testing Domain?

North America: Leading the Global Market

North America is expected to dominate the cancer biomarkers market, capturing 52.1% of the overall market revenue in the current year. The region's leadership position can be attributed to the rising burden of cancer, well-established healthcare infrastructure, and the increasing adoption of personalized medicine and precision oncology frameworks. In addition, strong investments in biomarker research, widespread availability of advanced diagnostic technologies, and favorable regulatory and reimbursement environments continue to support market growth across the region.

Which Type of Cancer Holds the Highest Share in the Market?

According to current market estimates, biomarker tests for breast cancer are projected to account for the largest share (25.1%) of the overall cancer biomarkers market revenue. This can be attributed to the high global prevalence of breast cancer as one of the leading causes of cancer-related mortality among women. As a result, there is significant demand for biomarker-driven diagnostics that support early detection, prognosis assessment, risk stratification, and personalized therapeutic interventions.

Looking ahead, the melanoma biomarker testing segment is anticipated to grow at a relatively faster pace, with a projected CAGR of 4.5% during the forecast period. This growth is primarily driven by the increasing global incidence of melanoma, continued advancements in targeted therapies, and the growing adoption of precision diagnostic approaches. In particular, the clinical uptake of BRAF and MEK inhibitors, alongside rising utilization of BRAF mutation testing and liquid biopsy-based biomarker assays, is expected to significantly contribute to segment expansion.

Example Players in Cancer Biomarkers Market

- ARUP Laboratories

- Asper Biogene

- BioReference

- Caris Life Sciences

- CeGaT

- Foundation Medicine

- Genekor Medical

- Guardant Health

- IQVIA Laborateries

- Labcorp

- MedGenome

- NeoGenomics Laboratories

- Nonacus

- OncoDNA

- Quest Diagnostics

- Oxford Gene Technology

- Personal Genome Diagnostics

- PhenoPath

- Positive Biosciences

- Tempus

- Thermo Fisher Scientific

- YuceBio

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

- Chief Technical Officer and Former Director of Preclinical Development & Strategic Partnerships, Small Company, US

- Business Manager, Mid-sized Company, Germany

- Former Chief Scientific Officer, Large Company, US

Cancer Biomarkers Market: Research Coverage

- Market Sizing and Opportunity Analysis: The report features an in-depth analysis of the cancer biomarkers market, focusing on key market segments, including [A] type of biomarker, [B] type of cancer and [C] geographical regions.

- Market Landscape: A comprehensive evaluation of testing solutions for novel cancer biomarkers, considering various parameters, such as [A] type of biomarker evaluated, [B] type of analytical technique used, [C] turnaround time, [D] type of sample supported, [E] type of nucleic acid tested, [F] type of cancer, [G] application area and [H] End-user. Additionally, it includes a detailed list of developers engaged in offering novel cancer biomarker testing solutions, along with analysis based on various parameters, such as [I] year of establishment, [J] company size (in terms of employee count) and [K] location of headquarters.

- Product Competitiveness Analysis: A comprehensive competitive analysis of novel cancer biomarker testing solutions, examining factors, such as product versatility and product competitiveness.

- Company Profiles: In-depth profiles of key industry players offering novel cancer biomarker testing solutions, focusing on [A] company overviews, [B] financial information, [C] cancer biomarker testing solutions portfolio, [D] recent developments and [E] an informed future outlook.

- Case Study: A general discussion on the innovative study designs involved in conducting biomarker-based clinical trial to evaluate drugs for oncological disorders. It includes details on the structure of each study design, highlighting their respective advantages and challenges.

- Clinical Trial Analysis: Examination of completed, ongoing, and planned clinical studies of various novel cancer biomarkers based on parameters like [A] trial registration year, [B] trial status, [C] trial phase, [D] enrolled patient population, [E] type of sponsor / collaborator, [F] most active players (in terms of number of registered trials), [G] study design, [H] target therapeutic area and [I] key geographical regions.

- Publication Analysis: A detailed publication analysis of over 630 articles that have been published highlighting the key focus areas of ongoing research related to novel cancer biomarkers. It highlights the prevalent trends based on the [A] year of publication, [B] type of publication, [C] type of cancer, [D] copyright holders, [E] emerging focus areas, [F] most active publishers (in terms of number of publications) and [G] key journals (in terms of journal impact factor and number of articles published).

- Big Pharma Analysis: A comprehensive examination of various initiatives focused on cancer biomarkers undertaken by major pharmaceutical companies. This analysis includes heat map visualizations that illustrate the distribution of leading pharmaceutical firms, as well as spider web diagrams that compare their initiatives across multiple relevant parameters.

- Case Study 1 - Analysis Of Value Chain in the Companion Diagnostics Industry: A comprehensive value chain analysis that explores the various stages involved in the production of companion diagnostics. This includes a discussion on research and development (R&D), clinical assessment of the product, manufacturing and assembly, payer negotiation and marketing activities and the cost distribution across each of the aforementioned stages.

- Case Study 2 - Future Growth Opportunities: A detailed discussion on the upcoming opportunities for cancer biomarker testing solution providers in this field that are likely to impact on the evolution of the market in the short to mid-term and mid to long-term.

- Market Impact Analysis: The report analyzes various factors such as drivers, restraints, opportunities, and challenges affecting the market growth.

Key Questions Answered in this Report

- Which are the leading companies in the cancer biomarkers market?

- Which region dominates the cancer biomarkers market?

- What are the key trends observed in the cancer biomarkers market?

- What factors are likely to influence the evolution of this market?

- What are the primary challenges faced by cancer biomarkers testing solution providers?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

- The report can aid businesses in identifying future opportunities in any sector. It also helps in understanding if those opportunities are worth pursuing.

- The report helps in identifying customer demand by understanding the needs, preferences, and behavior of the target audience in order to tailor products or services effectively.

- The report equips new entrants with requisite information regarding a particular market to help them build successful business strategies.

- The report allows for more effective communication with the audience and in building strong business relations.

Additional Benefits

- Complementary PPT Insights Pack

- Complementary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Report Coverage

- 1.3. Market Segmentation

- 1.4. Key Market Insights

- 1.5. Market Share Insights

- 1.6. Key Questions Answered

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. ECONOMIC AND OTHER PROJECT-SPECIFIC CONSIDERATIONS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

- 5.1. Cancer Biomarker Testing Solutions: Market Landscape

- 5.2. Cancer Biomarker Testing Solutions: Market Trends

- 5.3. Cancer Biomarker Testing Solutions: Market Forecast and Opportunity Analysis

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. An Overview of Cancer Biomarkers

- 6.2.1. Need for Cancer Biomarkers

- 6.2.2. Identification of a Candidate Biomarker

- 6.3. Type of Cancer Biomarkers

- 6.4. Novel Cancer Biomarkers

- 6.4.1. Tumor Mutation Burden (TMB)

- 6.4.1.1. Variation of TMB across Multiple Indications

- 6.4.1.2. Methods for Measurement of TMB

- 6.4.1.3. Factors Affecting Measurement of TMB

- 6.4.1.4. Initiatives for Assessment of TMB as a Potential Biomarker

- 6.4.2. Microsatellite Instability / Mismatch Repair Deficiency (MSI / MMR)

- 6.4.2.1. Variation of MSI across Multiple Indications

- 6.4.2.2. Methods for Measurement of MSI

- 6.4.3. Single Nucleotide Variants (SNVs)

- 6.4.3.1. Variation of SNV across Multiple Indications

- 6.4.3.2. Methods for Measurement of SNV

- 6.4.4. Copy Number Variants (CNVs)

- 6.4.4.1. Variation of CNV across Multiple Cancer Indications

- 6.4.4.2. Methods for Measurement of CNV

- 6.4.5. Indels and Other Novel Biomarkers

- 6.4.1. Tumor Mutation Burden (TMB)

- 6.5. Future Perspective

7. MARKET LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Cancer Biomarker Testing Solutions: Overall Market Landscape

- 7.2.1. Analysis by Type of Biomarker Evaluated

- 7.2.2. Analysis by Type of Analytical Technique Used

- 7.2.3. Analysis by Turnaround Time

- 7.2.4. Analysis by Type of Sample Supported

- 7.2.5. Analysis by Type of Nucleic Acid Tested

- 7.2.6. Analysis by Type of Cancer

- 7.2.7. Analysis by Application Area

- 7.2.8. Analysis by End-user

- 7.3. Cancer Biomarkers Testing Solutions: Provider Landscape

- 7.3.1. Analysis by Year of Establishment

- 7.3.2. Analysis by Company Size

- 7.3.3. Analysis by Location of Headquarters

- 7.3.4. Most Active Player: Analysis by Number of Testing Solutions Offered

8. PRODUCT COMPETITIVENESS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions / Key Parameters

- 8.3. Methodology

- 8.4. Overview of Peer Groups

- 8.5. Cancer Biomarkers Testing Solutions: Product Competitiveness Analysis

- 8.5.1. Cancer Biomarker Testing Solutions Offered by Providers Headquartered in North America

- 8.5.2. Cancer Biomarker Testing Solutions Offered by Providers Headquartered in Europe

- 8.5.3. Cancer Biomarker Testing Solutions Offered by Providers Headquartered in Asia-Pacific

9. COMPANY PROFILES: CANCER BIOMARKERS TESTING SOLUTION PROVIDERS

- 9.1. Chapter Overview

- 9.2. Agilent

- 9.2.1. Company Overview

- 9.2.2. Cancer Biomarker Testing Solutions Portfolio

- 9.3. ARUP Laboratories

- 9.3.1. Company Overview

- 9.3.2. Cancer Biomarker Testing Solutions Portfolio

- 9.4. Asper Biogene

- 9.4.1. Company Overview

- 9.4.2. Cancer Biomarker Testing Solutions Portfolio

- 9.5. BioReference

- 9.5.1. Company Overview

- 9.5.2. Cancer Biomarker Testing Solutions Portfolio

- 9.6. Caris Life Sciences

- 9.6.1. Company Overview

- 9.6.2. Cancer Biomarker Testing Solutions Portfolio

- 9.7. CeGaT

- 9.7.1. Company Overview

- 9.7.2. Cancer Biomarker Testing Solutions Portfolio

- 9.8. Foundation Medicine

- 9.8.1. Company Overview

- 9.8.2. Cancer Biomarker Testing Solutions Portfolio

- 9.9. Genekor Medical

- 9.9.1. Company Overview

- 9.9.2. Cancer Biomarker Testing Solutions Portfolio

- 9.10. Guardant Health

- 9.10.1. Company Overview

- 9.10.2. Cancer Biomarker Testing Solutions Portfolio

- 9.11. IQVIA Laboratories

- 9.11.1. Company Overview

- 9.11.2. Cancer Biomarker Testing Solutions Portfolio

- 9.12. Labcorp

- 9.12.1. Company Overview

- 9.12.2. Cancer Biomarker Testing Solutions Portfolio

- 9.13. MedGenome

- 9.13.1. Company Overview

- 9.13.2. Cancer Biomarker Testing Solutions Portfolio

- 9.14. NeoGenomics Laboratories

- 9.14.1. Company Overview

- 9.14.2. Cancer Biomarker Testing Solutions Portfolio

- 9.15. Nonacus

- 9.15.1. Company Overview

- 9.15.2. Cancer Biomarker Testing Solutions Portfolio

- 9.16. OncoDNA

- 9.16.1. Company Overview

- 9.16.2. Cancer Biomarker Testing Solutions Portfolio

- 9.17. Quest Diagnostics

- 9.17.1. Company Overview

- 9.17.2. Cancer Biomarker Testing Solutions Portfolio

- 9.19. Oxford Gene Technology

- 9.19.1. Company Overview

- 9.19.2. Cancer Biomarker Testing Solutions Portfolio

- 9.19. Personal Genome Diagnostics

- 9.19.1. Company Overview

- 9.19.2. Cancer Biomarker Testing Solutions Portfolio

- 9.20. PhenoPath

- 9.20.1. Company Overview

- 9.20.2. Cancer Biomarker Testing Solutions Portfolio

- 9.21. Positive Biosciences

- 9.21.1. Company Overview

- 9.21.2. Cancer Biomarker Testing Solutions Portfolio

- 9.22. Tempus AI

- 9.22.1. Company Overview

- 9.22.2. Cancer Biomarker Testing Solutions Portfolio

- 9.23. Thermo Fisher Scientific

- 9.23.1. Company Overview

- 9.23.2. Cancer Biomarker Testing Solutions Portfolio

- 9.24. YuceBio

- 9.24.1. Company Overview

- 9.24.2. Cancer Biomarker Testing Solutions Portfolio

10. INNOVATIVE STUDY DESIGNS FOR BIOMARKER-BASED CLINICAL TRIALS

- 10.1. Chapter Overview

- 10.2. Study Designs for Biomarker-based Clinical Trials

- 10.2.1. Enrichment Design

- 10.2.2. All-comers Design

- 10.2.3. Mixture / Hybrid Design

- 10.2.4. Adaptive Design

- 10.3. Regulatory Guidelines for Biomarker-based Clinical Trial Designs

- 10.4. Conclusion

11. CLINICAL TRIAL ANALYSIS

- 11.1. Chapter Overview

- 11.2. Scope and Methodology

- 11.3. Cancer Biomarkers: Clinical Trial Analysis

- 11.3.1. Analysis by Trial Registration Year

- 11.3.2. Analysis of Patients Enrolled by Trial Registration Year

- 11.3.3. Analysis by Trial Status

- 11.3.4. Analysis by Trial Registration Year and Trial Status

- 11.3.5. Analysis by Trial Phase

- 11.3.6. Analysis of Enrolled Patient Population by Trial Phase

- 11.3.7. Analysis by Patient Gender

- 11.3.8. Analysis by Study Design

- 11.3.8.1. Analysis by Type of Allocation

- 11.3.8.2. Analysis by Type of Intervention Model

- 11.3.8.3. Analysis by Type of Masking

- 11.3.8.4. Analysis by Type of Primary Purpose

- 11.3.9. Analysis by Type of Sponsor / Collaborator

- 11.3.10. Most Active Industry Player: Analysis by Number of Registered Trials

- 11.3.11. Most Active Non-Industry Player: Analysis by Number of Registered Trials

- 11.3.12. Analysis of Clinical Trials by Geography

- 11.3.13. Analysis of Clinical Trials by Trial Status and Geography

- 11.3.14. Analysis of Patients Enrolled by Trial Status and Geography

12. PUBLICATION ANALYSIS

- 12.1. Chapter Overview

- 12.2. Scope and Methodology

- 12.3. Cancer Biomarkers: Publication Analysis

- 12.3.1. Analysis by Year of Publication

- 12.3.2. Analysis by Type of Publication

- 12.3.3. Analysis by Type of Cancer

- 12.3.4. Analysis by Copyright Holders

- 12.3.5. Word Cloud: Emerging Focus Areas

- 12.3.6. Most Active Publishers: Analysis by Number of Publications

- 12.3.7. Key Journals: Analysis by Impact Factor

- 12.3.8. Key Journals: Analysis by Number of Publications

13. BIG PHARMA PLAYERS: BENCHMARK ANALYSIS

- 13.1. Chapter Overview

- 13.2. Scope and Methodology

- 13.3. Big Pharma Players: Benchmarking Analysis

- 13.3.1. Spider Web Analysis: Abbott

- 13.3.2. Spider Web Analysis: AbbVie

- 13.3.3. Spider Web Analysis: Amgen

- 13.3.4. Spider Web Analysis: AstraZeneca

- 13.3.5. Spider Web Analysis: Bayer

- 13.3.6. Spider Web Analysis: Boehringer Ingelheim

- 13.3.7. Spider Web Analysis: Bristol-Myers Squib

- 13.3.8. Spider Web Analysis: Eli Lilly

- 13.3.9. Spider Web Analysis: Gilead

- 13.3.10. Spider Web Analysis: GlaxoSmithKline

- 13.3.11. Spider Web Analysis: Merck

- 13.3.12. Spider Web Analysis: Novartis

- 13.3.13. Spider Web Analysis: Pfizer

- 13.3.14. Spider Web Analysis: Roche

- 13.3.15. Spider Web Analysis: Sanofi

- 13.4. Concluding Remarks

14. CASE STUDY: ANALYSIS OF VALUE CHAIN IN THE COMPANION DIAGNOSTICS INDUSTRY

- 14.1. Chapter Overview

- 14.2. Companion Diagnostics: Value Chain

- 14.3. Cost Distribution Across the Value Chain

- 14.3.1. Costs Associated with Research and Product Development

- 14.3.2. Costs Associated with Manufacturing and Assembly

- 14.3.3. Costs Associated with Clinical Trials, FDA Approval and Other Administrative Tasks

- 14.3.4. Costs Associated with Payer Negotiation and KOL Engagement

- 14.3.5. Costs Associated with Marketing and Sales

15. CASE STUDY: FUTURE GROWTH OPPORTUNITIES IN CANCER BIOMARKERS INDUSTRY

- 15.1. Chapter Overview

- 15.1.1. Growing Focus on Personalized Medicines

- 15.1.2. Rising need for Biomarker Testing for Various Oncological Disorders

- 15.1.3. Increase in Number of Biomarker-based Clinical Trials

- 15.1.4. Increased Adoption of Emerging Analytical Techniques for Biomarker Assessment

- 15.1.5. Development of Companion Diagnostic Products

- 15.2. Conclusion

16. GLOBAL CANCER BIOMARKERS MARKET

- 16.1. Chapter Overview

- 16.2. Assumptions and Methodology

- 16.3. Global Cancer Biomarkers Market, Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 16.3.1. Scenario Analysis

- 16.3.1.1. Conservative Scenario

- 16.3.1.2. Optimistic Scenario

- 16.3.1. Scenario Analysis

- 16.4. Key Market Segmentations

17. CANCER BIOMARKERS MARKET, BY TYPE OF BIOMARKER

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Cancer Biomarkers Market: Distribution by Type of Biomarker

- 17.3.1. Cancer Biomarkers Market for HER2 Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.2. Cancer Biomarkers Market for MET Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.3. Cancer Biomarkers Market for EGFR Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.4. Cancer Biomarkers Market for PD-L1 Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.5. Cancer Biomarkers Market for NTRK Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.6. Cancer Biomarkers Market for ALK Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.3.7. Cancer Biomarkers Market for Other Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4. Cancer Biomarkers Market: Distribution of Novel Biomarkers

- 17.4.1. Cancer Biomarkers Market for SNV Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4.2. Cancer Biomarkers Market for MSI Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4.3. Cancer Biomarkers Market for CNV Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4.4. Cancer Biomarkers Market for TMB Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4.5. Cancer Biomarkers Market for TIL Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.4.6. Cancer Biomarkers Market for Indel Biomarkers: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 17.5. Data Triangulation and Validation

18. CANCER BIOMARKERS MARKET, BY TYPE OF CANCER

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Cancer Biomarkers Market: Distribution by Type of Cancer

- 18.3.1. Cancer Biomarkers Market for Breast Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.2. Cancer Biomarkers Market for Colorectum Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.3. Cancer Biomarkers Market for Lung Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.4. Cancer Biomarkers Market for Prostate Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.5. Cancer Biomarkers Market for Thyroid Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.6. Cancer Biomarkers Market for Bladder Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.7. Cancer Biomarkers Market for Melanoma: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.8. Cancer Biomarkers Market for Non-Hodgkin Lymphoma: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.9. Cancer Biomarkers Market for Endometrial Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.10. Cancer Biomarkers Market for Kidney Cancer: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.3.11. Cancer Biomarkers Market for Leukemia: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 18.4. Data Triangulation and Validation

19. CANCER BIOMARKERS MARKET, BY GEOGRAPHICAL REGIONS

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Cancer Biomarkers Market: Distribution by Geographical Regions

- 19.3.1. Cancer Biomarkers Market in North America: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.1.1. North America Cancer Biomarkers Market in the US: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.1.2. North America Cancer Biomarkers Market in Canada: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2. Cancer Biomarkers Market in Europe: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2.1. Europe Cancer Biomarkers Market in Germany: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2.2. Europe Cancer Biomarkers Market in France: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2.3. Europe Cancer Biomarkers Market in the UK: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2.4. Europe Cancer Biomarkers Market in Italy: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.2.5. Europe Cancer Biomarkers Market in Spain: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3. Cancer Biomarkers Market in Asia-Pacific: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.1. Asia-Pacific Cancer Biomarkers Market in China: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.2. Asia-Pacific Cancer Biomarkers Market in Japan: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.3. Asia-Pacific Cancer Biomarkers Market in India: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.4. Asia-Pacific Cancer Biomarkers Market in South Korea: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.5. Asia-Pacific Cancer Biomarkers Market in Australia: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.3.6. Asia-Pacific Cancer Biomarkers Market in New Zealand: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.4. Cancer Biomarkers Market in Latin America: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.4.1. Latin America Cancer Biomarkers Market in Brazil: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.4.2. Latin America Cancer Biomarkers Market in Argentina: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.4.3. Latin America Cancer Biomarkers Market in Chile: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.5. Cancer Biomarkers Market in Middle East and North Africa: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.5.1. Middle East and North Africa Cancer Biomarkers Market in Egypt: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.3.1. Cancer Biomarkers Market in North America: Historical Trends (since 2021) and Forecasted Estimates (till 2035)

- 19.4. Market Dynamics Assessment

- 19.4.1. Penetration Growth (P-G) Matrix

- 19.4.2. Market Movement Analysis

- 19.5. Data Triangulation and Validation

- *Detailed information on cross sectional analysis is available in the Excel Data Packs shared along with the report**

20. CONCLUDING REMARKS

21. EXECUTIVE INSIGHTS

- 21.1. Chapter Overview

- 21.2. Company A

- 21.2.1. Company Snapshot

- 21.2.2. Interview Transcript: Chief Technical Officer and Former Director of Preclinical Development & Strategic Partnerships

- 21.3. Company B

- 21.3.1. Company Snapshot

- 21.3.2. Interview Transcript: Former Chief Scientific Officer

- 21.4. Company C

- 21.4.1. Company Snapshot

- 21.4.2. Interview Transcript: Business Manager