|

시장보고서

상품코드

2050384

생명과학용 AI 시장 예측(-2031년) : 제공(엔드 투 엔드, 니치/포인트, AI 기술), 용도(Drug Discovery, 임상시험, 품질 보증, 규제 대응), 툴(기계학습, 자연언어처리, 컴퓨터 비전), 최종사용자별(제약, 바이오테크놀러지)AI in Life Science Market by Offering (End-to-End, Niche/Point, AI Tech), Application (Drug Discovery, Clinical Trials, Quality Assurance, Regulatory), Tool (Machine Learning, NLP, Computer Vision), End User (Pharma, Biotech) - Global Forecast to 2031 |

||||||

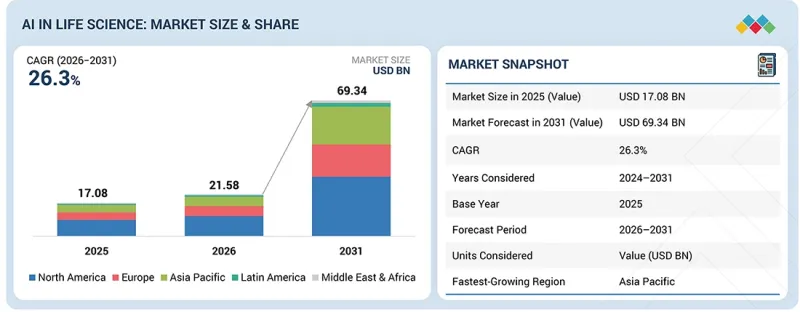

생명과학 분야에서 AI 시장 규모는 2026년 215억 8,000만 달러에서 예측 기간 중 CAGR 26.3%라는 높은 신장률로 확대하며, 2031년에는 693억 4,000만 달러에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(달러) |

| 부문 | 제공, 용도, 컴포넌트, 툴, 도입 형태, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

이러한 성장세는 생명과학 기업이 기존 분석에서 자율적인 시스템으로 전환하는 데 도움을 주는 데이터 지향적, 에이전트형 AI 아키텍처의 성장세에 힘입어 더욱 가속화되고 있습니다. 이러한 혁신은 특히 임상시험 최적화, 리얼월드 증거 수집, 시판 후 모니터링에 큰 영향을 미치고 있습니다. 기존에는 방대하고 분산된 데이터세트가 이러한 업무 효율성 향상에 걸림돌이 되었습니다. 또한 AI 기술이 탑재된 클라우드 기반 서비스 도입으로 생명과학 기업은 의료 데이터와 유전체 데이터부터 환자별 정보까지 다양한 데이터 소스를 통합하여 예측 모델링을 수행하고 신약 개발 프로세스를 가속화할 수 있게 되었습니다. 문헌 검색, 가설 수립, 환자 세분화와 같은 첨단 작업을 자동화하는 AI 에이전트의 등장도 업무 효율성 향상과 혁신 주기의 가속화에 기여하고 있습니다. 예를 들어 오라클(Oracle Corporation, 미국)은 2026년 1월, 1억 2,900만 건 이상의 익명화된 의료 기록과 생성형 AI 및 에이전트형 인텔리전스 솔루션을 결합하여 연구 및 임상시험을 가속화하는 'Oracle Life Sciences AI Data Platform'을 출시했습니다. Data Platform'을 출시했습니다. 또한 IQVIA Holdings Inc.(미국)는 2025년 6월, 타깃 식별 및 임상 데이터 분석을 포함한 임상 및 상업 업무의 워크플로우를 최적화하기 위해 AI 에이전트를 도입했습니다.

지역별로는 북미가 첨단 연구 네트워크의 존재, 높은 디지털화 수준, 생명공학 및 제약 분야의 혁신에 대한 막대한 투자로 인해 북미가 지배적인 지역으로 부상하고 있습니다. 이 지역은 대학, 병원, 기술 기업 간의 시너지 효과라는 강점을 활용하여 AI 주도의 진보를 더욱 빠르게 실현하고 있습니다. 또한 우호적인 규제 환경과 신약 개발 및 임상 시험에 있으며, 첨단 분석 기술의 빠른 도입으로 이 지역의 리더로서의 입지를 확고히 하고 있습니다. 유럽은 정부와 기업이 AI 기술과 데이터 프라이버시 요구사항을 준수하는 AI 제품에 대한 관심이 높아지면서 이 부문에서 두 번째로 큰 시장 규모를 차지하고 있습니다.

제품별로는 생명과학 밸류체인 전반에 걸쳐 데이터 수집, 모델 구축, 검증, 배포를 지원하는 통합 플랫폼에 대한 수요가 증가함에 따라 엔드투엔드 솔루션이 2025년 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 이러한 솔루션은 타겟 식별부터 임상 및 상업적 수준까지 생명과학 워크플로우를 보다 효율적이고 일관성 있게 만들어 줍니다. 현재 업계 기업은 확장성, 규제 준수, 부서 간 협업을 가능하게 하는 능력으로 인해 독립형 소프트웨어보다 풀스택 AI 플랫폼을 선호하는 경향이 있습니다. 이러한 변화는 실험적인 AI 애플리케이션에서 R&D 및 임상 시험에서 일관성, 재현성, 감사 가능한 프로세스를 필요로 하는 기업급 도입으로 전환하는 광범위한 시장 동향을 반영하고 있습니다. 예를 들어 2025년 10월 이탈리아 기업 expert.ai는 임상시험 설계 및 규제 및 연구 워크플로우를 최적화하는 AI 기반 솔루션을 출시했습니다. 또한 2025년 6월 ArisGlobal(미국)은 세계 유수의 제약회사에 자사의 LifeSphere NavaX AI 플랫폼을 도입하여 연간 약 35만 건의 안전성 사례를 자동 분석할 수 있도록 했습니다.

용도별로 보면 임상용 분야가 가장 빠른 성장세를 보일 것으로 예상됩니다. 이는 환자 경험 향상, 임상 시험의 효율화, 실시간 데이터 분석을 통한 정밀의료 도입을 위한 AI 활용 증가에 따른 것입니다. AI를 활용한 소프트웨어는 피험자 등록, 시험 관리, 프로토콜 최적화 개선에 기여하고 있으며, 이를 통해 시험 기간 단축과 성공률 향상에 기여하고 있습니다. 또한 환자 중심의 분산형 임상시험으로의 전환은 AI 기반 소프트웨어의 도입을 촉진하고 있습니다. 일례로 IQVIA는 2026년 3월까지 150개 이상의 AI 에이전트를 도입했으며, 상위 20개 제약사 중 19개 제약사가 이를 활용했습니다. 2025년 6월, IQVIA Holdings Inc.(미국)는 임상 업무 효율화를 위한 AI 에이전트를 출시했습니다.

세계의 생명과학 분야 AI 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 각종 영향요인 분석, 기술-특허 동향, 법-규제 환경, 사례 분석, 시장 규모 추이 및 예측, 각종 부문별-지역별-주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등의 정보를 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 규제 상황

제7장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 디스럽션

제8장 고객 상황과 구매 행동

제9장 생명과학용 AI 시장 : 툴별

제10장 생명과학용 AI 시장 : 용도별

제11장 생명과학용 AI 시장 : 컴포넌트별

제12장 생명과학용 AI 시장 : 도입 형태별

제13장 생명과학용 AI 시장 : 최종사용자별

제14장 생명과학용 AI 시장 : 제공별

제15장 생명과학용 AI 시장 : 지역별

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

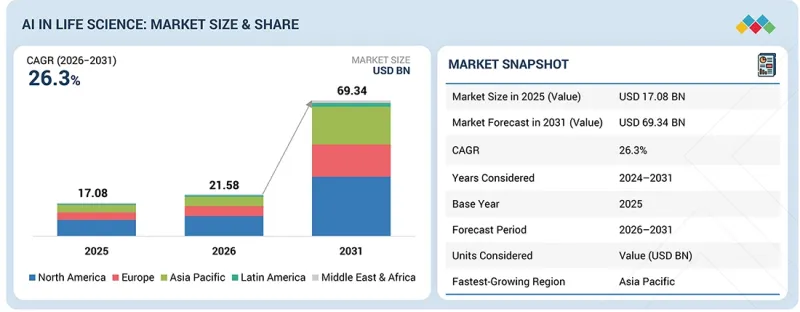

KSA 26.06.09The AI in life science market is projected to reach USD 69.34 billion by 2031, up from USD 21.58 billion in 2026, at a high CAGR of 26.3% over the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Offering, Application, Component, Tools, Deployment, and End User |

| Regions covered | North America, Europe, Asia Pacific, Latin America, and Middle East & Africa |

The growth rate is further fueled by the growing trend toward data-oriented and agentic AI architectures that help life science companies advance from conventional analytics to self-acting systems. These innovations particularly impact clinical trial optimization, real-world evidence collection, and post-market monitoring, as fragmented and vast data sets have limited the efficiency of these applications. In addition, the adoption of cloud-based services with AI technology allows life science companies to consolidate diverse data sources, ranging from medical and genomics data to patient-specific information, to facilitate predictive modeling and fast-track the drug development process. The emergence of AI agents that automate sophisticated tasks, such as literature search, hypothesis formulation, and patient segmentation, also contributes to increased operational efficiency and accelerated innovation cycles. For example, Oracle Corporation (US) released the Oracle Life Sciences AI Data Platform in January 2026, which combines more than 129 million de-identified medical records with generative AI and agentic intelligence solutions to speed up research and clinical trials. In addition, IQVIA Holdings Inc. (US) introduced AI agents in June 2025 to optimize workflows in clinical and commercial operations, including target identification and clinical data analytics.

Based on region, the AI in life science market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America is the dominant region in the global AI in life science market owing to the presence of sophisticated research networks, high levels of digitalization, and considerable investment in innovations in biotechnology and pharma. The region leverages its strengths in terms of synergies between universities, hospitals, and tech companies, helping to implement AI-driven advancements more quickly. Moreover, a positive regulatory environment and rapid adoption of sophisticated analytics in drug discovery and clinical trials have helped to consolidate the region's position as a leader in this market. Europe is the second-largest market in the segment due to the growing interest of governments and companies in AI technology and AI products compliant with data privacy requirements.

Based on offerings, the AI in life science market is divided into end-to-end solutions, niche/point solutions, AI technology, and services. In 2025, end-to-end solutions had the largest market share due to increasing demand for integrated platforms that support data ingestion, model building, validation, and deployment across the entire life sciences value chain. These solutions make the life sciences workflow more efficient and cohesive, from target identification to clinical and commercial levels. Companies in the industry now tend to prefer full-stack AI platforms over stand-alone software for their ability to scale, comply with regulations, and enable collaboration across functions. This shift reflects a broader market trend moving from experimental AI applications toward enterprise-level implementation that requires consistent, repeatable, and auditable processes for research and development and clinical trials. For example, in October 2025, the Italian organization expert.ai launched AI-powered solutions to optimize clinical trial design and regulatory and research workflows. Additionally, in June 2025, ArisGlobal (US) implemented its LifeSphere NavaX AI platform at a leading pharmaceutical company globally, enabling automated analysis of roughly 350,000 safety cases annually.

Based on application, the AI in life science market is divided into clinical applications and non-clinical applications. The clinical applications segment is expected to see the fastest growth in this market. This is attributed to the rise in the use of AI to improve patient experiences, conduct clinical trials more effectively, and adopt precision medicine through real-time data analysis. AI-powered software is helping to improve patient enrollment, trial management, and protocol optimization, thereby reducing trial periods and improving success rates. In addition, the transition toward patient-focused, decentralized clinical trials is driving the adoption of AI-powered software. This trend was reflected in the following development. By March 2026, IQVIA had deployed over 150 AI agents, which were used by 19 of the top 20 pharmaceutical firms. In June 2025, IQVIA Holdings Inc. (US) released AI agents to streamline clinical operations.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 AI IN LIFE SCIENCE MARKET OVERVIEW

- 3.2 AI IN LIFE SCIENCE MARKET, BY APPLICATION & REGION

- 3.3 AI IN LIFE SCIENCE MARKET: REGIONAL SNAPSHOT

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Surging demand for accelerated drug discovery and R&D pipeline optimization

- 4.2.1.2 Growing cross-industry partnerships

- 4.2.1.3 Expanding applications of AI in clinical trial design, patient recruitment, and operational efficiency

- 4.2.1.4 Growing availability of large-scale biomedical datasets and advances in computing infrastructure

- 4.2.1.5 Supportive government policies, funding initiatives, and regulatory frameworks

- 4.2.2 RESTRAINTS

- 4.2.2.1 Data privacy and cybersecurity concerns

- 4.2.2.2 Algorithmic bias and clinician trust deficits

- 4.2.2.3 High implementation costs, technical complexity, and integration challenges with legacy IT systems

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Generative AI and foundation models for de novo drug design

- 4.2.3.2 Rising focus on rare disease treatments

- 4.2.3.3 Growing demand for precision and personalized medicine

- 4.2.3.4 AI integration in academic research institutes and government-backed biomedical innovation programs

- 4.2.4 CHALLENGES

- 4.2.4.1 Low data fragmentation, interoperability deficits

- 4.2.4.2 Talent scarcity and organizational readiness

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL HEALTHCARE IT INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 INDICATIVE PRICE FOR AI IN LIFE SCIENCE MARKET (2025)

- 5.5.2 INDICATIVE PRICE FOR AI IN LIFE SCIENCE MARKET, BY REGION (2025)

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.10 IMPACT OF 2025 US TARIFF - AI IN LIFE SCIENCE MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END USERS

- 5.10.5.1 CRO & CDMO

- 5.10.5.2 Pharmaceutical & biotechnology companies

- 5.10.5.3 Research centers & academic institutes

- 5.10.5.4 Diagnostic companies

6 REGULATORY LANDSCAPE

- 6.1 REGIONAL REGULATIONS AND COMPLIANCE

- 6.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.1.2 NORTH AMERICA

- 6.1.3 EUROPE

- 6.1.4 ASIA PACIFIC

- 6.1.5 MIDDLE EAST & AFRICA

- 6.1.6 LATIN AMERICA

- 6.1.7 INDUSTRY STANDARDS

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 7.1 KEY EMERGING TECHNOLOGIES

- 7.1.1 GRAPH NEURAL NETWORKS

- 7.1.2 COMPUTER VISION

- 7.1.3 PREDICTIVE ANALYTICS

- 7.2 COMPLEMENTARY TECHNOLOGIES

- 7.2.1 NEXT-GENERATION SEQUENCING

- 7.2.2 REAL-WORLD EVIDENCE/REAL-WORLD DATA

- 7.2.3 PERSONALIZATION ENGINES

- 7.3 ADJACENT TECHNOLOGIES

- 7.3.1 CLOUD COMPUTING

- 7.3.2 BLOCKCHAIN

- 7.3.3 BIG DATA & ADVANCED ANALYTICS

- 7.4 TECHNOLOGY/PRODUCT ROADMAP

- 7.5 PATENT ANALYSIS

- 7.5.1 INSIGHTS: JURISDICTION AND TOP APPLICANT ANALYSIS

- 7.6 FUTURE APPLICATIONS

- 7.6.1 AI-DRIVEN DRUG DISCOVERY

- 7.6.2 GENOMIC ANALYSIS

- 7.6.3 PRECISION MEDICINE

- 7.6.4 VIRTUAL DRUG SCREENING

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 INTRODUCTION

- 8.2 DECISION-MAKING PROCESS

- 8.3 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.3.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.3.2 BUYING CRITERIA

- 8.4 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.5 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5.1 UNMET NEEDS

- 8.5.2 END USER EXPECTATIONS

- 8.6 MARKET PROFITABILITY

9 AI IN LIFE SCIENCE MARKET, BY TOOL

- 9.1 INTRODUCTION

- 9.2 MACHINE LEARNING

- 9.2.1 DEEP LEARNING

- 9.2.1.1 Convolutional neural networks

- 9.2.1.1.1 High-sensitivity medical imaging AI across oncology and radiology pathways - key driver

- 9.2.1.2 Recurrent neural networks

- 9.2.1.2.1 Sequential biological data processing drives adoption in clinical and genomic applications

- 9.2.1.3 Generative adversarial networks

- 9.2.1.3.1 Synthetic data generation to overcome life science data scarcity barriers boosts adoption

- 9.2.1.4 Graph neural networks

- 9.2.1.4.1 Graph AI architectures modeling molecular interactions to advance target and pathway discovery

- 9.2.1.5 Others

- 9.2.1.5.1 Transformer and diffusion architectures expanding deep learning frontiers in life sciences

- 9.2.1.1 Convolutional neural networks

- 9.2.2 SUPERVISED LEARNING

- 9.2.2.1 Segment driven by accurate prediction of compound potency and selectivity across diverse chemical series

- 9.2.3 REINFORCEMENT LEARNING

- 9.2.3.1 Optimized drug dosing, trial design, and autonomous laboratory systems to drive segment

- 9.2.4 UNSUPERVISED LEARNING

- 9.2.4.1 Unsupervised AI revealing hidden biological patterns within high-dimensional omics datasets

- 9.2.5 OTHER MACHINE LEARNING TECHNOLOGIES

- 9.2.5.1 Semi-supervised and federated learning overcome data scarcity and privacy constraints

- 9.2.1 DEEP LEARNING

- 9.3 NATURAL LANGUAGE PROCESSING

- 9.3.1 BIOMEDICAL LLMS AND CLINICAL NLP AUTOMATING KNOWLEDGE EXTRACTION FROM UNSTRUCTURED HEALTH DATA

- 9.4 CONTEXT-AWARE PROCESSING AND COMPUTING

- 9.4.1 SEGMENT DRIVEN BY DYNAMIC, PATIENT-SPECIFIC INSIGHTS ACROSS CLINICAL WORKFLOWS

- 9.5 COMPUTER VISION

- 9.5.1 TRANSFORMATION OF PATHOLOGY, DERMATOLOGY, AND DRUG MANUFACTURING INSPECTION PROCESSES - KEY DRIVERS

- 9.6 IMAGE ANALYSIS

- 9.6.1 ACCELERATED DIGITAL PATHOLOGY, LAB IMAGING, AND DOCUMENT PROCESSING TO BOOST ADOPTION

- 9.7 OTHER TOOLS

10 AI IN LIFE SCIENCE MARKET, BY APPLICATION

- 10.1 INTRODUCTION

- 10.2 CLINICAL APPLICATIONS

- 10.2.1 REDUCED DEVELOPMENT TIMELINES AND IMPROVED CLINICAL SUCCESS TO DRIVE SEGMENT

- 10.2.2 DRUG DISCOVERY

- 10.2.2.1 AI-driven target identification transforming biopharma R&D productivity and success rates

- 10.2.3 MEDICAL IMAGING & DIAGNOSTICS

- 10.2.3.1 Accelerating FDA clearances and radiology digitization drives clinical AI imaging adoption

- 10.2.4 CLINICAL TRIALS

- 10.2.4.1 AI-powered trial optimization and decentralized models accelerating patient-centric research

- 10.2.5 PRECISION MEDICINE

- 10.2.5.1 Multi-Omics AI integration enabling individualized therapy selection at population scale

- 10.2.6 OTHER CLINICAL APPLICATIONS

- 10.2.6.1 AI-augmented clinical decision support expanding into pharmacovigilance and rare disease

- 10.3 NON-CLINICAL APPLICATIONS

- 10.3.1 R&D SUPPORT

- 10.3.1.1 AI-enabled literature mining and lab automation multiplying R&D throughput significantly

- 10.3.2 DATA ANALYTICS & REPORTING

- 10.3.2.1 Real-world evidence and AI analytics transforming strategic decision-making across organizations

- 10.3.3 MANUFACTURING & QUALITY ASSURANCE

- 10.3.3.1 Predictive quality AI and continuous manufacturing reduce batch failures and compliance risk

- 10.3.4 REGULATORY AFFAIRS

- 10.3.4.1 FDA and EMA AI guidance catalyzing regulatory submission automation and pharmacovigilance efficiency

- 10.3.1 R&D SUPPORT

11 AI IN LIFE SCIENCE MARKET, BY COMPONENT

- 11.1 INTRODUCTION

- 11.2 SOFTWARE

- 11.2.1 AI SOFTWARE PLATFORMS BECOMING CORE INFRASTRUCTURE FOR LIFE SCIENCE DIGITAL TRANSFORMATION

- 11.3 SERVICE

- 11.3.1 SPECIALIZED AI SERVICES BRIDGING VALIDATION AND COMPLIANCE GAPS ACROSS LIFE SCIENCE ENTERPRISES

12 AI IN LIFE SCIENCE MARKET, BY DEPLOYMENT

- 12.1 INTRODUCTION

- 12.2 CLOUD-BASED SOLUTIONS

- 12.2.1 HYPERSCALE CLOUD INFRASTRUCTURE ACCELERATES LIFE SCIENCE AI SCALABILITY AND COLLABORATIVE RESEARCH

- 12.3 ON-PREMISE SOLUTIONS

- 12.3.1 DATA SOVEREIGNTY AND GXP COMPLIANCE SUSTAIN ON-PREMISE AI DEPLOYMENT ACROSS REGULATED ENVIRONMENTS

- 12.4 HYBRID SOLUTIONS

- 12.4.1 HYBRID ARCHITECTURES BALANCE REGULATORY COMPLIANCE, DATA SECURITY, AND AI SCALABILITY DEMANDS

13 AI IN LIFE SCIENCE MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 CRO & CDMO

- 13.2.1 AI-POWERED CROS & CDMOS COMPETE ON SPEED, QUALITY, AND DATA INTELLIGENCE DIFFERENTIATION

- 13.3 PHARMACEUTICAL COMPANIES

- 13.3.1 AI EMBEDDED ACROSS DISCOVERY, TRIALS, AND COMMERCIAL OPERATIONS BROADLY BY PHARMA LEADERS

- 13.4 BIOTECHNOLOGY COMPANIES

- 13.4.1 AI-NATIVE BIOTECH MODELS COMPRESSING DRUG DISCOVERY TIMELINES FROM YEARS TO MONTHS

- 13.5 DIAGNOSTIC COMPANIES

- 13.5.1 AI-AUGMENTED DIAGNOSTICS ELEVATE SENSITIVITY AND THROUGHPUT ACROSS MOLECULAR AND IMAGING PLATFORMS

- 13.6 ACADEMIC & GOVERNMENT LABORATORIES

- 13.6.1 PUBLIC AI RESEARCH PROGRAMS AND OPEN SCIENCE INITIATIVES BUILD FOUNDATIONAL LIFE SCIENCE INFRASTRUCTURE

- 13.7 OTHER END USERS

14 AI IN LIFE SCIENCE MARKET, BY OFFERING

- 14.1 INTRODUCTION

- 14.2 END-TO-END SOLUTION

- 14.2.1 INTEGRATED AI PLATFORMS COMPRESSING DRUG DEVELOPMENT TIMELINES ACROSS ENTIRE VALUE CHAINS

- 14.3 NICHE/POINT SOLUTIONS

- 14.3.1 DISEASE-SPECIFIC AI TOOLS DELIVER MEASURABLE OUTCOMES IN TARGETED RESEARCH WORKFLOWS

- 14.4 AI TECHNOLOGY

- 14.4.1 FOUNDATION MODELS AND GENERATIVE AI REDEFINE CORE SCIENTIFIC DISCOVERY CAPABILITIES

- 14.5 SERVICES

- 14.5.1 PROFESSIONAL AI SERVICES ENABLE COMPLIANT DEPLOYMENT ACROSS REGULATED LIFE SCIENCE ENVIRONMENTS

15 AI IN LIFE SCIENCE MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Record FDA approvals and federal funding propel AI medical device commercialization

- 15.2.3 CANADA

- 15.2.3.1 Federal AI investment and sovereign compute strategy catalyze life sciences innovation

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 GERMANY

- 15.3.2.1 Prescription digital health app framework propels market

- 15.3.3 FRANCE

- 15.3.3.1 National AI-health data strategy and health data hub anchor data-driven life sciences

- 15.3.4 UK

- 15.3.4.1 NHS Ten-Year Plan positions AI as core infrastructure for national care transformation

- 15.3.5 ITALY

- 15.3.5.1 National recovery plan digitization funding opens new hospital AI adoption pathways

- 15.3.6 SPAIN

- 15.3.6.1 National AI strategy and SNS digitization align life sciences sector with EU AI ambitions

- 15.3.7 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 CHINA

- 15.4.2.1 NMPA high-end device policy and AI standardization body streamline AI commercialization

- 15.4.3 JAPAN

- 15.4.3.1 PMDA adaptive AI framework and medical DX reforms accelerate SaMD commercialization

- 15.4.4 INDIA

- 15.4.4.1 IndiaAI mission and national health data infrastructure enable population-scale AI deployment

- 15.4.5 AUSTRALIA

- 15.4.5.1 My Health Record ecosystem and TGA SaMD pathways underpin AI-ready digital infrastructure

- 15.4.6 SOUTH KOREA

- 15.4.6.1 K-Medtech ecosystem and MFDS AI regulatory guidance propel smart hospital AI adoption

- 15.4.7 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 15.5.2 BRAZIL

- 15.5.2.1 RNDS National Health Network provides digital backbone for AI healthcare integration

- 15.5.3 MEXICO

- 15.5.3.1 IMSS digital transformation and National AI Strategy drive AI integration into public healthcare

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 15.6.2 GCC

- 15.6.3 SAUDI ARABIA

- 15.6.3.1 Vision 2030 health sector transformation program drives AI-enabled care delivery at scale

- 15.6.4 UAE

- 15.6.4.1 Malaffi, NABIDH interoperability and Emirati Genome Programme establish AI-ready data foundation

- 15.6.5 REST OF GCC

- 15.6.5.1 Rising demand for telehealth & virtual care to propel market

- 15.6.6 SOUTH AFRICA

- 15.6.6.1 National health insurance framework and digital health programs catalyze AI market entry

- 15.6.7 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 16.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN AI IN LIFE SCIENCE MARKET

- 16.3 REVENUE ANALYSIS

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- 16.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.5.5.1 Company footprint

- 16.5.5.2 Region footprint

- 16.5.5.3 Offering footprint

- 16.5.5.4 Application footprint

- 16.5.5.5 End user footprint

- 16.5.5.6 Tools footprint

- 16.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.6.1 PROGRESSIVE COMPANIES

- 16.6.2 RESPONSIVE COMPANIES

- 16.6.3 DYNAMIC COMPANIES

- 16.6.4 STARTING BLOCKS

- 16.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.6.5.1 Detailed list of key startups/SMEs

- 16.6.5.2 Competitive benchmarking of startups/SMEs

- 16.7 VALUATION & FINANCIAL METRICS

- 16.7.1 FINANCIAL METRICS

- 16.7.2 COMPANY VALUATION

- 16.8 BRAND/SOFTWARE COMPARISON

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT/SERVICE LAUNCHES & APPROVALS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 NVIDIA CORPORATION

- 17.1.1.1 Business overview

- 17.1.1.2 Products/Solutions offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Product launches & enhancements

- 17.1.1.3.2 Deals

- 17.1.1.3.3 Other developments

- 17.1.1.4 MnM view

- 17.1.1.4.1 Key strengths

- 17.1.1.4.2 Strategic choices

- 17.1.1.4.3 Weaknesses and competitive threats

- 17.1.2 ILLUMINA, INC.

- 17.1.2.1 Business overview

- 17.1.2.2 Products/Solutions offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches & enhancements

- 17.1.2.3.2 Deals

- 17.1.2.4 MnM view

- 17.1.2.4.1 Key strengths

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses and competitive threats

- 17.1.3 TEMPUS AI, INC.

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Deals

- 17.1.3.3.2 Other developments

- 17.1.4 RECURSION

- 17.1.4.1 Business overview

- 17.1.4.2 Products/Solutions offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Product launches & enhancements

- 17.1.4.3.2 Deals

- 17.1.4.3.3 Expansions

- 17.1.4.4 MnM view

- 17.1.4.4.1 Key strengths

- 17.1.4.4.2 Strategic choices

- 17.1.4.4.3 Weaknesses and competitive threats

- 17.1.5 DASSAULT SYSTEMES SE

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 Recent developments

- 17.1.5.3.1 Product launches & enhancements

- 17.1.5.3.2 Deals

- 17.1.5.3.3 Other developments

- 17.1.6 SCHRODINGER, INC.

- 17.1.6.1 Business overview

- 17.1.6.2 Products/Solutions offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.6.3.2 Other Developments

- 17.1.7 DATA4CURE, INC.

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches & enhancements

- 17.1.7.3.2 Other developments

- 17.1.8 MICROSOFT CORPORATION

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.8.3 Recent developments

- 17.1.8.3.1 Product launches & enhancements

- 17.1.8.3.2 Deals

- 17.1.8.3.3 Other developments

- 17.1.9 INSILICO MEDICINE

- 17.1.9.1 Business overview

- 17.1.9.2 Products/Services offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Product launches & enhancements

- 17.1.9.3.2 Deals

- 17.1.9.3.3 Other developments

- 17.1.9.3.4 Expansions

- 17.1.10 EUROFINS DISCOVERY

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Product launches & approvals

- 17.1.10.3.2 Deals

- 17.1.11 BENEVOLENTAI LIMITED

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 OWKIN

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product launches & approvals

- 17.1.12.3.2 Deals

- 17.1.12.3.3 Other developments

- 17.1.13 PATHAI

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.13.3 Recent developments

- 17.1.13.3.1 Product launches & approvals

- 17.1.13.3.2 Deals

- 17.1.14 AIDOC MEDICAL LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Product launches & approvals

- 17.1.14.3.2 Other developments

- 17.1.15 QURE.AI

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product launches & approvals

- 17.1.16 DEEP GENOMICS

- 17.1.16.1 Business overview

- 17.1.16.2 Products offered

- 17.1.16.3 Recent developments

- 17.1.16.3.1 Expansions

- 17.1.17 SOPHIA GENETICS SA

- 17.1.17.1 Business overview

- 17.1.17.2 Products offered

- 17.1.17.3 Recent developments

- 17.1.17.3.1 Product launches & enhancements

- 17.1.17.3.2 Deals

- 17.1.18 UNLEARN.AI

- 17.1.18.1 Business overview

- 17.1.18.2 Products offered

- 17.1.18.3 Recent developments

- 17.1.18.3.1 Deals

- 17.1.19 VERGE GENOMICS

- 17.1.19.1 Business overview

- 17.1.19.2 Products offered

- 17.1.19.3 Recent developments

- 17.1.19.3.1 Deals

- 17.1.1 NVIDIA CORPORATION

- 17.2 OTHER PLAYERS

- 17.2.1 SYNTHIO LABS LTD

- 17.2.2 BIOPTIMUS

- 17.2.3 KARYON BIO

- 17.2.4 COUNTERFORCE HEALTH

- 17.2.5 PROMISE BIO

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH APPROACH

- 18.1.1 SECONDARY RESEARCH

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY RESEARCH

- 18.1.2.1 Primary sources

- 18.1.2.2 Key data from primary sources

- 18.1.2.3 Breakdown of primary interviews

- 18.1.2.4 Insights from primary experts

- 18.1.1 SECONDARY RESEARCH

- 18.2 RESEARCH METHODOLOGY DESIGN

- 18.3 MARKET SIZE ESTIMATION

- 18.4 DATA TRIANGULATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RESEARCH LIMITATIONS

- 18.6.1 METHODOLOGY-RELATED

- 18.6.2 SCOPE-RELATED

- 18.7 RISK ASSESSMENT

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS:

- 19.5 AUTHOR DETAILS