|

시장보고서

상품코드

2055594

항공기 탑재형 ISR 시장 : 플랫폼별, 솔루션별, 용도별, 구성부품별, 최종사용자별, 지역별 - 예측(-2031년)Airborne ISR Market by Solution, Application (Search & Rescue, Border & Maritime Patrol, Target Acquisition), Component (Sensor, RF Module, Antenna, Optical Assemblies), End User, Platform, and Region- Global Forecast to 2031 |

||||||

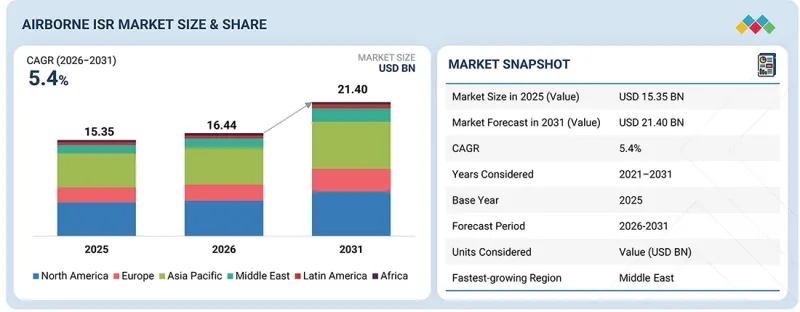

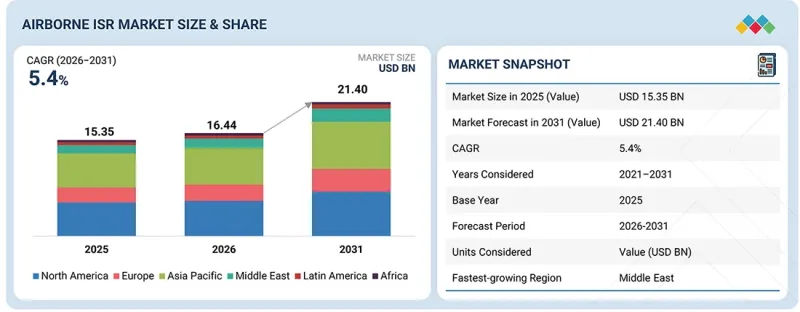

항공기 탑재형 ISR 시장 규모는 예측 기간 중에 CAGR5.4%로 확대되어 2026년 164억 4,000만 달러에서 2031년에는 214억 달러에 이를 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021년-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 플랫폼별, 솔루션별, 용도별, 구성부품별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 |

현대 방위군은 상황 인식 능력 향상, 동적 표적 추적 능력 강화, 그리고 복잡한 작전 환경에서의 신속한 의사결정을 지원하기 위해 항공기 탑재형 ISR 플랫폼 도입을 점점 더 확대되고 있습니다. 이에 따라 항공기 탑재형 ISR 시장은 성장하고 있습니다.

“고정익기 부문은 항공기 탑재형 ISR 분야에서 가장 큰 플랫폼입니다. '

플랫폼별로 보면, 2026년에는 고정익기 부문이 가장 큰 시장 점유율을 차지할 것으로 추정됩니다. 이들은 ISR 임무에 널리 사용되며, 특히 광활한 육지나 해역을 감시하면서 다양한 센서에서 수집된 데이터를 실시간으로 통합하는 임무를 수행하는 운용자에게 유용합니다. 비즈니스 제트기, 터보프롭기 및 군용 플랫폼을 ISR(정보·감시·정찰) 능력으로 전환하는 추세가 이 분야의 성장을 크게 견인하고 있습니다. 이러한 전환을 통해 방위·치안 기관은 레이더, 전기광학/적외선(EO/IR) 센서, 신호정보(SIGINT) 페이로드, 첨단 임무 콘솔, 보안 통신, 견고한 데이터 링크 등 첨단 시스템을 원활하게 통합할 수 있게 되어, 완전히 새로운 기체를 개발할 필요가 없어집니다.

“예측 기간 동안 군 및 방위 분야의 최종 사용자 부문은 가장 빠르게 성장할 것으로 전망됩니다.” '

최종 사용자별로 보면, 항공기 탑재형 ISR 시장에서 군 및 방위 부문은 국토안보 부문보다 더 빠른 속도로 성장할 것으로 전망됩니다. 현대 방위 작전에서는 위협 감지, 이동 추적, 신호 수집, 해상 감시에 뛰어난 고도의 항공기 탑재 시스템이 요구되며, 동시에 지휘관과의 거의 실시간에 가까운 정보 공유도 필요로 하고 있습니다. 이러한 운용상의 요건은 ISR 기능을 통합한 플랫폼에 대한 수요를 촉진하고 있으며, 여기에는 ISR 기능이 강화된 항공기, 무인항공기(UAV), 첨단 임무 컴퓨터, 첨단 레이더 시스템, EO/IR 페이로드, SIGINT 시스템 및 보안 통신 네트워크 등이 포함됩니다.

“중동은 예측 기간 동안 가장 빠르게 성장할 지역으로 전망됩니다. '

중동은 항공기 탑재형 ISR 분야에서 가장 빠르게 성장하고 있는 시장입니다. 미사일 공격, 드론 침입, 해양 안보 문제, 국경을 넘는 침략 등 다양한 위협으로부터 중요한 에너지 인프라, 해상 항만, 사막 주변 지역, 홍해 항로, 걸프만 항행 회랑 및 고가치 군사 시설을 보호해야 할 필요성이 높아짐에 따라, 이 지역에서의 고도화된 방위 능력에 대한 수요가 크게 확대되고 있습니다. 이 지역의 많은 국가들은 최첨단 방위 시스템을 도입할 뿐만 아니라, 무인항공기(UAV), 첨단 센서, 전기광학 시스템 및 종합적인 임무 통합 솔루션을 전문으로 생산하는 자국의 방위 산업을 구축하고 있습니다. 이러한 변화로 인해 중고도 장거리(MALE) 무인기, 전술 드론, 전기광학/적외선(EO/IR) 시스템, 레이더 기술, 전자정보 수집 페이로드, 보안 데이터 링크, 운용 소프트웨어는 물론, 현지 훈련 및 유지보수 체계에 대한 수요가 증가하고 있습니다.

조사 범위:

본 시장 조사는 다양한 부문 및 하위 부문에 걸친 항공기 탑재형 ISR 시장을 대상으로 합니다. 본 조사는 지역별로 이 시장 규모와 성장 가능성을 추정하는 것을 목적으로 합니다. 또한, 시장 내 주요 기업에 대한 상세한 경쟁 분석, 기업 프로파일, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 채택된 주요 시장 전략에 대해서도 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

본 보고서는 시장 선도 기업 및 신규 진출기업에게 항공기 탑재형 ISR 시장 전체 매출에 대한 가장 정확한 추정치를 제공합니다. 또한, 이해관계자들이 경쟁 구도를 파악하고 자사의 비즈니스를 더 유리한 위치에 두며, 적절한 시장 진출 전략을 수립하는 데 필요한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움을 주며, 주요 시장 성장 촉진요인, 시장 성장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서는 다음 사항에 대한 인사이트를 제공합니다.

- 시장 성장 촉진요인(지속적인 감시 요건, 기존 항공기 플랫폼의 ISR 업그레이드, 무인 및 유인 선택형 플랫폼에서의 ISR 커버리지 확대), 억제요인(높은 조달 비용 및 수명 주기 비용, 수출 규제 및 기술 이전 제한, 숙련된 ISR 운영자 및 분석가 부족), 기회(AI를 활용한 데이터 분석, ISR-as-a-Service의 등장, 저 SWaP 페이로드 개발), 과제(실시간 데이터 관리의 과제, 전자기파·사이버 환경에서경쟁 구도)

- 시장 침투: 시장을 선도하는 주요 기업들이 제공하는 항공기 탑재형 ISR에 관한 종합적인 정보

- 제품 개발/혁신 : 항공기 탑재형 ISR 시장의 향후 기술, 연구 개발 활동 및 제품 출시에 관한 상세한 인사이트

- 시장 개발: 다양한 지역의 수익성 높은 시장에 대한 종합적인 정보

- 시장의 다각화 : 항공기 탑재형 ISR 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : 항공기 탑재형 ISR 시장의 주요 기업별 시장 점유율, 성장 전략, 제품 및 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 현황과 구매 행동

제9장 항공기 탑재형 ISR 시장(플랫폼별)

제10장 항공기 탑재형 ISR 시장(솔루션별)

제11장 항공기 탑재형 ISR 시장(용도별)

제12장 항공기 탑재형 ISR 시장(구성부품별)

제13장 항공기 탑재형 ISR 시장(최종사용자별)

제14장 항공기 탑재형 ISR 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

LSH 26.06.19The airborne ISR market is projected to grow from USD 16.44 billion in 2026 to USD 21.40 billion by 2031, at a CAGR of 5.4% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | By Solution, Application, Component and Region |

| Regions covered | North America, Europe, APAC, RoW |

Modern defense forces are increasingly incorporating airborne ISR platforms to improve situational awareness, enhance tracking of dynamic targets, and support faster decision-making in complex operational environments. This is resulting in the growth of the airborne ISR market.

"The fixed-wing aircraft segment is the largest platform for airborne ISR."

Based on platform, the fixed-wing aircraft segment is estimated to account for the largest market share in 2026. They are widely used for ISR missions and particularly advantageous for operators tasked with overseeing vast terrestrial or maritime regions while synthesizing data from various sensors in real-time. The trend of converting business jets, turboprop aircraft, and military platforms into ISR capabilities is significantly driving growth in this sector. This conversion enables defense and security organizations to seamlessly integrate advanced systems, including radar, electro-optical/infrared (EO/IR) sensors, signals intelligence (SIGINT) payloads, sophisticated mission consoles, secure communications, and robust data links, eliminating the necessity for developing entirely new airframes.

"The military & defense end user segment is poised to be the faster-growing segment during the forecast period."

The military & defense segment is projected to grow at a faster rate than the homeland security segment in the airborne ISR market by end user. Modern defense operations necessitate advanced airborne systems proficient in threat detection, movement tracking, signals collection, and maritime surveillance, all while facilitating near real-time intelligence sharing with command personnel. This operational requirement is propelling the demand for platforms integrated with ISR capabilities, including ISR-enhanced aircraft, UAVs, advanced mission computers, sophisticated radar systems, EO/IR payloads, SIGINT systems, and secure communication networks.

"The Middle East is projected to be the fastest-growing region during the forecast period."

The Middle East is the fastest-growing market for airborne ISR. The imperative to secure critical energy infrastructure, maritime ports, desert peripheries, Red Sea shipping routes, Gulf navigation corridors, and high-value military installations against a spectrum of threats, including missile strikes, drone incursions, maritime security challenges, and cross-border aggressions, is significantly enhancing the demand for advanced defense capabilities in this region. Many countries in the region are not only acquiring cutting-edge defense systems but are also establishing indigenous defense industries that specialize in the production of UAVs, sophisticated sensors, electro-optical systems, and comprehensive mission integration solutions. This shift is driving the demand for Medium-Altitude Long-Endurance (MALE) UAVs, tactical drones, electro-optical/infrared (EO/IR) systems, radar technologies, electronic intelligence payloads, secure datalinks, operational software, as well as local training and maintenance frameworks.

The breakdown of profiles for primary participants in the airborne ISR market is provided below:

- By Company Type: Tier 1 - 55%, Tier 2 - 25%, and Tier 3 - 20%

- By Designation: C-Level - 75%, Manager-Level - 25%

- By Region: North America - 20%, Europe - 25%, Asia Pacific - 30%, Middle East - 10%, Rest of the World - 15%

Research Coverage:

This market study covers the airborne ISR market across various segments and subsegments. It aims to estimate the size and growth potential of this market across different regions. This study also includes an in-depth competitive analysis of the key players in the market, their company profiles, key observations related to their products and business offerings, recent developments, and key market strategies they adopted.

Reasons to Buy This Report:

The report will help the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall airborne ISR market. It will also help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the market pulse and will provide information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Market drivers (continuous surveillance requirements, ISR upgrades across existing airborne platforms, and expansion of ISR coverage on unmanned and optionally manned platforms), restraints (high procurement and lifecycle costs, export controls and technology transfer restrictions, and shortage of skilled ISR operators and analysts), opportunities (AI-enabled exploitation, advent of ISR-as-a-Service, and low-SWaP payload development), challenges (Real-time data management challenges and contested electromagnetic and cyber environments)

- Market Penetration: Comprehensive information on airborne ISR offered by the top players in the market

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the airborne ISR market

- Market Development: Comprehensive information about lucrative markets across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the airborne ISR market

- Competitive Assessment: In-depth assessment of market share, growth strategies, products, and manufacturing capabilities of leading players in the airborne ISR market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AIRBORNE ISR MARKET

- 3.2 AIRBORNE ISR MARKET, BY END USER

- 3.3 AIRBORNE ISR SERVICE MARKET, BY TYPE

- 3.4 AIRBORNE ISR MARKET, BY FIXED-WING AIRCRAFT TYPE

- 3.5 AIRBORNE ISR MARKET, BY UNMANNED AERIAL VEHICLE TYPE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Continuous surveillance requirements

- 4.2.1.2 ISR upgrades across existing airborne platforms

- 4.2.1.3 Expansion of ISR coverage on unmanned and optionally manned platforms

- 4.2.2 RESTRAINTS

- 4.2.2.1 High procurement and lifecycle costs

- 4.2.2.2 Export controls and technology transfer restrictions

- 4.2.2.3 Shortage of skilled ISR operators and analysts

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 AI-enabled exploitation

- 4.2.3.2 Advent of ISR-as-a-Service

- 4.2.3.3 Low-SWaP payload development

- 4.2.4 CHALLENGES

- 4.2.4.1 Real-time data management challenges

- 4.2.4.2 Contested electromagnetic and cyber environments

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 MISSION-READY ISR INTEGRATION PACKAGES REDUCING AIRCRAFT CONVERSION TIMELINES

- 4.3.2 AFFORDABLE WIDE-AREA SURVEILLANCE OPENING ADOPTION AMONG MEDIUM-BUDGET USERS

- 4.3.3 SOVEREIGN ISR DATA AND MISSION SOFTWARE CONTROL BECOMING BUYER PRIORITY

- 4.3.4 SIMPLER SUSTAINMENT AND FIELD SUPPORT MODELS IMPROVING MISSION AVAILABILITY

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 UNMANNED SYSTEM MARKET CREATING DEMAND FOR INTEGRATED ISR PAYLOAD SOLUTIONS

- 4.4.2 AI, DATA ANALYTICS, AND MISSION SOFTWARE MARKET SUPPORTING FASTER INTELLIGENCE EXPLOITATION

- 4.4.3 SECURE COMMUNICATIONS AND TACTICAL NETWORKING MARKET ENABLING REAL-TIME ISR SHARING

- 4.4.4 DEFENSE MRO AND MISSION SYSTEM INTEGRATION MARKET EXPANDING LIFECYCLE REVENUE

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 ECOSYSTEM ANALYSIS

- 5.1.1 PLATFORM AND SYSTEM INTEGRATORS

- 5.1.2 SENSOR AND MISSION PAYLOAD PROVIDERS

- 5.1.3 SOFTWARE, COMMUNICATIONS, AND DATA PROCESSING PROVIDERS

- 5.1.4 END USERS

- 5.2 VALUE CHAIN ANALYSIS

- 5.2.1 RESEARCH AND DEVELOPMENT (~25%)

- 5.2.2 SENSOR AND COMPONENT DEVELOPMENT (~15%)

- 5.2.3 PAYLOAD AND SYSTEM MANUFACTURING (~25%)

- 5.2.4 PLATFORM INTEGRATION AND TESTING (~20%)

- 5.2.5 LIFECYCLE SUPPORT AND SERVICES (~15%)

- 5.3 TRADE ANALYSIS

- 5.3.1 IMPORT SCENARIO (HS CODE 902750)

- 5.3.2 EXPORT SCENARIO (HS CODE 902750)

- 5.4 CASE STUDY ANALYSIS

- 5.4.1 US NAVY P-8A POSEIDON MARITIME ISR&T UPGRADE

- 5.4.2 US COAST GUARD CONTRACTOR-OPERATED UAS ISR SERVICES

- 5.4.3 NATO BALTIC SENTRY FOR UNDERSEA INFRASTRUCTURE MONITORING

- 5.4.4 CBP MQ-9 UAS FOR BORDER AND MARITIME DOMAIN AWARENESS

- 5.5 KEY CONFERENCES AND EVENTS, 2026

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 TOTAL COST OF OWNERSHIP

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 OPERATIONAL DATA

- 5.10 PRICING ANALYSIS

- 5.10.1 INDICATIVE PRICING ANALYSIS OF AIRBORNE ISR PLATFORMS, BY SOLUTION, 2025

- 5.10.2 INDICATIVE PRICING ANALYSIS OF AIRBORNE ISR PLATFORMS, BY SYSTEM, 2025

- 5.11 MACROECONOMIC OUTLOOK

- 5.12 GDP TRENDS AND FORECAST

- 5.12.1 TRENDS IN GLOBAL AIRBORNE ISR INDUSTRY

- 5.12.2 TRENDS IN GLOBAL AEROSPACE AND DEFENSE INDUSTRY

- 5.13 BILL OF MATERIALS

- 5.14 BUSINESS MODELS

- 5.14.1 MISSION SYSTEM INTEGRATION

- 5.14.2 ISR PAYLOAD AND SENSOR PRODUCT SALES

- 5.14.3 ISR-AS-A-SERVICE/COCO

- 5.14.4 LIFECYCLE SUPPORT AND UPGRADE CONTRACTS

- 5.14.5 SOFTWARE AND DATA EXPLOITATION

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ELECTRO-OPTICAL AND INFRARED PAYLOADS

- 6.1.2 AIRBORNE SURVEILLANCE RADARS

- 6.1.3 SIGNALS INTELLIGENCE SYSTEMS

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AI, EDGE PROCESSING, AND SENSOR FUSION

- 6.2.2 TACTICAL DATA LINKS, SATCOM, AND ISR VIDEO LINKS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 C4ISR AND BATTLE MANAGEMENT NETWORKS

- 6.3.2 ELECTRONIC WARFARE

- 6.4 TECHNOLOGY ROADMAP

- 6.5 IMPACT OF AI/ GEN AI

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 BEST PRACTICES

- 6.5.3 CASE STUDIES OF AI IMPLEMENTATION

- 6.5.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.5 CLIENTS' READINESS TO ADOPT GEN AI

- 6.6 PATENT ANALYSIS

- 6.7 FUTURE APPLICATIONS

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 PALANTIR TECHNOLOGIES: MAVEN SMART SYSTEM

- 6.8.2 GENERAL ATOMICS AERONAUTICAL SYSTEMS, INC.: SMART SENSOR ISR PROTOTYPE

- 6.8.3 ANDURIL INDUSTRIES: IRIS AIRBORNE AUTONOMOUS SENSOR FAMILY

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

9 AIRBORNE ISR MARKET, BY PLATFORM

- 9.1 INTRODUCTION

- 9.2 FIXED-WING AIRCRAFT

- 9.2.1 EXPANDING LONG-RANGE ISR PAYLOAD INTEGRATION TO DRIVE MARKET

- 9.2.2 SPECIAL MISSION AIRCRAFT

- 9.2.3 MARITIME PATROL AIRCRAFT

- 9.2.4 BORDER & HOMELAND SURVEILLANCE AIRCRAFT

- 9.2.5 ISR-MODIFIED TRANSPORT & UTILITY AIRCRAFT

- 9.3 ROTARY-WING AIRCRAFT

- 9.3.1 COMBINING CLOSE-RANGE SURVEILLANCE WITH MISSION RESPONSE TO DRIVE MARKET

- 9.3.2 MILITARY HELICOPTERS

- 9.3.3 COAST GUARD & MARITIME HELICOPTERS

- 9.3.4 SPECIAL OPERATIONS HELICOPTERS

- 9.4 UNMANNED AERIAL VEHICLES

- 9.4.1 EXTENDING PERSISTENT SURVEILLANCE WITH LOWER CREW EXPOSURE TO DRIVE MARKET

- 9.4.2 SMALL UNMANNED AERIAL VEHICLES

- 9.4.3 TACTICAL UNMANNED AERIAL VEHICLES

- 9.4.4 STRATEGIC UNMANNED AERIAL VEHICLES

- 9.4.4.1 MALE

- 9.4.4.2 HALE

10 AIRBORNE ISR MARKET, BY SOLUTION

- 10.1 INTRODUCTION

- 10.2 SYSTEMS

- 10.2.1 UPGRADING AIRBORNE PLATFORMS WITH MULTI-SENSOR MISSION PAYLOADS TO DRIVE MARKET

- 10.2.2 EO/IR GIMBAL & TURRET PAYLOADS

- 10.2.2.1 Small/Compact EO/IR gimbals (6-10 inches)

- 10.2.2.2 Medium EO/IR gimbals & turrets (11-15 inches)

- 10.2.2.3 Large/Long-range EO/IR turrets (>15 inches)

- 10.2.3 RADAR SURVEILLANCE SYSTEMS

- 10.2.3.1 Synthetic aperture radar

- 10.2.3.2 Ground moving target indicator radar

- 10.2.3.3 Maritime surveillance radar

- 10.2.3.4 Airborne search & multi-mode surveillance radar

- 10.2.4 SIGNALS INTELLIGENCE SYSTEMS

- 10.2.4.1 Communications intelligence systems

- 10.2.4.2 Electronic intelligence systems

- 10.2.4.3 Electronic support measures

- 10.2.4.4 RF detection & geo-location systems

- 10.3 SOFTWARE

- 10.3.1 TURNING SENSOR DATA INTO USABLE MISSION INTELLIGENCE TO DRIVE MARKET

- 10.3.2 SENSOR CONTROL & PAYLOAD MANAGEMENT SOFTWARE

- 10.3.2.1 Gimbal control

- 10.3.2.2 Sensor mode management

- 10.3.2.3 Payload health monitoring

- 10.3.2.4 Mission system interface

- 10.3.3 AI-BASED ANALYTICS & AUTO-TRACKING SOFTWARE

- 10.3.3.1 Automatic target detection

- 10.3.3.2 Automatic target tracking

- 10.3.3.3 Object classification

- 10.3.3.4 Moving target indication in video

- 10.3.4 TARGETING & GEO-LOCATION SOFTWARE

- 10.3.4.1 Target coordinate generation

- 10.3.4.2 Laser designation control

- 10.3.4.3 Range & bearing calculation

- 10.3.4.4 Sensor-to-Shooter data support

- 10.3.5 MISSION MANAGEMENT & VIDEO EXPLORATION SOFTWARE

- 10.3.5.1 Mission planning & sensor tasking

- 10.3.5.2 Video exploitation & annotation

- 10.3.5.3 ISR data management

- 10.3.5.4 Command & control integration

- 10.4 SERVICES

- 10.4.1 KEEPING ISR FLEETS MISSION-READY THROUGH INTEGRATION AND LIFECYCLE SUPPORT TO DRIVE MARKET

- 10.4.2 ISR-AS-A-SERVICE

- 10.4.3 INTEGRATION & INSTALLATION

- 10.4.4 MAINTENANCE, REPAIR, & OVERHAUL

- 10.4.5 TRAINING & SIMULATION

11 AIRBORNE ISR MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 SEARCH & RESCUE OPERATIONS

- 11.2.1 REDUCING SEARCH TIME IN COMPLEX RESCUE MISSIONS TO DRIVE MARKET

- 11.3 BORDER & MARITIME PATROL

- 11.3.1 IMPROVING WIDE-AREA MONITORING OF NON-COOPERATIVE ACTIVITY TO DRIVE MARKET

- 11.4 TARGET ACQUISITION & TRACKING

- 11.4.1 SENSOR-LED TARGET CONFIRMATION TO DRIVE MARKET

- 11.5 OTHER APPLICATIONS

12 AIRBORNE ISR MARKET, BY COMPONENT

- 12.1 INTRODUCTION

- 12.2 SENSOR & RECEIVER MODULES

- 12.2.1 ENHANCING DETECTION ACROSS DAY, NIGHT, WEATHER, AND SIGNAL ENVIRONMENTS TO DRIVE MARKET

- 12.2.2 DAYLIGHT ELECTRO-OPTICAL SENSORS

- 12.2.3 INFRARED SENSORS

- 12.2.4 LOW-LIGHT SENSORS

- 12.2.5 SWIR & MULTISPECTRAL SENSORS

- 12.2.6 RADAR RECEIVERS

- 12.2.7 SIGNALS INTELLIGENCE RECEIVERS

- 12.3 LASER & TARGETING MODULES

- 12.3.1 STRENGTHENING TARGET CONFIRMATION AND PRECISION MISSION SUPPORT TO DRIVE MARKET

- 12.3.2 LASER RANGEFINDERS

- 12.3.3 LASER POINTERS/ILLUMINATORS

- 12.3.4 LASER DESIGNATORS

- 12.4 STABILIZATION, CONTROL, & PROCESSING MODULES

- 12.4.1 CONVERTING RAW SENSOR INPUTS INTO STEADY AND USABLE MISSION INTELLIGENCE TO DRIVE MARKET

- 12.4.2 GIMBAL STABILIZATION UNITS

- 12.4.3 INERTIAL MEASUREMENT & LINE-OF-SIGHT CONTROL UNITS

- 12.4.4 PAYLOAD CONTROL UNITS

- 12.4.5 ONBOARD VIDEO PROCESSING HARDWARE

- 12.5 OPTICAL ASSEMBLIES

- 12.5.1 FOCUS ON ENHANCING IMAGE CLARITY AND SENSOR PERFORMANCE TO DRIVE MARKET

- 12.6 ANTENNAS

- 12.6.1 RELIABLE ISR DATA TRANSFER ACROSS AIRBORNE AND GROUND NETWORKS TO DRIVE MARKET

- 12.7 RF MODULES

- 12.7.1 EXPANDING ELECTRONIC SENSING AND SECURE COMMUNICATION CAPABILITY TO DRIVE MARKET

- 12.8 OTHER COMPONENTS

13 AIRBORNE ISR MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 MILITARY & DEFENSE

- 13.2.1 IMPROVING MISSION AWARENESS ACROSS CONTESTED OPERATING AREAS TO DRIVE MARKET

- 13.3 HOMELAND SECURITY

- 13.3.1 NEED FOR FASTER INCIDENT VERIFICATION AND BETTER COORDINATION BETWEEN AIRBORNE ASSETS TO DRIVE MARKET

14 AIRBORNE ISR MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Deep-sensing modernization and domestic ISR integration to drive market

- 14.2.2 CANADA

- 14.2.2.1 Arctic surveillance and multi-role maritime ISR expansion to drive market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Certified uncrewed ISR operations and NATO-focused surveillance modernization to drive market

- 14.3.2 GERMANY

- 14.3.2.1 SIGINT renewal and NATO eastern-flank surveillance to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Sovereign electronic intelligence and overseas maritime surveillance to drive market

- 14.3.4 ITALY

- 14.3.4.1 Multi-mission G550 fleet expansion and Mediterranean surveillance needs to drive market

- 14.3.5 SPAIN

- 14.3.5.1 Sovereign SIGINT development and maritime surveillance fleet renewal to drive market

- 14.3.6 POLAND

- 14.3.6.1 Eastern-flank threat monitoring and drone-based ISR expansion to drive market

- 14.3.7 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Western Pacific surveillance and indigenous high-end UAV development to drive market

- 14.4.2 JAPAN

- 14.4.2.1 Island-chain surveillance and uncrewed maritime ISR expansion to drive market

- 14.4.3 INDIA

- 14.4.3.1 Indian Ocean surveillance, border intelligence, and indigenous ISR modernization to drive market

- 14.4.4 SOUTH KOREA

- 14.4.4.1 North Korea threat monitoring and networked airborne surveillance to drive market

- 14.4.5 AUSTRALIA

- 14.4.5.1 Indo-Pacific maritime surveillance and ISR expansion to drive market

- 14.4.6 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 MIDDLE EAST

- 14.5.1 GCC

- 14.5.1.1 UAE

- 14.5.1.1.1 Gulf maritime security and local unmanned ISR production to drive market

- 14.5.1.2 Saudi Arabia

- 14.5.1.2.1 Defense localization and long-endurance UAV ISR expansion to drive market

- 14.5.1.1 UAE

- 14.5.2 ISRAEL

- 14.5.2.1 Multi-front threat monitoring and domestic ISR sensor production to market

- 14.5.3 TURKEY

- 14.5.3.1 Domestic UAV scale-up and cross-border ISR requirements to drive market

- 14.5.4 REST OF MIDDLE EAST

- 14.5.1 GCC

- 14.6 LATIN AMERICA

- 14.6.1 BRAZIL

- 14.6.1.1 Amazon border monitoring and C-390 maritime ISR development to drive market

- 14.6.2 MEXICO

- 14.6.2.1 Border security, anti-cartel surveillance, and domestic drone development to drive market

- 14.6.3 REST OF LATIN AMERICA

- 14.6.1 BRAZIL

- 14.7 AFRICA

- 14.7.1 SOUTH AFRICA

- 14.7.1.1 Border protection, maritime security, and local UAV capability to drive market

- 14.7.2 NIGERIA

- 14.7.2.1 Counter-insurgency surveillance and Gulf of Guinea security to drive market

- 14.7.3 REST OF AFRICA

- 14.7.1 SOUTH AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2021-2025

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 BRAND/PRODUCT COMPARISON

- 15.6 COMPANY VALUATION AND FINANCIAL METRICS

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Solution footprint

- 15.7.5.4 Platform footprint

- 15.7.5.5 End user footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING

- 15.8.5.1 List of startups/SMEs

- 15.8.5.2 Competitive benchmarking of startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 OTHER DEVELOPMENTS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 RTX

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Other developments

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 L3HARRIS TECHNOLOGIES, INC.

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.3.2 Other developments

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 LEONARDO DRS

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 THALES

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Deals

- 16.1.4.3.2 Other developments

- 16.1.4.4 MnM view

- 16.1.4.4.1 Right to win

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 NORTHROP GRUMMAN

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Other developments

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 BAE SYSTEMS

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Deals

- 16.1.6.3.2 Other developments

- 16.1.7 RHEINMETALL AG

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Other developments

- 16.1.8 GENERAL DYNAMICS CORPORATION

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.9 ELBIT SYSTEMS LTD.

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Other developments

- 16.1.10 GENERAL ATOMICS AERONAUTICAL SYSTEMS, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Deals

- 16.1.10.3.2 Other developments

- 16.1.11 TELEDYNE FLIR DEFENSE INC.

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Other developments

- 16.1.12 LOCKHEED MARTIN CORPORATION

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Deals

- 16.1.12.3.2 Other developments

- 16.1.13 RAFAEL ADVANCED DEFENSE SYSTEMS LTD.

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.14 SAAB AB

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Deals

- 16.1.14.3.2 Other developments

- 16.1.15 HENSOLDT AG

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Deals

- 16.1.15.3.2 Other developments

- 16.1.16 ASELSAN A.S.

- 16.1.16.1 Business overview

- 16.1.16.2 Products offered

- 16.1.16.3 Recent developments

- 16.1.16.3.1 Product launches

- 16.1.16.3.2 Deals

- 16.1.16.3.3 Other developments

- 16.1.17 ISRAEL AEROSPACE INDUSTRIES LTD.

- 16.1.17.1 Business overview

- 16.1.17.2 Products offered

- 16.1.17.3 Recent developments

- 16.1.17.3.1 Deals

- 16.1.17.3.2 Other developments

- 16.1.18 SAFRAN

- 16.1.18.1 Business overview

- 16.1.18.2 Products offered

- 16.1.18.3 Recent developments

- 16.1.18.3.1 Deals

- 16.1.18.3.2 Other developments

- 16.1.1 RTX

- 16.2 OTHER PLAYERS

- 16.2.1 OCTOPUS ISR SYSTEMS

- 16.2.2 TRAKKA SYSTEMS

- 16.2.3 BHARAT ELECTRONICS LIMITED

- 16.2.4 TATA ADVANCED SYSTEMS LIMITED

- 16.2.5 KAPPA OPTRONICS GMBH

- 16.2.6 DELOPT

- 16.2.7 ENORD

- 16.2.8 PAL AEROSPACE

- 16.2.9 SCHIEBEL CORPORATION

- 16.2.10 PERSISTENT SYSTEMS, LLC

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Primary sources

- 17.1.2.2 Key data from primary sources

- 17.1.2.3 Breakdown of primary interviews

- 17.1.2.4 Insights from primary experts

- 17.1.1 SECONDARY DATA

- 17.2 FACTOR ANALYSIS

- 17.2.1 DEMAND-SIDE INDICATORS

- 17.2.2 SUPPLY-SIDE INDICATORS

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.2 TOP-DOWN APPROACH

- 17.4 DATA TRIANGULATION

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 RESEARCH LIMITATIONS

- 17.7 RISK ASSESSMENT

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 ANNEXURE: DEFENSE PROGRAMS

- 18.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.4 CUSTOMIZATION OPTIONS

- 18.5 RELATED REPORTS

- 18.6 AUTHOR DETAILS