|

시장보고서

상품코드

2057468

HTS(High Throughput Screening) 시장 : 제공 제품별, 유형별, 기술별, 워크플로우별, 최종사용자별, 용도별, 지역별 - 예측(-2031년)High-Throughput Screening Market by Instruments, Consumables, Software, Services, Technology, Workflow, Application, Competition - Global Forecast to 2031 |

||||||

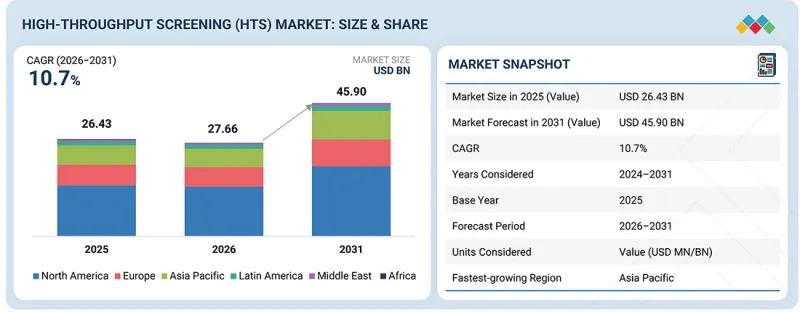

HTS(High Throughput Screening) 시장 규모는 2026년 276억 6,000만 달러에서 2031년에는 459억 달러에 이를 것으로 예측되며, 예측 기간 중 CAGR 10.7%를 기록할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제공 제품별, 유형별, 기술별, 워크플로우별, 최종사용자별, 용도별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카. |

오픈 이노베이션 모델의 도입 확대, 정부 자금 및 벤처 캐피털 투자 증가, 제약·바이오기술 기업의 연구개발비 증가 등의 요인이 꼽힙니다. 자동화, 고밀도 스크리닝, 세포 기반 분석, 라벨 프리 검출, AI를 활용한 데이터 분석 분야의 기술적 진보에 힘입어 스크리닝 효율이 더욱 향상되었으며, 이는 신약 개발 워크플로우 전반에 걸친 HTS 플랫폼의 보급을 촉진하고 있습니다.

제품군별로는 2025년 제품 부문이 고처리량 스크리닝(HTS) 시장에서 가장 큰 점유율을 차지했습니다.

제공 유형별로는 고처리량 스크리닝(HTS) 시장은 제품 및 서비스로 구분됩니다. 2025년, 제품 부문이 고처리량 스크리닝(HTS) 시장에서 가장 큰 점유율을 차지했습니다. 이는 분석 키트, 시약, 소모품, 마이크로플레이트, 화합물 라이브러리, 장비, 소프트웨어 및 자동화 플랫폼에 대한 지속적인 수요에 힘입은 결과입니다. HTS 워크플로우에서는 분석법 개발, 스크리닝, 데이터 분석, 히트 확인 등 전 과정에서 소모품 및 통합형 장비의 지속적인 사용이 필요하기 때문에 이 부문은 계속해서 지배적인 위치를 유지하고 있습니다. 자동 액체 핸들러, 마이크로플레이트 리더, 하이컨텐츠 이미징 시스템, 어세이 레디 키트의 도입이 급속히 진행되고 있는 점도 HTS 시장 내 제품의 수익 기여도를 더욱 촉진하고 있습니다.

용도별로는 2025년 신약 개발 부문이 고처리량 스크리닝(HTS) 시장에서 가장 큰 점유율을 차지했습니다.

용도별로 보면, 고처리량 스크리닝(HTS) 시장은 신약 개발, 기초 연구 및 기능 유전체학, 독성학 및 안전성 스크리닝, 정밀 의학 바이오마커 발견, 줄기세포 및 재생의학 연구, 그리고 기타 용도로 분류됩니다. 2025년, 신약 개발 부문은 고처리량 스크리닝(HTS) 시장에서 가장 큰 점유율을 차지했습니다. 이는 HTS가 방대한 화합물 라이브러리의 스크리닝, 유망 화합물의 동정, 표적 검증 및 선도 화합물의 최적화를 지원하는 데 널리 활용되고 있기 때문입니다. 제약 및 생명공학 기업들은 초기 단계의 신약 개발 생산성을 높이고, 후보 물질을 전임상 개발 단계로 이행하는 데 걸리는 시간을 단축하기 위해 계속해서 HTS 플랫폼에 의존하고 있습니다. 또한, 이 분야는 생물학적 관련성이 더 높은 후보 물질을 선별하기 위한 표현형 스크리닝, 세포 기반 분석법, 3D 모델 및 하이컨텐츠 이미징의 활용 확대로부터도 혜택을 받고 있습니다.

2026년부터 2031년에 걸쳐 아시아태평양은 고처리량 스크리닝(HTS) 시장에서 가장 높은 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다.

고속 스크리닝(HTS) 시장은 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카로 분류됩니다. 아시아태평양은 예측 기간 동안 상당한 연평균 성장률(CAGR)을 기록하며 성장할 것으로 예측됩니다. 이러한 증가는 제약 및 생명공학 분야의 연구개발 활동 확대, CRO(의약품 개발 수탁 기관)의 영향력 확대, 그리고 신약 개발 인프라에 대한 투자 증가에 힘입어 이루어지고 있습니다. 중국, 인도, 일본, 한국 등에서는 연구 자금 증가, 아웃소싱 수요의 확대, 그리고 자동화된 실험실 기술의 도입을 통해 스크리닝 역량을 강화하고 있습니다. 또한, 이 지역은 비용 효율적인 연구 운영, 생명공학 분야 스타트업의 활동 확대, 그리고 세계 제약 기업과 현지 신약 개발 서비스 제공업체간의 제휴 증가로 인한 혜택도 누리고 있습니다.

Thermo Fisher Scientific Inc.(미국), Agilent Technologies, Inc.(미국), Merck KGaA(독일), Danaher Corporation(미국), Revvity, Inc.(미국), Tecan Group Ltd.(스위스), Bio-Rad Laboratories, Inc.(미국), Corning Incorporated(미국), Mettler-Toledo International Inc.(미국), Lonza Group(스위스), Waters Corporation(미국), Sartorius AG(독일), Eppendorf SE(독일), Porvair Plc(영국), Greiner AG(오스트리아), Charles River Laboratories(미국), Eurofins Scientific(룩셈부르크), Hamilton Company(미국)는 HTS 솔루션을 제공하는 주요 기업 중 일부입니다.

조사 범위

본 조사 보고서에서는 하이 스루풋 스크리닝(HTS) 시장을 제공 내용(제품 및 서비스), 제품 유형(장비, 시약 및 키트·소모품, 소프트웨어·정보학, 서비스), 기술별(생화학적 스크리닝 기술, 세포 기반 스크리닝 기술, 하이컨텐츠 스크리닝(HCS) 기술, 라벨 프리 스크리닝 기술, 마이크로플루이딕스·소형화 스크리닝 기술, 3D 세포 배양·고도화된 세포 모델 기술, 초고속 처리·자동화 기술, AI 활용·컴퓨터 지원 스크리닝 기술), 워크플로우별(어세이 개발·최적화, 화합물 라이브러리 조성, 하이 스루풋 스크리닝, 데이터 분석·히트 동정, 히트 확인, 히트 검증·특성 평가), 최종 사용자별(제약·바이오기술 기업, CRO 및 CDMO, 학술·연구 기관, 기타 최종 사용자), 서비스 유형별(어세이 개발·최적화 서비스, 화합물 라이브러리 관리 서비스, 1차 스크리닝 서비스, 2차 스크리닝·히트 확인 서비스, 히트 검증·특성 평가 서비스, 데이터 분석·인포매틱스 서비스, 기타 서비스), 최종 사용자별(제약·바이오기술 기업, 학술·연구 기관, 기타 최종 사용자), 용도별(신약 개발, 기초 연구·기능 유전체학, 독성학·안전성 스크리닝, 정밀의학·바이오마커 발견, 줄기세포·재생의학 연구, 기타 용도), 지역별(북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카)로 분류되어 있습니다.

본 보고서의 조사 범위에는 하이 스루풋 스크리닝(HTS) 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 과제, 기회, 제약 등)에 대한 상세한 정보가 포함되어 있습니다. 주요 업계 진출기업에 대한 종합적인 분석을 수행하여, 사업 개요, 제품 및 서비스 포트폴리오, 그리고 제휴, 파트너십, 사업 확장, 계약, 인수, 고처리량 스크리닝(HTS) 시장의 최근 동향을 포함한 주요 전략에 대한 인사이트를 제공합니다. 본 보고서에는 고처리량 스크리닝(HTS) 시장 생태계 내 주요 기업 및 신생 스타트업에 대한 경쟁 분석이 포함되어 있습니다. 또한, 시장 성장을 주도하는 촉진요인, 제약 요인, 과제, 기회 등 주요 요인을 상세하게 설명하는 한편, 주요 업계 업체들의 솔루션, 제품, 최근 제품 출시, 합병 및 인수, 그리고 신흥 시장 동향에 대한 생태계를 심층적으로 분석했습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 고처리량 스크리닝(HTS) 시장에 대한 종합적인 개요를 제공합니다. 본 보고서는 다양한 부문 시장 규모와 향후 성장 기회를 평가하는 것을 목적으로 합니다. 또한, 주요 시장 진출 기업에 대한 상세한 경쟁 분석도 수록되어 있으며, 여기에는 기업 프로파일, 최근 동향, 주요 시장 전략 등이 포함되어 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

주요 촉진요인(오픈 이노베이션 모델의 확산, 연구개발 자금 증가 및 민관 투자 확대, 실험실 자동화 및 로봇 스크리닝 플랫폼의 확산, CRO 및 HTS 서비스 제공업체로의 스크리닝 업무 아웃소싱 증가) 분석, 제약 요인(HTS 장비와 관련된 높은 비용, 분석법 개발 및 검증의 복잡성), 기회(신흥 시장에서의 HTS 기술 채택 확대, 약물 전환 및 맞춤형 의료 분야에서의 HTS 응용 확대), 그리고 과제(데이터 관리·분석의 복잡성, 3D 어세이, 오가노이드 어세이, 영상 기반 어세이에서의 표준화 과제)

- 제품 및 서비스 개발·혁신 : 신규 출시된 제품 및 서비스에 대한 심층적인 인사이트, 그리고 고처리량 스크리닝(HTS) 시장의 기술적 평가.

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보. 본 보고서에서는 다양한 지역에 걸친 고처리량 스크리닝(HTS) 시장을 분석했습니다.

- 시장의 다각화 : 하이 스루풋 스크리닝(HTS) 시장의 미개척 신규 지역, 최근 동향 및 투자에 관한 종합적인 정보

경쟁사 평가: Thermo Fisher Scientific Inc.(미국), Agilent Technologies, Inc.(미국), Merck KGaA(독일), Danaher Corporation(미국), Revvity, Inc.(미국), Tecan Group Ltd.(스위스), Bio-Rad Laboratories, Inc.(미국), Corning Incorporated(미국), Mettler-Toledo International Inc.(미국), Lonza Group(스위스), Waters Corporation(미국), Sartorius AG(독일), Eppendorf SE(독일), Porvair Plc(영국), Greiner AG(오스트리아), Charles River Laboratories(미국), Eurofins Scientific(룩셈부르크), Hamilton Company(미국) 등, 하이 스루풋 스크리닝(HTS) 시장의 주요 기업들의 사업 전략 및 제품 라인업에 대해 분석했습니다.

또한, 본 보고서는 이해관계자들이 고처리량 스크리닝(HTS) 시장 동향을 이해하는 데 도움을 주며, 주요 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다. 주요 업계 참여 기업에 대한 상세한 분석을 통해 HTS 부문 시장의 전략, 제품 및 서비스 출시, 인수, 파트너십, 제휴, 최근 동향, 투자, 자금 조달, 브랜드 및 제품 비교, 공급업체 평가, 재무 지표에 대한 인사이트를 제공합니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 그리고 혁신

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 HTS(High Throughput Screening) 시장(제공 제품별)

제10장 High Throughput Screening 제품 시장(유형별)

제11장 High Throughput Screening 제품 시장(기술별)

제12장 High Throughput Screening 제품 시장(워크플로우별)

제13장 High Throughput Screening 제품 시장(최종사용자별)

제14장 High Throughput Screening 서비스 시장(유형별)

제15장 High Throughput Screening 서비스 시장(최종사용자별)

제16장 HTS(High Throughput Screening) 시장(용도별)

제17장 HTS(High Throughput Screening) 시장(지역별)

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 부록

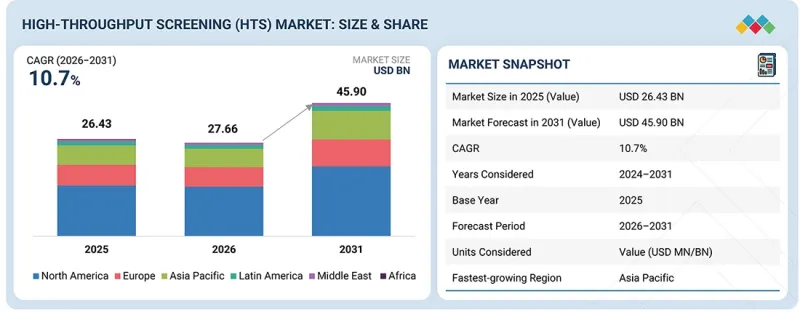

LSH 26.06.23The high-throughput screening (HTS) market is expected to reach USD 45.90 billion in 2031 from USD 27.66 billion in 2026, growing at a CAGR of 10.7% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Offering, Products by Type, Application, and Region |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. |

Factors such as the rising adoption of open innovation models, increasing government funding and venture capital investments, and higher R&D spending by pharmaceutical and biotechnology companies. Technological advancements in automation, high-content screening, cell-based assays, label-free detection, and AI-enabled data analysis are further improving screening efficiency and supporting wider adoption of HTS platforms across drug discovery workflows.

By offering, the products segment accounted for the largest share of the high-throughput screening (HTS) market in 2025.

Based on offering, the high-throughput screening (HTS) market is segmented into products and services. In 2025, the products segment held the largest share of the high-throughput screening (HTS) market. This is driven by recurring demand for assay kits, reagents, consumables, microplates, compound libraries, instruments, software, and automation platforms. The segment remains dominant because HTS workflows require continuous use of consumables and integrated instruments throughout assay development, screening, data analysis, and hit confirmation. Strong adoption of automated liquid handlers, microplate readers, high-content imaging systems, and assay-ready kits further supports the revenue contribution of products in the HTS market.

By application, the drug discovery & development segment accounted for the largest share of the high-throughput screening (HTS) market in 2025.

By application, the high-throughput screening (HTS) market is divided into drug discovery & development, basic research & functional genomics, toxicology & safety screening, precision medicine & biomarker discovery, stem cell & regenerative medicine research, and other applications. In 2025, the drug discovery & development segment held the largest share of the high-throughput screening (HTS) market, as HTS is widely used to screen large compound libraries, identify hits, validate targets, and support lead optimization. Pharmaceutical and biotechnology companies continue to rely on HTS platforms to improve early-stage discovery productivity and reduce the time required to move candidates into preclinical development. The segment also benefits from the growing use of phenotypic screening, cell-based assays, 3D models, and high-content imaging to identify more biologically relevant drug candidates.

The Asia Pacific region is expected to grow at the highest CAGR in the high-throughput screening (HTS) market from 2026 to 2031.

The high-throughput screening (HTS) market is divided into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. The Asia Pacific region is expected to grow at a significant CAGR during the forecast period. This increase is driven by expanding pharmaceutical and biotechnology R&D activity, growing CRO presence, and increasing investments in drug discovery infrastructure. Countries such as China, India, Japan, and South Korea are strengthening their screening capabilities through rising research funding, outsourcing demand, and the adoption of automated laboratory technologies. The region is also benefiting from cost-efficient research operations, expanding biotech start-up activity, and increasing partnerships between global pharma companies and local discovery service providers.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side (80%) and Demand Side (20%)

- By Designation: Managers (45%), CXOs & Directors (30%), and Executives (25%)

- By Region: North America (40%), Europe (25%), Asia Pacific (25%), Latin America (5%), the Middle East & Africa (5%)

Thermo Fisher Scientific Inc. (US), Agilent Technologies, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), Revvity, Inc. (US), Tecan Group Ltd. (Switzerland), Bio-Rad Laboratories, Inc. (US), Corning Incorporated (US), Mettler-Toledo International Inc. (US), Lonza Group (Switzerland), Waters Corporation (US), Sartorius AG (Germany), Eppendorf SE (Germany), Porvair Plc (UK), Greiner AG (Austria), Charles River Laboratories (US), Eurofins Scientific (Luxembourg), and Hamilton Company (US) are some of the key companies offering HTS solutions.

Research Coverage

This research report categorizes the high-throughput screening (HTS) market by offering (products and services), products by type (instruments; reagents, kits, and consumables; software & informatics; and services), products by technology (biochemical screening technologies, cell-based screening technologies, high-content screening (HCS) technologies, label-free screening technologies, microfluidic & miniaturized screening technologies, 3D cell culture & advanced cellular model technologies, ultra-high-throughput & automation technologies, and AI-enabled & computational screening technologies), products by workflow (assay development & optimization, compound library preparation, high-throughput screening, data analysis & hit identification, hit confirmation, hit validation & characterization), products by end user (pharmaceutical & biotechnology companies, CROs & CDMOs, academic & research institutes, and other end users), services by type (assay development & optimization services, compound library management services, primary screening services, secondary screening & hit confirmation services, hit validation & characterization services, data analysis & informatics services, and other services), services by end user (pharmaceutical & biotechnology companies, academic & research institutes, and other end users), application (drug discovery & development, basic research & functional genomics, toxicology & safety screening, precision medicine & biomarker discovery, stem cell & regenerative medicine research, and other applications), and region (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa).

The scope of the report provides detailed information on major factors such as drivers, challenges, opportunities, and restraints that influence the growth of the high-throughput screening (HTS) market. A comprehensive analysis of key industry players has been conducted to provide insights into their business overviews, product/service portfolios, and key strategies, including collaborations, partnerships, expansions, agreements, acquisitions, and recent developments in the high-throughput screening (HTS) market. This report includes a competitive analysis of top players and upcoming startups in the high-throughput screening (HTS) market ecosystem. The report also details primary factors like drivers, restraints, challenges, and opportunities shaping the market growth, along with an in-depth review of key industry players' solutions, products, recent product launches, mergers, acquisitions, and emerging market trends ecosystem.

Key Benefits of Buying the Report

This report offers a comprehensive overview of the high-throughput screening (HTS) market. It aims to assess the market size and future growth opportunities across various segments. The report also features an in-depth competitive analysis of the major market players, including their company profiles, recent developments, and key market strategies.

The report provides insights into the following pointers:

Analysis of key drivers (growing adoption of open innovative models, growing R&D funding and increasing public & private investments, growing adoption of lab automation and robotic screening platforms, and increasing outsourcing of screening activities to CROs and HTS service providers), restraints (high costs associated with HTS instruments and complexity in assay development and validation), opportunities (increasing adoption of HTS technologies in emerging markets and growing application of HTS in drug repurposing and personalized medicine), and challenges (complexity in data management & analysis, standardization challenges in 3D, organoid, and image-based assays)

- Product/Service Development/Innovation: Detailed insights on newly launched products/services, and technological assessment of the high-throughput screening (HTS) market.

- Market Development: Comprehensive information about lucrative markets; the report analyzes the high-throughput screening (HTS) market across varied regions.

- Market Diversification: Exhaustive information about new, untapped geographies, recent developments, and investments in the high-throughput screening (HTS) market

Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as Thermo Fisher Scientific Inc. (US), Agilent Technologies, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), Revvity, Inc. (US), Tecan Group Ltd. (Switzerland), Bio-Rad Laboratories, Inc. (US), Corning Incorporated (US), Mettler-Toledo International Inc. (US), Lonza Group (Switzerland), Waters Corporation (US), Sartorius AG (Germany), Eppendorf SE (Germany), Porvair Plc (UK), Greiner AG (Austria), Charles River Laboratories (US), Eurofins Scientific (Luxembourg), and Hamilton Company (US), among others, in the high-throughput screening (HTS) market.

The report also helps stakeholders understand trends in the high-throughput screening (HTS) market and provides information on key drivers, restraints, challenges, and opportunities. A detailed analysis of the key industry players has been conducted to offer insights into their strategies, product/service launches, acquisitions, partnerships, collaborations, recent activities, investments, funding, brand and product comparisons, vendor evaluations, and financial metrics of the HTS sector market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONS COVERED

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS & KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN HIGH-THROUGHPUT SCREENING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 HIGH-THROUGHPUT SCREENING MARKET OVERVIEW

- 3.2 NORTH AMERICA: HIGH-THROUGHPUT SCREENING MARKET, BY PRODUCT TYPE AND COUNTRY

- 3.3 HIGH-THROUGHPUT SCREENING MARKET: GEOGRAPHIC GROWTH OPPORTUNITIES

- 3.4 HIGH-THROUGHPUT SCREENING PRODUCTS MARKET SHARE, BY END USER, 2026 VS 2031 (%)

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing adoption of open innovative models

- 4.2.1.2 Technological advancements

- 4.2.1.3 Growing R&D funding and increasing public & private investments

- 4.2.1.4 Growing adoption of lab automation & robotic screening platforms

- 4.2.1.5 Increasing outsourcing of screening activities to CROs & CDMOs

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs associated with HTS instruments

- 4.2.2.2 Complexity in assay development and validation

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing adoption of HTS technologies in emerging markets

- 4.2.3.2 Growing application of HTS in drug repurposing and personalized medicine

- 4.2.3.3 Expansion of CRISPR, RNAi, and functional genomics screening

- 4.2.4 CHALLENGES

- 4.2.4.1 Complexity in data management and analysis

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS & WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.1.2 BARGAINING POWER OF SUPPLIERS

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 THREAT OF SUBSTITUTES

- 5.1.5 THREAT OF NEW ENTRANTS

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL HIGH-THROUGHPUT SCREENING INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND OF HTS PRODUCTS, BY KEY PLAYER, 2023-2025

- 5.5.2 AVERAGE SELLING PRICE TREND OF HTS PRODUCTS, BY REGION, 2023-2025

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 902730 & 902781)

- 5.6.2 EXPORT SCENARIO (HS CODE 902730& 902781)

- 5.7 KEY CONFERENCES & EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT & FUNDING SCENARIO

- 5.10 IMPACT OF 2025 US TARIFFS ON HIGH-THROUGHPUT SCREENING (HTS) MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 US

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.10.5.1 Pharmaceutical & biotechnology companies

- 5.10.5.2 CROs & CDMOs

- 5.10.5.3 Academic & research institutes

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, AND INNOVATIONS

- 6.1 TECHNOLOGICAL ANALYSIS

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.1.1.1 High-content screening

- 6.1.1.2 Label-free detection

- 6.1.1.3 Microfluidics

- 6.1.2 COMPLEMENTARY TECHNOLOGIES

- 6.1.2.1 Laboratory automation & robotic integration

- 6.1.2.2 Mass spectrometry

- 6.1.2.3 Flow cytometry

- 6.1.3 ADJACENT TECHNOLOGIES

- 6.1.3.1 Fragment-based drug discovery

- 6.1.3.2 Bioinformatics & cheminformatics

- 6.1.1 KEY EMERGING TECHNOLOGIES

- 6.2 TECHNOLOGY/PRODUCT ROADMAP

- 6.3 PATENT ANALYSIS

- 6.3.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR HIGH-THROUGHPUT SCREENING PATENTS, 2015-2025

- 6.4 FUTURE APPLICATIONS

- 6.5 IMPACT OF AI/GEN AI ON HIGH-THROUGHPUT SCREENING (HTS) MARKET

- 6.5.1 BEST PRACTICES IN HTS WORKFLOW

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN HIGH-THROUGHPUT SCREENING (HTS) MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEMS & IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN HIGH-THROUGHPUT SCREENING (HTS) MARKET

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS & BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 HIGH-THROUGHPUT SCREENING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.2 PRODUCTS

- 9.2.1 RECURRING CONSUMABLES DEMAND, AUTOMATION UPGRADES, AND ADVANCED SCREENING PLATFORMS TO DRIVE MARKET GROWTH

- 9.3 SERVICES

- 9.3.1 RISING OUTSOURCING OF ASSAY DEVELOPMENT, PRIMARY SCREENING, AND DATA ANALYSIS TO DRIVE GROWTH OF HTS SERVICES MARKET

10 HIGH-THROUGHPUT SCREENING PRODUCTS MARKET, BY TYPE

- 10.1 INTRODUCTION

- 10.2 REAGENTS, KITS, AND CONSUMABLES

- 10.2.1 SCREENING ASSAY KITS

- 10.2.1.1 Cell-based assays

- 10.2.1.1.1 Cell viability assays

- 10.2.1.1.1.1 Increasing use of viability readouts across oncology and toxicity screening to sustain assay kit demand

- 10.2.1.1.2 Cytotoxicity assays

- 10.2.1.1.2.1 Rising focus on early toxicity detection to improve lead selection and reduce drug development risk

- 10.2.1.1.3 Reporter gene assays

- 10.2.1.1.3.1 Growing use of pathway-specific functional readouts to strengthen reporter gene assay adoption

- 10.2.1.1.4 Other cell-based assays

- 10.2.1.1.1 Cell viability assays

- 10.2.1.2 Biochemical assays

- 10.2.1.2.1 Enzyme assays

- 10.2.1.2.1.1 Broad use of enzyme activity profiling in target-based drug discovery to sustain demand for enzyme assay kits

- 10.2.1.2.2 Kinase assays

- 10.2.1.2.2.1 Continued investment in targeted kinase inhibitor discovery to drive kinase assay kit demand

- 10.2.1.2.3 Binding assays

- 10.2.1.2.3.1 Rising use of target engagement and affinity profiling to improve hit validation quality

- 10.2.1.2.4 Other biochemical assays

- 10.2.1.2.1 Enzyme assays

- 10.2.1.3 Other assays & kits

- 10.2.1.1 Cell-based assays

- 10.2.2 BIOLOGICAL & CELL CULTURE REAGENTS

- 10.2.2.1 Rising use of disease-relevant cellular models to strengthen demand for biological and cell culture reagents

- 10.2.3 COMPOUND LIBRARIES

- 10.2.3.1 Expansion of focused and repurpose libraries to support compound library demand

- 10.2.4 DETECTION REAGENTS

- 10.2.4.1 Increasing adoption of fluorescence, luminescence, and biomarker-based readouts to drive detection reagent use

- 10.2.5 3D CELL CULTURE PRODUCTS

- 10.2.5.1 Scaffold-based 3D cell culture products

- 10.2.5.1.1 Rising demand for matrix-supported disease models to drive scaffold-based 3D culture product growth

- 10.2.5.2 Scaffold-free 3D cell culture products

- 10.2.5.2.1 Increasing use of spheroid-based screening to support scaffold-free 3D culture product adoption

- 10.2.5.3 Other 3D cell culture products

- 10.2.5.1 Scaffold-based 3D cell culture products

- 10.2.6 OTHER HTS CONSUMABLES

- 10.2.1 SCREENING ASSAY KITS

- 10.3 INSTRUMENTS

- 10.3.1 DETECTION & IMAGING SYSTEMS

- 10.3.1.1 Microplate readers

- 10.3.1.1.1 Growing use of multiplexed biochemical and cell-based assays to support microplate reader demand

- 10.3.1.2 High-content screening (HCS) & imaging systems

- 10.3.1.2.1 Increasing adoption of phenotypic screening and AI-based cellular analysis to drive growth of HCS systems

- 10.3.1.3 Cell analysis systems

- 10.3.1.3.1 Growing use of cell-based screening and functional biology assays to strengthen demand for cell analysis systems

- 10.3.1.4 Label-free detection systems

- 10.3.1.4.1 Rising need for real-time biomolecular interaction analysis to support adoption of label-free detection systems

- 10.3.1.5 Microfluidic & miniaturized screening systems

- 10.3.1.5.1 Assay miniaturization to drive adoption of microfluidic screening systems

- 10.3.1.1 Microplate readers

- 10.3.2 LIQUID HANDLING & AUTOMATION SYSTEMS

- 10.3.2.1 Increasing assay miniaturization and workflow standardization to drive growth of liquid handling & automation systems

- 10.3.3 ROBOTIC HTS PLATFORMS & AUTOMATED WORKFLOW SYSTEMS

- 10.3.3.1 Rising deployment of end-to-end laboratory automation systems to accelerate robotic HTS platform adoption

- 10.3.4 OTHER HTS INSTRUMENTS

- 10.3.1 DETECTION & IMAGING SYSTEMS

- 10.4 SOFTWARE & INFORMATICS

- 10.4.1 BIOINFORMATICS TOOLS TO HELP TURN RAW DATA INTO MEANINGFUL INSIGHTS

11 HIGH-THROUGHPUT SCREENING PRODUCTS MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 CELL-BASED SCREENING TECHNOLOGIES

- 11.2.1 INCREASING ADOPTION OF PHYSIOLOGICALLY RELEVANT PHENOTYPIC SCREENING WORKFLOWS TO STRENGTHEN CELL-BASED TECHNOLOGY DEMAND

- 11.3 ULTRA-HIGH-THROUGHPUT & AUTOMATION TECHNOLOGIES

- 11.3.1 GROWING DEMAND FOR SCALABLE ROBOTIC INFRASTRUCTURE & INTEGRATED AUTOMATION PLATFORMS TO SUPPORT MARKET GROWTH

- 11.4 HIGH-CONTENT SCREENING (HCS) TECHNOLOGIES

- 11.4.1 RISING ADOPTION OF AI-POWERED PHENOTYPIC IMAGING AND MULTIPARAMETRIC CELLULAR PROFILING TO ACCELERATE HCS TECHNOLOGY GROWTH

- 11.5 BIOCHEMICAL SCREENING TECHNOLOGIES

- 11.5.1 CONTINUED EXPANSION OF TARGET-BASED DRUG DISCOVERY PROGRAMS TO SUSTAIN BIOCHEMICAL SCREENING PRODUCT DEMAND

- 11.6 3D CELL CULTURE & ADVANCED CELLULAR MODEL TECHNOLOGIES

- 11.6.1 RISING ADOPTION OF ORGANOIDS, SPHEROIDS, AND TISSUE-LIKE SCREENING SYSTEMS TO ACCELERATE 3D CELLULAR TECHNOLOGY GROWTH

- 11.7 LABEL-FREE SCREENING TECHNOLOGIES

- 11.7.1 INCREASING USE OF REAL-TIME BINDING KINETICS AND BIOPHYSICAL PROFILING TO SUPPORT LABEL-FREE SCREENING ADOPTION

- 11.8 OTHER HTS TECHNOLOGIES

12 HIGH-THROUGHPUT SCREENING PRODUCTS MARKET, BY WORKFLOW

- 12.1 INTRODUCTION

- 12.2 PRIMARY SCREENING

- 12.2.1 LARGE-SCALE COMPOUND SCREENING REQUIREMENTS TO SUSTAIN PRODUCT DEMAND ACROSS PRIMARY HTS WORKFLOWS

- 12.3 ASSAY DEVELOPMENT & OPTIMIZATION

- 12.3.1 RISING NEED FOR ROBUST, MINIATURIZED, AND AUTOMATION-COMPATIBLE ASSAYS TO SUPPORT ASSAY DEVELOPMENT PRODUCT DEMAND

- 12.4 HIT CONFIRMATION/SECONDARY SCREENING

- 12.4.1 RISING FOCUS ON HIT QUALITY ASSESSMENT AND FALSE-POSITIVE REDUCTION TO SUPPORT SECONDARY SCREENING PRODUCT DEMAND

- 12.5 DATA ANALYSIS & HIT IDENTIFICATION

- 12.5.1 INCREASING INTEGRATION OF AI-DRIVEN ANALYTICS AND IMAGE-BASED SCREENING DATA TO ACCELERATE HIT IDENTIFICATION WORKFLOWS

- 12.6 COMPOUND LIBRARY PREPARATION

- 12.6.1 EXPANSION OF LARGE-SCALE AND FOCUSED SCREENING LIBRARIES TO STRENGTHEN DEMAND FOR COMPOUND PREPARATION PRODUCTS

- 12.7 HIT VALIDATION & CHARACTERIZATION

- 12.7.1 GROWING FOCUS ON PHENOTYPIC CHARACTERIZATION WORKFLOWS TO DRIVE HIT VALIDATION PRODUCT DEMAND

13 HIGH-THROUGHPUT SCREENING PRODUCTS MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 13.2.1 SUSTAINED BIOPHARMA R&D INVESTMENT AND AUTOMATION-LED DRUG DISCOVERY TO DRIVE HTS PRODUCT ADOPTION

- 13.3 CROS & CDMOS

- 13.3.1 RISING DISCOVERY OUTSOURCING AND CRO PLATFORM EXPANSION TO ACCELERATE HTS PRODUCT DEMAND

- 13.4 ACADEMIC & RESEARCH INSTITUTES

- 13.4.1 PUBLIC RESEARCH FUNDING AND TRANSLATIONAL BIOLOGY PROGRAMS TO SUPPORT HTS PRODUCT UPTAKE IN RESEARCH INSTITUTES

- 13.5 OTHER END USERS

14 HIGH-THROUGHPUT SCREENING SERVICES MARKET, BY TYPE

- 14.1 INTRODUCTION

- 14.2 PRIMARY SCREENING SERVICES

- 14.2.1 RISING HIGH-VOLUME SCREENING REQUIREMENTS TO DRIVE GROWTH OF PRIMARY HTS SCREENING SERVICES

- 14.3 ASSAY DEVELOPMENT & OPTIMIZATION SERVICES

- 14.3.1 INCREASING DEMAND FOR CUSTOMIZED AND MINIATURIZED ASSAYS TO SUPPORT ASSAY DEVELOPMENT SERVICE ADOPTION

- 14.4 SECONDARY SCREENING & HIT CONFIRMATION SERVICES

- 14.4.1 INCREASING EMPHASIS ON HIT VALIDATION AND SELECTIVITY ASSESSMENT TO SUPPORT SECONDARY SCREENING SERVICES

- 14.5 HIT VALIDATION & CHARACTERIZATION SERVICES

- 14.5.1 GROWING NEED FOR MECHANISM-OF-ACTION PROFILING TO STRENGTHEN HIT CHARACTERIZATION SERVICE ADOPTION

- 14.6 COMPOUND LIBRARY MANAGEMENT SERVICES

- 14.6.1 EXPANSION OF LARGE-SCALE SCREENING LIBRARIES TO STRENGTHEN DEMAND FOR COMPOUND MANAGEMENT SERVICES

- 14.7 DATA ANALYSIS & INFORMATICS SERVICES

- 14.7.1 GROWING ADOPTION OF AI-ENABLED SCREENING ANALYTICS AND IMAGE-BASED DATA INTERPRETATION TO DRIVE HTS INFORMATICS SERVICES GROWTH

- 14.8 OTHER HTS SERVICES

15 HIGH-THROUGHPUT SCREENING SERVICES MARKET, BY END USER

- 15.1 INTRODUCTION

- 15.2 PHARMACEUTICAL & BIOTECHNOLOGY COMPANIES

- 15.2.1 INCREASING COMPLEXITY OF DRUG DISCOVERY WORKFLOWS TO STRENGTHEN OUTSOURCING OF HTS SERVICES BY PHARMA AND BIOTECH COMPANIES

- 15.3 ACADEMIC & RESEARCH INSTITUTES

- 15.3.1 LIMITED IN-HOUSE AUTOMATION CAPACITY TO DRIVE ACADEMIC OUTSOURCING OF HTS SERVICES

- 15.4 OTHER END USERS

16 HIGH-THROUGHPUT SCREENING MARKET, BY APPLICATION

- 16.1 INTRODUCTION

- 16.2 DRUG DISCOVERY & DEVELOPMENT

- 16.2.1 INCREASING PHARMACEUTICAL R&D INVESTMENTS AND EXPANSION OF TARGET-BASED AND PHENOTYPIC DRUG DISCOVERY PROGRAMS TO DRIVE MARKET GROWTH

- 16.3 BASIC RESEARCH & FUNCTIONAL GENOMICS

- 16.3.1 GROWING ADOPTION OF CRISPR SCREENING, FUNCTIONAL GENOMICS, AND DISEASE PATHWAY CHARACTERIZATION TO DRIVE HTS DEMAND

- 16.4 TOXICOLOGY & SAFETY SCREENING

- 16.4.1 INCREASING EMPHASIS ON PREDICTIVE TOXICOLOGY AND REGULATORY PRESSURE TO REDUCE ANIMAL TESTING TO ACCELERATE HTS ADOPTION

- 16.5 PRECISION MEDICINE & BIOMARKER DISCOVERY

- 16.5.1 EXPANSION OF BIOMARKER-GUIDED THERAPEUTICS AND PERSONALIZED MEDICINE PIPELINES TO DRIVE RAPID GROWTH IN PRECISION MEDICINE SCREENING APPLICATIONS

- 16.6 STEM CELL & REGENERATIVE MEDICINE RESEARCH

- 16.6.1 GROWING DEVELOPMENT OF CELL THERAPIES AND REGENERATIVE MEDICINE PRODUCTS IS SUPPORTING HTS ADOPTION IN STEM CELL RESEARCH

- 16.7 OTHER APPLICATIONS

17 HIGH-THROUGHPUT SCREENING MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 NORTH AMERICA

- 17.2.1 US

- 17.2.1.1 Advanced automation, strong drug discovery infrastructure, and AI-enabled screening workflows to support market growth

- 17.2.2 CANADA

- 17.2.2.1 Academic screening infrastructure to support market growth

- 17.2.1 US

- 17.3 EUROPE

- 17.3.1 GERMANY

- 17.3.1.1 Increasing product launches and investments to boost market growth

- 17.3.2 UK

- 17.3.2.1 Industrial-scale screening access and academic HTS infrastructure to support market

- 17.3.3 FRANCE

- 17.3.3.1 Large pharmaceutical R&D expenditure to drive market growth

- 17.3.4 ITALY

- 17.3.4.1 Functional genomics and automated screening platforms to fuel growth

- 17.3.5 SPAIN

- 17.3.5.1 Academic screening platforms, chemical biology networks, and assay automation to boost market

- 17.3.6 REST OF EUROPE

- 17.3.1 GERMANY

- 17.4 ASIA PACIFIC

- 17.4.1 CHINA

- 17.4.1.1 Automation-led drug discovery and CRO-led screening capacity expansion to support growth of market

- 17.4.2 JAPAN

- 17.4.2.1 Advanced screening platforms and integrated drug discovery partnerships to support market growth

- 17.4.3 INDIA

- 17.4.3.1 Automation-led CRO expansion and biopharma R&D infrastructure growth to fuel market

- 17.4.4 AUSTRALIA

- 17.4.4.1 Robotic screening infrastructure and translational drug discovery programs to drive market growth

- 17.4.5 SOUTH KOREA

- 17.4.5.1 AI-enhanced screening platforms and translational R&D collaborations to favor market growth

- 17.4.6 REST OF ASIA PACIFIC (ROAPAC)

- 17.4.1 CHINA

- 17.5 LATIN AMERICA

- 17.5.1 BRAZIL

- 17.5.1.1 Automated bioassay infrastructure and disease-focused discovery programs to drive growth

- 17.5.2 MEXICO

- 17.5.2.1 Cost-efficient discovery capacity, antimicrobial research, and automated assay adoption to drive growth

- 17.5.3 REST OF LATIN AMERICA

- 17.5.1 BRAZIL

- 17.6 MIDDLE EAST

- 17.6.1 GCC COUNTRIES

- 17.6.1.1 Saudi Arabia

- 17.6.1.1.1 Growing pharmaceuticals industry to support market growth

- 17.6.1.2 UAE

- 17.6.1.2.1 Precision medicine investment, automated laboratory infrastructure, and AI-enabled discovery workflows to boost market growth

- 17.6.1.3 Rest of GCC Countries

- 17.6.1.1 Saudi Arabia

- 17.6.2 REST OF MIDDLE EAST

- 17.6.1 GCC COUNTRIES

- 17.7 AFRICA

- 17.7.1 INFECTIOUS DISEASE RESEARCH AND SHARED DISCOVERY NETWORKS TO AID MARKET GROWTH

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGY/RIGHT TO WIN

- 18.2.1 OVERVIEW OF STRATEGIES ADOPTED BY PLAYERS IN HIGH-THROUGHPUT SCREENING (HTS) MARKET

- 18.3 REVENUE ANALYSIS, 2021-2025

- 18.4 MARKET SHARE ANALYSIS, 2025

- 18.5 COMPANY EVALUATION QUADRANT: KEY PLAYERS, 2025

- 18.5.1 STARS

- 18.5.2 EMERGING LEADERS

- 18.5.3 PERVASIVE PLAYERS

- 18.5.4 PARTICIPANTS

- 18.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 18.5.5.1 Company footprint

- 18.5.5.2 Region footprint

- 18.5.5.3 Offering footprint

- 18.5.5.4 Product type footprint

- 18.5.5.5 Application footprint

- 18.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.6.1 PROGRESSIVE COMPANIES

- 18.6.2 RESPONSIVE COMPANIES

- 18.6.3 DYNAMIC COMPANIES

- 18.6.4 STARTING BLOCKS

- 18.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 18.6.5.1 Detailed list of key startups/SMEs

- 18.6.5.2 Competitive benchmarking of key startups/SMEs

- 18.7 COMPANY VALUATION & FINANCIAL METRICS

- 18.7.1 FINANCIAL METRICS

- 18.7.2 COMPANY VALUATION

- 18.8 BRAND/PRODUCT/SERVICE COMPARISON

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 THERMO FISHER SCIENTIFIC INC.

- 19.1.1.1 Business overview

- 19.1.1.2 Products & services offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Expansions

- 19.1.1.4 MnM view

- 19.1.1.4.1 Right to win

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses & competitive threats

- 19.1.2 DANAHER CORPORATION

- 19.1.2.1 Business overview

- 19.1.2.2 Products & services offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product & service launches

- 19.1.2.3.2 Deals

- 19.1.2.4 MnM view

- 19.1.2.4.1 Right to win

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses & competitive threats

- 19.1.3 MERCK KGAA

- 19.1.3.1 Business overview

- 19.1.3.2 Products & services offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Deals

- 19.1.3.3.2 Expansions

- 19.1.3.3.3 Other developments

- 19.1.3.4 MnM view

- 19.1.3.4.1 Right to win

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses & competitive threats

- 19.1.4 AGILENT TECHNOLOGIES, INC.

- 19.1.4.1 Business overview

- 19.1.4.2 Products & services offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches & upgrades

- 19.1.4.3.2 Deals

- 19.1.4.3.3 Expansions

- 19.1.4.3.4 Other developments

- 19.1.4.4 MnM view

- 19.1.4.4.1 Right to win

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses & competitive threats

- 19.1.5 REVVITY, INC.

- 19.1.5.1 Business overview

- 19.1.5.2 Products & services offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches

- 19.1.5.3.2 Deals

- 19.1.5.4 MnM view

- 19.1.5.4.1 Right to win

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses & competitive threats

- 19.1.6 TECAN GROUP LTD.

- 19.1.6.1 Business overview

- 19.1.6.2 Products & service offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches

- 19.1.6.3.2 Deals

- 19.1.7 BIO-RAD LABORATORIES, INC.

- 19.1.7.1 Business overview

- 19.1.7.2 Products & services offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches

- 19.1.8 CORNING INCORPORATED

- 19.1.8.1 Business overview

- 19.1.8.2 Products & services offered

- 19.1.9 METTLER-TOLEDO INTERNATIONAL INC.

- 19.1.9.1 Business overview

- 19.1.9.2 Products & services offered

- 19.1.10 LONZA GROUP

- 19.1.10.1 Business overview

- 19.1.10.2 Products & services offered

- 19.1.11 WATERS CORPORATION

- 19.1.11.1 Business overview

- 19.1.11.2 Products & services offered

- 19.1.11.3 Recent developments

- 19.1.11.3.1 Product launches

- 19.1.11.3.2 Deals

- 19.1.12 SARTORIUS AG

- 19.1.12.1 Business overview

- 19.1.12.2 Products & services offered

- 19.1.12.3 Recent developments

- 19.1.12.3.1 Product launches

- 19.1.12.3.2 Deals

- 19.1.12.3.3 Expansions

- 19.1.13 EPPENDORF SE

- 19.1.13.1 Business overview

- 19.1.13.2 Products & services offered

- 19.1.13.3 Recent developments

- 19.1.13.3.1 Product launches

- 19.1.13.3.2 Deals

- 19.1.13.3.3 Expansions

- 19.1.14 PORVAIR PLC

- 19.1.14.1 Business overview

- 19.1.14.2 Products & services offered

- 19.1.15 GREINER AG

- 19.1.15.1 Business overview

- 19.1.15.2 Products & services offered

- 19.1.16 CHARLES RIVER LABORATORIES

- 19.1.16.1 Business overview

- 19.1.16.2 products & services offered

- 19.1.16.3 Recent developments

- 19.1.16.3.1 Deals

- 19.1.17 EUROFINS SCIENTIFIC

- 19.1.17.1 Business overview

- 19.1.17.2 Products & services offered

- 19.1.17.3 Recent developments

- 19.1.17.3.1 Service launches

- 19.1.17.3.2 Deals

- 19.1.17.3.3 Expansions

- 19.1.18 HAMILTON COMPANY

- 19.1.18.1 Business overview

- 19.1.18.2 Products & services offered

- 19.1.18.3 Recent developments

- 19.1.18.3.1 Product launches

- 19.1.18.3.2 Deals

- 19.1.19 AURORA BIOMED INC.

- 19.1.19.1 Business overview

- 19.1.19.2 Products & services offered

- 19.1.20 GILSON INCORPORATED

- 19.1.20.1 Business overview

- 19.1.20.2 Products & services offered

- 19.1.21 BRAND GMBH + CO KG

- 19.1.21.1 Business overview

- 19.1.21.2 Products & services offered

- 19.1.1 THERMO FISHER SCIENTIFIC INC.

- 19.2 OTHER PLAYERS

- 19.2.1 BMG LABTECH GMBH

- 19.2.2 DIANA BIOTECHNOLOGIES, A.S.

- 19.2.3 CREATIVE BIOLABS

- 19.2.4 HIGHRES BIOSOLUTIONS

- 19.2.5 BIOMAT SRL

- 19.2.6 AXXAM S.P.A.

- 19.2.7 SYGNATURE DISCOVERY LIMITED

- 19.2.8 CROWN BIOSCIENCE

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 Key secondary sources

- 20.1.1.2 Key data from secondary research

- 20.1.2 PRIMARY DATA

- 20.1.2.1 Key primary participants

- 20.1.2.2 Breakdown of primary interviews

- 20.1.2.3 Key data from primary sources

- 20.1.1 SECONDARY DATA

- 20.2 MARKET SIZE ESTIMATION

- 20.2.1 GLOBAL HIGH-THROUGHPUT SCREENING MARKET ESTIMATION, 2025

- 20.2.1.1 Approach 1: Company revenue analysis-based estimation (bottom-up)

- 20.2.1.2 Approach 2: Primary research

- 20.2.1.2.1 Key industry insights

- 20.2.1.3 Approach 3: MnM repository analysis

- 20.2.2 SEGMENTAL MARKET SIZE ESTIMATION, 2025

- 20.2.1 GLOBAL HIGH-THROUGHPUT SCREENING MARKET ESTIMATION, 2025

- 20.3 MARKET GROWTH RATE PROJECTIONS

- 20.4 DATA TRIANGULATION

- 20.5 RESEARCH ASSUMPTIONS

- 20.6 RESEARCH LIMITATIONS AND RISK ASSESSMENT

21 APPENDIX

- 21.1 DISCUSSION GUIDE

- 21.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 21.3 CUSTOMIZATION OPTIONS

- 21.4 RELATED REPORTS

- 21.5 AUTHOR DETAILS