|

시장보고서

상품코드

2057472

압전 세라믹 시장 : 유형별, 최종 이용 산업별, 지역별 - 예측(-2031년)Piezoelectric Ceramics Market by Type (Barium Titanate, Potassium Niobate, Lead Zirconate Titanate), End-use Industry (Consumer Electronics, Aerospace & Defense, Industrial & Manufacturing, Automotive, Medical), and Region - Global Forecast To 2031 |

||||||

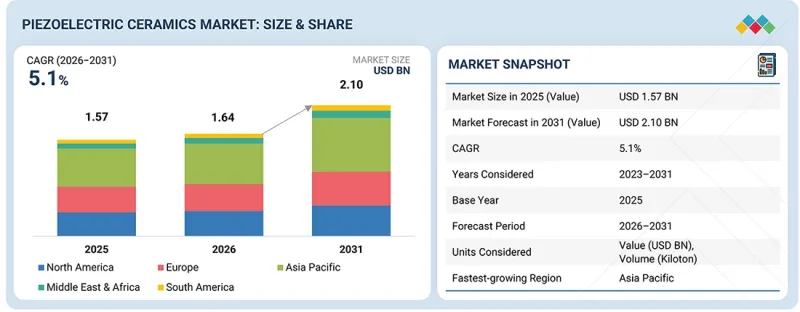

압전 세라믹 시장 규모는 2026년 16억 4,000만 달러에서 2031년까지 21억 달러로 성장하고, 예측 기간 중 연평균 복합 성장률(CAGR)은 5.1%를 나타낼 전망입니다.

바륨 티타네이트(BaTiO3)는 가장 널리 사용되는 무연 압전 세라믹 재료 중 하나입니다. 이는 첨단 전자 세라믹 개발의 기초 소재로 사용됩니다. 바륨 티타네이트는 뛰어난 유전 특성, 강유전 특성 및 압전 특성을 나타내므로, 센서, 액추에이터, 커패시터 및 전기 세라믹 용도에 적합합니다. 다층 세라믹 커패시터, 센서, 액추에이터, 초음파 트랜스듀서, 서미스터, 전기광학 소자 및 에너지 저장 용도로 널리 사용되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만 달러), 수량(천 톤) |

| 부문 | 유형별, 최종 이용 산업별, 지역별 |

| 대상 지역 | 유럽, 북미, 아시아태평양, 중동 및 아프리카, 남미 |

전자 산업 분야에서 이는 MLCC 제조, 특히 스마트폰, 노트북, 통신 기기, 자동차용 전자기기 및 기타 기기에 사용되는 가장 중요한 유전체 재료 중 하나입니다. 또한 초음파 진단 장치, 산업용 감시 장치, 압전 부저, 저전력 전자 기기 등 다양한 시스템에도 응용되고 있습니다.

“금액 기준으로는 산업 및 제조 분야가 최종 용도로서 압전 세라믹 시장 전체에서 가장 큰 점유율을 차지했습니다. '

산업 및 제조 부문은 자동화, 고정밀 센싱, 상태 모니터링, 그리고 스마트 제조 도구의 적극적인 도입에 힘입어 압전 세라믹의 최종 용도 시장을 형성하고 있습니다. 압전 세라믹는 산업용 센서, 초음파 세척 시스템, 진동 모니터링 장치, 액추에이터, 유량계, 비파괴 검사 장치 및 고정밀 위치 결정 시스템 등의 부품과 시스템에 널리 사용되고 있습니다. 산업 및 제조 분야에 대한 투자 확대와 더불어, 인더스트리 4.0, 로봇 공학, 예측 유지보수 시스템의 도입이 진행됨에 따라 고성능 압전 부품에 대한 수요가 급증하고 있습니다. 또한, 반도체 산업, 산업용 로봇, 에너지 절약형 생산 시스템에 대한 투자 확대 역시 현대 제조 업무에서 압전 세라믹 기술의 통합을 더욱 촉진하고 있습니다.

“아시아태평양은 예측 기간 동안 가장 큰 시장 점유율을 차지할 것으로 예측됩니다.

아시아태평양은 압전 세라믹의 주요 시장입니다. 이 지역은 국방 투자 및 현대화 프로그램의 확대, 산업화와 성장에 대한 정부의 강력한 추진, 그리고 산업 및 제조 부문에 대한 막대한 투자에 힘입어 크게 성장하고 있습니다. 또한, 아시아태평양은 원자재, 부품 및 모듈 제조, 시스템 통합사업자, 그리고 대규모 최종 사용 산업에 걸쳐 구축된 생태계의 혜택을 누리고 있습니다.

본 보고서에서는 주요 기업 프로파일에 대한 종합적인 분석을 제공합니다.

주요 기업으로는 KYOCERA Corporation(일본), CeramTec GmbH(독일), CTS Corporation(미국), Murata Manufacturing(일본), TDK Corporation(일본), Physik Instrumente(PI) GmbH & Co.(독일), APC International, Ltd.(미국), L3Harris Technologies, Inc.(미국), Meggitt PLC(영국), Piezo Technologies(미국), Tayca Corporation(일본) 등이 있습니다.

조사 범위

본 보고서에서는 시장 성장 촉진요인, 억제요인, 과제 및 성장 기회를 포함하여 압전 세라믹 시장의 성장을 좌우하는 주요 요인에 대한 상세한 정보를 제공합니다. 주요 업계 기업들을 철저히 분석하여 각사의 사업 개요, 솔루션 및 서비스, 주요 전략, 계약, 파트너십, 합의 내용에 대한 인사이트를 제공합니다. 또한 신제품 출시, 합병 및 인수, 그리고 압전 세라믹 시장의 최근 동향에 대해서도 다루고 있습니다. 본 보고서에는 압전 세라믹 시장 생태계에서 두각을 나타내고 있는 스타트업 기업에 대한 경쟁 분석도 포함되어 있습니다.

이 보고서를 구매해야 하는 이유:

본 보고서는 시장 선도 기업 및 신규 진출기업을 대상으로 압전 세라믹 시장 전체 및 그 하위 부문의 매출에 관한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 파악하고, 자사의 비즈니스를 보다 효과적으로 포지셔닝하며, 적절한 시장 진출 전략을 수립하는 데 필요한 인사이트를 얻을 수 있습니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악할 수 있도록 지원하며, 주요 시장 성장 촉진요인, 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 주요 촉진요인(민간용 전자기기 부문의 급속한 성장, 전 세계 방위 예산 증가 및 현대화 프로그램), 제약 요인(납 기반 재료와 관련된 환경 및 규제상의 우려), 기회(IoT의 급속한 확산), 그리고 과제(재료의 안정성 및 성능 관련 문제)에 대한 분석

- 제품 개발/혁신 : 압전 세라믹 시장의 향후 기술, 연구 개발 활동 및 서비스 출시와 관련된 심층적인 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역의 압전 세라믹 시장을 분석하고 있습니다

- 시장의 다각화 : 압전 세라믹 시장의 서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : KYOCERA Corporation(일본), CeramTec GmbH(독일), CTS Corporation(미국), Murata Manufacturing(일본), TDK Corporation(일본), Physik Instrumente(PI) GmbH & Co.(독일), APC International, Ltd.(미국), L3Harris Technologies, Inc.(미국), Meggitt PLC(영국), Piezo Technologies(미국), Tayca Corporation(일본) 등, 압전 세라믹 시장의 주요 기업들 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 압전 세라믹 시장(유형별)

제6장 압전 세라믹 시장(용도별)

제7장 압전 세라믹 시장(지역별)

제8장 경쟁 구도

제9장 기업 개요

제10장 조사 방법

제11장 부록

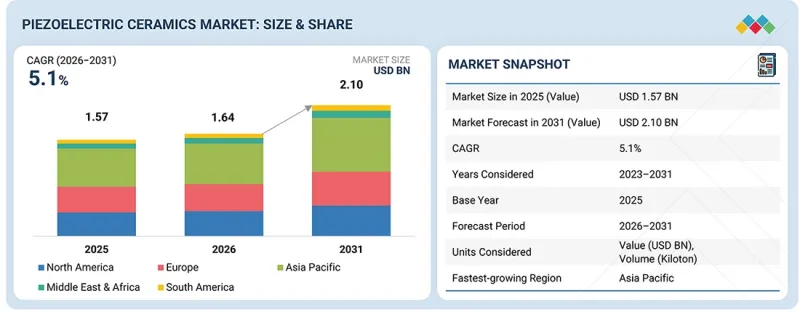

LSHThe piezoelectric ceramics market is projected to grow from USD 1.64 billion in 2026 to USD 2.10 billion by 2031, at a CAGR of 5.1% during the forecast period. Barium titanate (BaTiO3) is one of the most widely used lead-free piezoelectric ceramic materials. It serves as a base material in the development of advanced electronic ceramics. Barium titanate exhibits strong dielectric, ferroelectric, and piezoelectric properties, making it suitable for sensing, actuation, capacitor, and electroceramic applications. It is widely used in multilayer ceramic capacitors, sensors, actuators, ultrasonic transducers, thermistors, electro-optic devices, and energy storage applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million), Volume (Kiloton) |

| Segments | By Type, End-use Industry, and Region |

| Regions covered | Europe, North America, Asia Pacific, Middle East & Africa, and South America |

In the electronics industry, it is one of the most important dielectric materials used in MLCC manufacturing, particularly in smartphones, laptops, communication equipment, automotive electronics, and other devices. It also finds applications in various systems such as ultrasound systems, industrial monitoring equipment, piezoelectric buzzers, and low-power electronic devices.

''In terms of value, industrial and manufacturing as end-use accounted for the largest share of the overall piezoelectric ceramics market.''

The industrial and manufacturing sectors represent end-use markets for piezoelectric ceramics, driven by strong adoption of automation, precision sensing, condition monitoring, and smart manufacturing tools. Piezoelectric ceramics are widely used in components and systems such as industrial sensors, ultrasonic cleaning systems, vibration monitoring devices, actuators, flow meters, non-destructive testing equipment, and precision positioning systems. Growing investment in the industrial and manufacturing sectors, coupled with the implementation of Industry 4.0, robotics, and predictive maintenance systems, is accelerating demand for high-performance piezoelectric components. Additionally, growing investment in the semiconductor industry, industrial robotics, and energy-efficient production systems is further supporting the integration of piezoelectric ceramic-based technologies across modern manufacturing operations.

"Asia Pacific is projected to account for the largest market share during the forecast period.

Asia Pacific is the key market for piezoelectric ceramics. It is strongly driven by growing defense investments and modernization programs, a strong government focus on industrialization and growth, and significant investment in the industrial and manufacturing sectors. Also, Asia Pacific benefits from a well-established ecosystem spanning raw materials, component and module manufacturing, system integrators, and large end-use industries.

This study has been validated through primary interviews with industry experts globally. These primary sources have been divided into the following three categories:

- By Company Type - Tier 1- 40%, Tier 2- 30%, and Tier 3- 30%

- By Designation - Director Level- 70%, , Managers- 20% and Others- 10%

- By Region- North America- 20%, Europe- 30%, Asia Pacific- 30%, Middle East & Africa- 10%, and Latin America- 10%

The report provides a comprehensive analysis of company profiles:

Prominent companies are KYOCERA Corporation (Japan), CeramTec GmbH (Germany), CTS Corporation (US), Murata Manufacturing Co., Ltd (Japan), TDK Corporation (Japan), Physik Instrumente (PI) GmbH & Co. (Germany), APC International, Ltd. (US), L3Harris Technologies, Inc. (US), Meggitt PLC (UK), Piezo Technologies (US), and Tayca Corporation (Japan)

Study Coverage

This report provides detailed information on the major factors shaping the growth of the piezoelectric ceramics market, including drivers, restraints, challenges, and opportunities. A thorough examination of key industry players is presented to provide insights into their business overviews, solutions and services, key strategies, contracts, partnerships, and agreements. Product launches, mergers and acquisitions, and recent developments in the piezoelectric ceramics market are also covered. This report includes a competitive analysis of upcoming startups in the piezoelectric ceramics market ecosystem.

Reasons to buy this report:

The report will provide market leaders and new entrants with the closest approximations of revenue for the overall piezoelectric ceramics market and its subsegments. It will help stakeholders understand the competitive landscape and gain insights to position their businesses more effectively and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (rapid expansion of consumer electronics sector, rising global defense budgets and modernization programs), restraints (environmental and regulatory concerns associated with lead-based materials), opportunities (rapid expansion of IoT), and challenges (material stability and performance issues)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and service launches in the piezoelectric ceramics market

- Market Development: Comprehensive information about lucrative markets - the report analyzes the piezoelectric ceramics market across varied regions

- Market Diversification: Exhaustive information about services, untapped geographies, recent developments, and investments in the piezoelectric ceramics market

- Competitive Assessment: In-depth assessment of market share, growth strategies and service offerings of leading players such as KYOCERA Corporation (Japan), CeramTec GmbH (Germany), CTS Corporation (US), Murata Manufacturing Co., Ltd (Japan), TDK Corporation (Japan), Physik Instrumente (PI) GmbH & Co. (Germany), APC International, Ltd. (US), L3Harris Technologies, Inc. (US), Meggitt PLC (UK), Piezo Technologies (US), and Tayca Corporation (Japan), among others in the piezoelectric ceramics market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS OF STUDY

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING PIEZOELECTRIC CERAMICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PIEZOELECTRIC CERAMICS MARKET PLAYERS

- 3.2 PIEZOELECTRIC CERAMICS MARKET, BY TYPE

- 3.3 PIEZOELECTRIC CERAMICS MARKET, BY END-USE INDUSTRY

- 3.4 PIEZOELECTRIC CERAMICS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid expansion of consumer electronics sector

- 4.2.1.2 Rising global defense budgets and modernization programs

- 4.2.1.3 Rising demand from medical industry

- 4.2.1.4 Growth of automotive industry and vehicle electrification

- 4.2.2 RESTRAINTS

- 4.2.2.1 Environmental and regulatory concerns associated with lead-based materials

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Development and commercialization of lead-free piezoelectric materials and textured piezoceramics

- 4.2.3.2 Growing adoption of wearable electronics and miniaturized devices

- 4.2.3.3 Rapid expansion of IoT (Internet of Things)

- 4.2.3.4 Rapid expansion of 5G infrastructure and next-generation RF filter technologies

- 4.2.3.5 Energy harvesting for self-powered devices

- 4.2.4 CHALLENGES

- 4.2.4.1 Complexity of manufacturing and material processing

- 4.2.4.2 Material stability and performance issues

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN PIEZOELECTRIC CERAMICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.3 EMERGING BUSINESS MODELS

- 4.5 VALUE CHAIN ANALYSIS

- 4.6 PORTER'S FIVE FORCES ANALYSIS

- 4.6.1 THREAT OF NEW ENTRANTS

- 4.6.2 THREAT OF SUBSTITUTES

- 4.6.3 BARGAINING POWER OF SUPPLIERS

- 4.6.4 BARGAINING POWER OF BUYERS

- 4.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 4.7 PATENT ANALYSIS

- 4.7.1 METHODOLOGY

- 4.7.2 DOCUMENT TYPES

- 4.7.3 PUBLICATION TRENDS IN LAST 10 YEARS

- 4.7.4 INSIGHTS

- 4.7.5 JURISDICTION ANALYSIS

- 4.7.6 TOP 10 PATENT OWNERS IN LAST 10 YEARS

- 4.8 ECOSYSTEM/MARKET MAP

- 4.9 TRADE ANALYSIS

- 4.9.1 IMPORT SCENARIO FOR HS CODE 854160

- 4.9.2 EXPORT SCENARIO FOR HS CODE 854160

- 4.10 MACROECONOMIC OVERVIEW AND KEY TRENDS

- 4.10.1 SEMICONDUCTOR MANUFACTURING PLANTS

- 4.10.2 CELL PHONES

- 4.10.3 GDP TRENDS AND FORECASTS

- 4.11 PRICING ANALYSIS

- 4.11.1 AVERAGE SELLING PRICE TREND, BY REGION

- 4.11.2 AVERAGE SELLING PRICE TREND, BY END-USE INDUSTRY

- 4.12 TECHNOLOGY ANALYSIS

- 4.12.1 KEY EMERGING TECHNOLOGIES

- 4.12.1.1 Thin-film deposition technologies

- 4.12.1.2 Nanoengineering

- 4.12.2 COMPLEMENTARY TECHNOLOGIES

- 4.12.2.1 MEMS (Micro-Electro-Mechanical System)

- 4.12.1 KEY EMERGING TECHNOLOGIES

- 4.13 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 4.14 KEY CONFERENCES & EVENTS

- 4.15 SUSTAINABILITY INITIATIVES & REGULATORY LANDSCAPE

- 4.15.1 REGULATIONS

- 4.15.1.1 North America

- 4.15.1.2 Europe

- 4.15.1.3 Asia Pacific

- 4.15.1.4 Middle East & Africa and South America

- 4.15.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 4.15.1 REGULATIONS

- 4.16 KEY STAKEHOLDERS & BUYING CRITERIA

- 4.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 4.16.2 BUYING CRITERIA

- 4.16.2.1 Quality

- 4.16.2.2 Service

- 4.17 CASE STUDY ANALYSIS

- 4.17.1 CRYOGENIC AND EXTREME TEMPERATURE APPLICATIONS

- 4.18 IMPACT OF 2025 US TARIFF - OVERVIEW

- 4.18.1 INTRODUCTION

- 4.18.2 KEY TARIFF RATES

- 4.18.3 PRICE IMPACT ANALYSIS

- 4.18.4 IMPACT ON KEY COUNTRIES/REGIONS

- 4.18.4.1 US

- 4.18.4.2 Europe

- 4.18.4.3 Asia Pacific

- 4.18.5 IMPACT ON END-USE INDUSTRIES

- 4.19 INVESTMENT AND FUNDING SCENARIO

- 4.20 KEY INSIGHTS ON AEROSPACE & DEFENSE INDUSTRY

- 4.20.1 QUALITATIVE & QUANTITATIVE INSIGHTS/DEVELOPMENTS: KEY DEFENSE-SPENDING COUNTRIES SUCH AS US, CHINA, INDIA, RUSSIA, AND MAJOR EUROPEAN NATIONS

- 4.20.2 ADOPTION/PREFERENCE OF DIFFERENT PRODUCTS/TYPES OF PIEZOELECTRIC CERAMICS IN DIFFERENT APPLICATIONS WITHIN AEROSPACE & DEFENSE

- 4.21 US: DEFENSE VALUE CHAIN MAPPING-PIEZOELECTRIC CERAMIC TO END USER

- 4.22 EMERGING ALTERNATIVE TO PIEZOELECTRIC CERAMICS

5 PIEZOELECTRIC CERAMICS MARKET, BY TYPE

- 5.1 INTRODUCTION

- 5.2 BARIUM TITANATE

- 5.2.1 KEY MATERIAL DRIVING INNOVATION IN CAPACITORS AND PIEZOELECTRIC DEVICES

- 5.3 POTASSIUM NIOBATE

- 5.3.1 ENHANCEMENT AND FUNCTIONAL APPLICATIONS OF POTASSIUM NIOBATE-BASED LEAD-FREE FERROELECTRIC MATERIALS

- 5.4 LEAD ZIRCONATE TITANATE

- 5.4.1 DOMINATES MARKET WITH HIGH-PERFORMANCE PIEZOELECTRIC CAPABILITIES

- 5.5 SODIUM TUNGSTATE

- 5.5.1 STABILITY UNDER HIGH-TEMPERATURE CONDITIONS TO DRIVE DEMAND

- 5.6 OTHERS

6 PIEZOELECTRIC CERAMICS MARKET, BY END-USE INDUSTRY

- 6.1 INTRODUCTION

- 6.2 CONSUMER ELECTRONICS

- 6.2.1 CONSUMER ELECTRONICS DRIVING INNOVATION AND DEMAND FOR PIEZOELECTRIC CERAMICS

- 6.3 INDUSTRIAL & MANUFACTURING

- 6.3.1 HUGE INVESTMENT AND STRONG GROWTH IN INDUSTRIAL & MANUFACTURING SEGMENT TO DRIVE DEMAND

- 6.4 AUTOMOTIVE

- 6.4.1 INCREASED DEMAND FOR ELECTRIC VEHICLES TO DRIVE MARKET

- 6.5 MEDICAL

- 6.5.1 RISE IN HEALTHCARE SPENDING TO DRIVE DEMAND

- 6.6 DEFENSE

- 6.6.1 RISING DEFENSE MODERNIZATION AND DRONE WARFARE TO DRIVE DEMAND

- 6.6.2 SONAR & UNDERWATER SYSTEMS

- 6.6.3 AEROSPACE ACTUATORS

- 6.6.4 DEFENSE SENSING AND MONITORING SYSTEMS & OTHERS

- 6.7 OTHERS

7 PIEZOELECTRIC CERAMICS MARKET, BY REGION

- 7.1 INTRODUCTION

- 7.2 NORTH AMERICA

- 7.2.1 US

- 7.2.1.1 Strong and stable end-use industry to drive market

- 7.2.2 CANADA

- 7.2.2.1 High focus on strengthening defense segment to drive market

- 7.2.3 MEXICO

- 7.2.3.1 Strong growth in electronics industry to drive market growth

- 7.2.1 US

- 7.3 EUROPE

- 7.3.1 GERMANY

- 7.3.1.1 Strong focus on strengthening national air and missile defense capabilities to fuel market growth

- 7.3.2 UK

- 7.3.2.1 Strong government focus on digitalization to support market growth

- 7.3.3 FRANCE

- 7.3.3.1 Growing military spending to drive demand

- 7.3.4 ITALY

- 7.3.4.1 Increasing investment in defense spending and growing semiconductor industry to support market growth

- 7.3.5 SPAIN

- 7.3.5.1 Growing military spending to drive demand

- 7.3.6 REST OF EUROPE

- 7.3.1 GERMANY

- 7.4 ASIA PACIFIC

- 7.4.1 CHINA

- 7.4.1.1 Rapid expansion of defense capabilities and strong automotive sector to increase consumption

- 7.4.2 JAPAN

- 7.4.2.1 Strong focus on electronics industry and increasing defense capabilities to drive market

- 7.4.3 INDIA

- 7.4.3.1 Government initiatives and growing consumer electronics industry to drive market

- 7.4.4 SOUTH KOREA

- 7.4.4.1 Strong growth in electronics sector to support market growth

- 7.4.5 AUSTRALIA

- 7.4.5.1 Significant investments in defense sector to fuel market expansion

- 7.4.6 REST OF ASIA PACIFIC

- 7.4.1 CHINA

- 7.5 MIDDLE EAST & AFRICA

- 7.5.1 GCC

- 7.5.1.1 Saudi Arabia

- 7.5.1.1.1 Strong focus on local manufacturing and increasing spending on defense to propel demand

- 7.5.1.1 Saudi Arabia

- 7.5.2 SOUTH AFRICA

- 7.5.2.1 Strong focus on automotive industry to drive market

- 7.5.3 REST OF MIDDLE EAST & AFRICA

- 7.5.1 GCC

- 7.6 SOUTH AMERICA

- 7.6.1 BRAZIL

- 7.6.1.1 Growing consumer electronics sector to drive market

- 7.6.2 ARGENTINA

- 7.6.2.1 Favorable business environment and growing end-use industries to drive market

- 7.6.3 REST OF SOUTH AMERICA

- 7.6.1 BRAZIL

8 COMPETITIVE LANDSCAPE

- 8.1 OVERVIEW

- 8.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 8.3 REVENUE ANALYSIS, 2022-2024

- 8.4 MARKET SHARE ANALYSIS OF TOP FIVE PLAYERS (2025)

- 8.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 8.5.1 STARS

- 8.5.2 EMERGING LEADERS

- 8.5.3 PERVASIVE PLAYERS

- 8.5.4 PARTICIPANTS

- 8.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 8.5.5.1 Company footprint

- 8.5.5.2 Region footprint

- 8.5.5.3 End-use industry footprint

- 8.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 8.6.1 PROGRESSIVE COMPANIES

- 8.6.2 RESPONSIVE COMPANIES

- 8.6.3 DYNAMIC COMPANIES

- 8.6.4 STARTING BLOCKS

- 8.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 8.6.5.1 Detailed list of key startups/SMEs

- 8.6.5.2 Competitive benchmarking of key startups/SMEs

- 8.7 COMPANY VALUATION AND FINANCIAL METRICS

- 8.8 BRAND/PRODUCT COMPARISON

- 8.9 COMPETITIVE SCENARIO

- 8.9.1 PRODUCT LAUNCHES

- 8.9.2 DEALS

- 8.9.3 EXPANSIONS

9 COMPANY PROFILES

- 9.1 KEY PLAYERS

- 9.1.1 KYOCERA CORPORATION

- 9.1.1.1 Business overview

- 9.1.1.2 Products offered

- 9.1.1.3 Recent developments

- 9.1.1.3.1 Deals

- 9.1.1.3.2 Expansions

- 9.1.1.4 MnM view

- 9.1.1.4.1 Key strengths

- 9.1.1.4.2 Strategic choices

- 9.1.1.4.3 Weaknesses and competitive threats

- 9.1.2 CERAMTEC GMBH

- 9.1.2.1 Business overview

- 9.1.2.2 Products offered

- 9.1.2.3 Recent developments

- 9.1.2.3.1 Product launches

- 9.1.2.3.2 Expansions

- 9.1.2.4 MnM view

- 9.1.2.4.1 Key strengths

- 9.1.2.4.2 Strategic choices

- 9.1.2.4.3 Weaknesses and competitive threats

- 9.1.3 CTS CORPORATION

- 9.1.3.1 Business overview

- 9.1.3.2 Products offered

- 9.1.3.3 Recent developments

- 9.1.3.3.1 Product launches

- 9.1.3.3.2 Deals

- 9.1.3.4 MnM view

- 9.1.3.4.1 Key strengths

- 9.1.3.4.2 Strategic choices

- 9.1.3.4.3 Weaknesses and competitive threats

- 9.1.4 MURATA MANUFACTURING CO., LTD.

- 9.1.4.1 Business overview

- 9.1.4.2 Products offered

- 9.1.4.3 Recent developments

- 9.1.4.3.1 Deals

- 9.1.4.4 MnM view

- 9.1.4.4.1 Key strengths

- 9.1.4.4.2 Strategic choices

- 9.1.4.4.3 Weaknesses and competitive threats

- 9.1.5 TDK CORPORATION

- 9.1.5.1 Business overview

- 9.1.5.2 Products offered

- 9.1.5.3 Recent developments

- 9.1.5.3.1 Deals

- 9.1.5.4 MnM view

- 9.1.5.4.1 Key strengths

- 9.1.5.4.2 Strategic choices

- 9.1.5.4.3 Weaknesses and competitive threats

- 9.1.6 PHYSIK INSTRUMENTE (PI) GMBH & CO. (SUBSIDIARY OF HOERBIGER)

- 9.1.6.1 Business overview

- 9.1.6.2 Products offered

- 9.1.6.3 Recent developments

- 9.1.6.3.1 Deals

- 9.1.6.3.2 Expansions

- 9.1.6.4 MnM view

- 9.1.7 APC INTERNATIONAL, LTD.

- 9.1.7.1 Business overview

- 9.1.7.2 Products offered

- 9.1.7.3 MnM view

- 9.1.8 L3HARRIS TECHNOLOGIES, INC.

- 9.1.8.1 Business overview

- 9.1.8.2 Products offered

- 9.1.8.3 Recent developments

- 9.1.8.3.1 Deals

- 9.1.8.3.2 Expansions

- 9.1.8.4 MnM view

- 9.1.9 MEGGITT PLC (SUBSIDIARY OF PARKER GROUP)

- 9.1.9.1 Business overview

- 9.1.9.2 Products offered

- 9.1.9.3 Recent developments

- 9.1.9.3.1 Expansions

- 9.1.9.4 MnM view

- 9.1.10 PIEZO TECHNOLOGIES

- 9.1.10.1 Business overview

- 9.1.10.2 Products offered

- 9.1.10.3 MnM view

- 9.1.11 TAYCA CO. LTD.

- 9.1.11.1 Business overview

- 9.1.11.2 Products offered

- 9.1.11.3 Recent developments

- 9.1.11.3.1 Expansions

- 9.1.11.4 MnM view

- 9.1.1 KYOCERA CORPORATION

- 9.2 OTHER PLAYERS

- 9.2.1 PIEZO DIRECT

- 9.2.2 FUJI CERAMICS CORPORATION

- 9.2.3 PZT ELECTRONIC CERAMIC CO., LTD.

- 9.2.4 SPARKLER CERAMICS PVT. LTD.

- 9.2.5 PIEZO KINETICS, INC.

- 9.2.6 SIANSONIC

- 9.2.7 SENSORTECH CANADA

- 9.2.8 OMEGA PIEZO TECHNOLOGIES

- 9.2.9 CENTRAL ELECTRONICS LIMITED

- 9.2.10 EBL PRODUCTS, INC.

- 9.2.11 DEL PIEZO SPECIALTIES LLC

- 9.2.12 NITERRA CO., LTD.

- 9.2.13 KUNSHAN RISHENG ELECTRONIC CO., LTD.

- 9.2.14 ZIBO YUHAI ELECTRONIC CERAMICS CO., LTD.

- 9.2.15 NINGBO FBELE ELECTRONICS CO., LTD.

10 RESEARCH METHODOLOGY

- 10.1 RESEARCH DATA

- 10.1.1 SECONDARY DATA

- 10.1.1.1 Key data from secondary sources

- 10.1.2 PRIMARY DATA

- 10.1.2.1 Key data from primary sources

- 10.1.2.2 Key industry insights

- 10.1.2.3 Breakdown of primary interviews

- 10.1.1 SECONDARY DATA

- 10.2 MARKET SIZE ESTIMATION

- 10.2.1 BOTTOM-UP APPROACH

- 10.2.2 TOP-DOWN APPROACH

- 10.3 DATA TRIANGULATION

- 10.4 STUDY ASSUMPTIONS

- 10.5 RESEARCH LIMITATIONS

11 APPENDIX

- 11.1 DISCUSSION GUIDE

- 11.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 11.3 CUSTOMIZATION OPTIONS

- 11.4 RELATED REPORTS

- 11.5 AUTHOR DETAILS