|

시장보고서

상품코드

2062144

압전 세라믹 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Piezoelectric Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

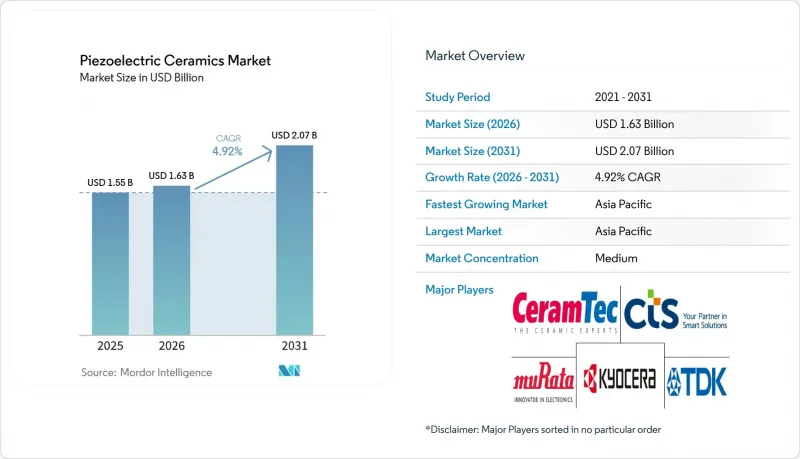

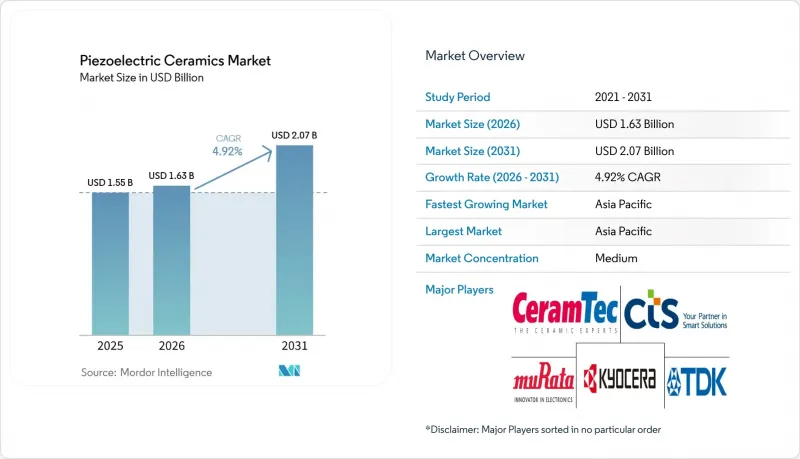

Mordor Intelligence에 의하면, 압전 세라믹 시장 규모는 2025년 15억 5,000만 달러, 2026년 16억 3,000만 달러에서 2031년까지 20억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.92%를 나타낼 것으로 예측됩니다.

본 보고서는 재료 구성(납 함유 및 무연), 용도(센서, 액추에이터, 에너지 하베스터 및 나노 발전기 등), 최종 사용자 산업(소비자 가전, 자동차 및 e-모빌리티 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 압전 세라믹 시장 동향 및 분석

의료용 영상 진단 장비 및 치료용 기기에서의 도입 확대

병원들이 휴대용 솔루션을 요구하는 가운데, 소형 초음파 기기에서 압전 세라믹이 기존의 트랜스듀서 소재를 대체하는 추세가 강해지고 있습니다. 무연 KNN 세라믹는 웨어러블 초음파 패치에서 d33 값 630 pC/N을 달성하여, 감도를 유지하면서도 독성에 대한 우려를 해소하고 있습니다. CMOS 공정으로 제조된 pMUT는 생산 비용을 절감하고, 현장 진단용 스캐너의 신호 통합 과정을 간소화합니다. 고강도 집속 초음파(HIFU) 시스템에는 현재 150mm가 넘는 CeramTec사의 반구형 디스크가 채택되어 있으며, 종양 절제에 필요한 전력 밀도 요건을 충족하고 있습니다. 미국 및 EU의 생체 적합성 규제로 인해 무연 BNT-BT 복합 소재로의 전환이 가속화되고 있습니다. 이 소재는 더 낮은 구동 온도에서도 PZT와 동등한 출력을 구현합니다. 그 결과, 장비 제조업체들은 성능 면과 규제 준수 면에서 모두 이점을 얻고 있으며, 압전 세라믹 시장을 확대되고 있습니다.

5G/6G RF 필터의 소형화에는 고유전율 압전 세라믹이 필요합니다.

mm파 기술 구현을 위해서는 1mm² 미만의 스마트폰 모듈 내에 탑재될 수 있는 고Q값 BAW 및 SAW 필터용 AlScN 및 LiNbO₃ 박막이 필요합니다. AlScN의 kt2가 10%를 초과함으로써, 대역이 혼잡한 주파수 할당 환경에서 휴대전화 제조업체가 필요로 하는 더 가파른 롤오프 특성을 얻을 수 있습니다. LiNbO3 LLSAW 필터는 6GHz 미만의 대역에 최적화되어 있으며, 석영에 비해 뛰어난 전력 처리 능력을 제공합니다. 후지필름의 니오브 첨가 PZT 다층막에 관한 2025년 특허는 7V 미만에서 d31이 389 pC/V를 달성하여, 저전압 모바일 전자기기의 요구 사항을 충족하고 있습니다. 6G 연구 개발 과정에서 주파수 대역이 급속히 확대됨에 따라 지속적인 수요가 보장되고, 이는 압전 세라믹 시장의 장기적인 성장을 뒷받침하고 있습니다.

PVDF계 피에조 폴리머와의 경쟁

PVDF의 유연성, 경량성 및 FDA 승인은 웨어러블 기기, 소프트 로보틱스 및 임베디드 센서로의 적용을 촉진하고 있으며, 경질 세라믹의 입지를 위협하고 있습니다. 이 d33 값은 20-30 pC/N으로 PZT보다 훨씬 낮아, 저전력 용도에는 충분합니다. 용액 주조나 일렉트로스피닝과 같은 비용 효율적인 제조 공정을 통해, 소비자 브랜드들은 폴리머 필름의 도입을 확대되고 있습니다. 이러한 엔트리 레벨 용도로의 전환은 가격 경쟁을 심화시켜, 압전 세라믹 시장 전체의 이익률에 부담을 주고 있습니다.

부문별 분석

2025년 현재, 납계 시스템은 압전 세라믹 시장 점유율의 81.11%를 차지하고 있으며, 이 점유율은 2031년까지 연평균 성장률(CAGR) 5.14%로 확대될 것으로 전망됩니다. PZT의 d33 값이 600 pC/N을 초과한다는 벤치마크 기준에 따라, 납계 제품 시장 규모는 전체 시장보다 더 빠르게 확대되고 있습니다. 후지필름의 7V 미만 다층 액추에이터 관련 특허에서 알 수 있듯이, 각 제조업체들은 니오브 등의 도판트를 사용하여 성능 향상을 꾀하고 있습니다. 향후 발생할 수 있는 규정 준수 위험을 줄이기 위해 무연화 프로그램이 병행하여 개발되고 있지만, 의료용 영상 진단이나 소나와 같은 고성능 용도에서는 PZT의 우월성을 아직 따라잡지 못하고 있습니다.

BNT-BT 디스크는 40kHz 초음파 세척기에서 발열을 억제하면서도 PZT와 동등한 음향 출력을 나타내는 반면, KNN 소프트 그레이드는 수중 수신기를 대상으로 합니다. 큐리점이 650°C를 초과하는 비스무트 층상 강유전체는 유정 시추 검사 같은 극한 온도 환경에서의 사용을 가능하게 합니다. 그러나 소재 교체에는 형상, 전압, 수명 측면에서의 재인증이 필요하기 때문에 보급 속도는 둔화되고 있지만, 압전 세라믹 시장의 수년까지 성장세를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 매출의 52.22%를 차지해, 2031년까지 연평균 성장률(CAGR) 5.78%로 성장할 것으로 전망됩니다. 중국은 대량 생산되는 분말 및 저비용 디스크 생산에서 우위를 점하고 있으며, 일본은 다층 및 박막 정밀 부품을 전문으로 하고, 한국과 대만은 스마트폰 및 5G 모듈에 부품을 탑재하고 있습니다. 2026년 2월에 완공된 무라타 제작소의 2억 3,300만 달러 규모의 후쿠이 연구개발 시설은 티타네이트 바륨 및 PZT 기술 개발에 주력하며, 해당 지역의 리더십을 강화하고 있습니다. Sparkler Ceramics와 같은 인도 기업들은 산업용 센서 생산을 확대하고 있는 반면, 호주의 광산 기업들은 가혹한 환경에서도 견딜 수 있는 내환경형 센서에 대한 수요를 주도하고 있습니다.

북미 수요는 항공우주, 방위 및 의료용 초음파 응용 분야에 의해 주도되고 있습니다. ‘CHIPS법’에 따른 제조 인센티브는 반도체 생산과 클린룸 시설을 공유함으로써, 간접적으로 압전 세라믹 분야에도 혜택을 주고 있습니다. TDK가 애플 제품을 위해 미국에 신설한 생산 라인은 지정학적 불확실성이 커지는 가운데 현지 조달이라는 선택지의 매력을 여실히 보여주고 있습니다. 캐나다와 멕시코는 항공우주용 공구 및 자동차용 센서 조립을 통해 기여하며, 지역 압전 세라믹 시장을 뒷받침하고 있습니다.

유럽에서는 독일의 자동차 및 산업 자동화 분야와 영국의 항공우주 산업이 주도적인 역할을 하고 있습니다. CeramTec사는 소나용 대형 PZT 디스크의 생산을 확대하고 있으며, 한편 PI Ceramic사가 2025년 4월 BNT 및 KNN 소재 분야에서 진전을 이루면서 양사의 공동 프로젝트가 가속화되고 있습니다. EU의 엄격한 RoHS 규제로 인해, 다른 지역보다 더 빠르게 무연 대체재의 도입이 진행되고 있습니다. 또한, 브라질의 해상 에너지 프로젝트와 사우디아라비아의 스마트 시티 구상은 규모는 작지만, 세계 압전 세라믹 시장에서 전략적으로 중요한 수요를 창출하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the piezoelectric ceramics market size is projected to expand from USD 1.55 billion in 2025 and USD 1.63 billion in 2026 to USD 2.07 billion by 2031, registering a CAGR of 4.92% between 2026 to 2031.

This report is Segmented by Material Composition (Lead-Based and Lead-Free), Application (Sensors, Actuators, Energy Harvesters and Nanogenerators, and More), End-User Industry (Consumer Electronics, Automotive and E-Mobility, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Piezoelectric Ceramics Market Trends and Insights

Rising Adoption in Medical Imaging and Therapeutic Devices

Piezoelectric ceramics are increasingly replacing older transducer materials in compact ultrasound equipment as hospitals demand portable solutions. Lead-free KNN ceramics have achieved a d33 of 630 pC/N in wearable ultrasound patches, addressing toxicity concerns while maintaining sensitivity. pMUTs manufactured on CMOS lines reduce production costs and simplify signal integration in point-of-care scanners. High-intensity focused ultrasound systems now utilize CeramTec hemispherical discs larger than 150 mm, meeting power-density requirements for tumor ablation. Biocompatibility regulations in the United States and EU are accelerating the transition to lead-free BNT-BT composites, which match PZT power output at lower drive temperatures. As a result, device manufacturers are achieving both performance and compliance benefits, strengthening the piezoelectric ceramics market.

5G/6G RF-Filter Miniaturization Needs High-k Piezoceramics

Millimeter-wave rollouts require AlScN and LiNbO3 thin films for high-Q BAW and SAW filters that fit inside smartphone modules under 1 mm2. AlScN's kt2 exceeding 10% provides a sharper roll-off that handset OEMs need for crowded spectrum allocations. LiNbO3 LLSAW filters are optimized for sub-6 GHz bands, offering superior power handling compared to quartz. FUJIFILM's 2025 patent on niobium-doped PZT multilayers achieves a d31 of 389 pC/V below 7 V, aligning with the requirements of low-voltage mobile electronics. The rapid multiplication of frequency bands in 6G R&D ensures sustained demand, supporting long-term growth in the piezoelectric ceramics market.

Competition from PVDF-Based Piezopolymers

PVDF's flexibility, lightweight properties, and FDA clearance are driving its adoption in wearables, soft robotics, and implantable sensors, challenging rigid ceramics. While its d33 of 20-30 pC/N is significantly lower than PZT, it is sufficient for low-force applications. Cost-effective production methods such as solution casting and electrospinning are encouraging consumer brands to adopt polymer films. This shift toward entry-level applications intensifies price competition, exerting pressure on margins across the piezoelectric ceramics market.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local MLCC Capacity Using PZT Dielectrics

- Quantum Transducer R&D Drives Cryogenic Piezoceramic Demand

- Supply-Chain Volatility of Nb2O5 and Ta2O5 for Lead-Free KNN Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-based systems accounted for 81.11% of the piezoelectric ceramics market share in 2025, with this share projected to grow at a 5.14% CAGR through 2031. The market size for lead-based variants is expanding faster than the overall market due to PZT's benchmark-setting d33 values exceeding 600 pC/N. Manufacturers are enhancing performance through dopants like niobium, as demonstrated by FUJIFILM's sub-7 V multilayer actuator patent. Parallel lead-free programs are being developed to mitigate future compliance risks but have yet to challenge PZT's dominance in high-performance applications such as medical imaging and sonar.

BNT-BT discs have shown equivalent acoustic power to PZT in 40 kHz ultrasonic cleaners with reduced heat generation, while KNN soft grades are targeting underwater receivers. Bismuth-layered ferroelectrics, with Curie points above 650 °C, are enabling extreme-temperature applications like oil-well logging. However, each substitution requires requalification in terms of geometry, voltage, and lifetime, which slows adoption but supports a multi-year growth trajectory within the piezoelectric ceramics market.

Geography Analysis

Asia-Pacific generated 52.22% of global revenue in 2025 and is projected to grow at a 5.78% CAGR through 2031. China dominates in high-volume powder and low-cost disc production, Japan specializes in multilayer and thin-film precision parts, and South Korea and Taiwan integrate components into smartphones and 5G modules. Murata's USD 233 million Fukui R&D facility, completed in February 2026, focuses on barium titanate and PZT advancements, reinforcing the region's leadership. Indian companies like Sparkler Ceramics are scaling industrial sensor production, while Australian miners drive demand for ruggedized sensors in challenging environments.

North America's demand is driven by aerospace, defense, and medical ultrasound applications. The CHIPS Act's fabrication incentives have indirectly benefited piezoelectric ceramics by sharing cleanroom facilities with semiconductor production. TDK's new U.S. production line for Apple products underscores the appeal of local sourcing amid geopolitical uncertainties. Canada and Mexico contribute through aerospace tooling and automotive sensor assembly, supporting the regional piezoelectric ceramics market.

Europe is led by Germany's automotive and industrial automation sectors and the United Kingdom's aerospace industry. CeramTec is scaling up production of large-format PZT discs for sonar applications, while PI Ceramic's April 2025 advancements in BNT and KNN materials have spurred collaborative projects. Strict EU RoHS regulations are accelerating the adoption of lead-free alternatives faster than in other regions. Additionally, Brazil's offshore energy projects and Saudi Arabia's smart-city initiatives contribute smaller but strategically significant volumes to the global piezoelectric ceramics market.

- APC International Ltd.

- Arkema

- CeramTec GmbH

- CTS Corporation

- FUJI CERAMICS CORPORATION

- Johnson Matthey

- KEMET

- Kistler Group

- KYOCERA Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- Physik Instrumente (PI) SE & Co. KG

- PI Ceramic GmbH

- Piezosystem Jena GmbH

- SAMSUNG ELECTRO-MECHANICS

- Sensortech Canada

- Sparkler Ceramics Pvt. Ltd.

- TDK Corporation

- TRS Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising adoption in medical imaging and therapeutic devices

- 4.2.2 5G/6G RF-filter miniaturisation needs high-k piezoceramics

- 4.2.3 Government incentives for local MLCC capacity using PZT dielectrics

- 4.2.4 Quantum transducer R&D drives cryogenic piezoceramic demand

- 4.2.5 Additive manufacturing enables complex aerospace piezo meta-structures

- 4.3 Market Restraints

- 4.3.1 Competition from PVDF-based piezopolymers

- 4.3.2 Supply-chain volatility of Nb2O5 and Ta2O5 for lead-free KNN systems

- 4.3.3 High scrap rates in additive-manufactured piezoceramics scale-up

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Composition

- 5.1.1 Lead-based (PZT, PMN-PT, PZN-PT)

- 5.1.2 Lead-free (BNT-BT, KNN, BaTiO3, ZnO)

- 5.2 By Application

- 5.2.1 Sensors (pressure, ultrasonic, MEMS mics)

- 5.2.2 Actuators (fuel injectors, micro-positioners)

- 5.2.3 Energy Harvesters and Nanogenerators

- 5.2.4 Ultrasonic Imaging and Cleaning

- 5.2.5 Frequency Control and Timing (SAW/BAW resonators)

- 5.3 By End-user Industry

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive and E-Mobility

- 5.3.3 Healthcare and Life-Sciences

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Aerospace and Defense

- 5.3.6 Energy and Utilities

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 NORDIC Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 APC International Ltd.

- 6.4.2 Arkema

- 6.4.3 CeramTec GmbH

- 6.4.4 CTS Corporation

- 6.4.5 FUJI CERAMICS CORPORATION

- 6.4.6 Johnson Matthey

- 6.4.7 KEMET

- 6.4.8 Kistler Group

- 6.4.9 KYOCERA Corporation

- 6.4.10 Morgan Advanced Materials

- 6.4.11 Murata Manufacturing Co., Ltd.

- 6.4.12 Physik Instrumente (PI) SE & Co. KG

- 6.4.13 PI Ceramic GmbH

- 6.4.14 Piezosystem Jena GmbH

- 6.4.15 SAMSUNG ELECTRO-MECHANICS

- 6.4.16 Sensortech Canada

- 6.4.17 Sparkler Ceramics Pvt. Ltd.

- 6.4.18 TDK Corporation

- 6.4.19 TRS Technologies Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment