|

시장보고서

상품코드

2059325

동물용 초음파 진단 장비 시장 : 유형별, 제품 유형별, 기술별, 대상 동물별, 용도별, 최종사용자별, 지역별 - 예측(-2031년)Veterinary Ultrasound Market by Type, Product, Technology, Animal Type, Application, End User, and Region - Global Forecast to 2031 |

||||||

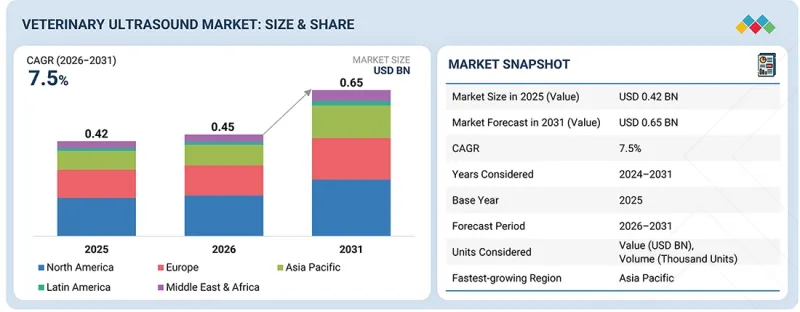

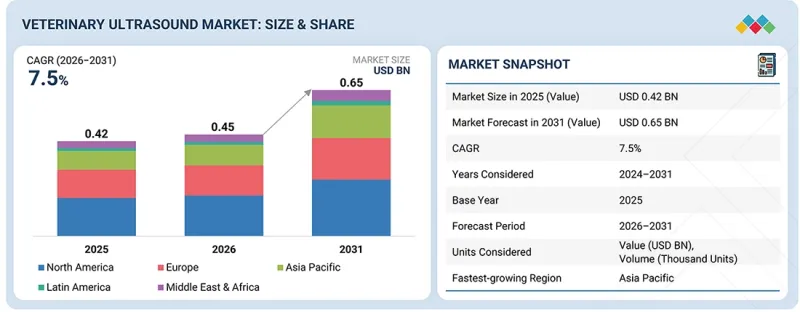

동물용 초음파 진단 장비 시장 규모는 2026년 4억 5,000만 달러에서 2031년까지 6억 5,000만 달러에 이르고, CAGR 7.5%를 기록할 것으로 예측됩니다.

이러한 성장은 동물 진단 영상, 예방 의료, 그리고 정밀 수의학의 미래를 형성하는 몇 가지 주요 요인에 의해 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 유형별, 제품 유형별, 기술별, 대상 동물별, 용도별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

동물용 초음파 진단기기 시장은 전 세계적으로 증가하는 반려동물 소유자, 특히 반려동물을 가족의 일원으로 여기는 젊은 층의 영향력을 크게 받고 있습니다. 그 결과, 고품질의 최신 수의학 서비스에 대한 수요가 증가하고 있으며, 동물병원에서는 질병을 조기에 정확하게 발견할 수 있도록 지원하기 위해 첨단 영상 진단 장비에 대한 투자가 확대되고 있습니다. 반려동물 주인들은 예방 및 진단 관리에 대한 관심이 높아지면서, 더욱 적극적으로 행동하고 있습니다. 또한 동물병원들도 임상 성과를 향상시킬 뿐만 아니라, 병원 내 진단 역량을 확립하기 위해 초음파 진단 장비 도입을 점차 확대되고 있습니다.

수요가 급격히 증가하고 있는 또 다른 중요한 요인은 반려동물의 만성 질환, 노화에 따른 질환, 그리고 생활 습관과 관련된 질환 증가입니다. 이에 따라 신속한 발견, 지속적인 모니터링, 그리고 효과적인 치료 계획이 필수적입니다. 고해상도 영상, 도플러 시스템, 휴대용 현장 진단 기기 등 첨단 초음파 기술을 도입함으로써 심장, 복부, 생식기, 근골격계 등 각 분야의 진단 정확도가 크게 향상되었습니다. 또한, 사례 수 증가에 대응하기 위해 보다 효율적이고 경제적인 영상 진단 솔루션에 대한 수요도 높아지고 있습니다.

초음파 진단 장치를 디지털 방식으로 연동하는 최근의 동향 또한 통합 솔루션의 풀 라인업 구축으로 이어지고 있습니다. 여기에는 AI를 활용한 이미지 분석, 클라우드 기반 이미지 저장, 원격 이미지 공유 등이 포함됩니다. 이러한 기술은 보다 신속하고 신뢰할 수 있는 진단을 가능하게 하며, 공동 진료 및 전문의와의 협진을 지원하고, 1차 진료부터 의뢰 진료에 이르기까지 고도의 영상 진단을 촉진합니다. 동물병원에서는 이러한 첨단 진단 솔루션이 도입되어 있으며, 그 결과 초음파 진단을 기반으로 한 수의학 치료의 전반적인 질과 효율이 지속적으로 향상되고 있습니다.

“기술별로는 디지털 영상 진단 부문이 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. '

동물용 초음파 진단기기 시장에서 디지털 영상 진단 부문이 가장 높은 성장률을 보일 것으로 예측됩니다. 이는 동물병원이 완전히 디지털화되고, 네트워크화된 진단 워크플로로 빠르게 전환되고 있기 때문입니다. 디지털 초음파 시스템에는 영상 획득 속도 향상, 화질 개선, 진료 관리 시스템과의 직접 연동, 원격 진료 및 전문의의 검토를 위한 스캔 데이터의 간편한 저장·공유 등 여러 가지 장점이 있습니다. 또한, AI를 활용한 영상 분석, 클라우드 연결, 소프트웨어 기반 업그레이드 역시 진료소나 병원에서 디지털 초음파 시스템의 도입을 가속화하고 있으며, 디지털 이미징은 가장 빠르게 성장하고 있는 기술 분야가 되었습니다.

“제품별로는 2025년에 기기 부문이 가장 큰 시장 점유율을 차지했습니다. '

2025년, 초음파 시스템은 동물병원 및 진료소에서 주요 진단 도구로 활용됨에 따라, 기기 부문이 동물용 초음파 진단기기 시장을 독점했습니다. 정기적인 서비스나 소모품에 비해 초음파 진단 장비나 프로브의 초기 구입 비용이 높기 때문에 시장 전체 수익에서 큰 비중을 차지하고 있습니다. 또한, 고해상도, 도플러 기능, 휴대용 형태를 갖춘 보다 첨단 시스템에 대한 투자와 병원 내 영상 진단 역량 강화를 위한 동물병원의 투자 증가로 인해, 장비 부문의 수익 기여도는 매우 높은 수준을 유지하고 있습니다.

“아시아태평양 지역은 예측 기간 동안 가장 높은 성장률을 보일 것으로 예측됩니다. '

아시아태평양은 동물용 초음파 진단기기 시장에서 가장 빠른 성장세를 보이고 있습니다. 아시아태평양 시장에서 이러한 성장이 이루어진 주된 요인은 중국, 인도 및 동남아시아 국가들의 반려동물 보유 수 증가, 소득 향상, 그리고 반려동물 건강에 대한 인식 제고입니다. 해당 지역에서는 수의학 시설의 확충, 민간 클리닉 및 전문센터 증가, 그리고 첨단 진단 장비에 대한 접근성 개선에 힘입어 초음파 시스템 도입이 활발히 진행되고 있습니다. 아시아태평양 시장이 강력한 성장을 이루고 있는 배경에는 동물의 만성 질환 및 감염병 증가뿐만 아니라, 전 세계 초음파 제조업체와 지역 유통업체들 시장 진출에 따른 투자 확대가 있습니다.

조사 범위

본 시장 조사는 여러 부문에 걸친 동물용 초음파 진단기기 시장을 대상으로 합니다. 본 조사는 유형, 제품, 기술, 대상 동물, 용도, 최종 사용자 및 지역별로 시장 규모 및 성장 잠재력을 추정하는 것을 목적으로 합니다. 또한, 시장 내 주요 기업에 대한 상세한 경쟁 분석 외에도 각 기업프로파일, 제품 유형 및 사업 내용에 관한 주요 관찰 사항, 최근 동향, 그리고 주요 시장 전략에 대해서도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

본 보고서는 기존 기업 및 신생·중소기업이 시장 동향을 파악하고 시장 점유율을 확대하는 데 도움이 됩니다. 본 보고서를 입수한 기업은 아래에 개요로 제시된 5가지 전략 중 1가지 이상을 실행할 수 있습니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다.

- 동물용 초음파 진단 기기 시장의 성장에 영향을 미치는 주요 촉진요인(반려동물 수 증가, 반려동물 보험에 대한 수요 증가, 반려동물 관리 지출 증가), 제약 요인(장비 및 시술 비용의 고가, 영상 품질 및 일관성에 영향을 미치는 조작자에 대한 의존도), 기회(신흥 시장의 성장 기회, 휴대용 및 현장 진단용 초음파 기기의 보급 확대), 과제(개발도상국의 동물 건강에 대한 인식 부족, 훈련된 전문가의 부족)에 대한 분석.

- 제품 개발/혁신 : 동물용 초음파 진단 기기 시장의 향후 기술 동향 및 신제품 출시에 관한 상세한 인사이트.

- 시장 개발: 수익성이 높은 신흥 시장에 대한 종합적인 정보. 본 보고서에서는 지역별 각종 동물용 초음파 제품 시장을 분석했습니다.

- 시장의 다양화: 제품, 미개척 지역, 최근 동향 및 동물용 초음파 진단 기기 시장에 대한 종합적인 정보

- 경쟁 분석 : 동물용 초음파 진단 기기 시장에서 주요 기업의 시장 점유율, 전략, 제품, 유통망 및 생산 능력에 대한 상세한 평가

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 그리고 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 현황과 구매 행동

제9장 동물용 초음파 기기 시장(유형별)

제10장 동물용 초음파 진단 장비 시장(제품별)

제11장 동물용 초음파 진단 장비 시장(기술별)

제12장 동물용 초음파 진단 장비 시장(대상 동물별)

제13장 동물용 초음파 진단 장비 시장(용도별)

제14장 동물용 초음파 진단 장비 시장(최종사용자별)

제15장 동물용 초음파 진단 장비 시장(지역별)

제16장 경쟁 구도

제17장 기업 개요

제18장 조사 방법

제19장 부록

LSH 26.06.25The veterinary ultrasound market is projected to grow from USD 0.45 billion in 2026 to USD 0.65 billion by 2031, at a CAGR of 7.5%. This growth is driven by several key factors shaping the future of veterinary diagnostic imaging, preventive care, and precision veterinary medicine.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | By Type, Product, Technology, Animal Type, Application, End User, Region |

| Regions covered | North America, Europe, APAC, LATAM, MEA |

The veterinary ultrasound market is significantly influenced by the growing number of pet owners worldwide, especially among young people who view pets as family members. As a result, demand for higher-quality, up-to-date veterinary services is rising, and clinics are investing in advanced diagnostic imaging to support early and accurate disease detection. Pet owners are becoming more aware and proactive in seeking preventive and diagnostic care, and veterinary practices are progressively equipping themselves with ultrasound systems to not only improve clinical outcomes but also establish in-house diagnostic capabilities.

Another important factor behind the dramatic increase in demand is the growing number of chronic, age-related, and lifestyle-associated conditions in pets, which has made rapid detection, continuous monitoring, and effective treatment planning necessary. By employing advanced ultrasound technologies, e.g., high-resolution imaging, Doppler systems, and handheld point-of-care devices, diagnostic accuracy has significantly improved in cardiac, abdominal, reproductive, and musculoskeletal applications. In addition, demand has risen for more efficient and economically viable imaging solutions to handle the increasing number of cases.

The recent trend of digitally linking ultrasound devices has also led to the creation of a full line of integrated solutions. These include AI-assisted image analysis, cloud-based image storage, and remote image sharing. They enable faster, more reliable diagnosis, support collaborative care and specialist consultations, and facilitate advanced imaging across primary care and referral settings. Veterinary practices are embracing these advanced diagnostic solutions, which naturally leads to continuous improvement in the overall quality and efficiency of ultrasound-based veterinary care.

"By technology, the digital imaging segment is projected to grow at the highest CAGR during the forecast period."

The digital imaging segment is expected to see the highest growth in the veterinary ultrasound market because veterinary practices have been rapidly transitioning to fully digital, connected diagnostic workflows. Digital ultrasound systems offer several advantages, including faster image acquisition, better image quality, direct integration with practice management systems, and easy storage and sharing of scans for remote doctor consultations and specialist review. AI-assisted image analysis, cloud connectivity, and software-based upgrades are also accelerating the adoption of digital ultrasound systems in clinics and hospitals, making digital imaging the fastest-growing technology segment.

"By product, the equipment segment accounted for the largest market share in 2025."

In 2025, the equipment segment dominated the veterinary ultrasound market because ultrasound systems serve as primary diagnostic tools in veterinary clinics and hospitals. Compared with recurring services and consumables, the initial high-cost purchases of ultrasound machines and probes account for a substantial share of overall market revenue. Furthermore, increasing investments by clinics in more sophisticated systems with higher resolution, Doppler features, and portable formats, as well as in expanding in-house diagnostic imaging, keep the equipment segment's revenue contribution very strong.

"The Asia Pacific region is expected to witness the highest growth rate during the forecast period."

The Asia Pacific region is growing at the fastest rate in the veterinary ultrasound market. The main drivers of this growth in the Asia Pacific market are increasing pet ownership, rising incomes, and greater awareness of pet health among people in China, India, and Southeast Asian nations. The region is seeing increased adoption of ultrasound systems due to expanded veterinary healthcare facilities, more private clinics and specialty centers, and better access to advanced diagnostic equipment. The Asia Pacific market is experiencing strong growth because of rising chronic and infectious diseases in animals, together with increasing investments from global ultrasound manufacturers and regional distributors entering the market.

Breakdown of supply-side primary interviews:

- By Company Type: Tier 1 (60%), Tier 2 (30%), and Tier 3 (10%)

- By Designation: C-level Executives (30%), Directors (50%), and Other Designations (20%)

- By Region: North America (45%), Europe (15%), Asia Pacific (25%), Latin America (10%), and the Middle East & Africa (5%)

Breakdown of demand-side primary interviews:

- By End User: Veterinary Clinics (50%), Veterinary Hospitals & Academic Institutes (33%), and Other End Users (17%)

By Designation: Veterinary Clinician / Diagnostic Imaging Specialist (47%), Medical Director or Practice Owner (22%), Procurement or Purchasing Manager (15%), and Others (16%)

- By Region: North America (25%), Europe (24%), Asia Pacific (25%), Latin America (11%), and the Middle East & Africa (15%)

Research Coverage

The market study covers the veterinary ultrasound market across multiple segments. It aims to estimate the market size and growth potential by type, product, technology, animal type, application, end user, and region. The study also includes an in-depth competitive analysis of key players in the market, along with their company profiles, key observations on their products and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report can help established companies and newer or smaller firms understand market trends, enabling them to capture a larger share of the market. Firms that acquire the report can implement one or more of the five strategies outlined below.

This report provides insights into the following points:

- Analysis of key drivers (growing companion animal population, rising demand for pet insurance and increasing pet care expenditure), restraints (high cost of instruments and procedures, operator dependency affecting image quality and consistency), opportunities (growing opportunities in emerging markets, increasing adoption of portable and point-of-care ultrasound devices), and challenges (low animal health awareness in developing countries, shortage of trained professionals) influencing the growth of the veterinary ultrasound market.

- Product Development/Innovation: Detailed insights on upcoming technologies and product launches in the veterinary ultrasound market.

- Market Development: Comprehensive information about lucrative emerging markets. The report analyzes the markets for various types of veterinary ultrasound products across regions.

- Market Diversification: Exhaustive information about products, untapped regions, recent developments, and investments in the veterinary ultrasound market

- Competitive Assessment: In-depth assessment of market share, strategies, products, distribution networks, and manufacturing capabilities of the leading players in the veterinary ultrasound market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 MARKET STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN VETERINARY ULTRASOUND MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 VETERINARY ULTRASOUND MARKET OVERVIEW

- 3.2 ASIA PACIFIC: VETERINARY ULTRASOUND MARKET, BY COUNTRY AND END USER

- 3.3 GEOGRAPHIC SNAPSHOT OF THE VETERINARY ULTRASOUND MARKET

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expanding pet ownership and rising expenditure on pet healthcare

- 4.2.1.2 Increasing pet insurance coverage, enabling advanced veterinary diagnostics

- 4.2.1.3 Rising disease burden in livestock, farm, and wildlife populations

- 4.2.1.4 Growing number of veterinary practitioners in developed economies

- 4.2.1.5 Technological innovations in veterinary ultrasound systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High instrument costs limiting adoption

- 4.2.2.2 Limited reimbursement coverage and high out-of-pocket expenditure in many regions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing number of untapped emerging markets

- 4.2.3.2 Integration of remote consultation for veterinary ultrasound

- 4.2.4 CHALLENGES

- 4.2.4.1 Operational barriers and limited access to veterinary care

- 4.2.4.2 Skill gap in advanced veterinary imaging and Doppler ultrasound interpretation

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKET

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF SUBSTITUTES

- 5.1.2 THREAT OF NEW ENTRANTS

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECAST

- 5.2.3 TRENDS IN GLOBAL VETERINARY MEDICAL DEVICE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL VETERINARY HEALTHCARE INDUSTRY

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 VALUE CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY PRODUCT (2023-2025)

- 5.6.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TYPE (2023-2025)

- 5.6.3 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY TECHNOLOGY (2023-2025)

- 5.6.4 AVERAGE SELLING PRICE TREND, BY REGION (2023-2025)

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO FOR HS CODE 9018.1200

- 5.7.2 EXPORT SCENARIO FOR HS CODE 9018.1200

- 5.8 KEY CONFERENCES & EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.12 IMPACT OF US TARIFFS-VETERINARY ULTRASOUND MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.5 IMPACT ON END USERS

- 5.12.5.1 Veterinary clinics

- 5.12.5.2 Veterinary hospitals

- 5.12.5.3 Academic institutes & veterinary teaching universities

- 5.12.5.4 Other end users

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 AI-ASSISTED IMAGE ACQUISITION & INTERPRETATION

- 6.1.2 HANDHELD/WHOLE-BODY POCUS DEVICES

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 CONTRAST AGENTS & CEUS PROTOCOLS

- 6.2.2 ULTRASOUND-GUIDED INTERVENTIONAL TOOLS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 WIRELESS PROBES & APP ECOSYSTEMS

- 6.3.2 VETERINARY TELEMEDICINE

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 NEAR-TERM (2025-2027)

- 6.4.2 MID-TERM (2028-2030)

- 6.4.3 LONG-TERM (2030+)

- 6.5 PATENT ANALYSIS

- 6.5.1 JURISDICTION & TOP APPLICANT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 AI-AUGMENTED ULTRASOUND DIAGNOSTIC & DECISION SUPPORT PLATFORMS

- 6.6.2 CLOUD-NATIVE ULTRASOUND ECOSYSTEMS, TELE-ULTRASOUND, AND IMAGING AS A SERVICE

- 6.6.3 INTELLIGENT ACQUISITION & ASSISTED SCANNING TECHNOLOGIES IN ULTRASOUND

- 6.6.4 GENERATIVE AI FOR ULTRASOUND TRAINING & CLINICAL DECISION SUPPORT

- 6.6.5 IOT-DRIVEN UPTIME OPTIMIZATION & PREDICTIVE MAINTENANCE

- 6.6.6 PORTABLE & POINT-OF-CARE IMAGING

- 6.7 IMPACT OF AI/GENERATIVE AI ON VETERINARY ULTRASOUND MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 AI USE CASES

- 6.7.3 BEST PRACTICES IN VETERINARY ULTRASOUND MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN VETERINARY ULTRASOUND MARKET

- 6.7.6 END-USER READINESS LANDSCAPE

7 SUSTAINABILITY & REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS & COMPLIANCE

- 7.1.1 REGULATORY ANALYSIS

- 7.1.1.1 NORTH AMERICA

- 7.1.2 EUROPE

- 7.1.3 ASIA PACIFIC

- 7.1.4 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.1 REGULATORY ANALYSIS

- 7.2 INDUSTRY STANDARDS

- 7.2.1 VETERINARY ULTRASOUND PRACTICE STANDARDS

- 7.2.2 ELECTRICAL SAFETY STANDARD- IEC 60601-1

- 7.2.3 SOFTWARE LIFECYCLE STANDARD- IEC 62304:2006

- 7.3 SUSTAINABILITY INITIATIVES

- 7.3.1 GE HEALTHCARE: ENVIRONMENTAL SUSTAINABILITY IN ULTRASOUND PRODUCT LIFECYCLE

- 7.3.2 ESAOTE S.P.A: ESG STRATEGY FOR ENVIRONMENTAL IMPACT REDUCTION

- 7.4 SUSTAINABILITY IMPACT & REGULATORY POLICY INITIATIVES

- 7.5 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS & BUYING CRITERIA

- 8.2.1 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 VETERINARY ULTRASOUND MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 2D ULTRASOUND

- 9.2.1 2D ULTRASOUND SEGMENT TO MAINTAIN MARKET LEADERSHIP DURING FORECAST PERIOD

- 9.3 DOPPLER ULTRASOUND

- 9.3.1 HIGHER DETAIL OF DOPPLER ULTRASOUND DRIVES DEMAND

- 9.4 3D/4D ULTRASOUND

- 9.4.1 3D/4D ULTRASOUND TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

10 VETERINARY ULTRASOUND MARKET, BY PRODUCT

- 10.1 INTRODUCTION

- 10.2 EQUIPMENT

- 10.2.1 CART-BASED ULTRASOUND SCANNERS

- 10.2.1.1 High-resolution imaging and multi-application capabilities propel demand

- 10.2.2 PORTABLE ULTRASOUND SCANNERS

- 10.2.2.1 Technological advancements and increased demand for point-of-care diagnostics to drive market

- 10.2.1 CART-BASED ULTRASOUND SCANNERS

- 10.3 ACCESSORIES & CONSUMABLES

- 10.3.1 INCREASING PROCEDURAL VOLUMES AND RISING DEMAND FOR ADVANCED TRANSDUCERS TO DRIVE MARKET

- 10.4 SOFTWARE

- 10.4.1 ADOPTION OF AI-ENABLED PLATFORMS, CLOUD-BASED WORKFLOW MANAGEMENT, AND AUTOMATED DIAGNOSTIC TOOLS SUPPORTS MARKET GROWTH

11 VETERINARY ULTRASOUND MARKET, BY TECHNOLOGY

- 11.1 INTRODUCTION

- 11.2 DIGITAL IMAGING

- 11.2.1 DIGITAL IMAGING SEGMENT DOMINATES MARKET

- 11.3 CONTRAST IMAGING

- 11.3.1 CLINICAL INDICATIONS, INCLUDING M-MODE IMAGING AND MYOCARDIAL PERFUSION, DRIVE SEGMENT

12 VETERINARY ULTRASOUND MARKET, BY ANIMAL TYPE

- 12.1 INTRODUCTION

- 12.2 SMALL COMPANION ANIMALS

- 12.2.1 DOGS

- 12.2.1.1 Rising ownership and increasing prevalence of chronic & respiratory diseases drive market

- 12.2.2 CATS

- 12.2.2.1 Rising prevalence of chronic kidney and cardiac diseases and increasing adoption of POC scanners propel market growth

- 12.2.3 OTHER SMALL COMPANION ANIMALS

- 12.2.1 DOGS

- 12.3 LARGE ANIMALS

- 12.3.1 EQUINE

- 12.3.1.1 Increasing demand for musculoskeletal & cardiac imaging and rising adoption of ultrasound-guided procedures propel market

- 12.3.2 BOVINE

- 12.3.2.1 Early pregnancy diagnosis, quick detection of disorders to support market growth

- 12.3.3 SWINE

- 12.3.3.1 Rising adoption for reproductive monitoring, AI-assisted pregnancy diagnosis, and precision herd management drive market

- 12.3.4 OTHER LARGE ANIMALS

- 12.3.1 EQUINE

- 12.4 OTHER ANIMALS

13 VETERINARY ULTRASOUND MARKET, BY APPLICATION

- 13.1 INTRODUCTION

- 13.2 OBSTETRICS/GYNECOLOGY

- 13.2.1 OBSTETRICS/GYNECOLOGY DOMINATED MARKET IN 2025

- 13.3 CARDIOLOGY

- 13.3.1 INCREASING PREVALENCE OF CVD IN DOGS AND CATS TO DRIVE MARKET

- 13.4 ORTHOPEDICS

- 13.4.1 ULTRASOUND FOR ORTHOPEDIC IMAGING IN SMALLER ANIMALS TO DRIVE SEGMENT

- 13.5 OTHER APPLICATIONS

14 VETERINARY ULTRASOUND MARKET, BY END USER

- 14.1 INTRODUCTION

- 14.2 VETERINARY CLINICS

- 14.2.1 VETERINARY CLINICS SEGMENT DOMINATED MARKET IN 2025

- 14.3 VETERINARY HOSPITALS

- 14.3.1 HIGH PROCEDURAL VOLUMES AND INFRASTRUCTURAL DEVELOPMENT TO DRIVE MARKET

- 14.4 VETERINARY ACADEMIC INSTITUTES

- 14.4.1 RISING RESEARCH AND INCREASING ADOPTION OF & TRAINING IN POC ULTRASOUND TO PROPEL MARKET

- 14.5 OTHER END USERS

15 VETERINARY ULTRASOUND MARKET, BY REGION

- 15.1 INTRODUCTION

- 15.2 NORTH AMERICA

- 15.2.1 MACROECONOMIC OUTLOOK FOR NORTH AMERICA

- 15.2.2 US

- 15.2.2.1 Rising pet ownership and demand for advanced diagnostic imaging to drive market growth

- 15.2.3 CANADA

- 15.2.3.1 Expanding veterinary workforce and increasing access to diagnostic imaging to support growth

- 15.3 EUROPE

- 15.3.1 MACROECONOMIC OUTLOOK FOR EUROPE

- 15.3.2 GERMANY

- 15.3.2.1 Rising livestock disease burden and increasing need for advanced ultrasound diagnostics drive market growth

- 15.3.3 UK

- 15.3.3.1 High pet insurance penetration enabling greater access to ultrasound imaging

- 15.3.4 FRANCE

- 15.3.4.1 Centralized healthcare system and growing integration of portable & POC ultrasound to propel market growth in France

- 15.3.5 ITALY

- 15.3.5.1 Dairy cattle dominance driving veterinary ultrasound adoption in Italy

- 15.3.6 SPAIN

- 15.3.6.1 Growing chronic disease burden and expanding specialty treatment centers to support market growth in Spain

- 15.3.7 RUSSIA

- 15.3.7.1 Growing meat consumption and large livestock base driving veterinary ultrasound demand in Russia

- 15.3.8 SWEDEN

- 15.3.8.1 Advanced healthcare infrastructure and strong academic network to support market growth

- 15.3.9 NORWAY

- 15.3.9.1 High pet healthcare spending and technology-driven diagnostic adoption drives market in Norway

- 15.3.10 REST OF EUROPE

- 15.4 ASIA PACIFIC

- 15.4.1 MACROECONOMIC OUTLOOK FOR ASIA PACIFIC

- 15.4.2 JAPAN

- 15.4.2.1 Increasing pet healthcare expenditure and expansion of diagnostic imaging companies fuel growth

- 15.4.3 CHINA

- 15.4.3.1 China to dominate APAC market, driven by rising pet healthcare demand, urbanization, and AI-based imaging adoption

- 15.4.4 INDIA

- 15.4.4.1 Expansion of India's dairy sector and growing bovine healthcare needs accelerate market growth

- 15.4.5 AUSTRALIA

- 15.4.5.1 Growing livestock population and expanding companion animal ownership support market expansion

- 15.4.6 SOUTH KOREA

- 15.4.6.1 Rising preventive healthcare adoption and aging companion animal population drive market growth in South Korea

- 15.4.7 THAILAND

- 15.4.7.1 Rapid urban veterinary infrastructure expansion and rising pet humanization drive imaging market growth in Thailand

- 15.4.8 NEW ZEALAND

- 15.4.8.1 High animal welfare awareness and preventive care culture sustain veterinary imaging market growth in New Zealand

- 15.4.9 REST OF ASIA PACIFIC

- 15.5 LATIN AMERICA

- 15.5.1 MACROECONOMIC OUTLOOK FOR LATIN AMERICA

- 15.5.2 BRAZIL

- 15.5.2.1 Brazil remains the largest veterinary ultrasound market in Latin America

- 15.5.3 MEXICO

- 15.5.3.1 Expanding livestock production and herd health management drive veterinary ultrasound adoption

- 15.5.4 REST OF LATIN AMERICA

- 15.6 MIDDLE EAST & AFRICA

- 15.6.1 MACROECONOMIC OUTLOOK FOR MIDDLE EAST & AFRICA

- 15.6.2 GCC COUNTRIES

- 15.6.2.1 Kingdom of Saudi Arabia (KSA)

- 15.6.2.1.1 Growing demand for reproductive monitoring and animal health diagnostics supports market expansion

- 15.6.2.2 United Arab Emirates (UAE)

- 15.6.2.2.1 Advancements in veterinary care and government investments strengthening veterinary ultrasound systems

- 15.6.2.3 Rest of GCC Countries

- 15.6.2.1 Kingdom of Saudi Arabia (KSA)

- 15.6.3 REST OF MIDDLE EAST & AFRICA

16 COMPETITIVE LANDSCAPE

- 16.1 INTRODUCTION

- 16.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2026

- 16.2.1 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN VETERINARY ULTRASOUND MARKET

- 16.3 REVENUE SHARE ANALYSIS OF KEY PLAYERS (2023-2025)

- 16.4 MARKET SHARE ANALYSIS, 2025

- 16.4.1 GLOBAL MARKET SHARE ANALYSIS (2025)

- 16.4.2 US MARKET SHARE ANALYSIS (2025)

- 16.4.3 EUROPE MARKET SHARE ANALYSIS (2025)

- 16.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- 16.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 16.5.5.1 Company footprint

- 16.5.5.2 Region footprint

- 16.5.5.3 Type footprint

- 16.5.5.4 Product footprint

- 16.5.5.5 Technology footprint

- 16.5.5.6 Animal type footprint

- 16.5.5.7 Application footprint

- 16.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 16.6.1 PROGRESSIVE COMPANIES

- 16.6.2 RESPONSIVE COMPANIES

- 16.6.3 DYNAMIC COMPANIES

- 16.6.4 STARTING BLOCKS

- 16.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 16.6.5.1 Detailed list of key startups/SMEs

- 16.6.5.2 Competitive benchmarking of key startups/SMEs

- 16.7 COMPANY VALUATION AND FINANCIAL METRICS

- 16.7.1 FINANCIAL METRICS

- 16.7.2 COMPANY VALUATION

- 16.8 BRAND/PRODUCT COMPARISON

- 16.9 COMPETITIVE SCENARIO

- 16.9.1 PRODUCT LAUNCHES & ENHANCEMENTS

- 16.9.2 DEALS

- 16.9.3 EXPANSIONS

- 16.9.4 OTHER DEVELOPMENTS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- 17.1.1 GE HEALTHCARE

- 17.1.1.1 Business overview

- 17.1.1.2 Products offered

- 17.1.1.3 Recent developments

- 17.1.1.3.1 Deals

- 17.1.1.4 MnM view

- 17.1.1.4.1 Right to win

- 17.1.1.4.2 Strategic Choices

- 17.1.1.4.3 Weaknesses & Competitive Threats

- 17.1.2 ESAOTE S.P.A.

- 17.1.2.1 Business overview

- 17.1.2.2 Products offered

- 17.1.2.3 Recent developments

- 17.1.2.3.1 Product launches

- 17.1.2.3.2 Deals

- 17.1.2.3.3 Expansions

- 17.1.2.4 MnM view

- 17.1.2.4.1 Right to win

- 17.1.2.4.2 Strategic choices

- 17.1.2.4.3 Weaknesses & competitive threats

- 17.1.3 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 17.1.3.1 Business overview

- 17.1.3.2 Products offered

- 17.1.3.3 Recent developments

- 17.1.3.3.1 Product launches

- 17.1.3.3.2 Deals

- 17.1.3.4 MnM view

- 17.1.3.4.1 Right to win

- 17.1.3.4.2 Strategic choices

- 17.1.3.4.3 Weaknesses & competitive threats

- 17.1.4 SAMSUNG ELECTRONICS CO. LTD.

- 17.1.4.1 Business overview

- 17.1.4.2 Products offered

- 17.1.4.3 Recent developments

- 17.1.4.3.1 Deals

- 17.1.4.4 MnM View

- 17.1.4.4.1 Right to Win

- 17.1.4.4.2 Strategic Choices

- 17.1.4.4.3 Weaknesses & Competitive Threats

- 17.1.5 SIEMENS HEALTHINEERS AG

- 17.1.5.1 Business overview

- 17.1.5.2 Products offered

- 17.1.5.3 MnM view

- 17.1.5.3.1 Key strengths/Right to win

- 17.1.5.3.2 Strategic choices

- 17.1.5.3.3 Weaknesses and competitive threats

- 17.1.6 FUJIFILM HOLDINGS CORPORATION

- 17.1.6.1 Business overview

- 17.1.6.2 Products offered

- 17.1.6.3 Recent developments

- 17.1.6.3.1 Deals

- 17.1.6.4 MnM view

- 17.1.6.4.1 Key strengths/Right to win

- 17.1.6.4.2 Strategic choices

- 17.1.6.4.3 Weaknesses and competitive threats

- 17.1.7 BUTTERFLY NETWORK, INC.

- 17.1.7.1 Business overview

- 17.1.7.2 Products offered

- 17.1.7.3 Recent developments

- 17.1.7.3.1 Product launches

- 17.1.7.3.2 Deals

- 17.1.8 LEPU MEDICAL TECHNOLOGY

- 17.1.8.1 Business overview

- 17.1.8.2 Products offered

- 17.1.9 CHISON MEDICAL TECHNOLOGIES CO., LTD.

- 17.1.9.1 Business overview

- 17.1.9.2 Products offered

- 17.1.9.3 Recent developments

- 17.1.9.3.1 Other developments

- 17.1.10 EDAN INSTRUMENTS, INC.

- 17.1.10.1 Business overview

- 17.1.10.2 Products offered

- 17.1.10.3 Recent developments

- 17.1.10.3.1 Other developments

- 17.1.11 IMV IMAGING

- 17.1.11.1 Business overview

- 17.1.11.2 Products offered

- 17.1.11.3 Recent developments

- 17.1.11.3.1 Deals

- 17.1.12 CLARIUS MOBILE HEALTH

- 17.1.12.1 Business overview

- 17.1.12.2 Products offered

- 17.1.12.3 Recent developments

- 17.1.12.3.1 Product launches

- 17.1.13 SONOSCAPE MEDICAL CORP.

- 17.1.13.1 Business overview

- 17.1.13.2 Products offered

- 17.1.14 VINNO TECHNOLOGY (SUZHOU) CO., LTD.

- 17.1.14.1 Business overview

- 17.1.14.2 Products offered

- 17.1.14.3 Recent developments

- 17.1.14.3.1 Deals

- 17.1.15 DRAMINSKI S.A.

- 17.1.15.1 Business overview

- 17.1.15.2 Products offered

- 17.1.15.3 Recent developments

- 17.1.15.3.1 Product enhancements

- 17.1.1 GE HEALTHCARE

- 17.2 OTHER PLAYERS

- 17.2.1 SHANTOU INSTITUTE OF ULTRASONIC INSTRUMENTS CO., LTD.

- 17.2.2 BMV ANIMAL TECHNOLOGY CO., LTD.

- 17.2.3 REPROSCAN TECHNOLOGIES, LLC.

- 17.2.4 CONTEC MEDICAL SYSTEMS CO., LTD.

- 17.2.5 INTERSON CORPORATION

- 17.2.6 SCINTICA INSTRUMENTATION, INC.

- 17.2.7 PROMED TECHNOLOGY CO., LTD.

- 17.2.8 LELTEK INC.

- 17.2.9 BCF TECHNOLOGY

- 17.2.10 XUZHOU KAIXIN ELECTRONIC INSTRUMENT CO., LTD.

18 RESEARCH METHODOLOGY

- 18.1 RESEARCH DATA

- 18.1.1 SECONDARY DATA

- 18.1.1.1 Key data from secondary sources

- 18.1.2 PRIMARY DATA

- 18.1.2.1 Key data from primary sources

- 18.1.2.2 Key industry insights

- 18.1.2.3 Key industry insights

- 18.1.1 SECONDARY DATA

- 18.2 MARKET SIZE ESTIMATION

- 18.3 GROWTH FORECAST

- 18.3.1 KEY INDUSTRY INSIGHTS

- 18.4 MARKET BREAKDOWN & DATA TRIANGULATION

- 18.5 RESEARCH ASSUMPTIONS

- 18.6 RISK ASSESSMENT

- 18.7 RESEARCH LIMITATIONS

- 18.8 LIMITATIONS

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS