|

시장보고서

상품코드

2059969

차세대 데이터 스토리지 시장 예측(-2032년) : 스토리지 시스템(다이렉트어태치드 스토리지, 네트워크어태치드 스토리지), 스토리지 미디어(하드 디스크 드라이브, 솔리드 스테이트 드라이브), 스토리지 아키텍처별(파일형, 오브젝트형 스토리지)Next-generation Data Storage Market By Storage System (Direct-attached Storage, Network-attached Storage), Storage Medium (Hard Disk Drives, Solid-state Drives), and Storage Architecture (File and Object-based Storage) - Global Forecast to 2032 |

||||||

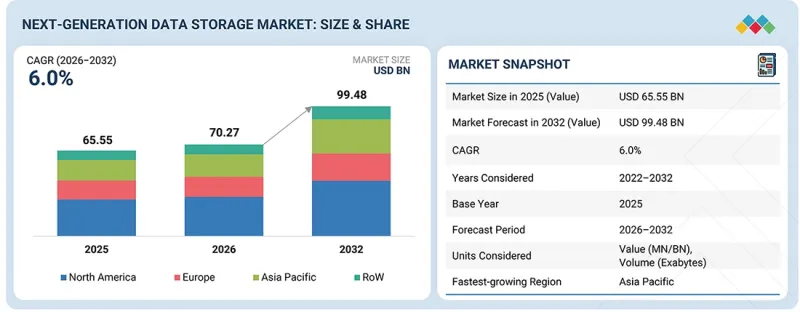

차세대 데이터 스토리지 시장 규모는 2026년 702억 7,000만 달러에서 2032년에는 994억 8,000만 달러로 확대하며, 2026-2032년까지 CAGR은 6.0%에 달할 것으로 예측됩니다.

기업 전반에 걸쳐 신뢰성 높은 데이터 보호, 재해 복구, 사업 운영의 지속에 대한 수요가 높아지고 있는 만큼, 해당 시장은 강력한 성장을 이룰 것으로 전망됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 금액(달러) |

| 부문 | 스토리지 시스템, 스토리지 매체, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

기업은 사이버 공격, 시스템 장애, 데이터 손실로 인한 위험을 최소화하기 위해 첨단 스토리지 인프라에 대한 투자를 빠르게 확대하고 있습니다. 또한 데이터 보존, 보안, 규정 준수와 관련된 규제 요건이 강화됨에 따라 기업은 백업 및 복구 기능이 강화된, 확장성이 뛰어나고 지능적인 스토리지 솔루션의 도입을 가속화하고 있습니다. 안전한 데이터 접근과 장기적인 데이터 관리의 중요성이 커지고 있는 점도 전 세계 차세대 데이터 스토리지 시장의 성장을 더욱 촉진하고 있습니다.

“저장 매체별로는 솔리드 스테이트 드라이브(SSD) 부문이 2026년에 가장 큰 시장 점유율을 차지할 것으로 전망된다”

이는 일관된 성능, 더 빠른 시작 시간, 대용량 데이터 워크로드를 효율적으로 처리할 수 있는 능력 덕분입니다. 기업 시스템, 클라우드 플랫폼, 가상화 환경 전반에 걸쳐 신속한 애플리케이션 성능과 원활한 데이터 전송에 대한 수요가 증가함에 따라 기업은 기존의 하드 디스크 드라이브(HDD)를 솔리드 스테이트 드라이브(SSD) 기반 솔루션으로 교체하도록 유도되고 있습니다. 또한 SSD의 컴팩트한 설계, 유지보수 요구 사항의 감소, 운영 효율성 향상은 현대의 데이터센터 인프라 및 미션 크리티컬 비즈니스 애플리케이션에 매우 적합하며, 이러한 점들로 인해 시장에서의 우위를 공고히 하고 있습니다.

"도입 형태별로는 하이브리드 부문이 예측 기간 중 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망된다"

도입 형태별로는 기업 전체적으로 유연하고 균형 잡힌 스토리지 인프라에 대한 수요가 높아지고 있는 만큼, 하이브리드 부문이 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 예상됩니다. 기업은 온프레미스형 스토리지의 보안 및 제어 기능과 클라우드 기반 스토리지 환경의 확장성 및 원격 접근성을 결합하기 위해 하이브리드 도입 모델을 점점 더 많이 채택하고 있습니다. 이러한 접근 방식을 통해 기업은 운영 비용을 최적화하고, 워크로드 관리를 개선하며, 동적인 데이터 요구 사항을 보다 효율적으로 지원할 수 있게 됩니다. 또한 멀티클라우드 전략과 디지털 전환(DX) 노력이 확산되고 있는 점도 전 세계에서 하이브리드 스토리지 도입 모델에 대한 수요를 더욱 가속화하고 있습니다.

“아시아·태평양 지역은 예측 기간 중 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망된다”

아시아태평양은 중국, 일본, 한국, 인도 등 주요 경제권에서의 급속한 디지털 전환, 하이퍼스케일 데이터센터에 대한 투자 확대, 클라우드 컴퓨팅의 보급 확대, AI, IoT, 5G 기술의 도입 증가에 힘입어 예측 기간 중 시장에서 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 또한 해당 지역에서는 제조업, E-Commerce, 통신, 금융 서비스 등 각 부문에서 기업 데이터 생성량이 크게 증가하고 있으며, 확장성, 고성능, 에너지 효율성이 뛰어난 스토리지 인프라에 대한 수요가 높아지고 있습니다. 또한 스마트 제조, 디지털 경제, 첨단 IT 인프라 개발을 지원하는 정부의 노력도 지역 전체에 걸쳐 차세대 데이터 스토리지 솔루션의 도입을 더욱 가속화하고 있습니다.

이 보고서에서는 전 세계 차세대 데이터 스토리지 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 현황, 주요 기업 개요 등을 정리하여 전해드립니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 차세대 데이터 스토리지 시장 : 스토리지 시스템별

제10장 차세대 데이터 스토리지 시장 : 스토리지 매체별

제11장 차세대 데이터 스토리지 시장 : 스토리지 아키텍처별

제12장 차세대 데이터 스토리지 시장 : 도입 모드별

제13장 차세대 데이터 스토리지 시장 : 최종사용자별

제14장 차세대 데이터 스토리지 시장 : 지역별

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 부록

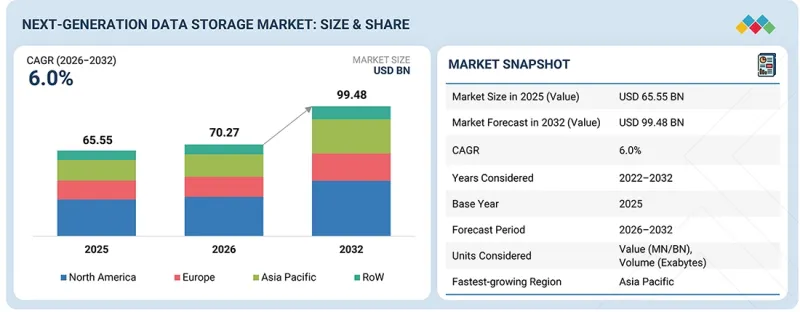

KSA 26.06.25The next-generation data storage market is anticipated to grow from USD 70.27 billion in 2026 to USD 99.48 billion by 2032, at a CAGR of 6.0% between 2026 and 2032. The market is expected to witness strong growth due to the increasing need for reliable data protection, disaster recovery, and uninterrupted business operations across enterprises.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Storage System, Storage Medium and Region |

| Regions covered | North America, Europe, APAC, RoW |

Organizations are rapidly investing in advanced storage infrastructure to minimize risks associated with cyberattacks, system failures, and data loss. In addition, growing regulatory requirements related to data retention, security, and compliance are encouraging enterprises to deploy scalable and intelligent storage solutions with enhanced backup and recovery capabilities. The rising importance of secure data accessibility and long-term data management is further supporting the expansion of the next-generation data storage market globally.

"The solid-state drives segment is estimated to hold the largest market share in 2026."

By storage medium, the solid-state drives segment is estimated to account for the largest share of the next-generation data storage market, owing to their ability to deliver consistent performance, faster boot times, and efficient handling of high-volume data workloads. The increasing requirement for rapid application performance and seamless data transfer across enterprise systems, cloud platforms, and virtualized environments is encouraging organizations to replace traditional hard disk drives with solid-state drive-based solutions. Moreover, the compact design, lower maintenance requirements, and improved operational efficiency of solid-state drives make them highly suitable for modern data center infrastructure and mission-critical business applications, thereby strengthening their market dominance.

"The hybrid segment is estimated to record the highest CAGR during the forecast period."

By deployment mode, the hybrid segment is expected to witness the highest CAGR in the next-generation data storage market due to the increasing need for flexible and balanced storage infrastructure across enterprises. Organizations are increasingly adopting hybrid deployment mode models to combine the security and control of on-premises storage with the scalability and remote accessibility of cloud-based storage environments. This approach enables businesses to optimize operational costs, improve workload management, and support dynamic data requirements more efficiently. In addition, the growing adoption of multi-cloud strategies and digital transformation initiatives is further accelerating demand for hybrid storage deployment models globally.

"Asia Pacific is expected to register the highest CAGR during the forecast period."

Asia Pacific is projected to register the highest CAGR in the next-generation data storage market during the forecast period due to rapid digital transformation, expanding hyperscale data center investments, rising cloud computing adoption, and increasing deployment of AI, IoT, and 5G technologies across major economies such as China, Japan, South Korea, and India. The region is also witnessing strong growth in enterprise data generation from manufacturing, e-commerce, telecommunications, and financial services sectors, which is increasing the demand for scalable, high-performance, and energy-efficient storage infrastructure. In addition, government initiatives supporting smart manufacturing, digital economies, and advanced IT infrastructure development are further accelerating the adoption of next-generation data storage solutions across the region.

Extensive primary interviews were conducted with key industry experts offering next-generation data storage solutions to determine and verify the market size for various segments and subsegments gathered through secondary research. The breakdown of primary participants for the report is provided below:

The study contains insights from various industry experts, from component suppliers to Tier 1 companies and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1-40%, Tier 2-35%, and Tier 3-25%

- By Designation: C-level-40%, Directors-45%, and Others-15%

- By Region: North America-41%, Europe-26%, Asia Pacific-28%, and RoW-5%

The report profiles key players in the next-generation data storage market with their respective market ranking analysis. Prominent players profiled in this report include Dell Inc. (US), Hewlett-Packard Enterprise (US), NetApp (US), Huawei Technologies Co., Ltd. (China), and Everpure, Inc. (US).

Hitachi, Ltd. (Japan), Fujitsu (Japan), IBM(US), DDN (US), and Micron Technology, Inc. (US) are among the few other companies in the next-generation data storage market.

Research Coverage:

This research report categorizes the next-generation data storage market based on storage system, storage medium, storage architecture, deployment mode, end user, and region. The report describes the major drivers, restraints, challenges, and opportunities pertaining to the next-generation data storage market and forecasts the same till 2032. Apart from this, the report also consists of leadership mapping and analysis of all the companies included in the next-generation data storage market ecosystem.

Key Benefits of Buying the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the numbers for the overall next-generation data storage market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (increased data generation attributed to surging use of smartphones and smart wearable devices, growing adoption of Internet of Things (IoT) technologies and connected devices, rising global demand for 5G technology, increasing adoption of Non-volatile Memory express (NVMe) in enterprise storage systems, growing demand for energy-efficient and compact storage solutions in homes and small offices, rising demand from AI/GenAI and real-time analytics workloads, and expansion of hyperscale and edge data center infrastructure), restraints (high cost of advanced storage solutions, long replacement cycles of legacy infrastructure, data security and privacy concerns), opportunities (adoption of hybrid cloud storage architectures, rising demand for high-performance storage, driven by real-time data processing needs, growth of AI-driven storage ecosystems, including AI/ML workloads and intelligent storage management, and expansion of storage-as-a-service (STaaS) and subscription-based models), and challenges (high power and cooling requirements of advanced storage infrastructure, and interoperability and multi-tenancy challenges across shared, multi-vendor storage environments)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the next-generation data storage market.

- Market Development: Comprehensive information about lucrative markets-the report analyzes the next-generation data storage market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the next-generation data storage market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, such as Dell Inc. (US), Hewlett-Packard Enterprise (US), NetApp (US), Huawei Technologies Co., Ltd. (China), and Everpure, Inc. (US), in the next-generation data storage market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN NEXT-GENERATION DATA STORAGE MARKET

- 3.2 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE SYSTEM

- 3.3 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE MEDIUM

- 3.4 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE ARCHITECTURE

- 3.5 NEXT-GENERATION DATA STORAGE MARKET, BY DEPLOYMENT MODE

- 3.6 NEXT-GENERATION DATA STORAGE MARKET, BY END USER

- 3.7 NEXT-GENERATION DATA STORAGE MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing adoption of IoT technologies and connected devices

- 4.2.1.2 Rising demand for 5G technology

- 4.2.1.3 Increasing adoption of NVMe in enterprise storage systems

- 4.2.1.4 Growing demand for energy-efficient and compact storage solutions in homes and small offices

- 4.2.1.5 Rising demand from AI/GenAI and real-time analytics workloads

- 4.2.1.6 Expansion of hyperscale and edge data center infrastructure

- 4.2.2 RESTRAINTS

- 4.2.2.1 High cost of advanced storage solutions

- 4.2.2.2 Long replacement cycles of legacy infrastructure

- 4.2.2.3 Data security and privacy concerns

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Adoption of hybrid cloud storage architecture

- 4.2.3.2 Rising demand for high-performance storage driven by real-time data processing needs

- 4.2.3.3 Growth of AI-driven storage ecosystems, including AI/ML workloads and intelligent storage management

- 4.2.3.4 Expansion of STaaS and subscription-based models

- 4.2.4 CHALLENGES

- 4.2.4.1 High power and cooling requirements of advanced storage infrastructure

- 4.2.4.2 Interoperability and multi-tenancy challenges across shared, multi-vendor storage environments

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 INTERCONNECTED MARKETS

- 4.3.2 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF HARD-DISK DRIVES (HDDS), BY KEY PLAYER, 2025

- 5.6.2 AVERAGE SELLING PRICE TREND, BY STORAGE MEDIUM, 2022-2025

- 5.6.3 AVERAGE SELLING PRICE TREND, BY REGION, 2022-2025

- 5.6.3.1 Average selling price trend of SSDs, by region

- 5.6.3.2 Average selling price trend of HDDs, by region

- 5.6.3.3 Average selling price trend of tapes, by region

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO (HS CODE 847170)

- 5.7.2 EXPORT SCENARIO (HS CODE 847170)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO, 2022-2025

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 QNAP ENHANCED X10STUDIO'S WORKFLOW QUALITY AND MANAGED DATA SECURELY

- 5.11.2 ITCE SELECTED BUFFALO'S TERASTATION 51210RH AS STORAGE SOLUTION FOR PRIVATE CLOUD BACKUP SERVICES

- 5.11.3 GIJIMA INSTALLED HITACHI VSP 5000 SERIES ARRAYS AND VSP G700 ARRAYS AT PRODUCTION DATA CENTER FOR DISASTER RECOVERY

- 5.11.4 IDEC CORPORATION IMPLEMENTED DELL EMC POWERMAX 2000 AS NEW STORAGE INFRASTRUCTURE THAT ENHANCED PERFORMANCE, RELIABILITY, AND AVAILABILITY OF STORAGE INFRASTRUCTURE

- 5.11.5 ZENUITY DEVELOPED AI INFRASTRUCTURE ON NVIDIA DGX-1 AND EVERPURE'S FLASHBLADE TO MAKE AUTONOMOUS VEHICLES SMART AND SAFE

- 5.11.6 MERCEDES-AMG PETRONAS STANDARDIZED EVERPURE'S FLASHARRAY AND FLASHBLADE, OFFERING FAST ACCESS TO TRACK-SLIDE FILES AND IMPROVED QUERY TIMES FOR DATABASE APPLICATIONS

- 5.11.7 WESTERN DIGITAL HELPED HY GROUP WITH BACKUP SOLUTION THAT IMPROVED DATA RETENTION

- 5.11.8 DDN ASSISTED RECURSION PHARMACEUTICALS WITH MACHINE LEARNING MODELS THAT REDUCED IDENTIFICATION TIME AND ENHANCED STORAGE SYSTEMS

- 5.11.9 PUREGOLD PRICE CLUB COLLABORATED WITH HUAWEI TECHNOLOGIES FOR EFFECTIVE STORAGE SOLUTIONS

- 5.12 IMPACT OF 2025 US TARIFF ON NEXT-GENERATION DATA STORAGE MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 KEY TARIFF RATES

- 5.12.3 PRICE IMPACT ANALYSIS

- 5.12.4 IMPACT ON COUNTRIES/REGIONS

- 5.12.4.1 US

- 5.12.4.2 Europe

- 5.12.4.3 Asia Pacific

- 5.12.5 IMPACT ON END USERS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 ADVANCED MEMORY TECHNOLOGIES FOR DATA STORAGE

- 6.1.2 DNA STORAGE

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AI AND ML

- 6.2.2 EDGE COMPUTING

- 6.3 TECHNOLOGY ROADMAP

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 IMPACT OF AI ON NEXT-GENERATION DATA STORAGE MARKET

- 6.6.1 TOP USE CASES AND MARKET POTENTIAL

- 6.6.2 BEST PRACTICES IN NEXT-GENERATION DATA STORAGE MARKET

- 6.6.3 CASE STUDIES OF AI IMPLEMENTATION IN NEXT-GENERATION DATA STORAGE MARKET

- 6.6.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.6.5 CLIENTS' READINESS TO ADOPT AI IN NEXT-GENERATION DATA STORAGE MARKET

7 REGULATORY LANDSCAPE

- 7.1 INTRODUCTION

- 7.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.3 STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END USERS

9 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE SYSTEM

- 9.1 INTRODUCTION

- 9.2 DIRECT-ATTACHED STORAGE

- 9.2.1 SIMPLIFIED DEPLOYMENT AND HIGH-PERFORMANCE LOCAL STORAGE REQUIREMENTS TO DRIVE ADOPTION

- 9.3 NETWORK-ATTACHED STORAGE

- 9.3.1 INCREASING NEED FOR CENTRALIZED AND COLLABORATIVE DATA ACCESS TO SUPPORT MARKET GROWTH

- 9.4 STORAGE AREA NETWORK

- 9.4.1 INCREASING DEPLOYMENT OF MISSION-CRITICAL APPLICATIONS TO DRIVE MARKET

10 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE MEDIUM

- 10.1 INTRODUCTION

- 10.2 HARD DISK DRIVES

- 10.2.1 INCREASING DEMAND FOR COST-EFFICIENT MASS DATA STORAGE TO DRIVE MARKET

- 10.3 SOLID-STATE DRIVES

- 10.3.1 RISING ADOPTION OF PERFORMANCE-INTENSIVE WORKLOADS TO ACCELERATE DEPLOYMENT

- 10.4 TAPES

- 10.4.1 GROWING NEED FOR LONG-TERM DATA ARCHIVING AND BACKUP TO SUPPORT MARKET GROWTH

11 NEXT-GENERATION DATA STORAGE MARKET, BY STORAGE ARCHITECTURE

- 11.1 INTRODUCTION

- 11.2 FILE- AND OBJECT-BASED STORAGE

- 11.2.1 FILE STORAGE

- 11.2.1.1 INCREASING DEMAND FOR STRUCTURED DATA MANAGEMENT AND SHARED ACCESS TO DRIVE ADOPTION

- 11.2.2 OBJECT STORAGE

- 11.2.2.1 EXPONENTIAL GROWTH IN UNSTRUCTURED DATA TO DRIVE MARKET

- 11.2.1 FILE STORAGE

- 11.3 BLOCK STORAGE

- 11.3.1 RISING ADOPTION OF PERFORMANCE-CRITICAL ENTERPRISE APPLICATIONS TO PROPEL MARKET

12 NEXT-GENERATION DATA STORAGE MARKET, BY DEPLOYMENT MODE

- 12.1 INTRODUCTION

- 12.2 ON-PREMISES

- 12.2.1 INCREASING EMPHASIS ON DATA CONTROL AND REGULATORY COMPLIANCE TO DRIVE ADOPTION

- 12.3 CLOUD

- 12.3.1 INCREASING DEMAND FOR SCALABLE AND FLEXIBLE STORAGE INFRASTRUCTURE TO DRIVE MARKET

- 12.4 HYBRID

- 12.4.1 DEMAND FOR SCALABLE AND FLEXIBLE STORAGE INFRASTRUCTURE TO DRIVE ADOPTION

13 NEXT-GENERATION DATA STORAGE MARKET, BY END USER

- 13.1 INTRODUCTION

- 13.2 ENTERPRISES

- 13.2.1 BFSI

- 13.2.1.1 Expanding digital financial services and stringent data security requirements to accelerate adoption

- 13.2.2 MANUFACTURING

- 13.2.2.1 Increasing adoption of Industry 4.0 and industrial automation to drive demand

- 13.2.3 CONSUMER GOODS & RETAIL

- 13.2.3.1 Increase in omnichannel retail and customer data analytics to drive demand

- 13.2.4 HEALTHCARE & LIFE SCIENCES

- 13.2.4.1 Rising adoption of digital health records and medical imaging to drive demand for advanced storage solutions

- 13.2.5 MEDIA & ENTERTAINMENT

- 13.2.5.1 Surge in digital content creation and streaming services to drive market

- 13.2.6 OTHER ENTERPRISES

- 13.2.6.1 Energy & power

- 13.2.6.1.1 Increasing deployment of smart grids and real-time monitoring systems to drive demand

- 13.2.6.2 Education & research

- 13.2.6.2.1 Expansion of data-intensive research activities and digital learning environments to accelerate adoption

- 13.2.6.3 Business & consulting

- 13.2.6.3.1 Increasing reliance on data-driven decision-making to drive adoption of advanced storage solutions

- 13.2.6.4 Transportation & logistics

- 13.2.6.4.1 Rising adoption of connected logistics and real-time tracking systems to drive market

- 13.2.6.1 Energy & power

- 13.2.1 BFSI

- 13.3 GOVERNMENT BODIES

- 13.3.1 INCREASING DIGITAL GOVERNANCE AND NATIONAL DATA MANAGEMENT INITIATIVES TO DRIVE ADOPTION

- 13.4 CLOUD SERVICE PROVIDERS

- 13.4.1 RAPID EXPANSION OF CLOUD-BASED SERVICES AND DATA-INTENSIVE APPLICATIONS TO DRIVE MARKET

- 13.5 TELECOM COMPANIES

- 13.5.1 SURGE IN DATA TRAFFIC AND 5G NETWORK DEPLOYMENT TO PROPEL MARKET

14 NEXT-GENERATION DATA STORAGE MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Early adoption of digital technologies by established players to boost demand

- 14.2.2 CANADA

- 14.2.2.1 Increasing investments in development of data center infrastructure to drive market

- 14.2.3 MEXICO

- 14.2.3.1 Growing need for improved telecommunication infrastructure to propel market

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 UK

- 14.3.1.1 Growing demand from BFSI service providers and telecom giants to fuel market growth

- 14.3.2 GERMANY

- 14.3.2.1 Rising demand for 5G telecom services to drive market

- 14.3.3 FRANCE

- 14.3.3.1 Booming healthcare sector to accelerate demand

- 14.3.4 REST OF EUROPE

- 14.3.1 UK

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Rising modernization of manufacturing sector to drive market

- 14.4.2 JAPAN

- 14.4.2.1 Thriving automotive and manufacturing sectors to drive market

- 14.4.3 INDIA

- 14.4.3.1 Adoption of big data, IoT, and other digital and virtualized platforms to accelerate market

- 14.4.4 SOUTH KOREA

- 14.4.4.1 Increasing investments in expansion of regional data center facilities to boost demand

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 ROW

- 14.5.1 MIDDLE EAST

- 14.5.1.1 Growing adoption of e-government services and smart city initiatives to drive market

- 14.5.1.2 GCC Countries

- 14.5.1.3 Rest of Middle East

- 14.5.2 AFRICA

- 14.5.2.1 Rapid data center expansion driven by digital transformation to fuel market growth

- 14.5.3 SOUTH AMERICA

- 14.5.3.1 Growing demand in telecommunications industry to drive adoption

- 14.5.1 MIDDLE EAST

15 COMPETITIVE LANDSCAPE

- 15.1 INTRODUCTION

- 15.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 COMPANY VALUATION AND FINANCIAL METRICS

- 15.6 BRAND COMPARISON

- 15.6.1 EVERPURE, INC.

- 15.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.7.1 STARS

- 15.7.2 EMERGING LEADERS

- 15.7.3 PERVASIVE PLAYERS

- 15.7.4 PARTICIPANTS

- 15.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.7.5.1 Company footprint

- 15.7.5.2 Region footprint

- 15.7.5.3 Storage system footprint

- 15.7.5.4 Storage medium footprint

- 15.7.5.5 Storage architecture footprint

- 15.7.5.6 End-user footprint

- 15.7.5.7 Deployment mode footprint

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 DELL INC.

- 16.1.1.1 Business overview

- 16.1.1.2 Products/Solutions/Services offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Key strengths/right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 HEWLETT PACKARD ENTERPRISE COMPANY

- 16.1.2.1 Business overview

- 16.1.2.2 Products/solutions/services offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Product launches

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Key strengths/right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 NETAPP

- 16.1.3.1 Business overview

- 16.1.3.2 Products/solutions/services offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.4 MnM view

- 16.1.3.4.1 Key strengths/right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 HUAWEI TECHNOLOGIES CO., LTD.

- 16.1.4.1 Business overview

- 16.1.4.2 Products/solutions/services offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths/right to win

- 16.1.4.4.2 Strategic choices made

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 EVERPURE, INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products/solutions/services offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.3.2 Deals

- 16.1.5.4 MnM view

- 16.1.5.4.1 Key strengths/right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 HITACHI, LTD.

- 16.1.6.1 Business overview

- 16.1.6.2 Products/solutions/services offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.6.3.2 Deals

- 16.1.7 FUJITSU

- 16.1.7.1 Business overview

- 16.1.7.2 Products/solutions/services offered

- 16.1.7.3 Recent developments

- 16.1.7.3.1 Product launches

- 16.1.7.3.2 Deals

- 16.1.8 IBM

- 16.1.8.1 Business overview

- 16.1.8.2 Products/solutions/services offered

- 16.1.8.3 Recent developments

- 16.1.8.3.1 Product launches

- 16.1.8.3.2 Deals

- 16.1.9 DDN

- 16.1.9.1 Business overview

- 16.1.9.2 Products/solutions/services offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.3.2 Deals

- 16.1.10 MICRON TECHNOLOGY, INC.

- 16.1.10.1 Business overview

- 16.1.10.2 Products/solutions/services offered

- 16.1.10.3 Recent developments

- 16.1.10.3.1 Product launches

- 16.1.10.3.2 Deals

- 16.1.1 DELL INC.

- 16.2 OTHER PLAYERS

- 16.2.1 CLOUDIAN

- 16.2.2 INFORTREND TECHNOLOGY, INC.

- 16.2.3 QUANTUM CORPORATION

- 16.2.4 WESTERN DIGITAL CORPORATION

- 16.2.5 SAMSUNG

- 16.2.6 NUTANIX

- 16.2.7 SEAGATE TECHNOLOGY LLC

- 16.2.8 SCALITY

- 16.2.9 NETGEAR

- 16.2.10 INSPUR CO., LTD.

- 16.2.11 SK HYNIX INC.

- 16.2.12 LUCIDLINK CORP.

- 16.2.13 DATACORE SOFTWARE

- 16.2.14 KIOXIA HOLDINGS CORPORATION

- 16.2.15 LENOVO

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.2 SECONDARY AND PRIMARY RESEARCH

- 17.2.1 SECONDARY DATA

- 17.2.1.1 Key data from secondary sources

- 17.2.1.2 List of key secondary sources

- 17.2.2 PRIMARY DATA

- 17.2.2.1 Key data from primary sources

- 17.2.2.2 List of primary interview participants

- 17.2.2.3 Breakdown of primaries

- 17.2.2.4 Key industry insights

- 17.2.1 SECONDARY DATA

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 BOTTOM-UP APPROACH

- 17.3.2 TOP-DOWN APPROACH

- 17.3.3 MARKET SIZE CALCULATION FOR BASE YEAR

- 17.4 MARKET FORECAST APPROACH

- 17.4.1 BOTTOM-UP APPROACH

- 17.4.2 TOP-DOWN APPROACH

- 17.5 DATA TRIANGULATION

- 17.6 FACTOR ANALYSIS

- 17.7 RESEARCH ASSUMPTIONS

- 17.8 RESEARCH LIMITATIONS

- 17.9 RISK ANALYSIS

18 APPENDIX

- 18.1 DISCUSSION GUIDE

- 18.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 18.3 CUSTOMIZATION OPTIONS

- 18.4 RELATED REPORTS

- 18.5 AUTHOR DETAILS