|

시장보고서

상품코드

2060328

재활용 플라스틱 시장 예측(-2033년) : 유형별, 원료별, 플라스틱 유형별, 최종 용도 산업별, 지역별Recycled Plastics Market By Source (Bottles, Fibers, Films, Foams), Process, Plastic Type (PET, PP, PVC, PS), Type, End-Use (Packaging, Textiles, Building & Construction, Automotive, Electrical & Electronics), and Region - Global Forecast to 2033 |

||||||

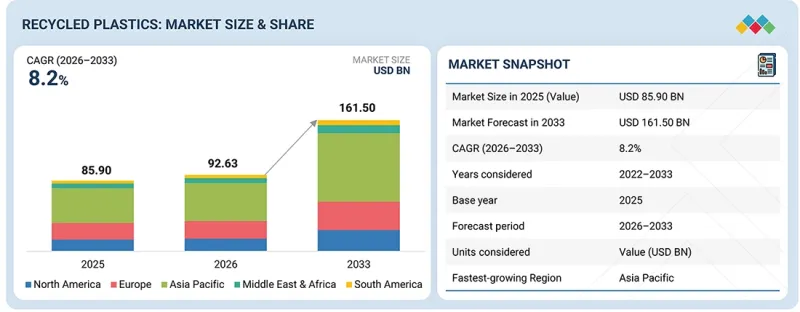

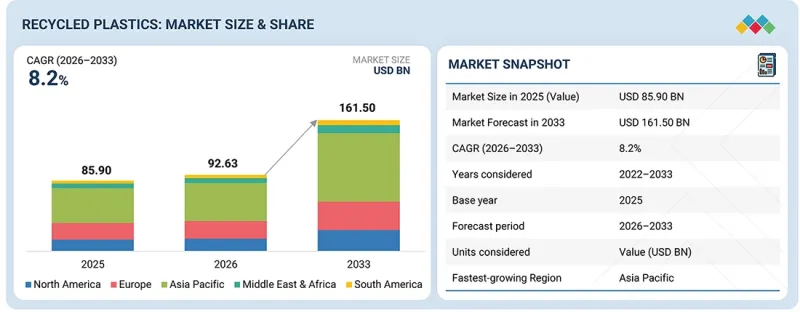

세계의 재활용 플라스틱 시장 규모는 2026년 926억 3,000만 달러에서 2033년까지 1,615억 달러로 성장하며, 예측 기간 중 CAGR은 8.2%에 달할 것으로 전망되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2033년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 대상 단위 | 금액(100만/10억 달러) 및 킬로톤 |

| 부문 | 유형별, 원료별, 플라스틱 유형별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 아시아태평양, 유럽, 북미, 중동 및 아프리카, 남미 |

재활용 플라스틱 시장은 포장, 섬유, 건축·건설, 자동차, 전기·전자기기, 기타 등 다양한 최종 용도 산업 분야에서 상당한 성장이 예상됩니다.

"유형별로는 산업용 재생 플라스틱 부문이 예측 기간 중 두 번째로 큰 점유율을 차지할 것으로 추정됩니다. "

산업용 재생 플라스틱 부문은 예측 기간 중 재생 플라스틱 시장 전체에서 2위의 점유율을 차지할 것으로 전망됩니다. 이 시장의 성장은 자동차, 건설, 전자기기 및 섬유 산업에서 지속가능한 제조 관행이 확대됨에 따라 주도되고 있습니다. 각 산업 분야는 생산 공정에 재생 플라스틱을 활용함으로써 환경 목표 달성을 향해 나아가고 있습니다. 새로운 재활용 기술의 개발로 인해 산업용 재생 플라스틱은 더 높은 품질 기준을 충족할 수 있게 되었으며, 이에 따라 이러한 소재들은 다양한 고성능 산업 분야에서 버진 플라스틱을 대체할 수 있게 되었습니다. 이 부문의 성장은 제조업체들의 순환 경제 원칙에 대한 이해가 깊어지고, 산업용 플라스틱 폐기물을 관리하는 시설에 대한 투자가 증가함에 따라 지원되고 있습니다. 기업이 환경적 지속가능성에 주력하면서 운영 비용 절감을 도모함에 따라 산업용 재생 플라스틱에 대한 수요는 계속해서 증가할 것으로 보입니다.

"예측 기간 중 포장 부문은 재생 플라스틱 시장에서 가장 큰 최종 용도 산업이 될 것으로 추정됩니다. "

지속가능한 포장 솔루션으로의 전환이 가속화됨에 따라 예측 기간 중 포장 부문이 전 세계 재생 플라스틱 시장을 주도할 것으로 예상됩니다. 일회용 플라스틱 사용 금지와 관련된 규제가 점점 더 엄격해지고 있습니다. 동시에, 많은 FMCG 기업과 대형 소매 체인들이 순환형 경제를 추진하고 있습니다. 또한 E-Commerce의 급속한 성장에 따라 가격이 저렴할 뿐만 아니라 튼튼하고 지속가능성 기준에도 부합하는 포장재에 대한 수요가 높아지고 있습니다. 화학적 재활용이나 고효율 선별 시스템 등 재활용 기술의 지속적인 발전으로 인해 재생 수지의 품질과 안정성이 향상되고 있습니다.

Veolia(프랑스), Indorama Ventures Public Company Limited(태국), Far Eastern New Century Corporation(대만), Alpek S.A.B. de C.V.(멕시코), Amcor plc(스위스)는 재생 플라스틱 시장에서 사업을 운영하는 주요 기업 중 일부입니다. 이 기업은 시장 점유율을 확대하기 위해 인수, 사업 확장, 제휴, 계약 등의 전략을 채택하고 있습니다.

조사 범위:

이 보고서에서는 유형, 원료 출처, 최종 용도 산업, 플라스틱 유형, 제조 공정 및 지역을 기준으로 재생 플라스틱 시장을 정의, 세분화 및 예측하고 있습니다. 또한 시장 성장에 영향을 미치는 주요 요인(촉진요인, 제약 요인, 기회, 과제 등)에 대한 상세한 정보를 제공하고 있습니다. 또한 재생 플라스틱 제조업체의 전략적 프로필을 작성하고, 시장 점유율과 핵심 경쟁력을 종합적으로 분석하는 한편, 각 기업이 시장에서 펼치고 있는 사업 확장, 제휴, 신제품 출시 등의 경쟁 동향을 추적·분석하고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 재생 플라스틱 시장 및 각 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 시장 선도 기업과 신규 진입 기업에 도움이 될 것으로 기대됩니다. 또한 이 보고서는 이해관계자들이 시장의 경쟁 구도에 대한 이해를 높이고, 자사의 사업적 입지를 강화하기 위한 인사이트를 얻어, 적절한 시장 진입 전략을 수립하는 데 도움이 될 것으로 기대됩니다. 또한 이해관계자들이 시장 동향을 파악하고, 주요 시장 촉진요인, 제약, 과제 및 기회에 관한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 재활용 플라스틱 시장의 성장에 영향을 미치는 주요 촉진요인(플라스틱 폐기물이 환경에 미치는 악영향, 에너지 절약 의식 고조 및 정부의 노력), 제약 요인(신규 플라스틱과의 치열한 경쟁, 다운사이클링으로 인한 악영향), 기회(선진국에서의 재생 플라스틱 이용 촉진을 위한 긍정적인 조치, 아시아태평양 개발도상국의 섬유 산업에서의 이용 확대) 및 과제(중국의 폐플라스틱 및 스크랩 플라스틱 수입 금지, 원자재 수집의 어려움)에 대해 재생 플라스틱 시장의 성장에 영향을 미치는 요인으로 분석하고 있습니다.

- 제품 개발/혁신: 재생 플라스틱 시장의 향후 기술 동향 및 연구개발 활동에 대한 상세 인사이트.

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 - 이 보고서에서는 다양한 지역의 재생 플라스틱 시장을 분석하고 있습니다.

- 시장의 다양화: 재생 플라스틱 시장의 신제품, 다양한 유형, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보.

- 경쟁사 분석: Veolia(프랑스), Indorama Ventures Public Company Limited(태국), Far Eastern New Century Corporation(대만), Alpek S.A.B. de C.V.(멕시코), Amcor plc(스위스), Biffa(영국), Cabka digital(독일), Jayplas(잉글랜드), KW Plastics(미국), Loop Industries(캐나다), MBA Polymers Inc.(미국), PET RECYCLING TEAM(오스트리아), Plastipak Holdings, Inc.(미국), REMONDIS SE &Co. KG(독일), Republic Services(미국), Stericycle, Inc.(미국), Ultra-Poly Corporation(미국) 등, 산업용 증발기 시장의 주요 기업입니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 재활용 플라스틱 시장(유형별)

제10장 재활용 플라스틱 시장(원료별)

제11장 재활용 플라스틱 시장(플라스틱 유형별)

제12장 재활용 플라스틱 시장(최종 용도 산업별)

제13장 재활용 플라스틱 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSAThe global recycled plastics market is projected to grow from USD 92.63 billion in 2026 to USD 161.50 billion by 2033, at a CAGR of 8.2% during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | Value (USD Million/Billion) and Volume (Kiloton) |

| Segments | By Source, Plastic Type, Type, Process, and End-use Industry |

| Regions covered | Asia Pacific, Europe, North America, Middle East & Africa, and South America |

The recycled plastics market is projected to witness significant growth across various end-use industries, such as packaging, textiles, building & construction, automotive, electrical & electronics, and others.

"The industrial recyclates segment, by type, is estimated to account for the second-largest share during the forecast period".

The industrial recyclates segment is projected to account for the second-largest share in the overall recycled plastics market during the forecast period. The growth of this market is driven by increasing sustainable manufacturing practices in the automotive, construction, electronics, and textiles industries. Industries are progressing toward their environmental goals by using recycled plastics in their production methods. The development of new recycling methods has enabled industrial recyclates to achieve higher quality standards, which enable these materials to replace virgin plastics in various high-performance industrial uses. The expansion of this segment is supported by manufacturers' growing understanding of circular economy principles and increasing investments in facilities that manage industrial plastic waste. The demand for industrial recyclates will continue to rise as companies focus on environmental sustainability while seeking to reduce their operational costs.

"The packaging segment is estimated to be the largest end-use industry of the recycled plastics market during the forecast period".

The packaging segment is expected to lead the global recycled plastics market during the forecast period due to the accelerating shift toward sustainable packaging solutions. Regulations regarding bans on single-use plastics are becoming increasingly stringent. At the same time, many FMCG firms and big retail chains are pushing the circular economy. Also, the rapid growth of e-commerce has raised the need for packaging that is not only affordable but also sturdy and still aligned with sustainability. Ongoing progress in recycling methods, for example, chemical recycling and high-efficiency sorting systems, is enhancing the quality and consistency of recycled resins.

Profile break-up of primary participants for the report:

- By Company Type: Tier 1 - 65%, Tier 2 - 20%, and Tier 3 - 15%

- By Designation: C-level- 25%, Director Level- 30%, and Others - 45%

- By Region: North America - 30%, Europe - 20%, Asia Pacific - 40%, Middle East & Africa - 7%, and South America - 3%

Veolia (France), Indorama Ventures Public Company Limited (Thailand), Far Eastern New Century Corporation (Taiwan), Alpek S.A.B. de C.V. (Mexico), and Amcor plc (Switzerland) are some of the major players operating in the recycled plastics market. These players have adopted strategies such as acquisitions, expansions, partnerships, and agreements to increase their market share.

Research Coverage:

The report defines, segments, and projects the recycled plastics market based on type, source, end-use industry, plastic type, process, and region. It provides detailed information regarding the major factors influencing the growth of the market, such as drivers, restraints, opportunities, and challenges. It strategically profiles recycled plastics manufacturers and comprehensively analyzes their market shares and core competencies, as well as tracks and analyzes competitive developments, such as expansions, partnerships, and new product launches, undertaken by them in the market.

Reasons to Buy the Report:

The report is expected to help the market leaders/new entrants in the market by providing them with the closest approximations of revenue numbers of the recycled plastics market and its segments. This report is also expected to help stakeholders obtain an improved understanding of the competitive landscape of the market, gain insights to improve the position of their businesses, and make suitable go-to-market strategies. It also enables stakeholders to understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Negative environmental impact on plastics disposal, Growing awareness regarding energy savings and governments initiatives), restraints (Strong competition from virgin plastics, Adverse impact of downcycling), opportunities (Favorable initiatives to promote use of recycled plastics in developed countries, Increasing use in textile industry in developing countries of Asia Pacific), and challenges (Ban on imports of waste or scrap plastics in China, Difficulty in collection of raw materials) influencing the growth of the recycled plastics market.

- Product Development/Innovation: Detailed insights on upcoming technologies and research & development activities in the recycled plastics market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the recycled plastics market across varied regions.

- Market Diversification: Exhaustive information about new products, various types, untapped geographies, recent developments, and investments in the recycled plastics market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and product offerings of leading players such as Veolia (France), Indorama Ventures Public Company Limited (Thailand), Far Eastern New Century Corporation (Taiwan), Alpek S.A.B. de C.V. (Mexico), Amcor plc (Switzerland), Biffa (UK), Cabka digital (Germany), Jayplas (England), KW Plastics (US), Loop Industries (Canada), MBA Polymers Inc. (US), PET RECYCLING TEAM (Austria), Plastipak Holdings, Inc. (US), REMONDIS SE & Co. KG (Germany), Republic Services (US), Stericycle, Inc. (US), Ultra-Poly Corporation (US), and others in the industrial evaporators market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN RECYCLED PLASTICS MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN RECYCLED PLASTICS MARKET

- 3.2 RECYCLED PLASTICS MARKET, BY PLASTIC TYPE

- 3.3 RECYCLED PLASTICS MARKET, BY END-USE INDUSTRY

- 3.4 RECYCLED PLASTICS MARKET, BY TYPE

- 3.5 RECYCLED PLASTICS MARKET, BY REGION

- 3.6 RECYCLED PLASTICS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Environmental impact of plastic waste and disposal

- 4.2.1.2 Government initiatives and growing awareness

- 4.2.1.3 Increasing use in packaging, automotive, and electrical & electronics industries

- 4.2.1.4 Rising emphasis on chemical recycling

- 4.2.2 RESTRAINTS

- 4.2.2.1 Strong competition from virgin plastics

- 4.2.2.2 Adverse impacts of downcycling

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Favorable initiatives to promote use of recycled plastics in developed countries

- 4.2.3.2 Increasing use in textiles industry in developed Asia Pacific countries

- 4.2.3.3 Development of new recycling technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Ban on imports of waste or scrap plastics in China

- 4.2.4.2 Difficulties in collecting raw materials

- 4.2.4.3 Low recycling rates for most plastics

- 4.2.4.4 Non-acceptance of pigmented plastics by most recycling facilities

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN RECYCLED PLASTICS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 BARGAINING POWER OF SUPPLIERS

- 5.1.2 BARGAINING POWER OF BUYERS

- 5.1.3 THREAT OF SUBSTITUTES

- 5.1.4 THREAT OF NEW ENTRANTS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMICS INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.2.4 TRENDS IN GLOBAL ELECTRONICS INDUSTRY

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 PROMINENT COMPANIES

- 5.3.2 SMALL & MEDIUM-SIZED ENTERPRISES

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE TREND, BY PLASTIC TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND OF PET, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA FOR HS CODE 3915

- 5.6.2 EXPORT DATA FOR HS CODE 3915

- 5.7 KEY CONFERENCES & EVENTS IN 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: HP PARTNERS WITH SUSTAINABLE LIVING SOLUTIONS FOR CLOSED-LOOP PLASTIC RECYCLING

- 5.10.2 CASE STUDY 2: PLASTIC RECYCLING INITIATIVES IN GERMANY

- 5.10.3 CASE STUDY 3: COMPARISON BETWEEN VARIOUS RPET MANAGEMENT METHODS

- 5.11 IMPACT OF 2025 US TARIFF - RECYCLED PLASTICS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON KEY COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END USE INDUSTRIES OF RECYCLED PLASTICS

- 5.11.5.1 Packaging

- 5.11.5.2 Automotive industry

- 5.11.5.3 Construction industry

- 5.11.5.4 Electrical & electronics

- 5.11.5.5 Textiles

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 INTRODUCTION

- 6.2 KEY TECHNOLOGIES

- 6.2.1 MECHANICAL RECYCLING

- 6.2.2 CHEMICAL RECYCLING

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 PLASTIC-TO-FUEL (PTF) TECHNOLOGIES

- 6.3.2 ADVANCED SORTING (AI-BASED + NIR + HYPERSPECTRAL IMAGING)

- 6.4 COMPLEMENTARY TECHNOLOGIES

- 6.4.1 ADDITIVE REMOVAL AND DECONTAMINATION TECHNOLOGY

- 6.4.2 COMPATIBILIZERS AND POLYMER BLENDS

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 METHODOLOGY

- 6.5.3 DOCUMENT TYPE

- 6.5.4 INSIGHTS

- 6.5.5 LEGAL STATUS OF PATENTS

- 6.5.6 JURISDICTION ANALYSIS

- 6.5.7 TOP APPLICANTS

- 6.5.7.1 List of major patents

- 6.6 FUTURE APPLICATIONS

- 6.6.1 EV BATTERY COMPONENTS: ADVANCED RECYCLED ENGINEERING PLASTICS FOR BATTERY ENCLOSURES, THERMAL BARRIERS, CABLE MANAGEMENT SYSTEMS, AND LIGHTWEIGHT EV STRUCTURES

- 6.6.2 3D-PRINTED CONSTRUCTION: ADVANCED FOAMS AND ELASTOMERS FOR BATTERY THERMAL MANAGEMENT AND FIRE PROTECTION

- 6.6.3 CIRCULAR POLYMER FEEDSTOCKS: CHEMICALLY RECYCLED PLASTICS SERVING AS VIRGIN-EQUIVALENT FEEDSTOCKS FOR FOOD-GRADE, MEDICAL-GRADE, AND HIGH-PERFORMANCE POLYMER PRODUCTION

- 6.6.4 SMART BUILDING MATERIALS: HIGH-PERFORMANCE RECYCLED PLASTIC COMPOSITES FOR INSULATION SYSTEMS, STRUCTURAL PANELS, UTILITY INFRASTRUCTURE, AND ENERGY-EFFICIENT BUILDINGS

- 6.7 IMPACT OF AI/GEN AI ON RECYCLED PLASTICS MARKET

- 6.7.1 INTRODUCTION

- 6.8 AI IN RECYCLING INFRASTRUCTURE & PROCESS OPTIMIZATION

- 6.8.1 TOP USE CASES AND MARKET POTENTIAL

- 6.8.2 BEST PRACTICES: COMPANIES/INSTITUTIONS USE CASES

- 6.8.3 CASE STUDIES OF RECYCLED PLASTICS MARKET

- 6.8.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.8.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN RECYCLED PLASTICS MARKET

- 6.8.5.1 Veolia (France): Ai-enabled resource recovery and recycling operations

- 6.8.5.2 Republic services (us): ai-driven recycling infrastructure and material recovery

- 6.8.5.3 Indorama ventures (Thailand) ai-supported digital transformation of circular materials operations

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO APPLICATIONS OF RECYCLED PLASTICS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELLING, AND ECO STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOUR

- 8.1 DECISION-MAKING PROCESS

- 8.1.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.1.2 BUYING CRITERIA

- 8.2 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.3 MARKET PROFITABILITY

- 8.3.1 REVENUE POTENTIAL

- 8.3.2 COST DYNAMICS

- 8.3.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

9 RECYCLED PLASTICS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 POST-CONSUMER RECYCLATES

- 9.2.1 INCREASED USE OF PLASTICS IN TEXTILES, FOOD & BEVERAGE, AND COSMETICS TO FUEL MARKET

- 9.3 INDUSTRIAL RECYCLATES

- 9.3.1 INDUSTRIAL RECYCLATES HELP REDUCE GREENHOUSE GAS EMISSIONS AND SAVE ENERGY

10 RECYCLED PLASTICS MARKET, BY SOURCE

- 10.1 INTRODUCTION

- 10.2 BOTTLES

- 10.2.1 BOTTLES TO BE LARGEST SOURCE OF MATERIAL FOR RECYCLED PLASTICS

- 10.3 FILMS

- 10.3.1 GROWING DEMAND FOR FLEXIBLE PACKAGING AND FILM RECYCLING TO DRIVE MARKET

- 10.4 FIBERS

- 10.4.1 GROWTH OF TEXTILE SECTOR TO PROPEL DEMAND

- 10.5 FOAMS

- 10.5.1 GROWING APPLICATIONS IN CUSHIONING MATERIALS AND PANELS FOR BUILDINGS TO DRIVE MARKET

- 10.6 OTHER SOURCES

11 RECYCLED PLASTICS MARKET, BY PLASTIC TYPE

- 11.1 INTRODUCTION

- 11.2 POLYETHYLENE TEREPHTHALATE (PET)

- 11.2.1 OFFERS REPEATED RECYCLEABILITY AND WIDE APPLICATION RANGE

- 11.3 POLYETHYLENE (PE)

- 11.3.1 EASY RECYCLABILITY TO DRIVE MARKET GROWTH

- 11.4 POLYVINYL CHLORIDE (PVC)

- 11.4.1 WIDE USAGE OF RECYCLED PVC IN BUILDING & CONSTRUCTION TO PROPEL MARKET GROWTH

- 11.5 POLYPROPYLENE (PP)

- 11.5.1 RAPID INDUSTRIALIZATION TO DRIVE GROWTH OF RECYCLED PP MARKET

- 11.6 POLYSTYRENE (PS)

- 11.6.1 ASIA PACIFIC TO BE DOMINANT MARKET FOR POLYSTYRENE SEGMENT

- 11.7 OTHER PLASTICS

12 RECYCLED PLASTICS MARKET, BY END-USE INDUSTRY

- 12.1 INTRODUCTION

- 12.2 PACKAGING

- 12.2.1 RISING USE OF RECYCLED PLASTICS IN PACKAGING INDUSTRY TO BOOST DEMAND

- 12.3 BUILDING & CONSTRUCTION

- 12.3.1 ASIA PACIFIC TO BE LARGEST MARKET FOR RECYCLED PLASTICS IN BUILDING & CONSTRUCTION

- 12.4 TEXTILES

- 12.4.1 USE OF RECYCLED PLASTICS INCREASING TO CREATE MORE SUSTAINABLE VERSIONS OF FABRICS

- 12.5 AUTOMOTIVE

- 12.5.1 GROWING SUSTAINABILITY CONCERNS FUELING ADOPTION

- 12.6 ELECTRICALS & ELECTRONICS

- 12.6.1 SUSTAINABILITY GOALS AND MOVE TOWARD CARBON NEUTRALITY TO SUPPORT MARKET GROWTH

- 12.7 OTHER END-USE INDUSTRIES

13 RECYCLED PLASTICS MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 ASIA PACIFIC

- 13.2.1 CHINA

- 13.2.1.1 Rapid industrialization to increase domestic plastic recycling

- 13.2.2 JAPAN

- 13.2.2.1 Rise in environmental awareness and increase in consumer plastic waste recycling services to enhance demand

- 13.2.3 INDIA

- 13.2.3.1 Rising demand for fast-moving consumer goods to drive market

- 13.2.4 SOUTH KOREA

- 13.2.4.1 Government initiatives for plastic recycling to support market growth

- 13.2.5 REST OF ASIA PACIFIC

- 13.2.1 CHINA

- 13.3 EUROPE

- 13.3.1 GERMANY

- 13.3.1.1 Presence of strong domestic recycling industry to drive market

- 13.3.2 UK

- 13.3.2.1 Increasing preference for recycled plastics among consumers and manufacturers to support growth

- 13.3.3 FRANCE

- 13.3.3.1 Increase in consumption of packaged food & beverage to fuel demand for recycled plastics

- 13.3.4 ITALY

- 13.3.4.1 Technological advancements to support expansion of plastic recycling

- 13.3.5 SPAIN

- 13.3.5.1 Investments in plastic recycling by plastic raw material manufacturers to drive market

- 13.3.6 REST OF EUROPE

- 13.3.1 GERMANY

- 13.4 NORTH AMERICA

- 13.4.1 US

- 13.4.1.1 Government initiatives to increase plastic recycling to drive demand

- 13.4.2 CANADA

- 13.4.2.1 Presence of well-established recycling infrastructure to boost demand for recycled plastics

- 13.4.3 MEXICO

- 13.4.3.1 Large consumption of bottled water offering significant opportunities for plastic recycling

- 13.4.1 US

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.5.1.1 Saudi Arabia

- 13.5.1.1.1 Consumers investing in innovative packaging designs for newer recycled plastic products to drive demand

- 13.5.1.2 Rest of GCC countries

- 13.5.1.1 Saudi Arabia

- 13.5.2 IRAN

- 13.5.2.1 Limited access to virgin plastics due to international sanctions to increase demand

- 13.5.3 SOUTH AFRICA

- 13.5.3.1 Increased use of recycled plastics in packaging applications to fuel growth

- 13.5.4 REST OF MIDDLE EAST & AFRICA

- 13.5.1 GCC COUNTRIES

- 13.6 SOUTH AMERICA

- 13.6.1 BRAZIL

- 13.6.1.1 High plastic waste generation to boost market growth

- 13.6.2 ARGENTINA

- 13.6.2.1 Large food & beverage sector to drive demand for plastic recycling

- 13.6.3 REST OF SOUTH AMERICA

- 13.6.1 BRAZIL

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 RANKING OF KEY MARKET PLAYERS, 2025

- 14.4.2 MARKET SHARE ANALYSIS, 2025

- 14.4.2.1 Veolia (France)

- 14.4.2.2 Republic Services (US)

- 14.4.2.3 Amcor plc (Switzerland)

- 14.4.2.4 Alpek S.A.B. de C.V (Mexico)

- 14.5 BRAND/PRODUCT COMPARISON

- 14.5.1 PLASTILOOP BY VEOLIA

- 14.5.2 DEJA

- 14.5.3 REPUBLIC SERVICES

- 14.5.4 AMCOR PLC

- 14.5.5 ALPEK POLYESTER

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 14.6.5.1 Company footprint

- 14.6.5.2 Region footprint

- 14.6.5.3 Plastic type footprint

- 14.6.5.4 Source footprint

- 14.6.5.5 Type footprint

- 14.6.5.6 Process footprint

- 14.6.5.7 End-use industry footprint

- 14.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 DYNAMIC COMPANIES

- 14.7.4 STARTING BLOCKS

- 14.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 14.7.5.1 Detailed list of key startups/SMEs

- 14.7.5.2 Competitive benchmarking of key startups/SMEs

- 14.8 COMPETITIVE SCENARIO

- 14.8.1 PRODUCT LAUNCHES

- 14.8.2 DEALS

- 14.8.3 EXPANSIONS

- 14.9 COMPANY VALUATION AND FINANCIAL METRICS

15 COMPANY PROFILES

- 15.1 MAJOR PLAYERS

- 15.1.1 VEOLIA

- 15.1.1.1 Business overview

- 15.1.1.2 Products offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Deals

- 15.1.1.4 Expansions

- 15.1.1.5 MnM view

- 15.1.1.5.1 Right to win

- 15.1.1.5.2 Strategic choices

- 15.1.1.5.3 Weaknesses and competitive threats

- 15.1.2 INDORAMA VENTURES

- 15.1.2.1 Business overview

- 15.1.2.2 Products offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Product launches

- 15.1.2.3.2 Deals

- 15.1.2.3.3 Expansions

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 REPUBLIC SERVICES, INC.

- 15.1.3.1 Business overview

- 15.1.3.2 Products offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Expansion

- 15.1.3.3.3 Others

- 15.1.3.3.4 Right to win

- 15.1.3.3.5 Strategic choices

- 15.1.3.3.6 Weaknesses and competitive threats

- 15.1.4 AMCOR PLC

- 15.1.4.1 Business overview

- 15.1.4.2 Products offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches

- 15.1.4.3.2 Deals

- 15.1.4.3.3 Expansions

- 15.1.4.3.4 Right to win

- 15.1.4.3.5 Strategic choices

- 15.1.4.3.6 Weaknesses and competitive threats

- 15.1.5 ALPEK S.A.B DE C.V.

- 15.1.5.1 Business overview

- 15.1.5.2 Products offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 BIFFA

- 15.1.6.1 Business overview

- 15.1.6.2 Products offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Product Launches

- 15.1.6.3.2 Deals

- 15.1.6.3.3 Expansions

- 15.1.7 FAR EASTERN NEW CENTURY CORPORATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Expansions

- 15.1.8 JAYPLAS

- 15.1.8.1 Business overview

- 15.1.8.2 Products offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Expansions

- 15.1.9 KW PLASTICS

- 15.1.9.1 Business overview

- 15.1.9.2 Products offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Deals

- 15.1.9.3.2 Expansions

- 15.1.10 LOOP INDUSTRIES, INC.

- 15.1.10.1 Business overview

- 15.1.10.2 Products offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Product launches

- 15.1.10.3.2 Deals

- 15.1.10.3.3 Expansion

- 15.1.11 MBA POLYMERS INC.

- 15.1.11.1 Business overview

- 15.1.11.2 Products offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Expansions

- 15.1.12 PET RECYCLING TEAM

- 15.1.12.1 Business overview

- 15.1.12.2 Products offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Expansions

- 15.1.13 PLASTIPAK HOLDINGS, INC.

- 15.1.13.1 Business overview

- 15.1.13.2 Products offered

- 15.1.13.3 Recent developments

- 15.1.13.3.1 Deals

- 15.1.13.3.2 Expansions

- 15.1.14 REMONDIS SE & CO. KG

- 15.1.14.1 Business overview

- 15.1.14.2 Products offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Deals

- 15.1.14.3.2 Expansions

- 15.1.15 UNIFI, INC.

- 15.1.15.1 Business overview

- 15.1.15.2 Products offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product Launches

- 15.1.15.3.2 Deals

- 15.1.16 ULTRA POLY CORPORATION

- 15.1.16.1 Business overview

- 15.1.16.2 Products offered

- 15.1.17 SUZHOU JIULONG RECYCLING TECHNOLOGY CO., LTD.

- 15.1.17.1 Business Overview

- 15.1.17.2 Products offered

- 15.1.17.3 Recent developments

- 15.1.17.3.1 Expansions

- 15.1.1 VEOLIA

- 15.2 OTHER PLAYERS

- 15.2.1 FRESH PAK

- 15.2.2 CUSTOM POLYMERS

- 15.2.3 ENVISION PLASTICS

- 15.2.4 GREENPATH ENTERPRISES, INC.

- 15.2.5 B&B PLASTICS INC.

- 15.2.6 PET PROCESSORS LLC

- 15.2.7 REPLAS

- 15.2.8 DALMIA POLYPRO INDUSTRIES PVT. LTD.

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.1.1 List of key secondary sources

- 16.1.1.2 Key data from secondary sources

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Key data from primary sources

- 16.1.2.2 Key industry insights

- 16.1.2.3 List of primary participants

- 16.1.2.4 Breakdown of primary interviews

- 16.1.1 SECONDARY DATA

- 16.2 MARKET SIZE ESTIMATION

- 16.2.1 BOTTOM-UP APPROACH

- 16.2.2 TOP-DOWN APPROACH

- 16.3 MARKET FORECAST APPROACH

- 16.3.1 DEMAND-SIDE ANALYSIS

- 16.3.2 SUPPLY-SIDE ANALYSIS

- 16.3.3 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 16.4 GROWTH FORECAST

- 16.5 DATA TRIANGULATION

- 16.6 RESEARCH ASSUMPTIONS

- 16.7 RESEARCH LIMITATIONS

- 16.8 RISK ASSESSMENT

- 16.9 FACTOR ANALYSIS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS