|

시장보고서

상품코드

2061157

바이오 비료 시장 예측(-2031년) : 유형별, 원료별, 시용 방법별, 형태별, 작물 유형별, 지역별Biofertilizer Market by Type, Crop Type, Mode of Application, Form, Source, Region - Global Forecast to 2031 |

||||||

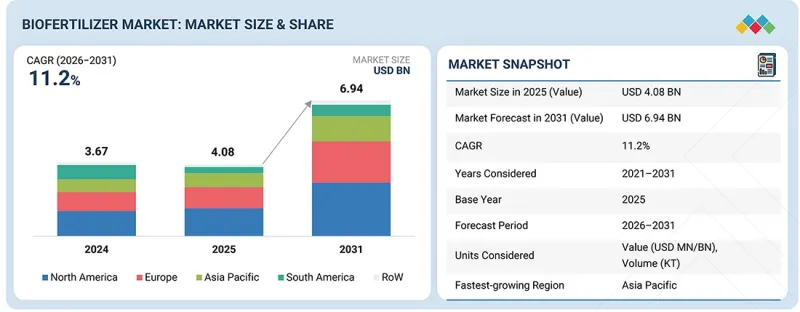

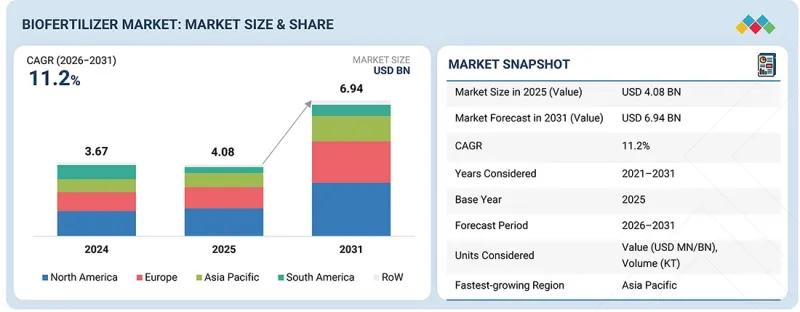

세계의 바이오 비료 시장은 2026년 408만 달러에서 2031년까지 694만 달러에 달할 것으로 예측되고 있으며, 2026-2031년까지 연평균 성장률(CAGR)은 11.2%에 달할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(100만/10억 달러) 및 수량(1,000톤) |

| 부문 | 유형별, 원료별, 시용 방법별, 형태별, 작물 유형별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 남미, 기타 지역 |

바이오 비료 업계는 바이오 작물 영양 솔루션에 대한 전 세계적 수요 증가, 토양 양분의 활용, 그리고 농업 관행에서의 지속가능성 추구에 힘입어 2031년까지 견고한 성장이 예상됩니다. 이 업계는 미생물 생명공학, 정밀농업, 생물제제 및 기타 재생형 농업 관행의 급속한 혁신과 보급에 힘입어 급속한 변화를 겪고 있습니다. Novonesis와 UPL Limited 등 주요 기업은 첨단 미생물 균주, 다영양소 바이오 비료 제제, 그리고 열대 농업용 바이오 솔루션 개발을 위해 협력을 강화하고 있습니다. 앞으로 등장할 혁신 기술에는 고성능 미생물 컨소시엄, 액상 생물 제제, 가뭄 및 염분 내성을 가진 미생물, 그리고 작물 특이적 영양분 동원제 등이 포함됩니다. 유기농 식품, 영양소 이용 효율, 통합 영양소 관리, 그리고 탄소 중립적인 작물 생산 방식에 대한 수요가 증가함에 따라 생물학적 연구 인프라, 첨단 발효 기술 및 표적 전달 시스템에 대한 투자가 늘어나고 있습니다. 토양 건강 상태의 악화, 화학 비료의 과다 사용, 기후 지속가능성에 대한 의식의 향상는 전 세계에서 바이오 작물 영양 솔루션에 대한 수요를 계속해서 끌어올릴 것으로 보입니다.

바이오 비료 시장의 기회와 변화

바이오 비료 시장은 미생물 솔루션 제공업체, 프로젝트 개발자, 지속가능한 농업 기술에 주력하는 혁신 기업 등 농업 생명공학 분야의 주요 주체들에게 강력한 성장 잠재력을 보여주고 있습니다. 이러한 추세는 생물 유래 작물 생산에 대한 전 세계적인 수요 증가와 재생 농업의 확산에 힘입어 나타나고 있습니다. 농자재 공급업체에게 주어진 기회로는 미생물 제제, 바이오 자극제, 정밀 시비 툴을 결합한 통합적인 영양 관리 시스템을 구축하여 자원을 보존하면서 작물의 수확량을 향상시키는 것을 들 수 있습니다. 또한 다양한 작물에 사용할 수 있는 다목적 생물제제, 스트레스 내성을 지닌 미생물 균주, 그리고 식물의 성장을 촉진하는 첨단 생물 시비 시스템을 개발하는 미생물 기술 제공업체에게도 시장 전망은 밝습니다. 시장 상황은 정밀농업의 급속한 보급, 화학 비료에 대한 규제 강화, 잔류물이 없는 제품에 대한 수요 증가, 그리고 기후 변화를 고려한 회복력 있는 농업에 대한 집중 등 여러 요인의 영향을 받아 여전히 매우 역동적인 양상을 보이고 있습니다. 주요 기업은 미생물 제품의 과학적 검증을 우선시하고, 포장에서 일관된 성능을 입증하며, 지속가능하고 비용 대비 효과가 높은 작물 생산 솔루션에 대한 농가의 요구를 충족시키는 기업이 될 것입니다.

AI를 활용한 영양분 최적화 - 바이오 비료 시장에서는 미생물 제제의 개발, 영양분 최적화 및 정밀농업의 실천을 개선하기 위해 인공지능(AI)과 기계 학습이 점점 더 많이 도입되고 있습니다. 이러한 기술은 토양 조건, 작물의 영양소 요구량 및 환경 요인을 분석하여 바이오 비료의 시비 효과를 높이는 데 도움이 됩니다.

첨단 제제 기술 - 바이오 비료 시장에서 이러한 기술들은 농업 용도에서 미생물의 안정성, 저장 기간 및 영양소 공급 효율 향상에 중점을 두고 있습니다. 액상 제제, 마이크로캡슐화, 운반체 기반 시스템, 서방형 전달 플랫폼 등의 기술을 통해, 포장 조건 하에서 유익한 미생물의 생존율과 성능이 향상되고 있습니다. 또한 기업은 질소 고정, 인산 용해 및 스트레스 내성을 동시에 개선할 수 있는 다기능 미생물 컨소시엄 개발도 추진하고 있습니다.

작물별 부문에서 곡물·곡류는 바이오 비료 시장에서 가장 큰 시장 점유율을 차지하고 있습니다.

곡물은 광대한 재배 면적, 높은 영양 요구량, 그리고 지속가능한 작물 생산 방식에 대한 수요 증가로 인해 전 세계 바이오 비료 시장의 작물별 부문에서 가장 큰 점유율을 차지하고 있습니다. 밀, 쌀, 옥수수, 보리, 수수 등 주요 곡물은 높은 생산성을 유지하기 위해 다량의 영양분을 공급해야 하므로, 전 세계의 대규모 농업 시스템에서 바이오 비료의 도입이 가속화되고 있습니다. 곡물 재배에서는 질소 고정, 인의 동원, 토양 미생물의 활성 및 양분 이용 효율을 높이는 동시에 화학 비료에 대한 의존도를 낮추기 위해 바이오 비료의 사용이 점점 확대되고 있습니다. 토양 열화, 토양 비옥도 저하, 그리고 화학 비료의 과다 사용으로 인한 환경 영향에 대한 우려가 커지면서, 농가가 곡물 생산에 있으며, 생물학적 영양소 관리 솔루션을 도입하도록 더욱 촉진하고 있습니다. 또한 전 세계 식량 수요의 증가, 지속가능한 농업 관행의 확대, 그리고 통합 영양소 관리 프로그램에 대한 정부의 지원 강화가 곡물 및 곡물 재배 지역 전반에 걸쳐 바이오 비료의 도입을 촉진하고 있습니다. 미생물 제제, 액체 바이오 비료 및 정밀농업 분야의 기술적 진보는 밭에서의 성능과 작물 생산성을 더욱 향상시키고 있으며, 전 세계 바이오 비료 시장에서 곡물 부문의 장기적인 성장을 지원하고 있습니다.

바이오 비료 시장에서 사업을 운영하는 주요 기업의 최고경영자(CEO), 이사 및 기타 임원들을 대상으로 심층 인터뷰를 시행했습니다. :

시장의 주요 기업으로는 Novonesis, UPL Limited, Syngenta AG, T. Stanes &Company, Lallemand Inc., Rizobacter Argentina S.A., Gujarat State Fertilizers and Chemicals Ltd(GSFC), Madras Fertilizers Limited, IPL Biologicals, Koppert Biological Systems, Corteva Agriscience, Kan Biosys, Mapleton Agri Biotech Pvt Ltd, Seipasa S.A. 및 AgriLife 등을 들 수 있습니다.

조사 범위:

이 보고서의 조사 범위는 전 세계 바이오 비료 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 억제요인, 과제 및 기회 등)에 관한 상세한 정보를 포괄하고 있습니다. 주요 업계 진출 기업에 대해 상세한 분석을 수행하고, 해당 기업의 사업 개요, 솔루션 및 서비스, 주요 전략, 계약, 파트너십, 그리고 합의 사항에 대한 인사이트를 제공합니다. 바이오 비료 시장과 관련된 신제품·서비스 출시, 합병·인수, 그리고 최근 동향. 이 보고서에서는 바이오 비료 시장 생태계내 신생 스타트업 기업의 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유:

이 보고서는 바이오 비료 시장 전체 및 각 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 시장 선도 기업과 신규 진입 기업을 지원합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 더 심층 인사이트를 얻어 자사의 비즈니스를 적절히 포지셔닝하며, 적절한 시장 진입 전략을 수립하는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움을 주며, 주요 시장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

1. 유형, 작물 유형, 형태, 원료, 시용 방법에 걸친 상세한 세분화 - 본 조사에서는 주요 촉진요인(지속가능한 농업 관행의 보급 확대, 토양 열화 및 화학 비료 과다 사용에 대한 우려 증가, 생물 유래 작물 영양 제품에 대한 정부의 지원, 작물 수확량 및 영양 효율 향상에 대한 관심 증가), 억제요인(개발도상국 시장에서 농가의 낮은 인지도, 유통 기한 및 저장 안정성의 한계, 기후 조건에 따른 포장내 성능의 편차), 기회(유기 농업 산업의 확대, 신흥 농업 경제권에서의 강력한 성장 잠재력, 미생물 및 제제 기술의 발전) 및 과제(제품 오염 및 품질 일관성 문제, 복잡한 규제 승인 요건, 저비용 화학 비료와의 경쟁)를 분석하고 있습니다.

2. 신흥 시장에 초점을 맞춘 지역별 인사이트 - 이 보고서는 아시아태평양, 북미, 유럽, 라틴아메리카, 중동 및 아프리카의 성장 기회를 강조하고, 국가 및 지역 차원의 상세한 분석을 제공합니다. 지역별 수요 패턴, 관개 보급률, 영양 관리와 관련된 규제 정책, 정밀농업에 대한 투자 동향을 평가하여 사업 확대 및 현지화를 위한 전략적 지침을 제공합니다.

3. 경쟁 정보 및 혁신 동향 - 주요 시장 진출 기업에 대한 조사 - Novonesis, UPL Limited, Syngenta AG, T. Stanes &Company, Lallemand Inc., Rizobacter Argentina S.A., Gujarat State Fertilizers and Chemicals Ltd(GSFC), Madras Fertilizers Limited, IPL Biologicals, Koppert Biological Systems, Corteva Agriscience, Kan Biosys, Mapleton Agri Biotech Pvt Ltd, Seipasa S.A. 및 AgriLife.

4. 데이터베이스 조사 기법에 따른 수요 예측 - 2031년까지 시장 규모 및 성장 전망은 탑다운(top-down) 및 바텀업(bottom-up) 접근법을 결합하여 수립되었으며, 업계 전문가, 업계 단체 및 정부의 공식 데이터를 통해 검증되었습니다. 이러한 인사이트는 세계 시장에서의 투자 계획 수립 및 시장 기회 평가를 위한 신뢰할 수 있는 지침이 됩니다.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 구상

제8장 고객 상황과 구매 행동

제9장 바이오 비료 시장(유형별)

제10장 바이오 비료 시장(원료별)

제11장 바이오 비료 시장(시용 방법별)

제12장 바이오 비료 시장(형태별)

제13장 바이오 비료 시장(작물 유형별)

제14장 바이오 비료 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 인접 시장 및 관련 시장

제19장 부록

KSA 26.06.25The biofertilizer market is projected to reach USD 6.94 million by 2031 from USD 4.08 million in 2026, at a CAGR of 11.2% from 2026 to 2031.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD MN/BN) and Volume (KT) |

| Segments | By Type, Crop Type, Mode of Application, Form, Source, and Region |

| Regions covered | North America, Europe, Asia Pacific, South America, RoW |

The biofertilizers industry is expected to witness robust growth through 2031, driven by soaring global demand for bio-crop nutrition solutions, the mobilization of soil nutrients, and the pursuit of sustainability in agricultural practices. The industry is witnessing a rapid transition driven by rapid innovation and adoption of microbial biotech, precision agriculture, biological formulations, and other regenerative farming practices. Leading players such as Novonesis and UPL Limited are aligning to develop advanced microbial strains, multi-nutrient biofertilizer formulations, and tropical agricultural biosolutions. Some of the upcoming innovations include high-performance microbial consortia, liquid biological formulations, drought and salinity-tolerant microbes, and crop-specific nutrient mobilizers. Investments are being increased in biological research infrastructure, advanced fermentation technologies, and targeted delivery systems to meet the rising demand for organic food, nutrient use efficiency, integrated nutrient management, and carbon-neutral crop production practices. Growing awareness of soil health degradation, chemical fertilizer overuse, and climate sustainability is likely to continue boosting demand for global bio-crop nutrition solutions.

Opportunities and Disruptions in the Biofertilizer Market

The biofertilizer market shows strong growth potential for players in the agricultural biotechnology sector, including microbial solution providers, project developers, and innovators focused on sustainable farming technology. This trend is driven by increasing global demand for biologically based crop production and the growing adoption of regenerative agriculture. Opportunities for agricultural input vendors include creating integrated nutrient management systems that combine microbial inoculants, biostimulants, and precision application tools to boost crop yields while conserving resources. Market prospects are also favorable for microbial technology providers developing multi-purpose biological formulations for different crops, stress-resistant microbial strains, and advanced biological application systems that promote plant growth. The market landscape remains highly dynamic, influenced by the rapid spread of precision farming, stricter regulations on chemical fertilizers, rising demand for residue-free products, and a focus on climate-smart, resilient agriculture. The leading companies will be those that prioritize scientific validation of microbial products, demonstrate consistent performance in the field, and meet farmers' needs for sustainable and cost-effective crop production solutions.

AI-driven nutrient optimization: Artificial intelligence and machine learning are increasingly being adopted in the biofertilizer market to improve microbial formulation development, nutrient optimization, and precision farming practices. These technologies help analyze soil conditions, crop nutrient requirements, and environmental factors to improve the effectiveness of biofertilizer applications.

Advanced formulation technologies: These technologies in the biofertilizer market focus on improving microbial stability, shelf life, and nutrient delivery efficiency in agricultural applications. Technologies such as liquid formulations, microencapsulation, carrier-based systems, and controlled-release delivery platforms are enhancing the survival and performance of beneficial microorganisms under field conditions. Companies are also developing multifunctional microbial consortia capable of simultaneously improving nitrogen fixation, phosphate solubilization, and stress tolerance.

Cereals & grains hold the largest market share in the biofertilizer market within the crop-type segment.

Cereals & grains account for the largest share of the crop-type segment of the global biofertilizer market, owing to their extensive cultivation area, high nutrient requirements, and growing demand for sustainable crop production practices. Major cereal and grain crops such as wheat, rice, maize, barley, and sorghum require significant nutrient inputs to maintain high productivity, accelerating the adoption of biofertilizers across large-scale farming systems globally. Biofertilizers are increasingly used in cereal cultivation to enhance nitrogen fixation, phosphorus mobilization, soil microbial activity, and nutrient-use efficiency, while reducing dependence on synthetic fertilizers. Rising concerns about soil degradation, declining soil fertility, and the environmental impacts associated with excessive chemical fertilizer use are further encouraging farmers to adopt biological nutrient management solutions in cereal production. In addition, growing global food demand, the expansion of sustainable agricultural practices, and increasing government support for integrated nutrient management programs are strengthening the adoption of biofertilizers across cereal and grain-farming regions. Technological advancements in microbial formulations, liquid biofertilizers, and precision farming are further improving field performance and crop productivity, supporting the long-term growth of the cereals & grains segment within the global biofertilizer market.

In-depth interviews were conducted with chief executive officers (CEOs), directors, and other executives from various key organizations operating in the Biofertilizer Market:

- By Company Type: Tier 1 - 25%, Tier 2 - 45%, and Tier 3 - 30%

- By Designation: Directors - 20%, Managers - 50%, Executives - 30%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 20%, South America - 15%, and Rest of the World (Middle East and Africa) -10%

Prominent companies in the market include Novonesis, UPL Limited, Syngenta AG, T. Stanes & Company, Lallemand Inc., Rizobacter Argentina S.A., Gujarat State Fertilizers and Chemicals Ltd (GSFC), Madras Fertilizers Limited, IPL Biologicals, Koppert Biological Systems, Corteva Agriscience, Kan Biosys, Mapleton Agri Biotech Pvt Ltd, Seipasa S.A., and AgriLife.

Research Coverage:

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the global biofertilizer market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions and services, key strategies, contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the biofertilizer market. This report covers competitive analysis of upcoming startups in the biofertilizer market ecosystem.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue figures for the overall biofertilizer market and the subsegments. This report will help stakeholders understand the competitive landscape and gain deeper insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

1. In-depth Segmentation across Type, Crop Type, Form, Source and Mode of Application: The study examines key drivers (rising adoption of sustainable farming practices, growing concerns over soil degradation and chemical fertilizer overuse, government support for biological crop nutrition products, increasing focus on improving crop yield and nutrient efficiency), restraints (low farmer awareness in developing markets, limited shelf life and storage stability, variable field performance across climatic conditions), opportunities (expanding organic agriculture industry, strong growth potential in emerging agricultural economies, advancements in microbial and formulation technologies), and challenges (product contamination and quality consistency issues, complex regulatory approval requirements, competition from low-cost chemical fertilizer).

2. Region-specific Insights with Focus on Emerging Markets: The report provides detailed country- and region-level analysis, highlighting growth opportunities across Asia Pacific, North America, Europe, Latin America, and the Middle East & Africa. It evaluates regional demand patterns, irrigation penetration, regulatory policies related to nutrient management, and investment trends in precision agriculture, offering strategic guidance for expansion and localization initiatives.

3. Competitive Intelligence and Innovation Landscape: A study of leading market participants: Novonesis, UPL Limited, Syngenta AG, T. Stanes & Company, Lallemand Inc., Rizobacter Argentina S.A., Gujarat State Fertilizers and Chemicals Ltd (GSFC), Madras Fertilizers Limited, IPL Biologicals, Koppert Biological Systems, Corteva Agriscience, Kan Biosys, Mapleton Agri Biotech Pvt Ltd, Seipasa S.A., and AgriLife.

4. Demand Forecasts Backed by Data-driven Methodologies: Market sizing and growth projections through 2031 are developed using a combination of top-down and bottom-up approaches, validated by industry experts, trade associations, and official government data. These insights provide reliable guidance for investment planning and market opportunity assessment in the global sector.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN BIOFERTILIZERS MARKET

- 2.4 HIGH-GROWTH SEGMENTS AND EMERGING FRONTIERS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN BIOFERTILIZER MARKET

- 3.2 BIOFERTILIZER MARKET, BY TYPE AND REGION

- 3.3 BIOFERTILIZER MARKET, BY SOURCE

- 3.4 BIOFERTILIZER MARKET, BY COUNTRY/REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rising adoption of sustainable farming practices

- 4.2.1.2 Growing concerns over soil degradation and chemical fertilizer overuse

- 4.2.1.3 Government support for biological crop nutrition products

- 4.2.1.4 Increasing focus on improving crop yield and nutrient efficiency

- 4.2.2 RESTRAINTS

- 4.2.2.1 Low farmer awareness in developing markets

- 4.2.2.2 Limited shelf life and storage stability

- 4.2.2.3 Variable field performance across climatic conditions

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Expanding organic agriculture industry

- 4.2.3.2 Strong growth potential in emerging agricultural economies

- 4.2.3.3 Advancements in microbial and formulation technologies

- 4.2.4 CHALLENGES

- 4.2.4.1 Product contamination and quality consistency issues

- 4.2.4.2 Complex regulatory approval requirements

- 4.2.4.3 Competition from Low-cost chemical fertilizers

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN BIOFERTILIZERS MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.2 ECOSYSTEM SHIFTS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 GLOBAL NITROGEN NUTRIENT DEMAND SUPPORTING ADOPTION OF NITROGEN-FIXING BIOFERTILIZERS

- 5.2.2 EXPANSION OF AGRICULTURAL VALUE ADDED SUPPORTING BIOFERTILIZER MARKET GROWTH

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 INTERMEDIATE PROCESSING & STRAIN DEVELOPMENT

- 5.3.3 FORMULATION & PRODUCT MANUFACTURING

- 5.3.4 CUSTOMIZATION & BRANDING & PRIVATE LABELING

- 5.3.5 DISTRIBUTION & SUPPLY NETWORK

- 5.3.6 END USERS & POST-SALES SUPPORT

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 DEMAND SIDE

- 5.4.2 SUPPLY SIDE

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE BY KEY PLAYERS, TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND, BY REGION

- 5.5.3 AVERAGE SELLING PRICE TREND, BY FORM

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO OF HS CODE 3101

- 5.6.2 IMPORT SCENARIO OF HS CODE 3101

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 AI-DRIVEN MICROBIAL DISCOVERY FOR NEXT-GENERATION BIOFERTILIZER DEVELOPMENT

- 5.9.2 LEVERAGING MACHINE LEARNING FOR ADVANCED MICROBIAL SEED TREATMENT INNOVATION

- 5.9.3 AI-ENABLED COMPUTATIONAL BIOLOGY FOR PRECISION MICROBIAL AGRICULTURAL SOLUTIONS

- 5.10 IMPACT OF 2026 US TARIFFS - BIOFERTILIZERS MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRIES/REGIONS

- 5.10.4.1 China (Asia Pacific)

- 5.10.4.2 India

- 5.10.4.3 European Union

- 5.10.4.4 Brazil

- 5.10.5 IMPACT ON END-USE INDUSTRIES

- 5.11 INVESTMENT AND FUNDING SCENARIO

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 SYNTHETIC MICROBIAL CONSORTIA (SYNCOM) & MULTI-STRAIN BIOFERTILIZERS

- 6.1.2 NANO-ENCAPSULATION & NANOBIOFERTILIZER TECHNOLOGY

- 6.1.3 AI-DRIVEN PRECISION BIOFERTILIZER & SMART AGRICULTURE INTEGRATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 PRECISION IRRIGATION & FERTIGATION SYSTEMS

- 6.2.2 DIGITAL AGRICULTURE & SOIL MONITORING PLATFORMS

- 6.2.3 BIOSTIMULANT INTEGRATION & HYBRID BIOLOGICAL INPUT TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BIOLOGICAL SEED ENHANCEMENT & MICROBIOME ENGINEERING

- 6.3.2 CONTROLLED ENVIRONMENT AGRICULTURE (CEA) & HYDROPONIC BIOLOGICAL NUTRITION

- 6.3.3 AGRICULTURAL BIOTECHNOLOGY & GENE-EDITED CROP COMPATIBILITY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | FOUNDATION & EARLY COMMERCIALIZATION

- 6.4.2 MID-TERM (2027-2030) | EXPANSION & STANDARDIZATION

- 6.4.3 LONG-TERM (2030-2035+) | MASS COMMERCIALIZATION & DISRUPTION

- 6.5 PATENT ANALYSIS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 BIO-ENGINEERED MICROBIAL CONSORTIA

- 6.6.2 AI-DRIVEN PRECISION BIOFERTILIZATION

- 6.6.3 ADVANCED ENCAPSULATION & CONTROLLED-RELEASE SYSTEMS

- 6.6.4 MULTI-FUNCTIONAL BIOLOGICAL INPUT SYSTEMS

- 6.6.5 SUSTAINABLE BIO-BASED PRODUCTION

- 6.7 IMPACT OF GENERATIVE AI ON BIOFERTILIZER MARKET

- 6.7.1 INTRODUCTION

- 6.7.2 USE OF GENERATIVE AI ON BIOFERTILIZER MARKET

- 6.7.3 TOP USE CASES AND MARKET POTENTIAL

- 6.7.4 BEST PRACTICES IN BIOFERTILIZERS INDUSTRY

- 6.7.5 CASE STUDIES OF AI IMPLEMENTATION IN BIOFERTILIZER MARKET

- 6.7.6 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.7 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN BIOFERTILIZER MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.3 IMPACT OF REGULATORY POLICIES ON SUSTAINABILITY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIER AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USER/END-USE INDUSTRIES

- 8.4.1 FIELD CROP FARMERS (CEREALS, GRAINS, OILSEEDS)

- 8.4.2 HORTICULTURE & SPECIALTY CROP PRODUCERS

- 8.4.3 ORGANIC FARMING INDUSTRY

- 8.4.4 GREENHOUSE & PROTECTED CULTIVATION SECTOR

- 8.4.5 AGRICULTURAL COOPERATIVES & INPUT DISTRIBUTORS

- 8.4.6 LARGE AGRIBUSINESS & COMMERCIAL FARMING ENTERPRISES

- 8.5 MARKET PROFITABILITY

9 BIOFERTILIZERS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 NITROGEN-FIXING BIOFERTILIZERS

- 9.2.1 RISING DEMAND FOR SUSTAINABLE NITROGEN MANAGEMENT SUPPORTING ADOPTION OF NITROGEN FIXING BIOFERTILIZERS

- 9.3 PHOSPHATE-SOLUBILIZING & -MOBILIZING BIOFERTILIZERS

- 9.3.1 INCREASING FOCUS ON PHOSPHORUS USE EFFICIENCY: ACCELERATING ADOPTION OF PHOSPHATE-SOLUBILIZING BIOFERTILIZERS

- 9.4 POTASSIUM-SOLUBILIZING & -MOBILIZING BIOFERTILIZERS

- 9.4.1 GROWING EMPHASIS ON SOIL NUTRIENT EFFICIENCY DRIVING DEMAND FOR POTASSIUM-MOBILIZING BIOFERTILIZERS

- 9.5 OTHER TYPES

10 BIOFERTILIZERS MARKET, BY SOURCE

- 10.1 INTRODUCTION

- 10.2 BACTERIAL

- 10.2.1 EXPANDING USE OF BENEFICIAL BACTERIAL STRAINS DRIVING GROWTH OF BACTERIAL BIOFERTILIZERS

- 10.3 FUNGAL

- 10.3.1 INCREASING FOCUS ON SOIL BIOLOGY AND ROOT HEALTH ACCELERATING ADOPTION OF FUNGAL BIOFERTILIZERS

- 10.4 CYANOBACTERIAL/ALGAL

- 10.4.1 RISING DEMAND FOR SUSTAINABLE SOIL ENRICHMENT DRIVING ADOPTION OF CYANOBACTERIAL AND ALGAL BIOFERTILIZERS

- 10.5 CONSORTIUM/MIXED

- 10.5.1 MULTIFUNCTIONAL NUTRIENT MANAGEMENT DRIVING DEMAND FOR CONSORTIUM-BASED BIOFERTILIZERS

11 BIOFERTILIZERS MARKET, BY MODE OF APPLICATION

- 11.1 INTRODUCTION

- 11.2 SOIL TREATMENT

- 11.2.1 INCREASING FOCUS ON SOIL HEALTH RESTORATION DRIVING ADOPTION OF SOIL TREATMENT BIOFERTILIZERS

- 11.3 SEED TREATMENT

- 11.3.1 RISING ADOPTION OF PRECISION NUTRIENT DELIVERY SUPPORTING GROWTH OF SEED TREATMENT BIOFERTILIZERS

- 11.4 OTHER MODES OF APPLICATION

12 BIOFERTILIZERS MARKET, BY FORM

- 12.1 INTRODUCTION

- 12.2 LIQUID BIOFERTILIZERS

- 12.2.1 INCREASING ADOPTION OF PRECISION AGRICULTURE DRIVING DEMAND FOR LIQUID BIOFERTILIZERS

- 12.3 CARRIER-BASED BIOFERTILIZERS

- 12.3.1 COST-EFFECTIVE NUTRIENT MANAGEMENT SOLUTIONS SUSTAINING DEMAND FOR CARRIER-BASED BIOFERTILIZERS

13 BIOFERTILIZERS MARKET, BY CROP TYPE

- 13.1 INTRODUCTION

- 13.2 CEREALS & GRAINS

- 13.2.1 RISING DEMAND FOR HIGH-YIELD FIELD CROPS DRIVING BIOFERTILIZER ADOPTION IN CEREALS AND GRAINS

- 13.3 PULSES & OILSEEDS

- 13.3.1 EXPANDING PROTEIN AND EDIBLE OIL DEMAND ACCELERATING BIOFERTILIZER USAGE IN PULSES AND OILSEEDS

- 13.4 FRUIT & VEGETABLES

- 13.4.1 INCREASING DEMAND FOR HIGH QUALITY HORTICULTURE PRODUCE DRIVING BIOFERTILIZER ADOPTION IN FRUITS AND VEGETABLES

- 13.5 OTHER CROP TYPES

14 BIOFERTILIZERS MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 US

- 14.2.1.1 Expansion of precision agriculture and biological soil health programs strengthening biofertilizer adoption in US

- 14.2.2 CANADA

- 14.2.2.1 Regenerative farming expansion and pulse crop cultivation accelerating biofertilizer penetration across Canada

- 14.2.3 MEXICO

- 14.2.3.1 Expansion of export-oriented horticulture and sustainable soil management practices driving biofertilizer demand in Mexico

- 14.2.1 US

- 14.3 EUROPE

- 14.3.1 GERMANY

- 14.3.1.1 Sustainable farming policies and precision biological nutrient technologies accelerating biofertilizer adoption in Germany

- 14.3.2 FRANCE

- 14.3.2.1 Expansion of regenerative viticulture and sustainable crop nutrition programs supporting biofertilizer growth in France

- 14.3.3 UK

- 14.3.3.1 Regenerative agriculture initiatives and soil health restoration programs expanding biofertilizer adoption in the United Kingdom

- 14.3.4 ITALY

- 14.3.4.1 Expansion of organic farming and high-value horticulture cultivation driving biofertilizer demand in Italy

- 14.3.5 SPAIN

- 14.3.5.1 Expansion of greenhouse agriculture and water-efficient farming practices accelerating biofertilizer adoption in Spain

- 14.3.6 REST OF EUROPE

- 14.3.1 GERMANY

- 14.4 ASIA PACIFIC

- 14.4.1 CHINA

- 14.4.1.1 Government-led fertilizer reduction policies and large-scale soil restoration programs driving biofertilizer expansion in China

- 14.4.2 INDIA

- 14.4.2.1 Rising government support for sustainable farming and soil health management accelerating biofertilizer adoption in India

- 14.4.3 JAPAN

- 14.4.3.1 Precision agriculture integration and high-value horticulture production supporting biofertilizer commercialization in Japan

- 14.4.4 AUSTRALIA & NEW ZEALAND

- 14.4.4.1 Regulation-driven market structure supported by high food standards and selective personal care demand

- 14.4.5 REST OF ASIA PACIFIC

- 14.4.1 CHINA

- 14.5 SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.5.1.1 Rising adoption of biological nitrogen fixation and regenerative agriculture practices strengthening Brazil's biofertilizers market growths

- 14.5.2 ARGENTINA

- 14.5.2.1 Sustainable soybean cultivation and precision nutrient management supporting biofertilizer adoption in Argentina

- 14.5.3 REST OF SOUTH AMERICA

- 14.5.1 BRAZIL

- 14.6 REST OF THE WORLD (ROW)

- 14.6.1 AFRICA

- 14.6.1.1 Soil rehabilitation programs and limited access to synthetic fertilizers accelerating biofertilizer adoption across Africa

- 14.6.2 MIDDLE EAST

- 14.6.2.1 Water-efficient agriculture and controlled environment farming expanding biofertilizer utilization across the Middle East

- 14.6.1 AFRICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER COMPETITIVE STRATEGIES/RIGHT TO WIN

- 15.3 REVENUE ANALYSIS, 2020-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.5 PRODUCT COMPARISON

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company footprint

- 15.6.5.2 Type footprint

- 15.6.5.3 Crop type footprint

- 15.6.5.4 Application footprint

- 15.6.5.5 Form footprint

- 15.7 COMPANY VALUATION AND FINANCIAL METRICS

- 15.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.8.1 PROGRESSIVE COMPANIES

- 15.8.2 RESPONSIVE COMPANIES

- 15.8.3 DYNAMIC COMPANIES

- 15.8.4 STARTING BLOCKS

- 15.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.8.5.1 Detailed list of key startups/SMEs

- 15.8.5.2 Competitive benchmarking of key startups/SMEs

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES

- 15.9.2 DEALS

- 15.9.3 EXPANSIONS

16 COMPANY PROFILES

- 16.1 KEY PLAYERS

- 16.1.1 NOVOZYMES A/S

- 16.1.1.1 Business overview

- 16.1.1.2 Products offered

- 16.1.1.3 Recent developments

- 16.1.1.3.1 Product launches

- 16.1.1.3.2 Deals

- 16.1.1.4 MnM view

- 16.1.1.4.1 Right to win

- 16.1.1.4.2 Strategic choices

- 16.1.1.4.3 Weaknesses and competitive threats

- 16.1.2 UPL

- 16.1.2.1 Business overview

- 16.1.2.2 Products offered

- 16.1.2.3 Recent developments

- 16.1.2.3.1 Deals

- 16.1.2.3.2 Deals

- 16.1.2.4 MnM view

- 16.1.2.4.1 Right to win

- 16.1.2.4.2 Strategic choices

- 16.1.2.4.3 Weaknesses and competitive threats

- 16.1.3 SYNGENTA

- 16.1.3.1 Business overview

- 16.1.3.2 Products offered

- 16.1.3.3 Recent developments

- 16.1.3.3.1 Product launches

- 16.1.3.3.2 Deals

- 16.1.3.3.3 Expansions

- 16.1.3.4 MnM view

- 16.1.3.4.1 Right to win

- 16.1.3.4.2 Strategic choices

- 16.1.3.4.3 Weaknesses and competitive threats

- 16.1.4 T. STANES AND COMPANY LIMITED

- 16.1.4.1 Business overview

- 16.1.4.2 Products offered

- 16.1.4.3 Recent developments

- 16.1.4.3.1 Product launches

- 16.1.4.4 MnM view

- 16.1.4.4.1 Key strengths

- 16.1.4.4.2 Strategic choices

- 16.1.4.4.3 Weaknesses and competitive threats

- 16.1.5 LALLEMAND INC.

- 16.1.5.1 Business overview

- 16.1.5.2 Products offered

- 16.1.5.3 Recent developments

- 16.1.5.3.1 Product launches

- 16.1.5.4 MnM view

- 16.1.5.4.1 Right to win

- 16.1.5.4.2 Strategic choices

- 16.1.5.4.3 Weaknesses and competitive threats

- 16.1.6 RIZOBACTER ARGENTINA S.A.

- 16.1.6.1 Business overview

- 16.1.6.2 Products offered

- 16.1.6.3 Recent developments

- 16.1.6.3.1 Product launches

- 16.1.6.3.2 Deals

- 16.1.6.3.3 Expansions

- 16.1.6.4 MnM view

- 16.1.7 GUJARAT STATE FERTILIZERS & CHEMICALS LIMITED

- 16.1.7.1 Business overview

- 16.1.7.2 Products offered

- 16.1.7.3 MnM view

- 16.1.8 MADRAS FERTILIZERS LIMITED

- 16.1.8.1 Business overview

- 16.1.8.2 Products offered

- 16.1.8.3 MnM view

- 16.1.9 IPL BIOLOGICALS

- 16.1.9.1 Business overview

- 16.1.9.2 Products offered

- 16.1.9.3 Recent developments

- 16.1.9.3.1 Product launches

- 16.1.9.3.2 Expansion

- 16.1.9.4 MnM view

- 16.1.10 KOPPERT

- 16.1.10.1 Business overview

- 16.1.10.2 Products offered

- 16.1.10.3 MnM view

- 16.1.11 CORTEVA AGRISCIENCE

- 16.1.11.1 Business overview

- 16.1.11.2 Products offered

- 16.1.11.3 Recent developments

- 16.1.11.3.1 Product launches

- 16.1.11.3.2 Deals

- 16.1.11.4 MnM view

- 16.1.12 KAN BIOSYS

- 16.1.12.1 Business overview

- 16.1.12.2 Products offered

- 16.1.12.3 Recent developments

- 16.1.12.3.1 Product launches

- 16.1.12.3.2 Deals

- 16.1.12.3.3 Expansions

- 16.1.12.4 MnM view

- 16.1.13 MAPLETON AGRI BIOTECH PT LTD

- 16.1.13.1 Business overview

- 16.1.13.2 Products offered

- 16.1.13.3 MnM view

- 16.1.14 SEIPASA

- 16.1.14.1 Business overview

- 16.1.14.2 Products offered

- 16.1.14.3 Recent developments

- 16.1.14.3.1 Product launches

- 16.1.14.3.2 Deals

- 16.1.14.3.3 Expansions

- 16.1.14.4 MnM view

- 16.1.15 AGRILIFE

- 16.1.15.1 Business overview

- 16.1.15.2 Products offered

- 16.1.15.3 Recent developments

- 16.1.15.3.1 Expansions

- 16.1.15.4 MnM view

- 16.1.1 NOVOZYMES A/S

- 16.2 OTHER PLAYERS

- 16.2.1 MANIDHARMA BIOTECH

- 16.2.1.1 Business overview

- 16.2.1.2 Products offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Product launches

- 16.2.1.4 MnM view

- 16.2.2 BIOMAX NATURALS

- 16.2.2.1 Business overview

- 16.2.2.2 Products offered

- 16.2.2.3 MnM view

- 16.2.3 JAIPUR BIO FERTILIZERS

- 16.2.3.1 Business overview

- 16.2.3.2 Products offered

- 16.2.3.3 MnM view

- 16.2.4 BIOCONSORTIA

- 16.2.4.1 Business overview

- 16.2.4.2 Products offered

- 16.2.4.3 MnM view

- 16.2.5 AUMGENE BIOSCIENCES PVT. LTD.

- 16.2.5.1 Business overview

- 16.2.5.2 Products offered

- 16.2.5.3 MnM view

- 16.2.6 AMERICAN VANGUARD CORPORATION

- 16.2.7 CRIYAGEN

- 16.2.8 LKB BIO FERTILIZER

- 16.2.9 VARSHA BIOFERTILIZER & TECHNOLOGY INDIA PVT. LTD.

- 16.2.10 NUTRA MAX LABORATORIES

- 16.2.1 MANIDHARMA BIOTECH

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.1.1 List of major secondary sources

- 17.1.1.2 Key data from secondary sources

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Key data from primary sources

- 17.1.2.2 Key industry insights

- 17.1.2.3 Breakdown of primaries

- 17.1.1 SECONDARY DATA

- 17.2 MARKET SIZE ESTIMATION

- 17.2.1 BOTTOM-UP APPROACH

- 17.2.2 TOP-DOWN APPROACH

- 17.2.2.1 Approach to estimate market size using top-down analysis

- 17.3 DATA TRIANGULATION

- 17.4 RESEARCH ASSUMPTIONS

- 17.5 RESEARCH LIMITATIONS AND RISK ASSESSMENT

18 ADJACENT AND RELATED MARKETS

- 18.1 INTRODUCTION

- 18.2 LIMITATIONS

- 18.3 AGRICULTURAL BIOLOGICALS MARKET

- 18.3.1 MARKET DEFINITION

- 18.3.2 MARKET OVERVIEW

- 18.4 INOCULANTS MARKET

- 18.4.1 MARKET DEFINITION

- 18.4.2 MARKET OVERVIEW

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 AVAILABLE CUSTOMIZATION

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS