|

시장보고서

상품코드

2061162

매니지드 서비스 시장 예측(-2031년) : 서비스 유형별, 배포 유형별, 조직 규모별, 업계별, 지역별Managed Services Market by Service Type (Managed IT Infrastructure & Data Center Service, Managed Network Service, Managed Security Service, Managed Communication & Collaboration Service, Managed Mobility, Managed Information) - Global Forecast to 2031 |

||||||

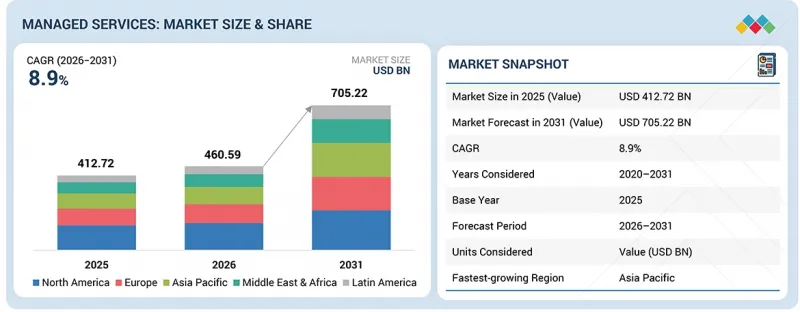

매니지드 서비스 시장 규모는 2031년까지 7,052억 2,000만 달러에 달하며, CAGR은 8.9%에 달할 것으로 예측됩니다.

시장의 성장은 하이브리드 IT 환경의 복잡화, 사이버 보안 위협의 증가, 기업내 클라우드 배포 확대, 그리고 확장 가능하고 비용 효율적인 IT 운영의 필요성에 의해 주도되고 있습니다. 매니지드 서비스를 통해 조직은 IT 관리를 외부에 위탁함으로써 인프라 가용성을 높이고, 네트워크 성능을 최적화하며, 사이버 보안 복원력을 강화하고, 운영 부담을 줄일 수 있습니다. 기업은 디지털 전환 노력을 지원하고, 분산된 운영 환경 전반에 걸쳐 사업 연속성을 유지하기 위해 매니지드 인프라, 매니지드 보안, 매니지드 네트워크 및 매니지드 커뮤니케이션 서비스의 도입을 점점 더 확대하고 있습니다. AI를 활용한 모니터링, 예측 분석, 자동화된 사고 대응, 클라우드 오케스트레이션 등의 고급 기능을 통해 서비스 효율성과 운영 가시성이 한층 더 향상되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 서비스 유형별, 배포 유형별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

원격 근무 지원, 멀티클라우드 관리, 규제 준수 및 지속적인 인프라 모니터링에 대한 수요가 증가함에 따라 업종을 불문하고 매니지드 서비스 도입이 가속화되고 있습니다. 또한 특히 북미 및 아시아태평양에서 클라우드 기반 관리형 플랫폼, 보안 운영 센터(SOC), 그리고 자동화 중심의 서비스 제공 모델에 대한 투자가 증가하고 있으며, 이러한 요인들이 관리형 서비스 시장의 성장에 크게 기여하고 있습니다.

서비스 유형별로는 예측 기간 중 매니지드 보안 부문이 가장 높은 성장률을 보일 것으로 예상됩니다.

2025년 4월, FBI의 인터넷 범죄 보고서에 따르면 2024년 사이버 범죄 관련 피해액이 160억 달러를 넘어섰으며, 이는 전 세계 기업을 표적으로 한 랜섬웨어, 피싱, 비즈니스 이메일 사기 및 인증 정보 탈취 공격의 급증세를 반영한 것입니다. PCI DSS, HIPAA, GDPR, SOX, NIS2와 관련된 규제 요건의 강화 역시 지속적인 규정 준수 모니터링, 감사 보고서, 관리형 SIEM 및 ID 거버넌스 서비스에 대한 기업의 수요를 가속화하고 있습니다. 하이브리드 클라우드, 원격 근무 인프라, 연결된 엔드포인트, AI 지원 애플리케이션의 도입 확대는 기업의 관리형 보안 운영 및 엔드포인트 보호 서비스에 대한 의존도를 더욱 높이고 있습니다. 조직들은 사이버 보안의 효율성과 운영 확장성을 높이기 위해 AI를 활용한 위협 분석, 제로 트러스트 보안 프레임워크, SASE 아키텍처, 그리고 자동화된 사고 대응 플랫폼의 도입을 점점 더 확대하고 있습니다. 관리형 보안 서비스 제공업체들은 진화하는 기업의 보안 요구 사항에 대응하기 위해 클라우드 보안 모니터링, 관리형 SOC 운영 및 위협 인텔리전스 기능을 확대하고 있습니다. 디지털 전환에 대한 투자 증가와 주요 산업 전반에 걸친 사이버 위험 노출 확대는 전 세계에서 관리형 보안 서비스에 강력한 장기 성장 기회를 지속적으로 창출하고 있습니다.

“구축 유형별로는 온프레미스 부문이 시장에서 가장 큰 점유율을 차지하고 있습니다. '

온프레미스형 매니지드 서비스란, 고객이 관리하는 데이터센터나 사설 시설 내에 구축된 기업 소유의 IT 인프라에 대한 모니터링, 관리, 유지보수, 보안, 백업 및 운영 지원을 아웃소싱하는 것을 의미합니다. 이러한 서비스는 서버, 스토리지, 데이터베이스, 사설 네트워크, 보안 어플라이언스, 백업 시스템은 물론, 정교한 제어, 데이터 상주성, 맞춤 설정, 규정 준수 보증이 필요한 미션 크리티컬 애플리케이션을 포괄합니다. 엄격한 규제 요건, 기밀성이 높은 워크로드, 레거시 인프라에 대한 의존도, 그리고 저지연 운영 요구 사항으로 인해 BFSI(은행·금융·보험), 의료, 정부, 통신, 에너지 등 각 부문에서 온프레미스형 매니지드 서비스에 대한 수요는 계속해서 견고할 것으로 예상됩니다. 사이버 보안 리스크의 증가가 온프레미스형 매니지드 서비스의 도입을 촉진할 것으로 예상됩니다. 예를 들어 2025년 4월, FBI는 2024년 사이버 범죄로 인한 피해액이 160억 달러를 넘어 2023년 대비 33% 증가했다고 보고했습니다. 이러한 증가에 따라 사내 IT 환경 내의 인프라 모니터링, 백업 관리, 재해 복구, 엔드포인트 보호, SIEM 관리 및 규정 준수 보고에 대한 수요가 높아지고 있습니다.

“지역별로는 2026년에 북미가 가장 큰 시장 점유율을 차지할 것으로 예측됩니다. ” '

북미는 대규모 기업 기반, 클라우드의 고도화된 도입, 그리고 아웃소싱된 IT 관리 및 보안 운영에 대한 수요를 가속화하고 있는 점점 더 복잡해지는 규제 및 사이버 보안 환경에 힘입어 매니지드 서비스 제공업체에게 전략적으로 가장 중요한 지역 중 하나가 되고 있습니다. 은행, 금융 서비스, 의료, 제조업 등의 기업은 IT의 복잡성에 직면함에 따라 기존의 사내 IT 모델에서 클라우드 인프라 관리, 관리형 탐지 및 대응, 최종사용자 컴퓨팅 서비스에 이르는 포괄적인 관리형 서비스 계약으로 적극적으로 전환하고 있습니다. 이러한 전환은 규정 준수 압박이 커짐에 따라 더욱 가속화되고 있습니다. 조직은 의료보험 상호운용성 및 책임에 관한 법률(HIPAA), 사이버 보안 성숙도 모델 인증(CMMC), 그리고 주 차원의 개인정보 보호법 등의 프레임워크 하에서 더욱 엄격해진 데이터 보호 요건에 대응해야 할 필요성에 직면해 있으며, 내장된 규정 준수 기능과 감사 대응이 가능한 보고 기능을 갖춘 관리형 서비스 제공업체에 대한 의존도를 높이고 있습니다. 이러한 추세를 지원하듯, 미국 사이버보안·인프라보안청(CISA)은 '2024년 사이버보안 연간 보고서'에서 연방 정부 및 중요 인프라 부문의 사이버보안 관련 아웃소싱 계약이 2022년 대비 40% 이상 증가했다고 보고했습니다. 이는 규제 집행 강화와 위협의 심화가 지역 전체에서 지속적인 관리형 서비스 수요로 이어지고 있음을 여실히 보여줍니다.

매니지드 서비스 시장의 주요 공급업체로는 IBM(미국), Accenture(아일랜드), Microsoft(미국), Cisco(미국), Fujitsu(일본), 구글(미국), TCS(인도), 인포시스(인도), 캡제미니(프랑스), 코그니잔트(미국) 등이 포함됩니다.

본 조사에서는 매니지드 서비스 시장의 주요 업체에 대한 상세한 경쟁 분석, 각 기업의 프로필, 최근 동향 및 주요 시장 전략을 포괄적으로 다루고 있습니다.

조사 범위

이 보고서에서는 매니지드 서비스 시장을 세분화하여 서비스 유형(매니지드 보안 서비스, 매니지드 네트워크 서비스, 매니지드 IT 인프라·데이터센터 서비스, 매니지드 커뮤니케이션·협업 서비스, 매니지드 모빌리티 서비스, 매니지드 정보 서비스), 조직 규모(대기업, 중소기업), 구축 유형(온프레미스, 클라우드), 조직 규모(대기업, 중소기업), 산업별(BFSI, 소매·소비재, 제조, 기술, 통신, 정부·공공 부문, 에너지·유틸리티, 헬스케어·생명과학, 미디어·엔터테인먼트, 기타 업종) 및 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)을 기준으로 시장을 세분화하고, 시장 규모를 예측하고 있습니다.

또한 본 조사에서는 시장의 주요 업체에 대한 상세한 경쟁 분석, 각 기업의 프로필, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 주요 시장 전략에 대해서도 다루고 있습니다.

이 보고서를 구매할 때의 주요 이점

이 보고서는 매니지드 서비스 시장 전체 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공함으로써, 시장 선도 기업 및 신규 진입 기업 여러분을 지원합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 유리한 위치에 놓으며, 적절한 시장 진입 전략을 수립하는 데 필요한 귀중한 인사이트를 얻는 데 도움이 됩니다. 또한 이 보고서는 이해관계자들이 시장 동향을 파악하고, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 제공하는 데 목적이 있습니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(성과 기반 관리형 서비스를 실현하는 AI-Ops 주도 자동화, 클라우드 아웃소싱을 가속화하는 하이퍼스케일러의 공동 판매 생태계, 사이버 범죄의 복잡화, SaaS 및 클라우드 네이티브 애플리케이션의 성장) , 제약 요인(클라우드, 사이버 보안, AI 운영 분야의 숙련된 인력 부족, 기업내 가시성 및 제어의 한계에 대한 우려), 기회(AI 인프라 및 GenAI 운영 서비스의 확대, FinOps 및 클라우드 비용 최적화 서비스의 확대, 엣지 및 분산형 인프라 관리 서비스의 확대, 제로 트러스트 및 MDR을 갖춘 매니지드 보안 서비스의 확대), 그리고 과제(비용 효율성과 SLA 성과에 대한 기대 간의 균형, 멀티클라우드 통합 및 상호 운용성의 복잡성)

- 제품 개발/혁신: 매니지드 서비스 시장의 향후 기술, 연구개발 활동 및 제품·서비스 출시에 대한 상세 인사이트.

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보. 이 보고서에서는 다양한 지역에 걸친 매니지드 서비스 시장을 분석하고 있습니다.

- 시장의 다양화: 매니지드 서비스 시장의 제품 및 서비스, 미개발 지역, 최근 동향, 그리고 투자에 관한 포괄적인 정보.

- 경쟁사 분석: 매니지드 서비스 시장에서 IBM(미국), Microsoft(미국), Accenture(아일랜드), Fujitsu(일본), Cisco(미국) 등 주요 기업의 시장 점유율, 성장 전략 및 서비스 제공에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 고객 상황과 구매 행동

제7장 기술, 특허, 디지털 기술, AI의 도입에 의한 전략적 파괴

제8장 규제 상황

제9장 매니지드 서비스 시장(서비스 유형별)

제10장 매니지드 서비스 시장(매니지드 보안 서비스별)

제11장 매니지드 서비스 시장(매니지드 네트워크 서비스별)

제12장 매니지드 서비스 시장(매니지드 IT 인프라·데이터센터 서비스별)

제13장 매니지드 서비스 시장(매니지드 커뮤니케이션·협업 서비스별)

제14장 매니지드 서비스 시장(매니지드 모빌리티 서비스별)

제15장 매니지드 서비스 시장(매니지드 정보 서비스별)

제16장 매니지드 서비스 시장(배포 유형별)

제17장 매니지드 서비스 시장(조직 규모별)

제18장 매니지드 서비스 시장(업계별)

제19장 매니지드 서비스 시장(지역별)

제20장 경쟁 구도

제21장 기업 개요

제22장 조사 방법

제23장 부록

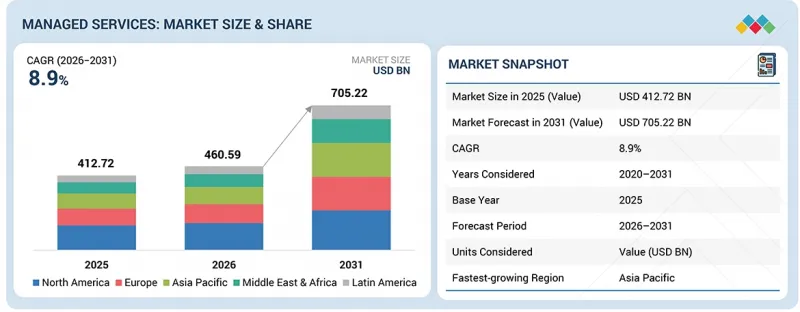

KSA 26.06.25The managed services market is projected to reach USD 705.22 billion by 2031, registering a compound annual growth rate (CAGR) of 8.9%. Market growth is driven by the increasing complexity of hybrid IT environments, rising cybersecurity threats, growing enterprise cloud adoption, and the need for scalable, cost-efficient IT operations. Managed services enable organizations to improve infrastructure availability, optimize network performance, strengthen cybersecurity resilience, and reduce operational burden through outsourced IT management. Enterprises are increasingly adopting managed infrastructure, managed security, managed network, and managed communication services to support digital transformation initiatives and maintain business continuity across distributed operating environments. Advanced capabilities such as AI-driven monitoring, predictive analytics, automated incident response, and cloud orchestration are further enhancing service efficiency and operational visibility.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) |

| Segments | Service Type, Deployment Type, Organization Size, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Rising demand for remote workforce support, multi-cloud management, regulatory compliance, and continuous infrastructure monitoring is accelerating managed service adoption across industries. In addition, increasing investments in cloud-based managed platforms, security operations centers (SOCs), and automation-led service delivery models, particularly across North America and the Asia Pacific, are contributing significantly to the growth of the managed services market.

By service type, the managed security segment is expected to grow at the highest rate during the forecast period.

In April 2025, the FBI Internet Crime Report highlighted cybercrime-related losses exceeding USD 16 billion during 2024, reflecting a sharp increase in ransomware, phishing, business email compromise, and credential theft attacks targeting enterprises globally. Growing regulatory requirements related to PCI DSS, HIPAA, GDPR, SOX, and NIS2 are also accelerating enterprise demand for continuous compliance monitoring, audit reporting, managed SIEM, and identity governance services. The increasing adoption of hybrid cloud, remote workforce infrastructure, connected endpoints, and AI-enabled applications is further increasing enterprise reliance on managed security operations and endpoint protection services. Organizations are increasingly adopting AI-enabled threat analytics, zero-trust security frameworks, SASE architecture, and automated incident response platforms to improve cybersecurity efficiency and operational scalability. Managed security service providers are expanding cloud security monitoring, managed SOC operations, and threat intelligence capabilities to address evolving enterprise security requirements. Rising digital transformation investments and increasing cyber risk exposure across critical industries continue to create strong long-term growth opportunities for managed security services globally.

"By deployment type, the on-premises segment holds the largest market share in the market."

On-premises managed services refer to outsourced monitoring, management, maintenance, security, backup, and operational support for enterprise-owned IT infrastructure deployed within customer-controlled data centers or private facilities. These services cover servers, storage, databases, private networks, security appliances, backup systems, and mission-critical applications that require higher control, data residency, customization, and compliance assurance. Demand for on-premises managed services is expected to remain strong across BFSI, healthcare, government, telecom, and energy sectors due to strict regulatory requirements, sensitive workloads, legacy infrastructure dependence, and low-latency operational needs. Increasing cybersecurity exposure is expected to drive the adoption of on-premises managed services. For instance, in April 2025, the FBI reported that cybercrime losses exceeded USD 16 billion in 2024, a 33% increase from 2023. This rise is increasing demand for managed infrastructure monitoring, managed backup, disaster recovery, endpoint protection, SIEM management, and compliance reporting within private IT environments.

"By region, North America is projected to hold the largest market share in 2026."

North America represents one of the most strategically significant regions for managed services providers, driven by its large enterprise base, advanced cloud adoption, and an increasingly complex regulatory and cybersecurity environment that is accelerating demand for outsourced IT management and security operations. As enterprises across banking, financial services, healthcare, and manufacturing grapple with rising IT complexity, they are actively transitioning from traditional in-house IT models toward comprehensive managed services engagements spanning cloud infrastructure management, managed detection and response, and end-user computing services. This shift is further reinforced by mounting compliance pressures, as organizations navigate stricter data protection mandates under frameworks such as the Health Insurance Portability and Accountability Act (HIPAA), Cybersecurity Maturity Model Certification (CMMC), and state-level privacy laws, pushing them to rely on managed services providers with built-in compliance capabilities and audit-ready reporting. Supporting this momentum, the US Cybersecurity and Infrastructure Security Agency (CISA) reported in its 2024 Cybersecurity Year in Review that cybersecurity-related outsourcing engagements across federal and critical infrastructure sectors increased by over 40% compared to 2022 levels, directly reflecting how regulatory enforcement and threat escalation are translating into sustained managed services demand across the region.

Breakdown of Primaries

The study draws insights from a range of industry experts, including component suppliers, Tier 1 companies, and OEMs. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 34%, Tier 2 - 43%, and Tier 3 - 23%

- By Designation: C-level - 50%, Directors - 30%, Others - 20%

- By Region: North America - 25%, Europe - 30%, Asia Pacific - 30%, Middle East & Africa - 10%, Latin America - 5%

Major vendors in the managed services market include IBM (US), Accenture (Ireland), Microsoft (US), Cisco (US), Fujitsu (Japan), Google (US), TCS (India), Infosys (India), Capgemini (France), and Cognizant (US).

The study includes an in-depth competitive analysis of the key players in the managed services market, their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the managed services market and forecasts its size based on service type (managed security services, managed network services, managed IT infrastructure & data center services, managed communication & collaboration services, managed mobility services, managed information services), organization size (large enterprises, SMEs), deployment type (on-premises, cloud), organization size (large enterprises, SMEs), vertical (BFSI, retail & consumer goods, manufacturing, technology, telecommunications, government & public sector, energy & utilities, healthcare & life sciences, media & entertainment, other verticals), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The study also includes an in-depth competitive analysis of the market's key players, their company profiles, key observations related to product and business offerings, recent developments, and key market strategies.

Key Benefits of Buying the Report

The report will help market leaders/new entrants with information on the closest approximations of revenue numbers for the overall managed services market and its subsegments. This report will help stakeholders understand the competitive landscape and gain valuable insights to better position their businesses and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of critical drivers (AI-Ops-driven automation enabling outcome-based managed services, Hyperscaler co-sell ecosystems accelerating cloud outsourcing, Rising cybercrime complexities, Growth of SaaS and cloud-native applications), restraints (Shortage of skilled workforce in cloud, cybersecurity, and AI operations, Limited visibility and control concerns among enterprises), opportunities (AI infrastructure and GenAI operations services expansion, FinOps and cloud cost optimization services expansion, Edge and distributed infrastructure management services expansion, Managed security services expansion with zero-trust and MDR), and challenges (Balancing cost efficiency with SLA performance expectations, Multi-cloud integration and interoperability complexity)

- Product Development/Innovation: Detailed insights on upcoming technologies, research development activities, and product & service launches in the managed services market.

- Market Development: Comprehensive information about lucrative markets - the report analyzes the managed services market across varied regions.

- Market Diversification: Exhaustive information about products and services, untapped geographies, recent developments, and investments in the managed services market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like IBM (US), Microsoft (US), Accenture (Ireland), Fujitsu (Japan), and Cisco (US) in the managed services market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN MANAGED SERVICES MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MANAGED SERVICES MARKET

- 3.2 MANAGED SERVICES MARKET, BY SERVICE TYPE

- 3.3 MANAGED SERVICES MARKET, BY DEPLOYMENT TYPE

- 3.4 MANAGED SERVICES MARKET, BY VERTICAL

- 3.5 MANAGED SERVICES MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 AI-Ops-driven automation enabling outcome-based managed services

- 4.2.1.2 Hyperscaler co-sell ecosystems accelerating cloud outsourcing

- 4.2.1.3 Rising cybercrime complexities

- 4.2.1.4 Growth of SaaS and cloud-native applications

- 4.2.2 RESTRAINTS

- 4.2.2.1 Shortage of skilled workforce in cloud, cybersecurity, and AI operations

- 4.2.2.2 Limited visibility and control concerns among enterprises

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 AI infrastructure and GenAI operations services expansion

- 4.2.3.2 FinOps and cloud cost optimization services expansion

- 4.2.3.3 Edge and distributed infrastructure management services expansion

- 4.2.3.4 Managed security services expansion with zero-trust and MDR

- 4.2.4 CHALLENGES

- 4.2.4.1 Balancing cost efficiency with SLA performance expectations

- 4.2.4.2 Multi-cloud integration and interoperability complexity

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN MANAGED SERVICES MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 EMERGING BUSINESS MODELS AND ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.5.1.1 Managed Service Business Models

- 4.5.2 ECOSYSTEM SHIFTS

- 4.5.1 EMERGING BUSINESS MODELS

- 4.6 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

- 4.6.1 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC INDICATORS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS & FORECASTS

- 5.2.3 TRENDS IN GLOBAL NETWORK MANAGED SERVICES MARKET

- 5.2.4 TRENDS IN GLOBAL CLOUD SERVICES MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF VENDORS, BY REGION, 2025

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia Pacific

- 5.5.1.4 Middle East & Africa

- 5.5.1.5 Latin America

- 5.5.2 PRICING LANDSCAPE FOR MANAGED SERVICES, 2025

- 5.5.3 INDICATIVE PRICING TRENDS, BY KEY VENDOR, 2025

- 5.5.1 AVERAGE SELLING PRICE OF VENDORS, BY REGION, 2025

- 5.6 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 IBM AND MERCK DELIVERED AI-DRIVEN MANAGED IT SERVICES FOR PHARMACEUTICAL OPERATIONS RELIABILITY

- 5.9.2 ACCENTURE AND VODAFONE TRANSFORMED NETWORK OPERATIONS THROUGH AI-ENABLED MANAGED SERVICES

- 5.9.3 TCS DELIVERED FULLY MANAGED IT INFRASTRUCTURE SERVICES FOR LEADING ISRAELI BANK

- 5.9.4 DXC TECHNOLOGY AND SCG ACHIEVED CLOUD-FIRST MANAGED TRANSFORMATION ON GOOGLE CLOUD

- 5.9.5 CAPGEMINI AND ENI DELIVERED END-TO-END MANAGED IT INFRASTRUCTURE FOR ENERGY TRANSITION

- 5.10 IMPACT OF 2025 US TARIFF - MANAGED SERVICES MARKET

- 5.10.1 INTRODUCTION

- 5.10.2 KEY TARIFF RATES

- 5.10.3 PRICE IMPACT ANALYSIS

- 5.10.4 IMPACT ON COUNTRY/REGION

- 5.10.4.1 North America

- 5.10.4.2 Europe

- 5.10.4.3 Asia Pacific

- 5.10.5 IMPACT ON VERTICALS

- 5.10.5.1 BFSI

- 5.10.5.2 Telecommunications

- 5.10.5.3 Healthcare & Life Sciences

- 5.10.5.4 Government & Public Sector

6 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 6.1 DECISION-MAKING PROCESS

- 6.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 6.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 6.2.2 BUYING CRITERIA

- 6.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 6.4 UNMET NEEDS IN VARIOUS END-USER INDUSTRIES

- 6.5 MARKET PROFITABILITY

- 6.5.1 REVENUE POTENTIAL

- 6.5.2 COST DYNAMICS

- 6.5.3 MARGIN OPPORTUNITIES IN KEY APPLICATIONS

7 STRATEGIC DISRUPTION THROUGH TECHNOLOGY, PATENTS, DIGITAL, AND AI ADOPTION

- 7.1 TECHNOLOGY ANALYSIS

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.1.1.1 AIOps

- 7.1.1.2 Observability Platforms

- 7.1.1.3 Big Data Analytics

- 7.1.2 COMPLEMENTARY TECHNOLOGIES

- 7.1.2.1 Robotic Process Automation

- 7.1.2.2 Internet of Things

- 7.1.2.3 Edge Computing

- 7.1.3 ADJACENT TECHNOLOGIES

- 7.1.3.1 Zero Trust Architecture

- 7.1.3.2 Software-defined Networking

- 7.1.3.3 Blockchain

- 7.1.1 KEY EMERGING TECHNOLOGIES

- 7.2 TECHNOLOGY/PRODUCT ROADMAP

- 7.2.1 SHORT-TERM (2026-2028) | AI-DRIVEN AUTOMATION & CLOUD-LED SERVICE DELIVERY

- 7.2.1.1 Focus Areas:

- 7.2.1.1.1 Technology Development

- 7.2.1.1.2 Product Innovations

- 7.2.1.1.3 Market Adoption

- 7.2.1.1 Focus Areas:

- 7.2.2 MID-TERM (2028-2031) | AUTONOMOUS OPERATIONS & EDGE-ENABLED MANAGED SERVICES

- 7.2.2.1 Focus Areas:

- 7.2.2.1.1 Technology Development

- 7.2.2.1.2 Product Innovations

- 7.2.2.1.3 Market Adoption

- 7.2.2.1 Focus Areas:

- 7.2.3 LONG-TERM (2031-2035+) | INTELLIGENT DIGITAL OPERATIONS & PLATFORM-CENTRIC MANAGED SERVICES

- 7.2.3.1 Focus Areas:

- 7.2.3.1.1 Technology Development

- 7.2.3.1.2 Product Innovations

- 7.2.3.1.3 Market Adoption

- 7.2.3.1 Focus Areas:

- 7.2.1 SHORT-TERM (2026-2028) | AI-DRIVEN AUTOMATION & CLOUD-LED SERVICE DELIVERY

- 7.3 PATENT ANALYSIS

- 7.4 IMPACT OF AI/GENERATIVE AI ON MANAGED SERVICES MARKET

- 7.4.1 TOP USE CASES AND MARKET POTENTIAL

- 7.4.2 BEST PRACTICES IN MANAGED SERVICES

- 7.4.3 CASE STUDY OF AI IMPLEMENTATION IN THE MANAGED SERVICES MARKET

- 7.4.3.1 Accenture and Google Cloud Helped Leading US Financial Institution Deliver Gen AI-powered Managed IT Services at Enterprise Scale

- 7.4.4 CLIENT READINESS TO ADOPT GENERATIVE AI IN THE MANAGED SERVICES MARKET

8 REGULATORY LANDSCAPE

- 8.1 REGULATORY LANDSCAPE

- 8.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 8.1.2 INDUSTRY STANDARDS, BY REGION

- 8.1.2.1 North America

- 8.1.2.2 Europe

- 8.1.2.3 Asia Pacific

- 8.1.2.4 Middle East & South Africa

- 8.1.2.5 Latin America

9 MANAGED SERVICES MARKET, BY SERVICE TYPE

- 9.1 INTRODUCTION

- 9.1.1 SERVICE TYPE: MANAGED SERVICES MARKET DRIVERS

- 9.2 MANAGED SECURITY SERVICES

- 9.2.1 RISING CYBERSECURITY THREATS DRIVE MANAGED SECURITY ADOPTION

- 9.3 MANAGED NETWORK SERVICES

- 9.3.1 RISING NETWORK COMPLEXITY DRIVES MANAGED NETWORK ADOPTION

- 9.4 MANAGED IT INFRASTRUCTURE & DATA CENTER SERVICES

- 9.4.1 RISING CLOUD MODERNIZATION DRIVES MANAGED INFRASTRUCTURE SERVICES ADOPTION

- 9.5 MANAGED COMMUNICATION & COLLABORATION SERVICES

- 9.5.1 RISING HYBRID WORK CULTURE DRIVES MANAGED COMMUNICATION ADOPTION

- 9.6 MANAGED MOBILITY SERVICES

- 9.6.1 RISING ENTERPRISE MOBILITY DRIVES MANAGED MOBILITY ADOPTION

- 9.7 MANAGED INFORMATION SERVICES

- 9.7.1 RISING DATA COMPLEXITY DRIVES MANAGED INFORMATION ADOPTION

10 MANAGED SERVICES MARKET, BY MANAGED SECURITY SERVICE

- 10.1 INTRODUCTION

- 10.1.1 MANAGED SECURITY SERVICES: MANAGED SERVICES MANAGEMENT MARKET DRIVERS

- 10.2 MANAGED IDENTITY AND ACCESS MANAGEMENT

- 10.2.1 MANAGED IAM SERVICES PROTECT ENTERPRISE DIGITAL IDENTITIES ACROSS HYBRID ENVIRONMENTS

- 10.2.2 PRIVILEGED ACCESS CONTROL

- 10.2.3 IDENTITY DIRECTORY AND FEDERATION MANAGEMENT

- 10.2.4 OTHERS

- 10.3 MANAGED FIREWALL

- 10.3.1 MANAGED FIREWALL SERVICES STRENGTHEN NETWORK PERIMETER SECURITY ACROSS ENTERPRISE ENVIRONMENTS

- 10.3.2 FIREWALL PERFORMANCE MONITORING

- 10.3.3 THREAT PREVENTION (IPS/IDS INTEGRATION)

- 10.3.4 OTHERS

- 10.4 MANAGED RISK AND COMPLIANCE MANAGEMENT

- 10.4.1 MANAGED RISK AND COMPLIANCE SERVICES ENABLE CONTINUOUS REGULATORY ADHERENCE ACROSS ENTERPRISES

- 10.4.2 RISK ASSESSMENT AND SCORING

- 10.4.3 AUDIT MANAGEMENT AND REPORTING

- 10.4.4 OTHERS

- 10.5 MANAGED VULNERABILITY MANAGEMENT

- 10.6 MANAGED DETECTION AND RESPONSE

- 10.6.1 MANAGED DETECTION AND RESPONSE SERVICES ACCELERATE THREAT IDENTIFICATION AND CONTAINMENT

- 10.6.2 INCIDENT RESPONSE AND CONTAINMENT

- 10.6.3 INCIDENT TRIAGE AND INVESTIGATION

- 10.6.4 OTHERS

- 10.7 MANAGED SIEM AND LOG MANAGEMENT

- 10.7.1 MANAGED SIEM AND LOG MANAGEMENT SERVICES POWER ENTERPRISE-WIDE SECURITY VISIBILITY

- 10.8 OTHERS

- 10.8.1 EMERGING MANAGED SECURITY SERVICES ADDRESS EVOLVING ENTERPRISE THREAT LANDSCAPES

11 MANAGED SERVICES MARKET, BY MANAGED NETWORK SERVICE

- 11.1 INTRODUCTION

- 11.1.1 MANAGED NETWORK SERVICES: MANAGED SERVICES MARKET DRIVER

- 11.2 MANAGED LAN

- 11.2.1 MANAGED LAN SERVICES DELIVER RELIABLE ENTERPRISE CAMPUS CONNECTIVITY AT SCALE

- 11.3 MANAGED WI-FI

- 11.3.1 MANAGED WI-FI SERVICES ENSURE SECURE AND HIGH-PERFORMANCE WIRELESS CONNECTIVITY

- 11.4 MANAGED IP/VPN

- 11.4.1 MANAGED IP AND VPN SERVICES SECURE ENTERPRISE REMOTE AND BRANCH CONNECTIVITY

- 11.5 MANAGED WAN

- 11.5.1 MANAGED WAN SERVICES OPTIMIZE ENTERPRISE-WIDE AREA NETWORK PERFORMANCE AND RELIABILITY

- 11.6 NETWORK MONITORING

- 11.6.1 MANAGED NETWORK MONITORING SERVICES DELIVER CONTINUOUS VISIBILITY ACROSS ENTERPRISE INFRASTRUCTURE

- 11.7 MANAGED NETWORK FUNCTION VIRTUALIZATION

- 11.7.1 MANAGED NFV SERVICES ACCELERATE SOFTWARE-DEFINED NETWORK FUNCTION DEPLOYMENT AND OPERATIONS

- 11.8 MANAGED NETWORK SECURITY

- 11.8.1 MANAGED NETWORK SECURITY SERVICES PROTECT ENTERPRISE CONNECTIVITY FROM EVOLVING CYBER THREATS

12 MANAGED SERVICES MARKET, BY MANAGED IT INFRASTRUCTURE AND DATA CENTER SERVICE

- 12.1 INTRODUCTION

- 12.1.1 MANAGED IT INFRASTRUCTURE & DATA CENTER SERVICES: MANAGED SERVICES MARKET DRIVERS

- 12.2 STORAGE AND DATABASE MANAGEMENT

- 12.2.1 MANAGED STORAGE AND DATABASE SERVICES ENSURE DATA AVAILABILITY AND INFRASTRUCTURE PERFORMANCE

- 12.2.2 BACKUP AND RECOVERY

- 12.2.3 CAPACITY PLANNING

- 12.2.4 PERFORMANCE MONITORING

- 12.3 SERVER MANAGEMENT

- 12.3.1 MANAGED SERVER SERVICES SUSTAIN ENTERPRISE COMPUTE INFRASTRUCTURE PERFORMANCE AND AVAILABILITY

- 12.3.2 SYSTEM PERFORMANCE MANAGEMENT

- 12.3.3 INSTALLING UPDATES

- 12.3.4 ACCOUNT MANAGEMENT

- 12.4 CLOUD AND DATA CENTER SERVICES

- 12.4.1 MANAGED CLOUD AND DATA CENTER SERVICES POWER ENTERPRISE DIGITAL INFRASTRUCTURE TRANSFORMATION

- 12.4.2 COLOCATION SERVICES

- 12.4.3 DATA CENTER MANAGEMENT

- 12.4.4 CLOUD MIGRATION

- 12.4.5 CLOUD HOSTING

- 12.5 OTHER MANAGED IT INFRASTRUCTURE AND DATA CENTER SERVICES

- 12.5.1 RISING INFRASTRUCTURE COMPLEXITY DRIVES ADOPTION OF SPECIALIZED MANAGED INFRASTRUCTURE SERVICES

13 MANAGED SERVICES MARKET, BY MANAGED COMMUNICATION & COLLABORATION SERVICE

- 13.1 INTRODUCTION

- 13.1.1 MANAGED COMMUNICATION AND COLLABORATION SERVICES: MANAGED SERVICES MARKET DRIVERS

- 13.2 MANAGED VOIP

- 13.2.1 MANAGED VOIP SERVICES DELIVER RELIABLE AND SECURE ENTERPRISE VOICE COMMUNICATIONS

- 13.3 MANAGED UNIFIED COMMUNICATION AS A SERVICE

- 13.3.1 MANAGED UCAAS SERVICES UNIFY ENTERPRISE COMMUNICATION AND COLLABORATION PLATFORMS

- 13.3.2 TELEPHONY

- 13.3.3 UNIFIED MESSAGING

- 13.3.4 VIDEO CONFERENCING

- 13.4 OTHER MANAGED COMMUNICATION AND COLLABORATION

- 13.4.1 RISING DIGITAL WORKPLACE EXPANSION DRIVES ADOPTION OF SPECIALIZED COMMUNICATION MANAGEMENT SERVICES

14 MANAGED SERVICES MARKET, BY MANAGED MOBILITY SERVICE

- 14.1 INTRODUCTION

- 14.1.1 MANAGED MOBILITY SERVICES: MANAGED SERVICES MARKET DRIVERS

- 14.2 MOBILE DEVICE MANAGEMENT

- 14.2.1 MANAGED MOBILE DEVICE MANAGEMENT SERVICES SECURE AND GOVERN ENTERPRISE ENDPOINT FLEETS

- 14.2.2 DEVICE PROVISIONING

- 14.2.3 DEVICE CONFIGURATION

- 14.2.4 APPLICATION MANAGEMENT

- 14.2.5 SECURITY POLICY MANAGEMENT

- 14.3 UNIFIED ENDPOINT MANAGEMENT

- 14.3.1 MANAGED UNIFIED ENDPOINT MANAGEMENT SERVICES GOVERN ALL ENTERPRISE ENDPOINTS FROM A SINGLE PLATFORM

- 14.3.2 CROSS PLATFORM MANAGEMENT

- 14.3.3 APPLICATION DEPLOYMENT

- 14.3.4 COMPLIANCE MONITORING

- 14.3.5 REPORTING AND ANALYTICS

15 MANAGED SERVICES MARKET, BY MANAGED INFORMATION SERVICE

- 15.1 INTRODUCTION

- 15.1.1 MANAGED INFORMATION SERVICES: MANAGED SERVICES MARKET DRIVERS

- 15.2 BUSINESS PROCESS MANAGEMENT

- 15.2.1 MANAGED BUSINESS PROCESS SERVICES OPTIMIZE ENTERPRISE OPERATIONS THROUGH INTELLIGENT OUTSOURCING

- 15.3 MANAGED OSS/BSS

- 15.3.1 MANAGED OSS AND BSS SERVICES ENABLE TELECOM OPERATIONAL AGILITY AND SERVICE INNOVATION

16 MANAGED SERVICES MARKET, BY DEPLOYMENT TYPE

- 16.1 INTRODUCTION

- 16.1.1 DEPLOYMENT TYPE: MANAGED SERVICES MARKET DRIVERS

- 16.2 ON-PREMISES

- 16.2.1 RISING COMPLIANCE AND INFRASTRUCTURE CONTROL REQUIREMENTS DRIVE ON-PREMISES MANAGED SERVICES ADOPTION

- 16.3 CLOUD

- 16.3.1 RISING CLOUD MODERNIZATION INITIATIVES DRIVE CLOUD MANAGED SERVICES ADOPTION

17 MANAGED SERVICES MARKET, BY ORGANIZATION SIZE

- 17.1 INTRODUCTION

- 17.1.1 ORGANIZATION SIZE: MANAGED SERVICES MARKET DRIVERS

- 17.2 LARGE ENTERPRISES

- 17.2.1 RISING INFRASTRUCTURE COMPLEXITY DRIVES MANAGED SERVICES ADOPTION ACROSS LARGE ENTERPRISES

- 17.3 SMES

- 17.3.1 RISING DIGITAL ADOPTION DRIVES MANAGED SERVICES DEMAND ACROSS SMES

18 MANAGED SERVICES MARKET, BY VERTICAL

- 18.1 INTRODUCTION

- 18.1.1 VERTICAL: MANAGED SERVICES MARKET DRIVERS

- 18.2 BFSI

- 18.2.1 RISING CYBERSECURITY THREATS DRIVE MANAGED SERVICES ADOPTION IN BFSI

- 18.3 HEALTHCARE & LIFE SCIENCES

- 18.3.1 RISING DIGITAL HEALTHCARE INFRASTRUCTURE

- 18.4 TELECOMMUNICATIONS

- 18.4.1 RISING NETWORK MODERNIZATION INITIATIVES

- 18.5 RETAIL & CONSUMER GOODS

- 18.5.1 GROWING OMNICHANNEL COMMERCE

- 18.6 GOVERNMENT & PUBLIC SECTOR

- 18.6.1 RISING DIGITAL GOVERNMENT INITIATIVES

- 18.7 ENERGY & UTILITIES

- 18.7.1 RISING SMART GRID AND INFRASTRUCTURE MODERNIZATION

- 18.8 MANUFACTURING

- 18.8.1 RISING SMART FACTORY ADOPTION DRIVES MANAGED SERVICES DEMAND IN MANUFACTURING

- 18.9 MEDIA & ENTERTAINMENT

- 18.9.1 RISING DIGITAL CONTENT CONSUMPTION

- 18.10 TECHNOLOGY (IT & ITES)

- 18.10.1 RISING CLOUD AND AI INFRASTRUCTURE EXPANSION

- 18.11 OTHER VERTICALS

19 MANAGED SERVICES MARKET, BY REGION

- 19.1 INTRODUCTION

- 19.2 NORTH AMERICA

- 19.2.1 US

- 19.2.1.1 Cybersecurity Regulation and Cloud Complexity Fuel US Managed Services

- 19.2.2 CANADA

- 19.2.2.1 Privacy Law Enforcement and Hybrid Cloud Adoption Drive Canada MS Growth

- 19.2.1 US

- 19.3 EUROPE

- 19.3.1 UK

- 19.3.1.1 Cyber Resilience Mandates and Post-Brexit Compliance Shape UK Managed Services Demand

- 19.3.2 GERMANY

- 19.3.2.1 Industrial IT Complexity and Data Sovereignty Norms Drive German MS Adoption

- 19.3.3 FRANCE

- 19.3.3.1 Digital Sovereignty Push and SecNumCloud Framework Shape French Managed Services Market

- 19.3.4 ITALY

- 19.3.4.1 PNRR Digital Investment and NIS2 Compliance Propel Italy's MS Adoption

- 19.3.5 REST OF EUROPE

- 19.3.1 UK

- 19.4 ASIA PACIFIC

- 19.4.1 CHINA

- 19.4.1.1 Data Localization Laws and Industrial Digitalization Drive China MS Demand

- 19.4.2 INDIA

- 19.4.2.1 DPDP Act Compliance and GCC Expansion Strengthen India MS Market

- 19.4.3 JAPAN

- 19.4.3.1 Legacy IT Modernization and Cyber Policy Reform Accelerate Japan MS Adoption

- 19.4.4 AUSTRALIA & NEW ZEALAND

- 19.4.4.1 Cyber Resilience Mandates and Cloud Maturity Anchor ANZ MS Demand

- 19.4.5 SOUTH KOREA

- 19.4.5.1 5G Proliferation and PIPA Enforcement Propel South Korea's MS Growth

- 19.4.6 REST OF ASIA PACIFIC

- 19.4.1 CHINA

- 19.5 MIDDLE EAST & AFRICA

- 19.5.1 GCC COUNTRIES

- 19.5.1.1 Saudi Arabia

- 19.5.1.1.1 Vision 2030 Digital Programs and NCA Mandates Accelerate Saudi MS Adoption

- 19.5.1.2 UAE

- 19.5.1.2.1 Smart City Programs and Cloud Mandates Position UAE as MS Leader

- 19.5.1.3 Other GCC countries

- 19.5.1.1 Saudi Arabia

- 19.5.2 SOUTH AFRICA

- 19.5.2.1 POPIA Compliance and Public Sector Cloud Demand Anchor South Africa MS Growth

- 19.5.3 REST OF MIDDLE EAST & AFRICA

- 19.5.1 GCC COUNTRIES

- 19.6 LATIN AMERICA

- 19.6.1 BRAZIL

- 19.6.1.1 LGPD Enforcement and Cloud Expansion Position Brazil as Regional MS Leader

- 19.6.2 MEXICO

- 19.6.2.1 Nearshore IT Expansion and Data Privacy Regulation Drive Mexico MS Market Growth

- 19.6.3 REST OF LATIN AMERICA

- 19.6.1 BRAZIL

20 COMPETITIVE LANDSCAPE

- 20.1 INTRODUCTION

- 20.2 KEY PLAYERS' STRATEGIES/RIGHT TO WIN

- 20.3 REVENUE ANALYSIS, 2021-2025

- 20.4 MARKET SHARE ANALYSIS, 2025

- 20.4.1 IBM

- 20.4.2 ACCENTURE

- 20.4.3 MICROSOFT

- 20.4.4 FUJITSU

- 20.4.5 CISCO

- 20.4.6 CONCLUSION

- 20.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 20.5.1 STARS

- 20.5.2 EMERGING LEADERS

- 20.5.3 PERVASIVE PLAYERS

- 20.5.4 PARTICIPANTS

- 20.5.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 20.5.5.1 Company footprint

- 20.5.5.2 Region footprint

- 20.5.5.3 Solution type footprint

- 20.5.5.4 Deployment type footprint

- 20.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 20.6.1 PROGRESSIVE COMPANIES

- 20.6.2 RESPONSIVE COMPANIES

- 20.6.3 DYNAMIC COMPANIES

- 20.6.4 STARTING BLOCKS

- 20.6.5 COMPETITIVE BENCHMARKING: STARTUP/SMES, 2025

- 20.6.5.1 Detailed list of key startups/SMEs

- 20.6.5.2 Competitive benchmarking of key startups/SMEs

- 20.7 COMPANY VALUATION AND FINANCIAL METRICS

- 20.7.1 COMPANY VALUATION OF KEY VENDORS

- 20.7.2 FINANCIAL METRICS OF KEY VENDORS

- 20.8 COMPETITIVE SCENARIO

- 20.8.1 PRODUCT LAUNCHES/ENHANCEMENTS

- 20.8.2 DEALS

21 COMPANY PROFILES

- 21.1 INTRODUCTION

- 21.2 MAJOR PLAYERS

- 21.2.1 IBM

- 21.2.1.1 Business overview

- 21.2.1.2 Products/Solutions/Services offered

- 21.2.1.3 Recent developments

- 21.2.1.3.1 Product/Service launches and enhancements

- 21.2.1.3.2 Deals

- 21.2.1.4 MnM view

- 21.2.1.4.1 Right to win

- 21.2.1.4.2 Strategic choices

- 21.2.1.4.3 Weaknesses and competitive threats

- 21.2.2 ACCENTURE

- 21.2.2.1 Business overview

- 21.2.2.2 Products/Solutions/Services offered

- 21.2.2.3 Recent developments

- 21.2.2.3.1 Product/service launches and enhancements

- 21.2.2.3.2 Deals

- 21.2.2.4 MnM view

- 21.2.2.4.1 Right to win

- 21.2.2.4.2 Strategic choices

- 21.2.2.4.3 Weaknesses and competitive threats

- 21.2.3 MICROSOFT

- 21.2.3.1 Business overview

- 21.2.3.2 Products/Solutions/Services offered

- 21.2.3.3 Recent developments

- 21.2.3.3.1 Product/Service launches and enhancements

- 21.2.3.3.2 Deals

- 21.2.3.4 MnM view

- 21.2.3.4.1 Right to win

- 21.2.3.4.2 Strategic choices

- 21.2.3.4.3 Weaknesses and competitive threats

- 21.2.4 CISCO

- 21.2.4.1 Business overview

- 21.2.4.2 Products/Solutions/Services offered

- 21.2.4.3 Recent developments

- 21.2.4.3.1 Product/Service launches and enhancements

- 21.2.4.3.2 Deals

- 21.2.4.4 MnM view

- 21.2.4.4.1 Right to win

- 21.2.4.4.2 Strategic choices

- 21.2.4.4.3 Weaknesses and competitive threats

- 21.2.5 FUJITSU

- 21.2.5.1 Business overview

- 21.2.5.2 Products/Solutions/Services offered

- 21.2.5.3 MnM view

- 21.2.5.3.1 Right to win

- 21.2.5.3.2 Strategic choices

- 21.2.5.3.3 Weaknesses and competitive threats

- 21.2.5.4 Recent developments

- 21.2.5.4.1 Product/Service launches and enhancements

- 21.2.5.4.2 Deals

- 21.2.6 GOOGLE

- 21.2.6.1 Business overview

- 21.2.6.2 Products/Solutions/Services offered

- 21.2.6.3 Recent developments

- 21.2.6.3.1 Product/Service launches and enhancements

- 21.2.6.3.2 Deals

- 21.2.7 TATA CONSULTANCY SERVICES (TCS)

- 21.2.7.1 Business overview

- 21.2.7.2 Products/Solutions/Services offered

- 21.2.7.3 Recent developments

- 21.2.7.3.1 Product/Service launches and enhancements

- 21.2.7.3.2 Deals

- 21.2.8 INFOSYS

- 21.2.8.1 Business overview

- 21.2.8.2 Products/Solutions/Services offered

- 21.2.8.3 Recent developments

- 21.2.8.3.1 Product/Service launches and enhancements

- 21.2.8.3.2 Deals

- 21.2.9 CAPGEMINI

- 21.2.9.1 Business overview

- 21.2.9.2 Products/Solutions/Services offered

- 21.2.9.2.1 Recent developments

- 21.2.9.2.2 Deals

- 21.2.10 COGNIZANT

- 21.2.10.1 Business overview

- 21.2.10.2 Products/Solutions/Services offered

- 21.2.10.3 Recent developments

- 21.2.10.3.1 Product launches

- 21.2.10.3.2 Deals

- 21.2.1 IBM

- 21.3 OTHER PLAYERS

- 21.3.1 NOKIA

- 21.3.2 KYNDRYL

- 21.3.3 HCL TECHNOLOGIES

- 21.3.4 DXC TECHNOLOGY

- 21.3.5 WIPRO

- 21.3.6 VERIZON

- 21.3.7 BT GROUP

- 21.3.8 ERICSSON

- 21.3.9 SOPHOS

- 21.3.10 HUAWEI

- 21.3.11 DELOITTE

- 21.3.12 RACKSPACE TECHNOLOGY

- 21.3.13 FORTRA

- 21.3.14 METTEL

- 21.3.15 HAPPIEST MINDS

- 21.3.16 SECUREKLOUD

- 21.3.17 DATAPRISE

- 21.3.18 AC3

- 21.3.19 INTACT

- 21.3.20 CORSICA TECHNOLOGIES

- 21.3.21 EMPIST

- 21.3.22 1-NET

- 21.3.23 ASCEND TECHNOLOGIES

- 21.3.24 MAGNA5

- 21.3.25 ATERA

- 21.3.26 AUNALYTICS

- 21.3.27 CLOUD SPECIALISTS

- 21.3.28 BAE SYSTEMS

- 21.3.29 7LAYER SOLUTIONS

- 21.3.30 CYBERDUO

- 21.3.31 CORTAVO

- 21.3.32 EXC MANAGED SERVICES

- 21.3.33 ESSENTIAL ENTERPRISE SOLUTIONS

22 RESEARCH METHODOLOGY

- 22.1 RESEARCH APPROACH

- 22.1.1 SECONDARY DATA

- 22.1.1.1 Key data from secondary sources

- 22.1.1.2 Breakup of primary profiles

- 22.1.1.3 Key industry insights

- 22.1.1 SECONDARY DATA

- 22.2 MARKET BREAKUP AND DATA TRIANGULATION

- 22.3 MARKET SIZE ESTIMATION

- 22.4 MARKET FORECAST

- 22.5 RESEARCH ASSUMPTIONS

- 22.6 RESEARCH LIMITATIONS

23 APPENDIX

- 23.1 DISCUSSION GUIDE

- 23.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 23.3 CUSTOMIZATION OPTIONS

- 23.4 RELATED REPORTS

- 23.5 AUTHOR DETAILS