|

시장보고서

상품코드

2070353

교통 관리 시장 : 제공별, 적용 분야별, 최종사용자별, 지역별 - 세계 예측(-2032년)Traffic Management Market by Solution, Areas of Application, End User - Global Forecast to 2032 |

||||||

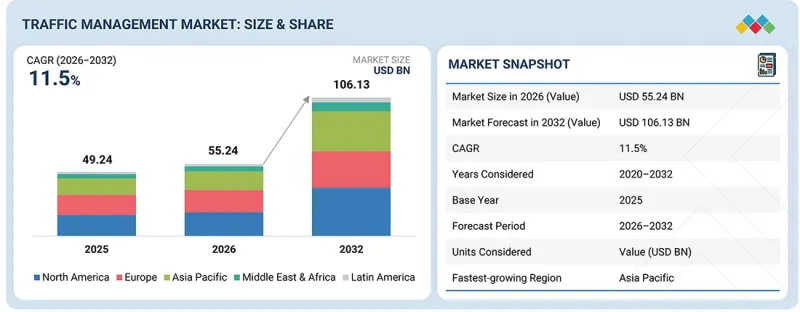

교통 관리 시장 규모는 2026년 552억 4,000만 달러에서 2032년까지 1,061억 3,000만 달러로 성장할 것으로 추정되며, 2026년부터 2032년까지 CAGR은 11.5%를 기록할 전망입니다.

교통 관리 시장은 교통 당국이 이동성 향상, 교통 체증 완화, 그리고 도로망 전반의 운영 효율 제고를 도모하고 있기 때문에 꾸준한 성장을 이루고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2020-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 대상 단위 | 금액(10억 달러) |

| 부문 | 제공별, 적용 분야별, 최종사용자별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

이 시장은 지능형 교통 시스템(ITS), 교통 감시 기술, 그리고 실시간 교통 관리를 가능하게 하는 통합 교통 제어 플랫폼에 대한 투자 확대의 혜택을 받고 있습니다. 최신 교통 관리 솔루션은 교통 감시, 분석, 사고 감지 및 중앙 제어 기능을 결합하여, 운영 담당자가 충분한 정보를 바탕으로 의사결정을 내리고 변화하는 교통 상황에 신속하게 대응할 수 있도록 지원합니다. 증가하는 교통량을 감당하면서 기존 교통 인프라를 최대한 활용할 필요성이 높아짐에 따라, 공공기관들은 도심 및 고속도로 네트워크 전반에 첨단 교통 관리 기술을 도입하도록 권장받고 있습니다. 교통 시스템의 상호연결성과 데이터 기반화가 진전되는 가운데, 교통 관리 솔루션은 더욱 안전하고 효율적이며 탄력적인 모빌리티 생태계를 뒷받침하는 데 중요한 역할을 하고 있습니다.

“예측 기간 동안 도시 교통 관리 애플리케이션 분야가 교통 관리 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다.”

도시 교통 관리 솔루션은 인구 밀집 지역의 교통 체증 해소, 교통 흐름 개선 및 도로 안전성 향상을 도모하기 위해 지자체와 교통 기관에서 널리 도입되고 있습니다. 이러한 솔루션을 통해 복잡한 도시 도로망 전반에 걸쳐 실시간 교통 모니터링, 적응형 신호 제어, 사고 대응 및 교통 최적화가 가능해집니다. 도시화가 진행되고 차량 밀도가 증가함에 따라, 대규모 도로 확장 없이도 교통 효율을 높일 수 있는 기술에 대한 수요가 높아지고 있습니다. 또한 각 도시에서는 교통 관리 플랫폼을 대중교통 시스템, 여행객 대상 정보 서비스, 스마트 시티 구상과 통합하여 모빌리티 전반의 성과 향상을 도모하고 있습니다. 교통 정체 완화와 통근 환경 개선에 대한 지속적인 노력이 예측 기간 동안 도시 교통 관리 부문의 우위를 뒷받침할 것으로 예상됩니다.

“예측 기간 동안 적응형 교통 제어 시스템(ATCS) 부문이 가장 높은 성장률을 기록할 것으로 전망됩니다.”

적응형 교통 제어 시스템은 실시간 교통 상황을 바탕으로 신호 타이밍을 동적으로 조정하여, 교통 기관이 교차로의 성능을 향상시키고 교통 지연을 줄이는 데 도움을 줍니다. 이러한 솔루션은 센서, 카메라, 교통 감지기로부터 수집된 데이터를 활용하여 신호 운영을 최적화하고, 하루 종일 변화하는 교통 패턴에 대응합니다. 기존 신호 시스템과 비교했을 때, 적응형 교통 제어 기술은 교통 흐름을 개선하고, 차량의 정지 횟수를 줄이며, 도로 이용 효율을 높입니다. 지능형 교통 인프라에 대한 투자 증가와 실시간 교통 최적화에 대한 수요 증가에 따라, 지자체들은 도심 및 교외의 전체 교통 네트워크에 적응형 교통 제어 솔루션을 도입하고 있습니다. 도시들이 더욱 스마트하고 대응력이 뛰어난 교통 운영을 지속적으로 추구함에 따라, 적응형 교통 제어 시스템의 도입이 크게 가속화될 것으로 예상됩니다.

“아시아태평양은 예측 기간 동안 가장 높은 성장률을 기록할 것으로 전망됩니다.”

아시아태평양은 급속한 도시화, 교통 인프라 확충, 그리고 스마트 모빌리티 구상에 대한 정부 투자의 증가로 인해 가장 빠르게 성장하는 지역 시장으로 부상할 것으로 전망됩니다. 중국, 인도, 일본, 한국, 호주, 싱가포르 등의 국가들은 교통 체증 문제를 해결하고 교통 효율을 높이기 위해 지능형 교통 기술을 적극적으로 도입하고 있습니다. 대규모 스마트 시티 프로젝트, 도로 현대화 프로그램, 디지털 교통 인프라에 대한 투자가 해당 지역 전체의 교통 관리 솔루션 제공업체들에게 큰 비즈니스 기회를 창출하고 있습니다. 또한, 자동차 보유 대수의 증가와 효율적인 도시 모빌리티에 대한 수요가 높아짐에 따라, 교통 당국은 첨단 교통 감시, 교통 제어 및 모빌리티 관리 솔루션의 도입을 추진하고 있습니다. 이러한 요인들로 인해, 예측 기간 동안 아시아태평양 전체에서 강력한 시장 성장이 예상됩니다.

주요 응답자의 구성

교통 관리 시장의 주요 기업으로는 Cisco(미국), Mundys SpA(이탈리아), SWARCO(오스트리아), Siemens(독일), IBM(미국), Kapsch TrafficCom(오스트리아), Q-Free(노르웨이), Umovity(독일), Teledyne FLIR Systems Inc.(미국), Cubic Corporation(미국), Almaviva SpA.(이탈리아), TOMTOM(네덜란드), Huawei(중국), ST Engineering(싱가포르), 그리고 Indra Sistemas(스페인)가 있습니다. 이 기업들은 교통 관리 시장에서의 사업 기반을 확대하기 위해 파트너십, 계약 및 제휴, 신제품 출시, 제품 기능 강화, 인수합병 등 다양한 성장 전략을 채택하고 있습니다.

조사 범위

본 시장 조사는 다양한 부문에 걸친 교통 관리 시장의 규모를 포괄하고 있습니다. 본 조사의 목적은 구성요소(하드웨어, 솔루션, 서비스), 적용 분야, 최종사용자, 지역 등 다양한 부문의 시장 규모와 성장 가능성을 추정하는 것입니다. 본 조사에는 주요 기업에 대한 상세한 경쟁 분석, 각 기업 개요, 제품 및 사업 제공과 관련된 주요 관찰 사항, 최근 동향, 그리고 시장 전략이 포함되어 있습니다.

본 보고서를 구매할 때의 주요 이점

본 보고서는 전 세계 교통 관리 시장의 매출액 및 하위 부문에 대한 가장 정확한 추정치를 제공함으로써, 시장을 선도하는 기업과 신규 진입 기업을 지원합니다. 또한, 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 나은 위치로 이끌며, 적절한 시장 진입 전략을 수립하기 위한 추가적인 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악할 수 있도록 인사이트를 제공할 뿐만 아니라, 주요 시장 촉진요인, 억제요인, 과제 및 기회에 대한 정보도 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인(운전자 및 승객의 실시간 교통 정보 수요 증가, 도시 인구 증가, 차량 대수 증가, 인프라 미비), 제약요인(신규 프로젝트를 제한하는 인력 부족, 인프라 부문의 성장 둔화, 기존 인프라의 효율화를 위한 표준화 및 통합된 기술의 부재), 기회(교통 관리 업계의 가격 책정 동향 변화, 친환경 자동차 기술에 따른 환경 보호에 대한 관심 증가, 분석 소프트웨어의 성장), 그리고 과제(데이터 관리 및 빅데이터 관련 문제, 여러 센서 및 접점을 통한 데이터 융합의 과제, 보안 위협 및 해킹 문제) 등, 교통 관리 시장의 성장에 영향을 미치는 요인들에 대해 분석하고 있습니다.

- 제품 개발/혁신 : 교통 관리 시장의 향후 기술, 연구 개발 활동 및 신제품·서비스 출시에 관한 상세한 인사이트.

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역에 걸친 교통 관리 시장을 분석하고 있습니다.

- 시장의 다양화 : 교통 관리 시장의 신제품·서비스, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보입니다.

- 경쟁사 분석 : Cisco(미국), Mundys SpA(이탈리아), SWARCO(오스트리아), Siemens(독일), IBM(미국), Kapsch TrafficCom(오스트리아), Q-Free(노르웨이), Umovity(독일), Teledyne FLIR Systems Inc.(미국), Cubic Corporation(미국), Almaviva SpA(이탈리아), TOMTOM(네덜란드), Huawei(중국), ST Engineering(싱가포르), Indra Sistemas(스페인) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공 내용에 대한 상세한 평가.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황과 지속가능성에 대한 대처

제8장 고객 상황과 구매 행동

제9장 교통 관리 시장(제공별)

제10장 교통 관리 시장(적용 분야별)

제11장 교통 관리 시장(최종사용자별)

제12장 교통 관리 시장(지역별)

제13장 경쟁 구도

제14장 기업 개요

제15장 조사 방법

제16장 부록

KSM 26.07.02The traffic management market is estimated to grow from USD 55.24 billion in 2026 to USD 106.13 billion by 2032, at a CAGR of 11.5% from 2026 to 2032. The traffic management market is experiencing steady growth as transportation authorities seek to improve mobility, reduce congestion, and enhance operational efficiency across road networks.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Area of Application, End User |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

The market is benefiting from increasing investments in intelligent transportation systems (ITS), traffic monitoring technologies, and integrated traffic control platforms that enable real-time traffic management. Modern traffic management solutions combine traffic surveillance, analytics, incident detection, and centralized control capabilities to help operators make informed decisions and respond rapidly to changing traffic conditions. The growing need to maximize existing transportation infrastructure while supporting increasing traffic volumes is encouraging public agencies to deploy advanced traffic management technologies across urban and highway networks. As transportation systems become more connected and data-driven, traffic management solutions are playing a critical role in supporting safer, more efficient, and more resilient mobility ecosystems.

"During the forecast period, the urban traffic management application segment is expected to account for the largest share of the traffic management market."

Urban traffic management solutions are widely deployed by municipalities and transportation agencies to address congestion, improve traffic flow, and enhance roadway safety in densely populated areas. These solutions enable real-time traffic monitoring, adaptive signal coordination, incident management, and traffic optimization across complex urban road networks. Growing urbanization and increasing vehicle density are driving demand for technologies that improve transportation efficiency without requiring significant roadway expansion. In addition, cities are integrating traffic management platforms with public transportation systems, traveler information services, and smart city initiatives to improve overall mobility outcomes. The continued focus on reducing congestion and improving commuter experiences is expected to support the dominance of the urban traffic management segment throughout the forecast period.

"The adaptive traffic control system (ATCS) segment is projected to register the highest growth rate during the forecast period."

Adaptive traffic control systems dynamically adjust traffic signal timings based on real-time traffic conditions, helping transportation agencies improve intersection performance and reduce traffic delays. These solutions utilize data collected from sensors, cameras, and traffic detectors to optimize signal operations and respond to changing traffic patterns throughout the day. Compared with conventional traffic signal systems, adaptive traffic control technologies improve traffic flow, reduce vehicle stoppages, and enhance roadway efficiency. Increasing investments in intelligent transportation infrastructure and growing demand for real-time traffic optimization are encouraging municipalities to deploy adaptive traffic control solutions across urban and suburban transportation networks. As cities continue to pursue smarter and more responsive traffic operations, adoption of adaptive traffic control systems is expected to accelerate significantly.

"Asia Pacific is expected to register the highest growth rate during the forecast period."

Asia Pacific is projected to emerge as the fastest-growing regional market due to rapid urbanization, expanding transportation infrastructure, and increasing government investments in smart mobility initiatives. Countries such as China, India, Japan, South Korea, Australia, and Singapore are actively deploying intelligent transportation technologies to address congestion challenges and improve transportation efficiency. Large-scale smart city projects, roadway modernization programs, and investments in digital transportation infrastructure are creating substantial opportunities for traffic management solution providers across the region. Additionally, increasing vehicle ownership and rising demand for efficient urban mobility are encouraging transportation authorities to adopt advanced traffic monitoring, traffic control, and mobility management solutions. These factors are expected to drive strong market growth across Asia Pacific throughout the forecast period.

Breakdown of primaries

The study contains insights from various industry experts, from solution vendors to Tier 1 companies. The break-up of the primaries is as follows:

- By Company Type: Tier 1 - 25%, Tier 2 - 40%, and Tier 3 - 35%

- By Designation: C-level - 47%, D-level - 32%, and Managers - 21%

- By Region: North America - 40%, Europe - 35%, Asia Pacific - 20%, and RoW-5%

The major players in the traffic management market are Cisco (US), Mundys SpA (Italy), SWARCO (Austria), Siemens (Germany), IBM (US), Kapsch TrafficCom (Austria), Q-Free (Norway), Umovity (Germany), Teledyne FLIR Systems Inc. (US), Cubic Corporation (US), Almaviva SpA. (Italy), TOMTOM (Netherlands), Huawei (China), ST Engineering (Singapore), and Indra Sistemas (Spain). These players have adopted various growth strategies, such as partnerships, agreements and collaborations, product launches, product enhancements, and acquisitions to expand their footprint in the traffic management market.

Research Coverage

The market study covers the traffic management market size across different segments. It aims to estimate the market size and the growth potential across different segments, including components (hardware, solutions, and services), areas of application, end users, and regions. The study includes an in-depth competitive analysis of the leading market players, their company profiles, key observations related to product and business offerings, recent developments, and market strategies.

Key Benefits of Buying the Report

The report will help market leaders and new entrants with information on the closest approximations of the global traffic management market's revenue numbers and subsegments. It will also help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. Moreover, the report will provide insights for stakeholders to understand the market's pulse and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (rising demand for real-time traffic information to drivers and passengers, an increasingly urban population, rising number of vehicles, inadequate infrastructure), restraints (labor shortage limiting new projects, slow growth in the infrastructure sector, lack of standardized and uniform technologies to streamline legacy infrastructure), opportunities (changing pricing dynamics in the traffic management industry, increasing concerns about protecting environment with eco-friendly automobile technology, growth of analytics software), and challenges (data management and big data issues, multiple sensors and touchpoints pose data fusion challenges, security threats and hacking challenges) influencing the growth of the traffic management market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the traffic management market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the traffic management market across various regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the traffic management market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Cisco (US), Mundys SpA (Italy), SWARCO (Austria), Siemens (Germany), IBM (US), Kapsch TrafficCom (Austria), Q-Free (Norway), Umovity (Germany), Teledyne FLIR Systems Inc. (US), Cubic Corporation (US), Almaviva SpA. (Italy), TOMTOM (Netherlands), Huawei (China), ST Engineering (Singapore), and Indra Sistemas (Spain).

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN TRAFFIC MANAGEMENT MARKET

- 2.4 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TRAFFIC MANAGEMENT MARKET

- 3.2 TRAFFIC MANAGEMENT MARKET, BY OFFERING

- 3.3 TRAFFIC MANAGEMENT MARKET, BY SOLUTION

- 3.4 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION

- 3.5 TRAFFIC MANAGEMENT MARKET, BY END USER

- 3.6 NORTH AMERICA: TRAFFIC MANAGEMENT MARKET: TOP THREE SOLUTIONS AND END USER

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increased traffic congestion and need for road safety measures

- 4.2.1.2 Increasing adoption of AI-driven traffic optimization and predictive mobility management

- 4.2.1.3 Expansion of connected vehicle and V2X ecosystems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High capital investment and lengthy procurement cycles

- 4.2.2.2 Budget constraints among municipalities and transportation agencies

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Sustainable mobility and emissions reduction initiatives

- 4.2.3.2 Expansion of connected and autonomous vehicle ecosystems

- 4.2.3.3 Modernization of highway and smart corridor infrastructure

- 4.2.3.4 5G-enabled intelligent transportation systems

- 4.2.4 CHALLENGES

- 4.2.4.1 Data management and big data complexity

- 4.2.4.2 Cybersecurity threats to transportation networks

- 4.2.4.3 Integration of multi-source transportation data

- 4.2.1 DRIVERS

- 4.3 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.3.1 CROSS-SECTOR OPPORTUNITIES

- 4.4 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN TRAFFIC MANAGEMENT MARKET

- 5.3 SUPPLY CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY SOLUTION

- 5.5.2 INDICATIVE PRICING ANALYSIS OF KEY PLAYERS

- 5.6 TRADE ANALYSIS

- 5.6.1 EXPORT SCENARIO FOR HS CODE: 8530

- 5.6.2 IMPORT SCENARIO FOR HS CODE: 8530

- 5.7 KEY CONFERENCES AND EVENTS, 2026

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 CASE STUDY 1: BUENOS AIRES DEPLOYED SGIM SOFTWARE IN CONJUNCTION WITH KAPSCH'S ECOTRAFIX PLATFORM TO UNIFY EXISTING UTC SYSTEMS

- 5.10.2 CASE STUDY 2: HUAWEI HELPED LAHORE CITY DEVELOP NEW TRAFFIC MANAGEMENT SYSTEM TO MANAGE CONGESTION

- 5.10.3 CASE STUDY 3: ROMANIAN CITY OF TIMISOARA DEPLOYED SWARCO'S INTEGRATED TRAFFIC CONTROL AND VIDEO SURVEILLANCE SYSTEM TO SMOOTHEN TRAFFIC FLOW

- 5.10.4 CASE STUDY 4: DATA COLLECTION LIMITED ENHANCED ROAD INFRASTRUCTURE MANAGEMENT WITH TELEDYNE FLIR IMAGING SOLUTIONS

- 5.10.5 CASE STUDY 5: THTC & TOMTOM SUCCESSFULLY MANAGED TRAFFIC AT 2023 AFC ASIAN CUP QATAR

- 5.11 IMPACT OF 2025 US TARIFF - TRAFFIC MANAGEMENT MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.3.1 Strategic shifts and emerging trends

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 US

- 5.11.4.2 China

- 5.11.4.3 Europe

- 5.11.4.4 Asia Pacific (excluding China)

- 5.11.5 IMPACT ON END-USER INDUSTRIES

- 5.11.5.1 Government & Transportation Authorities

- 5.11.5.2 Smart Cities & Municipalities

- 5.11.5.3 Highways & Toll Operators

- 5.11.5.4 Public Transit Operators

- 5.11.5.5 Airports & Transportation Hubs

- 5.11.5.6 Commercial & Industrial Facilities

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ARTIFICIAL INTELLIGENCE (AI)

- 6.1.2 INTERNET OF THINGS (IOT)

- 6.1.3 GEOGRAPHIC INFORMATION SYSTEMS (GIS)

- 6.1.4 AUTOMATIC NUMBER PLATE RECOGNITION (ANPR)

- 6.1.5 VEHICLE-TO-INFRASTRUCTURE (V2I) AND VEHICLE-TO-EVERYTHING (V2X)

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 BIG DATA AND ANALYTICS

- 6.2.2 EDGE COMPUTING

- 6.2.3 5G

- 6.3 TECHNOLOGY ROADMAP

- 6.3.1 SHORT-TERM ROADMAP (2026-2027)

- 6.3.2 MID-TERM ROADMAP (2028-2027)

- 6.3.3 LONG-TERM ROADMAP (2029-2030+)

- 6.4 PATENT ANALYSIS

- 6.4.1 LIST OF MAJOR PATENTS (2018-2026)

- 6.5 IMPACT OF AI/GEN AI ON TRAFFIC MANAGEMENT MARKET

- 6.5.1 TOP USE CASES AND MARKET POTENTIAL

- 6.5.2 CASE STUDIES OF AI IMPLEMENTATION IN TRAFFIC MANAGEMENT MARKET

- 6.5.3 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.5.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN TRAFFIC MANAGEMENT MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 KEY REGULATIONS

- 7.1.2.1 North America

- 7.1.2.1.1 Manual on Traffic Control Devices for Streets and Highways

- 7.1.2.1.2 National Highway Traffic Safety Administration (NHTSA)

- 7.1.2.1.3 Federal Motor Carrier Safety Administration

- 7.1.2.1.4 Federal Highway Administration

- 7.1.2.2 Europe

- 7.1.2.2.1 General Data Protection Regulation

- 7.1.2.2.2 General Safety Regulation (GSR)

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 General Safety Regulation (GSR)

- 7.1.2.3.2 Road Traffic Safety Law of the People's Republic of China

- 7.1.2.3.3 Road Traffic Act

- 7.1.2.3.4 Road Transport Vehicle Act

- 7.1.2.4 Rest of the World

- 7.1.2.4.1 Manual on Traffic Control Devices for Streets and Highways

- 7.1.2.4.2 National Road Traffic Act, 1996

- 7.1.2.4.3 Mexico's National Law of Mobility and Road Safety

- 7.1.2.1 North America

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 SUSTAINABLE MOBILITY AND INTELLIGENT TRAFFIC OPERATIONS

- 7.2.2 ECO-APPLICATIONS AND SUSTAINABILITY USE CASES

- 7.3 CERTIFICATIONS, LABELING, ECO-STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF VARIOUS END-USE INDUSTRIES

9 TRAFFIC MANAGEMENT MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: TRAFFIC MANAGEMENT MARKET DRIVERS

- 9.2 SOLUTIONS

- 9.2.1 TRAFFIC MONITORING & ANALYTICS

- 9.2.1.1 Enabling data-driven visibility across transportation networks

- 9.2.2 ADAPTIVE TRAFFIC CONTROL

- 9.2.2.1 Optimizing signal operations through dynamic traffic management

- 9.2.3 TRAFFIC ENFORCEMENT MANAGEMENT

- 9.2.3.1 Strengthening roadway compliance and traffic safety outcomes

- 9.2.4 INCIDENT DETECTION & MANAGEMENT

- 9.2.4.1 Accelerating incident response through real-time situational awareness

- 9.2.5 ELECTRONIC TOLL MANAGEMENT

- 9.2.5.1 Advancing seamless toll collection and roadway monetization

- 9.2.6 OTHER SOLUTIONS

- 9.2.1 TRAFFIC MONITORING & ANALYTICS

- 9.3 SERVICES

- 9.3.1 CONSULTING

- 9.3.1.1 Optimizing traffic management and infrastructure

- 9.3.2 IMPLEMENTATION

- 9.3.2.1 Streamlining business applications by integrating various modules of day-to-day operations

- 9.3.3 SUPPORT & MAINTENANCE

- 9.3.3.1 Ensuring smooth functioning of traffic management solutions

- 9.3.1 CONSULTING

10 TRAFFIC MANAGEMENT MARKET, BY AREA OF APPLICATION

- 10.1 INTRODUCTION

- 10.1.1 AREA OF APPLICATION: TRAFFIC MANAGEMENT MARKET DRIVERS

- 10.2 URBAN

- 10.2.1 SUPPORTING EFFICIENT MOBILITY IN INCREASINGLY COMPLEX URBAN TRANSPORTATION NETWORKS

- 10.3 INTER-URBAN

- 10.3.1 ENHANCING CONNECTIVITY AND OPERATIONAL EFFICIENCY ACROSS REGIONAL TRANSPORTATION CORRIDORS

- 10.4 RURAL

- 10.4.1 IMPROVING ROADWAY SAFETY AND TRANSPORTATION ACCESSIBILITY ACROSS RURAL NETWORKS

11 TRAFFIC MANAGEMENT MARKET, BY END USER

- 11.1 INTRODUCTION

- 11.1.1 END USER: TRAFFIC MANAGEMENT MARKET DRIVERS

- 11.2 GOVERNMENT

- 11.2.1 ADVANCING TRANSPORTATION EFFICIENCY AND PUBLIC SAFETY THROUGH INTELLIGENT TRAFFIC MANAGEMENT

- 11.3 PRIVATE

- 11.3.1 IMPROVING OPERATIONAL EFFICIENCY AND MOBILITY SERVICES THROUGH INTELLIGENT TRANSPORTATION SOLUTIONS

12 TRAFFIC MANAGEMENT MARKET, BY REGION

- 12.1 INTRODUCTION

- 12.2 NORTH AMERICA

- 12.2.1 US

- 12.2.1.1 Government initiatives to revamp, expand, and modernize existing traffic management infrastructure to drive market

- 12.2.2 CANADA

- 12.2.2.1 Development of smart cities to drive market

- 12.2.1 US

- 12.3 EUROPE

- 12.3.1 UK

- 12.3.1.1 Government initiatives to standardize transport interfaces supported by collaborations and partnerships to drive market

- 12.3.2 ITALY

- 12.3.2.1 Government investment in road safety, traffic flow, and congestion alleviation to drive market

- 12.3.3 GERMANY

- 12.3.3.1 2030 Federal Transport Infrastructure Plan to drive market

- 12.3.4 FRANCE

- 12.3.4.1 Advancements in robotics and IoT, especially in public transportation, to drive market

- 12.3.5 SPAIN

- 12.3.5.1 Focus on bolstering public transportation to drive market

- 12.3.6 REST OF EUROPE

- 12.3.1 UK

- 12.4 ASIA PACIFIC

- 12.4.1 CHINA

- 12.4.1.1 Investment in AI-powered traffic management systems and Internet of Vehicle Technologies (IoVT) to drive market

- 12.4.2 INDIA

- 12.4.2.1 Government focus on AI adoption for enhanced road safety to drive market

- 12.4.3 JAPAN

- 12.4.3.1 Establishment of Digital Agency for Society 5.0 to drive market

- 12.4.4 AUSTRALIA & NEW ZEALAND

- 12.4.4.1 Implementation of smart city projects to accelerate market growth

- 12.4.5 REST OF ASIA PACIFIC

- 12.4.1 CHINA

- 12.5 MIDDLE EAST & AFRICA

- 12.5.1 KSA

- 12.5.1.1 Initiatives toward comprehensive transport planning analysis and performance reporting to drive market

- 12.5.2 UAE

- 12.5.2.1 Collaborations with prominent players for building smart traffic systems to drive market

- 12.5.3 SOUTH AFRICA

- 12.5.3.1 Rising urban congestion and safety concerns to drive market

- 12.5.4 REST OF MIDDLE EAST & AFRICA

- 12.5.1 KSA

- 12.6 LATIN AMERICA

- 12.6.1 BRAZIL

- 12.6.1.1 Increasing focus on vehicle monitoring and incident management to drive market

- 12.6.2 MEXICO

- 12.6.2.1 Rising demand for improved transport infrastructure to drive market

- 12.6.3 REST OF LATIN AMERICA

- 12.6.1 BRAZIL

13 COMPETITIVE LANDSCAPE

- 13.1 INTRODUCTION

- 13.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2024-2025

- 13.3 REVENUE ANALYSIS, 2022-2024

- 13.4 MARKET SHARE ANALYSIS, 2025

- 13.5 BRAND/PRODUCT COMPARISON

- 13.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 13.6.1 STARS

- 13.6.2 EMERGING LEADERS

- 13.6.3 PERVASIVE PLAYERS

- 13.6.4 PARTICIPANTS

- 13.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 13.6.5.1 Company footprint

- 13.6.5.2 Region footprint

- 13.6.5.3 Offering footprint

- 13.6.5.4 Area of application footprint

- 13.6.5.5 End user footprint

- 13.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 13.7.1 PROGRESSIVE COMPANIES

- 13.7.2 RESPONSIVE COMPANIES

- 13.7.3 DYNAMIC COMPANIES

- 13.7.4 STARTING BLOCKS

- 13.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 13.7.5.1 Detailed list of key startups/SMEs

- 13.7.5.2 Competitive benchmarking of key startups/SMEs

- 13.8 COMPETITIVE SCENARIO

- 13.8.1 PRODUCT LAUNCHES

- 13.8.2 DEALS

- 13.9 TRAFFIC MANAGEMENT PRODUCT BENCHMARKING

- 13.9.1 PROMINENT TRAFFIC MANAGEMENT SOLUTIONS

- 13.9.1.1 IBM intelligent transportation solution

- 13.9.1.2 Huawei intelligent traffic management system (ITMS)

- 13.9.1.3 Kapsch TrafficCom intelligent transportation system (ITS)

- 13.9.1.4 SWARCO cooperative intelligent transport system (SWARCO C-ITS)

- 13.9.1 PROMINENT TRAFFIC MANAGEMENT SOLUTIONS

- 13.10 COMPANY VALUATION AND FINANCIAL METRICS

14 COMPANY PROFILES

- 14.1 MAJOR PLAYERS

- 14.1.1 HUAWEI

- 14.1.1.1 Business overview

- 14.1.1.2 Products/Solutions/Services offered

- 14.1.1.3 Recent developments

- 14.1.1.3.1 Products launches

- 14.1.1.3.2 Deals

- 14.1.1.4 MnM view

- 14.1.1.4.1 Right to win

- 14.1.1.4.2 Strategic choices

- 14.1.1.4.3 Weaknesses and competitive threats

- 14.1.2 MUNDYS SPA

- 14.1.2.1 Business overview

- 14.1.2.2 Products/Solutions/Services offered

- 14.1.2.3 Recent developments

- 14.1.2.3.1 Products launches

- 14.1.2.3.2 Deals

- 14.1.2.4 MnM view

- 14.1.2.4.1 Right to win

- 14.1.2.4.2 Strategic choices

- 14.1.2.4.3 Weaknesses and competitive threats

- 14.1.3 KAPSCH TRAFFICCOM

- 14.1.3.1 Business overview

- 14.1.3.2 Products/Solutions/Services offered

- 14.1.3.3 Recent developments

- 14.1.3.3.1 Product launches & enhancements

- 14.1.3.3.2 Deals

- 14.1.3.4 MnM View

- 14.1.3.4.1 Right to Win

- 14.1.3.4.2 Strategic Choices

- 14.1.3.4.3 Weaknesses and Competitive Threats

- 14.1.4 SWARCO

- 14.1.4.1 Business overview

- 14.1.4.2 Products/Solutions/Services offered

- 14.1.4.3 Recent developments

- 14.1.4.3.1 Product launches & enhancements

- 14.1.4.3.2 Deals

- 14.1.4.4 MnM view

- 14.1.4.4.1 Right to win

- 14.1.4.4.2 Strategic choices

- 14.1.4.4.3 Weaknesses and competitive threats

- 14.1.5 ST ENGINEERING

- 14.1.5.1 Business overview

- 14.1.5.2 Products/Solutions/Services offered

- 14.1.5.3 Recent developments

- 14.1.5.3.1 Product launches & enhancements

- 14.1.5.3.2 Deals

- 14.1.5.4 MnM View

- 14.1.5.4.1 Right to Win

- 14.1.5.4.2 Strategic Choices

- 14.1.5.4.3 Weaknesses and Competitive Threats

- 14.1.6 INDRA

- 14.1.6.1 Business overview

- 14.1.6.2 Products/Solutions/Services offered

- 14.1.6.3 Recent developments

- 14.1.6.3.1 Deals

- 14.1.6.4 MnM View

- 14.1.6.4.1 Right to Win

- 14.1.6.4.2 Strategic Choices

- 14.1.6.4.3 Weaknesses and Competitive Threats

- 14.1.7 UMOVITY

- 14.1.7.1 Business overview

- 14.1.7.2 Products/Solutions/Services offered

- 14.1.7.3 Recent developments

- 14.1.7.3.1 Product launches & enhancements

- 14.1.7.3.2 Deals

- 14.1.8 Q-FREE

- 14.1.8.1 Business overview

- 14.1.8.2 Products/Solutions/Services offered

- 14.1.8.3 Recent developments

- 14.1.8.3.1 Product launches & enhancements

- 14.1.8.3.2 Deals

- 14.1.9 ALMAVIVA SPA

- 14.1.9.1 Business overview

- 14.1.9.2 Products/Solutions/Services offered

- 14.1.9.3 Recent developments

- 14.1.9.3.1 Product launches & enhancements

- 14.1.9.3.2 Deals

- 14.1.10 TOMTOM

- 14.1.10.1 Business overview

- 14.1.10.2 Products/Solutions/Services offered

- 14.1.10.3 Recent developments

- 14.1.10.3.1 Product launches & enhancements

- 14.1.10.3.2 Deals

- 14.1.11 JENOPTIK

- 14.1.12 TELEDYNE FLIR

- 14.1.13 SIEMENS

- 14.1.14 CISCO

- 14.1.15 IBM

- 14.1.16 CUBIC CORPORATION

- 14.1.1 HUAWEI

- 14.2 STARTUPS/SMES

- 14.2.1 INRIX

- 14.2.2 NOTRAFFIC

- 14.2.3 TAGMASTER

- 14.2.4 BERCMAN TECHNOLOGIES

- 14.2.5 VALERANN

- 14.2.6 MIOVISION

- 14.2.7 BLUESIGNAL

- 14.2.8 TELEGRA

- 14.2.9 ORIUX

- 14.2.10 INVARION

- 14.2.11 REKOR

15 RESEARCH METHODOLOGY

- 15.1 RESEARCH DATA

- 15.1.1 SECONDARY DATA

- 15.1.1.1 Key data from secondary sources

- 15.1.1.2 List of secondary sources

- 15.1.2 PRIMARY DATA

- 15.1.2.1 Breakup of primary profiles

- 15.1.2.2 Key insights from industry experts

- 15.1.2.3 Key data from primary sources

- 15.1.1 SECONDARY DATA

- 15.2 MARKET SIZE ESTIMATION

- 15.3 DATA TRIANGULATION

- 15.4 MARKET FORECAST APPROACH

- 15.5 RESEARCH ASSUMPTIONS

- 15.6 RESEARCH LIMITATIONS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS