|

시장보고서

상품코드

2074458

완제 공정 세계 시장(-2031년) : 소모품(PFS, 바이알, 바이알 마개, 카트리지, 세포치료용 백), 기기(통합형)·유형(자동화), 서비스, 기업별Fill Finish Manufacturing Market by Consumables (PFS, Vials, Vial Stoppers, Cartridges, Cell Therapy Bags), Instruments (Integrated), Type (Automated), Services, Competition - Global Forecast to 2031 |

||||||

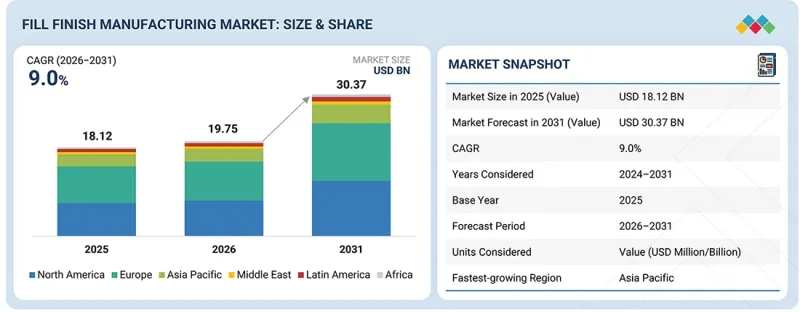

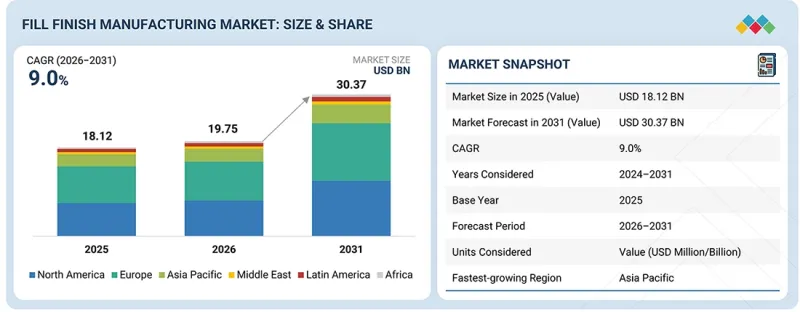

세계의 완제 공정 시장 규모는 2026년 197억 5,000만 달러에서 2031년에는 303억 7,000만 달러에 이를 것으로 추정되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 9.0`%를 기록할 전망입니다.

시장의 성장은 바이오의약품, 바이오시밀러, 백신, 주사제 파이프라인의 확대, CDMO로의 아웃소싱 증가, 무균 제조 능력에 대한 수요 증가에 힘입어 이루어지고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2024-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(달러) |

| 부문 | 제품, 최종사용자 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 라틴아메리카, 중동 및 아프리카 |

무균 충전, 아이솔레이터 시스템, 로봇 공학, 즉시 사용 가능한 부품 분야의 기술 발전이 시장 확대를 더욱 촉진하고 있습니다. 그러나 한편으로는 막대한 설비 투자가 필요하다는 점, 엄격한 규제 준수 기준, 운영상의 복잡성, 숙련된 인력 부족 등이 시장의 성장을 어느 정도 저해할 가능성이 있습니다.

“제품별로는 소모품 부문이 2025년에 가장 큰 시장 점유율을 차지했습니다.”

제품별로 살펴보면, 충전, 밀봉, 검사, 포장 등 각 공정에서 널리 사용되고 있는 점을 배경으로, 2025년에는 소모품 부문이 가장 큰 시장 점유율을 차지했습니다. 바이알, 프리필드 주사기, 카트리지, 스토퍼, 씰, 기타 용기 및 밀봉 부품 등의 소모품은 모든 생산 배치에 필요하기 때문에 지속적인 수요를 창출하고 있습니다. 바이오의약품, 바이오시밀러, 백신, 첨단 치료제의 생산 확대에 더해, RTU(Ready-to-Use) 및 일회용 기술의 도입이 확대됨에 따라 전 세계 제약 기업 및 CDMO에서 소모품에 대한 견조한 수요가 계속해서 시장을 견인하고 있습니다.

“최종 사용자별로는 2025년에 수탁 제조 기관(CMO)이 가장 큰 점유율을 차지했습니다.”

이러한 성장은 비용 절감, 전문적인 노하우 활용, 제품 상용화 가속화를 목표로 하는 제약회사 및 생명공학 기업들의 무균 제조 업무 아웃소싱 증가에 힘입어 이루어지고 있습니다. CMO는 첨단 무균 처리 능력, 유연한 생산 능력, 견고한 규제 준수 체계를 갖추고 있어, 바이오의약품, 바이오시밀러, 백신, 주사제 분야에서 우선적으로 선택받는 파트너로 자리매김하고 있습니다. 확장성이 뛰어나고 고품질의 제조 서비스에 대한 수요가 증가함에 따라, 시장에서 CMO의 입지는 계속해서 더욱 공고해지고 있습니다.

“아시아태평양은 2026년부터 2031년에 걸쳐 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다.”

예측 기간 동안 아시아태평양은 바이오의약품 생산 확대, 무균 주사제 생산에 대한 투자 증가, 바이오의약품, 바이오시밀러, 백신에 대한 수요 증가에 힘입어 가장 높은 연평균 성장률(CAGR)을 보일 것으로 추정됩니다. 또한, CDMO 서비스의 급속한 확대, 첨단 무균 충전 기술의 도입 확대, 중국, 인도, 한국, 일본에서의 제조 인프라에 대한 지속적인 투자가 이러한 성장을 뒷받침하고 있습니다. 주요 생산 거점의 존재와 지속적인 생산 능력 확대를 통해, 세계 충전 및 마감제조 시장에서 해당 지역의 입지는 계속해서 공고해지고 있습니다.

본 보고서에서는 전 세계 충전 및 마감제조 시장을 조사했으며, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추이 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 프로파일 등을 정리했습니다.

자주 묻는 질문

목차

제1장 서론

제2장 주요 요약

제3장 프리미엄 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI의 영향, 특허, 혁신, 향후 응용

제7장 규제 상황과 지속가능성 이니셔티브

제8장 고객 현황과 구매 행동

제9장 완제 공정 시장 : 제품별

제10장 완제 공정 시장 : 최종사용자별

제11장 완제 공정 시장 : 지역별

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

LSHThe global fill finish manufacturing market is estimated to reach USD 30.37 billion by 2031, up from USD 19.75 billion in 2026, at a CAGR of 9.0% from 2026 to 2031. Market growth is driven by the expanding biologics, biosimilars, vaccines, and injectable drug pipelines, increasing outsourcing to CDMOs, and rising demand for sterile manufacturing capacity.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2024-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD billion) |

| Segments | Product, end user |

| Regions covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

Technological advancements in aseptic filling, isolator systems, robotics, and ready-to-use components are further supporting market expansion. However, high capital investment requirements, stringent regulatory compliance standards, operational complexity, and skilled workforce shortages may restrain market growth to some extent.

"The consumables segment accounted for the largest market share, by product, in 2025."

Based on product, the fill finish manufacturing market is broadly segmented into consumables and instruments. In 2025, the consumables accounted for the largest market share, driven by their extensive use across filling, containment, inspection, and packaging operations. Consumables such as vials, prefilled syringes, cartridges, stoppers, seals, and other container & closure components are required for every production batch, creating recurring demand. The growing production of biologics, biosimilars, vaccines, and advanced therapies, coupled with increasing adoption of ready-to-use and single-use technologies, continues to drive strong demand for consumables across pharmaceutical companies and CDMOs globally.

"Contract manufacturing organization accounted for the largest share of the fill finish manufacturing market, by end user, in 2025."

Based on end user, the global fill finish manufacturing market is segmented into CMO, pharmaceutical and biopharmaceutical companies, and other end users. The CMOs segment accounted for the largest share of the global fill finish manufacturing market. Growth is driven by increasing outsourcing of sterile manufacturing operations by pharmaceutical and biotechnology companies seeking to reduce costs, access specialized expertise, and accelerate product commercialization. CMOs offer advanced aseptic processing capabilities, flexible production capacity, and strong regulatory compliance, making them preferred partners for biologics, biosimilars, vaccines, and injectable drugs. Rising demand for scalable and high-quality manufacturing services continues to strengthen their position in the market.

"Asia Pacific is projected to register the highest CAGR in the fill finish manufacturing market from 2026 to 2031."

The fill finish manufacturing market is segmented into North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. During the forecast period, the Asia Pacific region is estimated to grow at the highest CAGR, driven by expanding biopharmaceutical manufacturing, increasing investments in sterile injectable production, and rising demand for biologics, biosimilars, and vaccines. Growth is further supported by the rapid expansion of CDMO services, increasing adoption of advanced aseptic filling technologies, and ongoing investments in manufacturing infrastructure across China, India, South Korea, and Japan. The presence of major regional manufacturing hubs and continuous capacity expansions continues to strengthen the region's position in the global fill-finish manufacturing market.

The primary interviews conducted for this report can be categorized as follows:

- By Respondent: Supply Side - 70% and Demand Side - 30%

- By Company Type: Tier 1 - 40%, Tier 2 - 30%, and Tier 3 - 30%

- By Designation: CXOs and Directors - 30%, Managers - 45%, and Others - 25%

- By Region: North America - 40%, Europe - 25%, Asia Pacific - 20%, Latin America - 10%, and the Middle East - 5%

List of Companies Profiled in the Report

- West Pharmaceutical Services Inc.

- BD & Co

- Syntegon Technology GmbH

- I.M.A. S.P.A.

- Gerresheimer AG

- AptarGroup Inc.

- Datwyler Holding Inc.

- Danaher

- Stevanato Group S.p.A.

- OPTIMA

- Bausch+Strobel

- Groninger & Co. GmbH

- SCHOTT

- Nipro Corporation

- Bausch Advanced Technology Group

- Maquinaria Industrial Dara SI

Research Coverage

This research report categorizes the fill finish manufacturing market by product, type, end user, and region. The scope of the report covers detailed information regarding the major factors, such as drivers, challenges, opportunities, and restraints, influencing the growth of the fill finish manufacturing market. A detailed analysis of the key industry players has been done to provide insights into their business overview, product portfolio, key strategies such as product and service approvals and launches, collaborations, partnerships, expansions, agreements, and recent developments associated with the fill finish manufacturing market. This report covers competitive analysis of top players and upcoming startups in the fill finish manufacturing market ecosystem.

Key Benefits of Buying the Report

The report will help market leaders/new entrants by providing the closest approximations of revenue for the overall fill finish manufacturing market and its subsegments. It will also help stakeholders better understand the competitive landscape and gain more insights to position their business more effectively and develop suitable go-to-market strategies. This report will enable stakeholders to understand the market's pulse and provide information on key market drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (GLP-1/ Incretin Injectables for obesity driving demand outpacing capacity, Biosimilars & ADC pipeline expansion driving sterile injectable contract manufacturing growth, EU GMP Annex 1 compliance & global sterile manufacturing regulatory harmonization driving capital investments for isolator and RABS, robotics, automation & gloveless isolator technologies gaining traction with improved efficiency), restraints (Price pressure in sterile generics and hospital injectables, Workforce constraints in sterile manufacturing operations, High Capex and lead times constraining fill finish capacity addition, Oral peptides and GLP-1 drug delivery restraining fill finish volume growth), opportunities (Growing demand for cell & gene therapy/mRNA small batch manufacturing, Rising need for automated visual inspection and container closure integrity testing, Integration of predictive analytics, Radiopharmaceutical and Theranostic drug product fill-finish emerging as high growth niche segment) and challenges (Sustainability pressure and high energy intensity of sterile manufacturing) influencing the growth of fill finish manufacturing market

- Product Development/Innovation: Detailed insights on newly launched products of the fill finish manufacturing market

- Market Development: Comprehensive information about lucrative markets - the report analyses the fill finish manufacturing market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the fill finish manufacturing market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and product offerings of leading players such as West Pharmaceutical Services Inc. (US), BD & Co. (US), I.M.A S.p.A (Italy), Syntegon Technology GmbH (Germany), and Gerresheimer AG (Germany), among others

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONS CONSIDERED

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNITS CONSIDERED

- 1.4 STAKEHOLDERS

- 1.5 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING THE MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 FILL-FINISH MANUFACTURING MARKET OVERVIEW

- 3.2 FILL-FINISH MANUFACTURING MARKET, BY TYPE & REGION

- 3.3 FILL-FINISH MANUFACTURING MARKET: GEOGRAPHIC SNAPSHOT

- 3.4 FILL-FINISH MANUFACTURING MARKET: BY TYPE, 2026 VS 2031

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Rapid adoption of GLP-1/incretin injectables for obesity driving demand

- 4.2.1.2 Biosimilars & ADC pipeline expansion driving sterile injectable contract manufacturing growth

- 4.2.1.3 EU GMP Annex 1 compliance & global sterile manufacturing harmonization driving capital investment for isolators and RABS

- 4.2.1.4 Robotics, automation, and gloveless isolator technologies gaining traction

- 4.2.2 RESTRAINTS

- 4.2.2.1 Price pressure in sterile generics and hospital injectables

- 4.2.2.2 Workforce constraints in sterile manufacturing operations

- 4.2.2.3 High CapEx and long lead times constraining fill-finish capacity addition

- 4.2.2.4 Oral peptides and oral GLP-1 drug delivery restraining fill-finish volume growth

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Growing demand for cell & gene therapy/mRNA small-batch manufacturing

- 4.2.3.2 Rising need for automated visual inspection and container closure integrity testing

- 4.2.3.3 Integration of predictive analytics

- 4.2.3.4 Radiopharmaceutical and theranostic drug product fill-finish emerging as high-growth niche

- 4.2.4 CHALLENGES

- 4.2.4.1 Sustainability pressure and high energy intensity of sterile manufacturing

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS & CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF BUYERS

- 5.1.4 BARGAINING POWER OF SUPPLIERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC OUTLOOK

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECAST

- 5.2.3 TRENDS IN GLOBAL FILL-FINISH MANUFACTURING MARKET

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 MANUFACTURING SITES, EXPANSIONS, AND CAPEX TRENDS OF KEY SUPPLIERS

- 5.5.2 MANUFACTURING SITES, EXPANSIONS, AND CAPEX TRENDS OF KEY FILL-FINISH CDMOS

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING ANALYSIS, BY KEY PLAYER (2025)

- 5.6.2 INDICATIVE SELLING PRICE, BY REGION, 2025

- 5.7 TRADE ANALYSIS

- 5.7.1 TRADE ANALYSIS FOR HS CODE 701010

- 5.7.2 TRADE ANALYSIS FOR HS CODE 3923

- 5.7.3 TRADE ANALYSIS FOR HS CODE 7017

- 5.7.4 TRADE ANALYSIS FOR HS CODE 401490

- 5.8 KEY CONFERENCES & EVENTS

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.9.1 KEY LAUNCHES AND PIPELINE OF BIOSIMILARS, GLP-1, CGT, ADC & RADIOPHARMACEUTICALS

- 5.9.2 US FDA APPROVAL TRENDS OF DRUG APPROVALS, BY DOSAGE FORM

- 5.9.2.1 Injectable dosage forms

- 5.9.2.2 Subcutaneous vs. intramuscular biologics

- 5.10 INVESTMENT & FUNDING SCENARIO

- 5.11 IMPACT OF US TARIFFS-FILL-FINISH MANUFACTURING MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 IMPACT ON COUNTRIES/REGIONS

- 5.11.4.1 North America

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 CMOS

- 5.11.5.2 Pharmaceutical and biotechnology companies

- 5.11.5.3 Other end users

- 5.12 FILL-FINISH OUTSOURCING TRENDS

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 ASEPTIC PROCESSING

- 6.1.2 STERILIZATION

- 6.2 ADJACENT TECHNOLOGIES

- 6.2.1 SINGLE-USE SYSTEMS

- 6.2.2 INSPECTION AND QUALITY CONTROL

- 6.3 COMPLEMENTARY TECHNOLOGIES

- 6.3.1 AUTOMATION AND ROBOTICS

- 6.3.2 ISOLATOR TECHNOLOGY

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.5 PATENT ANALYSIS

- 6.5.1 TOP APPLICANTS/OWNERS (COMPANIES) FOR FILL-FINISH MANUFACTURING PATENTS, 2015-2025

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON FILL-FINISH MANUFACTURING MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 CASE STUDIES OF AI IMPLEMENTATION IN FILL-FINISH MANUFACTURING MARKET

- 6.7.3 INTERCONNECTED ADJACENT ECOSYSTEMS AND IMPACT ON MARKET PLAYERS

- 6.7.4 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN FILL-FINISH MANUFACTURING MARKET

7 REGULATORY LANDSCAPE AND SUSTAINABILITY INITIATIVES

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 REGULATORY FRAMEWORK

- 7.1.3 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.3 CERTIFICATIONS, LABELING, & ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 KEY BUYING CRITERIA FOR CONSUMABLES, BY END USER

- 8.2.3 KEY BUYING CRITERIA FOR INSTRUMENTS, BY END USER

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 FILL-FINISH MANUFACTURING MARKET, BY PRODUCT

- 9.1 INTRODUCTION

- 9.2 CONSUMABLES

- 9.2.1 PREFILLED SYRINGES

- 9.2.1.1 Prefilled syringes, by component

- 9.2.1.1.1 Prefilled syringe systems & components

- 9.2.1.1.1.1 Rising demand for prefilled syringe systems to drive market growth

- 9.2.1.1.2 Plunger stoppers

- 9.2.1.1.2.1 Rising prevalence of chronic diseases to positively impact demand for prefilled syringe plunger stoppers

- 9.2.1.1.1 Prefilled syringe systems & components

- 9.2.1.2 Prefilled syringes, by material

- 9.2.1.2.1 Glass

- 9.2.1.2.1.1 Rising adoption of glass-based delivery systems to strengthen market share in biologics and vaccines

- 9.2.1.2.2 Polymer

- 9.2.1.2.2.1 Surging demand for polymer prefilled syringes in biologics and home care

- 9.2.1.2.1 Glass

- 9.2.1.1 Prefilled syringes, by component

- 9.2.2 VIALS

- 9.2.2.1 Vials, by material

- 9.2.2.1.1 Glass

- 9.2.2.1.1.1 Growth in biologics and vaccinations to drive market growth

- 9.2.2.1.2 Polymer

- 9.2.2.1.2.1 Rising demand for break-resistant, low-leachable packaging solutions for sensitive biologics and high-value injectable drugs

- 9.2.2.1.1 Glass

- 9.2.2.2 Vials, by format

- 9.2.2.2.1 Bulk vials

- 9.2.2.2.1.1 Growing use of bulk vials to support high-volume fill-finish operations

- 9.2.2.2.2 RTU vials

- 9.2.2.2.2.1 Rising adoption of RTU vials to streamline aseptic fill-finish processes

- 9.2.2.2.1 Bulk vials

- 9.2.2.1 Vials, by material

- 9.2.3 VIAL STOPPERS

- 9.2.3.1 RTS/RFS vial stoppers

- 9.2.3.1.1 Growing preference for RTS and RFS stoppers to enhance fill-finish efficiency

- 9.2.3.2 RTU vial stoppers

- 9.2.3.2.1 Accelerated shift toward RTU vial stoppers for sterile manufacturing

- 9.2.3.1 RTS/RFS vial stoppers

- 9.2.4 CARTRIDGES

- 9.2.4.1 Rising cases of diabetes and autoimmune disorders to drive growth of cartridges

- 9.2.5 CELL THERAPY FILL-FINISH BAGS

- 9.2.5.1 Specialized fill-finish bags enable safe and sterile cell therapy delivery

- 9.2.6 CAPS

- 9.2.6.1 Crimp/press-fit caps

- 9.2.6.1.1 Rising adoption of crimp and press-fit vial caps to support container-closure integrity in sterile injectables

- 9.2.6.2 Push-fit caps

- 9.2.6.2.1 Growing use of push-fit vial caps to reduce crimping complexity and particle risk in sterile fill-finish

- 9.2.6.1 Crimp/press-fit caps

- 9.2.7 OTHER CONSUMABLES

- 9.2.1 PREFILLED SYRINGES

- 9.3 INSTRUMENTS

- 9.3.1 INSTRUMENTS, BY SYSTEM TYPE

- 9.3.1.1 Integrated systems

- 9.3.1.1.1 Integrated systems, by format

- 9.3.1.1.1.1 Integrated vial filling lines

- 9.3.1.1.1.1.1 Increasing adoption of integrated vial filling lines to improve aseptic throughput and sterility assurance

- 9.3.1.1.1.2 Integrated prefilled syringe & cartridge filling lines

- 9.3.1.1.1.2.1 Increasing demand for integrated filling lines to support self-administered injectables

- 9.3.1.1.1.3 Other integrated systems

- 9.3.1.1.1.1 Integrated vial filling lines

- 9.3.1.1.2 Integrated systems, by barrier technology

- 9.3.1.1.2.1 Integrated isolator-based filling systems

- 9.3.1.1.2.1.1 Increasing adoption of integrated isolator-based filling systems to strengthen sterility assurance

- 9.3.1.1.2.2 Integrated RABS-based filling systems

- 9.3.1.1.2.2.1 Continued use of integrated RABS-based filling systems to support flexible aseptic manufacturing

- 9.3.1.1.2.3 Gloveless robotic fill-finish systems

- 9.3.1.1.2.3.1 Rising deployment of gloveless robotic fill-finish systems to reduce interventions and product loss

- 9.3.1.1.2.4 Conventional cleanroom-based filling systems

- 9.3.1.1.2.4.1 Ongoing role of conventional cleanroom-based systems in cost-sensitive and legacy fill-finish operations

- 9.3.1.1.2.1 Integrated isolator-based filling systems

- 9.3.1.1.1 Integrated systems, by format

- 9.3.1.2 Standalone systems

- 9.3.1.2.1 Standalone filling machines

- 9.3.1.2.1.1 Growing use of standalone filling machines to support flexible clinical and commercial sterile production

- 9.3.1.2.2 Standalone stoppering, capping, and sealing machines

- 9.3.1.2.2.1 Rising demand for standalone stoppering, capping, and sealing machines to strengthen vial closure reliability

- 9.3.1.2.3 Standalone washing, sterilization, and depyrogenation equipment

- 9.3.1.2.3.1 Continued adoption of standalone washing, sterilization, and depyrogenation equipment to support contamination control

- 9.3.1.2.4 Standalone lyophilization equipment

- 9.3.1.2.4.1 Increasing need for standalone lyophilization equipment to support biologics and high-value injectable stability

- 9.3.1.2.5 Other standalone systems

- 9.3.1.2.1 Standalone filling machines

- 9.3.1.1 Integrated systems

- 9.3.2 INSTRUMENTS, BY MACHINE TYPE

- 9.3.2.1 Automated machines

- 9.3.2.1.1 Fully automated vial filling machines

- 9.3.2.1.1.1 Increasing use of fully automated vial filling machines to support high-throughput sterile injectable production

- 9.3.2.1.2 Fully automated prefilled syringe & cartridge filling machines

- 9.3.2.1.2.1 Rising demand for automated prefilled syringe and cartridge filling machines to support self-administered injectables

- 9.3.2.1.3 Automated stoppering, capping, and sealing machines

- 9.3.2.1.3.1 Growing adoption of automated stoppering, capping, and sealing machines to improve closure reliability

- 9.3.2.1.4 Automated washing, sterilization, and depyrogenation systems

- 9.3.2.1.4.1 Increasing deployment of automated washing, sterilization, and depyrogenation systems to strengthen contamination control

- 9.3.2.1.5 Other automated machines

- 9.3.2.1.1 Fully automated vial filling machines

- 9.3.2.2 Semi-automated and manual machines

- 9.3.2.2.1 Semi-automated vial, prefilled syringe, and cartridge filling machines

- 9.3.2.2.1.1 Continued use of semi-automated filling machines to support flexible small-batch manufacturing

- 9.3.2.2.2 Other semi-automated & manual machines

- 9.3.2.2.1 Semi-automated vial, prefilled syringe, and cartridge filling machines

- 9.3.2.1 Automated machines

- 9.3.1 INSTRUMENTS, BY SYSTEM TYPE

- 9.4 FILL-FINISH CDMO SERVICES

10 FILL-FINISH MANUFACTURING MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 CMOS

- 10.2.1 GROWING RELIANCE ON CMOS AS KEY END USERS IN FILL-FINISH MANUFACTURING MARKET

- 10.3 PHARMACEUTICAL & BIOPHARMACEUTICAL COMPANIES

- 10.3.1 INCREASING IN-HOUSE FILL-FINISH CAPABILITIES AMONG PHARMACEUTICAL AND BIOPHARMACEUTICAL COMPANIES

- 10.4 OTHER END USERS

11 FILL-FINISH MANUFACTURING MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Rising number of pipeline products for fill-finish manufacturing to drive market

- 11.2.2 CANADA

- 11.2.2.1 Competitive business environment to boost market

- 11.2.1 US

- 11.3 EUROPE

- 11.3.1 GERMANY

- 11.3.1.1 Rising focus on clinical research and patent approvals to drive market

- 11.3.2 UK

- 11.3.2.1 Growth in biopharmaceutical industry to support market growth

- 11.3.3 FRANCE

- 11.3.3.1 Increasing focus on developing biologics to drive demand for fill-finish technologies

- 11.3.4 ITALY

- 11.3.4.1 Investments and advancements to drive market

- 11.3.5 SPAIN

- 11.3.5.1 Innovations in fill-finish manufacturing market to drive growth

- 11.3.6 SWITZERLAND

- 11.3.6.1 Outsourcing trends and collaboration with CMOs to drive growth

- 11.3.7 REST OF EUROPE

- 11.3.1 GERMANY

- 11.4 ASIA PACIFIC

- 11.4.1 CHINA

- 11.4.1.1 Increased investments in biologics and biosimilar drug research to drive market

- 11.4.2 JAPAN

- 11.4.2.1 Rise in aging population to drive demand for medications

- 11.4.3 INDIA

- 11.4.3.1 Large domestic consumption and export of generic drugs to drive market

- 11.4.4 SOUTH KOREA

- 11.4.4.1 Well-developed healthcare industry and presence of major pharmaceutical manufacturers to drive market

- 11.4.5 REST OF ASIA PACIFIC

- 11.4.1 CHINA

- 11.5 LATIN AMERICA

- 11.5.1 BRAZIL

- 11.5.1.1 Strong manufacturing ecosystem to boost market

- 11.5.2 MEXICO

- 11.5.2.1 Government initiatives in healthcare industry to fuel demand for pharmaceutical products

- 11.5.3 REST OF LATIN AMERICA

- 11.5.1 BRAZIL

- 11.6 MIDDLE EAST

- 11.6.1 GROWING FOCUS ON GENETIC MEDICINE DEVELOPMENT PROJECTS TO DRIVE GROWTH

- 11.6.2 GCC COUNTRIES

- 11.6.3 SAUDI ARABIA (KSA)

- 11.6.3.1 More comprehensive access to healthcare services to fuel demand for pharmaceuticals

- 11.6.4 UNITED ARAB EMIRATES (UAE)

- 11.6.4.1 Increasing initiatives for domestic pharmaceutical production to drive market

- 11.6.5 REST OF GCC COUNTRIES

- 11.6.6 REST OF MIDDLE EAST

- 11.7 AFRICA

- 11.7.1 GROWING COLLABORATIONS AND HIGH INCIDENCE OF DISEASES TO DRIVE MARKET

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN FILL-FINISH MANUFACTURING MARKET, 2023-2026

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS

- 12.5 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 12.5.1 STARS

- 12.5.2 EMERGING LEADERS

- 12.5.3 PERVASIVE PLAYERS

- 12.5.4 PARTICIPANTS

- 12.5.5 COMPETITIVE BENCHMARKING OF TOP PLAYERS, 2025

- 12.5.5.1 Company footprint

- 12.5.5.2 Region footprint

- 12.5.5.3 Product footprint

- 12.5.5.4 End-user footprint

- 12.6 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.6.1 PROGRESSIVE COMPANIES

- 12.6.2 RESPONSIVE COMPANIES

- 12.6.3 DYNAMIC COMPANIES

- 12.6.4 STARTING BLOCKS

- 12.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.6.5.1 Detailed list of key startups/SMEs

- 12.6.5.2 Competitive benchmarking of key startups/SMEs

- 12.7 VALUATION AND FINANCIAL METRICS OF FILL-FINISH MANUFACTURING MARKET VENDORS

- 12.7.1 FINANCIAL METRICS

- 12.7.2 COMPANY VALUATION

- 12.8 BRAND/PRODUCT COMPARISON

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 WEST PHARMACEUTICAL SERVICES, INC.

- 13.1.1.1 Business overview

- 13.1.1.2 Products/Services/Solutions offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches and approvals

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Key strengths/Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weaknesses & competitive threats

- 13.1.2 BECTON, DICKINSON, AND COMPANY

- 13.1.2.1 Business overview

- 13.1.2.2 Products/Services/Solutions offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches and approvals

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Key strengths/Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 SYNTEGON TECHNOLOGY GMBH

- 13.1.3.1 Business overview

- 13.1.3.2 Products/Services/Solutions offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches and approvals

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.3.4 Other developments

- 13.1.3.4 MnM view

- 13.1.3.4.1 Key strengths

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses & competitive threats

- 13.1.4 I.M.A. S.P.A.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Services/Solutions offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches and approvals

- 13.1.4.3.2 Deals

- 13.1.4.4 MnM view

- 13.1.4.4.1 Key strengths/Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses & competitive threats

- 13.1.5 STEVANATO GROUP S.P.A.

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Services/Solutions offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches and approvals

- 13.1.5.3.2 Deals

- 13.1.5.4 MnM view

- 13.1.5.4.1 Key strengths/Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses & competitive threats

- 13.1.6 GERRESHEIMER AG

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Services/Solutions offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches and approvals

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.7 APTARGROUP, INC.

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Services/Solutions offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Product launches and approvals

- 13.1.7.3.2 Deals

- 13.1.7.3.3 Expansions

- 13.1.8 DATWYLER HOLDING INC.

- 13.1.8.1 Business overview

- 13.1.8.2 Products/Services/Solutions offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches and approvals

- 13.1.8.3.2 Deals

- 13.1.9 DANAHER CORPORATION

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Services/Solutions offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Deals

- 13.1.10 OPTIMA

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Services/Solutions offered

- 13.1.10.3 Recent developments

- 13.1.10.3.1 Expansions

- 13.1.11 BAUSCH+STROBEL

- 13.1.11.1 Business overview

- 13.1.11.2 Products/Services/Solutions offered

- 13.1.11.3 Recent developments

- 13.1.11.3.1 Product launches and approvals

- 13.1.12 GRONINGER & CO. GMBH

- 13.1.12.1 Business overview

- 13.1.12.2 Products/Services/Solutions offered

- 13.1.12.3 Recent developments

- 13.1.12.3.1 Expansions

- 13.1.13 SGD PHARMA

- 13.1.13.1 Business overview

- 13.1.13.2 Products/Services/Solutions offered

- 13.1.13.3 Recent developments

- 13.1.13.3.1 Deals

- 13.1.13.3.2 Expansions

- 13.1.14 SCHOTT PHARMA AG & CO. KGAA

- 13.1.14.1 Business overview

- 13.1.14.2 Products/Services/Solutions offered

- 13.1.14.3 Recent developments

- 13.1.14.3.1 Product launches and approvals

- 13.1.14.3.2 Deals

- 13.1.14.3.3 Expansions

- 13.1.15 NIPRO CORPORATION

- 13.1.15.1 Business overview

- 13.1.15.2 Products/Services/Solutions offered

- 13.1.15.3 Recent developments

- 13.1.15.3.1 Product launches and approvals

- 13.1.15.3.2 Expansions

- 13.1.16 BAUSCH ADVANCED TECHNOLOGY GROUP

- 13.1.16.1 Business overview

- 13.1.16.2 Products/Services/Solutions offered

- 13.1.16.3 Recent developments

- 13.1.16.3.1 Deals

- 13.1.17 MAQUINARIA INDUSTRIAL DARA, S.L.

- 13.1.17.1 Business overview

- 13.1.17.2 Products/Services/Solutions offered

- 13.1.17.3 Recent developments

- 13.1.17.3.1 Product launches and approvals

- 13.1.17.3.2 Deals

- 13.1.1 WEST PHARMACEUTICAL SERVICES, INC.

- 13.2 OTHER PLAYERS

- 13.2.1 STERILINE S.R.L.

- 13.2.2 AUTOMATED SYSTEMS OF TACOMA, LLC

- 13.2.3 WEILER ENGINEERING, INC.

- 13.2.4 FEDEGARI AUTOCLAVI S.P.A.

- 13.2.5 SHANDONG PHARMACEUTICAL GLASS

- 13.2.6 MITSUBISHI GAS CHEMICAL

- 13.2.7 TERUMO CORPORATION

- 13.2.8 SKAN AG

- 13.2.9 ATS LIFE SCIENCE SYSTEMS

- 13.2.10 CORNING INC.

- 13.2.11 CREDENCE MEDSYSTEMS

- 13.2.12 3P INNOVATION LTD.

- 13.2.13 COLANAR AG.

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.2 PRIMARY DATA

- 14.2 MARKET ESTIMATION METHODOLOGY

- 14.2.1 MARKET SIZE ESTIMATION

- 14.2.2 INSIGHTS OF PRIMARY EXPERTS

- 14.2.3 TOP-DOWN APPROACH

- 14.3 MARKET GROWTH RATE PROJECTIONS

- 14.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RESEARCH LIMITATIONS

- 14.7 RISK ANALYSIS

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 CUSTOMIZATION OPTIONS

- 15.3 RELATED REPORTS

- 15.4 AUTHOR DETAILS