|

시장보고서

상품코드

2066567

완제 제조 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fill Finish Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

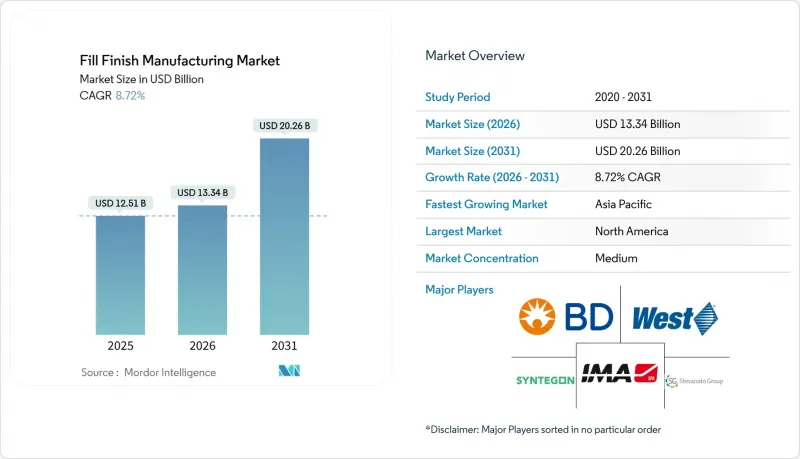

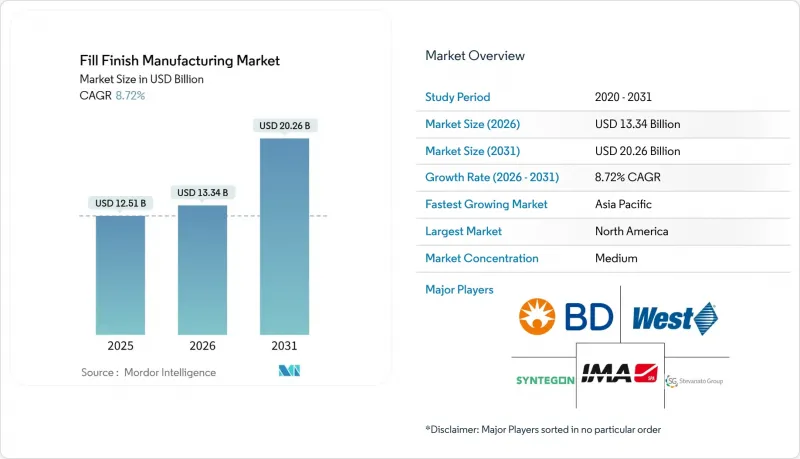

Mordor Intelligence에 의하면, 완제 제조 시장 규모는 2025년 125억 1,000만 달러로 평가되었습니다. 2026년에는 133억 4,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 8.72%로 성장을 지속하여, 2031년에는 202억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(소모품(프리필드 주사기, 카트리지, 바이알, 기타), 기기/시스템(독립형, 통합형, 자동화형, 반자동화/수동형)), 최종 사용자(CMO, 제약·바이오기술, 기타), 용기 소재(유리, 폴리머), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 완제 제조 시장 동향 및 인사이트

RTU 주사기 및 카트리지 분야의 기술 발전

RTU(즉시 사용형) 포맷을 통해 세척 및 열 제거 처리가 필요 없어져 생산 리드타임을 2-3일 단축할 수 있을 뿐만 아니라, 안정성 범위가 좁은 바이오의약품을 보호할 수 있습니다. 2024년에 출시된 SCHOTT사의 ‘syriQ BioPure’는 미리 멸균 처리된 유리 배럴을 출하하며, 일괄 세척된 부품에 비해 육안으로 확인되는 입자 혼입으로 인한 불량품을 40% 줄여줍니다. West Pharmaceutical사가 2025년에 출시할 ‘Daikyo Crystal Zenith’ 폴리머 카트리지는 1회 투여용 GLP-1 펜에서 발생하는 실리콘 오일 이온화 문제를 해결하고 있습니다. 장비 공급업체들도 이러한 전환을 지원하고 있습니다. 신테곤사의 ‘ALAsys’는 RTU(즉시 사용 가능) 네스트 처리를 통합하고, 전환 시간을 90분 미만으로 단축함으로써 연속 멸균 사이클이 필요 없는 다품종 대응의 유연성을 실현하고 있습니다. 완제 제조 시장에서 규제 기준이 강화되는 가운데, FDA와 EMA는 현재 RTU 용기를 부속서 1의 오염 관리 요건을 충족하기 위한 모범 사례로 간주하고 있으며, 이에 따라 CDMO와 자체 생산 시설 모두에서 RTU 용기의 도입이 가속화되고 있습니다.

CDMO/CMO로의 아웃소싱 증가

자본 집약적인 특성 때문에 혁신 기업들은 무균 제조 시설 건설을 주저하고 있습니다. 단일 고속 생산 라인의 총 비용은 1억 달러를 초과하기도 합니다. 삼성바이오로직스는 바이오시밀러 및 mRNA 백신 개발사들 수요를 확보하기 위해, 2025년까지 7억 4,000만 달러 규모로 진행될 인천 확장 계획에 4개의 필-피니시 라인을 추가했습니다. WuXi Biologics는 쑤저우 사업장을 12개의 무균 생산 라인으로 확충한 후, 아달리무맙 및 릿시맙 바이오시밀러와 관련된 세계 계약을 수주했습니다. Lonza의 4억 달러 규모의 포츠머스 프로젝트에서는 분당 400개 단위의 생산 능력을 갖춘 트윈 주사기 생산 라인이 도입되었는데, 이는 중규모 생명공학 기업에서는 재현할 수 없는 규모입니다. 이러한 투자를 통해 완제 제조 시장은 임상 파이프라인에서 발생하는 급증하는 생산량을 흡수하는 동시에, 규제 리스크를 전문 공급업체들 간에 분산시킬 수 있게 됩니다.

세계 각국의 엄격한 GMP 및 검증 비용

최신 개정안에서는 지속적인 환경 모니터링, 3회의 미디어 필터 시험 통과, 그리고 연례 재인증이 의무화되어 있으며, 이러한 조치에는 라인 1개당 연간 200만-500만 달러의 비용이 소요됩니다. 2024년 FDA 개정안에 따라 실시간 입자 동향 모니터링 기능이 추가됨에 따라, 각 기업은 아이솔레이터에 자동 샘플링 노드를 사후 장착하는 개조를 실시해야 하는 상황에 놓여 있습니다. 중국 국가의약품감독관리국(NMPA)은 국내 GMP를 ICH Q7에 부합하도록 조정했습니다. 이로 인해 소규모 CDMO 업체들은 도저히 구입할 수 없는 차압 경보 장치나 자가 세척식 아이솔레이터를 어쩔 수 없이 구입해야 하는 상황에 처해 있습니다. 검증 지연은 시장 출시까지의 기간을 연장시킵니다. 또한, 배지 충전 과정에서 단 한 개의 유닛에서라도 오염이 검출되면 18개월의 적합성 확인 일정이 초기화되어, 자원이 제한된 지역의 필-피니시 제조 시장의 성장세가 주춤해지고 있습니다.

부문별 분석

각 배치마다 새로운 바이알, 마개, 카트리지, 프리필드 주사기가 소모되기 때문에 2025년 매출의 62.81%를 소모품이 차지했습니다. 그러나 기기 및 시스템 분야의 완제 제조 시장 규모는 더욱 빠르게 확대되고 있으며, 연평균 성장률(CAGR) 9.50%로 성장을 지속하고, 있습니다. 이는 업계가 처리 능력과 규정 준수를 중시하고 있음을 반영합니다. 자동화된 모노블록 장비는 충전, 스토퍼 삽입, 캡핑 및 100% 육안 검사를 하나의 본체에 통합하여, 작업자의 개입이나 데이터 무결성 관련 위험을 줄여줍니다. Syntegon사의 ‘ALAsys’ 및 IMA사의 ‘Adapta’ 시리즈는 충전 정밀도 ±1%를 유지하면서 분당 400유닛 이상의 처리 능력을 발휘합니다. 각 CDMO 기업은 대형 제약사 스폰서로부터 생산 할당량을 확보하기 위해 이에 투자하고 있습니다. 반자동 설비는 인건비가 로봇 도입 비용보다 낮은 저소득 지역에서 여전히 사용되고 있지만, 인도와 중국에서 ICH 기준에 부합하는 GMP 규정이 도입됨에 따라 구매자들은 완전 자동화로 전환해 나갈 것입니다.

그렇긴 하지만, 완제 제조 시장에서 소모품은 여전히 필수적이며, 경기 침체의 영향을 덜 받는 분야입니다. GLP-1 주사제가 바이알에서 점차 전환됨에 따라 프리필드 주사기 시장 점유율이 확대되고 있는 반면, 만성 질환용 펜형 기기의 등장으로 카트리지 사용도 급증하고 있습니다. 이 공급업체는 배럴, 엘라스토머 플런저, 니들 쉴드를 한 세트로 묶은 다년 계약을 체결함으로써, 사실상 고객을 자사의 독자적인 생태계에 묶어두고 있습니다. 새로운 RTU 네스트 덕분에 라인 전환이 간소화되었습니다. 또한, SCHOTT사의 NxT 패키징은 부품 준비 시간을 50% 단축합니다. 이는 눈에 보이지 않는 중요한 장점이며, 생산 라인 가동률이 80%를 넘어서는 상황에서 특히 중요합니다. 현재, 지속가능성에 대한 고려가 부품 명세서(BOM)에 영향을 미치고 있습니다. 폐쇄형 순환 재활용 시스템을 제공하는 폴리머 공급업체는 ESG 스코어카드의 압박을 받고 있는 조달 팀으로부터 우선 공급업체로서의 지위를 누리고 있습니다.

지역별 분석

북미는 혁신적인 기업과 저명한 CDMO가 밀집해 있을 뿐만 아니라, 견고한 FDA 감사 체계 덕분에 2025년 전 세계 매출의 37.44%를 계속 차지했습니다. 이 지역에는 약 180개의 상업용 무균 생산 라인이 있는 것으로 추정되며, 그중 상당수는 95%의 가동률을 보장해야 하는 수직 통합형 대형 제약사의 캠퍼스 내에 설치되어 있습니다. 멕시코는 미국의 니어쇼어링 전략에 대응하기 위해 후아레스에서 주사기 생산 능력을 확충하고 있으며, 통관 지연 및 관세 위험을 줄이려 하고 있습니다. 캐나다의 성장은 완만하지만, 바이오시밀러에 중점을 두고 있습니다. 아포텍스와 파마사이언스의 두 신규 생산 라인은 2027년까지 총 연간 1억 2,000만 개의 프리필드 디바이스를 공급할 것으로 예측됩니다.

유럽에는 세계 최고 수준의 용기 공급업체가 존재하는 반면, 규제 환경은 복잡하게 얽혀 있습니다. 브렉시트 이후 규제 차이로 인해 MHRA와 EMA 양 기관의 검증 절차가 의무화됨에 따라, 다국적 CDMO 기업들은 독일이나 이탈리아와 같은 유럽 대륙의 허브 거점을 우선적으로 선택하고 있습니다. EU 폐기물 지침에 따라 폴리머를 많이 사용하는 사업의 운영 비용은 증가하고 있지만, 게레스하이머, 숏, 스테바나트 그룹은 사내 연구 개발을 활용하여 GMP 무균 기준과 환경 목표를 동시에 충족하는 재활용 가능한 플랫폼 개발을 주도하고 있습니다. 동유럽 국가들은 저비용 필피니시 거점으로서의 입지를 다져가고 있지만, 많은 국가에서는 여전히 미국 바이어들이 요구하는 검사 실적이 부족하여 대서양을 가로지르는 계약 체결이 지체되고 있습니다.

아시아태평양은 명백한 성장 동력이며, 연평균 성장률(CAGR) 9.82%로 지속적인 확장을 이어가고 있어, 완제 제조 시장의 기존 무역 경로에 점차 변화를 가져오고 있습니다. 중국 국가의약품감독관리국(NMPA)은 2024년부터 2025년에 걸쳐 23개의 바이오시밀러를 승인함으로써 우시 바이오로직스와 복성제약(Fosun Pharma)의 2억 달러 이상의 사업 확장을 뒷받침했습니다. 인도의 세람 인스티튜트는 연간 15억 회분 규모의 생산 능력을 갖춘 6개의 생산 라인을 구축하여, 소아마비 및 HPV 백신에 관한 GAVI의 조달을 주도하고 있습니다. 한국은 삼성바이오로직스와 SK바이오사이언스에 대한 공적 지원을 제공하고 있으며, 두 회사 모두 현지 로봇 공학 전문 지식을 활용하여 무인화(라이트아웃) 주사기 포장을 실현하고 있습니다. 일본에서는 고령화 사회에 대응하기 위해 장시간 작용형 주사제의 국내 생산 능력이 확대되고 있지만, PMDA의 엄격한 심사로 인해 한국이나 싱가포르에 비해 리드타임이 길어지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the fill finish manufacturing market size is expected to grow from USD 12.51 billion in 2025 to USD 13.34 billion in 2026 and is forecast to reach USD 20.26 billion by 2031 at 8.72% CAGR over 2026-2031.

This report is Segmented by Product Type (Consumables [Prefilled Syringes, Cartridges, Vials, Others], Instruments/Systems [Stand-Alone, Integrated, Automated, Semi-Automated/Manual]), End User (CMOs, Pharma & Biotech, Others), Container Material (Glass, Polymer), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Fill Finish Manufacturing Market Trends and Insights

Technological Advances in RTU Syringes & Cartridges

RTU formats eliminate washing and depyrogenation, trimming two to three days from production lead time and safeguarding biologics with narrow stability windows. SCHOTT's syriQ BioPure, launched in 2024, ships pre-sterilized glass barrels that cut visible-particulate rejects by 40% compared with bulk-washed components. West Pharmaceutical's expansion of Daikyo Crystal Zenith polymer cartridges in 2025 is solving silicone-oil migration challenges for single-dose GLP-1 pens. Equipment suppliers support the shift: Syntegon's ALAsys integrates RTU nest handling and reduces changeovers to under 90 minutes, enabling multi-product flexibility without serial sterilization cycles. As the Fill-Finish Manufacturing market tightens regulatory focus, the FDA and EMA now consider RTU containers a best-practice mitigation for Annex 1 contamination-control expectations, accelerating adoption by both CDMOs and captive plants.

Rising Outsourcing to CDMOs / CMOs

Capital intensity discourages innovators from building sterile suites; a single high-speed line can exceed USD 100 million in all-in costs. Samsung Biologics added four fill-finish lines during its USD 740 million Incheon expansion in 2025 to capture demand from biosimilar and mRNA vaccine sponsors. WuXi Biologics secured global contracts for adalimumab and rituximab biosimilars after upgrading its Suzhou site to 12 aseptic lines. Lonza's USD 400 million Portsmouth project introduced twin syringe lines rated at 400 units per minute, a scale that mid-sized biotech firms cannot replicate. These investments help the Fill-Finish Manufacturing market absorb surging volumes from clinical pipelines while spreading regulatory risk across specialized providers.

Stringent Global GMP & Validation Costs

Modern revisions mandate continuous environmental monitoring, three successful media fills, and annual requalification-regimens that cost USD 2 million to USD 5 million per line each year. FDA updates in 2024 added real-time particle trending, pushing firms to retrofit isolators with automated sampling nodes. China's NMPA aligned domestic GMP with ICH Q7, compelling small CDMOs to buy differential-pressure alarms and self-cleaning isolators they can scarcely afford. Validation delays lengthen time-to-market; any contaminated unit during media fills resets the 18-month qualification calendar, dampening Fill-Finish Manufacturing market momentum in resource-constrained regions.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Biologics & Injectable Pipeline

- Sustainability Push for Recyclable Polymer Components

- High CAPEX for Aseptic Fill-Finish Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumables anchored 62.81% of 2025 revenue because every batch consumes fresh vials, stoppers, cartridges, and prefilled syringes. Yet the Fill-Finish Manufacturing market size for instruments and systems is expanding faster, clocking a 9.50% CAGR that reflects industry fixation on throughput and compliance. Automated monoblocs integrate filling, stoppering, capping, and 100% vision inspection in one housing, curbing operator intervention and data-integrity risks. Syntegon's ALAsys and IMA's Adapta lines clock 400-plus units per minute while maintaining +-1% fill accuracy; CDMOs invest here to assure slot reservations from big pharma sponsors. Semi-automated equipment lingers in low-income geographies where labor costs undercut robotics, but incoming ICH-aligned GMP rules in India and China will nudge buyers toward full automation.

Consumables nonetheless remain indispensable and recession-resistant within the Fill-Finish Manufacturing market. Prefilled syringes are gaining share as GLP-1 injectables migrate from vials, while cartridge usage is ballooning on the back of pen devices for chronic diseases. Suppliers secure multi-year contracts bundling barrels, elastomer plungers, and needle shields, effectively locking customers into proprietary ecosystems. New RTU nests simplify line changeovers; SCHOTT's NxT packaging reduces component prep time by 50%, an intangible yet important benefit as line-utilization targets creep past 80%. Sustainability considerations now influence bill-of-materials: polymer suppliers offering closed-loop recycling enjoy preferred-supplier status with procurement teams under ESG scorecard pressure.

Geography Analysis

North America retained 37.44% of global billings in 2025 thanks to its dense cluster of innovators, marquee CDMOs, and a robust FDA inspection framework. The region hosts an estimated 180 commercial aseptic lines, many embedded in vertically integrated big-pharma campuses that demand 95% runtime reliability. Mexico is building syringe capacity in Juarez to serve U.S. near-shoring strategies, trimming customs delays and tariff risk. Canada's growth is modest but focused on biosimilars; two new lines at Apotex and Pharmascience will collectively deliver 120 million prefilled devices per year by 2027.

Europe combines world-class container suppliers with complex regulatory dynamics. Post-Brexit divergence forces dual MHRA and EMA validations, nudging multinational CDMOs to favor continental hubs in Germany and Italy. The EU waste directive increases operating expenses for polymer-heavy operations, yet Gerresheimer, SCHOTT, and Stevanato Group leverage in-house R&D to pioneer recyclable platforms that square GMP sterility with environmental targets. Eastern European nations position themselves as lower-cost fill-finish nodes, yet many still lack the inspection history demanded by U.S. buyers, stalling cross-Atlantic contracts.

Asia-Pacific is the clear growth engine, advancing at an 9.82% CAGR and gradually disrupting established trade routes in the Fill-Finish Manufacturing market. China's NMPA cleared 23 biosimilars over 2024-2025, catalyzing USD 200 million-plus expansions at WuXi Biologics and Fosun Pharma. India's Serum Institute readied six lines capable of 1.5 billion doses annually, anchoring GAVI procurement for polio and HPV. South Korea funnels public incentives into Samsung Biologics and SK Bioscience, both of which embed local robotics expertise for lights-out syringe packaging. Japan's demographic focus on aging spurs in-country capacity for long-acting injectables, though its stringent PMDA validation extends lead times relative to Korea and Singapore.

- Aptar

- Bausch+Strobel

- Beckton Dickinson

- Corning

- Daikyo Seiko Ltd.

- FUJIFILM

- Gerresheimer

- Groninger & Co. GmbH

- IMA S.p.A.

- Marchesini Group S.p.A.

- Nipro

- Novo Nordisk A/S (Catalent, Inc.)

- OPTIMA Packaging Group GmbH

- Owen Mumford Pharmaceutical Services (UK)

- SCHOTT

- SGD Pharma

- Stevanato Group

- Syntegon Technology

- Thermo Fisher Scientific (Patheon)

- West Pharmaceutical Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Technological advances in RTU syringes & cartridges

- 4.2.2 Rising outsourcing to CDMOs / CMOs

- 4.2.3 Expanding biologics & injectable pipeline

- 4.2.4 Sustainability push for recyclable polymer components

- 4.2.5 Modular micro-batch isolator systems for cell & gene therapies

- 4.2.6 AI-driven predictive maintenance of fill-finish lines

- 4.3 Market Restraints

- 4.3.1 Stringent global GMP & validation costs

- 4.3.2 High CAPEX for aseptic fill-finish lines

- 4.3.3 EU plastics-waste regulation on single-use disposables

- 4.3.4 Talent shortage for advanced-therapy micro-batch lines

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Consumables

- 5.1.1.1 Prefilled Syringes

- 5.1.1.2 Cartridges

- 5.1.1.3 Vials

- 5.1.1.4 Others

- 5.1.2 Instruments / Systems

- 5.1.2.1 Stand-Alone Systems

- 5.1.2.2 Integrated Lines

- 5.1.2.3 Automated Machines

- 5.1.2.4 Semi-Automated / Manual Machines

- 5.1.1 Consumables

- 5.2 By End User

- 5.2.1 Contract Manufacturing Organizations

- 5.2.2 Pharmaceutical & Biotechnology Firms

- 5.2.3 Others

- 5.3 By Container Material

- 5.3.1 Glass

- 5.3.2 Polymer (COP/COC & other plastics)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Aptar

- 6.3.2 Bausch+Strobel

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Corning Incorporated

- 6.3.5 Daikyo Seiko Ltd.

- 6.3.6 FUJIFILM Diosynth Biotechnologies

- 6.3.7 Gerresheimer AG

- 6.3.8 Groninger & Co. GmbH

- 6.3.9 IMA S.p.A.

- 6.3.10 Marchesini Group S.p.A.

- 6.3.11 Nipro Corporation

- 6.3.12 Novo Nordisk A/S (Catalent, Inc.)

- 6.3.13 OPTIMA Packaging Group GmbH

- 6.3.14 Owen Mumford Pharmaceutical Services (UK)

- 6.3.15 SCHOTT AG

- 6.3.16 SGD Pharma

- 6.3.17 Stevanato Group

- 6.3.18 Syntegon Technology GmbH

- 6.3.19 Thermo Fisher Scientific (Patheon)

- 6.3.20 West Pharmaceutical Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment