|

시장보고서

상품코드

2076875

구역별 자율 제어 시장 : 그리드 자동화 시스템, 엣지 인텔리전스 및 엣지 제어 시스템, 데이터 관리 및 제어 플랫폼, 발전, 송전, 배전, 석유 및 가스, 데이터센터, 방위, 금속 및 광업별 - 세계 예측(-2032년)Zonal Autonomous Control Market by Grid Automation Systems, Edge Intelligence & Edge Control Systems, Data Management & Control Platforms, Generation, Transmission, Distribution, Oil & Gas, Data Center, Defense, Metal & Mining - Global Forecast to 2032 |

||||||

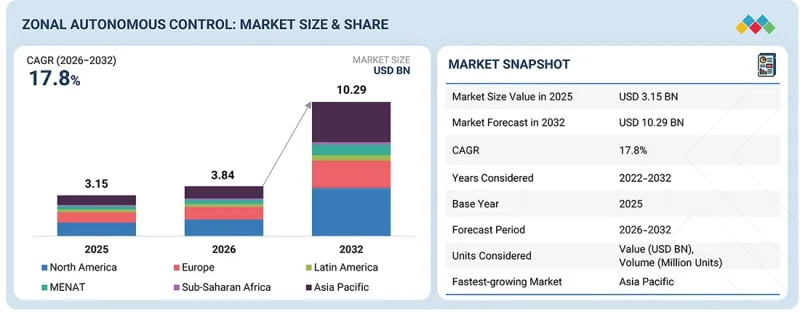

세계의 구역별 자율 제어 시장 규모는 2026년 38억 4,000만 달러에서 2032년에는 102억 9,000만 달러에 달할 것으로 추정되며, CAGR은 17.8%를 기록할 전망입니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2032년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2032년 |

| 단위 | 금액(달러) |

| 부문 | 솔루션 유형, 용도, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 기타 지역 |

노후화된 전력 인프라의 현대화가 진행되는 가운데, 송전망의 신뢰성, 기후 관련 장애, 재생에너지 통합에 대한 우려가 커지면서 구역별 자율 제어(ZAC) 시스템의 도입이 크게 확대되고 있습니다. 전력 회사는 운영의 연속성을 높이고, 자가 복구 기능을 구현하며, 분산형 에너지 자원을 관리하고, 실시간 분산형 의사결정을 지원하기 위해 지능형 송전망 자동화 기술에 대한 투자를 확대하고 있습니다. 또한, 전기화의 진전, 이상 기후, 전력 소비 증가를 배경으로 회복탄력성과 유연성을 갖춘 송전망 운영에 대한 수요가 높아짐에 따라, 송전, 배전, 산업용 에너지 네트워크 전반에 걸쳐 자율 제어 플랫폼의 도입이 가속화되고 있습니다.

"발전 부문에서는 재생에너지 부문이 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다."

발전 부문에서 재생에너지는 주로 전 세계가 청정하고 분산형 에너지 시스템으로의 전환을 가속화하고 있는 만큼, 예측 기간 동안 가장 높은 연평균 성장률(CAGR)을 기록할 것으로 전망됩니다. 태양광, 풍력 및 기타 분산형 에너지 자원(DER)의 통합이 진행됨에 따라, 전력계의 변동성, 간헐성 및 양방향 전력 흐름을 관리하기 위한 첨단 구역별 자율 제어 솔루션의 필요성이 높아지고 있습니다. 전 세계 정부와 규제 당국은 엄격한 탈탄소화 목표와 재생에너지 도입 의무를 도입하고 있으며, 이로 인해 전력망 현대화 및 지능형 제어 시스템에 대한 투자가 더욱 촉진되고 있습니다. 또한, 마이크로그리드, 에너지 저장 시스템, 프로슈머(생산자 겸 소비자) 기반의 에너지 모델 도입이 확대됨에 따라 송전망 운영이 복잡해지고 있으며, 구역 단위에서 실시간으로 지역 밀착형 자율 제어가 요구되고 있습니다. 그 결과, 전력 사업자들은 송전망의 유연성, 안정성 및 효율성을 높이기 위해 ZAC 솔루션 도입을 확대하고 있으며, 재생에너지 통합 분야가 가장 빠르게 성장하고 있는 부문이 되었습니다.

"산업 부문에서는 데이터센터 부문이 2032년까지 가장 큰 시장 점유율을 차지할 것으로 예측됩니다."

클라우드 컴퓨팅, AI 워크로드, 하이퍼스케일 데이터 처리 요구 사항에 힘입어 디지털 인프라가 급속히 확대됨에 따라, 데이터센터의 최종사용자 부문이 2032년까지 가장 큰 시장 점유율을 차지할 것으로 전망됩니다. 데이터센터는 신뢰성이 높고 중단 없는 효율적인 전력 공급이 필요하기 때문에 그리드 에지에서 실시간 모니터링, 장애 파악, 에너지 최적화를 위한 첨단 구역별 자율 제어 솔루션을 조기에 도입하고 있습니다. 데이터센터 내 재생에너지원 및 현장 발전(마이크로그리드, 에너지 저장 시스템 등)의 도입이 증가함에 따라, 복잡한 전력 흐름을 관리하고 전력망의 안정성을 확보하기 위한 지능형 제어 시스템에 대한 필요성이 더욱 커지고 있습니다. 또한, 가동 시간, 내결함성, 에너지 효율에 대한 엄격한 요구 사항과 더불어 하이퍼스케일 사업자들의 투자 증가가 맞물리면서, 자동화된 분산형 그리드 제어 기술의 도입이 가속화되고 있습니다. 그 결과, 데이터센터 부문은 ZAC 솔루션에 대한 수요를 지속적으로 견인하며, 예측 기간 동안 가장 큰 시장 점유율을 확보하고 있습니다.

"2025년에는 북미가 가장 큰 시장 점유율을 차지했습니다."

북미는 선진적인 전력망 인프라, 스마트 그리드 기술의 조기 도입, 주요 기술 공급업체들의 강력한 입지 덕분에 2025년 시장에서 가장 큰 시장 점유율을 차지했습니다. 해당 지역에서는 정부의 지원 정책과 규제 체계에 힘입어 전력망의 현대화, 디지털화, 분산형 에너지 자원(DER) 통합을 위한 막대한 투자가 이루어져 왔습니다. 또한, 재생에너지 프로젝트, 데이터센터, 전기화 이니셔티브의 급속한 확대로 인해 지능형 분산형 전력망 제어 솔루션에 대한 수요가 증가하고 있습니다. 미국과 캐나다의 전력 회사들은 전력망의 신뢰성, 복원력 및 운영 효율성을 높이기 위해 AI를 활용한 전력망 관리 시스템, DERMS, 엣지 제어 기술을 적극적으로 도입하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 2025년 전 세계 ZAC 시장에서 북미가 가장 큰 비중을 차지하고 있습니다.

본 보고서에서는 전 세계 구역별 자율 제어 시장을 조사하여, 시장 개요, 시장 성장에 영향을 미치는 다양한 요인에 대한 분석, 기술 및 특허 동향, 법규제 환경, 사례 연구, 시장 규모 추정 및 전망, 각종 분류·지역/주요 국가별 상세 분석, 경쟁 구도, 주요 기업 개요 등을 정리하고 있습니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제4장 시장 평가

제5장 구역별 자율 제어 시장 : 지역별

제6장 경쟁 구도

제7장 기업 개요

제8장 조사 방법

제9장 부록

KSM 26.07.10The global zonal autonomous control market is estimated to reach USD 10.29 billion by 2032 from USD 3.84 billion in 2026, registering a CAGR of 17.8%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2032 |

| Base Year | 2025 |

| Forecast Period | 2026-2032 |

| Units Considered | Value (USD Billion) |

| Segments | By Solution Type, Application and Region |

| Regions covered | North America, Europe, APAC, RoW |

The increasing modernization of aging power infrastructure, combined with rising concerns over grid reliability, climate-related disruptions, and renewable energy integration, is significantly driving the adoption of zonal autonomous control (ZAC) systems. Utilities are increasingly investing in intelligent grid automation technologies to improve operational continuity, enable self-healing capabilities, manage distributed energy resources, and support real-time decentralized decision-making. In addition, the growing demand for resilient and flexible grid operations amid electrification, extreme weather events, and rising power consumption is accelerating the deployment of autonomous control platforms across transmission, distribution, and industrial energy networks.

"Renewable end use of the generation segment projected to grow at the highest CAGR during the forecast period"

The renewable end-use of generation segment is projected to grow at the highest CAGR during the forecast period, primarily due to the accelerating global transition toward clean and decentralized energy systems. Increasing integration of solar, wind, and other distributed energy resources (DERs) is driving the need for advanced zonal autonomous control solutions to manage grid variability, intermittency, and bidirectional power flows. Governments and regulators worldwide are implementing stringent decarbonization targets and renewable energy mandates, further boosting investments in grid modernization and intelligent control systems. Additionally, the rising deployment of microgrids, energy storage systems, and prosumer-based energy models is increasing the complexity of grid operations, thereby necessitating real-time, localized, and autonomous control at the zonal level. As a result, utilities are increasingly adopting ZAC solutions to enhance grid flexibility, stability, and efficiency, making renewable energy integration the fastest-growing application segment.

"Data center end use of industries segment projected to hold the largest market share by 2032"

The data center end-use segment is projected to hold the largest market share by 2032 due to the rapid expansion of digital infrastructure driven by cloud computing, AI workloads, and hyperscale data processing requirements. Data centers demand highly reliable, uninterrupted, and efficient power supply, making them early adopters of advanced zonal autonomous control solutions for real-time monitoring, fault isolation, and energy optimization at the grid edge. The increasing deployment of renewable energy sources and on-site generation (such as microgrids and energy storage systems) within data centers further necessitates intelligent control systems to manage complex power flows and ensure grid stability. Additionally, stringent requirements for uptime, resilience, and energy efficiency, coupled with rising investments by hyperscale operators, are accelerating the adoption of automated, decentralized grid control technologies. As a result, the data center segment continues to dominate demand for ZAC solutions, securing the largest market share over the forecast period.

"North America held the largest market share in 2025"

North America held the largest market share in the zonal autonomous control (ZAC) market in 2025 due to its advanced grid infrastructure, early adoption of smart grid technologies, and strong presence of leading technology providers. The region has witnessed significant investments in grid modernization, digitalization, and integration of distributed energy resources (DERs), driven by supportive government policies and regulatory frameworks. Additionally, the rapid growth of renewable energy projects, data centers, and electrification initiatives has increased the need for intelligent, decentralized grid control solutions. Utilities across the US and Canada are actively deploying AI-driven grid management systems, DERMS, and edge control technologies to enhance grid reliability, resilience, and operational efficiency. These factors collectively position North America as the leading contributor to the global ZAC market in 2025.

The breakdown of the profile of primary participants in the home automation system market is as follows:

- By Company Type: Tier 1 - 52%, Tier 2 - 28%, Tier 3 - 20%

- By Designation: C-level Executives - 24%, Directors - 33%, Others - 43%

- By Region: Asia Pacific - 38%, Europe - 27%, North America - 22%, MENAT - 5%, Latin America - 4%, and Sub-Saharan Africa - 4%

Note: Other designations include sales, marketing, and product managers.

The three tiers of the companies are based on their total revenues as of 2024: Tier 1: >USD 1 billion, Tier 2: USD 500 million-1 billion, and Tier 3: USD 500 million.

The zonal autonomous control market is dominated by a few globally established players such as GE Vernova, Schneider Electric, Siemens, Hitachi Energy Ltd, Landis+Gyr, ABB, S&C Electric Company, Honeywell International Inc, Smarter Grid Solutions, Inc., Itron Inc., gridX, Oracle, and Eaton. The study includes an in-depth competitive analysis of these key players in the home automation system market, with their company profiles, recent developments, and key market strategies.

Research Coverage

The report segments the zonal autonomous control market and forecasts its size by solution type, application, end use, and region. It also provides a comprehensive review of drivers, restraints, opportunities, and challenges influencing market growth. The report covers both qualitative and quantitative aspects of the market.

Reasons to Buy the Report:

The report will help leaders/new entrants in this market by providing approximate revenue figures for the overall zonal autonomous control market and related segments. This report will help stakeholders understand the competitive landscape and gain deeper insights to strengthen their market position and plan effective go-to-market strategies. The report will also help stakeholders understand the market pulse and provide information on key drivers, restraints, opportunities, and challenges.

The report provides insights into the following pointers:

- Analysis of key drivers (rising electrification & EV infrastructure expansion); restraints (legacy infrastructure incompatibility); opportunities (AI-driven edge intelligence & autonomous decision-making convergence); challenges (cybersecurity vulnerabilities & autonomous control governance risks)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product launches in the zonal autonomous control market

- Market Development: Comprehensive information about lucrative markets by analyzing the zonal autonomous control market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the zonal autonomous control market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like GE Vernova, Schneider Electric, Siemens, Hitachi Energy Ltd, Landis+Gyr, ABB, S&C Electric Company, Honeywell International Inc, Smarter Grid Solutions, Inc., Itron Inc., gridX, Oracle, and Eaton are some of the key players in the zonal autonomous control market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 OBJECTIVE

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.4 INCLUSION AND EXCLUSION

2 EXECUTIVE SUMMARY AND PREMIUM INSIGHTS

3 MARKET OVERVIEW AND DYNAMICS

- 3.1 INTRODUCTION

- 3.2 MARKET DYNAMICS

- 3.2.1 DRIVERS

- 3.2.2 RESTRAINTS

- 3.2.3 OPPORTUNITIES

- 3.2.4 CHALLENGES

- 3.3 VALUE CHAIN ANALYSIS

- 3.4 ECOSYSTEM ANALYSIS

- 3.5 CASE STUDY ANALYSIS

- 3.6 REGULATORY LANDSCAPE

4 MARKET ASSESSMENT

- 4.1 ZONAL AUTONOMOUS CONTROL MARKET, BY SOLUTION TYPE

- 4.1.1 INTRODUCTION

- 4.1.2 GRID AUTOMATION SYSTEMS

- 4.1.3 EDGE INTELLIGENCE & CONTROL SYSTEMS

- 4.1.4 DATA MANAGEMENT & CONTROL PLATFORMS

- 4.2 ZONAL AUTONOMOUS CONTROL MARKET, BY APPLICATION

- 4.2.1 INTRODUCTION

- 4.2.2 SUBSTATION MONITORING & OPERATIONS

- 4.2.3 ASSET MANAGEMENT

- 4.2.4 EDGE MANAGEMENT

- 4.2.5 CYBERSECURITY & THREAT DETECTION

- 4.3 ZONAL AUTONOMOUS CONTROL MARKET, BY END USE

- 4.3.1 INTRODUCTION

- 4.3.2 GENERATION

- 4.3.2.1 Conventional

- 4.3.2.2 Renewable

- 4.3.3 TRANSMISSION

- 4.3.4 DISTRIBUTION

- 4.3.5 INDUSTRIES

- 4.3.5.1 Oil & Gas

- 4.3.5.2 Data Centers

- 4.3.5.3 Defense

- 4.3.5.4 Manufacturing

- 4.3.5.5 Metals & Mining

- 4.3.5.6 Other Industries

5 ZONAL AUTONOMOUS CONTROL MARKET, BY REGION

- 5.1 INTRODUCTION

- 5.2 NORTH AMERICA

- 5.2.1.1 US

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 EUROPE

- 5.2.2.1 Germany

- 5.2.2.2 UK

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 LATIN AMERICA

- 5.2.3.1 Brazil

- 5.2.3.2 Argentina

- 5.2.3.3 Chile

- 5.2.3.4 Rest of LATAM

- 5.2.4 MIDDLE EAST, NORTH AFRICA & TURKEY

- 5.2.4.1 GCC Countries

- 5.2.4.1.1 Saudi Arabia

- 5.2.4.1.2 UAE

- 5.2.4.1.3 Rest of GCC Countries

- 5.2.4.2 Turkey

- 5.2.4.3 North Africa

- 5.2.4.4 Rest of Middle East, North Africa & Turkey

- 5.2.4.1 GCC Countries

- 5.2.5 SUB-SAHARAN AFRICA

- 5.2.5.1 South Africa

- 5.2.5.2 Nigeria

- 5.2.5.3 Rest of Sub-Saharan Africa

- 5.2.6 ASIA PACIFIC

- 5.2.6.1 India

- 5.2.6.2 China

- 5.2.6.3 Oceania

- 5.2.6.3.1 Australia

- 5.2.6.3.2 New Zealand

- 5.2.6.4 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 OVERVIEW

- 6.2 REVENUE ANALYSIS

- 6.3 MARKET SHARE ANALYSIS

- 6.4 CAPABILITY BENCHMARKING OF PLAYERS: BASED ON PRODUCT FOOTPRINT AND BUSINESS STRATEGY

- 6.4.1 STARS

- 6.4.2 EMERGING LEADERS

- 6.4.3 PERVASIVE PLAYERS

- 6.4.4 PARTICIPANTS

- 6.4.5 COMPANY FOOTPRINT

- 6.4.5.1 Solution Type Footprint

- 6.4.5.2 Application Footprint

- 6.4.5.3 End Use Footprint

- 6.4.5.4 Region Footprint

- 6.4.6 COMPETITIVE SCENARIO

- 6.4.7 PRODUCT LAUNCHES

- 6.4.7.1 Deals

7 COMPANY PROFILES

- 7.1 INTRODUCTION

- 7.2 KEY PLAYERS

- 7.2.1 GE VERNOVA

- 7.2.2 SCHNEIDER ELECTRIC

- 7.2.3 SIEMENS

- 7.2.4 HITACHI ENERGY LTD

- 7.2.5 LANDIS+GYR

- 7.2.6 ABB

- 7.2.7 S&C ELECTRIC COMPANY

- 7.2.8 MITSUBISHI CORPORATION

- 7.2.9 ITRON INC.

- 7.2.10 HONEYWELL INTERNATIONAL INC.

- 7.3 OTHER PLAYERS

- 7.3.1 ORACLE

- 7.3.2 EATON CORPORATION PLC

- 7.3.3 SCHWEITZER ENGINEERING LABORATORIES, INC.

- 7.3.4 SURVALENT TECHNOLOGY CORPORATION

- 7.3.5 GRIDX GMBH

- 7.3.6 G&W ELECTRIC

- 7.3.7 PSI SOFTWARE SE

- 7.3.8 EMERSON ELECTRIC CO.