|

시장보고서

상품코드

2043852

자동차용 전자제어장치 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Automotive Electronic Control Unit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

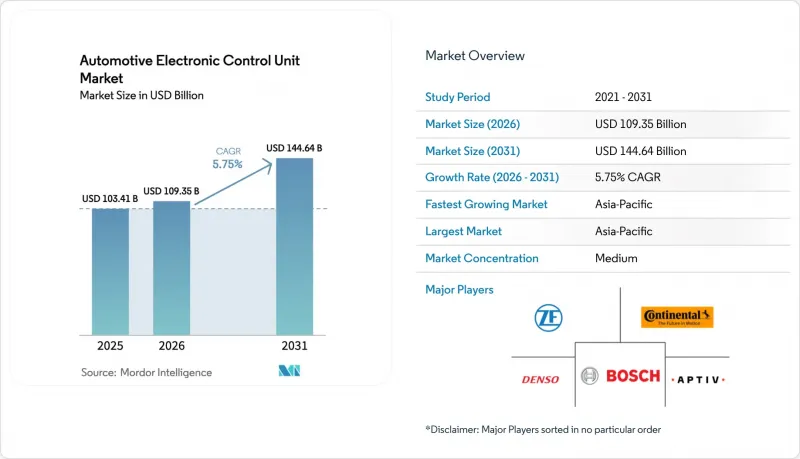

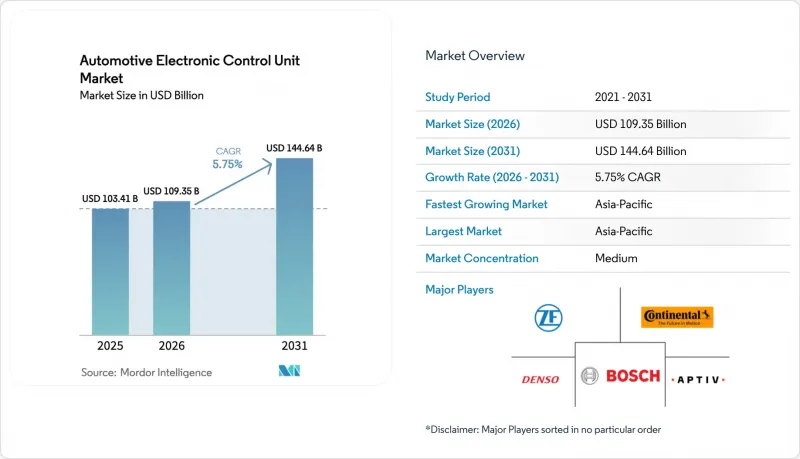

2026년 자동차용 전자제어장치(ECU) 시장 규모는 1,093억 5,000만 달러에 달할 것으로 예상됩니다. 2025년 1,034억 1,000만 달러에서 성장하여 2031년에는 1,446억 4,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.75%를 나타낼 것으로 전망됩니다.

주요 성장 요인으로는 첨단운전자보조시스템(ADAS) 규제 기한, 승용차 및 상용차의 급속한 전동화, 중앙집중식 차량 아키텍처로의 전환 등을 꼽을 수 있습니다. 배터리 전기자동차(BEV)는 배터리, 인버터, 차량용 충전기, 열 관리 등 여러 가지 새로운 제어 영역이 필요해 차량당 반도체 부품 비용이 증가하고 있습니다.

세계의 자동차 전자제어장치(ECU) 시장 동향 및 인사이트

전동화 물결로 차량당 ECU 수가 증가합니다.

배터리식 전기 파워트레인에는 배터리 관리, 인버터 로직, 충전 협상, 회생제동 등을 위한 전용 제어 유닛이 도입됩니다. 각 기능은 기존 내연기관 플랫폼에 필요하지 않은 처리 부하를 추가하고, 대당 반도체 비용은 2019년 420달러에서 2030년까지 1,350달러에 달할 것으로 예상되고 있습니다. 하이브리드 구성에서는 두 추진원을 원활하게 연동하는 알고리즘이 필요하기 때문에 통합의 복잡성이 증가합니다. 커민스에 따르면, 자사의 전자식 파워트레인 제어 모듈은 디젤, 수소, 천연가스 및 완전 전기 시스템을 최적화하고 있으며, 이는 다양한 연료 전략이 ECU의 탑재량을 계속 높은 수준으로 유지할 것으로 예상하고 있습니다. 그 결과, 자동차 ECU 시장은 OEM이 새로운 배터리 전기자동차나 연료전지 프로그램을 출시할 때마다 그 규모가 확대되고 있습니다.

미국, EU, 중국의 ADAS 의무화, 수요 증가로 수요 증가

유럽연합(EU)은 2024년 7월 개정된 일반 안전 규정을 발효하여 모든 신차에 지능형 속도 보조, 자동 긴급 제동, 후방 감지 기능 탑재를 의무화했습니다. 중국의 '스마트 커넥티드카' 규제에 따라 2024년 상반기 신차 승용차 판매에서 레벨2 기능의 보급률은 42.4%에 달했으며, NHTSA(미국 도로교통안전국)도 북미에 유사한 ADAS 규제를 추진하고 있습니다. 각 규정에는 실시간 센서 융합과 기능 안전 진단이 가능한 고신뢰성 컨트롤러가 필요합니다. 이에 따른 수요 증가는 자동차 ECU 시장으로 직결됩니다.

세계 반도체 공급 변동

자동차 ECU는 여전히 성숙된 90nm 이상의 공정 기술에 의존하고 있으며, 이 노드급에서 세계 웨이퍼 공급 능력은 만성적으로 부족합니다. VDA의 추산에 따르면, 자동차 제조업체의 반도체 수요는 2030년까지 3배 증가할 것으로 예상되지만, 전체 반도체 생산량에서 차지하는 비중은 8%에서 14%까지만 증가할 것으로 예측됩니다. 공급업체는 파운드리 생산 라인을 구세대 공정 노드로 쉽게 전환 할 수 없기 때문에 최첨단 공정공급이 개선되어도 공급 부족은 해소되지 않습니다. 지멘스는 실리콘이 완성되기 전에 소프트웨어 팀이 ECU 코드를 검증할 수 있는 모델 기반 검증을 추진하고 있으며, 이를 통해 물리적 칩 부족의 영향을 어느 정도 완화하고 있습니다. 그럼에도 불구하고 공급 부족은 전체 차량 출시를 지연시킬 수 있으며, 이는 자동차 전자제어장치 시장의 CAGR을 낮추는 요인으로 작용할 수 있습니다.

부문 분석

2025년에는 내연기관 플랫폼이 자동차 ECU 시장 점유율의 60.78%를 차지했지만, 2026년부터 2031년까지 배터리 전기차가 6.51%의 가장 높은 CAGR로 성장할 것으로 예측됩니다. 대형차 부문은 이러한 추세를 더욱 가속화하고 있습니다. 2024년 전 세계 전기 트럭 등록 대수는 80% 가까이 급증할 것으로 예상되며, 중국에서는 430여 종의 배터리식 대형 전기 트럭이 출시되었습니다. 커민스는 디젤에서 수소, 심지어 완전한 배터리 팩까지 적응할 수 있는 유연한 제어 펌웨어를 강조하며, 추진 시스템의 다양화가 어떻게 코드의 복잡성과 ECU의 총 수요를 증가시키는지 보여주고 있습니다.

반면, 내연기관 플랫폼의 경우 배출가스 규제가 연식별로 강화됨에 따라 엔진 관리 유닛에 대한 대량 주문이 이어지고 있습니다. 2024년에 공표된 유로 7 규정은 미립자 물질 필터와 배터리 내구성에 대한 차량 내 모니터링을 의무화하고, 기존 파워트레인 ECU에 새로운 진단 채널을 추가했습니다. 따라서 OEM들은 지난 10년간 연소 제어의 견고성을 유지하면서 하이브리드 및 순수 전기차(EV) 프로그램을 위한 전자 제어 기능을 단계적으로 추가하는 듀얼 플랫폼 전략에 직면해 있습니다. 이러한 상충되는 요구 사항으로 인해 파워트레인 아키텍처가 분화되는 가운데서도 자동차 전자제어장치 시장에서는 꾸준한 매출 증가가 예상됩니다.

2025년에는 파워트레인 컨트롤러가 시장 점유율의 40.92%를 차지했습니다. 내연기관차, 하이브리드 자동차, 순수 전기자동차 등 모든 자동차는 토크, 열, 에너지 관리가 필요하기 때문입니다. 한편, ADAS 및 안전 컨트롤러는 CAGR 4.27%로 성장하고 있으며, 자동차 전자제어장치 시장 혁신의 주력으로 부상하고 있습니다. 유럽의 일반 안전 규정과 중국의 스마트 커넥티드카 가이드라인은 자동 긴급 제동, 운전자 모니터링 카메라, 지능형 속도 보조 등의 기능을 의무화하고 있으며, 각각 전용 고 대역폭 마이크로컨트롤러에 의존하고 있습니다. LiDAR와 레이더의 가격이 하락함에 따라 센서 융합의 부하가 증가함에 따라 64비트 멀티코어 프로세서에 대한 수요가 증가하고 있습니다.

차체, 컴포트, 조명의 서브시스템은 전통적인 영역이 어떻게 진화하고 있는지를 보여줍니다. 현재는 윈도우, HVAC, 시트 모터를 위한 여러 개의 독립적인 박스가 존 컨트롤러로 대체되고 있습니다. 인포테인먼트 및 텔레매틱스는 여전히 시장 점유율이 가장 작은 분야이지만, OTA 서비스와 구독 모델의 확산으로 OEM 업체들은 헤드유닛을 기가헤르츠급 시스템온칩(SoC)으로 업그레이드할 수밖에 없는 상황입니다. 안전 규제와 디지털 서비스 수익이라는 두 가지 요인이 결합하여 파워트레인 시장의 포화 이후에도 자동차 전자제어장치(ECU) 시장은 지속적으로 성장할 여지가 있습니다.

자동차 전자제어장치 시장은 추진방식(내연기관, 하이브리드, 배터리 전기차), 용도(ADAS 및 안전시스템 등), ECU 용량(16비트 ECU, 32비트 ECU, 64비트 ECU), 자율주행 수준(기존(L0-L1 등), 차종(승용차 등), 지역별로 세분화되어 있습니다.), 지역별로 구분되어 있습니다. 시장 예측은 금액(USD) 및 수량(대수)으로 제공됩니다.

지역별 분석

아시아태평양은 중국의 스마트 커넥티드카 로드맵과 국내 반도체 공급망에서의 확고한 우위를 바탕으로 2025년 시장 점유율 48.29%를 차지하며 CAGR 7.72%로 확대되었습니다. 레벨 2의 보급률이 40%를 넘어선 것은 이 지역이 새로운 제어 영역을 얼마나 빠르게 채택하고 있는지를 보여주며, 중국 자동차 제조업체들은 2024년에만 430개 이상의 배터리 전기 트럭을 출시하였습니다. 일본과 한국은 자율주행 관련 통일된 법규로 인해 추진력을 얻고 있는 반면, 인도의 생산 연동형 인센티브 제도는 인도를 미래형 전자기기 제조 거점으로 자리매김하고 있습니다. 이러한 조치들이 결합되어 풍부한 ECU 계약 파이프라인을 보장하고, 자동차 ECU 시장에서 아시아태평양의 우위를 확고히 하고 있습니다.

유럽은 가장 엄격한 규제 제정국으로 그 뒤를 잇고 있습니다. 2024년 5월에 공표된 유로 7은 핵심 배출가스 규제에 더해 배터리 내구성에 대한 지표를 부과하고 있으며, 보다 복잡한 파워트레인 컨트롤러를 요구하고 있습니다. 동시에 일반 안전 규정(General Safety Regulation)은 모든 경차에 지능형 속도 보조, 후방 카메라 및 운전자 모니터링 시스템 장착을 의무화하고 있습니다. 칩 공급의 현지화를 위해 유럽투자은행(EIB)은 자동차 레이더 및 5nm 프로세서 연구개발(R& : D)을 위해 NXP에 10억 유로의 융자금을 지원했습니다. 이에 반해, 콘티넨탈은 애프터마켓을 위한 700개의 새로운 엔진 관리 제품을 추가하여 유럽 공급업체들이 규제 변화를 어떻게 수익화하고 있는지를 보여주고 있습니다. 이러한 요인들로 인해 유럽은 꾸준한 점유율 확대의 토대를 마련하고 있습니다.

반면 북미는 기술 격차를 해소하기 위해 재정적 인센티브에 의존하고 있습니다. 보쉬는 전기 구동계용 실리콘 카바이드 웨이퍼 제조를 위해 미국 CHIPS 법으로부터 최대 2억 2,500만 달러의 자금을 확보했습니다. 또한, EPA의 3차 온실가스 계획은 2027년부터 OEM 업체들에게 대형 트럭의 배출량을 대폭 감축할 것을 의무화하고 있습니다. REPAIR법은 독립 정비업체 육성을 목적으로 진단 데이터 공개를 제안하고 있으며, 이는 OEM과 애프터마켓 사업자 간의 ECU 소프트웨어 역할 분담에 영향을 미치고 있습니다. 한편, NXP와 VIS는 미래 자동차 ECU 시장 수요에 대한 지역적 공급 탄력성을 확보하기 위해 싱가포르에 300mm 팹을 건설하기 위해 78억 달러를 투자하여 2027년에 생산을 시작할 예정입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측(금액(달러) 및 수량(대수))

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

KTH 26.05.29The Automotive Electronic Control Unit Market size in 2026 is estimated at USD 109.35 billion, growing from 2025 value of USD 103.41 billion with 2031 projections showing USD 144.64 billion, growing at 5.75% CAGR over 2026-2031.

The primary growth engines are regulatory deadlines for advanced driver-assistance systems, rapid electrification of passenger and commercial fleets, and the migration to centralized vehicle architectures. Battery electric vehicles require multiple new control domains-battery, inverter, on-board charger, and thermal management, multiplying the semiconductor bill of materials per vehicle.

Global Automotive Electronic Control Unit Market Trends and Insights

Electrification Wave Raises ECU Count Per Vehicle

Battery electric powertrains introduce dedicated control units for battery management, inverter logic, charging negotiation, and regenerative braking. Each function adds processing overhead that traditional combustion platforms never required, lifting semiconductor spend per vehicle from USD 420 in 2019 to an expected USD 1,350 by 2030. Hybrid configurations magnify integration complexity because algorithms must coordinate two propulsion sources seamlessly. Cummins reports that its electronic powertrain control modules optimize diesel, hydrogen, natural-gas, and fully electric systems, a preview of how diversified fuel strategies will keep ECU counts elevated. Consequently, the Automotive ECU Market gains incremental volume every time an OEM launches a new battery-electric or fuel-cell program.

ADAS Mandates in US, EU, China Boost Demand

The European Union activated the revised General Safety Regulation in July 2024, obligating every new car to ship with intelligent speed assistance, autonomous emergency braking, and reversing detection. China's Level-2 penetration reached 42.4% of new passenger-car sales in 1H 2024 under its intelligent connected-vehicle rules, and NHTSA is advancing similar ADAS provisions for North America. Each mandate needs a high-reliability controller capable of real-time sensor fusion and functional-safety diagnostics. The resulting volume uplift directly feeds the automotive ECU market.

Global Chip-Supply Volatility

Automotive ECUs still rely on mature 90 nm and larger process technology, a node class where global wafer capacity is chronically tight. VDA estimates that semiconductor demand from automakers will triple by 2030 while their share of overall chip output rises only from 8% to 14%. Suppliers cannot easily pivot foundry lines to trailing-edge nodes, so shortages linger even as leading-edge supply improves. Siemens promotes model-based verification that allows software teams to validate ECU code before silicon arrives, somewhat insulating programs from physical chip scarcity. Still, shortfalls can delay entire vehicle launches, knocking percentages off the automotive electronic control unit market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Centralized/Zonal E/E Architectures Need High-Performance ECUs

- Cyber-Secure, Over-the-Air Update Capability Becomes Sourcing Criterion

- OEM Reluctance to Cede Data-Control to Tier-1s

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Even though internal-combustion platforms retained 60.78% of the automotive ECU market share in 2025, battery electric vehicles added the fastest 6.51% CAGR between 2026 and 2031. Heavy-duty segments supercharge the trend: global electric-truck registrations jumped nearly 80% in 2024, with China launching more than 430 battery-electric heavy-duty models. Cummins emphasizes flexible control firmware that can adapt from diesel to hydrogen to full battery packs, illustrating how propulsion diversity increases code complexity and total ECU demand.

In contrast, combustion platforms continue to place large orders for engine-management units because emissions rules tighten every model year. Euro 7, published in 2024, mandates onboard monitoring of particulate filters and battery durability, adding new diagnostics channels to existing powertrain ECUs. OEMs therefore face a dual platform strategy through the decade: maintain robust combustion controls while adding incremental electronics for hybrid and pure EV programs. This tension supports steady incremental revenue for the automotive electronic control unit market even as powertrain architectures diverge.

Powertrain controllers generated 40.92% of the market share in 2025 because every vehicle-combustion, hybrid, or full electric-still needs torque, thermal, and energy management. ADAS & safety controllers, however, expand at 4.27% CAGR, making them the innovation flagship of the automotive electronic control unit market. Europe's General Safety Regulation and China's intelligent-connected guidelines require features such as automatic emergency braking, driver-monitoring cameras, and intelligent speed assistance, each relying on dedicated high-bandwidth microcontrollers. As lidar and radar migrate down price tiers, sensor-fusion loads grow, intensifying demand for 64-bit multicore processors.

Body, comfort, and lighting subsystems illustrate how legacy domains evolve; zonal controllers now replace multiple discrete boxes for windows, HVAC, and seat motors. Infotainment and telematics remain the smallest slice, but OTA services and subscription models compel OEMs to upgrade head units to gigahertz-class system-on-chips. The combined push from safety regulation and digital-service revenue gives the automotive electronic control unit market continuous headroom even after powertrain saturation.

The Automotive Electronic Control Unit Market is Segmented by Propulsion (Internal Combustion Engine, Hybrid, and Battery Electric Vehicle), Application (ADAS and Safety System, and More), ECU Capacity(16-Bit ECU, 32-Bit ECU, and 64-Bit ECU), Autonomy Level (Conventional (L0-L1), and More), Vehicle Type ( Passenger Car, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific anchored 48.29% of the market share in 2025, thanks to China's intelligent-connected vehicle roadmap and deep domestic semiconductor supply chain advantages, expanding at a CAGR of 7.72%. Level-2 penetration above 40% underscores how quickly the region adopts new control domains, and Chinese OEMs launched more than 430 battery-electric truck models in 2024 alone. Japan and South Korea added momentum with unified autonomous-driving legislation, while India's Production Linked Incentive scheme positions the country as a future electronics manufacturing hub. Collectively, these programs guarantee a dense pipeline of ECU contracts, securing Asia-Pacific's lead within the automotive ECU market

Europe follows as the strictest rule-setter. Euro 7, published in May 2024, layers battery durability metrics on top of core emissions caps, demanding more complex powertrain controllers. The General Safety Regulation simultaneously mandates intelligent speed assistance, reversing cameras, and driver-monitoring systems in all light vehicles. To localize chip supply, the European Investment Bank extended a EUR 1 billion loan to NXP for R&D in automotive radar and 5 nm processors. Continental responded by adding 700 new engine-management references for the aftermarket, illustrating how European suppliers monetize regulatory churn. These factors position Europe for steady share gains,

North America leans on financial incentives to close technology gaps. Bosch secured up to USD 225 million from the US CHIPS Act to build silicon-carbide wafers for electric drivetrains, and the EPA's Phase 3 greenhouse gas plan obligates OEMs to slash heavy-truck emissions beginning in 2027. The REPAIR Act proposes open diagnostic data to foster independent servicing, influencing how ECU software is partitioned between OEMs and aftermarket players. NXP and VIS meanwhile will spend USD 7.8 billion on a 300 mm fab in Singapore-production starts 2027-to guarantee regional supply resilience for future automotive ECU market demand.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- Lear Corporation

- ZF Friedrichshafen AG

- Hyundai Mobis Co. Ltd.

- Hitachi Astemo, Ltd.

- Nidec Corporation

- Panasonic Corporation (Automotive)

- Magneti Marelli (Marelli Holdings)

- Leopold Kostal GmbH & Co. KG

- Autoliv Inc.

- Veoneer Inc.

- Valeo SA

- NXP Semiconductors

- Renesas Electronics

- Infineon Technologies AG

- Texas Instruments Inc.

- Visteon Corporation

- Pektron Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification wave raises ECU count per vehicle

- 4.2.2 ADAS mandates in US, EU, China boost demand

- 4.2.3 Centralised / zonal E/E architectures need high-performance ECUs

- 4.2.4 Rapid semiconductor cost declines enable 64-bit migration

- 4.2.5 Cyber-secure, over-the-air (OTA) update capability becomes sourcing criterion (under-reported)

- 4.2.6 Heavy-duty & off-highway electrification creates a new ECU TAM (under-reported)

- 4.3 Market Restraints

- 4.3.1 Global chip-supply volatility

- 4.3.2 Software-hardware integration complexity

- 4.3.3 OEM reluctance to cede data-control to tier-1s (under-reported)

- 4.3.4 Emerging right-to-repair laws threaten aftermarket ECU margins (under-reported)

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Propulsion

- 5.1.1 Internal Combustion Engine

- 5.1.2 Hybrid

- 5.1.3 Battery Electric Vehicle

- 5.2 By Application

- 5.2.1 ADAS & Safety Systems

- 5.2.2 Body Control & Comfort Systems

- 5.2.3 Infotainment & Communication Systems

- 5.2.4 Powertrain Systems

- 5.3 By ECU Capacity

- 5.3.1 16-bit ECU

- 5.3.2 32-bit ECU

- 5.3.3 64-bit ECU

- 5.4 By Autonomy Level

- 5.4.1 Conventional (L0-L1)

- 5.4.2 Semi-Autonomous (L2-L3)

- 5.4.3 Autonomous (L4-L5)

- 5.5 By Vehicle Type

- 5.5.1 Passenger Car

- 5.5.2 Commercial Vehicle

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Egypt

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Denso Corporation

- 6.4.4 Aptiv PLC

- 6.4.5 Lear Corporation

- 6.4.6 ZF Friedrichshafen AG

- 6.4.7 Hyundai Mobis Co. Ltd.

- 6.4.8 Hitachi Astemo, Ltd.

- 6.4.9 Nidec Corporation

- 6.4.10 Panasonic Corporation (Automotive)

- 6.4.11 Magneti Marelli (Marelli Holdings)

- 6.4.12 Leopold Kostal GmbH & Co. KG

- 6.4.13 Autoliv Inc.

- 6.4.14 Veoneer Inc.

- 6.4.15 Valeo SA

- 6.4.16 NXP Semiconductors

- 6.4.17 Renesas Electronics

- 6.4.18 Infineon Technologies AG

- 6.4.19 Texas Instruments Inc.

- 6.4.20 Visteon Corporation

- 6.4.21 Pektron Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment