|

시장보고서

상품코드

2076888

농업기계 시장 : 출력별, 설비 유형별, 기능별, 추진 방식별, 구동 유형별, 제품 유형별, 지역별 - 세계 예측(-2033년)Farm Equipment Market by Power, Type (Tractors, Balers, Sprayers, Harvesters), Function, & Propulsion, and Region - Global Forecast to 2033 |

||||||

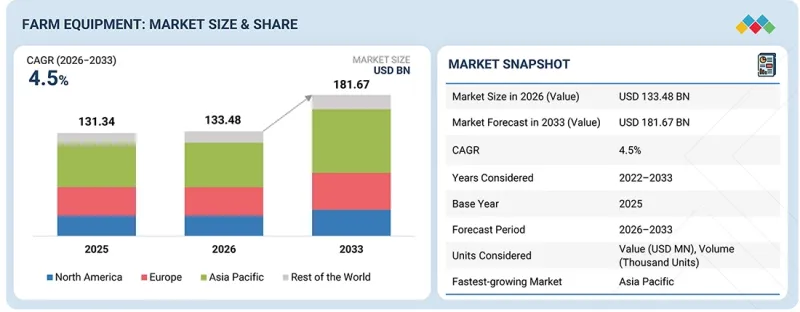

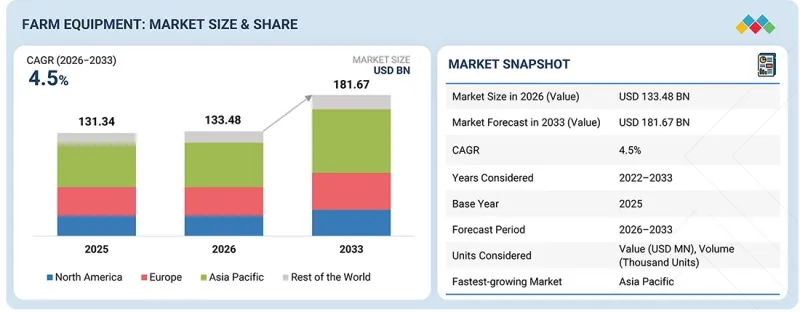

농업기계 시장 규모는 2026년 1,334억 8,000만 달러에서 2033년까지 1,816억 7,000만 달러로 성장할 것으로 예상되며, CAGR은 4.5%에 달할 것으로 예측됩니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2026-2033년 |

| 기준 연도 | 2025년 |

| 예측 기간 | 2026-2033년 |

| 대상 단위 | 10억 달러 |

| 부문 | 출력별, 설비 유형별, 기능별, 추진 방식별, 구동 유형별, 제품 유형별, 지역별 |

| 대상 지역 | 아시아·오세아니아, 유럽, 북미, 기타 지역 |

2025년, 세계 농업용 트랙터 시장에서는 주로 농가 소득 부진, 높은 금리, 그리고 교체 주기의 지연으로 인해 주요 지역 전반에 걸쳐 수요가 완만하게 감소했습니다. AEM, CEMA 및 각 지역의 농업 기관이 발표한 업계 전망에 따르면, 트랙터 판매 대수는 북미에서 약 7-9%, 유럽에서 약 22-24%, 아시아·오세아니아에서 약 4-6% 감소한 것으로 추정됩니다. 아시아·오세아니아 지역에서는 정부의 보조금과 견조한 내수(특히 인도)가 판매 둔화를 막는 데 일조했습니다. 농가들이 신규 기계 구매를 자제하고 기존 장비의 수명을 연장하는 경향을 보이고 있어, 이러한 영향은 고출력 트랙터나 콤바인 부문에서 더욱 두드러지게 나타나고 있습니다. 게다가 이스라엘과 이란 간의 분쟁으로 인해 중동 공급 루트의 혼란이 우려되고, 연료비와 물류 비용의 불확실성이 높아지면서 단기적인 압박이 더욱 심화되고 있습니다. 이로 인해, 특히 가격에 민감한 시장에서 농가 수익성이 저하되어 기계 구입이 미뤄지고 있습니다. 그러나 그 영향은 간접적이고 단기적인 수준에 그치고 있으며, 전 세계 식량 수요와 진행 중인 기계화 추세로 인해 장기적인 수요는 안정적입니다.

"임대 시장에서 수확 및 탈곡 부문은 예측 기간 동안 가장 빠르게 성장할 부문입니다."

수확·탈곡 장비는 농업용 기계 시장에서 가장 큰 부문 중 하나를 차지하고 있습니다. 이는 작물 생산 과정에서 가장 노동 집약적이고 시간적 제약이 엄격한 단계, 즉 작물 수확과 손실을 최소화하면서 판매 가능한 곡물을 짚에서 분리하는 작업과 직접적으로 관련되어 있기 때문입니다. 특히 아시아태평양(중국, 인도, 동남아시아), 북미, 유럽, 라틴아메리카와 같은 주요 곡물 생산 지역에서는 수요가 활발합니다. 이 지역들에서는 농업 임금 상승, 노동력 부족, 농장 규모 확대, 수확 적기 단축 등이 복합적으로 작용하여 기계화가 가속화되고 있습니다. 이러한 기계들은 밀, 쌀, 옥수수, 보리, 대두 및 기타 곡물 작물의 수확에 널리 사용되고 있으며, 농가는 곡물 손실을 줄이고, 곡물 품질을 향상시키며, 노동력에 대한 의존도를 낮추고, 악천후가 수확량에 영향을 미치기 전에 수확 작업을 완료할 수 있습니다.

최근의 기술 혁신으로 인해 도입 속도가 더욱 빨라지고 있습니다. 예를 들어, 2025년 2월, John Deere는 작물 포집 및 수확 효율을 향상시키도록 설계된 첨단 작물 공급 시스템을 탑재한 차세대 콤바인을 출시했습니다. 또한, 2025년 6월에는 자동화 강화, 정밀 농업 기술, 그리고 작업 생산성 향상을 특징으로 하는 자가주행형 사료 수확기 'F8' 및 'F9'를 발매했습니다. 또한, 인도의 벼 재배 지역을 대상으로 한 콤바인 'PRO588i-G'를 발매했습니다. 이 기종에는 일본이 설계한 특수한 탈곡 장치가 탑재되어 있어, 바스마티 쌀의 알곡 파손을 줄이는 동시에 잔여물 관리를 지원하며, 수확 후 남은 줄기의 소각을 줄여줍니다. 마찬가지로, 각 OEM 업체들은 생산성을 극대화하고 작업자의 개입을 줄이기 위해 GPS 안내, 수확 조정 자동화, 텔레매틱스, AI를 활용한 기계 최적화 기능을 콤바인 및 수확기에 점점 더 많이 통합하고 있습니다. 세계 곡물 생산량이 지속적으로 증가하고, 농장 규모가 확대되며 상업화가 진행됨에 따라 수확 및 탈곡 장비에 대한 수요는 계속해서 견조할 것으로 예상되며, 이 분야는 세계 농업기계화의 가장 중요한 촉진요인 중 하나가 될 것입니다.

"배터리식 전기 트랙터가 농업용 트랙터 업계의 미래를 이끌어 갈 것입니다."

전기 트랙터는 주로 배기가스, 소음, 운영 비용을 최소화해야 하는 저출력 작업, 정밀 작업 및 통제된 환경에서 사용됩니다. 주요 용도로는 과수원, 포도원, 원예, 온실 재배, 축산 농장, 지자체 농업, 그리고 일상적인 작업 시간 동안의 경량-중량급 밭일이 포함됩니다. 유럽과 미국에서는 소형 전기 트랙터가 특히 포도밭에서 큰 인기를 끌고 있습니다. 이는 좁은 줄 사이에서도 효율적으로 작업할 수 있을 뿐만 아니라, 토양에 미치는 영향을 줄이고 배기가스를 제로로 만들 수 있기 때문입니다. 또한 소음 수준이 낮고 유지보수 부담도 적기 때문에 지자체에서도 도시 유지관리 작업에 이를 활용하는 사례가 늘고 있습니다. 대표적인 모델로는 Monarch Tractor MK-V(배터리 용량 약 70 kWh), Solectrac e25 및 e70(약 22-70 kWh), Fendt e100 V Vario(약 100 kWh), 그리고 아시아·오세아니아 시장을 겨냥한 쿠보타(Kubota)의 소형 전기 트랙터 등이 있습니다. 농장 내 야간 충전, 태양광발전 기반 충전 시스템, 작업 틈틈이 진행하는 단시간 보충 충전과 같은 선진적인 충전 전략을 통해 전동 농업기계의 실용성과 보급이 확대되고 있습니다. 또한, 정부가 지원하는 농업 대출 면제 조치, 저금리 농업 융자 제도, 그리고 농기계 구입 자금 융자 프로그램이 농가들의 현대식 농기계 투자를 뒷받침하고 있어, 농업의 기계화와 첨단 농업 기술 도입을 더욱 가속화하고 있습니다.

정부의 지원은 도입을 가속화하는 주요 요인입니다. 캘리포니아주에서는 CORE 프로그램이 판매 시점에 인센티브를 제공하여 전기 트랙터의 초기 비용을 대폭 절감하고 있습니다. 지원 금액은 일반적으로 소형 트랙터의 경우 약 16,000달러부터, 중형 농업기계의 경우 43,000-130,000달러에 이르며, 일부 대형 품목의 경우 자격 요건에 따라 그보다 더 높은 금액이 될 수도 있습니다. 유럽에서는 EU 그린딜, 공동농업정책(CAP)의 친환경 제도, 그리고 독일이나 프랑스 등 각국의 보조금 프로그램을 통해 도입이 지원되고 있으며, 캐나다와 아시아태평양(APAC)의 일부에서도 이와 유사한 청정 장비에 대한 자금 지원이 이루어지고 있습니다. 전기 트랙터는 기존의 디젤 모델보다 초기 비용이 높지만, 연료비와 유지비 절감, 에너지 효율 향상, 배기가스 감축을 통해 장기적으로는 상당한 비용 절감을 기대할 수 있습니다. 정부의 인센티브, 유리한 융자 프로그램, 충전 인프라 확충, 그리고 점점 더 엄격해지는 배출 규제의 뒷받침을 받아, 주요 농업 시장, 특히 지속가능성 노력이 활발하고 농업기계화가 진행되고 있는 지역에서 전기 트랙터에 대한 수요는 꾸준히 확대될 것으로 예상됩니다.

"포워더 분야는 임업 기계 시장에서 가장 빠르게 성장하고 있는 분야로 추정됩니다."

포워더는 기계화 임업 장비 분야에서 가장 중요한 성장 부문 중 하나로 부상하고 있으며, 수요와 기술 도입 측면에서는 유럽이 분명히 주도적인 입지를 차지하고 있습니다. 스웨덴, 핀란드, 중부 유럽 등의 국가에서는 포워더가 컷-투-렌지(CTL) 벌채 시스템에서 널리 사용되고 있습니다. 이 시스템은 엄격한 환경 규제, FSC/PEFC 인증 요건, 그리고 목재 1입방미터당 토양 훼손 및 탄소 배출량 감축에 대한 강한 중시 덕분에 현대 지속가능한 임업 분야에서 주류로 자리 잡고 있습니다. OEM의 수요는 적재량 12-20톤 이상의 범위에 집중되어 있으며, 코마츠의 845/855/875/895나 폰세의 버팔로 및 엘리펀트 시리즈 등, 높은 생산성, 급경사지 작업, 지속적인 간벌 주기를 염두에 두고 설계된 모델들이 인기를 끌고 있습니다. 유럽의 포워더 시장은 구식 스키더 기반 시스템이 더 높은 정밀도를 자랑하고 친환경적이며 디지털로 연결된 기계로 대체되는 '함대 업데이트'에 의해 주도되고 있습니다. 북미에서는 캐나다와 미국의 특정 임업 지역에서, 특히 컷-투-렌지(CTL) 작업용으로 도입이 점차 확대되고 있는 반면, 대규모 벌채 작업에서는 여전히 스키더가 주류를 이루고 있습니다. John Deere나 Komatsu Forest와 같은 주요 OEM 업체들은 텔레매틱스, 연비 효율이 높은 유압 시스템, 운전자 지원 기술 등을 활용하여 포워더의 성능 향상을 도모하고 있으며, 향후 개발에서는 반자율주행, AI를 활용한 적재량 최적화, 하이브리드 동력 시스템에 초점이 맞춰질 것으로 예상됩니다.

"유럽은 지역별 시장 중 두 번째로 큰 규모를 기록할 것으로 예상됩니다."

CEMA와 VDMA에 따르면, 유럽 트랙터 시장은 2025년에 2024년 대비 약 22% 위축되었으며, 이는 최근 몇 년간 가장 급격한 위축 중 하나였습니다. 프랑스에서는 농업 소득 부진, 높은 금리, 그리고 차량 교체 주기의 지연으로 인해 17.2%(27,844대) 감소했습니다. 튀르키예에서는 통화 가치 하락, 인플레이션, 구매력 저하로 인해 36.3%(40,505대)라는 큰 폭의 감소를 기록했으며, 러시아에서는 공급 제약과 무역 제한으로 인해 31%(24,150대) 감소했습니다. 반면 이탈리아에서는 포도밭과 과수원의 보조금 주도형 교체 수요에 힘입어 14.1%(17,573대) 증가했습니다. 한편, 폴란드에서는 EU의 공동농업정책(CAP)에 따른 강력한 자금 지원, 농장 통합, 그리고 차량 현대화의 가속화로 인해 22.1%(10,433대) 증가했습니다.

트랙터의 마력별로 살펴보면, 131-250 HP 구간은 복합 농업 및 도급 업무에서 여전히 핵심적인 수요 기반을 형성하고 있는 반면, 250 HP 초과 구간은 농지 통합 및 생산성 향상에 대한 요구가 높아짐에 따라 프랑스, 독일, 동유럽에서 더욱 빠르게 성장하고 있습니다. 이러한 전환은 EU 스테이지 V 규제, 2027년 기계 규제 체계, 그린 딜과 같은 정책 및 비용 측면의 압박에 힘입어 더욱 강력하게 추진되고 있습니다. 유럽에서 100-200 HP급 전기 트랙터는 여전히 초기 단계에 있지만 빠르게 성장하고 있는 부문으로, 주로 포도원, 과수원, 온실 및 지자체에서 사용되고 있습니다. 이러한 상황에서는 고출력보다 저소음, 무공해 및 정밀 작업이 중시됩니다.

농업기계 시장은 Deere & Company(미국), AGCO Corporation(미국), CNH Industrial N.V.(네덜란드), Kubota Corporation(일본), CLAAS KGaA mbH(독일), Mahindra & Mahindra Ltd.(인도), ISEKI(일본), Escorts Kubota Limited(인도), SDF Group(독일), Yanmar Holdings(일본) 등 세계적인 기업들이 주도하고 있습니다. 이 기업들은 시장에서 입지를 강화하기 위해 제품 개발 및 제휴 등의 전략을 채택했습니다.

조사 범위:

본 조사에서는 농업기계 시장을 세분화하여 출력별, 구동 방식별, 설비 유형별, 기능별, 추진 방식별 및 지역별로 분석하고 있습니다. 또한, 농업기계 시장 생태계 내 주요 기업들의 경쟁 현황과 기업 개요에 대해서도 포괄적으로 다루고 있습니다.

본 보고서의 주요 장점

본 보고서는 시장을 선도하는 기업 및 신규 진입 기업을 대상으로, 농업기계 시장 및 그 하위 부문의 매출액에 대한 가장 정확한 추정치를 제공합니다. 본 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 더 나은 위치로 이끌며, 적절한 시장 진입 전략을 수립하는 데 필요한 인사이트를 얻는 데 도움이 됩니다. 또한, 본 보고서는 이해관계자들이 시장 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 시장 억제요인, 과제 및 기회에 대한 정보를 제공합니다.

본 보고서에서는 다음 사항에 대한 인사이트를 제공합니다:

- 주요 촉진요인 분석(농가 대상 대출 면제·신용 대출에 대한 정부 지원, 딜러의 서비스 및 렌탈 사업을 지원하기 위한 OEM/판매 인센티브, 계약 농업, 농업기계화의 진전) , 제약요인(렌탈 시장의 확대, 신흥국에서의 장비 고비용), 기회(정밀 농업의 보급 확대, 연구 개발 강화 및 전기 트랙터 도입 확대), 그리고 과제(급변하는 배기가스 규제 및 의무)에 대해 농업기계 시장의 성장에 영향을 미치는 요인을 분석하고 있습니다.

- 제품 개발 및 혁신 : 농업기계 시장의 향후 기술, 연구 개발 활동 및 신제품 출시에 관한 상세한 인사이트

- 시장 개발 : 수익성이 높은 시장에 대한 종합적인 정보 - 본 보고서에서는 다양한 지역의 농업기계 시장을 분석하고 있습니다.

- 시장의 다양화 : 농업기계 시장의 신제품, 미개척 지역, 최근 동향 및 투자에 관한 종합적인 정보

- 경쟁사 분석 : Deere & Company(미국), AGCO Corporation(미국), CNH Industrial N.V.(네덜란드), Kubota Corporation(일본), CLAAS KGaA mbH(독일), Mahindra & Mahindra(인도), ISEKI & Co., Ltd.(일본), Escorts Kubota Limited(인도), SDF Group(독일), Yanmar Holdings(일본) 등, 농업기계 시장의 주요 기업들의 시장 점유율, 성장 전략, 서비스 제공 내용에 대해 상세히 평가합니다.

자주 묻는 질문

목차

제1장 소개

제2장 주요 요약

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, 특허, 혁신, 그리고 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 농업용 트랙터 시장(출력별)

제10장 농업기계 시장(설비 유형별)

제11장 농업기계 시장(기능별)

제12장 전동 농업용 트랙터 시장(추진 방식별)

제13장 농업용 트랙터 렌탈 시장 개요

제14장 농업용 트랙터 렌탈 시장(구동 유형별)

제15장 농업기계 렌탈 시장(설비 유형별)

제16장 임업 기계 시장(제품 유형별)

제17장 농업용 트랙터 시장(지역별)

제18장 경쟁 구도

제19장 기업 개요

제20장 조사 방법

제21장 시장의 제안

제22장 부록

KSM 26.07.07The farm equipment market is projected to grow from USD 133.48 billion in 2026 to USD 181.67 billion by 2033, registering a CAGR of 4.5%.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2026-2033 |

| Base Year | 2025 |

| Forecast Period | 2026-2033 |

| Units Considered | USD Billion |

| Segments | by Power, Type, Function, Propulsion & Region |

| Regions covered | Asia Oceania, Europe, North America, and the Rest of the World |

In 2025, the global farm tractor market saw a moderate decline in demand across key regions, mainly due to weak farm incomes, high interest rates, and delayed replacement cycles. Based on industry outlooks from AEM, CEMA, and regional agricultural agencies, tractor sales are estimated to have declined by around ~7-9% in North America, ~22-24% in Europe, and ~4-6% in Asia Oceania, where government subsidies and stronger domestic demand (especially in India) helped limit the slowdown. The impact is more visible in high-horsepower tractors and combine segments, as farmers extend equipment life instead of purchasing new machines. Moreover, the Israel-Iran conflict adds further short-term pressure by increasing uncertainty in fuel and logistics costs due to potential Middle East supply route disruptions, which reduces farm profitability and delays equipment purchases, especially in price-sensitive markets. However, the impact remains indirect and short-term, while long-term demand stays stable due to global food needs and ongoing mechanization trends.

"The harvester & threshing segment in the rental market is the fastest-growing segment during the forecast period."

Harvesting and threshing equipment represent one of the largest segments of the agricultural implements market because they directly address the most labor-intensive and time-critical stage of crop production - harvesting crops and separating marketable grain from straw with minimal losses. Demand is particularly strong across major grain-producing regions, including Asia Pacific (China, India, and Southeast Asia), North America, Europe, and Latin America, where rising farm wages, labor shortages, larger farm sizes, and increasingly narrow harvesting windows are accelerating mechanization. These machines are widely used for wheat, rice, maize, barley, soybean, and other cereal crops, enabling farmers to reduce grain losses, improve grain quality, lower labor dependency, and complete harvesting operations before adverse weather affects yields.

Recent innovations are further strengthening adoption; for example, in February 2025, John Deere introduced next-generation combine harvesting equipment with advanced crop-feeding systems designed to improve crop capture and harvesting efficiency, while in June 2025, the company launched its F8 and F9 self-propelled forage harvesters featuring enhanced automation, precision farming technologies, and improved operational productivity. It launched the PRO588i-G combine harvester for India's rice-growing regions, incorporating a specialized Japanese-designed threshing mechanism that reduces grain breakage in Basmati rice while supporting residue management and reducing stubble burning. Similarly, OEMs are increasingly integrating GPS guidance, automated harvesting adjustments, telematics, and AI-driven machine optimization into combines and harvesters to maximize productivity and reduce operator intervention. As global cereal production continues to rise and farms become larger and more commercialized, demand for harvesting and threshing equipment is expected to remain strong, making this segment one of the most critical drivers of agricultural mechanization worldwide.

"Battery electric tractors would lead the future of the farm tractor industry."

Electric tractors are mainly used in low-power, precision, and controlled-environment applications where emissions, noise, and operating costs need to be minimized. Key applications include orchards, vineyards, horticulture, greenhouse operations, livestock farms, municipal agriculture, and light-to-medium-duty field work for daily operating hours. In Europe and the US, small EV tractors are particularly popular in vineyards because they can operate efficiently in narrow rows while reducing soil disturbance and eliminating exhaust emissions. Municipal bodies also increasingly use them for city maintenance work due to their low noise levels and lower maintenance requirements. Leading models include Monarch Tractor MK-V (~70 kWh battery), Solectrac e25 and e70 (~22-70 kWh), Fendt e100 V Vario (~100 kWh), and compact electric offerings from Kubota in Asia Oceania markets. Advanced charging strategies such as on-farm overnight charging, solar-powered charging systems, and opportunity charging through short top-ups during operational breaks are improving the practicality and adoption of electric farm equipment. Additionally, government-supported farm loan waivers, low-interest agricultural credit schemes, and equipment financing programs are helping farmers invest in modern machinery, further accelerating farm mechanization and the adoption of advanced agricultural technologies.

Government support is a major factor accelerating adoption. In California, the CORE programme provides point-of-sale incentives that significantly reduce upfront costs for electric tractors, with support typically ranging from USD ~16,000 for small compact tractors to USD 43,000-130,000 for mid-sized agricultural equipment, and in some heavy-duty categories even higher depending on eligibility. In Europe, adoption is supported through the EU Green Deal, CAP eco-schemes, and national subsidy programs in countries like Germany and France, while similar clean equipment funding exists in parts of Canada and APAC. Although electric tractors have higher upfront costs than conventional diesel models, they offer significant long-term savings through lower fuel and maintenance expenses, improved energy efficiency, and reduced emissions. Supported by government incentives, favorable financing programs, expanding charging infrastructure, and increasingly stringent emission regulations, demand for electric tractors is expected to grow steadily across key agricultural markets, particularly in regions with strong sustainability initiatives and mechanized farming practices.

"The forwarders segment is estimated to be the fastest growing in the forest machinery market."

Forwarders are emerging as one of the most important growth segments in mechanized forestry equipment, with Europe clearly leading demand and technology adoption. In countries like Sweden, Finland, and Central Europe, forwarders are widely used in cut-to-length (CTL) harvesting systems, which dominate modern sustainable forestry due to strict environmental regulations, FSC/PEFC certification requirements, and a strong focus on reducing soil damage and carbon emissions per cubic meter of timber. OEM demand is concentrated in the 12-20+ ton payload range, with popular models such as Komatsu 845/855/875/895 and Ponsse Buffalo and Elephant series designed for high productivity, steep terrain operation, and continuous thinning cycles. Europe's forwarder market is driven by fleet replacement, as older skidder-based systems are being replaced with more precise, environmentally friendly, and digitally connected machines. In North America, adoption is growing gradually in Canada and selected U.S. forestry regions, particularly for cut-to-length (CTL) operations, while skidders continue to dominate large-scale harvesting. Leading OEMs such as John Deere and Komatsu Forest are enhancing forwarders with telematics, fuel-efficient hydraulics, and operator-assist technologies, while future developments are expected to focus on semi-autonomous operation, AI-based load optimization, and hybrid power systems.

"Europe is projected to be the second-largest regional market."

According to CEMA and VDMA, the European tractor market declined by around ~22% during 2025 as compared to 2024, marking one of the sharpest contractions in recent years. France declined by -17.2% (27,844 units) due to weaker farm income, high interest rates, and delayed replacement cycles. Turkey recorded a sharp -36.3% drop (40,505 units) driven by currency depreciation, inflation, and reduced purchasing power, and Russia declined by -31% (24,150 units) due to supply constraints and trade restrictions. In contrast, Italy grew by +14.1% (17,573 units), supported by subsidy-led replacement demand in vineyards and orchards, while Poland rose by +22.1% (10,433 units), driven by strong EU CAP funding, farm consolidation, and faster modernization of fleets.

Based on the horsepower of tractors, the 131-250 HP segment remains the core demand base for mixed farming and contracting, while the >250 HP segment is growing faster in France, Germany, and Eastern Europe due to land consolidation and higher productivity requirements. This transition is driven more by policy and cost pressure such as EU Stage V norms, the Machinery Regulation 2027 framework, and the Green Deal. EV tractors with 100-200 HP in Europe are still in an early-stage but fast-emerging segment, mainly used in vineyards, orchards, greenhouses, and municipal applications where low noise, zero emissions, and precision work are more important than high power.

In-depth interviews were conducted with CEOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: OEMs - 80%, Farm Equipment Manufacturing Companies - 20%

- By Designation: C Levels - 50%, Directors - 30%, Others - 20%

- By Region: North America - 30%, Europe - 20%, Asia Oceania - 40%, Rest of the World - 10%

The farm equipment market is dominated by global players such as Deere & Company (US), AGCO Corporation (US), CNH Industrial N.V. (Netherlands), Kubota Corporation (Japan), CLAAS KGaA mbH (Germany), Mahindra&Mahindra Ltd. (India), ISEKI & Co., Ltd. (Japan), Escorts Kubota Limited (India), SDF Group (Germany), and Yanmar Holdings Co., Ltd (Japan). These companies adopted strategies such as product development, deals, and others to gain traction in the market.

Research Coverage:

The study segments the farm equipment market and forecasts the market size based on power output (<30 HP, 31-70 HP, 71-130 HP, 131-250 HP, and >250 HP), drive type (two-wheel drive and four-wheel drive), farm equipment market, rental market, by equipment type (tractors, combines, sprayers, balers, others), forestry machinery market, by implement type (skidders, forwarders, bunchers, swing machines, harvesters, loaders, and other forestry machinery), by function (plowing & cultivation, sowing & planting, harvesting & threshing, and others), by equipment type (cereal combines, non-cereal, combines, balers, self-propelled sprayers, tractor-mounted sprayers, and tillers), rental market, by power output (<30 HP, 31-70 HP, 71-130 HP, 131-250 HP, >250 HP), electric tractor market, by propulsion (battery electric, hybrid electric, and hydrogen), and region (Asia Oceania, North America, Europe, and the Rest of the World [RoW]). It also covers the competitive landscape and company profiles of the major players in the farm equipment market ecosystem.

Key Benefits of the Report

The report will provide market leaders and new entrants with the closest approximations of revenue figures for the farm equipment market and its subsegments. This report will help stakeholders understand the competitive landscape and gain insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the market pulse and provides information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Government support with farmer loan waivers/credit finance, OEM/sales incentives to support dealer services and rental operations, Contract farming, and Increase in farm mechanization), restraints (Growth of rental market, High equipment cost in emerging economies), opportunities (Growing adoption of precision agriculture, Increasing R&D and adoption of electric tractors), and challenges (Rapidly changing emission norms and mandates) influencing the growth of the farm equipment market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the farm equipment market

- Market Development: Comprehensive information about lucrative markets - the report analyses the farm equipment market across varied regions.

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the farm equipment market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Deere & Company (US), AGCO Corporation (US), CNH Industrial N.V. (Netherlands), Kubota Corporation (Japan), and CLAAS KGaA mbH (Germany), Mahindra & Mahindra (India), ISEKI & Co., Ltd. (Japan), Escorts Kubota Limited (India), SDF Group (Germany), and Yanmar Holdings Co., Ltd (Japan), among others, in the farm equipment market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 SUMMARY OF CHANGES

- 1.6 STAKEHOLDERS

2 EXECUTIVE SUMMARY

- 2.1 MARKET INSIGHTS AND KEY HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN FARM EQUIPMENT MARKET

- 3.2 FARM EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 3.3 FARM TRACTOR MARKET, BY POWER OUTPUT

- 3.4 FARM TRACTOR MARKET, BY DRIVE TYPE

- 3.5 FARM IMPLEMENT MARKET, BY FUNCTION

- 3.6 ELECTRIC TRACTOR MARKET, BY PROPULSION

- 3.7 FARM EQUIPMENT RENTAL MARKET, BY EQUIPMENT TYPE

- 3.8 FOREST MACHINERY MARKET, BY PRODUCT TYPE

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Government-backed mechanization financing and farm equipment modernization programs

- 4.2.1.2 Government and OEM incentives to support dealer services and rental operations

- 4.2.1.3 Rise of contract farming

- 4.2.1.4 Surge in farm mechanization

- 4.2.2 RESTRAINTS

- 4.2.2.1 Booming rental market

- 4.2.2.2 High cost of farm equipment in emerging economies

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Rapid adoption of precision farming

- 4.2.3.2 Increasing R&D activities and growing use of electric tractors

- 4.2.4 CHALLENGES

- 4.2.4.1 Changing emission norms and mandates

- 4.2.4.2 Shortage of skilled technicians for electric tractors

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 MACROECONOMIC INDICATORS

- 5.1.1 GDP TRENDS AND FORECAST

- 5.1.2 TRENDS IN GLOBAL FARM EQUIPMENT MARKET

- 5.1.2.1 Regional GDP dynamics

- 5.1.2.1.1 Developed markets

- 5.1.2.1.2 Emerging markets

- 5.1.2.2 Investment environment

- 5.1.2.1 Regional GDP dynamics

- 5.2 SUPPLY CHAIN ANALYSIS

- 5.3 ECOSYSTEM ANALYSIS

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE TREND, BY POWER OUTPUT AND REGION

- 5.5 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT SCENARIO (HS CODE 843210)

- 5.6.2 EXPORT SCENARIO (HS CODE 843210)

- 5.7 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.8 INVESTMENT AND FUNDING SCENARIO

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 SOLECTRAC'S ELECTRIC TRACTORS FOR MUSHROOM FARM

- 5.9.2 AGRIMACS' ELECTRIC TRACTORS FOR SUSTAINABLE AGRICULTURAL PRACTICES

- 5.9.3 WENTE VINEYARDS' MONARCH TRACTORS FOR IMPROVED OPERATIONAL EFFICIENCY AND COST-EFFECTIVENESS

- 5.10 TOTAL COST OF OWNERSHIP

- 5.10.1 TOTAL COST OF OWNERSHIP FOR ELECTRIC AND DIESEL TRACTORS

- 5.10.1.1 Diesel tractors

- 5.10.1.2 Electric tractors

- 5.10.1.3 Cumulative result of TCO for electric vs. diesel tractors

- 5.10.1 TOTAL COST OF OWNERSHIP FOR ELECTRIC AND DIESEL TRACTORS

- 5.11 OEM ANALYSIS

- 5.11.1 ELECTRIC/HYBRID TRACTOR BATTERY CAPACITY VS. MOTOR OUTPUT

- 5.11.2 REGIONAL TREND OF DIESEL TRACTORS, BY DRIVE TYPE

- 5.11.3 HORSEPOWER ANALYSIS OF KEY PLAYERS

- 5.11.4 SEMI-AUTONOMOUS VS. AUTONOMOUS FARM TRACTOR OFFERINGS

- 5.11.5 FUTURE INVESTMENTS IN FARM EQUIPMENT TECHNOLOGIES

- 5.12 PRICE RANGES OF TRACTORS BY TOP OEMS

- 5.12.1 YANMAR AMERICA CORPORATION

- 5.12.2 DEERE & COMPANY

- 5.12.3 MASSEY FERGUSON (AGCO CORPORATION)

- 5.12.4 EICHER TRACTOR (TAFE)

- 5.12.5 SONALIKA

- 5.12.6 NEW HOLLAND

- 5.13 IMPACT OF ISRAEL-IRAN WAR ON FARM EQUIPMENT MARKET

- 5.13.1 SURGE IN OIL PRICES

- 5.13.2 RISE IN DIESEL PRICES

- 5.13.3 HYPOTHESIS OF WAR IMPACT

- 5.14 BRAND-WISE TRACTOR SALES IN KEY COUNTRIES

- 5.14.1 GERMANY: BRAND-WISE TRACTOR SALES

- 5.14.2 FRANCE: BRAND-WISE SALES

- 5.14.3 SPAIN: BRAND-WISE SALES

- 5.14.4 ITALY: BRAND-WISE SALES

- 5.14.5 TURKEY: BRAND-WISE SALES

- 5.14.6 UK: BRAND-WISE SALES

- 5.14.7 INDIA: BRAND-WISE SALES

- 5.14.8 SOUTH KOREA: BRAND-WISE SALES

- 5.15 OEM-WISE PRODUCTION CAPACITY OF TRACTORS

- 5.16 FUTURE INVESTMENTS FOR INCREASING TRACTOR PRODUCTION CAPACITY

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 FARM EQUIPMENT AUTOMATION

- 6.1.2 AGRICULTURE 5.0

- 6.1.3 ELECTRIFICATION

- 6.1.4 TRACTOR-IMPLEMENT COMMUNICATION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 FARM MANAGEMENT SOFTWARE

- 6.2.2 CNG TRACTORS

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 PRECISION FARMING

- 6.3.2 HIGH-PRECISION RTK AND PPP CORRECTIONS

- 6.4 PATENT ANALYSIS

- 6.5 FUTURE APPLICATIONS

- 6.6 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 NON-ROAD MOBILE MACHINERY EMISSION (NRMM) REGULATION OUTLOOK

- 7.2.1 NORTH AMERICA

- 7.2.1.1 US

- 7.2.2 EUROPE

- 7.2.3 ASIA OCEANIA

- 7.2.3.1 China

- 7.2.3.2 India

- 7.2.1 NORTH AMERICA

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS AND BUYING CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING EVALUATION PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS OF END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

9 FARM TRACTOR MARKET, BY POWER OUTPUT

- 9.1 INTRODUCTION

- 9.2 <30 HP

- 9.2.1 RISE OF MECHANIZATION THROUGH GOVERNMENT SUBSIDIES, MACHINERY GRANTS, AND COOPERATIVE OWNERSHIP MODELS

- 9.2.2 OPERATIONAL DATA FOR <30 HP TRACTORS

- 9.3 30-70 HP

- 9.3.1 UPGRADE OF TRADITIONAL PLATFORMS WITH HIGHER LIFTING CAPACITIES AND CONNECTED TECHNOLOGIES

- 9.3.2 OPERATIONAL DATA FOR 30-70 HP TRACTORS

- 9.4 71-130 HP

- 9.4.1 NEED FOR TRACTORS WITH HIGHER POWER AND EFFICIENCY IN EXTENSIVE FARMLANDS

- 9.5 131-250 HP

- 9.5.1 SIGNIFICANT PRESENCE OF LARGE FARMLANDS IN EUROPE

- 9.6 >250 HP

- 9.6.1 GROWING ORGANIZED FARMING ACTIVITIES

- 9.7 INDUSTRY INSIGHTS

10 FARM EQUIPMENT MARKET, BY EQUIPMENT TYPE

- 10.1 INTRODUCTION

- 10.2 CEREAL COMBINES

- 10.2.1 SURGE IN CEREAL DEMAND FROM FOOD, FEED, AND BIOFUEL INDUSTRIES

- 10.3 NON-CEREAL COMBINES

- 10.3.1 RISING LABOR SHORTAGES AND INCREASING CULTIVATION OF COMMERCIAL CROPS

- 10.4 BALERS

- 10.4.1 EXPANSION OF GLOBAL LIVESTOCK SECTOR AND ELEVATED DEMAND FOR HIGH-QUALITY FORAGE

- 10.5 SELF-PROPELLED SPRAYERS

- 10.5.1 NEED FOR TIMELY APPLICATION OF HERBICIDES, FUNGICIDES, AND FERTILIZERS ACROSS LARGE-SCALE FARMING OPERATIONS

- 10.6 TRACTOR-MOUNTED SPRAYERS

- 10.6.1 GROWING DEMAND FOR PESTICIDES, HERBICIDES, FUNGICIDES, AND LIQUID FERTILIZERS

- 10.7 INDUSTRY INSIGHTS

11 FARM IMPLEMENT MARKET, BY FUNCTION

- 11.1 INTRODUCTION

- 11.2 PLOWING & CULTIVATING

- 11.2.1 HIGHER YIELDS CATERING TO NEEDS OF GROWING POPULATION

- 11.3 SOWING & PLANTING

- 11.3.1 HIGH CONCENTRATION IN LARGE AGRICULTURAL PRODUCTION SYSTEMS

- 11.4 PLANT PROTECTION & FERTILIZING

- 11.4.1 ESCALATING CROP PRODUCTION AND ENHANCING FOOD QUALITY

- 11.5 HARVESTING & THRESHING

- 11.5.1 EXPANDING PRODUCTION OF HIGH-CAPACITY HARVESTING IMPLEMENTS FOR SMALL AND LARGE FARMS

- 11.6 OTHER FUNCTIONS

- 11.7 INDUSTRY INSIGHTS

12 ELECTRIC FARM TRACTOR MARKET, BY PROPULSION

- 12.1 INTRODUCTION

- 12.2 BATTERY ELECTRIC

- 12.2.1 REDUCTION IN BATTERY MANUFACTURING COSTS

- 12.3 HYBRID ELECTRIC

- 12.3.1 HIGHER POWER OUTPUT THAN BATTERY ELECTRIC TRACTORS

- 12.4 HYDROGEN

- 12.4.1 ADVANCEMENTS IN FUEL CELL TECHNOLOGY AND INFRASTRUCTURE

- 12.5 INDUSTRY INSIGHTS

13 FARM TRACTOR RENTAL MARKET OVERVIEW

- 13.1 INTRODUCTION

- 13.2 RENTAL ECONOMICS AND ASSET UTILIZATION ANALYSIS

- 13.2.1 REGIONAL PENETRATION OF RENTAL TRACTORS

- 13.2.2 PRICE STRUCTURE FOR RENTAL TRACTORS (PER DAY/WEEK)

- 13.2.3 AVERAGE ANNUAL UTILIZATION RATE

- 13.2.4 RENTAL DAYS PER YEAR BY TRACTOR HP CATEGORY

- 13.3 FARM EQUIPMENT RENTAL BUSINESS MODEL EVOLUTION

- 13.3.1 TRADITIONAL FARM EQUIPMENT RENTAL BUSINESS MODEL VS. SUBSCRIPTION MODEL

- 13.3.2 EQUIPMENT-AS-A-SERVICE (EAAS)

- 13.4 OEM RENTAL PROGRAMS AND STRATEGIES

- 13.4.1 PARTNERSHIPS WITH DIGITAL RENTAL PROGRAMS

- 13.5 FUTURE REVENUE ANALYSIS

14 FARM TRACTOR RENTAL MARKET, BY DRIVE TYPE

- 14.1 INTRODUCTION

- 14.2 TWO-WHEEL DRIVE (2WD)

- 14.2.1 LOWER ACQUISITION AND RENTAL COSTS, REDUCED FUEL CONSUMPTION, AND SUITABILITY FOR ROUTINE ACTIVITIES

- 14.3 FOUR-WHEEL DRIVE (4WD)

- 14.3.1 NEED FOR GREATER PRODUCTIVITY AND LABOR EFFICIENCY

- 14.4 INDUSTRY INSIGHTS

15 FARM EQUIPMENT RENTAL MARKET, BY EQUIPMENT TYPE

- 15.1 INTRODUCTION

- 15.2 TRACTORS

- 15.2.1 ONGOING COLLABORATIONS BETWEEN OEMS AND APPLICATION COMPANIES

- 15.3 COMBINES

- 15.3.1 IMPROVED MACHINE UTILIZATION RATES AND REDUCED IDLE CAPITAL

- 15.4 SPRAYERS

- 15.4.1 GROWING ADOPTION OF PRECISION AGRICULTURE AND STRICTER REGULATIONS ON CHEMICAL APPLICATION

- 15.5 BALERS

- 15.5.1 INCREASING PREFERENCE FOR ROUND BALERS WITH PRE-CUTTING SYSTEMS

- 15.6 OTHER RENTAL EQUIPMENT

- 15.7 INDUSTRY INSIGHTS

16 FOREST MACHINERY MARKET, BY PRODUCT TYPE

- 16.1 INTRODUCTION

- 16.2 FELLER BUNCHERS

- 16.2.1 HIGH DEMAND FOR FTL PROCESS IN AMERICAS

- 16.3 HARVESTERS

- 16.3.1 LABOR SHORTAGES AND SUSTAINABILITY REQUIREMENTS ACCELERATING MECHANIZATION

- 16.4 FORWARDERS

- 16.4.1 EMPHASIS ON REDUCING WOOD LOSSES DURING EXTRACTION

- 16.5 LOADERS

- 16.5.1 INCREASE IN COMMERCIAL CONSTRUCTION ACTIVITIES

- 16.6 SKIDDERS

- 16.6.1 CONTINUOUS EXPANSION OF INDUSTRIAL TIMBER PRODUCTION AND PLANTATION FORESTRY

- 16.7 SWING MACHINES

- 16.7.1 ADAPTABILITY AND EFFICIENCY IN DIVERSE TERRAINS PROPELLING DEMAND

- 16.8 OTHER FOREST MACHINERY

- 16.9 INDUSTRY INSIGHTS

17 FARM TRACTOR MARKET, BY REGION

- 17.1 INTRODUCTION

- 17.2 ASIA OCEANIA

- 17.2.1 AUSTRALIA

- 17.2.1.1 Large-scale mechanized agriculture and technology adoption to drive market

- 17.2.2 CHINA

- 17.2.2.1 Declined demand due to post-subsidy demand correction and weaker replacement cycles

- 17.2.3 INDIA

- 17.2.3.1 Government subsidies, rural income stability, and mechanization access through rental and service models to drive market

- 17.2.4 JAPAN

- 17.2.4.1 Seasonal sales and concentration on pre-planting and harvest periods to drive market

- 17.2.5 SOUTH KOREA

- 17.2.5.1 Weakening trend due to shift in equipment preferences toward smaller utility machines, smart farming tools, and drones

- 17.2.6 REST OF ASIA OCEANIA

- 17.2.1 AUSTRALIA

- 17.3 EUROPE

- 17.3.1 FRANCE

- 17.3.1.1 Farmers prioritizing cost control over machinery upgrades to impede market

- 17.3.2 GERMANY

- 17.3.2.1 Shortage of farm labor to drive market

- 17.3.3 ITALY

- 17.3.3.1 Increasing demand for precision agriculture to drive market

- 17.3.4 POLAND

- 17.3.4.1 EU-linked modernization incentives and investment support programs to drive demand

- 17.3.5 RUSSIA

- 17.3.5.1 Strong shift toward 4WD and high-efficiency mechanization to drive market

- 17.3.6 SPAIN

- 17.3.6.1 EU CAP-backed subsidies, improved farm income, and modernization demand in permanent crops to drive market

- 17.3.7 TURKEY

- 17.3.7.1 Declining growth due to rising input costs

- 17.3.8 UK

- 17.3.8.1 Non-arable and diversified farm use cases to drive market

- 17.3.9 REST OF EUROPE

- 17.3.1 FRANCE

- 17.4 NORTH AMERICA

- 17.4.1 US

- 17.4.1.1 Reduced demand due to high interest rates, lower commodity prices, and elevated dealer inventories

- 17.4.2 CANADA

- 17.4.2.1 Smaller tractor demand and steady replacement cycles to drive market

- 17.4.3 MEXICO

- 17.4.3.1 Increasing presence of OEMs to drive market

- 17.4.1 US

- 17.5 REST OF THE WORLD

- 17.5.1 ARGENTINA

- 17.5.1.1 Prevalence of mid- and high-horsepower tractor segments to drive market

- 17.5.2 BRAZIL

- 17.5.2.1 Improved financing through agricultural credit programs to drive market

- 17.5.3 OTHERS

- 17.5.1 ARGENTINA

- 17.6 INDUSTRY INSIGHTS

18 COMPETITIVE LANDSCAPE

- 18.1 OVERVIEW

- 18.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2026

- 18.3 REVENUE ANALYSIS, 2021-2025

- 18.4 MARKET SHARE ANALYSIS, 2025

- 18.5 COMPANY VALUATION AND FINANCIAL METRICS

- 18.6 BRAND/PRODUCT COMPARISON

- 18.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 18.7.1 STARS

- 18.7.2 EMERGING LEADERS

- 18.7.3 PERVASIVE PLAYERS

- 18.7.4 PARTICIPANTS

- 18.7.5 COMPANY FOOTPRINT

- 18.7.5.1 Company footprint

- 18.7.5.2 Region footprint

- 18.7.5.3 Propulsion footprint

- 18.7.5.4 Drive type footprint

- 18.7.5.5 Equipment type footprint

- 18.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 18.8.1 PROGRESSIVE COMPANIES

- 18.8.2 RESPONSIVE COMPANIES

- 18.8.3 DYNAMIC COMPANIES

- 18.8.4 STARTING BLOCKS

- 18.8.5 COMPETITIVE BENCHMARKING

- 18.8.5.1 List of startups/SMEs

- 18.8.5.2 Competitive benchmarking of startups/SMEs

- 18.9 COMPETITIVE SCENARIO

- 18.9.1 PRODUCT LAUNCHES/DEVELOPMENTS

- 18.9.2 DEALS

- 18.9.3 EXPANSIONS

- 18.9.4 OTHER DEVELOPMENTS

19 COMPANY PROFILES

- 19.1 KEY PLAYERS

- 19.1.1 DEERE & COMPANY

- 19.1.1.1 Business overview

- 19.1.1.2 Products offered

- 19.1.1.3 Recent developments

- 19.1.1.3.1 Product launches/developments

- 19.1.1.3.2 Deals

- 19.1.1.3.3 Expansions

- 19.1.1.3.4 Other developments

- 19.1.1.4 MnM view

- 19.1.1.4.1 Key strengths

- 19.1.1.4.2 Strategic choices

- 19.1.1.4.3 Weaknesses and competitive threats

- 19.1.2 CNH INDUSTRIAL

- 19.1.2.1 Business overview

- 19.1.2.2 Products offered

- 19.1.2.3 Recent developments

- 19.1.2.3.1 Product launches/developments

- 19.1.2.3.2 Deals

- 19.1.2.3.3 Expansions

- 19.1.2.3.4 Other developments

- 19.1.2.4 MnM view

- 19.1.2.4.1 Key strengths

- 19.1.2.4.2 Strategic choices

- 19.1.2.4.3 Weaknesses and competitive threats

- 19.1.3 MAHINDRA & MAHINDRA

- 19.1.3.1 Business overview

- 19.1.3.2 Products offered

- 19.1.3.3 Recent developments

- 19.1.3.3.1 Product launches/developments

- 19.1.3.3.2 Deals

- 19.1.3.3.3 Expansions

- 19.1.3.4 MnM view

- 19.1.3.4.1 Key strengths

- 19.1.3.4.2 Strategic choices

- 19.1.3.4.3 Weaknesses and competitive threats

- 19.1.4 AGCO CORPORATION

- 19.1.4.1 Business overview

- 19.1.4.2 Products offered

- 19.1.4.3 Recent developments

- 19.1.4.3.1 Product launches/developments

- 19.1.4.3.2 Deals

- 19.1.4.3.3 Expansions

- 19.1.4.3.4 Other developments

- 19.1.4.4 MnM view

- 19.1.4.4.1 Key strengths

- 19.1.4.4.2 Strategic choices

- 19.1.4.4.3 Weaknesses and competitive threats

- 19.1.5 KUBOTA CORPORATION

- 19.1.5.1 Business overview

- 19.1.5.2 Products offered

- 19.1.5.3 Recent developments

- 19.1.5.3.1 Product launches/developments

- 19.1.5.3.2 Deals

- 19.1.5.3.3 Expansions

- 19.1.5.3.4 Other developments

- 19.1.5.4 MnM view

- 19.1.5.4.1 Key strengths

- 19.1.5.4.2 Strategic choices

- 19.1.5.4.3 Weaknesses and competitive threats

- 19.1.6 CLAAS KGAA

- 19.1.6.1 Business overview

- 19.1.6.2 Products offered

- 19.1.6.3 Recent developments

- 19.1.6.3.1 Product launches/developments

- 19.1.6.3.2 Deals

- 19.1.6.3.3 Expansions

- 19.1.6.3.4 Other developments

- 19.1.7 ISEKI & CO., LTD.

- 19.1.7.1 Business overview

- 19.1.7.2 Products offered

- 19.1.7.3 Recent developments

- 19.1.7.3.1 Product launches/developments

- 19.1.7.3.2 Expansions

- 19.1.8 ESCORTS KUBOTA LIMITED

- 19.1.8.1 Business overview

- 19.1.8.2 Products offered

- 19.1.8.3 Recent developments

- 19.1.8.3.1 Product launches/developments

- 19.1.8.3.2 Deals

- 19.1.8.3.3 Expansions

- 19.1.9 SDF GROUP

- 19.1.9.1 Business overview

- 19.1.9.2 Products offered

- 19.1.9.3 Recent developments

- 19.1.9.3.1 Product launches/developments

- 19.1.9.3.2 Deals

- 19.1.9.3.3 Expansions

- 19.1.9.3.4 Other developments

- 19.1.10 YANMAR HOLDINGS CO., LTD.

- 19.1.10.1 Business overview

- 19.1.10.2 Products offered

- 19.1.10.3 Recent developments

- 19.1.10.3.1 Product launches/developments

- 19.1.10.3.2 Deals

- 19.1.10.3.3 Expansions

- 19.1.10.3.4 Other developments

- 19.1.1 DEERE & COMPANY

- 19.2 OTHER PLAYERS

- 19.2.1 JCB

- 19.2.2 TRACTORS AND FARM EQUIPMENT

- 19.2.3 SONALIKA

- 19.2.4 TYM CORPORATION

- 19.2.5 DAEDONG CORPORATION

- 19.2.6 EXEL INDUSTRIES LTD.

- 19.2.7 BUCHER INDUSTRIES AG

- 19.2.8 ZETOR TRACTORS A.S.

- 19.2.9 ARGO TRACTORS S.P.A.

- 19.2.10 CONCERN TRACTOR PLANTS

- 19.2.11 AMAZONE H. DREYER GMBH & CO. KG

- 19.2.12 BUHLER INDUSTRIES INC.

- 19.2.13 AUTONOMOUS TRACTOR CORPORATION

- 19.2.14 CHANGZHOU DONGFENG AGRICULTURAL MACHINERY GROUP CO., LTD.

- 19.2.15 CHINA NATIONAL MACHINERY INDUSTRY CORPORATION

- 19.2.16 WEICHAI LOVOL HEAVY INDUSTRY CO., LTD.

- 19.2.17 BERNARD KRONE HOLDING SE & CO.

- 19.2.18 VERMEER CORPORATION

- 19.2.19 POTTINGER LANDTECHNIK GMBH

- 19.2.20 MINSK TRACTOR WORKS

- 19.2.21 HENAN QIANLI MACHINERY CO., LTD.

- 19.2.22 MASCHIO GASPARDO S.P.A.

- 19.2.23 ALAMO GROUP INC.

- 19.2.24 KOMATSU LTD.

- 19.2.25 CATERPILLAR INC.

- 19.2.26 PONSSE PLC

- 19.2.27 TIGERCAT INTERNATIONAL INC.

20 RESEARCH METHODOLOGY

- 20.1 RESEARCH DATA

- 20.1.1 SECONDARY DATA

- 20.1.1.1 List of secondary sources

- 20.1.1.2 Key data from secondary sources

- 20.1.2 PRIMARY DATA

- 20.1.2.1 List of primary participants

- 20.1.2.2 Breakdown of primary interviews

- 20.1.2.3 Major objectives of primary research

- 20.1.1 SECONDARY DATA

- 20.2 MARKET ESTIMATION METHODOLOGY

- 20.2.1 BOTTOM-UP APPROACH

- 20.2.2 TOP-DOWN APPROACH

- 20.3 DATA TRIANGULATION

- 20.4 FACTOR ANALYSIS

- 20.5 RESEARCH LIMITATIONS

- 20.6 RESEARCH ASSUMPTIONS AND RISK ASSESSMENT

21 RECOMMENDATIONS BY MARKETSANDMARKETS

- 21.1 ASIA OCEANIA TO DOMINATE FARM EQUIPMENT MARKET

- 21.2 KEY FOCUS AREAS OF ELECTRIC FARM TRACTORS

- 21.3 4WD TRACTORS FOR FUTURE APPLICATIONS

- 21.4 GROWTH IN DEMAND FOR AUTONOMOUS TRACTORS IN COMING YEARS

- 21.5 CONCLUSION

22 APPENDIX

- 22.1 INSIGHTS FROM INDUSTRY EXPERTS

- 22.2 DISCUSSION GUIDE

- 22.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 22.4 CUSTOMIZATION OPTIONS

- 22.4.1 FARM EQUIPMENT MARKET, BY DRIVE TYPE & COUNTRY

- 22.4.1.1 Asia Oceania

- 22.4.1.1.1 China

- 22.4.1.1.2 India

- 22.4.1.1.3 Japan

- 22.4.1.1.4 South Korea

- 22.4.1.1.5 Australia

- 22.4.1.1.6 Rest of Asia Oceania

- 22.4.1.2 Europe

- 22.4.1.2.1 Germany

- 22.4.1.2.2 France

- 22.4.1.2.3 UK

- 22.4.1.2.4 Spain

- 22.4.1.2.5 Russia

- 22.4.1.2.6 Italy

- 22.4.1.2.7 Poland

- 22.4.1.2.8 Turkiye

- 22.4.1.2.9 Rest of Europe

- 22.4.1.3 North America

- 22.4.1.3.1 US

- 22.4.1.3.2 Canada

- 22.4.1.3.3 Mexico

- 22.4.1.4 Rest of the World

- 22.4.1.4.1 Brazil

- 22.4.1.4.2 Argentina

- 22.4.1.4.3 Others

- 22.4.1.1 Asia Oceania

- 22.4.2 ELECTRIC TRACTOR MARKET, BY POWER OUTPUT & COUNTRY

- 22.4.2.1 Asia Oceania

- 22.4.2.1.1 China

- 22.4.2.1.2 India

- 22.4.2.1.3 Japan

- 22.4.2.1.4 South Korea

- 22.4.2.1.5 Australia

- 22.4.2.1.6 Rest of Asia Oceania

- 22.4.2.2 Europe

- 22.4.2.2.1 Germany

- 22.4.2.2.2 France

- 22.4.2.2.3 UK

- 22.4.2.2.4 Spain

- 22.4.2.2.5 Russia

- 22.4.2.2.6 Italy

- 22.4.2.2.7 Poland

- 22.4.2.2.8 Turkey

- 22.4.2.2.9 Rest of Europe

- 22.4.2.3 North America

- 22.4.2.3.1 US

- 22.4.2.3.2 Canada

- 22.4.2.3.3 Mexico

- 22.4.2.4 Rest of the World

- 22.4.2.4.1 Brazil

- 22.4.2.4.2 Argentina

- 22.4.2.4.3 Others

- 22.4.2.1 Asia Oceania

- 22.4.3 AGRICULTURE SPRAYER MARKET, BY TYPE

- 22.4.3.1 Self-propelled sprayers

- 22.4.3.2 Tractor-mounted sprayers

- 22.4.3.3 Trailed sprayers

- 22.4.3.4 Handheld sprayers

- 22.4.4 DETAILED ANALYSIS AND PROFILING OF ADDITIONAL MARKET PLAYERS (UP TO THREE)

- 22.4.1 FARM EQUIPMENT MARKET, BY DRIVE TYPE & COUNTRY

- 22.5 RELATED REPORTS

- 22.6 AUTHOR DETAILS