|

시장보고서

상품코드

2079664

자연언어처리(NLP) 시장 예측(-2031년) : 오퍼링별, 기술별, 능력별, 용도별, 업계별, 지역별Natural Language Processing (NLP) Market by Offering (NLP Platforms, NLP APIs, Integrated NLP Solutions), Capability (NLU, NLG, Machine Translation), Application (Customer Experience & Support, Document Process Automation) - Global Forecast to 2031 |

||||||

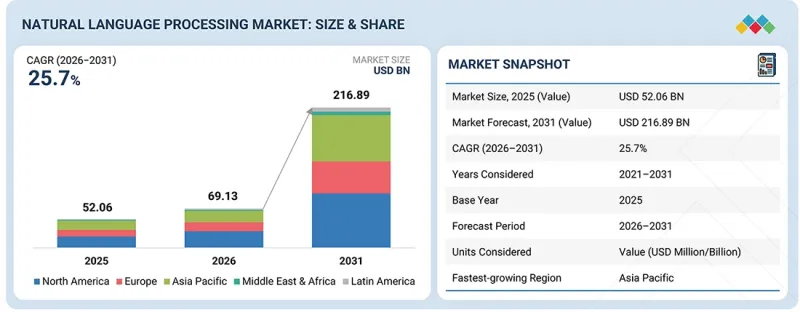

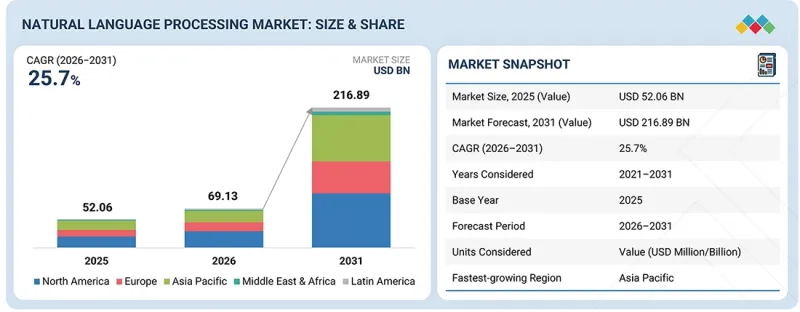

세계의 자연언어처리(NLP) 시장 규모는 2026년 691억 3,000만 달러에서 2031년까지 2,168억 9,000만 달러로 성장하며, 예측 기간 중 CAGR은 25.7%에 달할 것으로 전망되고 있습니다.

이러한 성장은 비정형 텍스트, 음성, 문서, 이메일, 티켓, 채팅, 계약서, 지식 저장소 등을 실용적인 비즈니스 인텔리전스로 전환하고자 하는 기업의 수요가 증가함에 따라 주도되고 있습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러) |

| 부문 | 오퍼링별, 기술별, 능력별, 용도별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카 및 라틴아메리카 |

생성형 AI, RAG, 기업 코파일럿, 대화형 인터페이스, 문서 인텔리전스의 급속한 보급에 따라 NLP의 활용 범위는 분석 중심의 사용 사례에서 워크플로우 자동화 및 지식 접근으로 확대되고 있습니다. 고객 지원, BFSI(은행·금융·보험), 의료, 소매, 법무 및 기업 생산성 향상 워크플로우 분야에서의 도입 확대가 시장 성장을 더욱 견인하고 있습니다. 그러나 높은 도입 비용, 통합의 복잡성, 양질의 도메인 특화 데이터 부족, 환각 위험, 편향, 개인정보 보호 문제, 낮은 추적성 등은 특히 규제가 엄격한 환경이나 대규모 기업 환경에서 계속해서 도입의 걸림돌이 되고 있습니다.

'RAG를 활용한 NLP는 신뢰할 수 있는 기업 지식에 대한 접근을 가능하게 하는 가장 빠르게 성장하고 있는 기술 계층으로 자리매김하고 있습니다.'

기술별로 살펴보면, 기업이 범용 모델의 출력 결과에서 내부 데이터나 승인된 지식 저장소와 연결된, 근거가 명확하고 출처가 명시된 응답으로 전환해 감에 따라 RAG 기반 NLP가 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다. 기업에서는 언어 모델을 계약서, 정책, 제품 설명서, 서비스 기록, 재무 문서, 기술 문서, 고객용 지식 기반과 연동하기 위해 검색 강화 생성(RAG)의 활용이 점점 더 늘어나고 있습니다. 이를 통해 조직은 답변의 관련성을 높이고, 근거 없는 응답을 줄이며, 직원과 고객이 기업 정보에 더 쉽게 접근할 수 있게 됩니다. 벤더에게 있으며, 큰 성장 기회는 벡터 검색, 기업 커넥터, 액세스 제어, 메타데이터 필터링, 워크플로우 통합 및 인용 지원 기능을 갖춘 RAG 지원 플랫폼을 구축하는 데 있습니다. 조직이 AI 파일럿 운영으로부터 실전 환경으로의 전환을 진행함에 따라 RAG를 지원하는 NLP는 지식 어시스턴트, 고객 지원 자동화, 법무 검토, 규정 준수 워크플로우, 현장 서비스 지원 및 기업 검색의 현대화 분야에서 핵심적인 역할을 수행하고 있습니다.

'자연 언어 이해는 기업 업무 흐름에 깊이 뿌리내리고 있으므로 2026년에도 여전히 가장 큰 기능 부문이 될 것입니다.'

역량별로 살펴보면, 자연 언어 이해는 업종을 불문하고 많은 성숙한 NLP 도입의 기반이 되고 있으므로 2026년에는 가장 큰 시장 점유율을 차지할 것으로 예상됩니다. 기업은 NLU를 활용하여 텍스트 분류, 의도 탐지, 엔티티 추출, 감정 식별, 티켓 라우팅, 문서 분석, 고객 문의 이해, 그리고 비정형 데이터로부터의 비즈니스 맥락 해석을 수행하고 있습니다. 이러한 높은 시장 점유율은 고객 서비스, BFSI(은행·금융·보험), 의료, 소매, 인사, 법무 및 기업의 지식 업무 흐름 분야에서 광범위하게 도입된 데 힘입은 것입니다. 이러한 분야에서는 조직이 방대한 양의 언어 데이터를 구조화된 유용한 정보로 변환해야 합니다. 생성형 AI의 기능은 급속히 발전하고 있지만, NLU는 챗봇, 컨택 센터, 보험금 청구 처리, 규정 준수 모니터링, 문서 분석, 고객의 목소리(VoC) 플랫폼 등의 운영 시스템에 계속해서 깊이 통합되고 있습니다. 벤더는 도메인별 정확도 향상, 다국어 지원, 기업 시스템과의 통합, 그리고 규제 대상 사용 사례에서의 설명 가능성 향상을 통해 이 분야에서 입지를 강화할 수 있습니다.

'북미는 기업의 AI 도입이 활발하고 공급업체가 집중되어 있으며, 여전히 최대 NLP 시장으로 자리 잡고 있습니다. 한편, 아시아태평양은 다국어 NLP 도입이 확대되고 있으며, 가장 빠르게 성장하고 있는 NLP 시장이 되었습니다.

2026년에는 미국을 필두로 북미가 자연 언어 처리 시장에서 가장 큰 점유율을 차지할 것으로 예상됩니다. 이 지역은 높은 클라우드 보급률, 기업의 디지털 성숙도 향상, 그리고 마이크로소프트, 구글, AWS, OpenAI, Anthropic, 세일즈포스, IBM, 오라클, Databricks와 같은 주요 NLP 및 AI 벤더들의 입지라는 이점을 누리고 있습니다. 이 지역의 기업은 고객 지원 자동화, 의료 문서 관리, BFSI(은행·금융·보험) 분야의 규정 준수, 기업 검색, 생산성 향상 지원 툴, 법무 워크플로우, 문서 인텔리전스 등 다양한 분야에서 NLP를 적극적으로 도입하고 있습니다. 또한 성숙한 데이터 인프라, AI 예산 확충, NLP를 파일럿 단계로부터 실전 환경으로 전환할 준비가 갖춰진 점도 대규모 도입을 지원하고 있습니다.

아시아태평양은 급속한 디지털 전환, 클라우드 배포 확대, 기업내 자동화 진전, 그리고 다국어 커뮤니케이션에 대한 강력한 수요에 힘입어 자연 언어 처리 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상됩니다. 중국, 인도, 일본, 한국, 싱가포르, 호주 등에서는 고객 참여, 번역, 음성 분석, BFSI, 의료, E-Commerce, 통신, 정부 서비스 등 다양한 분야에서 NLP에 대한 수요가 증가하고 있습니다. 또한 정부 주도의 AI 프로그램, 대규모 디지털 사용자 기반, 현지 언어를 지원하는 AI 모델에 대한 투자 확대도 이 지역의 성장을 지원하고 있습니다. 벤더는 지역 언어 지원, 유연한 가격 정책, 클라우드 파트너십, 그리고 산업별 맞춤형 NLP 솔루션을 통해 이러한 기회를 활용할 수 있습니다.

IBM(미국), Microsoft(미국), AWS(미국), Google(미국), Oracle(미국), OpenAI(미국), Baidu(중국), SAP(독일), Salesforce(미국), SAS(미국), Alibaba Cloud(중국), Tencent Cloud(중국), Anthropic(미국), Databricks(미국), iFLYTEK(중국), Qualtrics(미국), Medallia(미국), Elastic(미국), ABBYY(미국), Nuance Communications(미국), Cohere(캐나다), DataRobot(미국), Kore.ai(미국), Cerence AI(미국), DeepL(독일), Mistral AI(프랑스), Hugging Face(미국), AI21 Labs(이스라엘), Explosion(독일), Expert.ai(이탈리아), Deepgram(미국), AssemblyAI(미국), Speechmatics(영국), ElevenLabs(미국), Gladia(프랑스), Unbabel(포르투갈), Smartling(미국), Rasa(미국), Cognigy(독일), Parloa(독일), PolyAI(영국), Ada(캐나다), Hyro(미국), Algolia(미국), Instabase(미국), Hyperscience(미국), John Snow Labs(미국), Writer(미국), SoundHound AI(미국), Symbl.ai(미국), Rossum(영국), Lexalytics(미국), LlamaIndex(미국) 및 Glean(미국)은 자연언어처리 시장의 주요 기업의 일부입니다.

본 조사에서는 자연 언어 처리 시장의 주요 기업에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 조사 보고서에서는 자연 언어 처리 시장을 제공 형태(소프트웨어 및 서비스), 기술(규칙 기반 및 기호형 NLP, 통계적 및 고전적 기계학습 NLP, 딥러닝 및 신경망 NLP, 트랜스포머 기반 및 생성형 NLP, RAG 지원 NLP, 기타 기술), 기능(자연 언어 이해, 자연 언어 생성, 기계 번역·다국어 처리, 음성·구어 처리), 용도(고객 경험·지원, 마케팅·브랜드 인텔리전스, 지식 관리·발견, 규정 준수, 법무·리스크 인텔리전스, 조사·정보 인텔리전스, 직원 생산성·자동화, 번역·현지화, 문서 처리 자동화 및 기타 용도), 산업별(BFSI, 헬스케어·생명과학, 소매·E-Commerce, 소프트웨어·기술, 미디어·엔터테인먼트, 통신, 정부·국방, 제조, 물류·운송, 교육·EdTech 및 기타 산업), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카 및 라틴아메리카)로 분류되어 있습니다. 이 보고서의 조사 범위에는 자연 언어 처리 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약 요인, 과제, 기회 등)에 관한 상세한 정보가 포함되어 있습니다. 주요 업계 기업에 대해서는 사업 개요, 솔루션, 서비스, 주요 전략, 계약·제휴·합의, 신제품·서비스 출시, 합병·인수, 그리고 자연 언어 처리 시장과 관련된 최근 동향에 대한 인사이트를 제공하기 위해 상세한 분석이 이루어지고 있습니다. 이 보고서에서는 자연 언어 처리 시장의 생태계에서 두각을 보이고 있는 스타트업 기업에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 선도 기업 및 신규 진입 기업을 대상으로, 자연 언어 처리 시장 전체 및 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 파악하고, 자사의 비즈니스를 보다 적절하게 포지셔닝하며, 적절한 시장 진입 전략을 수립하기 위한 추가적인 인사이트를 얻을 수 있습니다. 또한 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 얻는 데에도 도움이 됩니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인 분석(비정형 데이터 인텔리전스에 대한 기업의 지출 증가가 NLP 도입을 촉진하고 있습니다. 생성형 AI는 NLP의 적용 범위를 분석에서 컨텐츠 및 지식 워크플로로 확대하고 있습니다. 고객 지원 및 직원 생산성 향상과 같은 활용 사례가 도입을 가속화하고 있습니다. 다국어 및 음성 중심의 참여가 대상 시장을 확대하고 있습니다.), 제약 요인(기업내 NLP 도입은 여전히 비용이 높고 통합 작업이 번거롭습니다; 깨끗하고 라벨이 지정된 도메인별 데이터가 부족하여 모델의 성능이 제한되고 있습니다.), 기회(RAG를 활용한 NLP가 신뢰할 수 있는 지식에 대한 접근을 실현하는 기업 계층으로 부상하고 있습니다; 산업 특화형 NLP가 고부가가치의 규제 대상 워크플로우를 개발하고 있습니다; 문서 인텔리전스는 NLP에 있으며, 가장 명확한 수익화 경로 중 하나를 제공하고 있습니다.) 및 과제(환각 현상, 편향, 추적 가능성의 부족이 여전히 신뢰를 제한하고 있습니다; 언어, 형식, 기업 시스템을 아우르는 NLP의 확장성은 여전히 어렵습니다.)

- 제품 개발/혁신: 자연 언어 처리 시장의 향후 기술, 연구개발 활동 및 신제품·서비스 출시에 관한 상세 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 - 다양한 지역에 걸친 자연 언어 처리 시장 분석

- 시장의 다양화: 자연 언어 처리 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁 분석 : 자연언어처리 시장에서 Microsoft(미국), Google(미국), AWS(미국), OpenAI(미국), Anthropic(미국), Salesforce(미국), IBM(미국), iFLYTEK(중국), Oracle(미국), Nuance Communications(미국) 등의 시장 점유율, 성장 전략, 서비스 제공에 관한 상세한 평가

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, 특허, 혁신, 향후 응용

제7장 규제 상황

제8장 고객 상황과 구매 행동

제9장 자연언어처리 시장(오퍼링별)

제10장 자연언어처리 시장(기술별)

제11장 자연언어처리 시장(능력별)

제12장 자연언어처리 시장(용도별)

제13장 자연언어처리 시장(업계별)

제14장 자연언어처리 시장(지역별)

제15장 경쟁 구도

제16장 기업 개요

제17장 조사 방법

제18장 인접 시장 및 관련 시장

제19장 부록

KSAThe global natural language processing (NLP) market is projected to grow from USD 69.13 billion in 2026 to USD 216.89 billion by 2031, at a CAGR of 25.7% during the forecast period. Growth is being driven by rising enterprise demand to convert unstructured text, speech, documents, emails, tickets, chats, contracts, and knowledge repositories into usable business intelligence.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Offering, Technology, Capability, Application, Vertical, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

The rapid adoption of generative AI, RAG, enterprise copilots, conversational interfaces, and document intelligence is expanding NLP from analytics-led use cases to workflow automation and knowledge access. Increasing deployment across customer support, BFSI, healthcare, retail, legal, and enterprise productivity workflows is further strengthening market growth. However, high implementation cost, integration complexity, shortage of clean domain-specific data, hallucination risk, bias, privacy concerns, and weak traceability continue to restrain adoption, especially in regulated and large-scale enterprise environments.

"RAG-enabled NLP is becoming the fastest-growing technology layer for trusted enterprise knowledge access"

By technology, RAG-enabled NLP is expected to be the fastest-growing market as enterprises shift from generic model outputs to grounded, source-backed responses linked to internal data and approved knowledge repositories. Businesses are increasingly using retrieval-augmented generation to connect language models with contracts, policies, product manuals, service records, financial documents, technical documentation, and customer knowledge bases. This allows organizations to improve answer relevance, reduce unsupported responses, and make enterprise information more accessible to employees and customers. The high-growth opportunity for vendors lies in building RAG-ready platforms with vector search, enterprise connectors, access controls, metadata filtering, workflow integration, and citation support. As organizations move from AI pilots to production deployments, RAG-enabled NLP is becoming central to knowledge assistants, customer support automation, legal review, compliance workflows, field service support, and enterprise search modernization.

"Natural language understanding remains the largest capability segment in 2026 due to its deep enterprise workflow penetration"

By capability, natural language understanding is expected to hold the largest market share in 2026 because it forms the foundation for many mature NLP deployments across industries. Enterprises use NLU to classify text, detect intent, extract entities, identify sentiment, route tickets, analyze documents, understand customer queries, and interpret business context from unstructured data. Its larger share is supported by widespread adoption in customer service, BFSI, healthcare, retail, HR, legal, and enterprise knowledge workflows, where organizations need to convert large volumes of language data into structured, usable information. While generative capabilities are growing rapidly, NLU remains deeply embedded in operational systems such as chatbots, contact centers, claims processing, compliance monitoring, document analytics, and voice-of-customer platforms. Vendors can strengthen their position in this segment by improving domain accuracy, multilingual support, integration with enterprise systems, and explainability for regulated use cases.

"North America remains the largest NLP market due to strong enterprise AI adoption and vendor concentration, while Asia Pacific is the fastest-growing NLP market as multilingual NLP adoption expands"

North America is expected to hold the largest share of the natural language processing market in 2026, led by the US. The region benefits from high cloud adoption, strong enterprise digital maturity, and the presence of leading NLP and AI vendors such as Microsoft, Google, AWS, OpenAI, Anthropic, Salesforce, IBM, Oracle, and Databricks. Enterprises in the region are actively deploying NLP across customer support automation, healthcare documentation, BFSI compliance, enterprise search, productivity copilots, legal workflows, and document intelligence. Large-scale adoption is also supported by mature data infrastructure, stronger AI budgets, and greater readiness to move NLP from pilots into production-grade deployments.

Asia Pacific is expected to be the fastest-growing region in the natural language processing market, supported by rapid digital transformation, rising cloud adoption, expanding enterprise automation, and strong multilingual communication needs. Countries such as China, India, Japan, South Korea, Singapore, and Australia are seeing increased demand for NLP across customer engagement, translation, speech analytics, BFSI, healthcare, e-commerce, telecom, and government services. Regional growth is also supported by government-backed AI programs, large digital user bases, and increasing investment in local-language AI models. Vendors can tap this opportunity through regional language support, flexible pricing, cloud partnerships, and verticalized NLP solutions.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the Natural language processing market.

- By Company: Tier 1 - 25%, Tier 2 - 41%, and Tier 3 - 34%

- By Designation: Directors - 31%, Managers - 46%, and Others - 23%

- By Region: North America - 39%, Europe - 22%, Asia Pacific - 28%, Middle East & Africa - 4%, and Latin America - 7%

IBM (US), Microsoft (US), AWS (US), Google (US), Oracle (US), OpenAI (US), Baidu (China), SAP (Germany), Salesforce (US), SAS (US), Alibaba Cloud (China), Tencent Cloud (China), Anthropic (US), Databricks (US), iFLYTEK (China), Qualtrics (US), Medallia (US), Elastic (US), ABBYY (US), Nuance Communications (US), Cohere (Canada), DataRobot (US), Kore.ai (US), Cerence AI (US), DeepL (Germany), Mistral AI (France), Hugging Face (US), AI21 Labs (Israel), Explosion (Germany), Expert.ai (Italy), Deepgram (US), AssemblyAI (US), Speechmatics (UK), ElevenLabs (US), Gladia (France), Unbabel (Portugal), Smartling (US), Rasa (US), Cognigy (Germany), Parloa (Germany), PolyAI (UK), Ada (Canada), Hyro (US), Algolia (US), Instabase (US), Hyperscience (US), John Snow Labs (US), Writer (US), SoundHound AI (US), Symbl.ai (US), Rossum (UK), Lexalytics (US), LlamaIndex (US), and Glean (US) are some of the key players in the natural language processing market.

The study includes an in-depth competitive analysis of these key players in the natural language processing market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the natural language processing market by offering (software and services), by technology (rule-based & symbolic NLP, statistical & classical machine learning NLP, deep learning & neural NLP, transformer-based & generative NLP, RAG-enabled NLP, and other technologies), by capability (natural language understanding, natural language generation, machine translation & multilingual processing, and speech & spoken language processing), by application (customer experience & support, marketing & brand intelligence, knowledge management & discovery, compliance, legal & risk intelligence, research & information intelligence, workforce productivity & automation, translation & localization, document process automation, and other applications), by vertical (BFSI, healthcare & life sciences, retail & e-commerce, software & technology, media & entertainment, telecommunications, government & defense, manufacturing, logistics & transportation, education & ed-tech, and other verticals), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the natural language processing market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements; new product & service launches; mergers and acquisitions; and recent developments associated with the natural language processing market. Competitive analysis of upcoming startups in the natural language processing market ecosystem is covered in this report.

Reasons to Buy This Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall natural language processing market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business better and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (growing enterprise spending on unstructured data intelligence is driving NLP adoption; generative AI is expanding NLP from analytics to content and knowledge workflows; customer support and employee productivity use cases are accelerating deployment; multilingual and voice-led engagement is widening the addressable market), restraints (enterprise NLP deployments remain costly and integration-heavy; shortage of clean, labeled, domain-specific data limits model performance), opportunities (RAG-enabled NLP is emerging as the enterprise layer for trusted knowledge access; vertical-specific NLP is opening high-value regulated workflows; document intelligence offers one of the clearest monetization paths for NLP), and challenges (hallucination, bias, and weak traceability continue to limit trust; scaling NLP across languages, formats, and enterprise systems remains difficult)

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and new product & service launches in the natural language processing market

- Market Development: Comprehensive information about lucrative markets - analysis of the natural language processing market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the natural language processing market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of Microsoft (US), Google (US), AWS (US), OpenAI (US), Anthropic (US), Salesforce (US), IBM (US), iFLYTEK (China), Oracle (US), and Nuance Communications (US), among others, in the natural language processing market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN NATURAL LANGUAGE PROCESSING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES IN NATURAL LANGUAGE PROCESSING MARKET

- 3.2 NATURAL LANGUAGE PROCESSING MARKET, BY REGION

- 3.3 NATURAL LANGUAGE PROCESSING MARKET: TOP THREE NLP SOFTWARE

- 3.4 NORTH AMERICA: NATURAL LANGUAGE PROCESSING MARKET, BY OFFERING AND CAPABILITY

- 3.5 NATURAL LANGUAGE PROCESSING MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Growing enterprise spending on unstructured data intelligence is driving NLP adoption

- 4.2.1.2 Generative AI is expanding NLP from analytics to content and knowledge workflows

- 4.2.1.3 Customer support and employee productivity use cases are accelerating deployment

- 4.2.1.4 Multilingual and voice-led engagement is widening the addressable market

- 4.2.2 RESTRAINTS

- 4.2.2.1 Enterprise NLP deployments remain costly and integration-heavy

- 4.2.2.2 Shortage of clean, labeled, domain-specific data limits model performance

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 RAG-enabled NLP is emerging as the enterprise layer for trusted knowledge access

- 4.2.3.2 Vertical-specific NLP is opening high-value regulated workflows

- 4.2.3.3 Document intelligence offers one of the clearest monetization paths for NLP

- 4.2.4 CHALLENGES

- 4.2.4.1 Hallucination, bias, and weak traceability continue to limit trust

- 4.2.4.2 Scaling NLP across languages, formats, and enterprise systems remains difficult

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN NATURAL LANGUAGE PROCESSING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 EVOLUTION OF NLP

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 INTENSITY OF COMPETITIVE RIVALRY

- 5.2.2 BARGAINING POWER OF SUPPLIERS

- 5.2.3 BARGAINING POWER OF BUYERS

- 5.2.4 THREAT OF SUBSTITUTES

- 5.2.5 THREAT OF NEW ENTRANTS

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN THE CONVERSATIONAL AI INDUSTRY

- 5.3.4 TRENDS IN THE GENERATIVE AI INDUSTRY

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 NLP SOLUTION PROVIDERS

- 5.5.1.1 NLP Platform Providers

- 5.5.1.2 NLP API Providers

- 5.5.1.3 Language Model Platform Providers

- 5.5.1.4 NLP Development Tool Providers

- 5.5.1.5 Integrated NLP Solution Providers

- 5.5.2 NLP SERVICE PROVIDERS

- 5.5.2.1 Professional Service Providers

- 5.5.2.2 Managed Service Providers

- 5.5.1 NLP SOLUTION PROVIDERS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF OFFERINGS, BY KEY PLAYER, 2026

- 5.6.2 AVERAGE SELLING PRICE OF APPLICATIONS, 2026

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 ERAJAYA ENHANCED E-COMMERCE SEARCH AND CUSTOMER SERVICE WITH GENERATIVE NLP

- 5.10.2 KLARNA DEPLOYED MULTILINGUAL AI ASSISTANT TO AUTOMATE CUSTOMER SERVICE AT SCALE

- 5.10.3 VOLVO GROUP STREAMLINED INVOICE AND CLAIMS PROCESSING WITH AI DOCUMENT INTELLIGENCE

- 5.10.4 MAYO CLINIC AND GOOGLE CLOUD ADVANCED GENERATIVE SEARCH FOR CLINICAL KNOWLEDGE DISCOVERY

- 5.10.5 BHASHINI EXPANDED MULTILINGUAL NLP ACCESS FOR DIGITAL PUBLIC SERVICES

- 5.10.6 VODAFONE ENHANCED TELECOM CUSTOMER SUPPORT THROUGH TOBI'S GENERATIVE CONVERSATIONAL AI

- 5.10.7 THOMSON REUTERS STRENGTHENED LEGAL RESEARCH AND DRAFTING WITH COCOUNSEL LEGAL

- 5.10.8 SERVICENOW SCALED NOW ASSIST ACROSS IT, HR, CUSTOMER SERVICE, AND KNOWLEDGE WORKFLOWS

- 5.11 IMPACT OF 2025 US TARIFF - NATURAL LANGUAGE PROCESSING MARKET

- 5.11.1 INTRODUCTION

- 5.11.1.1 Tariff/Trade Policy Updates (January-June 2026)

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.3.1 Strategic shifts and emerging trends

- 5.11.4 IMPACT ON COUNTRY/REGION

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 China

- 5.11.4.4 Asia Pacific (excluding China)

- 5.11.5 IMPACT ON END-USE INDUSTRIES

- 5.11.5.1 BFSI

- 5.11.5.2 Retail & E-commerce

- 5.11.5.3 Healthcare & Life Sciences

- 5.11.5.4 Software & Technology

- 5.11.5.5 Media & Entertainment

- 5.11.5.6 Telecommunications

- 5.11.5.7 Government & Defense

- 5.11.5.8 Manufacturing

- 5.11.5.9 Logistics & Transportation

- 5.11.5.10 Education & Ed-Tech

- 5.11.1 INTRODUCTION

6 TECHNOLOGICAL ADVANCEMENTS, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 TRANSFORMER ARCHITECTURE

- 6.1.2 ATTENTION MECHANISMS

- 6.1.3 WORD EMBEDDINGS & CONTEXTUAL EMBEDDINGS

- 6.1.4 SEQUENCE-TO-SEQUENCE MODELING

- 6.1.5 NAMED ENTITY RECOGNITION & INFORMATION EXTRACTION

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 REINFORCEMENT LEARNING FROM HUMAN FEEDBACK (RHLF)

- 6.2.2 FEDERATED LEARNING

- 6.2.3 DIFFERENTIAL PRIVACY

- 6.2.4 EXPLAINABLE AI

- 6.2.5 SYNTHETIC DATA GENERATION

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 AUTOMATIC SPEECH RECOGNITION

- 6.3.2 OPTICAL CHARACTER RECOGNITION

- 6.3.3 KNOWLEDGE GRAPHS

- 6.3.4 SEMANTIC SEARCH

- 6.3.5 MULTIMODAL AI

- 6.4 PATENT ANALYSIS

- 6.4.1 METHODOLOGY

- 6.4.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2026

- 6.4.3 INNOVATION AND PATENT APPLICATIONS

- 6.5 FUTURE APPLICATIONS

- 6.5.1 ENTERPRISE KNOWLEDGE AGENTS

- 6.5.2 CLINICAL LANGUAGE COPILOTS

- 6.5.3 REGULATORY INTELLIGENCE SYSTEMS

- 6.5.4 MULTILINGUAL CITIZEN SERVICES

- 6.5.5 AUTONOMOUS DOCUMENT WORKFLOWS

7 REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 KEY REGULATIONS

- 7.1.2.1 North America

- 7.1.2.1.1 Executive Order 14179 - Removing Barriers to American Leadership in NLP (US)

- 7.1.2.1.2 Federal Trade Commission Act, Section 5 (US)

- 7.1.2.1.3 NIST AI Risk Management Framework 1.0 (US)

- 7.1.2.1.4 Personal Information Protection and Electronic Documents Act (Canada)

- 7.1.2.2 Europe

- 7.1.2.2.1 Artificial Intelligence Act, Regulation (EU) 2024/1689 (EU)

- 7.1.2.2.2 General Data Protection Regulation (EU)

- 7.1.2.2.3 Digital Services Act (EU)

- 7.1.2.2.4 Federal Data Protection Act (Germany)

- 7.1.2.2.5 Data Protection Act (France)

- 7.1.2.2.6 Personal Data Protection Code (Italy)

- 7.1.2.2.7 Organic Law 3/2018 on Data Protection and Guarantee of Digital Rights (Spain)

- 7.1.2.2.8 UK General Data Protection Regulation and Data Protection Act 2018 (UK)

- 7.1.2.3 Asia Pacific

- 7.1.2.3.1 Act on the Protection of Personal Information (Japan)

- 7.1.2.3.2 Interim Measures for the Management of Generative Artificial Intelligence Services (China)

- 7.1.2.3.3 Personal Information Protection Law (China)

- 7.1.2.3.4 Digital Personal Data Protection Act, 2023 (India)

- 7.1.2.3.5 ASEAN Guide on AI Governance and Ethics (Southeast Asia)

- 7.1.2.3.6 Act on the Development of Artificial Intelligence and Establishment of Trust (South Korea)

- 7.1.2.3.7 Privacy Act 1988 (Australia)

- 7.1.2.4 Latin America

- 7.1.2.4.1 General Personal Data Protection Law (Brazil)

- 7.1.2.4.2 Federal Law on the Protection of Personal Data Held by Private Parties (Mexico)

- 7.1.2.4.3 Personal Data Protection Act, Law No. 25.326 (Argentina)

- 7.1.2.5 Middle East & Africa

- 7.1.2.5.1 Federal Decree-Law No. 45 of 2021 on Personal Data Protection (UAE)

- 7.1.2.5.2 Personal Data Protection Law (Saudi Arabia)

- 7.1.2.5.3 Protection of Personal Information Act (South Africa)

- 7.1.2.1 North America

- 7.1.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS VERTICALS

9 NATURAL LANGUAGE PROCESSING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 DRIVERS: NATURAL LANGUAGE PROCESSING MARKET, BY OFFERING

- 9.2 SOFTWARE

- 9.2.1 NLP PLATFORMS

- 9.2.1.1 NLP platforms evolving from single-task tools to unified orchestration environments covering full NLP lifecycles

- 9.2.1.2 Text Analytics Platforms

- 9.2.1.3 Text Mining Platforms

- 9.2.1.4 Knowledge Extraction Platforms

- 9.2.1.5 Domain-specific NLP Platforms

- 9.2.2 NLP APIS

- 9.2.2.1 NLP APIs become default delivery mechanism for language capability

- 9.2.2.2 Text Analytics APIs

- 9.2.2.3 Sentiment Analysis APIs

- 9.2.2.4 Entity Recognition APIs

- 9.2.2.5 Language Detection APIs

- 9.2.2.6 PII Detection APIs

- 9.2.3 LANGUAGE MODEL PLATFORMS

- 9.2.3.1 Language model platforms consolidating into tiered market where domain custodians occupy distinct commercial positions

- 9.2.3.2 Pre-trained Language Models

- 9.2.3.3 Fine-tuned Language Models

- 9.2.3.4 Domain-specific Language Models

- 9.2.3.5 Multilingual Language Models

- 9.2.4 NLP DEVELOPMENT TOOLS

- 9.2.4.1 NLP development tools shifting from low-level library toolkits to managed evaluation and orchestration environments

- 9.2.4.2 NLP Frameworks

- 9.2.4.3 NLP SDKs

- 9.2.4.4 Annotation Tools

- 9.2.4.5 Model Evaluation Tools

- 9.2.4.6 Prompt Engineering Tools

- 9.2.5 INTEGRATED NLP SOFTWARE

- 9.2.5.1 Integrated NLP software gaining prominence as language capability embeds into core SaaS applications

- 9.2.5.2 Customer Interaction NLP Software

- 9.2.5.3 Enterprise Workflow NLP Software

- 9.2.5.4 Document Processing NLP Software

- 9.2.5.5 Productivity NLP Software

- 9.2.5.6 Knowledge Management NLP Software

- 9.2.1 NLP PLATFORMS

- 9.3 SERVICES

- 9.3.1 PROFESSIONAL SERVICES

- 9.3.1.1 Professional services expanding as enterprise NLP deployments require regulatory alignment and multi-system integration

- 9.3.1.2 Consulting Services

- 9.3.1.3 System Integration Services

- 9.3.1.4 Custom Model Development Services

- 9.3.1.5 Model Fine-tuning Services

- 9.3.2 MANAGED SERVICES

- 9.3.2.1 Managed NLP services growing as production model operations complexity exceeds internal engineering capacity of enterprises

- 9.3.2.2 Model Monitoring Services

- 9.3.2.3 Data Annotation Services

- 9.3.2.4 Support & Maintenance Services

- 9.3.1 PROFESSIONAL SERVICES

10 LANGUAGE PROCESSING MARKET, BY TECHNOLOGY

- 10.1 INTRODUCTION

- 10.1.1 DRIVERS: NATURAL LANGUAGE PROCESSING MARKET, BY TECHNOLOGY

- 10.2 RULE-BASED & SYMBOLIC NLP

- 10.2.1 RULE-BASED & SYMBOLIC NLP RETAINS COMMERCIAL RELEVANCE IN RESOURCE-CONSTRAINED DEPLOYMENTS

- 10.3 STATISTICAL & CLASSICAL MACHINE LEARNING NLP

- 10.3.1 STATISTICAL & CLASSICAL ML NLP MAINTAINS COMMERCIAL NICHE IN HIGH-VOLUME, LOW-LATENCY APPLICATIONS

- 10.4 DEEP LEARNING & NEURAL NLP

- 10.4.1 DEEP LEARNING & NEURAL NLP DELIVER PROVEN ACCURACY AT MANAGEABLE INFERENCE COST

- 10.5 TRANSFORMER-BASED & GENERATIVE NLP

- 10.5.1 TRANSFORMER-BASED & GENERATIVE NLP ENABLE GENERAL-PURPOSE LANGUAGE PROCESSING AT COMMERCIALLY VIABLE COST

- 10.6 RAG-ENABLED NLP

- 10.6.1 RAG-ENABLED NLP RESOLVES KNOWLEDGE CURRENCY AND HALLUCINATION LIMITATIONS OF STATIC LANGUAGE MODELS

11 NATURAL LANGUAGE PROCESSING MARKET, BY CAPABILITY

- 11.1 INTRODUCTION

- 11.1.1 DRIVERS: NATURAL LANGUAGE PROCESSING MARKET, BY CAPABILITY

- 11.2 NATURAL LANGUAGE UNDERSTANDING (NLU)

- 11.2.1 NLU FORMS SEMANTIC FOUNDATION OF ENTERPRISE NLP PIPELINES THAT POWER DOWNSTREAM DECISION-MAKING

- 11.2.2 TEXT CLASSIFICATION & CATEGORIZATION

- 11.2.3 INFORMATION EXTRACTION

- 11.2.4 SENTIMENT, EMOTION & INTENT ANALYTICS

- 11.2.5 SEMANTIC & CONTEXTUAL UNDERSTANDING

- 11.3 NATURAL LANGUAGE GENERATION (NLG)

- 11.3.1 NLG TRANSITIONING FROM TEMPLATED REPORT PRODUCTION TO GENERATIVE, CONTEXT-AWARE TEXT CREATION

- 11.3.2 TEXT GENERATION

- 11.3.3 SUMMARIZATION

- 11.3.4 AUTOMATED NARRATIVE GENERATION

- 11.3.5 TEXT REWRITING & TRANSFORMATION

- 11.4 MACHINE TRANSLATION & MULTILINGUAL PROCESSING

- 11.4.1 MACHINE TRANSLATION & MULTILINGUAL PROCESSING GAINING STRATEGIC RELEVANCE IN CROSS-BORDER DIGITAL COMMERCE

- 11.4.2 MACHINE TRANSLATION

- 11.4.3 LOCALIZATION & LANGUAGE ADAPTATION

- 11.4.4 CROSS-LINGUAL INTELLIGENCE

- 11.5 SPEECH & SPOKEN LANGUAGE PROCESSING

- 11.5.1 SPEECH & SPOKEN LANGUAGE PROCESSING TURNING INTO COMPLETE INTELLIGENCE LAYER FOR ENTERPRISE AUDIO

- 11.5.2 SPEECH-TO-TEXT & TRANSCRIPTION

- 11.5.3 SPOKEN LANGUAGE UNDERSTANDING

- 11.5.4 VOICE & CONVERSATION ANALYTICS

12 NATURAL LANGUAGE PROCESSING MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- 12.1.1 DRIVERS: NATURAL LANGUAGE PROCESSING MARKET, BY APPLICATION

- 12.2 CUSTOMER EXPERIENCE & SUPPORT

- 12.2.1 CUSTOMER EXPERIENCE & SUPPORT LEADING NLP ADOPTION THROUGH AUTOMATED CUSTOMER INTERACTIONS

- 12.3 MARKETING & BRAND INTELLIGENCE

- 12.3.1 MARKETING & BRAND INTELLIGENCE TURNING CUSTOMER LANGUAGE SIGNALS INTO DECISION-READY INSIGHTS

- 12.4 KNOWLEDGE MANAGEMENT & DISCOVERY

- 12.4.1 KNOWLEDGE MANAGEMENT & DISCOVERY BECOMING BACKBONE OF ENTERPRISE KNOWLEDGE ACCESS

- 12.5 COMPLIANCE, LEGAL & RISK INTELLIGENCE

- 12.5.1 COMPLIANCE, LEGAL & RISK INTELLIGENCE STRENGTHENING GOVERNANCE IN LANGUAGE-HEAVY PROCESSES

- 12.6 RESEARCH & INFORMATION INTELLIGENCE

- 12.6.1 RESEARCH & INFORMATION INTELLIGENCE ACCELERATING INSIGHT EXTRACTION FROM UNSTRUCTURED CONTENT

- 12.7 WORKFORCE PRODUCTIVITY & AUTOMATION

- 12.7.1 WORKFORCE PRODUCTIVITY & AUTOMATION SCALING AS NLP ENTERS DAILY ENTERPRISE WORK

- 12.8 TRANSLATION & LOCALIZATION

- 12.8.1 TRANSLATION & LOCALIZATION SUPPORTING MULTILINGUAL ENGAGEMENT ACROSS GLOBAL OPERATIONS

- 12.9 DOCUMENT PROCESS AUTOMATION

- 12.9.1 DOCUMENT PROCESS AUTOMATION CONVERTING ENTERPRISE DOCUMENTS INTO STRUCTURED WORKFLOWS

- 12.10 OTHER APPLICATIONS

13 NATURAL LANGUAGE PROCESSING MARKET, BY VERTICAL

- 13.1 INTRODUCTION

- 13.1.1 DRIVERS: NATURAL LANGUAGE PROCESSING MARKET, BY VERTICAL

- 13.2 BFSI

- 13.2.1 BFSI STRENGTHENING RISK, COMPLIANCE, AND CUSTOMER INTELLIGENCE THROUGH NLP

- 13.3 RETAIL & E-COMMERCE

- 13.3.1 RETAIL & E-COMMERCE SCALING PERSONALIZED DISCOVERY AND CUSTOMER ENGAGEMENT WITH NLP

- 13.4 HEALTHCARE & LIFE SCIENCES

- 13.4.1 HEALTHCARE & LIFE SCIENCES ACCELERATING CLINICAL DOCUMENTATION AND RESEARCH INTELLIGENCE WITH NLP

- 13.5 SOFTWARE & TECHNOLOGY

- 13.5.1 SOFTWARE & TECHNOLOGY EMBEDDING NLP ACROSS DEVELOPER, SUPPORT, AND PRODUCT WORKFLOWS

- 13.6 MEDIA & ENTERTAINMENT

- 13.6.1 MEDIA & ENTERTAINMENT EXPANDING CONTENT INTELLIGENCE, LOCALIZATION, AND AUDIENCE ANALYTICS THROUGH NLP

- 13.7 TELECOMMUNICATIONS

- 13.7.1 TELECOMMUNICATIONS ENHANCING CUSTOMER OPERATIONS AND NETWORK SUPPORT INTELLIGENCE WITH NLP

- 13.8 GOVERNMENT & DEFENSE

- 13.8.1 GOVERNMENT & DEFENSE ADVANCING MULTILINGUAL SERVICES, INTELLIGENCE ANALYSIS, AND DOCUMENT AUTOMATION WITH NLP

- 13.9 MANUFACTURING

- 13.9.1 MANUFACTURING UNLOCKING OPERATIONAL INSIGHTS FROM SERVICE RECORDS, MANUALS, AND QUALITY DOCUMENTS

- 13.10 LOGISTICS & TRANSPORTATION

- 13.10.1 LOGISTICS & TRANSPORTATION IMPROVING EXCEPTION MANAGEMENT AND SHIPMENT INTELLIGENCE WITH NLP

- 13.11 EDUCATION & ED-TECH

- 13.11.1 EDUCATION & ED-TECH PERSONALIZING LEARNING, ASSESSMENT, AND STUDENT SUPPORT THROUGH NLP

- 13.12 OTHER VERTICALS

14 NATURAL LANGUAGE PROCESSING MARKET, BY REGION

- 14.1 INTRODUCTION

- 14.2 NORTH AMERICA

- 14.2.1 NORTH AMERICA: NATURAL LANGUAGE PROCESSING MARKET DRIVERS

- 14.2.2 US

- 14.2.2.1 United States setting global pace for NLP through frontier models, federal procurement, and enterprise automation

- 14.2.2.2 Key developments:

- 14.2.3 CANADA

- 14.2.3.1 Canada translating NLP research strength into enterprise adoption through compute access and applied AI programs

- 14.2.4 KEY DEVELOPMENTS:

- 14.3 EUROPE

- 14.3.1 EUROPE: NATURAL LANGUAGE PROCESSING MARKET DRIVERS

- 14.3.2 UK

- 14.3.2.1 United Kingdom accelerating NLP adoption through public sector AI, financial services demand, and flexible regulation

- 14.3.3 KEY DEVELOPMENTS

- 14.3.4 GERMANY

- 14.3.4.1 Germany strengthening NLP adoption through manufacturing workflows, compliance needs, and domestic AI infrastructure

- 14.3.5 KEY DEVELOPMENTS:

- 14.3.6 FRANCE

- 14.3.6.1 France building European NLP sovereignty through Mistral AI, low-carbon compute, and national AI infrastructure

- 14.3.7 KEY DEVELOPMENTS:

- 14.3.8 ITALY

- 14.3.8.1 Italy expanding NLP adoption through document intelligence and public administration modernization

- 14.3.9 KEY DEVELOPMENTS:

- 14.3.10 SPAIN

- 14.3.10.1 Spain scaling NLP through financial services maturity while working to improve SME adoption

- 14.3.11 KEY DEVELOPMENTS:

- 14.3.12 NETHERLANDS

- 14.3.12.1 Netherlands to advance production NLP through digital maturity, vector infrastructure, and responsible AI programs

- 14.3.13 KEY DEVELOPMENTS:

- 14.3.14 REST OF EUROPE

- 14.4 ASIA PACIFIC

- 14.4.1 ASIA PACIFIC: NATURAL LANGUAGE PROCESSING MARKET DRIVERS

- 14.4.2 CHINA

- 14.4.2.1 China to expand NLP influence through domestic LLMs, platform ecosystems, and AI content governance

- 14.4.3 INDIA

- 14.4.3.1 India to scale multilingual NLP through BHASHINI, IndiaAI compute access, and public digital infrastructure

- 14.4.4 JAPAN

- 14.4.4.1 Japan to promote Japanese-language NLP through national AI legislation and enterprise modernization

- 14.4.5 SOUTH KOREA

- 14.4.5.1 South Korea to accelerate sovereign NLP through national AI planning and semiconductor-backed infrastructure

- 14.4.6 ASEAN

- 14.4.6.1 ASEAN to build regional NLP sovereignty through SEA-LION, national LLMs, and mobile-first language demand

- 14.4.7 AUSTRALIA & NEW ZEALAND

- 14.4.7.1 Australia & New Zealand to expand NLP adoption through government AI enablement and enterprise productivity use cases

- 14.4.8 REST OF ASIA PACIFIC

- 14.5 MIDDLE EAST & AFRICA

- 14.5.1 MIDDLE EAST & AFRICA: NATURAL LANGUAGE PROCESSING MARKET DRIVERS

- 14.5.2 SAUDI ARABIA

- 14.5.2.1 Saudi Arabia to build Arabic NLP capability through HUMAIN, national AI programs, and sovereign compute

- 14.5.3 UAE

- 14.5.3.1 UAE to mainstream Arabic NLP through Stargate UAE, national AI access, and sovereign platforms

- 14.5.4 SOUTH AFRICA

- 14.5.4.1 South Africa to expand enterprise NLP readiness through cloud infrastructure, BFSI adoption, and AI skilling

- 14.5.5 TURKEY

- 14.5.5.1 Turkey to grow Turkish-language NLP through public digital services, banking adoption, and local technology capacity

- 14.5.6 QATAR

- 14.5.6.1 Qatar to advance Arabic NLP through national AI programs, digital government, and language resource development

- 14.5.7 REST OF MIDDLE EAST & AFRICA

- 14.6 LATIN AMERICA

- 14.6.1 LATIN AMERICA: AI TEST AUTOMATION MARKET DRIVERS

- 14.6.2 BRAZIL

- 14.6.2.1 1 Brazil to lead Latin American NLP through Portuguese-language demand, public AI policy, and data center expansion

- 14.6.3 MEXICO

- 14.6.3.1 Mexico to scale bilingual NLP through nearshoring, manufacturing documentation, and customer service automation

- 14.6.4 ARGENTINA

- 14.6.4.1 Argentina to position NLP growth around Spanish-language talent and planned AI infrastructure, despite execution risks

- 14.6.5 REST OF LATIN AMERICA

15 COMPETITIVE LANDSCAPE

- 15.1 OVERVIEW

- 15.2 KEY PLAYER STRATEGIES, 2021-2026

- 15.3 REVENUE ANALYSIS, 2021-2025

- 15.4 MARKET SHARE ANALYSIS, 2025

- 15.4.1 MARKET RANKING ANALYSIS, 2025

- 15.5 PRODUCT COMPARATIVE ANALYSIS

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS OF NLP PLATFORMS

- 15.5.1.1 Watson Natural Language Understanding/watsonx (IBM)

- 15.5.1.2 Visual Text Analytics (SAS)

- 15.5.1.3 Expert.ai Platform (expert.ai)

- 15.5.1.4 Healthcare NLP (John Snow Labs)

- 15.5.2 PRODUCT COMPARATIVE ANALYSIS OF INTEGRATED NLP SOFTWARE

- 15.5.2.1 Microsoft 365 Copilot (Microsoft)

- 15.5.2.2 Einstein/Agentforce (Salesforce)

- 15.5.2.3 Fusion AI (Oracle)

- 15.5.2.4 Joule (SAP)

- 15.5.1 PRODUCT COMPARATIVE ANALYSIS OF NLP PLATFORMS

- 15.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2025

- 15.6.1 STARS

- 15.6.2 EMERGING LEADERS

- 15.6.3 PERVASIVE PLAYERS

- 15.6.4 PARTICIPANTS

- 15.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2025

- 15.6.5.1 Company Footprint

- 15.6.5.2 Regional Footprint

- 15.6.5.3 Offering Footprint

- 15.6.5.4 Application Footprint

- 15.6.5.5 Vertical Footprint

- 15.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 15.7.1 PROGRESSIVE COMPANIES

- 15.7.2 RESPONSIVE COMPANIES

- 15.7.3 DYNAMIC COMPANIES

- 15.7.4 STARTING BLOCKS

- 15.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 15.7.5.1 Detailed list of key startups/SMEs

- 15.7.5.2 Competitive benchmarking of key startups/SMEs

- 15.8 COMPANY VALUATION AND FINANCIAL METRICS

- 15.9 COMPETITIVE SCENARIO

- 15.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 15.9.2 DEALS

16 COMPANY PROFILES

- 16.1 INTRODUCTION

- 16.2 KEY PLAYERS

- 16.2.1 IBM

- 16.2.1.1 Business overview

- 16.2.1.2 Products/Solutions/Services offered

- 16.2.1.3 Recent developments

- 16.2.1.3.1 Product launches & enhancements

- 16.2.1.3.2 Deals

- 16.2.1.4 MnM view

- 16.2.1.4.1 Key strengths

- 16.2.1.4.2 Strategic choices

- 16.2.1.4.3 Weaknesses and competitive threats

- 16.2.2 MICROSOFT

- 16.2.2.1 Business overview

- 16.2.2.2 Products/Solutions/Services offered

- 16.2.2.3 Recent developments

- 16.2.2.3.1 Product launches & enhancements

- 16.2.2.3.2 Deals

- 16.2.2.4 MnM view

- 16.2.2.4.1 Key strengths

- 16.2.2.4.2 Strategic choices

- 16.2.2.4.3 Weaknesses and competitive threats

- 16.2.3 AWS

- 16.2.3.1 Business overview

- 16.2.3.2 Products/Solutions/Services offered

- 16.2.3.3 Recent developments

- 16.2.3.3.1 Product launches & enhancements

- 16.2.3.3.2 Deals

- 16.2.3.4 MnM view

- 16.2.3.4.1 Key strengths

- 16.2.3.4.2 Strategic choices

- 16.2.3.4.3 Weaknesses and competitive threats

- 16.2.4 GOOGLE

- 16.2.4.1 Business overview

- 16.2.4.2 Products/Solutions/Services offered

- 16.2.4.3 Recent developments

- 16.2.4.3.1 Product launches & enhancements

- 16.2.4.3.2 Deals

- 16.2.4.4 MnM view

- 16.2.4.4.1 Key strengths

- 16.2.4.4.2 Strategic choices

- 16.2.4.4.3 Weaknesses and competitive threats

- 16.2.5 ORACLE

- 16.2.5.1 Business overview

- 16.2.5.2 Products/Solutions/Services offered

- 16.2.5.3 Recent developments

- 16.2.5.3.1 Product launches & enhancements

- 16.2.5.3.2 Deals

- 16.2.5.4 MnM view

- 16.2.5.4.1 Key strengths

- 16.2.5.4.2 Strategic choices

- 16.2.5.4.3 Weaknesses and competitive threats

- 16.2.6 OPENAI

- 16.2.6.1 Business overview

- 16.2.6.2 Products/Solutions/Services offered

- 16.2.6.3 Recent developments

- 16.2.6.3.1 Product launches & enhancements

- 16.2.6.3.2 Deals

- 16.2.7 BAIDU

- 16.2.7.1 Business overview

- 16.2.7.2 Products/Solutions/Services offered

- 16.2.7.3 Recent developments

- 16.2.7.3.1 Product launches and enhancements

- 16.2.7.3.2 Deals

- 16.2.8 SAP

- 16.2.8.1 Business overview

- 16.2.8.2 Products/Solutions/Services offered

- 16.2.8.3 Recent developments

- 16.2.8.3.1 Product launches & enhancements

- 16.2.8.3.2 Deals

- 16.2.9 SALESFORCE

- 16.2.9.1 Business overview

- 16.2.9.2 Products/Solutions/Services offered

- 16.2.9.3 Recent developments

- 16.2.9.3.1 Product launches and enhancements

- 16.2.9.3.2 Deals

- 16.2.10 SAS INSTITUTE

- 16.2.10.1 Business overview

- 16.2.10.2 Products/Solutions/Services offered

- 16.2.10.3 Recent developments

- 16.2.10.3.1 Product launches and enhancements

- 16.2.10.3.2 Deals

- 16.2.11 ALIBABA CLOUD

- 16.2.12 TENCENT CLOUD

- 16.2.13 ANTHROPIC

- 16.2.14 DATABRICKS

- 16.2.15 IFLYTEK

- 16.2.16 QUALTRICS

- 16.2.17 MEDALLIA

- 16.2.18 ELASTIC

- 16.2.19 ABBYY

- 16.2.20 NUANCE COMMUNICATIONS

- 16.2.21 COHERE

- 16.2.22 DATAROBOT

- 16.2.23 KORE.AI

- 16.2.24 CERENCE AI

- 16.2.25 DEEPL

- 16.2.1 IBM

- 16.3 STARTUP/SME PROFILES

- 16.3.1 MISTRAL AI

- 16.3.2 HUGGING FACE

- 16.3.3 AI21 LABS

- 16.3.4 EXPLOSION

- 16.3.5 EXPERT.AI

- 16.3.6 DEEPGRAM

- 16.3.7 ASSEMBLYAI

- 16.3.8 SPEECHMATICS

- 16.3.9 ELEVENLABS

- 16.3.10 GLADIA

- 16.3.11 UNBABEL

- 16.3.12 SMARTLING

- 16.3.13 RASA

- 16.3.14 NICE COGNIGY

- 16.3.15 PARLOA

- 16.3.16 POLYAI

- 16.3.17 ADA

- 16.3.18 HYRO

- 16.3.19 ALGOLIA

- 16.3.20 INSTABASE

- 16.3.21 HYPERSCIENCE

- 16.3.22 JOHN SNOW LABS

- 16.3.23 WRITER

- 16.3.24 SOUNDHOUND AI

- 16.3.25 SYMBL.AI

- 16.3.26 ROSSUM

- 16.3.27 LEXALYTICS

- 16.3.28 LLAMAINDEX

- 16.3.29 GLEAN

17 RESEARCH METHODOLOGY

- 17.1 RESEARCH DATA

- 17.1.1 SECONDARY DATA

- 17.1.2 PRIMARY DATA

- 17.1.2.1 Breakup of primary profiles

- 17.1.2.2 Key industry insights

- 17.2 MARKET BREAKUP AND DATA TRIANGULATION

- 17.3 MARKET SIZE ESTIMATION

- 17.3.1 TOP-DOWN APPROACH

- 17.3.2 BOTTOM-UP APPROACH

- 17.4 MARKET FORECAST

- 17.5 RESEARCH ASSUMPTIONS

- 17.6 STUDY LIMITATIONS

18 ADJACENT AND RELATED MARKETS

- 18.1 INTRODUCTION

- 18.2 CONVERSATIONAL AI MARKET - GLOBAL FORECAST TO 2031

- 18.2.1 MARKET DEFINITION

- 18.2.2 MARKET OVERVIEW

- 18.2.2.1 Conversational AI Market, By Offering

- 18.2.2.2 Conversational AI Market, By Product Type

- 18.2.2.3 Conversational AI Market, By Business Function

- 18.2.2.4 Conversational AI Market, By End User

- 18.2.2.5 Conversational AI Market, By Region

- 18.3 DOCUMENT AI MARKET - GLOBAL FORECAST TO 2030

- 18.3.1 MARKET DEFINITION

- 18.3.2 MARKET OVERVIEW

- 18.3.2.1 Document AI Market, By Offering

- 18.3.2.2 Document AI Market, By Deployment Mode

- 18.3.2.3 Document AI Market, By Document Type

- 18.3.2.4 Document AI Market, By Vertical

- 18.3.2.5 Document AI Market, By Region

19 APPENDIX

- 19.1 DISCUSSION GUIDE

- 19.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.3 CUSTOMIZATION OPTIONS

- 19.4 RELATED REPORTS

- 19.5 AUTHOR DETAILS