|

시장보고서

상품코드

2081120

3D 매핑 및 모델링 시장 예측(-2031년) : 오퍼링별, 배포 모드별, 조직 규모별, 업계별, 지역별3D Mapping and Modeling Market by Hardware (Data Capture, Mapping, Scanners, LIDAR, UAVs/Drones), Software (GIS & Spatial Analytics, Digital Twin, 3D Visualization, Reality Reconstruction, BIM, Point Cloud, Georeferencing) - Global Forecast to 2031 |

||||||

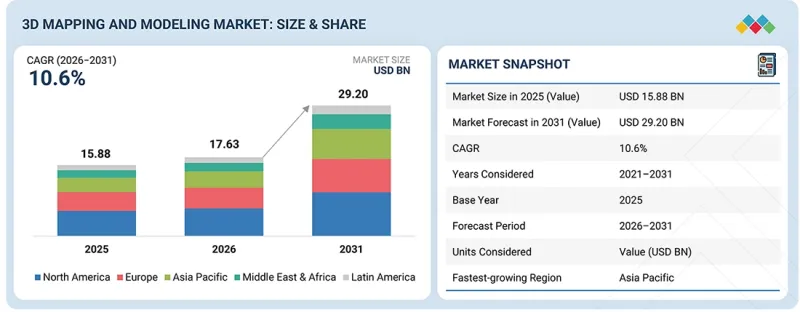

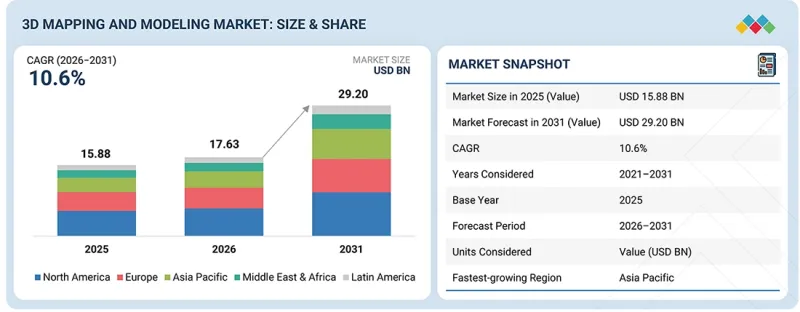

세계의 3D 매핑 및 모델링 시장 규모는 2026년 176억 3,000만 달러에서 2031년까지 292억 달러로 성장하며, CAGR은 10.6%에 달할 것으로 예측됩니다.

AI를 활용한 지리공간 플랫폼과 디지털 엔지니어링 워크플로우 덕분에 3D 매핑 및 모델링 시장의 발전이 가속화되고 있습니다. 이는 인프라 개발, 건설, 교통, 공공사업, 자산 관리 등 각 분야에서 조직들이 지능형 공간 기술을 점점 더 많이 도입하고 있다는 점이 배경이 되고 있습니다. AI를 활용한 특징 추출, 클라우드 기반 리얼리티 캡처, 디지털 트윈, 빌딩 정보 모델링(BIM), 자동 포인트 클라우드 처리 등의 혁신 기술을 통해 조직은 고정밀 3D 모델과 실용적인 지리 공간 인사이트를 생성할 수 있게 되었습니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2021-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(100만/10억 달러) |

| 부문 | 오퍼링별, 배포 모드별, 조직 규모별, 업계별, 지역별 |

| 대상 지역 | 북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카 |

기업은 계획의 정확성, 업무 효율성 및 프로젝트 간 협력을 향상시키기 위해, 광검출·거리측정(LiDAR), 사진측량, 전지구위성항법시스템(GNSS) 및 무인항공기(UAV)를 활용한 매핑 기술을 연결된 디지털 워크플로우에 통합하는 움직임을 강화하고 있습니다. 동시에, 클라우드 네이티브 플랫폼과 AI를 활용한 시각화 기능을 통해 대규모 지리공간 데이터 처리가 효율화되어 의사결정이 신속해지는 것은 물론, 복잡한 인프라 환경 전반에 걸친 종단간 디지털 엔지니어링 워크플로우가 지원되고 있습니다.

3D 매핑 및 모델링 시장의 각 업체들은 AI 기반 분석, 클라우드 협업, 리얼리티 캡처 기술, 상호 운용 가능한 지리 공간 플랫폼을 통합한 통일된 디지털 생태계를 구축함으로써 경쟁력을 강화하고 있습니다. 최신 솔루션은 고정밀 데이터 수집, 자동 모델 생성, 디지털 트윈, 지능형 시각화를 결합하여 인프라 계획, 건설 모니터링, 자산 점검, 수명 주기 관리의 향상을 도모하고 있습니다. 이러한 플랫폼은 현장과 사무실의 업무 흐름을 원활하게 동기화하는 동시에, 엔지니어링 및 지리공간 애플리케이션 전반에 걸친 데이터 접근성을 향상시킵니다. 조직들이 디지털 전환 노력을 가속화하는 가운데, 통합형 3D 매핑 플랫폼은 프로젝트 생산성, 공간 인텔리전스 및 인프라의 회복탄력성을 향상시키는 데 필수적인 요소로 자리 잡고 있습니다. 또한 각 벤더사는 지능형 지리공간 솔루션의 전사적 도입을 지원하기 위해 자동화, 오픈 데이터의 상호운용성, 그리고 확장 가능한 클라우드 아키텍처의 추진에도 힘쓰고 있습니다.

'인프라의 디지털화가 가속화되는 가운데, 디지털 트윈 플랫폼은 가장 빠르게 성장하는 소프트웨어 분야로 부상하고 있습니다'

업종을 불문하고, 조직들이 인프라의 디지털화와 자산의 현대화를 가속화함에 따라 디지털 트윈 소프트웨어 분야는 급속히 확대되고 있습니다. 디지털 트윈은 물리적 인프라 및 산업 자산의 실시간 가시화, 시뮬레이션, 수명 주기 관리를 가능하게 합니다. 조직들은 상호 연계된 엔지니어링 워크플로우를 구축하기 위해 디지털 트윈을 BIM, GIS, LiDAR, 리얼리티 캡처 기술과 통합하는 움직임을 강화하고 있습니다. 이러한 통합을 통해 자산의 전체 수명 주기에 걸쳐 프로젝트 계획, 운영 효율성, 예측 유지보수 및 인프라의 회복탄력성이 향상됩니다. AI를 활용한 분석 기능은 인프라 모니터링, 엔지니어링 관련 의사결정 및 위험 평가 능력을 강화합니다. 클라우드 연결을 통해 물리적 환경과 디지털 환경 간의 지속적인 동기화가 가능해질 뿐만 아니라, 공동 프로젝트 수행도 지원됩니다. 스마트 인프라, 커넥티드 건설 및 지능형 자산 관리에 대한 투자 확대는 디지털 트윈 소프트웨어의 도입을 더욱 가속화하고 있습니다. 이러한 장점 덕분에 디지털 트윈 플랫폼은 예측 기간 중 가장 빠르게 성장하는 소프트웨어 분야로서의 입지를 확고히 하고 있습니다.

'조직들이 확장 가능하고 상호 연계된 지리공간 워크플로우를 우선시함에 따라 2026년에는 클라우드 배포이 시장을 주도할 것으로 전망됩니다.'

조직들이 기업 환경 전반에 걸쳐 확장성이 뛰어나고 연결성이 높으며 데이터베이스의 지리공간 워크플로를 우선시함에 따라 클라우드 배포는 계속해서 확대되고 있습니다. 클라우드 플랫폼은 여러 프로젝트 현장에서 활동하는 엔지니어링, 측량, 건축, 건설, 인프라 개발 팀 간의 협업을 간소화합니다. 조직은 접근성이 향상된 클라우드 네이티브 환경을 통해 대규모 포인트 클라우드 데이터세트, 이미지, 지리 공간 정보를 안전하게 처리합니다. 클라우드 플랫폼은 분산된 팀 간의 상호 운용성, 통합된 데이터 관리, 그리고 전사적인 프로젝트 조정 능력을 향상시킵니다. 각 벤더사는 업무 효율을 높이기 위해 AI를 활용한 분석, 디지털 트윈, BIM 및 리얼리티 캡처 워크플로우를 클라우드 생태계에 통합하는 움직임을 강화하고 있습니다. 클라우드 배포을 통해 인프라의 복잡성이 완화되는 동시에, 소프트웨어 도입, 시스템 업그레이드 및 공동 의사결정이 가속화됩니다. 디지털 엔지니어링 활동, 원격 프로젝트 관리, 그리고 기업의 디지털 전환 전략 확대에 힘입어, 업종을 불문하고 클라우드 배포이 지속적으로 확대되고 있습니다. 이러한 기능 덕분에 2026년에는 클라우드 배포이 가장 큰 비중을 차지할 것으로 전망됩니다.

'북미는 첨단 지리공간 기술의 도입과 인프라 투자를 통해 2026년에도 계속해서 최대 규모의 3D 매핑 및 모델링 시장이 될 것입니다.'

북미는 첨단 지리공간 기술과 디지털 엔지니어링 솔루션의 조기 도입을 통해 2026년에도 여전히 가장 큰 시장 점유율을 유지하고 있습니다. 인프라 현대화를 위한 노력은 엔지니어링, 건설, 운송, 공공사업, 광업, 공공 인프라 등 각 분야에서 계속해서 투자를 주도하고 있습니다. 조직은 프로젝트 성과를 높이기 위해 LiDAR, 레이저 스캔, BIM, 디지털 트윈, 사진측량, AI를 활용한 매핑 플랫폼의 도입을 점점 더 확대하고 있습니다. 강력한 기술 생태계 덕분에, 산업 전반에 걸쳐 리얼리티 캡처, 클라우드 기반 협업, 공간 인텔리전스 플랫폼 분야의 혁신이 가속화되고 있습니다. 정부의 인프라 투자와 스마트 시티 구상은 첨단 매핑 및 모델링 기술에 대한 수요를 더욱 높이고 있습니다. 기업은 업무 효율성을 높이기 위해 클라우드 기반의 지리공간 워크플로우, 지능형 자동화, 통합형 엔지니어링 애플리케이션을 우선적으로 도입하고 있습니다. 지속적인 제품 혁신을 통해 인프라 계획, 프로젝트 가시화, 자산 수명 주기 관리 및 예측 유지보수 기능이 강화되고 있습니다. 이러한 요인들로 인해 예측 기간 중 북미는 전 세계 3D 매핑 및 모델링 시장에서 주도적인 입지를 공고히 할 것입니다.

'아시아태평양은 인프라 현대화와 지리공간 기술 도입이 가속화되고 있는 것을 배경으로, 3D 매핑 및 모델링 시장에서 가장 빠른 성장을 이룰 것으로 예상됩니다.'

아시아태평양은 대규모 인프라 투자와 급속한 도시화에 힘입어, 3D 매핑 및 모델링 기술 분야에서 가장 빠르게 성장하고 있는 지역 시장이 되었습니다. 각국 정부는 주요 경제권에서 교통, 공공사업, 산업 회랑, 스마트 시티 및 디지털 인프라 현대화 프로그램에 대한 투자를 지속하고 있습니다. 각 조직은 엔지니어링 생산성과 프로젝트 수행 능력을 향상시키기 위해 LiDAR, UAV 매핑, BIM, 디지털 트윈, 리얼리티 캡처의 도입을 확대하고 있습니다. 건설 활동과 인프라 확충은 여전히 첨단 지리공간 데이터 수집 및 시각화 솔루션에 대한 수요를 견인하고 있습니다. 산업의 디지털화는 제조, 광업, 에너지, 공공 인프라 등 각 분야에서 기술 도입을 더욱 가속화하고 있습니다. 클라우드 기반 엔지니어링 플랫폼, AI를 활용한 지리공간 분석, 그리고 커넥티드 건설 솔루션에 대한 투자 확대가 장기적인 시장 성장을 지원하고 있습니다. 이러한 추세에 따라 아시아태평양은 예측 기간 중 가장 빠르게 성장하는 지역 시장이 될 것으로 보이며, 건축·엔지니어링·건설(AEC), 에너지·공공사업, 정부·국방, 제조 등 여러 산업 분야에서 지속적인 비즈니스 기회가 예상됩니다.

이 보고서에는 3D 매핑 및 모델링용 하드웨어 시스템, 소프트웨어 툴, 플랫폼을 제공하는 주요 기업에 대한 조사 결과와 상세한 기업 개요이 포함되어 있습니다. 3D 매핑 및 모델링 분야의 주요 기업으로는 Trimble(미국), Autodesk(미국), Hexagon AB(스웨덴), AMETEK Inc.(미국), Topcon Corporation(일본), Teledyne Technologies(미국), Fugro(네덜란드), CoStar Group(미국), Bentley Systems(미국), Airbus(프랑스), TomTom(네덜란드), Esri(미국), Woolpert(미국), SAM Companies(미국), NavVis GmbH(독일), Artec 3D(룩셈부르크), VertiGIS(오스트리아), RIEGL Laser Measurement Systems(오스트리아), YellowScan(프랑스), Pix4D(스위스), Agisoft(러시아), DroneDeploy(미국), Safe Software(캐나다), Carlson Software(미국), Cupix(미국), Cintoo(프랑스), OpenSpace(미국), vGIS(캐나다), Nearmap(호주), Aerometrex(호주), Intermap Technologies(캐나다), Dynamic Map Platform(일본), Vexcel Imaging(오스트리아), CARTO(미국), MapLarge(미국), EarthDaily(캐나다), Caliper Corporation(미국), Spargeo(한국), Emesent(호주) 등이 있습니다.

조사 범위

본 조사 보고서에서는 3D 매핑 및 모델링 시장을 제공 유형별(하드웨어, 소프트웨어, 서비스), 배포 방식별(클라우드, 온프레미스, 하이브리드), 조직 규모별(대기업 및 중소기업), 산업별(농림업, 건축·엔지니어링·건설(AEC), 에너지·공공사업, 정부·국방, 제조업, 광업·광물, 석유 및 가스; 통신; 운송·물류; 기타) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카)로 분류하고 있습니다. 이 보고서의 조사 범위에는 3D 매핑 및 모델링 시장의 성장에 영향을 미치는 주요 요인(촉진요인, 제약 요인, 과제, 기회 등)에 대한 상세한 정보가 포함되어 있습니다. 주요 업계 진출 기업에 대한 상세한 분석을 통해 각 기업의 사업 개요, 솔루션, 서비스, 주요 전략, 계약·제휴·합의, 제품·서비스 출시, 합병·인수, 그리고 3D 매핑·모델링 시장과 관련된 최근 동향에 대한 인사이트를 제공합니다. 또한 이 보고서에서는 3D 매핑·모델링 시장 생태계에 진출하는 신생 기업에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 선도 기업 및 신규 진입 기업을 대상으로, 3D 매핑 및 모델링 시장 전체와 그 하위 부문의 매출에 대한 가장 정확한 추정치를 제공합니다. 이를 통해 이해관계자들은 경쟁 구도를 파악하고, 자사의 비즈니스를 보다 적절하게 포지셔닝하며, 적절한 시장 진입 전략을 수립하기 위한 추가적인 인사이트를 얻을 수 있습니다. 또한 시장 동향을 파악하고 주요 시장 촉진요인·과제 및 기회에 관한 정보를 얻는 데에도 도움이 됩니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

- 주요 촉진요인(산업·제조 자산에서의 디지털 트윈 도입 확대, 대규모 지리 공간 데이터 수집을 위한 UAV(무인 항공기)를 활용한 리얼리티 캡처의 채택 확대), 제약 요인(대규모 3D 데이터세트에 대한 높은 처리 능력 및 인프라 요구 사항, 항공 매핑 업무에 영향을 미치는 규제 및 공역 제한), 기회(기후 변화에 대한 내성, 환경 모니터링, 재해 모델링에 대한 수요 증가, 메타버스 및 확장 현실(XR) 애플리케이션에서의 몰입형 공간 경험 활용 확대), 그리고 과제(여러 데이터 수집 시스템에 걸쳐 정확성과 일관성 유지; 다양한 지리공간 데이터 형식 및 소프트웨어 생태계 간의 상호 운용성 확보)

- 제품 개발/혁신: 3D 매핑 및 모델링 시장의 향후 기술, 연구개발 활동, 그리고 제품 및 서비스 출시에 관한 상세 인사이트

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 및 각 지역의 3D 매핑·모델링 시장 분석

- 시장의 다양화: 3D 매핑 및 모델링 시장의 신제품·서비스, 미개발 지역, 최근 동향 및 투자에 관한 포괄적인 정보

- 경쟁사 분석: 3D 매핑 및 모델링 시장의 주요 기업, 즉 Trimble(미국), Autodesk(미국), Hexagon AB(스웨덴), AMETEK Inc.(미국), Topcon Corporation(일본), Teledyne Technologies(미국), Fugro(네덜란드), CoStar Group(미국), Bentley Systems(미국), Airbus(프랑스), TomTom(네덜란드), ESRI(미국), Woolpert(미국), SAM Companies(미국), NavVis GmbH(독일), Artec 3D(룩셈부르크) 등 주요 참여 기업의 시장 점유율, 성장 전략, 제공 제품 및 서비스에 대한 상세한 평가. 또한 이 보고서는 이해관계자들이 3D 매핑 및 모델링 시장의 동향을 파악하는 데 도움이 되며, 주요 시장 촉진요인, 제약 요인, 과제 및 기회에 대한 정보를 제공합니다.

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술 진보, AI에 의한 영향, 특허, 혁신, 향후 응용

제7장 관세와 규제 상황

제8장 고객 상황과 구매 행동

제9장 3D 매핑 및 모델링 시장(오퍼링별)

제10장 3D 매핑 및 모델링 시장(배포 모드별)

제11장 3D 매핑 및 모델링 시장(조직 규모별)

제12장 3D 매핑 및 모델링 시장(업계별)

제13장 3D 매핑 및 모델링 시장(지역별)

제14장 경쟁 구도

제15장 기업 개요

제16장 조사 방법

제17장 부록

KSAThe global 3D mapping and modeling market is projected to grow from USD 17.63 billion in 2026 to USD 29.20 billion by 2031, at a CAGR of 10.6%. AI-enabled geospatial platforms and digital engineering workflows are accelerating advancements in the 3D mapping and modeling market as organizations increasingly adopt intelligent spatial technologies for infrastructure development, construction, transportation, utilities, and asset management. Innovations such as AI-assisted feature extraction, cloud-based reality capture, digital twins, building information modeling (BIM), and automated point cloud processing enable organizations to generate highly accurate 3D models and actionable geospatial insights.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Million/Billion) |

| Segments | By Offering, Hardware, Software, Services, Deployment mode, Organization size, & Vertical |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, Latin America |

Enterprises are increasingly integrating light-detection and ranging (LiDAR), photogrammetry, global navigation satellite system (GNSS), and unmanned aerial vehicle (UAV) mapping technologies into connected digital workflows to improve planning accuracy, operational efficiency, and project collaboration. At the same time, cloud-native platforms and AI-driven visualization capabilities are streamlining large-scale geospatial data processing, enabling faster decision-making and supporting end-to-end digital engineering workflows across complex infrastructure environments.

Vendors in the 3D mapping and modeling market are strengthening their competitive capabilities by integrating AI-powered analytics, cloud collaboration, reality capture technologies, and interoperable geospatial platforms into unified digital ecosystems. Modern solutions combine high-accuracy data acquisition, automated model generation, digital twins, and intelligent visualization to improve infrastructure planning, construction monitoring, asset inspection, and lifecycle management. These platforms enable seamless synchronization of field and office workflows while improving data accessibility across engineering and geospatial applications. As organizations accelerate digital transformation initiatives, integrated 3D mapping platforms are becoming essential for enhancing project productivity, spatial intelligence, and infrastructure resilience. Vendors are also advancing automation, open data interoperability, and scalable cloud architectures to support enterprise-wide deployment of intelligent geospatial solutions.

"Digital twin platforms are emerging as the fastest-growing software segment as infrastructure digitalization accelerates"

The digital twin software segment is expanding rapidly as organizations accelerate infrastructure digitalization and asset modernization initiatives across industries. Digital twins enable real-time visualization, simulation, and lifecycle management of physical infrastructure and industrial assets. Organizations increasingly integrate digital twins with BIM, GIS, LiDAR, and reality capture technologies to establish connected engineering workflows. This integration improves project planning, operational efficiency, predictive maintenance, and infrastructure resilience throughout the asset lifecycle. AI-enabled analytics strengthen infrastructure monitoring, engineering decision-making, and risk assessment capabilities. Cloud connectivity enables continuous synchronization between physical and digital environments while supporting collaborative project execution. Growing investments in smart infrastructure, connected construction, and intelligent asset management further accelerate digital twin software adoption. These advantages position digital twin platforms as the fastest-growing software segment throughout the forecast period.

"Cloud deployment is likely to lead the market in 2026 as organizations prioritize scalable and connected geospatial workflows"

Cloud deployment continues to expand as organizations prioritize scalable, connected, and data-driven geospatial workflows across enterprise environments. Cloud platforms simplify collaboration among engineering, surveying, architecture, construction, and infrastructure development teams operating across multiple project locations. Organizations securely process large point cloud datasets, imagery, and geospatial information through cloud-native environments with improved accessibility. Cloud platforms improve interoperability, centralized data management, and enterprise-wide project coordination capabilities across distributed teams. Vendors increasingly integrate AI-powered analytics, digital twins, BIM, and reality capture workflows within cloud ecosystems to improve operational efficiency. Cloud deployment reduces infrastructure complexity while accelerating software implementation, system upgrades, and collaborative decision-making. Increasing digital engineering initiatives, remote project management, and enterprise digital transformation strategies continue strengthening cloud adoption across industries. These capabilities position cloud deployment as the largest deployment segment in 2026.

"North America remains the largest 3D mapping and modeling market in 2026 due to advanced geospatial technology adoption and infrastructure investments"

North America maintains the largest market share in 2026 through early adoption of advanced geospatial technologies and digital engineering solutions. Infrastructure modernization initiatives continue driving investments across engineering, construction, transportation, utilities, mining, and public infrastructure sectors. Organizations increasingly deploy LiDAR, laser scanning, BIM, digital twins, photogrammetry, and AI-enabled mapping platforms to improve project outcomes. Strong technology ecosystems accelerate innovation in reality capture, cloud-based collaboration, and spatial intelligence platforms across industries. Government infrastructure investments and smart city initiatives further strengthen demand for advanced mapping and modeling technologies. Enterprises prioritize cloud-enabled geospatial workflows, intelligent automation, and integrated engineering applications to improve operational efficiency. Continuous product innovation enhances infrastructure planning, project visualization, asset lifecycle management, and predictive maintenance capabilities. These factors reinforce North America's leadership in the global 3D mapping and modeling market throughout the forecast period.

"Asia Pacific is expected to be the fastest-growing 3D mapping and modeling market, driven by accelerating infrastructure modernization and geospatial technology adoption"

Asia Pacific represents the fastest-growing regional market for 3D mapping and modeling technologies, supported by large-scale infrastructure investments and rapid urbanization. Governments continue investing in transportation, utilities, industrial corridors, smart cities, and digital infrastructure modernization programs across major economies. Organizations are expanding LiDAR, UAV mapping, BIM, digital twin, and reality capture deployments to improve engineering productivity and project execution. Construction activities and infrastructure expansion continue driving demand for advanced geospatial data acquisition and visualization solutions. Industrial digitalization further accelerates technology adoption across manufacturing, mining, energy, and public infrastructure sectors. Growing investments in cloud-based engineering platforms, AI-enabled geospatial analytics, and connected construction solutions support long-term market expansion. These developments position Asia Pacific as the fastest-growing regional market during the forecast period, with sustained opportunities across multiple verticals, such as architecture, engineering, & construction (AEC); energy & utilities; government & defense; and manufacturing.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the 3D mapping and modeling market.

- By Company: Tier 1 - 38%, Tier 2 - 47%, and Tier 3 - 15%

- By Designation: C-level Executives- 31%, Directors - 46%, and Others - 23%

- By Region: North America - 39%, Europe - 22%, Asia Pacific - 28%, - Middle East & Africa - 4%, and Latin America - 7%

Note: Others include sales, marketing, and product managers.

Tier 1 companies' revenues are more than USD 500 million, tier 2 companies' revenues range between USD 500 and 100 million, and tier 3 companies' revenues are equals to or less than USD 100 million.

Source: Industry Experts

The report includes the study and in-depth company profiles of key players offering 3D mapping and modeling hardware systems. software tools and platforms. The major players in 3D mapping and modeling are Trimble (US), Autodesk (US), Hexagon AB (Sweden), AMETEK Inc. (US), Topcon Corporation (Japan), Teledyne Technologies (US), Fugro (Netherlands), CoStar Group (US), Bentley Systems (US), Airbus (France), TomTom (Netherlands), Esri (US), Woolpert (US), SAM Companies (US), NavVis GmbH (Germany), Artec 3D (Luxembourg), VertiGIS (Austria), RIEGL Laser Measurement Systems (Austria), YellowScan (France), Pix4D (Switzerland), Agisoft (Russia), DroneDeploy (US), Safe Software (Canada), Carlson Software (US), Cupix (US), Cintoo (France), OpenSpace (US), vGIS (Canada), Nearmap (Australia), Aerometrex (Australia), Intermap Technologies (Canada), Dynamic Map Platform (Japan), Vexcel Imaging (Austria), CARTO (US), MapLarge (US), EarthDaily (Canada), Caliper Corporation (US), Spargeo (South Korea), Emesent (Australia).

Research Coverage

This research report categorizes the 3D mapping and modeling market by offering (hardware, software and services), by deployment mode (cloud, on-premises, and hybrid), by organization size (large enterprises and SMEs), by vertical (agriculture & forestry; architecture, engineering, & construction (AEC); energy & utilities; government & defense; manufacturing; mining & minerals; oil & gas; telecommunications; transportation & logistics; and other verticals), and by region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the 3D mapping and modeling market. A detailed analysis of the key industry players has been made to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements; product and service launches; mergers and acquisitions; and recent developments associated with the 3D mapping and modeling market. Competitive analysis of upcoming startups in the 3D mapping and modeling market ecosystem is covered in this report.

Reasons to Buy This Report

The report will provide market leaders and new entrants with information on the closest approximations of the revenue numbers for the overall 3D mapping and modeling market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to position their business better and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (expansion of digital twin deployments across industrial and manufacturing assets; growing adoption of UAV-based reality capture for large-scale geospatial data collection), restraints (high processing and infrastructure requirements for large-scale 3D datasets; regulatory and airspace restrictions affecting aerial mapping operations), opportunities (increasing demand for climate resilience, environmental monitoring, and disaster modeling; growing use of immersive spatial experiences in metaverse and extended reality applications), and challenges ( maintaining accuracy and consistency across multi-source data acquisition systems; ensuring interoperability across diverse geospatial data formats and software ecosystems)

- Product development/innovation: Detailed insights into upcoming technologies, research & development activities, and product and service launches in the 3D mapping and modeling market

- Market development: Comprehensive information about lucrative markets, analysis of the 3D mapping and modeling market across varied regions

- Market Diversification: Exhaustive information about new products and services, untapped geographies, recent developments, and investments in the 3D mapping and modeling market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and offerings of the major players in 3D mapping and modeling market, namely, Trimble (US), Autodesk (US), Hexagon AB (Sweden), AMETEK Inc. (US), Topcon Corporation (Japan), Teledyne Technologies (US), Fugro (Netherlands), CoStar Group (US), Bentley Systems (US), Airbus (France), TomTom (Netherlands), Esri (US), Woolpert (US), SAM Companies (US), NavVis GmbH (Germany), Artec 3D (Luxembourg),. The report also helps stakeholders understand the pulse of the 3D mapping & modeling market, providing them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 EXECUTIVE SUMMARY

- 2.1 MARKET HIGHLIGHTS AND KEY INSIGHTS

- 2.2 KEY MARKET PARTICIPANTS: MAPPING OF STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS IN 3D MAPPING AND MODELING MARKET

- 2.4 HIGH-GROWTH SEGMENTS

- 2.5 REGIONAL SNAPSHOT: MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN 3D MAPPING AND MODELING MARKET

- 3.2 3D MAPPING AND MODELING MARKET, BY REGION

- 3.3 3D MAPPING AND MODELING MARKET, BY TOP 3 SOFTWARE TYPES

- 3.4 NORTH AMERICA: 3D MAPPING AND MODELING MARKET, BY OFFERING AND DEPLOYMENT MODE

- 3.5 3D MAPPING AND MODELING MARKET, BY REGION

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Expansion of digital twin deployments across industrial and manufacturing assets

- 4.2.1.2 Growing adoption of UAV-based reality capture for large-scale geospatial data collection

- 4.2.1.3 Advancements in AI-powered automated feature extraction and model generation

- 4.2.1.4 Accelerating investments in autonomous mobility and location-aware systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High processing and infrastructure requirements for large-scale 3D datasets

- 4.2.2.2 Regulatory and airspace restrictions affecting aerial mapping operations

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing demand for climate resilience, environmental monitoring, and disaster modeling

- 4.2.3.2 Growing use of immersive spatial experiences in metaverse and extended reality applications

- 4.2.3.3 Expansion of indoor digital mapping for smart buildings and facility intelligence

- 4.2.3.4 Transition from periodic surveys to continuous spatial monitoring

- 4.2.4 CHALLENGES

- 4.2.4.1 Maintaining accuracy and consistency across multi-source data acquisition systems

- 4.2.4.2 Ensuring interoperability across diverse geospatial data formats and software ecosystems

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN 3D MAPPING AND MODELING MARKET

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.5 STRATEGIC MOVES BY TIER-1/2/3 PLAYERS

5 INDUSTRY TRENDS

- 5.1 EVOLUTION OF 3D MAPPING AND MODELING

- 5.2 PORTER'S FIVE FORCES ANALYSIS

- 5.2.1 THREAT OF NEW ENTRANTS

- 5.2.2 THREAT OF SUBSTITUTES

- 5.2.3 BARGAINING POWER OF SUPPLIERS

- 5.2.4 BARGAINING POWER OF BUYERS

- 5.2.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.3 MACROECONOMIC OUTLOOK

- 5.3.1 INTRODUCTION

- 5.3.2 GDP TRENDS AND FORECAST

- 5.3.3 TRENDS IN GLOBAL CONVERGENCE OF GIS, BIM, DIGITAL TWIN & REALITY CAPTURE

- 5.3.4 TRENDS IN GLOBAL DIGITAL TWIN SOLUTIONS INDUSTRY

- 5.3.5 TRENDS IN GLOBAL REALITY CAPTURE INDUSTRY

- 5.3.6 TRENDS IN GLOBAL INFRASTRUCTURE INTELLIGENCE PLATFORMS

- 5.3.7 TRENDS IN GLOBAL GEOSPATIAL AI & SPATIAL INTELLIGENCE

- 5.3.8 TRENDS IN GLOBAL AUTONOMOUS SYSTEMS & ROBOTICS

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 HARDWARE PROVIDERS

- 5.5.1.1 Data capture hardware providers

- 5.5.1.2 Mapping hardware providers

- 5.5.1.3 Visualization & computing hardware providers

- 5.5.2 SOFTWARE PROVIDERS

- 5.5.2.1 Data capture & processing software providers

- 5.5.2.2 GIS & spatial analytics software providers

- 5.5.2.3 Digital twin platform providers

- 5.5.2.4 Visualization & collaboration platform providers

- 5.5.3 SERVICE PROVIDERS

- 5.5.3.1 Data capture service providers

- 5.5.3.2 Modeling & processing service providers

- 5.5.3.3 Professional service providers

- 5.5.3.4 Managed service providers

- 5.5.1 HARDWARE PROVIDERS

- 5.6 PRICING ANALYSIS

- 5.6.1 AVERAGE SELLING PRICE OF KEY PLAYERS, BY OFFERING, 2026

- 5.6.2 AVERAGE SELLING PRICE, BY DEPLOYMENT MODE, 2026

- 5.7 TRADE ANALYSIS

- 5.7.1 EXPORT SCENARIO OF LASER SCANNERS (HSN: 901320)

- 5.7.2 IMPORT SCENARIO OF LASER SCANNERS (HSN: 901320)

- 5.8 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 AUTODESK AND CROSS RIVER RAIL ENABLE BIM-GIS INTEGRATION FOR DIGITAL TWIN DEVELOPMENT

- 5.11.2 TRIMBLE AND NETWORK RAIL SCOTLAND IMPROVE RAIL INFRASTRUCTURE MODELING THROUGH 3D SCANNING

- 5.11.3 HEXAGON AND 3DNL ENABLE NATIONWIDE 3D REALITY CAPTURE FOR GEOSPATIAL DATA MODERNIZATION

- 5.11.4 FUGRO ROAMES AND NEW ZEALAND UTILITIES ENABLE DIGITAL TWIN DEVELOPMENT FOR POWER GRID NETWORK MANAGEMENT

- 5.11.5 BENTLEY SYSTEMS AND SINGAPORE LAND AUTHORITY ENABLE NATIONWIDE 3D DIGITAL TWIN DEVELOPMENT

- 5.12 IMPACT OF 2025 US TARIFF - 3D MAPPING AND MODELING MARKET

- 5.12.1 INTRODUCTION

- 5.12.2 TARIFF/TRADE POLICY UPDATES, JANUARY-JUNE 2026

- 5.12.3 KEY TARIFF RATES

- 5.12.4 PRICE IMPACT ANALYSIS

- 5.12.4.1 Strategic shifts and emerging trends

- 5.12.5 IMPACT ON COUNTRIES/REGIONS

- 5.12.5.1 US

- 5.12.5.2 Europe

- 5.12.5.3 China

- 5.12.5.4 Asia Pacific (excluding China)

- 5.12.6 IMPACT ON END-USE INDUSTRIES

- 5.12.6.1 Agriculture & forestry

- 5.12.6.2 Architecture, engineering, & construction (AEC)

- 5.12.6.3 Energy & utilities

- 5.12.6.4 Government & defense

- 5.12.6.5 Manufacturing

- 5.12.6.6 Mining & minerals

- 5.12.6.7 Oil & gas

- 5.12.6.8 Telecommunications

- 5.12.6.9 Transportation & logistics

6 TECHNOLOGICAL ADVANCEMENTS, AI-DRIVEN IMPACT, PATENTS, INNOVATIONS, AND FUTURE APPLICATIONS

- 6.1 KEY EMERGING TECHNOLOGIES

- 6.1.1 LIDAR (LIGHT DETECTION AND RANGING)

- 6.1.2 PHOTOGRAMMETRY

- 6.1.3 SIMULTANEOUS LOCALIZATION AND MAPPING

- 6.1.4 STRUCTURED LIGHT SCANNING

- 6.1.5 POINT CLOUD PROCESSING

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 GNSS/RTK POSITIONING

- 6.2.2 SENSOR FUSION

- 6.2.3 EDGE AI PROCESSING

- 6.2.4 GPU ACCELERATION

- 6.2.5 SPATIAL DATABASES

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 BUILDING INFORMATION MODELING

- 6.3.2 GEOGRAPHIC INFORMATION SYSTEMS

- 6.3.3 COMPUTER-AIDED DESIGN

- 6.3.4 DIGITAL TWIN TECHNOLOGIES

- 6.3.5 REMOTE SENSING

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 KEY TAKEAWAYS FOR MARKET

- 6.5 PATENT ANALYSIS

- 6.5.1 METHODOLOGY

- 6.5.2 PATENTS FILED, BY DOCUMENT TYPE, 2016-2025

- 6.5.3 INNOVATION AND PATENT APPLICATIONS

- 6.6 FUTURE APPLICATIONS

- 6.7 IMPACT OF AI/GEN AI ON 3D MAPPING AND MODELING MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES FOLLOWED BY MANUFACTURERS/OEMS IN 3D MAPPING AND MODELING MARKET

- 6.7.3 CASE STUDIES RELATED TO AI IMPLEMENTATION IN 3D MAPPING AND MODELING MARKET

- 6.7.4 INTERCONNECTED ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT AI-INTEGRATED IN 3D MAPPING AND MODELING MARKET

- 6.8 SUCCESS STORIES AND REAL-WORLD APPLICATIONS

- 6.8.1 CROSS RIVER RAIL: BIM-GIS DIGITAL TWIN FOR LARGE-SCALE TRANSPORT INFRASTRUCTURE

- 6.8.2 NETWORK RAIL: 3D LASER SCANNING FOR RAILWAY ASSET MANAGEMENT AND CLEARANCE ANALYSIS

- 6.8.3 COUNTIES ENERGY: DIGITAL TWIN DEVELOPMENT FOR ELECTRICITY NETWORK MANAGEMENT

7 TARIFF AND REGULATORY LANDSCAPE

- 7.1 TARIFF RELATED TO LASER SCANNER UNITS (HSN: 901320)

- 7.2 REGIONAL REGULATIONS AND COMPLIANCE

- 7.2.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.2.2 KEY REGULATIONS

- 7.2.2.1 North America

- 7.2.2.1.1 Federal Aviation Administration Small Unmanned Aircraft Systems Rule (FAA Part 107) (US)

- 7.2.2.1.2 Federal Communications Commission (FCC) Part 15 Rules for Ground Penetrating Radar (GPR) (US)

- 7.2.2.1.3 Innovation, Science and Economic Development Canada (ISED) RSS-220 - Ground Penetrating Radar and Wall Imaging Radar Standards (Canada)

- 7.2.2.2 Europe

- 7.2.2.2.1 INSPIRE Directive (Directive 2007/2/EC) (European Union)

- 7.2.2.2.2 EU Implementing Regulation (EU) 2019/947 on the Rules and Procedures for the Operation of Unmanned Aircraft (Unified UAS/Drone Regulation) (European Union)

- 7.2.2.2.3 UK Air Navigation Order 2016 and Civil Aviation Authority (CAA) Drone Regulations (CAP 722) (UK)

- 7.2.2.2.4 Federal Geodata Access Act (Geodatenzugangsgesetz - GeoZG) (Germany)

- 7.2.2.2.5 ELAN Law (Loi ELAN - Law No. 2018-1021 on Housing, Development and Digital Transformation) (France)

- 7.2.2.2.6 Spanish Land Law (Ley de Suelo y Rehabilitacion Urbana - Royal Legislative Decree) (Spain)

- 7.2.2.2.7 Ministerial Decree No. 560/2017 (Italy BIM Mandate for Public Procurement) (Italy)

- 7.2.2.3 Asia Pacific

- 7.2.2.3.1 Surveying and Mapping Law of the People's Republic of China

- 7.2.2.3.2 Guidelines for Acquiring and Producing Geospatial Data and Geospatial Data Services Including Maps (2021) (India)

- 7.2.2.3.3 Basic Act on the Advancement of Utilizing Geospatial Information (Act No. 63 of 2007) (Japan)

- 7.2.2.3.4 National Spatial Data Infrastructure Act (NSDI Act) (South Korea)

- 7.2.2.4 Middle East & Africa

- 7.2.2.4.1 Mandatory Technical Compliance Requirements (Articles 5 and 12) - (Saudi Arabia)

- 7.2.2.4.2 Federal Decree-Law No. 5 of 2019 on Space Activities and Geospatial Data Governance Requirements (UAE)

- 7.2.2.4.3 Law No. 7221 on Geographic Information Systems and Amendments to Certain Laws (National Geographic Information System Law) (Turkey)

- 7.2.2.4.4 Spatial Data Infrastructure Act, 2003 (Act No. 54 of 2003) (South Africa)

- 7.2.2.5 Latin America

- 7.2.2.5.1 National Spatial Data Infrastructure Decree (INDE) - Decree No. 6,666/2008 (Brazil)

- 7.2.2.5.2 General Law on National Geographic and Statistical Information System (Ley del Sistema Nacional de Informacion Estadistica y Geografica - LSNIEG) (Mexico)

- 7.2.2.5.3 National Spatial Data Infrastructure Law (Argentina)

- 7.2.2.1 North America

- 7.2.3 INDUSTRY STANDARDS

8 CUSTOMER LANDSCAPE AND BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 KEY STAKEHOLDERS INVOLVED IN BUYING PROCESS AND THEIR EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS AND INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS INDUSTRY VERTICALS

9 3D MAPPING AND MODELING MARKET, BY OFFERING

- 9.1 INTRODUCTION

- 9.1.1 OFFERING: 3D MAPPING AND MODELING MARKET DRIVERS

- 9.2 HARDWARE

- 9.2.1 DATA CAPTURE HARDWARE

- 9.2.1.1 Enabling high-accuracy spatial data acquisition through advanced sensing and measurement technologies

- 9.2.1.2 Scanners & LiDAR systems

- 9.2.1.3 Cameras & imaging systems

- 9.2.1.4 Positioning & navigation systems

- 9.2.1.5 Other systems

- 9.2.2 MAPPING HARDWARE

- 9.2.2.1 Enabling efficient spatial data collection through mobile, aerial, and marine mapping platforms

- 9.2.2.2 UAVs/Drones

- 9.2.2.3 Mobile mapping systems

- 9.2.2.4 Marine mapping systems

- 9.2.2.5 Other systems

- 9.2.3 VISUALIZATION & COMPUTING HARDWARE

- 9.2.3.1 Enabling real-time processing, visualization, and analysis of spatial data

- 9.2.4 OTHER HARDWARE

- 9.2.1 DATA CAPTURE HARDWARE

- 9.3 SOFTWARE

- 9.3.1 DATA CAPTURE & PROCESSING SOFTWARE

- 9.3.1.1 Converting raw spatial data into accurate and usable 3D mapping outputs

- 9.3.1.2 Photogrammetry software

- 9.3.1.3 Point cloud processing software

- 9.3.1.4 Registration & georeferencing software

- 9.3.1.5 Reality reconstruction software

- 9.3.1.6 Other software

- 9.3.2 GIS & SPATIAL ANALYTICS SOFTWARE

- 9.3.2.1 Enabling advanced spatial intelligence and data-driven decision-making through geospatial analysis platforms

- 9.3.2.2 3D GIS platforms

- 9.3.2.3 Terrain & surface modeling platforms

- 9.3.2.4 Utility & network mapping platforms

- 9.3.2.5 Corridor mapping platforms

- 9.3.2.6 Spatial analytics platforms

- 9.3.2.7 Other platforms

- 9.3.3 DIGITAL TWIN PLATFORMS

- 9.3.3.1 Enabling real-time digital representations of physical assets and environments

- 9.3.3.2 Building digital twin platforms

- 9.3.3.3 Infrastructure digital twin platforms

- 9.3.3.4 Industrial digital twin platforms

- 9.3.3.5 City digital twin platforms

- 9.3.3.6 Other platforms

- 9.3.4 VISUALIZATION & COLLABORATION PLATFORMS

- 9.3.4.1 Enhancing spatial understanding and cross-functional decision-making through immersive visualization technologies

- 9.3.4.2 3D visualization platforms

- 9.3.4.3 Model collaboration platforms

- 9.3.4.4 XR visualization platforms

- 9.3.4.5 Other platforms

- 9.3.1 DATA CAPTURE & PROCESSING SOFTWARE

- 9.4 SERVICES

- 9.4.1 DATA CAPTURE SERVICES

- 9.4.1.1 Delivering accurate spatial intelligence through professional reality capture operations

- 9.4.1.2 Aerial survey services

- 9.4.1.3 Terrestrial survey services

- 9.4.1.4 Mobile mapping services

- 9.4.1.5 Indoor mapping services

- 9.4.1.6 Other services

- 9.4.2 PROCESSING & MODELING SERVICES

- 9.4.2.1 Transforming reality capture data into actionable 3D models and digital assets

- 9.4.2.2 Point cloud processing services

- 9.4.2.3 Reality capture processing services

- 9.4.2.4 3D modeling services

- 9.4.2.5 Scan-to-BIM services

- 9.4.2.6 Digital twin creation services

- 9.4.2.7 Other services

- 9.4.3 PROFESSIONAL SERVICES

- 9.4.3.1 Accelerating successful 3D mapping and modeling adoption through specialized technical and implementation expertise

- 9.4.3.2 Consulting services

- 9.4.3.3 Integration & deployment services

- 9.4.3.4 Training services

- 9.4.3.5 Support services

- 9.4.4 MANAGED SERVICES

- 9.4.4.1 Optimizing 3D mapping operations through managed reality capture, modeling, and digital asset services

- 9.4.4.2 Managed mapping services

- 9.4.4.3 Managed GIS services

- 9.4.4.4 Managed digital twin services

- 9.4.4.5 Managed spatial data services

- 9.4.4.6 Other services

- 9.4.1 DATA CAPTURE SERVICES

10 3D MAPPING AND MODELING MARKET, BY DEPLOYMENT MODE

- 10.1 INTRODUCTION

- 10.1.1 DEPLOYMENT MODE: 3D MAPPING AND MODELING MARKET DRIVERS

- 10.2 CLOUD

- 10.2.1 ENABLING SCALABLE, COLLABORATIVE, AND DATA-DRIVEN 3D MAPPING OPERATIONS THROUGH CLOUD-BASED PLATFORMS

- 10.3 ON-PREMISES

- 10.3.1 PROVIDING ENHANCED DATA CONTROL, SECURITY, AND PERFORMANCE FOR MISSION-CRITICAL MAPPING ENVIRONMENTS

- 10.4 HYBRID

- 10.4.1 BALANCING FLEXIBILITY, SECURITY, AND PERFORMANCE THROUGH INTEGRATED DEPLOYMENT ARCHITECTURES

11 3D MAPPING AND MODELING MARKET, BY ORGANIZATION SIZE

- 11.1 INTRODUCTION

- 11.1.1 ORGANIZATION SIZE: 3D MAPPING AND MODELING MARKET DRIVERS

- 11.2 LARGE ENTERPRISES

- 11.2.1 DRIVING LARGE-SCALE DIGITAL TRANSFORMATION THROUGH ENTERPRISE-WIDE 3D MAPPING AND MODELING INVESTMENTS

- 11.3 SMALL & MEDIUM-SIZED ENTERPRISES (SMES)

- 11.3.1 EXPANDING ACCESS TO ADVANCED SPATIAL INTELLIGENCE THROUGH SCALABLE AND COST-EFFECTIVE SOLUTIONS

12 3D MAPPING AND MODELING MARKET, BY VERTICAL

- 12.1 INTRODUCTION

- 12.1.1 VERTICAL: 3D MAPPING AND MODELING MARKET DRIVERS

- 12.2 ARCHITECTURE, ENGINEERING, & CONSTRUCTION (AEC)

- 12.2.1 DRIVING DIGITAL CONSTRUCTION AND INFRASTRUCTURE DEVELOPMENT THROUGH ADVANCED 3D MAPPING AND MODELING TECHNOLOGIES

- 12.2.2 BUILDING DESIGN & PLANNING

- 12.2.3 SITE SURVEYING

- 12.2.4 CONSTRUCTION PROGRESS MONITORING

- 12.2.5 FACILITY MANAGEMENT

- 12.2.6 OTHER AEC USE CASES

- 12.3 TRANSPORTATION & LOGISTICS

- 12.3.1 ENHANCING TRANSPORTATION INFRASTRUCTURE PLANNING AND ASSET MANAGEMENT THROUGH 3D MAPPING AND DIGITAL INFRASTRUCTURE MODELING

- 12.3.2 ROAD & HIGHWAY MAPPING

- 12.3.3 RAILWAY MAPPING

- 12.3.4 AIRPORT MAPPING

- 12.3.5 BRIDGE & TUNNEL INSPECTION

- 12.3.6 OTHER TRANSPORTATION & LOGISTICS USE CASES

- 12.4 GOVERNMENT & DEFENSE

- 12.4.1 STRENGTHENING NATIONAL INFRASTRUCTURE, SECURITY, AND PUBLIC SECTOR PLANNING THROUGH ADVANCED 3D MAPPING AND MODELING TECHNOLOGIES

- 12.4.2 LAND SURVEYING

- 12.4.3 URBAN PLANNING

- 12.4.4 DEFENSE MAPPING

- 12.4.5 DISASTER MANAGEMENT

- 12.4.6 OTHER GOVERNMENT & DEFENSE USE CASES

- 12.5 ENERGY & UTILITIES

- 12.5.1 MODERNIZING CRITICAL INFRASTRUCTURE MANAGEMENT THROUGH 3D ASSET MODELING AND DIGITAL TWIN TECHNOLOGIES

- 12.5.2 UTILITY ASSET MAPPING

- 12.5.3 POWERLINE INSPECTION

- 12.5.4 RENEWABLE ENERGY PLANNING

- 12.5.5 SUBSTATION MODELING

- 12.5.6 OTHER ENERGY & UTILITIES USE CASES

- 12.6 OIL & GAS

- 12.6.1 IMPROVING ASSET VISIBILITY, INFRASTRUCTURE INTEGRITY, AND OPERATIONAL EFFICIENCY THROUGH ADVANCED 3D MAPPING AND DIGITAL ASSET MODELING

- 12.6.2 PIPELINE MAPPING

- 12.6.3 FACILITY MODELING

- 12.6.4 EXPLORATION SURVEYING

- 12.6.5 OFFSHORE INSPECTION

- 12.6.6 OTHER OIL & GAS USE CASES

- 12.7 TELECOMMUNICATIONS

- 12.7.1 ACCELERATING TELECOMMUNICATIONS INFRASTRUCTURE DIGITIZATION THROUGH ADVANCED 3D MAPPING AND MODELING TECHNOLOGIES

- 12.7.2 TOWER MAPPING

- 12.7.3 FIBER ROUTE PLANNING

- 12.7.4 5G DEPLOYMENT PLANNING

- 12.7.5 INFRASTRUCTURE MONITORING

- 12.7.6 SITE SURVEYING

- 12.7.7 OTHER TELECOMMUNICATIONS USE CASES

- 12.8 MINING & MINERALS

- 12.8.1 OPTIMIZING MINING OPERATIONS AND RESOURCE DEVELOPMENT THROUGH ADVANCED 3D MAPPING AND MODELING TECHNOLOGIES

- 12.8.2 MINE PLANNING

- 12.8.3 GEOLOGICAL MODELING

- 12.8.4 STOCKPILE MEASUREMENT

- 12.8.5 ASSET MONITORING

- 12.8.6 OTHER MINING & MINERALS USE CASES

- 12.9 AGRICULTURE & FORESTRY

- 12.9.1 IMPROVING LAND ASSESSMENT AND RESOURCE PLANNING THROUGH ADVANCED 3D MAPPING AND MODELING TECHNOLOGIES

- 12.9.2 PRECISION AGRICULTURE

- 12.9.3 IRRIGATION PLANNING

- 12.9.4 YIELD FORECASTING

- 12.9.5 OTHER AGRICULTURE & FORESTRY USE CASES

- 12.10 MANUFACTURING

- 12.10.1 ADVANCING INDUSTRIAL ASSET MANAGEMENT AND FACILITY MODERNIZATION THROUGH 3D MAPPING AND DIGITAL TWIN TECHNOLOGIES

- 12.10.2 FACTORY MODELING

- 12.10.3 REVERSE ENGINEERING

- 12.10.4 FACILITY INSPECTION

- 12.10.5 INDUSTRIAL DIGITAL TWINS

- 12.10.6 OTHER MANUFACTURING USE CASES

- 12.11 OTHER VERTICALS

13 3D MAPPING AND MODELING MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: 3D MAPPING AND MODELING MARKET DRIVERS

- 13.2.2 US

- 13.2.2.1 Enterprise digital twin adoption and infrastructure asset visualization requirements to drive market

- 13.2.3 CANADA

- 13.2.3.1 Mining digitization, utility modernization, and large-scale reality capture adoption to drive market

- 13.3 EUROPE

- 13.3.1 EUROPE: 3D MAPPING AND MODELING MARKET DRIVERS

- 13.3.2 UK

- 13.3.2.1 Focus on infrastructure digital twins and lifecycle-focused asset management to drive market

- 13.3.3 GERMANY

- 13.3.3.1 Manufacturing facility digitization and high-precision reality capture requirements to drive market

- 13.3.4 FRANCE

- 13.3.4.1 Transportation asset digitization and expanding digital twin investments to drive market

- 13.3.5 SPAIN

- 13.3.5.1 Transportation infrastructure development and BIM-integrated construction projects to drive market

- 13.3.6 ITALY

- 13.3.6.1 Transportation modernization and engineering reality capture adoption to drive market

- 13.3.7 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: 3D MAPPING AND MODELING MARKET DRIVERS

- 13.4.2 CHINA

- 13.4.2.1 Infrastructure digitization and large-scale digital twin deployment to drive market

- 13.4.3 INDIA

- 13.4.3.1 Infrastructure expansion and digital construction adoption to drive market

- 13.4.4 JAPAN

- 13.4.4.1 Infrastructure lifecycle management and industrial asset digitization to drive market

- 13.4.5 SOUTH KOREA

- 13.4.5.1 Smart infrastructure and engineering digitization to drive market

- 13.4.6 ASEAN

- 13.4.6.1 Urban infrastructure development and smart city investments to drive market

- 13.4.7 AUSTRALIA AND NEW ZEALAND

- 13.4.7.1 Utility modernization and digital engineering adoption to drive market

- 13.4.8 REST OF ASIA PACIFIC

- 13.5 MIDDLE EAST & AFRICA

- 13.5.1 MIDDLE EAST & AFRICA: 3D MAPPING AND MODELING MARKET DRIVERS

- 13.5.2 SAUDI ARABIA

- 13.5.2.1 Digital twin adoption and large-scale infrastructure development to drive market

- 13.5.3 UAE

- 13.5.3.1 Smart infrastructure and asset visualization initiatives to drive market

- 13.5.4 TURKEY

- 13.5.4.1 Transportation modernization and engineering workflow digitization to drive market

- 13.5.5 SOUTH AFRICA

- 13.5.5.1 Mining digitization and network modernization to drive market

- 13.5.6 REST OF MIDDLE EAST & AFRICA

- 13.6 LATIN AMERICA

- 13.6.1 LATIN AMERICA: 3D MAPPING AND MODELING MARKET DRIVERS

- 13.6.2 BRAZIL

- 13.6.2.1 Transportation development and resource-sector digitization to drive market

- 13.6.3 MEXICO

- 13.6.3.1 Transportation investment and industrial development to drive market

- 13.6.4 ARGENTINA

- 13.6.4.1 Utility modernization and engineering digitization to drive market

- 13.6.5 REST OF LATIN AMERICA

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 KEY PLAYER COMPETITIVE STRATEGIES, 2022-2026

- 14.3 REVENUE ANALYSIS, 2021-2025

- 14.4 MARKET SHARE ANALYSIS, 2025

- 14.4.1 MARKET RANKING ANALYSIS, 2025

- 14.5 PRODUCT COMPARISON

- 14.5.1 COMPARATIVE ANALYSIS OF 3D MAPPING AND MODELING DIGITAL TWIN PLATFORMS

- 14.5.1.1 Trimble (Trimble Connect/Trimble Reality Capture Platform)

- 14.5.1.2 Autodesk (Autodesk Tandem)

- 14.5.1.3 Hexagon AB (HxDR/HxGN Digital Reality Platform)

- 14.5.1.4 Bentley Systems (iTwin Platform)

- 14.5.1.5 CoStar Group/Matterport (Matterport Digital Twin Platform)

- 14.5.2 COMPARATIVE ANALYSIS OF 3D MAPPING AND MODELING HARDWARE (MOBILE MAPPING SYSTEM)

- 14.5.2.1 Trimble (Trimble MX90 Mobile Mapping System)

- 14.5.2.2 Topcon (Topcon IP-S3 HD1 Mobile Mapping System)

- 14.5.2.3 Hexagon (Leica Pegasus TRK Mobile Mapping System)

- 14.5.2.4 Teledyne (Teledyne Optech CL-360 Mobile Mapping System)

- 14.5.1 COMPARATIVE ANALYSIS OF 3D MAPPING AND MODELING DIGITAL TWIN PLATFORMS

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS (INTEGRATED SOFTWARE & HARDWARE VENDORS), 2025

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.6.5 COMPANY FOOTPRINT: KEY PLAYERS (HARDWARE & SOFTWARE VENDORS), 2025

- 14.6.5.1 Company footprint (integrated hardware & software vendors)

- 14.6.5.2 Regional footprint (integrated hardware & software vendors)

- 14.6.5.3 Offering footprint (integrated hardware & software vendors)

- 14.6.5.4 Organization size footprint (integrated hardware & software vendors)

- 14.6.5.5 Vertical footprint (integrated hardware & software vendors)

- 14.7 COMPANY EVALUATION MATRIX (SOFTWARE PROVIDERS)

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT: 3D MAPPING AND MODELING MARKET: SOFTWARE PROVIDERS

- 14.7.5.1 Company footprint: (Software providers)

- 14.7.5.2 Regional footprint (software providers)

- 14.7.5.3 Offering footprint (software providers)

- 14.7.5.4 Organization size footprint (software providers)

- 14.7.5.5 Vertical footprint (software providers)

- 14.8 COMPANY VALUATION AND FINANCIAL METRICS

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 14.9.2 DEALS

15 COMPANY PROFILES

- 15.1 INTRODUCTION

- 15.2 KEY PLAYERS

- 15.2.1 AUTODESK, INC.

- 15.2.1.1 Business overview

- 15.2.1.2 Products/Solutions/Services offered

- 15.2.1.3 Recent developments

- 15.2.1.3.1 Product launches & enhancements

- 15.2.1.3.2 Deals

- 15.2.1.4 MnM view

- 15.2.1.4.1 Key strengths

- 15.2.1.4.2 Strategic choices

- 15.2.1.4.3 Weaknesses and competitive threats

- 15.2.2 TRIMBLE INC.

- 15.2.2.1 Business overview

- 15.2.2.2 Products/Solutions/Services offered

- 15.2.2.3 Recent developments

- 15.2.2.3.1 Product launches & enhancements

- 15.2.2.3.2 Deals

- 15.2.2.4 MnM view

- 15.2.2.4.1 Key strengths

- 15.2.2.4.2 Strategic choices

- 15.2.2.4.3 Weaknesses and competitive threats

- 15.2.3 HEXAGON AB

- 15.2.3.1 Business overview

- 15.2.3.2 Products/Solutions/Services offered

- 15.2.3.3 Recent developments

- 15.2.3.3.1 Product launches & enhancements

- 15.2.3.3.2 Deals

- 15.2.3.4 MnM view

- 15.2.3.4.1 Key strengths

- 15.2.3.4.2 Strategic choices

- 15.2.3.4.3 Weaknesses and competitive threats

- 15.2.4 AMETEK, INC.

- 15.2.4.1 Business overview

- 15.2.4.2 Products/Solutions/Services offered

- 15.2.4.3 Recent developments

- 15.2.4.3.1 Product launches & enhancements

- 15.2.4.3.2 Deals

- 15.2.4.4 MnM view

- 15.2.4.4.1 Key strengths

- 15.2.4.4.2 Strategic choices

- 15.2.4.4.3 Weaknesses and competitive threats

- 15.2.5 TOPCON CORPORATION

- 15.2.5.1 Business overview

- 15.2.5.2 Products/Solutions/Services offered

- 15.2.5.3 Recent developments

- 15.2.5.3.1 Product launches & enhancements

- 15.2.5.3.2 Deals

- 15.2.5.4 MnM view

- 15.2.5.4.1 Key strengths

- 15.2.5.4.2 Strategic choices

- 15.2.5.4.3 Weaknesses and competitive threats

- 15.2.6 TELEDYNE TECHNOLOGIES

- 15.2.6.1 Business overview

- 15.2.6.2 Products/Solutions/Services offered

- 15.2.6.3 Recent developments

- 15.2.6.3.1 Product launches & enhancements

- 15.2.6.3.2 Deals

- 15.2.7 FUGRO

- 15.2.7.1 Business overview

- 15.2.7.2 Products/Solutions/Services offered

- 15.2.7.3 Recent developments

- 15.2.7.3.1 Product launches & enhancements

- 15.2.7.3.2 Deals

- 15.2.7.3.3 Other developments

- 15.2.8 COSTAR GROUP, INC.

- 15.2.8.1 Business overview

- 15.2.8.2 Products/Solutions/Services offered

- 15.2.8.3 Recent developments

- 15.2.8.3.1 Product launches & enhancements

- 15.2.8.3.2 Deals

- 15.2.9 BENTLEY SYSTEMS, INCORPORATED

- 15.2.9.1 Business overview

- 15.2.9.2 Products/Solutions/Services offered

- 15.2.9.3 Recent developments

- 15.2.9.3.1 Product launches & enhancements

- 15.2.9.3.2 Deals

- 15.2.10 AIRBUS

- 15.2.10.1 Business overview

- 15.2.10.2 Products/Solutions/Services offered

- 15.2.10.3 Recent developments

- 15.2.10.3.1 Product launches & enhancements

- 15.2.10.3.2 Deals

- 15.2.10.3.3 Other developments

- 15.2.11 ESRI

- 15.2.12 WOOLPERT

- 15.2.13 SAM

- 15.2.14 TOMTOM INTERNATIONAL B.V.

- 15.2.1 AUTODESK, INC.

- 15.3 STARTUPS/SMES

- 15.3.1 NAVVIS

- 15.3.2 ARTEC 3D

- 15.3.3 VERTIGIS

- 15.3.4 RIEGL LASER MEASUREMENT SYSTEMS

- 15.3.5 YELLOWSCAN

- 15.3.6 AGISOFT

- 15.3.7 DRONEDEPLOY

- 15.3.8 SAFE SOFTWARE

- 15.3.9 CARLSON SOFTWARE

- 15.3.10 CUPIX

- 15.3.11 CINTOO

- 15.3.12 OPENSPACE

- 15.3.13 VGIS

- 15.3.14 NEARMAP

- 15.3.15 AEROMETREX

- 15.3.16 INTERMAP TECHNOLOGIES

- 15.3.17 DYNAMIC MAP PLATFORM

- 15.3.18 VEXCEL IMAGING

- 15.3.19 CARTO

- 15.3.20 MAPLARGE

- 15.3.21 EARTHDAILY

- 15.3.22 CALIPER CORPORATION

- 15.3.23 SPARKGEO

- 15.3.24 PIX4D

- 15.3.25 EMESENT

16 RESEARCH METHODOLOGY

- 16.1 RESEARCH DATA

- 16.1.1 SECONDARY DATA

- 16.1.2 PRIMARY DATA

- 16.1.2.1 Breakup of primary profiles

- 16.1.2.2 Key industry insights

- 16.2 MARKET BREAKUP AND DATA TRIANGULATION

- 16.3 MARKET SIZE ESTIMATION

- 16.3.1 TOP-DOWN APPROACH

- 16.3.2 BOTTOM-UP APPROACH

- 16.4 MARKET FORECAST

- 16.5 RESEARCH ASSUMPTIONS

- 16.6 RESEARCH LIMITATIONS

17 APPENDIX

- 17.1 DISCUSSION GUIDE

- 17.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 17.3 CUSTOMIZATION OPTIONS

- 17.4 RELATED REPORTS

- 17.5 AUTHOR DETAILS