|

시장보고서

상품코드

2082814

컨포멀 코팅 시장 예측(-2031년) : 유형별, 최종 용도 산업별, 지역별Conformal Coating Market by Type, By End-use Industry, and Region - Global Forecast to 2031 |

||||||

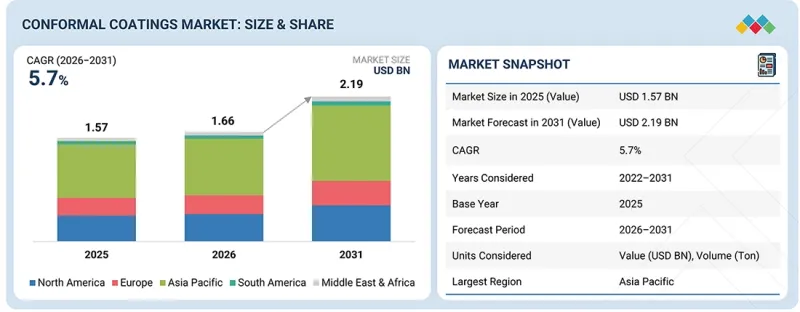

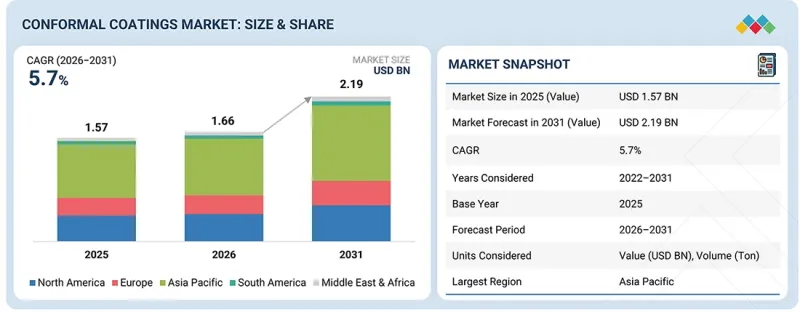

컨포멀 코팅 시장 규모는 2026년 16억 6,000만 달러에서 2031년까지 21억 9,000만 달러로 성장할 것으로 예측되고 있으며, 이 기간의 CAGR은 5.7%에 달합니다.

| 조사 범위 | |

|---|---|

| 조사 대상 기간 | 2022-2031년 |

| 기준연도 | 2025년 |

| 예측 기간 | 2026-2031년 |

| 산정 단위 | 금액(10억 달러) 톤 |

| 부문 | 유형별, 최종 용도 산업별, 지역별 |

| 대상 지역 | 북미, 아시아태평양, 유럽, 중동 및 아프리카, 남미 |

전자 기기의 소형화 및 부품 고밀도화 추세에 따라 첨단 컨포멀 코팅의 도입이 확대되고 있습니다. 이를 통해 장치의 기능성이나 설계 유연성을 저해하지 않으면서도, 콤팩트한 회로 구조를 습기, 화학 물질 노출, 염수 분무 및 전기 누설로부터 확실하게 보호할 수 있습니다.

'예측 기간 중 실리콘 계열 부문은 시장에서 두 번째로 큰 부문이 될 것으로 전망됩니다.'

실리콘 부문은 가혹하거나 열악한 작동 환경에서 실리콘이 제공하는 독보적인 장기 보호 성능 덕분에, 예측 기간 중 컨포멀 코팅 시장에서 2위의 규모를 차지할 것으로 전망됩니다. 실리콘 콘포멀 코팅은 뛰어난 열 안정성, 유연성, 내습성 및 유전 특성을 갖추고 있으며, 극심한 온도 변화, 높은 습도, 진동 및 실외 환경에 노출되는 전자 기기에 사용하기에 가장 적합합니다. 실리콘 콘포멀 코팅이 본래 지닌 물리적·화학적 특성 덕분에, 자동차용 전자기기, 재생에너지 시스템, 통신 인프라, 항공우주 기기 및 산업용 자동화 분야에서 이러한 소재의 사용이 증가하고 있습니다. 전기자동차, 첨단 배터리 관리 시스템, 전력 전자 장치, 5G 기지국 및 실외 통신 장비의 도입 확대가 실리콘계 코팅재 수요 증가를 이끌고 있습니다. 다른 많은 기존의 코팅 화학 물질과 달리, 실리콘 배합물은 장기간에 걸친 열적 및 환경적 스트레스 하에서도 그 보호 특성을 유지합니다. 경화 메커니즘의 개선이나 환경 규제를 준수하는 소재 등, 실리콘 소재 기술의 지속적인 혁신을 통해 이러한 코팅의 용도는 앞으로도 계속 확대될 것입니다. 각 업계가 전자 기기의 내구성과 신뢰성에 계속해서 중점을 두는 가운데, 실리콘 콘포멀 코팅은 예측 기간 중 높은 수요를 유지할 것으로 전망됩니다.

'예측 기간 중 통신 업계는 콘포멀 코팅 시장에서 2위의 규모를 차지할 것으로 전망됩니다.'

통신 부문은 주로 5G 무선 서비스의 급속한 성장에 힘입어, 예측 기간 중 컨포멀 코팅 시장에서 규모 면에서 2위를 차지할 최종사용자 산업 부문이 될 것으로 전망됩니다. 이러한 성장은 광섬유 네트워크의 급속한 확산, 엣지 컴퓨팅을 활용한 데이터 저장을 위한 신규 시설의 설립, 그리고 전 세계에서 데이터 통신 기술을 활용한 첨단 통신 시스템의 도입 등이 한 요인으로 작용하고 있습니다. 통신 장비에는 일반적으로 매우 복잡한 전자 어셈블리가 내장되어 있으며, 이러한 장비들은 습기, 먼지, 온도 변화, 공기 중의 오염 물질 및 자연 기상 조건에 노출되어 있음에도 불구하고 지속적인 작동을 유지해야 합니다. 컨포멀 코팅을 통한 보호는 물의 침투, 부식, 전기적 단락 및 오염으로 인한 고장으로부터 전자 기기를 보호하여 장기적인 작동을 가능하게 합니다. 실외에 설치되는 기지국, 안테나, 라우터, 스위치, 전송 장비의 수가 증가함에 따라 가혹한 운영 환경을 견딜 수 있는 첨단 코팅 기술에 대한 수요가 높아지고 있습니다. 또한 클라우드 컴퓨팅 솔루션, 데이터센터 건설, IoT 연결, 차세대 통신 기술에 대한 투자 확대에 따라 내구성이 뛰어난 전자기기 보호 솔루션에 대한 수요는 더욱 증가하고 있습니다. 통신 네트워크 사업자들이 네트워크의 장기적인 가동 유지, 유지보수 비용 절감, 그리고 장비 수명 연장을 여전히 중시하는 가운데, 콘포멀 코팅의 역할은 현대 통신 인프라에서 계속해서 필수적인 요소로 자리매김하며, 이 기간 중 강력한 시장 성장을 지원할 것입니다.

'금액 기준으로 볼 때, 북미는 예측 기간 중 시장 규모 2위를 차지할 것으로 전망됩니다.'

북미는 예측 기간 중 콘포멀 코팅의 지역별 시장 규모에서 2위를 차지할 것으로 추정됩니다. 이는 주로 대량 생산되는 전자기기, 항공우주, 자동차용 전자기기, 통신 인프라, 그 밖의 첨단 산업 기술 등 부가가치가 높은 분야에서 북미가 확고한 입지를 구축하고 있기 때문입니다. 북미에서는 높은 수준의 성능이 요구되는 첨단 전자 시스템의 개발 및 도입을 위한 정교한 생태계가 구축되어 있으며, 습기, 부식, 열 응력 및 현지 환경에 포함된 오염 물질로 인한 화학적 침식으로부터도 보호하고 있습니다. 또한 전기자동차, 첨단 운전자 보조 시스템(ADAS), 방위용 전자기기, 의료기기, 산업용 자동화 분야에 대한 투자 확대를 배경으로, 이러한 산업 분야에서 컨포멀 코팅의 용도에 대한 수요도 크게 증가할 것으로 전망됩니다. 5G 네트워크, 클라우드 기반 컴퓨팅 서비스, 하이퍼스케일 데이터센터의 지속적인 확장은 컨포멀 코팅을 통한 주요 어셈블리의 신뢰성 높은 보호에 대한 수요를 더욱 높이고 있습니다. 또한 특히 항공우주, 의료, 방위 산업 분야의 엄격한 성능, 안전성, 신뢰성 기준에 따라 업계를 선도하는 뛰어난 성능을 갖춘 코팅 기술의 도입이 모든 산업 분야에서 확대되고 있습니다. 주요 기술 개발 기업과 독자적인 전속 코팅 제조업체를 보유한 전자기기 혁신 기업 및 제조 기업의 강력한 존재감이, 콘포멀 코팅 분야에서 세계 유수의 시장으로서 북미의 위상을 지원하고 있습니다. 이러한 추세에 더해, 해당 업계에서 전자 기기의 신뢰성, 운영 효율성 및 제품 수명 주기에 대한 중요성이 커지고 있는 만큼, 북미는 예측 기간 중 콘포멀 코팅의 지역별 시장 규모에서 2위 자리를 계속 유지할 것으로 전망됩니다.

대상 기업: Henkel AG & Co. KGaA(독일), Illinois Tool Works Inc.(ITW)(미국), Shin-Etsu Chemical(일본), Dow Inc.(미국), H.B. Fuller(미국), Element Solutions Inc(ESI), ALTANA AG(독일), Chase Corp.(미국), Dymax(미국), MG Chemicals(캐나다) 등이 이 보고서의 대상입니다.

본 조사에서는 콘포멀 코팅 시장의 주요 기업에 대해 기업 개요, 최근 동향 및 주요 시장 전략을 포함한 상세한 경쟁 분석을 수행하고 있습니다.

조사 범위

본 조사 보고서에서는 콘포멀 코팅 시장을 유형별(아크릴, 실리콘, 에폭시, 우레탄, 파릴렌, 기타), 최종 용도 산업별(소비자용 전자기기, 자동차, 항공우주·방위, 산업용, 통신, 기타 최종 용도 산업) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류하고 있습니다. 이 보고서의 범위에는 콘포멀 코팅 시장의 성장에 영향을 미치는 촉진요인, 제약 요인, 과제 및 성장 기회에 관한 상세한 정보가 포함되어 있습니다. 주요 업계 업체에 대한 상세한 분석을 통해 사업 개요, 제공 제품, 그리고 컨포멀 코팅 시장과 관련된 파트너십, 제휴, 제품 출시, 사업 확장, 인수합병 등 주요 전략에 대한 인사이트를 제공합니다. 또한 이 보고서에서는 콘포멀 코팅 시장의 생태계에서 두각을 보이고 있는 스타트업 기업에 대한 경쟁 분석도 다루고 있습니다.

이 보고서를 구매해야 하는 이유

이 보고서는 시장 선도 기업 및 신규 진입 기업을 대상으로, 컨포멀 코팅 시장 전체 및 각 하위 부문의 매출에 관한 가장 정확한 추정치를 제공합니다. 이 보고서는 이해관계자들이 경쟁 구도를 이해하고, 자사의 비즈니스를 보다 적절하게 포지셔닝하기 위한 인사이트를 높이며, 적절한 시장 진입 전략을 수립하는 데 도움이 됩니다. 또한 시장 동향을 파악하고 주요 시장 촉진요인, 억제요인, 과제 및 기회에 관한 정보를 제공합니다.

이 보고서에서는 다음 사항에 대한 인사이트를 제공합니다. :

주요 촉진요인(안전성이 극히 중요하고 높은 신뢰성이 요구되는 용도에서의 전자 부품 채택 확대, 자동차의 전동화 및 전기자동차용 파워 일렉트로닉스의 확대, 재생에너지 및 에너지 저장 시스템에서의 전자 부품 도입 증가) 및 제약 요인(고급 컨포멀 코팅의 재가공, 수리, 제거에 드는 높은 비용, 소형화 및 고밀도 PCB 아키텍처로 인한 코팅의 복잡화), 기회(5G, 엣지 컴퓨팅, 데이터센터용 전자 인프라의 채택 확대, 플렉서블, 스트레치 가능 및 기판형 PCB 기술의 확대, 반도체 제조 및 첨단 패키징 분야의 수요 확대) 및 과제(VOC 배출 및 유해 화학 물질 사용에 대한 규제 당국의 감시 강화, 전자기기 제조 전반에 걸친 성능 요건과 비용 압박 간의 균형 조정)에 대한 인사이트를 제공합니다.

- 제품 개발 및 혁신: 컨포멀 코팅 시장의 향후 기술, 연구개발 활동, 그리고 제품 및 서비스 출시에 관한 상세 인사이트.

- 시장 개발: 수익성이 높은 시장에 대한 포괄적인 정보 -- 이 보고서에서는 다양한 지역에 걸친 컨포멀 코팅 시장을 분석하고 있습니다.

시장의 다양화: 컨포멀 코팅 시장의 신제품 및 서비스, 미개발 지역, 최근 동향, 그리고 투자에 관한 포괄적인 정보.

- 경쟁사 분석: Henkel AG & Co. KGaA(독일), Illinois Tool Works Inc.(ITW)(미국), Shin-Etsu Chemical(일본), Dow Inc.(미국), H.B. Fuller(미국), Element Solutions Inc(ESI), ALTANA AG(독일), Chase Corp.(미국), Dymax(미국), MG Chemicals(캐나다) 등 주요 기업의 시장 점유율, 성장 전략, 서비스 제공에 대한 상세한 평가

목차

제1장 서론

제2장 개요

제3장 주요 인사이트

제4장 시장 개요

제5장 업계 동향

제6장 기술의 진보

제7장 지속가능성과 규제 상황

제8장 고객 상황과 구매 행동

제9장 컨포멀 코팅 시장(유형별)

제10장 컨포멀 코팅 시장(최종 용도 산업별)

제11장 컨포멀 코팅 시장(지역별)

제12장 경쟁 구도

제13장 기업 개요

제14장 조사 방법

제15장 부록

KSAThe conformal coatings market is projected to grow from USD 1.66 billion in 2026 to USD 2.19 billion by 2031, representing a compound annual growth rate (CAGR) of 5.7% during this period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2022-2031 |

| Base Year | 2025 |

| Forecast Period | 2026-2031 |

| Units Considered | Value (USD Billion) Volume (Tons) |

| Segments | Type, End-Use Industry, and Region |

| Regions covered | North America, Asia Pacific, Europe, the Middle East & Africa, and South America |

The growing trend toward electronic miniaturization and higher component density is driving adoption of advanced conformal coatings, which enable reliable protection of compact circuit architectures against humidity, chemical exposure, salt spray, and electrical leakage without impacting device functionality or design flexibility.

"The silicone type segment projected to be the second-largest segment during the forecast period."

The silicone segment is projected to be the second-largest in the conformal coatings market during the forecast period because of the unique long-term protection that silicone has to offer in harsh or demanding operating environments. Silicone conformal coatings can provide exceptional thermal stability, flexibility, moisture resistance, and dielectric performance, making them ideal for use in electronics exposed to extreme temperature changes, high humidity levels, vibration, and outdoor conditions. The inherent physical and chemical properties of silicone conformal coatings have resulted in the increased usage of these materials in automotive electronics, renewable energy systems, telecommunications infrastructure, aerospace equipment, and industrial automation applications. The increasing deployment of electric vehicles, advanced battery management systems, power electronics, 5G base stations, and outdoor communication equipment is driving the increasing demand for silicone-based coatings. Unlike many other conventional coating chemistries, silicone formulations retain their protective properties under extended thermal and environmental stress. Continuous innovation in silicone material technology, such as improved curing mechanisms and environmentally compliant materials, will continue to expand the application of these coatings. As industries continue to focus on durability and reliability for their electronics, silicone conformal coatings should remain in great demand throughout the forecast period.

"The telecommunication end-use industry segment is projected to be the second-largest segment during the forecast period."

The telecommunication segment is projected to be the second-largest end-use industry in the conformal coatings market during the forecast period primarily due to the rapid growth of 5G wireless service. This growth is being driven in part by the rapid deployment of fiber optic networks; the establishment of new facilities for storing data using edge computing; and advanced communications systems using data communication technologies across the Globe. Telecommunications equipment typically contains very complex electronic assemblies which require continuous operation while being subjected to moisture, dust, fluctuation in temperature, airborne contamination, and exposure to the natural weather. The protection provided by conformal coatings helps protect electronics against water intrusion, corrosion, electrical shorting, and failure due to contamination thereby allowing them to be used for long-term operation. As a result of the growing number of base stations, antennas, routers, switches, and transmission equipment being mounted outside; there is a growing requirement for advanced coating technologies that can withstand extreme operational environments. In addition, increased spending on cloud computing solutions; data center construction; iot connectivity; and next generation communication technologies creates even more demand for long-lasting electronic protection solutions. As operators of telecommunication networks continue to place a high value on long-lasting uptime of their network; low maintenance expense; and increased equipment life, the role of conformal coatings will continue to be an integral part of modern telecommunications infrastructure, supporting strong market growth during this timeframe.

"In terms of value, North America is projected to be the second-largest segment during the forecast period."

North America is estimated to be the second-largest regional market for conformal coatings during the forecast period, mainly due to its robust presence in value-added sectors, including high-volume electronics, aerospace, automotive electronics, telecommunications infrastructure and other advanced industrial technologies. North America has developed a sophisticated ecosystem for developing and deploying advanced electronic systems requiring high-level performance, as well as protection against moisture, corrosion, thermal stress, and chemical attacks from contaminants in the local environment. There will also be significant demand increases for conformal coating applications in these industries, driven by increased investment in electric vehicles, advanced driver assistance systems (ADAS), defense electronics and medical devices and industrial automation. The continued rollout of 5G networks, cloud-based computing services and hyperscale data centres all further increase the demand for the reliable protection of critical assemblies by conformal coatings, along with the increased adoption of industry-leading coating technologies with superior performance abilities across industries due to stringent performance, safety and reliability standards in the aerospace, healthcare and defence industries in particular. The strong presence of leading technology developers and electronic innovator and manufacturers with their own dedicated coating manufacturer supports North America's position as one of the leading worldwide markets for conformal coatings. Due to this trend, and with increasing emphasis on electronic reliability, operational efficiency, and product life cycle within such industries, North America continues to position itself as the second largest regional market for conformal coatings through the forecast period.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and Middle East & Africa 20%

Notes: Other designations include sales, marketing, and product managers.

Tier 1: >USD 1 Billion; Tier 2: USD 500 million-1 Billion; and Tier 3: <USD 500 million

Companies Covered: Henkel AG & Co. KGaA (Germany), Illinois Tool Works Inc. (ITW) (US), Shin-Etsu Chemical Co., Ltd. (Japan), Dow Inc. (US), H.B. Fuller (US), Element Solutions Inc (ESI), ALTANA AG (Germany), Chase Corp. (US), Dymax (US), MG Chemicals (Canada) among others are covered in the report.

The study includes an in-depth competitive analysis of these key players in the conformal coatings market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the conformal coatings market by type (acrylic, silicone, epoxy, urethane, parylene, other types), by end-use industry (consumer electronics, automotive, aerospace & defense, industrial, telecommunication, other end-use industries), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding the drivers, restraints, challenges, and opportunities influencing the growth of the conformal coatings market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, product launches, expansions, and acquisitions, associated with the conformal coatings market. This report covers a competitive analysis of upcoming startups in the conformal coatings market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall conformal coatings market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (increasing electronics content in safety-critical and high-reliability applications, electrification of vehicles and expansion of ev power electronics, rising deployment of electronics in renewable energy and energy storage systems), restraints (high rework, repair, and removal costs of advanced conformal coatings, miniaturization and high-density pcb architectures increasing coating complexity),opportunities (increasing adoption of electronics infrastructure for 5g, edge computing, and data centers, expansion of flexible, stretchable, and substrate-like pcb technologies, growing demand from semiconductor manufacturing and advanced packaging), and challenges (increasing regulatory scrutiny on voc emissions and hazardous chemical usage, balancing performance requirements with cost pressures across electronics manufacturing).

- Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the conformal coatings market.

- Market Development: Comprehensive information about profitable markets - the report analyzes the conformal coatings market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the conformal coatings market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as Henkel AG & Co. KGaA (Germany), Illinois Tool Works Inc. (ITW) (US), Shin-Etsu Chemical Co., Ltd. (Japan), Dow Inc. (US), H.B. Fuller (US), Element Solutions Inc (ESI), ALTANA AG (Germany), Chase Corp. (US), Dymax (US), and MG Chemicals (Canada)

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED & REGIONAL SCOPE

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.3.4 CURRENCY CONSIDERED

- 1.3.5 UNIT CONSIDERED

- 1.3.6 STAKEHOLDERS

- 1.4 SUMMARY OF STRATEGIC CHANGES IN MARKET

2 EXECUTIVE SUMMARY

- 2.1 KEY INSIGHTS AND MARKET HIGHLIGHTS

- 2.2 KEY MARKET PARTICIPANTS: SHARE INSIGHTS AND STRATEGIC DEVELOPMENTS

- 2.3 DISRUPTIVE TRENDS SHAPING MARKET

- 2.4 HIGH-GROWTH SEGMENTS & EMERGING FRONTIERS

- 2.5 SNAPSHOT: GLOBAL MARKET SIZE, GROWTH RATE, AND FORECAST

3 PREMIUM INSIGHTS

- 3.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN CONFORMAL COATINGS MARKET

- 3.2 CONFORMAL COATINGS MARKET, BY TYPE AND END-USE INDUSTRY

- 3.3 CONFORMAL COATINGS MARKET, BY COUNTRY

4 MARKET OVERVIEW

- 4.1 INTRODUCTION

- 4.2 MARKET DYNAMICS

- 4.2.1 DRIVERS

- 4.2.1.1 Increasing electronics content in safety-critical and high-reliability applications

- 4.2.1.2 Electrification of vehicles and expansion of EV power electronics

- 4.2.1.3 Rising deployment of electronics in renewable energy and energy storage systems

- 4.2.2 RESTRAINTS

- 4.2.2.1 High costs of rework, repair, and removal of advanced conformal coatings

- 4.2.2.2 Miniaturization and high-density PCB architectures increasing coating complexity

- 4.2.3 OPPORTUNITIES

- 4.2.3.1 Increasing adoption of electronics infrastructure for 5G, edge computing, and data centers

- 4.2.3.2 Expansion of flexible, stretchable, and substrate-like PCB technologies

- 4.2.3.3 Growing demand from semiconductor manufacturing and advanced packaging

- 4.2.4 CHALLENGES

- 4.2.4.1 Increasing regulatory scrutiny on VOC emissions and hazardous chemical usage

- 4.2.4.2 Balancing performance requirements with cost pressures across electronics manufacturing

- 4.2.1 DRIVERS

- 4.3 UNMET NEEDS AND WHITE SPACES

- 4.3.1 UNMET NEEDS IN CONFORMAL COATINGS MARKET

- 4.3.1.1 High-performance conformal coatings with simplified rework and repair capabilities

- 4.3.1.2 Uniform protection of ultra-high-density electronic assemblies without application defects

- 4.3.2 WHITE SPACE OPPORTUNITIES

- 4.3.2.1 Self-healing and predictive-reliability conformal coatings for mission-critical electronics

- 4.3.2.2 Specialized conformal coatings for advanced semiconductor packaging and heterogeneous integration

- 4.3.1 UNMET NEEDS IN CONFORMAL COATINGS MARKET

- 4.4 INTERCONNECTED MARKETS AND CROSS-SECTOR OPPORTUNITIES

- 4.4.1 INTERCONNECTED MARKETS

- 4.4.2 CROSS-SECTOR OPPORTUNITIES

- 4.4.3 STRATEGIC MOVES BY TIER 1/2/3 PLAYERS

- 4.4.4 KEY MOVES AND STRATEGIC FOCUS

5 INDUSTRY TRENDS

- 5.1 PORTER'S FIVE FORCES' ANALYSIS

- 5.1.1 THREAT OF NEW ENTRANTS

- 5.1.2 THREAT OF SUBSTITUTES

- 5.1.3 BARGAINING POWER OF SUPPLIERS

- 5.1.4 BARGAINING POWER OF BUYERS

- 5.1.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.2 MACROECONOMIC ANALYSIS

- 5.2.1 INTRODUCTION

- 5.2.2 GDP TRENDS AND FORECASTS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF CONFORMAL COATINGS OFFERED BY KEY PLAYERS, BY TYPE

- 5.5.2 AVERAGE SELLING PRICE TREND OF CONFORMAL COATINGS, BY REGION

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA RELATED TO HS CODE 320820, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.6.2 EXPORT DATA RELATED TO HS CODE 320820, BY COUNTRY, 2021-2025 (USD THOUSAND)

- 5.7 KEY CONFERENCES AND EVENTS, 2026-2027

- 5.8 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.9 INVESTMENT AND FUNDING SCENARIO

- 5.10 CASE STUDY ANALYSIS

- 5.10.1 DYMAX - HIGH-PERFORMANCE SOLUTIONS FOR EV CHARGING STATIONS

- 5.10.2 DYMAX - AEROSPACE PCB CONFORMAL COATING PROCESS IMPROVEMENT

- 5.10.3 HUMISEAL - SHARP EDGE COVERAGE TECHNOLOGY FOR HIGH-DENSITY PCBS

- 5.11 IMPACT OF 2025 US TARIFFS ON CONFORMAL COATINGS MARKET

- 5.11.1 INTRODUCTION

- 5.11.2 KEY TARIFF RATES

- 5.11.3 PRICE IMPACT ANALYSIS

- 5.11.4 KEY IMPACT ON VARIOUS REGIONS

- 5.11.4.1 US

- 5.11.4.2 Europe

- 5.11.4.3 Asia Pacific

- 5.11.5 IMPACT ON END-USE INDUSTRIES

6 TECHNOLOGICAL ADVANCEMENTS

- 6.1 KEY TECHNOLOGIES

- 6.1.1 SELECTIVE CONFORMAL COATING AUTOMATION

- 6.1.2 UV-CURABLE CONFORMAL COATING TECHNOLOGY

- 6.1.3 PARYLENE VAPOR DEPOSITION TECHNOLOGY

- 6.2 COMPLEMENTARY TECHNOLOGIES

- 6.2.1 AUTOMATED OPTICAL INSPECTION (AOI) FOR COATING VERIFICATION

- 6.2.2 PLASMA SURFACE TREATMENT TECHNOLOGY

- 6.3 ADJACENT TECHNOLOGIES

- 6.3.1 ELECTRONICS ENCAPSULATION & POTTING TECHNOLOGIES

- 6.3.2 THERMAL INTERFACE MATERIAL (TIM) TECHNOLOGIES

- 6.4 TECHNOLOGY/PRODUCT ROADMAP

- 6.4.1 SHORT-TERM (2025-2027) | AUTOMATION & HIGH-RELIABILITY PROCESS OPTIMIZATION PHASE

- 6.4.2 MID-TERM (2027-2030) | ADVANCED MATERIALS & SMART MANUFACTURING INTEGRATION PHASE

- 6.4.3 LONG-TERM (2030-2035+): INTELLIGENT MULTIFUNCTIONAL PROTECTION ECOSYSTEM PHASE

- 6.5 PATENT ANALYSIS

- 6.5.1 INTRODUCTION

- 6.5.2 APPROACH

- 6.5.3 TOP APPLICANTS

- 6.6 FUTURE APPLICATIONS

- 6.6.1 SELF-HEALING CONFORMAL COATINGS FOR AUTONOMOUS ELECTRONICS

- 6.6.2 EMBEDDED SENSOR-INTEGRATED SMART COATINGS

- 6.6.3 ADAPTIVE EMI-SHIELDING CONFORMAL COATINGS

- 6.6.4 CONFORMAL COATINGS FOR FLEXIBLE NEURAL IMPLANT ELECTRONICS

- 6.7 IMPACT OF AI/GENERATIVE AI ON CONFORMAL COATINGS MARKET

- 6.7.1 TOP USE CASES AND MARKET POTENTIAL

- 6.7.2 BEST PRACTICES IN CONFORMAL COATINGS

- 6.7.3 CASE STUDIES OF AI IMPLEMENTATION IN CONFORMAL COATINGS MARKET

- 6.7.4 INTERCONNECTED ADJACENT ECOSYSTEM AND IMPACT ON MARKET PLAYERS

- 6.7.5 CLIENTS' READINESS TO ADOPT GENERATIVE AI IN CONFORMAL COATINGS MARKET

7 SUSTAINABILITY AND REGULATORY LANDSCAPE

- 7.1 REGIONAL REGULATIONS AND COMPLIANCE

- 7.1.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 7.1.2 INDUSTRY STANDARDS

- 7.2 SUSTAINABILITY INITIATIVES

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CONFORMAL COATINGS

- 7.2.1.1 Carbon impact reduction

- 7.2.1.2 Eco-applications

- 7.2.1 CARBON IMPACT AND ECO-APPLICATIONS OF CONFORMAL COATINGS

- 7.3 SUSTAINABILITY IMPACT AND REGULATORY POLICY INITIATIVES

- 7.4 CERTIFICATIONS, LABELING, AND ECO-STANDARDS

8 CUSTOMER LANDSCAPE & BUYER BEHAVIOR

- 8.1 DECISION-MAKING PROCESS

- 8.2 BUYER STAKEHOLDERS AND BUYING EVALUATION CRITERIA

- 8.2.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 8.2.2 BUYING CRITERIA

- 8.3 ADOPTION BARRIERS & INTERNAL CHALLENGES

- 8.4 UNMET NEEDS FROM VARIOUS END-USE INDUSTRIES

- 8.5 MARKET PROFITABILITY

- 8.5.1 REVENUE POTENTIAL

- 8.5.2 COST DYNAMICS

- 8.5.3 MARGIN OPPORTUNITIES, BY END-USE INDUSTRY

9 CONFORMAL COATINGS MARKET, BY TYPE

- 9.1 INTRODUCTION

- 9.2 SILICONE

- 9.2.1 SILICONE CONFORMAL COATINGS PROTECT CRITICAL ELECTRONICS OPERATING UNDER EXTREME CONDITIONS

- 9.3 ACRYLIC

- 9.3.1 ACRYLIC CONFORMAL COATINGS SUPPORT EFFICIENT MANUFACTURING AND SIMPLIFIED ELECTRONICS REWORK

- 9.4 EPOXY

- 9.4.1 EPOXY CONFORMAL COATINGS PROTECT ELECTRONICS EXPOSED TO CHEMICALS AND PHYSICAL STRESS

- 9.5 URETHANE

- 9.5.1 URETHANE CONFORMAL COATINGS PREVENT CHEMICAL-INDUCED FAILURES IN SENSITIVE ELECTRONICS

- 9.6 PARYLENE

- 9.6.1 PARYLENE CONFORMAL COATINGS PROTECT MINIATURIZED ELECTRONICS IN MISSION CRITICAL APPLICATIONS

- 9.7 OTHER TYPES

10 CONFORMAL COATINGS MARKET, BY END-USE INDUSTRY

- 10.1 INTRODUCTION

- 10.2 AUTOMOTIVE

- 10.2.1 AUTOMOTIVE ELECTRONICS DRIVE ADVANCED CONFORMAL COATING REQUIREMENTS ACROSS VEHICLE ARCHITECTURES

- 10.3 CONSUMER ELECTRONICS

- 10.3.1 DEVICE MINIATURIZATION AND WATER RESISTANCE TRENDS ACCELERATE COATING ADOPTION

- 10.4 AEROSPACE & DEFENSE

- 10.4.1 MEDICAL GRADE SILICONE SYSTEMS REDEFINING DEVICE SAFETY AND BIOCOMPATIBILITY STANDARDS IN HEALTHCARE

- 10.5 INDUSTRIAL

- 10.5.1 INDUSTRIAL DIGITALIZATION INCREASING EXPOSURE OF ELECTRONICS TO HARSH OPERATING CONDITIONS

- 10.6 TELECOMMUNICATION

- 10.6.1 5G NETWORK EXPANSION INCREASES RELIABILITY REQUIREMENTS ACROSS TELECOMMUNICATIONS INFRASTRUCTURE

- 10.7 OTHER END-USE INDUSTRIES

11 CONFORMAL COATINGS MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.2 NORTH AMERICA

- 11.2.1 US

- 11.2.1.1 Expanding domestic electronics and EV manufacturing accelerating adoption

- 11.2.2 CANADA

- 11.2.2.1 Expanding digital infrastructure and Arctic defense programs increasing demand

- 11.2.3 MEXICO

- 11.2.3.1 Nearshoring investments and export manufacturing accelerating adoption

- 11.2.1 US

- 11.3 ASIA PACIFIC

- 11.3.1 CHINA

- 11.3.1.1 Scaling advanced manufacturing ecosystems strengthening consumption

- 11.3.2 TAIWAN

- 11.3.2.1 Expanding advanced electronics manufacturing increasing demand for protective coatings

- 11.3.3 INDIA

- 11.3.3.1 Expanding domestic component manufacturing is accelerating conformal coating adoption

- 11.3.4 JAPAN

- 11.3.4.1 Advancing precision manufacturing standards increasing adoption

- 11.3.5 SOUTH KOREA

- 11.3.5.1 Artificial intelligence infrastructure expansion driving advanced market

- 11.3.6 VIETNAM

- 11.3.6.1 Advancing manufacturing capabilities continue to accelerate coating adoption across industries

- 11.3.7 THAILAND

- 11.3.7.1 Growing electronics investments continue accelerating adoption

- 11.3.8 REST OF ASIA PACIFIC

- 11.3.1 CHINA

- 11.4 EUROPE

- 11.4.1 GERMANY

- 11.4.1.1 Expanding electronics and mobility sectors accelerating demand

- 11.4.2 FRANCE

- 11.4.2.1 Expanding high technology industries increasing demand for conformal coatings

- 11.4.3 UK

- 11.4.3.1 Expanding electronics and advanced manufacturing sectors driving demand

- 11.4.4 RUSSIA

- 11.4.4.1 Expanding electronics and industrial sectors strengthening demand

- 11.4.5 REST OF EUROPE

- 11.4.1 GERMANY

- 11.5 MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.5.1.1 Saudi Arabia

- 11.5.1.1.1 Industrial localization strategy increasing conformal coatings demand

- 11.5.1.2 UAE

- 11.5.1.2.1 Technology localization and defense electronics expansion supporting demand

- 11.5.1.3 Rest of GCC Countries

- 11.5.1.1 Saudi Arabia

- 11.5.2 SOUTH AFRICA

- 11.5.2.1 Automotive electrification and industrial technology investments supporting demand

- 11.5.3 REST OF MIDDLE EAST & AFRICA

- 11.5.1 GCC COUNTRIES

- 11.6 SOUTH AMERICA

- 11.6.1 BRAZIL

- 11.6.1.1 Expanding automotive and digital infrastructure sectors fueling demand

- 11.6.2 ARGENTINA

- 11.6.2.1 Recovering electronics and automotive industries support conformal coatings demand

- 11.6.3 REST OF SOUTH AMERICA

- 11.6.1 BRAZIL

12 COMPETITIVE LANDSCAPE

- 12.1 OVERVIEW

- 12.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 12.3 REVENUE ANALYSIS, 2021-2025

- 12.4 MARKET SHARE ANALYSIS, 2025

- 12.5 BRAND COMPARISON

- 12.6 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2026

- 12.6.1 STARS

- 12.6.2 EMERGING LEADERS

- 12.6.3 PERVASIVE PLAYERS

- 12.6.4 PARTICIPANTS

- 12.6.5 COMPANY FOOTPRINT: KEY PLAYERS, 2026

- 12.6.5.1 Company footprint

- 12.6.5.2 Region footprint

- 12.6.5.3 Type footprint

- 12.6.5.4 End-use industry footprint

- 12.7 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2025

- 12.7.1 PROGRESSIVE COMPANIES

- 12.7.2 RESPONSIVE COMPANIES

- 12.7.3 DYNAMIC COMPANIES

- 12.7.4 STARTING BLOCKS

- 12.7.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2025

- 12.7.5.1 List of key startups/SMEs

- 12.7.6 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 12.8 COMPANY VALUATION AND FINANCIAL METRICS

- 12.8.1 COMPANY VALUATION

- 12.8.2 FINANCIAL METRICS

- 12.9 COMPETITIVE SCENARIO

- 12.9.1 PRODUCT LAUNCHES

- 12.9.2 DEALS

- 12.9.3 EXPANSIONS

13 COMPANY PROFILES

- 13.1 KEY PLAYERS

- 13.1.1 HENKEL AG & CO. KGAA

- 13.1.1.1 Business overview

- 13.1.1.2 Products offered

- 13.1.1.3 Recent developments

- 13.1.1.3.1 Product launches

- 13.1.1.3.2 Deals

- 13.1.1.3.3 Expansions

- 13.1.1.4 MnM view

- 13.1.1.4.1 Right to win

- 13.1.1.4.2 Strategic choices

- 13.1.1.4.3 Weakness and competitive threats

- 13.1.2 ILLINOIS TOOL WORKS INC. (ITW)

- 13.1.2.1 Business overview

- 13.1.2.2 Products offered

- 13.1.2.3 Recent developments

- 13.1.2.3.1 Product launches

- 13.1.2.3.2 Deals

- 13.1.2.3.3 Expansions

- 13.1.2.4 MnM view

- 13.1.2.4.1 Right to win

- 13.1.2.4.2 Strategic choices

- 13.1.2.4.3 Weaknesses & competitive threats

- 13.1.3 SHIN-ETSU CHEMICAL CO., LTD.

- 13.1.3.1 Business overview

- 13.1.3.2 Products offered

- 13.1.3.3 Recent developments

- 13.1.3.3.1 Product launches

- 13.1.3.3.2 Deals

- 13.1.3.3.3 Expansions

- 13.1.3.4 MnM view

- 13.1.3.4.1 Right to win

- 13.1.3.4.2 Strategic choices

- 13.1.3.4.3 Weaknesses and competitive threats

- 13.1.4 DOW INC.

- 13.1.4.1 Business overview

- 13.1.4.2 Products/Solutions/Services offered

- 13.1.4.3 Recent developments

- 13.1.4.3.1 Product launches

- 13.1.4.3.2 Deals

- 13.1.4.3.3 Expansions

- 13.1.4.4 MnM view

- 13.1.4.4.1 Right to win

- 13.1.4.4.2 Strategic choices

- 13.1.4.4.3 Weaknesses and competitive threats

- 13.1.5 H.B. FULLER

- 13.1.5.1 Business overview

- 13.1.5.2 Products/Solutions/Services offered

- 13.1.5.3 Recent developments

- 13.1.5.3.1 Product launches

- 13.1.5.3.2 Deals

- 13.1.5.3.3 Expansions

- 13.1.5.4 MnM view

- 13.1.5.4.1 Right to win

- 13.1.5.4.2 Strategic choices

- 13.1.5.4.3 Weaknesses and competitive threats

- 13.1.6 ELEMENT SOLUTIONS INC (ESI)

- 13.1.6.1 Business overview

- 13.1.6.2 Products/Solutions/Services offered

- 13.1.6.3 Recent developments

- 13.1.6.3.1 Product launches

- 13.1.6.3.2 Deals

- 13.1.6.3.3 Expansions

- 13.1.6.4 MnM view

- 13.1.7 ALTANA AG

- 13.1.7.1 Business overview

- 13.1.7.2 Products/Solutions/Services offered

- 13.1.7.3 Recent developments

- 13.1.7.3.1 Deals

- 13.1.7.4 MnM view

- 13.1.8 CHASE CORP.

- 13.1.8.1 Business overview

- 13.1.8.2 Products offered

- 13.1.8.3 Recent developments

- 13.1.8.3.1 Product launches

- 13.1.8.3.2 Deals

- 13.1.8.3.3 Expansions

- 13.1.8.4 MnM view

- 13.1.9 DYMAX

- 13.1.9.1 Business overview

- 13.1.9.2 Products/Solutions/Services offered

- 13.1.9.3 Recent developments

- 13.1.9.3.1 Product launches

- 13.1.9.3.2 Deals

- 13.1.9.4 MnM view

- 13.1.10 MG CHEMICALS

- 13.1.10.1 Business overview

- 13.1.10.2 Products/Solutions/Services offered

- 13.1.10.3 MnM view

- 13.1.1 HENKEL AG & CO. KGAA

- 13.2 OTHER PLAYERS

- 13.2.1 SPECIALTY COATING SYSTEMS (SCS)

- 13.2.2 CHT GERMANY GMBH

- 13.2.3 CSL SILICONES INC.

- 13.2.4 EUROPLASMA NV

- 13.2.5 PETERS GROUP

- 13.2.6 CONINS PUNE

- 13.2.7 AI TECHNOLOGY, INC.

- 13.2.8 MASTER BOND

- 13.2.9 ACULON, INC.

- 13.2.10 PERCISION COATINGS INC.

- 13.2.11 MERIDIAN ADHESIVES GROUP

- 13.2.12 SHRI MAHALUXMI CHEMICALS

- 13.2.13 CRC INDUSTRIES

- 13.2.14 ELECTRONIC MATERIALS INC. (EMI)

- 13.2.15 ANABOND LIMITED

14 RESEARCH METHODOLOGY

- 14.1 RESEARCH DATA

- 14.1.1 SECONDARY DATA

- 14.1.1.1 Key data from secondary sources

- 14.1.2 PRIMARY DATA

- 14.1.2.1 Key data from primary sources

- 14.1.2.2 Key industry insights

- 14.1.1 SECONDARY DATA

- 14.2 MARKET SIZE ESTIMATION

- 14.2.1 GLOBAL PCB PRODUCTION

- 14.2.2 PCB REVENUE

- 14.2.3 BOTTOM-UP APPROACH

- 14.2.4 TOP-DOWN APPROACH

- 14.3 DATA TRIANGULATION

- 14.4 FACTOR ANALYSIS

- 14.5 RESEARCH ASSUMPTIONS

- 14.6 RESEARCH LIMITATIONS AND RISK ASSESSMENT

15 APPENDIX

- 15.1 DISCUSSION GUIDE

- 15.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 15.3 CUSTOMIZATION OPTIONS

- 15.4 RELATED REPORTS

- 15.5 AUTHOR DETAILS