|

시장보고서

상품코드

1978987

스마트 상업용 빌딩의 AI(2026년)AI in Smart Commercial Buildings 2026 |

||||||

이 보고서는 AI가 상업용 빌딩을 진정으로 변화시키고 있는 분야와 그렇지 않은 분야를 이해하기 위한 결정적인 증거에 기반한 정보입니다.

상업용 빌딩에서 AI의 현주소는 제목이 암시하는 것보다 더 복잡합니다. 2024년 기업의 AI 투자 규모는 전 세계적으로 2,523억 달러에 달할 것으로 예상되며, 조사 데이터에 따르면 상업용 부동산 기업의 92%가 현재 AI를 시험 도입하거나 계획하고 있지만, 의미 있는 성과로 전환되는 비율은 놀라울 정도로 낮습니다. AI 프로그램 목표의 대부분을 달성했다고 보고한 기업은 5% 미만에 불과합니다.

본 보고서는 스마트 상업용 빌딩의 인공지능에 대한 Memoori의 분석 보고서의 3번째 버전으로, 2021년과 2024년에 발행된 버전을 확장한 것입니다. 총 2부작으로 구성된 시리즈의 첫 번째 작품입니다. 이 책에서는 시장 역학, 기술 기반, 이용 사례 및 기회 전망에 대해 살펴봅니다.

이번 조사는 NYSERDA, NREL, LBNL, DOE의 프로그램 평가, 동료 평가 학술 연구, 업계 조사, 그리고 벤더의 주장과 독립적으로 검증된 결과를 구분하는 명확한 증거 평가 프레임워크에 따라 평가된 벤더 사례 연구를 체계적으로 분석한 결과를 기반으로 합니다. 이 보고서는 당사의 2026 엔터프라이즈 구독 서비스에 포함되어 있습니다.

2026년 이 조사가 중요한 이유

- 상업용 건물에서 AI 도입의 가장 큰 장벽으로 과소평가되고 있는 것은 사용 가능한 모델의 고도화나 클라우드 인프라 비용이 아니라 기존 건물에 AI를 통합하는 데 드는 비용과 복잡성입니다. 검증된 도입 사례에 따르면, 엔지니어링 노력과 예산의 최대 75%는 분석 자체가 아니라 기존 시스템을 분석 레이어가 이해할 수 있는 형태로 만드는 데 사용됩니다.

- 벤더의 투명성 문제는 뿌리 깊고, 점점 더 악화되고 있는 문제입니다. 벤더가 보고하는 에너지 절감률은 일반적으로 20-50%로 알려져 있지만, 포트폴리오 규모의 독립적인 평가에서는 일관되게 3-15%로 수렴하고 있습니다. 654개소를 대상으로 한 NYSERDA의 실시간 에너지 관리 프로그램에서는 벤더가 보고한 값에 대한 실현률이 48%에 불과한 것으로 나타났습니다. 본 보고서에서는 모든 성능 주장에 대해 이 기준에 따라 평가했습니다.

- 보험 측면에서는 그동안 거의 간과되어 왔던 새로운 리스크가 등장하고 있습니다. 2026년 1월부터 표준화된 ISO 특약에 따라 머신러닝 시스템으로 인한 신체적 상해, 재산적 손해 및 개인적 상해에 대한 절대적 AI 면책 조항이 도입됩니다. 미국 내 수백 개의 보험사가 ISO 양식을 기준으로 삼고 있기 때문에 건물 운영자가 AI에 부여하는 자율적 통제권이 커지면 커질수록 그 보상 범위의 격차는 더 커질 것입니다.

- 비용 측면에서는 양극화가 빠르게 진행되고 있습니다. 2022년부터 2024년까지 AI 추론 비용은 약 280분의 1로 감소하여 소프트웨어 도입이 더욱 쉬워질 것입니다. 그러나 2018년 이후 센서 가격은 45.6%, BAS 컨트롤러는 35.2%, 네트워크 장비는 32.7% 상승했으며, 이는 대부분의 상업용 건물 재고에서 AI 도입을 위한 여정이 여전히 그 어느 때보다 비싸다는 것을 의미합니다.

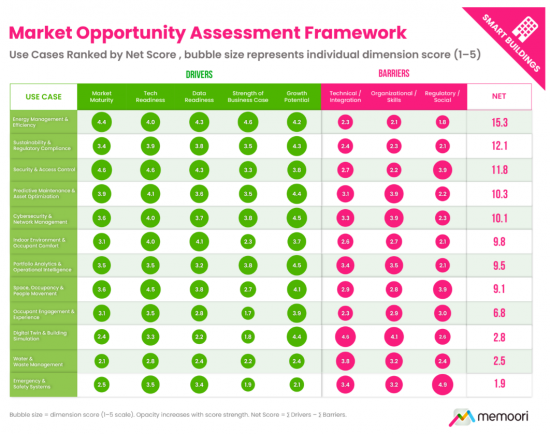

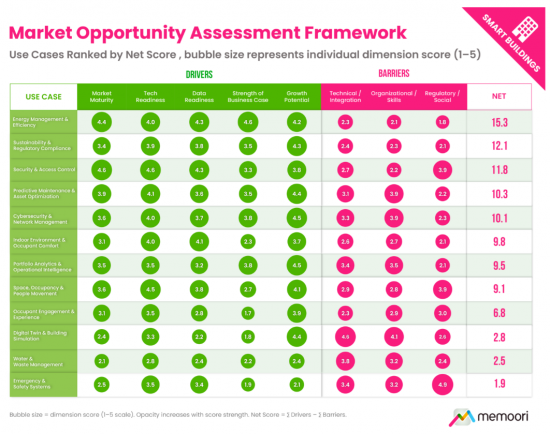

12개 응용 분야에 걸친 69개 AI 이용 사례 평가

이 보고서는 스마트 빌딩 시장을 위해 AI가 활발히 개발 또는 상용화되고 있는 69개의 다양한 이용 사례를 12개의 용도 영역으로 분류하고 있습니다.

각 도메인은 아래와 같은 8차원 평가 프레임워크를 사용하여 평가됩니다. 이 프레임워크는 5가지 긍정적 시장 성장 촉진요인(시장 성숙도, 기술 준비도, 데이터 준비도, 비즈니스 사례의 강점, 성장 가능성)과 3가지 장벽 카테고리(기술 및 통합, 조직 및 기술, 규제 및 사회적 장벽)로 구성되어 있습니다.

에너지 관리 및 효율화

에너지 관리는 20점 만점에 15.3점을 획득하여 유일하게 도입 수준이 가장 높은 영역입니다. 그러나 여기서도 성과에는 중요한 계층 구조가 존재한다는 것이 밝혀졌습니다. 수동적인 대시보드에서는 약 2-3%의 에너지 절감 효과를 얻을 수 있으며, 고장 감지 및 진단에서는 약 9%, 자율 모니터링 및 최적화에서는 독립적인 평가 프로그램에서 약 12-13%의 전력 절감 효과가 입증되었습니다. 시설 관리자에게 고장을 알리는 것과 자율적으로 수정하는 것의 차이는 사소한 것이 아닙니다. 그 차이는 엄청나게 큽니다.

독립적인 증거를 통해 얻은 중요한 직관적이지 않은 중요한 결과는 엄격한 평가에서 소규모 상업용 빌딩이 항상 대규모 빌딩을 능가하는 결과를 보인다는 것입니다. 이는 그동안 고급 벤더의 서비스가 충분히 제공되지 않았던 소규모 상업용 빌딩이 단기적으로 불균형적으로 큰 기회를 가질 수 있음을 시사합니다.

또한, 에너지 관리의 영역은 그리드 연계형 상업용 건물, 가상 발전소, EV 충전 통합, 그리고 매우 중요한 점으로 자동화된 측정 및 검증(M&V)까지 확대되고 있습니다. M&V는 에너지 절감 효과 주장의 '진실의 원천'을 누가 장악할 것인가를 결정하는 전략적 쟁점이 되고 있습니다.

도입 전망: 2031년까지 3단계에 걸쳐 도입 예정

본 보고서에서는 AI 모델의 역량이 아닌 데이터 정비 상태, 의미론적 상호운용성, 거버넌스 및 비즈니스 모델의 성숙도에 따라 3단계의 도입 패턴을 구분하여 제시한다:

- 1단계(현재 - 12개월) : 코파일럿 및 분석 도구 도입. 계측 장비가 잘 갖추어진 건물에서 자연어 인터페이스, 보고서 작성 자동화 및 장애 우선순위 지정이 가능합니다. 경쟁 차별화 요소는 기본 모델이 아니라 워크플로우 통합의 깊이에 있습니다.

- 2단계(12-36개월) : ASHRAE 223P와 같은 시맨틱 상호운용성 표준별 가능, 포트폴리오 규모 모니터링 및 최적화. 건물 성능 기준 준수가 주요 수요의 원동력이 됩니다.

- 3단계(36-60개월) : 특정 서브시스템의 제한적 자율화. 측정 체계가 견고하고 절약 효과를 직접 측정할 수 있는 중앙 플랜트 및 기계 시스템의 폐쇄 루프 AI 제어

미국 상업용 건물 재고의 약 94%를 차지하는 소규모 건물의 대중 시장 문제는 예측 기간 동안 구조적으로 해결되지 않은 채로 남을 것입니다. 시장이 잠재력을 더 빨리 발휘할 수 있는지는 알고리즘의 발전보다는 데이터 인프라, 제공 모델의 혁신, 그리고 구매자가 점점 더 요구하는 엄격한 평가 기준을 충족시키려는 업계의 의지에 달려 있습니다.

본 보고서 구매 대상자

본 조사는 다음과 같은 분들에게 도움이 될 것입니다.

- AI 투자가 진정으로 정당화되는 분야, 도입 순서, 그리고 독립적인 증거를 바탕으로 공급업체의 주장을 평가하는 방법을 이해하고자 하는 상업용 건물 소유주 및 운영자.

- 기술 벤더와 솔루션 제공업체는 구매자의 준비 상태, 규제 압력, 경쟁 환경, 단기적으로 가장 확실한 기회를 창출할 수 있는 영역을 파악해야 합니다.

- 상업용 빌딩 시스템 제조업체는 AI 기능이 각 하드웨어 카테고리에 어떻게 통합되고 있는지, 그리고 통합 계층에서 경쟁의 무대가 어디로 옮겨가고 있는지 평가했습니다.

- 스마트빌딩의 AI 스택 중 어느 영역에서 지속적인 가치가 창출되고 있는지, 그리고 현재 시장 구조가 향후 더욱 통합될 가능성이 높은 영역을 평가하고 있는 투자자(VC, PE 펀드, 기업 VC 부문)

- 기업의 부동산 및 시설 관리팀은 파일럿 단계에서 본격적 배포까지의 격차를 극복하고 전체 포트폴리오에서 AI 투자 우선순위를 정할 수 있는 독립적인 프레임워크를 원하고 있습니다.

- 스마트빌딩 컨설턴트 및 시스템 통합사업자는 고객에 대한 자문 업무에 도움이 될 수 있도록 이용 사례 현황을 반영한 증거 기반 지도를 필요로 합니다.

본 조사는 PDF 보고서로 제공되며, 69개의 이용 사례 평가, 독자적인 에너지 절감 효과에 대한 실증 분석, 부록 A - 모든 소스에 걸친 실증 데이터 세트를 포함하고 있습니다.

LSH 26.04.17This Report is the Definitive Evidence-Based Resource for Understanding Where AI is Genuinely Transforming Commercial Buildings, and Where it is Not

The AI story in commercial buildings is more complicated than the headlines suggest. While corporate AI investment reached $252.3 billion globally in 2024, and survey data shows 92% of commercial real estate organizations are now piloting or planning AI, the conversion to meaningful results has been startlingly poor: fewer than 5% report achieving most of their AI program goals.

This is the third edition of Memoori's analysis of artificial intelligence in smart commercial buildings, extending editions published in 2021 and 2024. It is the first in a two-part series. This volume examines market dynamics, technology foundations, use cases, and the opportunity landscape.

The research draws on program evaluations from NYSERDA, NREL, LBNL, and the DOE; peer-reviewed academic research; industry surveys; and systematic analysis of vendor case studies assessed against an explicit evidence-grading framework that distinguishes independently verified outcomes from vendor claims. This report is included in our 2026 Enterprise Subscription Service.

Why This Research Matters in 2026?

- The most under-appreciated barrier to commercial buildings AI is neither the sophistication of available models nor the cost of cloud infrastructure; it is the cost and complexity of integrating AI with the existing building stock. In documented deployments, up to 75% of engineering effort and budget goes to making existing systems legible to the analytics layer, not to the analytics itself.

- Vendor transparency is a persistent and worsening problem. Vendor-reported energy savings commonly cite 20-50%, while portfolio-scale independent evaluations consistently converge on 3-15%. NYSERDA's real-time energy management program, covering 654 sites, found a realization rate of just 48% against vendor-reported figures. This report grades every performance claim accordingly.

- A new and largely overlooked risk has emerged on the insurance side. From January 2026, standardized ISO endorsements introduce absolute AI exclusions covering bodily injury, property damage, and personal injury arising from machine-learning systems. Because hundreds of US carriers use ISO forms as their baseline, the more autonomous control a building operator grants to AI, the wider their coverage gap becomes.

- The cost picture is bifurcating sharply. AI inference costs dropped approximately 280-fold between 2022 and 2024, making software deployments more accessible. But sensor prices are up 45.6%, BAS controllers up 35.2%, and networking equipment up 32.7% since 2018, meaning the path to AI-readiness still costs more than ever for most of the commercial buildings stock.

69 AI Use Cases Assessed Across 12 Application Domains

This report identifies 69 distinct use cases where AI is being actively developed or commercialized for the smart buildings market, organized across 12 application domains.

Each domain is evaluated using an eight-dimensional scoring framework, which you can see below, covering five positive market drivers (market maturity, technology readiness, data readiness, strength of business case, and growth potential) offset by three barrier categories (technical and integration, organizational and skills, and regulatory and social barriers).

Energy Management & Efficiency

Energy management is the only domain in the top deployment tier, scoring 15.3 out of 20. But even here, the evidence reveals a critical hierarchy of outcomes. Passive dashboards deliver around 2-3% energy savings; fault detection and diagnostics around 9%; and autonomous supervisory optimization achieves verified electric savings of approximately 12-13% in independently evaluated programs. The distinction between alerting a facilities manager to a fault and autonomously correcting it is not marginal; it is order-of-magnitude.

An important counter-intuitive finding from the independent evidence base is that smaller commercial buildings consistently outperform larger ones under rigorous evaluation, suggesting that light commercial buildings, historically underserved by sophisticated vendors, may represent a disproportionate near-term opportunity.

The energy management domain is also expanding to encompass grid-interactive commercial buildings, virtual power plants, EV charging integration, and, critically, automated measurement and verification, which is becoming a strategic battleground determining who controls the source of truth for energy savings claims.

Deployment Outlook: Three Phases Through 2031

The report identifies a three-phase deployment pattern gated not by AI model capability, but by data readiness, semantic interoperability, governance, and commercial model maturity:

- Phase 1 (Now - 12 months): Copilot and analytics deployment. Natural language interfaces, reporting automation, and fault triage in well-instrumented buildings. Competitive differentiation comes from the depth of workflow integration, not the underlying model.

- Phase 2 (12-36 months): Portfolio-scale supervisory optimization, enabled by semantic interoperability standards, like ASHRAE 223P. Building performance standard enforcement is the primary demand driver.

- Phase 3 (36-60 months): Bounded autonomy in specific subsystems. Closed-loop AI control in central plant and mechanical systems where instrumentation is robust, and savings are directly measurable.

The mass-market problem for smaller buildings, roughly 94% of the US commercial buildings stock by count, remains structurally unsolved during the forecast period. Whether the market reaches its potential faster will depend less on algorithmic advances than on data infrastructure, delivery model innovation, and the industry's willingness to meet the rigorous evaluation standards that buyers are increasingly demanding.

Who Should Buy This Report?

This research will be valuable to:

- Commercial Buildings owners and operators seeking to understand where AI investment is genuinely justified, how to sequence deployment, and how to evaluate vendor claims against independent evidence.

- Technology vendors and solution providers who need to understand where buyer readiness, regulatory pressure, and competitive dynamics are creating the most defensible near-term opportunity.

- Commercial Buildings systems manufacturers assessing how AI capability is becoming embedded in hardware categories and where the integration layer battleground is moving.

- Investors (VCs, PE firms, corporate VC arms) evaluating where in the smart buildings AI stack durable value is being created and where the current market structure is likely to consolidate further.

- Corporate real estate and facilities management teams navigating the pilot-to-scale gap and seeking an independent framework for prioritising AI investment across their portfolios.

- Smart building consultants and system integrators who need a current, evidence-based map of the use case landscape to inform client advisory work.

The research is provided as a PDF report with 69 use case assessments, an original energy savings evidence analysis, and Appendix A: the full cross-source evidence dataset.