|

시장보고서

상품코드

1690796

피스 피킹 로봇 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Piece Picking Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

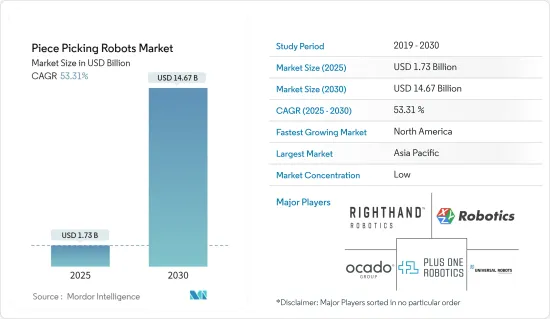

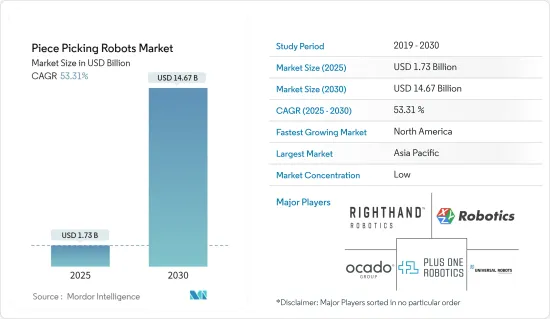

피스 피킹 로봇 시장 규모는 2025년에 17억 3,000만 달러로 예측되고, 2030년에는 146억 7,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 53.31%를 나타낼 전망입니다.

주요 하이라이트

- 자동화에 대한 투자는 특히 전자상거래, 물류, 제조와 같은 분야에서 피스 피킹 로봇의 성장을 촉진하고 있습니다. 효율성, 정밀성, 확장성, 비용 효율성 향상에 대한 요구가 이러한 자동화 트렌드를 주도하고 있습니다. 코로나19 팬데믹과 급증하는 전자상거래 수요로 인해 창고 및 물류 분야의 노동력 부족이 심화되면서 자동화에 대한 투자가 더욱 활발해졌습니다. 그 결과, 피스 피킹 로봇이 주문 피킹과 같은 노동 집약적인 역할을 점점 더 많이 맡으면서 방대한 인력에 대한 의존도가 줄어들고 있습니다.

- 2024년 9월, 이스라엘 메이타에 본사를 둔 Pickommerce는 340만 달러의 투자를 유치했습니다. 이 회사는 이번 투자 유치를 통해 주력 제품인 피코봇 피킹 로봇의 개발, 생산, 마케팅에 박차를 가할 것이라고 발표했습니다. 또한 Pickommerce는 오늘날 물류 허브에서 자동화 추세가 확대되고 있음을 강조하며 로봇이 상자 수집 및 패키지 하역과 같은 업무를 주로 담당하고 있다고 언급했습니다.

- 여러 지역에서 임금이 상승함에 따라 기업들은 운영 비용을 절감하기 위해 로봇에 점점 더 의존하고 있습니다. 피스 피킹 로봇과 자동화 기술에 대한 초기 투자 비용이 만만치 않지만, 장기적으로 인건비를 절감할 수 있고 피로 없이 지속적으로 작업할 수 있다는 장점 때문에 많은 기업들이 로봇을 도입하고 있습니다. 또한 뱅크 오브 아메리카는 2025년까지 전체 제조업의 45%가 로봇 기술이 지배할 것으로 예상하고 있습니다.

- 피스 피킹 로봇은 막대한 초기 투자가 필요하기 때문에 시장 성장에 큰 장애물이 되고 있습니다.

- 다른 첨단 기술과 마찬가지로 피스 피킹 로봇도 정기적인 유지보수가 필요하며, 이는 운영 중단으로 이어질 수 있습니다. 이러한 로봇이 처리량이 많은 산업에 원활하게 적용되려면 이러한 중단을 최소화하는 것이 중요합니다. 또한 다양한 산업에서 고유한 워크플로와 제품 유형을 고려할 때 사용자 정의에 대한 수요가 높습니다. 이러한 요구는 피스 피킹 솔루션의 배포를 복잡하게 만들어 시간과 비용을 모두 증가시킵니다.

- 현재 진행 중인 우크라이나 분쟁으로 인해 피스 피킹 로봇 제조에 필수적인 원자재와 부품의 공급망에 차질이 빚어지고 있습니다. 이러한 중단은 공급 부족, 리드 타임 연장, 비용 증가로 이어질 수 있으며, 이는 모두 시장에 직접적인 영향을 미칩니다. 이에 대응하여 기업들은 대체 공급업체로 전환하거나 현지 생산을 강화하여 시장 역학 관계와 가격을 재편할 수 있습니다. 러시아와 우크라이나의 지속적인 긴장과 중국의 '무관용 정책'이 맞물리면서 전 세계 인플레이션이 눈에 띄게 상승하고 있습니다.

피스 피킹 로봇 시장 동향

소매, 창고, 유통 센터, 물류 센터가 가장 큰 최종 사용자가 될 것

- 시장 수요가 빠르게 변화함에 따라 로봇 공학은 소매업체의 중요한 자산으로 부상하고 있습니다.

- Amazon과 Walmart와 같은 주요 기업들이 이러한 수요의 급증을 주도하고 있습니다. 전 세계 기업들은 주로 인건비 절감을 위해 물류창고에 로봇 자동화를 도입하고 있습니다.

- 물류창고를 넘어 로봇 공학은 리테일 업계에 큰 파장을 일으키고 있습니다. 매장 내 로봇은 단순히 고객을 지원하는 데 그치지 않고 재고를 관리하고 청소 업무까지 담당하고 있습니다. 이러한 혁신은 운영 효율성을 높일 뿐만 아니라 소매업체가 맞춤형 서비스를 제공할 수 있게 해줍니다. 기술의 발전과 경쟁 차별화를 위한 노력으로 로봇 기술의 도입은 둔화될 기미가 보이지 않습니다.

- 전통적인 비즈니스의 패러다임 변화, 특히 오프라인 매장에서 온라인 플랫폼으로 전환하는 소매업의 변화는 조사 대상 시장의 성장을 촉진하고 있습니다. 2024년 2분기에 전자상거래는 미국 전체 소매 판매의 16%를 차지했으며, 이는 전 분기보다 증가한 수치입니다.

- 급증하는 전자상거래 수요, 인력 부족, 신속하고 정확한 주문 처리의 필요성에 대응하기 위해 기업들이 노력하면서 소매, 창고, 유통 센터, 물류 센터에서 피스 피킹 로봇의 도입이 눈에 띄게 증가하고 있습니다. 인공지능(AI), 머신러닝, 3D 비전, 자율 이동 로봇(AMR) 등의 기술 발전에 힘입어 피스 피킹 로봇은 현대 소매 및 물류 인프라의 필수 구성 요소로서 그 위상을 확고히 하고 있습니다.

- Amazon, Walmart, DHL, Alibaba와 같은 거대 기업들이 이러한 기술에 지속적으로 투자하면서 글로벌 물류 및 소매 주문 처리의 궤적에 큰 영향을 미치고 있으며, 이 시장에서 로봇 시스템의 빠른 성장을 예고하고 있습니다.

북미가 큰 시장 점유율을 차지

- 미국과 캐나다와 같은 국가를 포함하는 북미 지역은 전 세계 피스 피킹 로봇 시장에서 상당한 점유율을 차지하고 있습니다. 이러한 우위는 이 지역의 첨단 기술 인프라, 자동화에 대한 강력한 수요, 제조, 물류, 소매 및 창고업과 같은 진화하는 부문에 기인합니다. 북미 지역에서 피스 피킹 로봇을 도입하는 주요 동인으로는 운영 효율성, 비용 절감, 전자상거래의 급증, 노동 시장의 긴축 등이 있습니다.

- 특히 반복적인 수작업에 의존하는 유통 및 창고 부문에서 노동력 부족이 미국과 캐나다에서 자동화 도입을 촉진하고 있습니다. 임금이 상승하고 노동력이 부족해지면서 기업들은 생산을 유지하고 운영 비용을 절감하기 위해 로봇 솔루션으로 눈을 돌리고 있습니다.

- 미국 상공회의소에 따르면 제조업 부문은 팬데믹이 시작되면서 약 140만 개의 일자리가 사라지는 등 큰 타격을 입었습니다. 미국 노동통계국의 2023년 2월 데이터에 따르면 제조업에서 약 75만 개의 일자리가 미충원된 것으로 나타났습니다. 2030년까지 미국에서 200만 개 이상의 제조업 일자리가 공석으로 남을 것이라는 예측도 있습니다. 이로 인해 제조업과 비제조업 기업 모두 자동화 및 로봇 기술을 점점 더 많이 도입하고 있습니다. 또한 수많은 시장 플레이어들이 이 지역에서의 입지를 적극적으로 강화하고 있습니다.

- 예를 들어, 협력 작업 로봇(Rapyuta PA-AMR)과 창고 솔루션으로 알려진 Rapyuta Robotics는 2023년 2월 미국 자회사를 설립했습니다. 이번 미국 법인 설립은 인도에 이어 Rapyuta의 두 번째 해외 진출입니다. 첨단 기술과 하드웨어를 바탕으로 미국 시장에 상당한 가치를 제공하고자 하는 것이 Rapyuta의 목표입니다. 시카고 사무소는 미국 고객들에게 확실한 투자 수익을 보장하기 위한 회사의 노력을 강조하면서 미국 전역의 판매 및 운영을 강화할 것입니다.

- 전자상거래 급증, 기술 발전, 노동력 문제, 자동화에 대한 투자 증가 등의 요인으로 북미의 피스 피킹 로봇 시장이 빠르게 성장하고 있습니다. 제조, 물류, 소매, 전자상거래 등 다양한 분야의 기업들이 효율성을 높이고 비용을 절감하며 정확도를 높이기 위해 로봇을 활용하고 있습니다. 인공지능(AI), 머신러닝, 로봇 시스템의 지속적인 발전을 고려할 때 북미는 향후 몇 년 동안 크게 성장할 뿐만 아니라 전 세계 피스 피킹 로봇 분야에서 중추적인 역할을 유지할 것으로 전망됩니다.

피스 피킹 로봇 산업 개요

피스 피킹 로봇 시장에는 SSI Schaefer, Swisslog, Dematic, RightHand Robotics 등 주요 기업이 있습니다. 이들의 존재와 지속적인 혁신이 시장 지형을 재편하고 있습니다.

예를 들어, 2023년 9월, 선진적인 창고 자동화 솔루션의 구축과 전개에 있어서의 중요한 참가 기업인 MOVU Robotics는 최신의 혁신인 「Movu Eligo」로봇 피킹 암을 발표했습니다.

참가 장벽이 완만한 가운데, 벤처 캐피탈(VC)의 지원을 받은 신규 참가 기업 몇사가 세력을 늘리고 있어 시장 경쟁이 격화할 가능성이 있습니다. 또한 인공지능(AI), 딥러닝, 비전 기술 등의 첨단 기술에도 투자하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력 - Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

- 산업 밸류체인 분석

- COVID-19의 자동화 산업에 대한 영향 평가

- 피스 피킹 로봇의 소프트웨어 기술과 발전

제5장 시장 역학

- 시장 성장 촉진요인

- 풀 케이스 또는 팔레트 피킹에서 피스 플로우로의 전환 및 기술 투자 개선

- 자동화 투자 증가

- 시장의 과제

- 느린 속도, 그리퍼가 비정상적인 품목을 처리할 수 없음, 신뢰성 문제

제6장 시장 세분화

- 로봇의 유형별

- 협력형

- 모바일 기타

- 최종 사용자용도별

- 의약품

- 소매, 창고, 유통 센터, 물류 센터

- 기타 최종 사용자 용도

- 지역별

- 북미

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 라틴아메리카

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- Plus One Robotics Inc.

- Ocado Group Plc

- Universal Robots A/S(TERADYNE, INC.)

- XYZ Robotics Inc.

- Righthand Robotics Inc.

- Berkshire Grey Inc.

- Robomotive BV

- Lyro Robotics Pty Ltd.

- Knapp AG

- Grey Orange Pte. Ltd.

- Hand Plus Robotics Pte Ltd

- Dematic Group(KION Group AG)

- Nomagic Inc.

- Fizyr BV

- Mujin Inc.

- Nimble Robotics Inc.

- Swisslog Holding AG

- Daifuku Co., Ltd.

- Osaro Inc.

- Covariant

- SSI Schaefer Group

제8장 투자 분석

제9장 시장의 미래

HBR 25.05.09The Piece Picking Robots Market size is estimated at USD 1.73 billion in 2025, and is expected to reach USD 14.67 billion by 2030, at a CAGR of 53.31% during the forecast period (2025-2030).

Key Highlights

- Investment in automation is propelling the growth of piece-picking robots, particularly in sectors like e-commerce, logistics, and manufacturing. The push for enhanced efficiency, precision, scalability, and cost-effectiveness is driving this automation trend. Labor shortages in warehousing and logistics, exacerbated by the COVID-19 pandemic and surging e-commerce demands, have spurred heightened investments in automation. As a result, piece-picking robots are increasingly taking on labor-intensive roles, such as order picking, thereby diminishing the reliance on a vast workforce.

- In September 2024, Pickommerce, hailing from Meitar, Israel, clinched funding of USD 3.4 million. The company announced that this capital infusion would accelerate the development, production, and marketing of its flagship, the PickoBot piece-picking robot. Furthermore, Pickommerce underscored the escalating trend of automation in today's logistics hubs, noting that robots are now chiefly tasked with duties like crate collection and package unloading.

- As wages climb in various regions, businesses are increasingly leaning on robots to trim operational expenses. While the upfront investment in piece-picking robots and automation tech can be steep, the promise of long-term labor savings and the benefit of continuous, fatigue-free operation make it enticing. Moreover, Bank of America projects that by 2025, a significant 45% of all manufacturing will be dominated by robotics. In alignment with this trajectory, industry giants such as Raymond Limited, a prominent Indian textile firm, and Foxconn Technology Group, a key Chinese supplier for tech behemoths like Samsung, are poised to substitute 10,000 and 60,000 workers, respectively, with automation in their production facilities.

- Piece-picking robots demand a hefty upfront investment, presenting a notable hurdle to market growth. This investment is further magnified by the necessity for supportive infrastructure. Moreover, technical constraints of these robots-such as their slower speeds, difficulties gripping unconventional items, and concerns about reliability-hinder market expansion.

- Like other advanced technologies, piece-picking robots need regular maintenance, which can lead to operational downtime. To ensure these robots fit seamlessly into high-throughput industries, it's crucial to minimize such interruptions. Additionally, given the unique workflows and product types across various industries, there's a strong demand for customization. This need complicates the deployment of piece-picking solutions, increasing both time and costs.

- The ongoing Ukraine conflict has disrupted the supply chain for raw materials and components vital to manufacturing piece picking robots. Such disruptions can result in shortages, longer lead times, and increased costs, all of which directly influence the market. In response, companies might turn to alternative suppliers or bolster local production, potentially reshaping market dynamics and pricing. The persistent Russia-Ukraine tensions, coupled with China's "Zero Tolerance Policy," have spurred a notable rise in global inflation. This inflation surge has reverberated across various sectors, notably the electronic components and industrial automation industries, driving up component prices and stunting the studied market's growth. Furthermore, elevated inflation and interest rates have curtailed consumer spending, further constraining market expansion.

Piece Picking Robots Market Trends

Retail, Warehousing, Distribution Centers, and Logistics Centers to be the Largest End Users

- As market demands shift swiftly, robotics is emerging as a vital asset for retail companies. Leading the charge are major players such as Amazon, Bossa Nova Robotics, and Brain Corp, propelling this surge in demand. Across the globe, organizations are adopting robotic automation in their warehouses, primarily to cut down on labor costs.

- Retail behemoths, including Amazon.com and Walmart, have seamlessly integrated mobile robots into their warehouses and retail outlets. With consumer expectations leaning towards on-demand retail, there's a noticeable shift in inventory strategies. In light of this, retailers are pouring investments into e-commerce infrastructure, omnichannel fulfillment, and setting up smaller stores in closer proximity to consumers.

- Beyond warehousing, robotics is making waves in retail. In-store robots are not just assisting customers; they're managing inventory and even taking on cleaning duties. Such innovations are not only boosting operational efficiency but also allowing retailers to provide tailored services. With technological strides and a push for competitive differentiation, the adoption of robotics shows no signs of slowing down. As the retail landscape continues to evolve, those companies that harness robotics adeptly stand to gain a pronounced advantage in the market.

- The shifting paradigms of traditional businesses, notably the retail sector's pivot from physical stores to online platforms, are fueling growth in the examined market. For instance, data from the US Census Bureau underscores the steady ascent of e-commerce's prominence in the US retail arena. In Q2 2024, e-commerce constituted 16% of the total retail sales in the US, a rise from the previous quarter. Additionally, from April to June 2024, US retail e-commerce sales eclipsed USD 291 billion, marking a historic high for quarterly revenue.

- As businesses strive to adapt to surging e-commerce demands, labor shortages, and the necessity for swift and accurate order fulfillment, the adoption of piece-picking robots is witnessing a notable uptick across Retail, Warehousing, Distribution Centers, and Logistics Centers. Thanks to technological advancements such as artificial intelligence (AI), machine learning, 3D vision, and Autonomous Mobile Robots (AMRs), piece-picking robots are cementing their status as integral components of modern retail and logistics infrastructure.

- With industry giants like Amazon, Walmart, DHL, and Alibaba continuously investing in these technologies, the trajectory of global logistics and retail fulfillment is set to be significantly influenced, heralding rapid growth for robotic systems in this market.

North America Holds Significant Market Share

- The North American segment, encompassing countries like the US and Canada, holds a significant share of the global piece-picking robots market. This dominance is attributed to the region's advanced technological infrastructure, a robust demand for automation, and evolving sectors such as manufacturing, logistics, retail, and warehousing. Key drivers for the adoption of piece-picking robots in North America include the push for operational efficiency, cost reduction, the surge of e-commerce, and a tightening labor market.

- Labor shortages, particularly in distribution and warehousing sectors reliant on repetitive manual tasks, have notably spurred the adoption of automation in the US and Canada. With wages on the rise and labor becoming scarce, companies are turning to robotic solutions to sustain production and curtail operating costs.

- According to the US Chamber of Commerce, the manufacturing sector faced a major blow, shedding around 1.4 million jobs at the pandemic's onset. Data from February 2023 by the US Bureau of Labor & Statistics highlighted about 750,000 unfilled positions in manufacturing. Projections suggest over 2 million manufacturing roles could remain vacant in the US by 2030. Such dynamics have driven both manufacturing and non-manufacturing entities to increasingly adopt automation and robotic technologies. Furthermore, numerous market players are actively bolstering their presence in the region.

- For example, in February 2023, Rapyuta Robotics, known for its collaborative pick-assist robots (Rapyuta PA-AMR) and warehouse solutions, inaugurated its US subsidiary. This move marks Rapyuta's second international venture following its establishment in India. With its advanced technology and hardware, Rapyuta aims to deliver substantial value to the US market. The Chicago office is poised to boost Rapyuta's sales and operations nationwide, underscoring the company's commitment to ensuring a solid return on investment for its American customers.

- Factors like the e-commerce surge, technological advancements, labor challenges, and heightened investment in automation are propelling the swift growth of North America's piece-picking robots market. Businesses spanning manufacturing, logistics, retail, and e-commerce are leveraging these robots to enhance efficiency, cut costs, and boost accuracy. Given the ongoing advancements in artificial intelligence (AI), machine learning, and robotic systems, North America is not only poised for significant growth in the coming years but is also set to maintain its pivotal role in the global piece-picking robot arena.

Piece Picking Robots Industry Overview

The piece-picking robot market includes several key players, including SSI Schaefer, Swisslog, Dematic, and RightHand Robotics. Their presence and ongoing innovations are reshaping the market landscape.

For instance, in September 2023, MOVU Robotics, a significant player in crafting and deploying advanced warehouse automation solutions, announced its latest innovation, the 'Movu Eligo' robot picking arm. Given their market penetration and advanced product offerings, competitive rivalry is set to escalate during the forecast period.

With moderate entry barriers, several Venture Capital (VC)-)-backed newcomers have gained traction, potentially heightening market competition. To secure a competitive advantage, players enhance bot capabilities for better Return on Investment (ROI) and quicker pick rates. They also invest in advanced technologies like Artificial Intelligence (AI), deep learning, and vision tech. Moreover, consistent access to quality components boosts performance. In summary, the market is characterized by intense competition and high rivalry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Automation Industry

- 4.5 Piece-picking Robot Software Technology and Evolution

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 A Shift from Full-case or Pallet Picking to Piece Flow and Improved Technology Investments

- 5.1.2 Increasing Investments in Automation

- 5.2 Market Challenges

- 5.2.1 Slower Speeds, Inability of the Grippers to Deal with Unusual Items, and Reliability Issues

6 MARKET SEGMENTATION

- 6.1 By Type of Robot

- 6.1.1 Collaborative

- 6.1.2 Mobile and others

- 6.2 By End User Application

- 6.2.1 Pharmaceutical

- 6.2.2 Retail/Warehousing/Distribution Centers/Logistics Centers

- 6.2.3 Other End User Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Plus One Robotics Inc.

- 7.1.2 Ocado Group Plc

- 7.1.3 Universal Robots A/S (TERADYNE, INC.)

- 7.1.4 XYZ Robotics Inc.

- 7.1.5 Righthand Robotics Inc.

- 7.1.6 Berkshire Grey Inc.

- 7.1.7 Robomotive BV

- 7.1.8 Lyro Robotics Pty Ltd.

- 7.1.9 Knapp AG

- 7.1.10 Grey Orange Pte. Ltd.

- 7.1.11 Hand Plus Robotics Pte Ltd

- 7.1.12 Dematic Group (KION Group AG)

- 7.1.13 Nomagic Inc.

- 7.1.14 Fizyr B.V.

- 7.1.15 Mujin Inc.

- 7.1.16 Nimble Robotics Inc.

- 7.1.17 Swisslog Holding AG

- 7.1.18 Daifuku Co., Ltd.

- 7.1.19 Osaro Inc.

- 7.1.20 Covariant

- 7.1.21 SSI Schaefer Group