|

시장보고서

상품코드

1431449

플라스틱 필름 커패시터 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2024-2029년)Plastic Film Capacitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

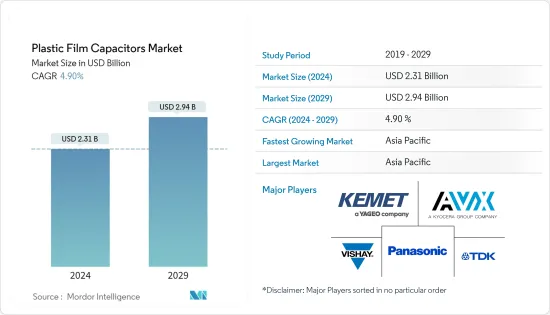

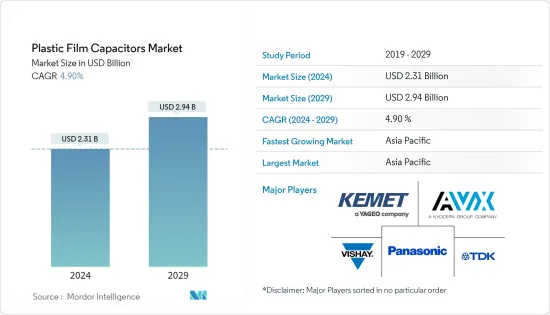

세계 플라스틱 필름 커패시터 시장 규모는 2024년 23억 1,000만 달러로 추정되며, 2029년에는 29억 4,000만 달러에 달할 것으로 예상되며, 예측 기간(2024-2029년) 동안 연평균 4.90%의 CAGR로 성장할 것으로 예상됩니다.

플라스틱 필름 커패시터는 주로 다양한 플라스틱을 유전체 재료로 사용하는 여러 커패시터 제품군을 포함합니다. 오디오, 라디오 회로, 저전압에서 중전압으로 작동하는 회로와 같은 응용 분야에서 종이형 커패시터를 크게 대체하고 있습니다. 커패시터에 자주 사용되는 플라스틱에는 폴리카보네이트, 폴리프로필렌(PP), 폴리에스테르(PET), 폴리스티렌, 폴리설폰, 캅톤 폴리이미드, 테플론(PTFE 불소수지), 금속화 폴리에스테르(금속화 플라스틱) 등이 있습니다.

주요 하이라이트

- 플라스틱 필름 커패시터 사용의 가장 큰 장점은 낮은 왜곡률과 뛰어난 주파수 특성을 가지고 있다는 것입니다. 또한 이러한 커패시터에 사용되는 플라스틱 필름의 범위가 넓기 때문에 다재다능합니다. 이 커패시터는 빠르게 마모되지 않기 때문에 커플링 회로, 디커플링 회로, 오디오 회로의 ADC와 같은 고전압 및 고주파 애플리케이션에 적합합니다.

- 다양한 산업 분야에서 지속가능한 발전 솔루션에 대한 관심이 높아지면서 태양광 및 풍력 발전용 인버터에 대한 수요가 증가하고 있습니다. 이에 대응하기 위해 업체들은 새로운 플라스틱 필름 커패시터를 출시하고 있습니다. 예를 들어, 2021년 5월 New Yorker Electronics는 얇은 금속화 폴리프로필렌 필름으로 제조되어 높은 정전 용량을 제공하는 CDE-Illinois 커패시터(33-220uF, 최대 1,440WVDC, -40°C-85°C)를 출시했습니다. 이 제품은 DC 링크, 전기 히터, 모터 구동, 유도 히터, UPS 시스템, 태양광 및 풍력 인버터 등의 애플리케이션을 위해 설계되었습니다.

- 또한, 헬스케어 분야에서의 웨어러블 채택은 지난 몇 년 동안 견인력을 얻고 있으며, 이는 조사 시장에 영향을 미치는 중요한 요인 중 하나입니다. 웨어러블 커넥티드 디바이스의 주요 동향으로는 통증 관리 웨어러블 디바이스에 대한 수요 증가, 심혈관 질환 관리를 위한 웨어러블 사용 증가 등을 들 수 있습니다.

- 또한, 2022년 4월 Electronix는 자체 개발한 유기 금속 분해(MOD) 전도성 금속 잉크 솔루션의 전체 제품군을 생산 규모에서 사용할 수 있게 되었다고 발표했습니다. 일렉트로닉스는 단일 잉크 제품을 출시하는 것뿐만 아니라 CircuitJet이라는 주문형 인쇄회로기판(PCB) 인쇄 및 수리를 위한 독자적인 소형 데스크톱 프로토타입 애디티브 제조 솔루션 등 잉크 제품군을 통해 고객에게 토탈 솔루션을 제공합니다. 토탈 솔루션을 고객에게 제공하고 있습니다. 이러한 신흥국 시장 개척도 연구 시장을 견인할 것으로 보입니다.

- COVID-19의 대유행은 전 세계 산업 전반의 공급망에 큰 혼란을 가져왔습니다. 바이러스 확산에 대응하기 위해 전 세계적으로 많은 기업이 운영을 중단하거나 축소했습니다. 그러나 대유행 이후 시나리오에서 전자부품 시장은 원자재 및 부품 생산 수준의 공급망 전체에서 작동 수준이 증가했습니다. 이로 인해 다양한 지역과 국가에서 매출이 증가했습니다.

- 또한 전자부품은 자원 집약적입니다. 표면 실장 전자부품의 대량 생산에 소비되는 재료는 일반적으로 설계된 분말 또는 페이스트 형태로 제공되며 커패시터와 같은 수동 부품 생산과 관련된 가장 큰 "변동 비용"을 구성합니다.

플라스틱 필름 커패시터 시장 동향

가전제품이 큰 시장 점유율을 차지할 전망

- 가전제품에 대한 수요가 급증하면서 시장을 견인하고 있습니다. 스마트폰, 태블릿과 같은 기기에는 고성능을 발휘할 수 있는 소형 안테나가 필요합니다. 이러한 안테나 시스템에는 특정 성능 특성을 가진 커패시터가 필요합니다. 커패시터는 안테나 시스템에서 중요한 부품입니다. 안테나 시스템에서 커패시터의 가장 일반적인 용도는 주파수 조정, 임피던스 정합, 필터링 등입니다. 이러한 용도에 사용되는 커패시터는 낮은 누설 전류, 고품질 계수, 높은 선형성 등 우수한 성능 특성이 요구됩니다.

- 스마트폰 안테나 시스템의 엄격한 성능 요건을 충족하는 커패시터를 생산하기 위해 커패시터 기술은 많은 발전을 거듭해 왔습니다. 예를 들어, 커패시터 제조업체는 미세전자기계시스템(MEMS) 기술을 활용하여 스마트폰 안테나 시스템용 초소형, 초박형 커패시터를 생산하고 있습니다.

- 소비자기술협회에 따르면 미국 가전제품 시장의 소매 판매량은 2012년부터 2021년까지 지속적으로 증가하고 있으며, 2023년 소매 판매량 예측에 따르면 미국 가전제품 소매 판매량은 4,850억 달러에 달할 것으로 예상됩니다.

- 또한 커패시터는 일반적으로 카메라 플래시 모듈에 내장되어 있습니다. 카메라 플래시 커패시터는 저저항, 저인덕턴스 구조로 설계되어 플래시 튜브에 에너지를 최대한 빠르게 공급하고 전류 펄스의 빠른 상승 시간을 실현합니다. 또한, 고전류로 인한 국부적인 발열을 피하기 위해 내부 연결은 더욱 견고하게 만들어졌습니다. 플래시 커패시터가 없으면 디지털 카메라의 배터리는 빠르게 소모됩니다.

- 또한 스마트 워치, 헤드 마운트 디스플레이, 바디 마운트 카메라, 귀에 착용하는 장치, 피트니스 트래커와 같은 웨어러블 전자 제품의 발전은 플라스틱 필름 커패시터의 기술 혁신과 채택을 촉진하고 있습니다. 예를 들어, 커패시터는 10,000회 충전 및 방전 후 에너지 성능이 몇 % 포인트 감소하는 내마모성 때문에 웨어러블 가전 제품에 널리 사용되고 있습니다.

아시아태평양이 큰 시장 점유율을 차지할 것으로 예상

- 아시아태평양은 커패시터의 가장 중요한 시장 중 하나입니다. 중국에서는 자동차 산업이 증가하고 있으며 세계 자동차 시장에서 점점 더 중요한 역할을 하고 있습니다. 중국 정부는 자동차 부품 부문을 포함한 자동차 산업을 국가 주력 산업 중 하나로 간주하고 있습니다. 중국 정부는 중국의 자동차 생산량이 2020년까지 3,000만 대, 2025년까지 3,500만 대에 달할 것으로 예상하고 있습니다. 이는 연구용 커패시터 수요를 견인할 것으로 예상됩니다.

- 전기차의 인기가 높아지고 있으며, 중국은 전기차를 채택하는 주요 국가 중 하나로 여겨지고 있습니다. 중국의 13차 5개년 계획은 하이브리드 자동차, 전기차 등 친환경 운송 솔루션의 개발을 장려하고 있으며, 이는 중국 교통 부문의 발전을 촉진할 것으로 기대됩니다.

- 중국승용차협회(CPCA)의 데이터에 따르면 2021년 11월과 12월 신에너지 자동차(NEV) 판매량은 2배 이상 증가하여 연간 169% 증가한 299만 대를 기록했으며, 세계 최대 자동차 시장인 중국 신차 판매량의 14.8%를 차지했습니다. 이는 중국의 플라스틱 필름 커패시터 채택을 촉진할 것으로 예상됩니다.

- IEA에 따르면 중국은 재생에너지 성장의 확실한 선두주자이며, 2022년까지 전체 청정에너지 믹스의 약 40%를 차지할 것으로 추정됩니다. 또한 중국은 2020년 태양광 패널 목표를 초과 달성했습니다.

- 또한 호주 뉴사우스웨일스(NSW) 주정부는 무공해 자동차 도입을 촉진하기 위해 2021년에 전기자동차 전략을 도입하고 총 5억 호주 달러의 자금을 지원했습니다. 2021년 상반기 호주에서는 8,688대의 전기차가 판매되었습니다. 호주는 전기차 지원 인프라도 확대되고 있습니다. 호주에는 3,000개 이상의 전기차 공용 충전기가 있습니다. 호주 전기차 시장에는 31개의 전기차 모델이 있으며, 2022년 말에는 58개의 전기차 모델이 존재할 것으로 추정됩니다.

플라스틱 필름 커패시터 산업 개요

플라스틱 필름 커패시터 시장은 세분화되어 있으며, 여러 대기업이 존재합니다. 시장 점유율이 높은 이들 대기업들은 해외 고객 기반 확대에 주력하고 있습니다. Panasonic Corporation, Vishay Intertechnology Inc., TDK Corporation, AVX Corporation, KEMET Corporation 및 기타 여러 기업이 이 시장에 참여하고 있습니다. 이들 기업은 전략적 협력 이니셔티브를 통해 시장 점유율과 수익성을 높이고 있습니다.

- 2023년 11월 일렉트로큐브는 다양한 군용, 상업용, 육상 및 해상 응용 분야에 사용되는 고전력 인버터용으로 특별히 조정된 금속화 폴리프로필렌 필름 커패시터를 개발했습니다. 이 커패시터는 AC 신호 및 펄스 신호로 인한 고온 및 고전류 환경에서도 우수한 성능을 발휘할 수 있도록 세심하게 설계 및 최적화되어 있습니다. 또한, 열화 없이 높은 서지 전류를 견딜 수 있는 뛰어난 능력으로 전해 커패시터를 대체할 수 있는 탁월한 대안이 될 수 있습니다.

- 2023년 5월 사빅의 엘크레스는 폴리카보네이트 공중합체를 기반으로 한 HTV150A 필름을 발표했습니다. 이 필름은 최대 150℃의 온도와 100kHz의 주파수에 노출될 경우 소산 손실을 최대 40%까지 줄일 수 있습니다. 이 소재는 이미 박막 커패시터 필름에서 그 효과를 입증한 바 있습니다. 엔지니어들은 엘크레스 HTV150A 유전체 필름의 낮은 소산 손실로 인해 작동 효율 향상, 내부 발열 감소, 핫스팟 온도 안정화 등의 이점을 누릴 수 있어 커패시터 설계의 유연성을 향상시킬 수 있습니다. 이 필름은 커패시터의 손실을 줄일 수 있을 것으로 기대됩니다.

기타 혜택:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 매력 - Porter's Five Forces 분석

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 신규 참여업체의 위협

- 경쟁 기업 간의 경쟁 관계

- 산업 밸류체인 분석

- 거시경제 동향 업계에 대한 영향 평가

제5장 시장 역학

- 시장 성장 촉진요인

- EV의 등장에 의한 자동차 업계 수요 확대

- 일렉트로닉스 복잡화

- 시장 성장 억제요인

- 금속 가격 상승이 부품 제조 비용에 영향

제6장 시장 세분화

- 유형

- 폴리프로필렌

- 폴리에틸렌

- 기타 유형(PTFE, PPS 등)

- 용도

- 자동차

- 통신

- 산업용

- 항공우주 및 방위

- 가전

- 의료

- 기타 용도

- 지역

- 아메리카

- 유럽·중동 및 아프리카

- 아시아태평양(일본과 한국을 제외)

- 일본과 한국

제7장 경쟁 상황

- 기업 개요

- KEMET Corporation(Yageo company)

- Panasonic Corporation

- Vishay Intertechnology Inc.

- TDK Corporation

- AVX Corporation(Kyocera Corp)

- Murata Manufacturing Co. Ltd.

- Cornell Dubilier Electronics Inc.

- Desai Electronics

- Shanghai Yinyan Electronic

- Rubycon Corporation

- Nantong Jianghai Capacitor Co. Ltd.

- Nichicon Corporation

- Wima GmBH & Co. KG

제8장 투자 분석

제9장 시장 향후 전망

KSM 24.03.07The Plastic Film Capacitors Market size is estimated at USD 2.31 billion in 2024, and is expected to reach USD 2.94 billion by 2029, growing at a CAGR of 4.90% during the forecast period (2024-2029).

Plastic Film capacitors primarily include multiple families of capacitors that use different plastics as dielectric materials. They significantly replace paper-type capacitors in applications such as audio, radio circuits, and circuits operating at low to moderate voltages. Some of the commonly used plastics in these capacitors include polycarbonate, polypropylene (PP), polyester (PET), polystyrene, polysulfone, Kapton polyimide, Teflon (PTFE fluorocarbon), and metalized polyester (metalized plastic).

Key Highlights

- The significant advantage of using a plastic film capacitor is that it has a low distortion factor and exceptional frequency characteristics. Also, the wide range of plastic films that are used for these capacitors makes them versatile. These capacitors do not wear off quickly and are suited for high-voltage and high-frequency applications such as coupling and decoupling circuits and audio circuit ADCs.

- With a rising focus on sustainable solutions across various industries for power generation, the demand for solar and wind power inverters has increased. To cater to this, vendors are introducing new plastic-film capacitors. For instance, in May 2021, New Yorker Electronics introduced CDE-Illinois capacitors (33 to 220 uF and up to 1,440 WVDC, -40°C to +85°C) that are manufactured with low-profile metalized polypropylene film and offer high capacitance. The product is designed for applications such as DC links, electric heaters, motor drives, induction heaters, UPS systems, and solar and wind power inverters.

- Moreover, the adoption of wearables in the healthcare sector has been gaining traction in recent times, which, in turn, has been one of the significant factors influencing the market studied. The major trends in wearable connected devices include the increasing demand for pain management wearable devices and the increased use of wearables for cardiovascular disease management, among others.

- Further, in April 2022, Electroninks, Inc. announced the production-scale availability of its full suite of proprietary metal-organic decomposition (MOD) conductive metal ink solutions. In addition to bringing standalone ink products to market, Electroninks is also bringing total solutions to the customer with its line of ink products, including its own small desktop prototype additive manufacturing solution for rapid on-demand printed circuit board (PCB) printing and repair, called CircuitJet. These developments will also drive the study market.

- The COVID-19 pandemic led to immense disruptions in supply chains across industries globally. Many businesses globally halted or reduced operations to help combat the spread of the virus. However, in post pandemic scenario, the electronic components market, leading to increased operation levels across the supply chain for raw materials and component production levels. This denoted a rise in sales among a range of regions and countries.

- Moreover, electronic components are resource-intensive. The materials consumed in the mass production of surface-mount electronic components usually come in the form of engineered powders and pastes, making up the largest "variable cost" associated with producing passive components like capacitors.

Plastic Film Capacitors Market Trends

Consumer Electronics is Expected to Hold Significant Market Share

- The rapid surge in demand for consumer electronics products has boosted the market. Devices such as smartphones and tablets need small antennas capable of delivering high performance. These antenna systems demand capacitors with specific performance characteristics. Capacitors are critical components in antenna systems. The most general applications of capacitors in antenna systems include frequency tuning, impedance matching, and filtering. Capacitors for use in these applications must have prominent performance characteristics, including low leakage current, a high quality factor, and high linearity.

- Numerous advancements in capacitor technology have been made to produce capacitors that meet the strict performance requirements of smartphone antenna systems. For instance, capacitor manufacturers use microelectromechanical systems (MEMS) technology to make ultra-small and thin capacitors for smartphone antenna systems.

- According to the Consumer Technology Association, the retail revenue of the consumer electronics market in the United States constantly increased during the period from 2012 to 2021. Based on the projected retail sales for 2023, consumer electronics retail sales in the United States is expected to reach USD 485 billion.

- Moreover, capacitors are commonly incorporated in the flash module of cameras. Camera flash capacitors are constructed to have low resistance and significantly low inductance to deliver their energy to the flash tube as fast as possible, achieving a fast rise time on the pulse of current. The internal connections are also made more robust to avoid localized heating due to the high current. Without the flash capacitor, the batteries located inside the digital cameras would drain quickly.

- Furthermore, developments in wearable electronics, such as smartwatches, head-mounted displays, body-worn cameras, ear-worn devices, and fitness trackers, among others, drive innovations and the adoption of plastic film capacitors. For instance, capacitors are being widely used in wearable consumer electronics due to their wear and tear capability, which exhibits a loss of a few percentage points of energy performance after 10,000 cycles of charging and discharging.

Asia-Pacific is Expected to Hold Significant Market Share

- The Asia-Pacific region is one of the most important markets for capacitors. The automotive industry is increasing in China, and the country plays an increasingly important role in the global automotive market. The government views its automotive industry, including the auto parts sector, as one of the country's pillar industries. The government of China estimates that China's automobile output is expected to reach 30 million units by 2020 and 35 million units by 2025. This is expected to drive the studied capacitors' demand.

- The popularity of EVs is growing, and China is regarded as one of the dominant adopters of electric vehicles. The country's 13th Five-Year Plan promotes the development of green transportation solutions, such as hybrid and electric vehicles, for advancements in the country's transportation sector.

- According to data by the China Passenger Car Association (CPCA), sales of these new energy vehicles (NEVs) more than doubled in November and December of 2021, increasing full-year deliveries by 169% to a record 2.99 million units, or 14.8% of new sales in China, the world's largest vehicle market. This is anticipated to boost the country's adoption of plastic film capacitors.

- According to the IEA, China was the undisputed leader in renewable growth, estimated to account for around 40% of its total clean energy mix by 2022. The country also surpassed its 2020 solar panel target.

- Additionally, to promote the adoption of zero-emission vehicles, the New South Wales (NSW) state government in Australia introduced an Electric Vehicle Strategy in 2021 with funding totaling almost AUD 500 million. 8,688 electric vehicles were sold during the first half of 2021 in Australia. The country is witnessing a growing electric vehicle support infrastructure as well. Australia has more than 3,000 public chargers for electric vehicles. The country's EV market had 31 electric vehicle models, and by the end of 2022, it was estimated that there would be 58 electric vehicle models in the country.

Plastic Film Capacitors Industry Overview

The plastic film capacitors market is fragmented and has several major players. These major players with prominent shares in the market are focusing on expanding their customer base across foreign countries. The market comprises Panasonic Corporation, Vishay Intertechnology Inc., TDK Corporation, AVX Corporation, KEMET Corporation, and many others. These companies leverage strategic collaborative initiatives to increase their market shares and profitability.

- November 2023: Electrocube has developed a range of metalized polypropylene film capacitors specifically tailored for high-power inverters used in various military, commercial, land, and sea applications. These capacitors have been carefully designed and optimized to function exceptionally well in high temperature and high current scenarios with AC and pulsing signals. Furthermore, their remarkable capability to withstand high surge currents without deterioration makes them an outstanding alternative to electrolytic capacitors.

- May 2023: Sabic's Elcres introduced its polycarbonate copolymer-based HTV150A films, which can potentially decrease dissipation losses by up to 40% when exposed to temperatures up to 150°C and frequencies up to 100 kHz. This material has already demonstrated its effectiveness in thin-wall capacitor films. By utilizing Elcres HTV150A dielectric films with lower dissipation losses, engineers can benefit from improved operating efficiency, reduced internal heat generation, and more stable hot spot temperatures, resulting in increased flexibility when designing capacitors. It is anticipated that these films will lead to reduced dissipation losses in capacitors.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Buyers

- 4.2.2 Bargaining Power of Suppliers

- 4.2.3 Threat of Substitute Products

- 4.2.4 Threat of New Entrants

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macro Economic Trends on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Demand from the Automotive Industry due to the Advent of EVs

- 5.1.2 Increasing Complexity of Electronics

- 5.2 Market Restraints

- 5.2.1 Rising Metal Prices Impacting Component Production Costs

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Polypropylene

- 6.1.2 Polyethylene

- 6.1.3 Other Types (PTFE, PPS, etc.)

- 6.2 Applications

- 6.2.1 Automotive

- 6.2.2 Telecommunications

- 6.2.3 Industrial

- 6.2.4 Aerospace & Defense

- 6.2.5 Consumer Electronics

- 6.2.6 Medical

- 6.2.7 Other Applications

- 6.3 Geography

- 6.3.1 Americas

- 6.3.2 Europe, Middle East & Africa

- 6.3.3 Asia-Pacific (Excl. Japan and Korea)

- 6.3.4 Japan and Korea

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 KEMET Corporation (Yageo company)

- 7.1.2 Panasonic Corporation

- 7.1.3 Vishay Intertechnology Inc.

- 7.1.4 TDK Corporation

- 7.1.5 AVX Corporation (Kyocera Corp)

- 7.1.6 Murata Manufacturing Co. Ltd.

- 7.1.7 Cornell Dubilier Electronics Inc.

- 7.1.8 Desai Electronics

- 7.1.9 Shanghai Yinyan Electronic

- 7.1.10 Rubycon Corporation

- 7.1.11 Nantong Jianghai Capacitor Co. Ltd.

- 7.1.12 Nichicon Corporation

- 7.1.13 Wima GmBH & Co. KG