|

시장보고서

상품코드

1437321

수술실 통합 : 세계 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2024-2029년)Global Operating Room Integration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

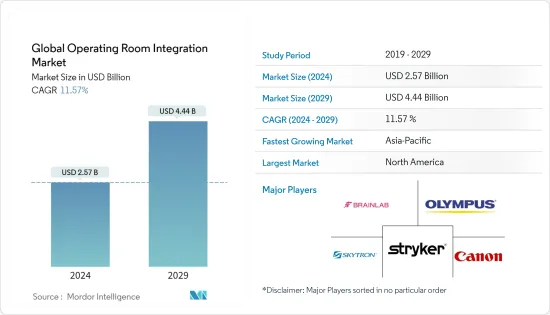

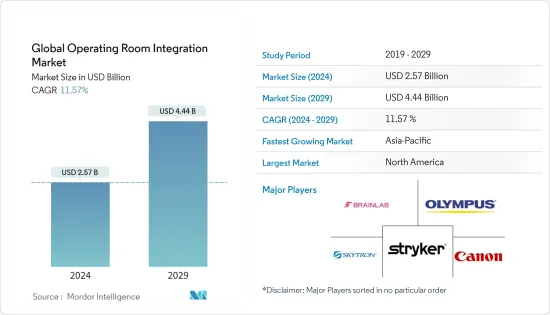

세계의 수술실 통합 시장 규모는 2024년 25억 7,000만 달러로 추정되고, 2029년까지 44억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2029년) 동안 11.57%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다.

COVID-19에서 수술을 기다리는 환자에게 상당한 대기 시간이 발생했습니다. British Journal of Surgery에 게재된 연구에 따르면 COVID-19의 영향으로 2020년에는 세계에서 2,800만 건의 수술이 연기 또는 취소되었으며, 수백만 건의 수술이 2021년으로 연기되었습니다. 따라서 수천 명의 환자가 수술 지연에 직면하고 있기 때문에 일정 효율성을 높일 필요성이 더욱 중요해졌습니다. 게다가 팬데믹에 의해 시장 관계자는 새로운 방법으로의 운영을 강요받아 디지털화가 가속하고 있습니다. 팬데믹에 의한 수술 전 계획, 화상 회의, 원격으로 수술 후 환자 참여가 증가함에 따라 수술실과 수술 절차는 다음 세 가지 방법으로 변경되었습니다.

저침습 수술에 대한 환자의 급증과 같은 요인이 시장 성장의 주요 요인이 되었습니다. 이는 주로 비만 등의 증상을 치료하기 위한 외과적 개입에 대한 의식이 높아져 의료기기 제조업체가 첨단 수술실 통합의 개발을 진행해 왔기 때문입니다. 게다가 노인 인구 증가로 수술 수요가 증가하고 수술 건수가 누적적으로 증가하는 것도 시장 성장을 가속할 것으로 예상됩니다. 예를 들어, 2020년 '미국에서 노인에 대한 대수술의 발생률 및 누적 위험'이라는 제목의 기사에서는 고령자 100명당 연간 9건 가까이의 대수술이 진행되고 있어 메디케어 수급자의 7명에게 1명 이상이 5년 동안 주요 수술을 받았으며, 이는 거의 500만명 가까이의 노인을 대상으로 한 재수술이었다고 합니다.

게다가 말기 만성질환은 일반적으로 수술이 필요하기 때문에 세계에서 만성질환의 부담이 증가하고 있는 것도 수술실 수요를 증가시키는 주요 요인 중 하나입니다. 예를 들어 미국 보건협회에 따르면 2022년 수술실이 활동을 재개하고 의료건강 치료와 수술 급증이 관찰되었으며, 그 결과 2020년 말까지의 수술률은 2019년에 비해 10%밖에 저하하지 않았습니다. 경제협력 개발기구(OECD)에 따르면 2020년 터키에서 보고된 백내장 수술 건수는 393,901건이었습니다. 이 정보원에 따르면, 2020년 이탈리아에서의 인공 고관절 치환술의 건수는 84,647건, 제왕 절개의 건수는 약 114,601건이었습니다. 따라서 이 수술 수가 증가하면 수술실 수요가 증가하여 시장 성장에 기여할 것으로 보입니다.

따라서, 상기 요인은 예측 기간 동안 시장 성장을 가속할 것으로 예상됩니다.

수술실 통합 시장 동향

심장혈관 수술 부문은 수술실 통합 시장에서 주요 시장 점유율을 유지할 것으로 예상됩니다.

신형 코로나바이러스 감염(COVID-19)의 갑작스런 발달로 인해 다양한 정부가 전 세계적으로 갑작스런 한계를 부과했기 때문에 시장 성장이 방해된 것으로 나타났습니다. 이로 인해 공급망 인력이 줄어들고 제조 공정에도 영향을 미쳤습니다. 그러나 팬데믹 기간 이후의 엄격한 봉쇄 완화는 환자 유입을 증가시켜 시장 성장을 가속시켰습니다.

심장혈관 질환 및 관련 수술이 세계에서 급증하고 있기 때문에 심장혈관 수술 부문은 조사 대상 시장에서 압도적인 점유율을 유지할 것으로 예상됩니다. 예를 들어, 유럽 심장 네트워크가 2021년에 발표한 데이터에 따르면, 유럽 연합에서는 6,000만명 이상이 심혈관 질환을 앓고 있으며, 매년 1,300만명 가까이가 새롭게 심혈관 질환으로 진단되고 있습니다. 또한 비만과 같은 건강에 해로운 라이프스타일로 인한 질병 부담이 증가하고 있기 때문에 과체중이 시장 성장을 가속할 것으로 예상됩니다. 2020년에 A-mansia Biotech가 발표한 논문에서는 세계 20억 명 이상의 18세 이상의 성인이 과체중이라고 말했습니다. 이 중 세계 6억 5,000만 명 이상이 비만입니다. 세계보건기구(WHO)는 2021년, 담배 사용 등의 수정 가능한 행동 위험인자가 매년 720만명 이상의 사망의 원인이 되고 있으며, 연간 160만명이 신체활동 부족에 기인하고 있을 가능성 있다고 발표했습니다. 2021년 영국 심장재단이 발표한 연구에 따르면 2020년 영국에서 약 37만 1,000건의 심장수술과 수술이 이루어졌습니다. 또한 2021년 미국 심장협회가 발표한 논문에 따르면 미국에서는 매년 약 4만 명의 어린이가 선천성 심장 수술을 받고 있습니다. 이러한 심장혈관 수술 수 증가는 심장혈관 수술 수요 증가 및 수술실 통합 절차의 개선으로 이어집니다.

따라서, 상기 요인은 예측 기간 동안 조사 대상 부문의 성장을 가속할 것으로 예상됩니다.

북미는 시장에서 중요한 점유율을 유지할 것으로 예상되며, 예측 기간에도 비슷한 점유율을 획득할 것으로 예상됩니다.

미국은 이 지역에서 만성 질환의 만연과 첨단 수술 치료의 채택 증가로 세계 시장을 주도할 가능성이 높습니다. 예를 들어, 국립 만성질환 예방건강 증진센터(2021년 1월)에 따르면 미국 성인 10명 중 6명이 만성질환을 앓고 있으며 성인 10명 중 4명이 2개 이상의 만성질환을 안고 그리고 이러한 증상이 발생합니다. 이 나라의 헬스케어 제도에는 약 3조 8,000억 달러의 헬스케어비가 들어가고 있습니다. 게다가 미국 수술실 통합시장의 높은 성장 가능성으로 인해 이 나라에서 사업을 전개하고 있는 기업은 경쟁사보다 우위를 차지하기 위한 시장전략을 신청하고 있으며, 이에 따라 조사 대상이 되고 있는 미국 시장은 예측기간 동안 성장이 더욱 확대될 것으로 예상됩니다. 예를 들어, Getinge는 2021년 6월에 AI 기반 수술실 관리 시스템 'Torin'을 미국에서 출시했다고 밝혔습니다.

게다가 연구개발 활동 증가, 첨단 기술에 대한 신속한 적응, 양호한 헬스케어 인프라의 존재로 인해 지역 시장 전체의 성장이 크게 촉진되고 있습니다.

수술실 통합 산업 개요

수술실 통합 시장은 세분화되어 경쟁이 심하고 여러 주요 기업으로 구성되어 있습니다. 시장 점유율의 점에서 현재, 몇몇 대기업은 시장을 독점하고 있습니다. 현재 시장을 독점하는 기업으로는 Brain Lab AG, Canon Inc., Doricon Medical Systems, Getinge AB, Karl Storz GMBH, Olympus Corporation, Merivaara Corp., Steris PLC, Stryker Corporation, Skytron LLC 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제 조건 및 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 외과 수술 건수 증가

- 저침습 수술을 요구하는 환자의 급증 및 수술실에서 환자의 안전에 대한 우려

- 시장 성장 억제요인

- 높은 수술실 통합의 비용 및 유지보수

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체 제품의 위협

- 경쟁 기업간 경쟁 관계의 격렬

제5장 시장 세분화

- 컴포넌트별

- 소프트웨어

- 서비스

- 용도별

- 일반 외과

- 정형 외과

- 심장혈관 수술

- 뇌신경 외과

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Brain Lab AG

- Canon Inc

- Doricon Medical Systems

- Getinge AB

- Karl Storz GMBH &Co. KG

- Olympus Corporation

- Merivaara Corp.

- Steris PLC

- Stryker Corporation

- Skytron LLC

제7장 시장 기회 및 미래 동향

AJY 24.03.08The Global Operating Room Integration Market size is estimated at USD 2.57 billion in 2024, and is expected to reach USD 4.44 billion by 2029, growing at a CAGR of 11.57% during the forecast period (2024-2029).

The COVID-19 caused considerable wait times for patients standing by for surgery. A study published in the British Journal of Surgery showed that COVID-19 led to 28 million postponed or canceled surgeries globally in 2020 with millions of surgeries pushed into 2021. Thus, with thousands of patients facing delays in surgeries the necessity to enhance scheduling efficiencies has become more important. Furthermore, the pandemic has pushed market players to operate in new ways, thus accelerating digitization. Operating rooms and surgical procedures changed in the following three ways in response to the pandemic-increased pre-surgical planning, video conferencing, and remote post-surgical patient engagement.

The factors such as a surge in patient procedures for minimally invasive surgeries are the major driving factors for the growth of the market. This is mainly due to the increasing awareness about the surgical interventions to treat conditions such as obesity has led medical device manufacturers to develop advanced operating room integration. Additionally, growth in the geriatric population resulting in the rising demand for surgeries which results in a cumulative increase in the number of operating procedures is also expected to drive the growth of the market. For instance, in 2020, the article titled 'The Incidence and Cumulative Risk of Major Surgery in Older Persons in the United States mentioned that nearly 9 major surgeries were performed annually for every 100 older persons, and more than 1 in 7 Medicare beneficiaries underwent a major surgery over 5 years, representing nearly 5 million unique older people.

Moreover, the rising burden of chronic disease across the globe is also one of the major factors increasing the demand for the operating room, as end-stage chronic diseases generally demand surgery. For instance, as per the American Health Association, in 2022, operating rooms resumed their activities and observed an upsurge in medical health treatments and surgeries, leading to only a 10% lower rate of surgery by the end of 2020 in comparison to 2019. Moreover, per the Organization for Economic Cooperation and Development (OECD), the number of cataract surgical procedures reported in 2020 in Turkey was 393,901. According to the same source, the number of hip replacement procedures in Italy in 2020 was 84,647, and cesarean section procedures were approximately 114,601. Thus, this growth in the number of surgical procedures will likely increase the demand for the operating room, thereby contributing to market growth.

Thus the above-mentioned factors are expected to drive the growth of the market during the forecast period.

Operating Room Integration Market Trends

The Cardiovascular Surgery Segment is Expected to Hold a Major Market Share in the Operating Room Integration Market

The sudden outbreak of COVID-19 seemed to impede the growth of the market due to the sudden imposition of restrictions across the world by different governments. This reduced the manpower in the supply chain and also affected the manufacturing processes as well. However, the relaxation of strict lockdowns during the post-pandemic period has increased the patient influx and thereby propelling the growth of the market.

The Cardiovascular surgery segment is expected to hold a dominating share in the studied market owing to the surge in cardiovascular diseases and related surgeries across the globe. For instance, The data published by the European Heart network in 2021 reported that in the European Union, more than 60 million people live with cardiovascular disease and that close to 13 million new cases of cardiovascular diseases are diagnosed every year. Moreover, with the rising burden of diseases caused by unhealthy lifestyles, such as obesity, being overweight is expected to drive the growth of the market. The article published by A-mansia Biotech in 2020 states that more than 2 billion adults 18 years and older were overweight across the world. Of these, over 650 million were obese in the world. The World Health Organization (WHO) published in 2021 that modifiable behavioral risk factors such as tobacco use account for over 7.2 million deaths every year, and 1.6 million deaths annually can be attributed to insufficient physical activity. As per the study published by the British Heart Foundation in 2021, Around 371,000 heart procedures and operations in England in 2020. Also, the article published by the American Heart Association in 2021, Approximately 40,000 children undergo congenital heart surgery in the United States each year. Such an increasing number of cardiovascular surgeries leads to the rise in the demand for cardiovascular surgery and better operating room integration procedures.

Thus, the above-mentioned factors are expected to drive the growth of the studied segment during the forecast period.

North America is Expected to Hold a Significant Share in the Market and is expected to do the Same in the Forecast Period.

The United States is likely to command the global market due to the growing prevalence of chronic diseases and the rising adoption of advanced surgical treatment methodologies in the region. For instance, as per the National Center for Chronic Disease Prevention and Health Promotion (January 2021), 6 in 10 adults in the United States have a chronic disease, and 4 in 10 adults have two or more chronic diseases, and these conditions are posing around USD 3.8 trillion of healthcare costs on the country's healthcare system. Furthermore, due to the high growth potential of the United States operating room integration market, the companies operating in the country are filing for market strategies to have the edge over their competitors, which is further expected to augment the growth of the studied market in the country over the forecast period. For instance, in June 2021, Getinge revealed that it released the 'Torin' AI-based OR management system in the United States.

Additionally, an increase in research and development activities, quick adaptability to advanced technology, and the presence of favorable healthcare infrastructure are fueling the growth of the overall regional market to a large extent.

Operating Room Integration Industry Overview

The operating room integration market is fragmented and competitive and consists of several major players. In terms of market share, a few of the major players are currently dominating the market. Some of the companies which are currently dominating the market are Brain Lab AG, Canon Inc., Doricon Medical Systems, Getinge AB, Karl Storz GMBH, Olympus Corporation, Merivaara Corp., Steris PLC, Stryker Corporation, Skytron LLC, and others..

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in number of surgical procedures

- 4.2.2 Surge in patient preference for minimally invasive surgeries and Patient Safety concerns in operating room

- 4.3 Market Restraints

- 4.3.1 High cost and maintenance of the operating room integration

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Application

- 5.2.1 General Surgery

- 5.2.2 Orthopedic Surgery

- 5.2.3 Cardiovascular Surgery

- 5.2.4 Neurosurgery

- 5.2.5 Others

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Brain Lab AG

- 6.1.2 Canon Inc

- 6.1.3 Doricon Medical Systems

- 6.1.4 Getinge AB

- 6.1.5 Karl Storz GMBH & Co. KG

- 6.1.6 Olympus Corporation

- 6.1.7 Merivaara Corp.

- 6.1.8 Steris PLC

- 6.1.9 Stryker Corporation

- 6.1.10 Skytron LLC