|

시장보고서

상품코드

1437610

사격 통제 시스템 : 시장 점유율 분석, 업계 동향과 통계, 성장 예측(2024-2029년)Fire Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

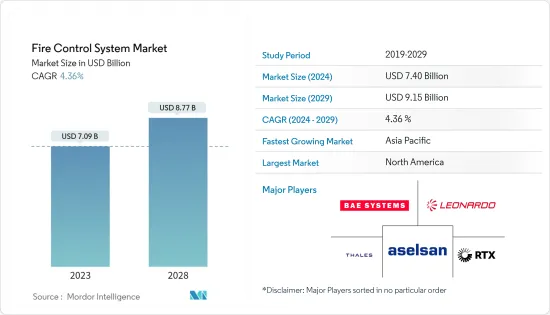

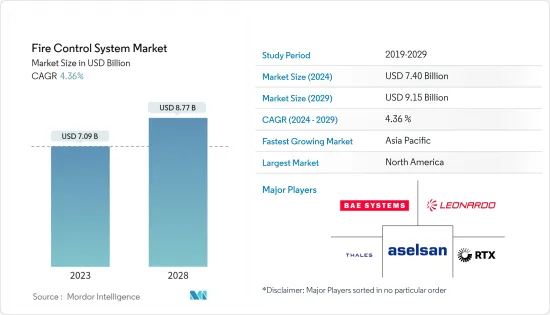

사격 통제 시스템 시장 규모는 2024년에 74억 달러로 추정되고 2029년까지 91억 5,000만 달러에 달할 것으로 예측되고 있으며, 예측 기간(2024-2029년) 중 4.36%의 CAGR로 성장합니다.

주요 하이라이트

- 사격통제시스템은 군 및 방위산업에서 폭넓게 활용될 수 있습니다. 군의 정밀 무기 수요 증가, 원격조종무기(ROP) 스테이션 수 증가, 국방비 지출 증가로 인해 사격통제시스템 세계 시장은 빠르게 성장하고 있습니다.

- 지향성 에너지 무기(DEW)의 출현은 군적 용도에서 엄청난 잠재력을 가지고 있으며, 공격 및 방어 무기 개발 및 운영 비용을 크게 절감할 수 있습니다. DEW의 광범위한 채택은 시장 역학에 근본적인 변화를 일으킬 수 있습니다.

- 억제력과 같은 기술적 제한과 액티브 방호 시스템 사용 증가는 시스템 설계자에게 도전이 되고 있습니다. 최신 전자 시스템은 비용이 많이 들기 때문에 화재 안전 표준을 준수해야 할 필요성이 증가하고 있습니다.

사격통제 시스템 시장 동향

사격통제시스템 시장의 공수 플랫폼 부문은 큰 폭으로 성장할 것으로 추정

사격통제시스템은 전투기에서 공대공 임무에서 목표물을 정확하게 공격하기 위해 매우 중요합니다. 전 세계의 모든 전투기와 헬리콥터에는 사격 통제 시스템이 장착되어 있습니다. 공수 플랫폼도 다양한 작전을 수행할 수 있는 다임무 전투기를 지원하기 위해 개발되었습니다. 이 플랫폼은 방공, 근접항공지원, 폭격, 지휘통제, 공중권, 정찰 등 다양한 임무에 사용할 수 있습니다.

2023년 9월, 미 해군은 미 해군 항공시스템사령부(NAVAIR)와 8억 4,550만 달러 규모의 델타 시스템 소프트웨어 구성(DSSC) E-2D 플랫폼 계약을 체결하고 2028년 운용을 개시할 예정입니다. 이 계약에는 유리 조종석 외에도 해군 통합 사격통제(NIFC)의 일부인 협력 교전(CEC) 기능과 비행 중 급유 기능도 포함됩니다.

이러한 플랫폼은 지휘통제, 방공, 폭격, 제압, 근접항공지원, 정찰 및 기타 임무를 수행할 수 있습니다. 마찬가지로 2023년 6월, 에어버스 헬리콥터스는 독일 공군의 CH-53GS/GE 운송 헬리콥터에 공중전자전 자기방어(AEWS) 시스템을 공급하기 위해 엘비트 시스템즈와 새로운 계약을 체결했습니다. 이 계약에는 디지털 레이더 경보 수신기(DRW), 전자전 컨트롤러(EWC) 및 대책 분배 시스템(CMDS)이 포함되어 헬리콥터의 운영 효율성과 임무 성공률을 향상시킬 수 있습니다. 이러한 발전은 이 부문의 성장을 가속할 것으로 예상됩니다.

예측 기간 중 북미가 시장을 독점

이 지역의 주요 방위 주체인 미국은 무력 전쟁의 선구자이며, 첨단 무기 시스템 조달의 꾸준한 성장을 통해 군적 우위의 정점에 서 있습니다.

전쟁의 성격 변화는 미 국방부가 군의 더 나은 무기 장비에 대한 지출을 늘리는 주요 이유 중 하나입니다. 2023년 11월, L3 Harris Technologies는 미군과 전 세계 동맹군이 전장에서 우위를 점할 수 있도록 지원하는 로켓 발사 로켓 사격 통제 시스템을 개발 및 업그레이드하는 계약을 체결했습니다. 각각 미화 1억 2,400만 달러 상당의 계약으로 L3 Harris는 공통 사격통제 시스템을 제공할 수 있게 되었습니다.

새로운 무기는 신뢰할 수 있는 작동을 보장하고 새롭게 통합된 설계 변경으로 인한 성능 향상 수준을 추정하기 위해 광범위한 테스트를 거치게 됩니다. 예를 들어 2022년 7월General Dynamics의 사업부 인 General Dynamics Mission Systems는 콜롬비아 급 및 드레드노트 급 탄도 미사일의 개발, 제조 및 설치를 지원하기 위해 미 해군 계약을 2억 7,990만 달러 상당의 미 해군 계약을 체결했습니다. 미사일 잠수함.

예를 들어 이 지역의 다른 주요 군에서 스웨덴의 Aimpoint는 2022년 11월 캐나다 국방부(DoD)에 FCS13-RE 사격통제시스템(FCS) 및 TH-60 열화상 조준경 공급 계약을 체결하였습니다. 배치된 작전에서 FCS 13-RE는 캐나다의 작동 불가능한 Saab(Saab M3) 84mm 칼 구스타프 무기의 주요 주야간 제어 시스템(FCCS)으로 사용됩니다.

또한 정밀유도무기 배치, 연구개발 투자 증가, 방위산업의 현대화 노력에 대한 관심이 높아짐에 따라 이 지역의 사격통제시스템 세계 시장은 더욱 확대될 것으로 보입니다.

사격 통제 시스템 산업 개요

이 시장은 본질적으로 반통합적이며, 특히 Leonardo SpA, RTX Corporation, BAE Systems plc, Rheinmetall AG, ASELSAN AS, THALES와 같은 주요 기업이 존재합니다. 시장은 경쟁이 치열하며, 유명한 업체들이 더 큰 시장 점유율을 차지하기 위해 경쟁하고 있습니다.

국방 분야의 엄격한 안전 및 규제 정책으로 인해 신규 진입이 제한될 것으로 예상됩니다. 또한 기술 기반 플랫폼의 매출은 주로 미국 및 아시아태평양과 같은 주요 시장의 경제 상황에 영향을 받습니다. 따라서 경기 침체기에는 구매가 연기되거나 취소되어 도입 속도가 상대적으로 느려질 수 있으며 그 결과 시장 역학에 부정적인 영향을 미칠 수 있습니다.

또한 계약에는 종종 상계 조항이 포함되어 있으며, 프로젝트가 적시에 완료될 수 있는 위험이 증가합니다. 기술적 측면과 관련된 위험으로 인해 활동의 일정과 비용은 거시경제적 요인에 따라 변경될 수 있으며, 이는 계약 관련 당사자의 관련 이익에 영향을 미칠 수 있습니다.

기타 혜택

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 촉진요인

- 시장 억제요인

- Porter's Five Forces 분석

- 신규 진출업체의 위협

- 구매자의 교섭력

- 공급 기업의 교섭력

- 대체품의 위협

- 경쟁 기업간 경쟁의 강도

제5장 시장 세분화

- 시스템

- 목표 획득·지도 체제

- 인터페이스 시스템

- 내비게이션 시스템

- 기타 시스템

- 플랫폼

- 지상파

- 항공사진

- 해군

- 지역

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 기타 라틴아메리카

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 이집트

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 벤더의 시장 점유율

- 기업 개요

- ASELSAN AS

- BAE Systems plc

- Elbit Systems Ltd.

- General Dynamics Corporation

- Indra Sistemas, SA

- Leonardo SpA

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Rheinmetall AG

- Saab AB

- Safran SA

- THALES

- Ultra Electronics

제7장 시장 기회와 향후 동향

KSA 24.03.07The Fire Control System Market size is estimated at USD 7.40 billion in 2024, and is expected to reach USD 9.15 billion by 2029, growing at a CAGR of 4.36% during the forecast period (2024-2029).

Key Highlights

- Fire control systems can be used by the military and defense industry for a wide range of applications. The global market for fire control systems is growing rapidly due to the increasing demand for precision weapons in the military, the increasing number of remotely operated weapon (ROP) stations, and the increase in defense spending.

- The emergence of directed energy weapons (DEW) possesses immense potential for military applications and could dramatically reduce the cost associated with the development and operation of both offensive and defensive weaponry. Widespread adoption of DEWs can trigger a radical change in market dynamics.

- Technological limitations, such as deterrents, and the increasing use of active protection systems pose a challenge to system designers. Due to the high cost of modern electronic systems, the need to comply with fire safety standards has increased.

Fire Control System Market Trends

The Airborne Platform Segment of the Fire Control System Market is Estimated to Grow Significantly

Fire control systems are critical in combat aircraft for accurately hitting targets in air-to-air missions. Every other fighter aircraft and helicopter in the world is outfitted with fire control systems. Airborne platforms have also been developed to support multi-mission warfare machines that can carry out a variety of operations. These platforms can be utilized for a variety of tasks, including air defense, close air support, bombing, command and control, air dominance, and reconnaissance.

In September 2023, the US Navy awarded a contract for USD 845.5 million to the US Naval Air Systems Command (NAVAIR) for a delta system software configuration (DSSC) E-2D platform scheduled to enter service in 2028. The platform is equipped with a glass cockpit, as well as the capability of cooperative engagement (CEC), which is part of the Naval Integrated Fire Control (NIFC) as well as the in-flight refueling capability.

These platforms are capable of command and control, air defense, bombing, air domination, close air support, reconnaissance, and other missions. Similarly, in June 2023, Airbus Helicopters awarded Elbit Systems a new contract to supply Airborne Electronic warfare self-protection (AEWS) systems for German air force CH-53GS/GE transport helicopters. The contract covers Digital Radar Warning Receivers (DRW), Electronic Warfare Controllers (EWC) and Countermeasure Dispensing Systems (CMDS) to improve the helicopter's operational efficiency and mission success. These developments are expected to aid the segment growth.

North America to Dominate the Market During the Forecast Period

The major defense player in the region, the US has been the pioneer of armed warfare and has positioned itself at the apex of military dominance through a steady growth in the procurement of advanced weapon systems.

The changing nature of warfare is one of the prime reasons for the US DoD's increased spending toward arming its armed forces with better weapons. In November 2023, L3Harris Technologies won contracts to develop and upgrade fire control systems for rocket launch vehicles that assist the United States Army and allied forces worldwide in achieving battlefield superiority. The contracts, valued at USD 124 million each, will enable L3Harris to provide a common fire control system.

New weapons are subjected to extensive testing to ensure reliable operation and estimate the level of performance enhancement due to a newly integrated design change. For instance, In July 2022, General Dynamics Mission Systems, a business unit of General Dynamics was awarded a U.S. Navy contract worth USD 279.9 million to support the development, production, and installation of fire control systems for the Columbia- and Dreadnought classes of ballistic missile submarines.

Other major armed forces in the region for instance, in November 2022, Sweden's Aimpoint was awarded a contract to supply the Canada Department of Defence (DoD) with a range of FCS13-RE Fire Control System (FCS) and TH-60 thermal sight .On deployed operations, the FCS 13-RE will be used as the main day and night control system (FCCS) on Canada's in-operable Saab (Saab M3) 84mm Carl Gustav weapons.

In addition, the increased focus on the deployment of precision-guided weapons, increased research and development investments, and modernization initiatives in the defense industry will further expand the global market for fire control systems in the region.

Fire Control System Industry Overview

The market is semi-consolidated in nature with a presence of major players such as Leonardo S.p.A., RTX Corporation and BAE Systems plc., Rheinmetall AG, ASELSAN A.S., and THALES among others. The market is highly competitive, and the prominent players are competing for a larger market share.

The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. Furthermore, the sales of technology-based platforms are primarily influenced by the prevalent economic situations in dominant markets such as the US and Asia-Pacific. Hence, in periods of economic downturn, purchases may be subjected to deferral or cancellation and a relatively slower rate of adoption, which in turn, can adversely affect the market dynamics.

Moreover, the contracts are often subjected to include offset clauses which enhances the risks of timely completion of the project. Since the associated risks regarding the technical aspects, scheduling of activities and costs are subject to change based on macroeconomic factors and subsequently influence the associative profits of the associated parties in a contract.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 System

- 5.1.1 Target Acquisition and Guidance System

- 5.1.2 Interface System

- 5.1.3 Navigation System

- 5.1.4 Other Systems

- 5.2 Platform

- 5.2.1 Terrestrial

- 5.2.2 Aerial

- 5.2.3 Naval

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 ASELSAN A.S.

- 6.2.2 BAE Systems plc

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 General Dynamics Corporation

- 6.2.5 Indra Sistemas, S.A.

- 6.2.6 Leonardo S.p.A.

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Northrop Grumman Corporation

- 6.2.9 RTX Corporation

- 6.2.10 Rheinmetall AG

- 6.2.11 Saab AB

- 6.2.12 Safran SA

- 6.2.13 THALES

- 6.2.14 Ultra Electronics