|

시장보고서

상품코드

1851065

항공기용 보조 동력 장치(APU) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aircraft Auxiliary Power Unit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

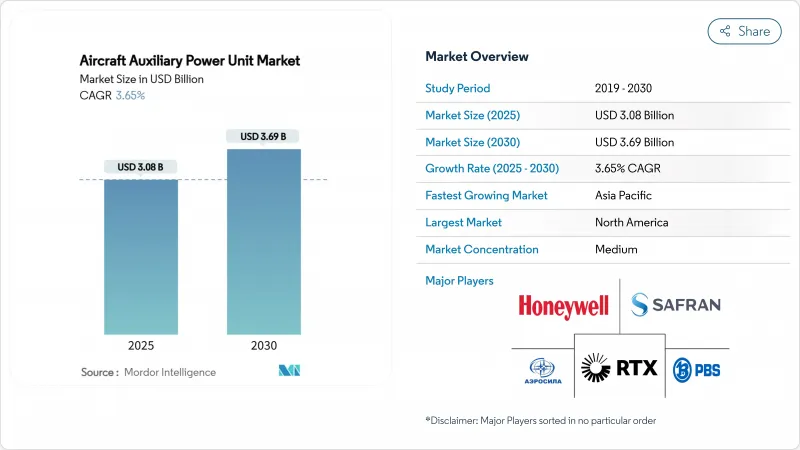

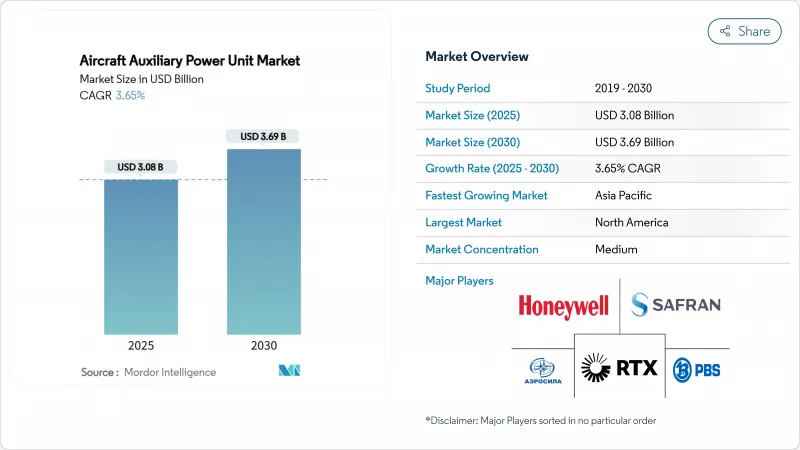

항공기용 보조 동력 장치(APU) 시장 규모는 2025년에 30억 8,000만 달러로 추정되고, 2030년에는 36억 9,000만 달러에 이를 전망이며, CAGR 3.65%로 성장할 것으로 예측됩니다.

완만한 확대는 항공사가 전기 시스템 및 수소 대응 시스템으로 이동하는 한편, 규제 당국이 지상 배출 규제를 강화하고 기상 APU보다 게이트에서 공급되는 전력을 우선시하고 있기 때문입니다. APU 오프 정책을 시행하는 공항은 고정 전력으로 인한 지상 전력을 사용할 수 있는 경우 램프 배출량을 최대 50% 삭감합니다. 민간 항공사는 단일 통로 납품으로 수량을 벌고, 군는 회전익 업그레이드로 기술 요구를 가속화하며, UAV 조달 증가는 초소형 정격 유닛 수요를 확대합니다. 에어버스가 수소 APU를 검증하고 하니웰이 기존 제품 라인 전체에서 100% 지속 가능한 항공연료 인증을 위한 경쟁을 벌이는 가운데 연료전지 프로토타입이 기세를 늘리고 있습니다. 한편, 희토류 규제가 공급망에 미치는 영향으로 서양 OEM은 발전기 재설계와 조달 대상의 다양화를 강요합니다.

세계의 항공기용 보조 동력 장치 시장 동향 및 인사이트

차세대 저연비 내로우 바디기 납품 증가

중국의 민간 항공기는 2043년까지 2배의 9,740기가 될 것으로 예상되고 있으며, 단통로 운항에 최적화된 APU에 대한 수요가 지속적으로 높아지고 있습니다. 에어 아라비아와 같은 항공사는 고효율 모드에서 1-2%의 연료 절약을 확보하기 위해 A320neo형기에 131대의 하니웰 131-9A 유닛을 선택했습니다. 신속한 시동과 최소한의 열 부하를 중시한 컴팩트한 아키텍처는 사이클이 높은 내로우 바디 스케줄에 적합합니다. LEAP 엔진과의 시너지 효과는 항공사가 기존 CFM56 플릿에서 대체할 때 파견 신뢰성을 향상시킵니다. 이러한 납품의 파도는 항공기용 보조 동력 장치 시장의 라인 피팅 수익 및 예비 파이프라인의 확대를 지원합니다.

규제에 의한 APU 오프 의무화에 의한 레트로 피트 증가

유럽의 허브 공항에서는 항공기 턴어라운드 시 지상 전력을 사용해야 하므로 항공사는 새로운 APU를 조달하는 대신 호환되는 인터페이스 키트를 사용하여 레거시 기계를 업그레이드해야 합니다. 카타르 항공은 지역 최초의 HGT1700 오버홀 능력을 확보하여 자산 수명을 연장하면서 컴플라이언스 비용을 절감했습니다. 아사이아의 램프 모니터링 분석을 통해 공항은 APU OFF 준수를 검증할 수 있으며 자발적인 에코 대책을 강제 업그레이드로 바꿀 수 있습니다. 그 결과, 애프터마켓의 마진은 오리지널 기기의 판매 대수가 두드러지더라도 상승해, 기존 공급자에게 매력적인 서비스 수입을 제공합니다.

발전기 부품에 사용되는 희토류 재료의 가격 불안정성

중국에 의한 네오디뮴과 디스프로슘의 수출 억제는 자석 비용을 상승시키고 APU 영구 자석 발전기의 가격 설정을 불안정하게 만듭니다. 미국 공군의 분석은 항공우주 공급 취약성의 상위 수준에 희토류 의존성을 포함하고 있으며, OEM은 출력 밀도를 손상시킬 수 있는 재활용 및 페라이트 기반 설계를 검토하도록 촉구하고 있습니다. 계약 가격은 현재 상용 익스포저에 연동되어 있으며 장기 유지 보수 계약에 영향을 미치고 항공기용 보조 동력 장치 시장 전체의 마진을 침식하고 있습니다.

부문 분석

상업용 부문은 2024년 매출의 68.21%를 차지했으며, 항공기용 보조 동력 장치 시장의 뼈대를 유지하고 있습니다. 라인 핏 수요는 에어 버스 및 보잉의 증산과 일치하며, 항공사는 배기가스 규제를 충족하기 위해 APU의 교환이 아닌 개수를 추구하고 있습니다. 군용 플랫폼은 현재의 베이스는 작지만, 미국의 회전익 현대화 등 프로그램이 보다 고출력의 전기 시스템을 지정하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 4.69%로 가속할 전망입니다. 이러한 국방의 순풍은 민간기에 대한 기술 파급을 지지하고 항공기용 보조 동력 장치 산업 전체의 가치 창조를 지속시킵니다.

아시아와 북미에서 지속적인 내로우 바디 머신 공급이 양을 지원하는 반면, 와이드 바디 머신은 갤리와 환경 제어 팩에 전력을 공급하기 위해 더 높은 정격 APU가 필요합니다. 군용기에서 UAV와 운송기는 마이크로 정격 및 매크로 정격 솔루션을 채택하여 용도의 폭을 넓히고 있습니다. 비즈니스 제트기는 신속한 스풀업과 캐빈의 편안함을 중시하는 프리미엄 틈새를 형성하여 평균 이상의 애프터마켓 수익률을 창출하고 있습니다.

고정익기는 단통로기의 생산 사이클과 화물기로의 전환을 반영해 2024년 출하를 80.65% 유지했습니다. 회전익의 업그레이드는 보다 깨끗한 전기 공급을 필요로 하는 디지털 바이오닉스 및 전자전 패키지를 포함하는 프로그램에 뒷받침되며 CAGR 3.87%를 추가합니다. 헬리콥터의 APU는 제한된 베이에 적합하며 진동을 견디어야 하며 소형화된 열교환기 및 가변 속도 아키텍처를 추진합니다.

신흥 eVTOL 프로토타입은 백업 전원 및 시스템 이중화를 위해 보조 발전에 의존하며 새로운 설계 기준을 제시합니다. 에어 버스 A330의 고정 날개 연료전지 테스트는 인증 장애물이 지워지면 장거리 플랫폼이 대체 에너지로 축 발을 옮길 가능성을 보여 항공기용 보조 동력 장치 시장 전망 수요 패턴을 설정합니다.

지역 분석

북미는 2024년에 32.78%의 점유율을 유지해, 차세대 솔루션의 연구개발을 맡는 보잉의 납품과 국방부의 지속적인 지출에 지지를 받았습니다. 국내의 중요한 광물 처리에 대한 정부의 자극책도 희토류에 대한 노출을 줄이기 위한 것입니다. 항공기용 보조 동력 장치 시장 규모는 GTF와 LEAP 함대가 성숙하고 무거운 정비 사이클에 들어가면서 꾸준히 성장할 것으로 예측됩니다.

아시아태평양은 2030년까지 CAGR 5.40%로 가장 급성장이 전망되고 있으며 중국의 C919 롤아웃과 인도의 2043년까지 19,500대의 신규 항공기 예측에 견인되고 있습니다. Safran-HAL과 같은 합작 투자는 부품 생산을 현지화하고, 리드 타임을 단축하며, 지역의 오프셋 지령에 맞춥니다. 지역 함대가 2043년까지 1,290억 달러의 서비스 금액에 도달하여 항공기용 보조 동력 장치 시장의 발자국이 깊어짐에 따라 애프터마켓 수익이 증가합니다.

유럽은 깨끗한 항공 산하의 낮은 배출 전력 유닛을 추진하기 위한 정책적 리더십을 활용합니다. 수소 인프라 파일럿과 엄격한 APU 오프 시행은 낮은 NOx 연소와 연료전지의 기술 혁신을 촉진합니다. 지상 전원의 보급은 유닛 판매를 억제하는 한편, 엄격한 턴어라운드와 환경 컴플라이언스에 직면하는 항공사를 만족시키는 초고효율 제품을 제공하도록 공급자에게 압력을 가합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 차세대 저연비 내로우 바디기의 납입 증가

- APU 오프 운용의 규제 의무화에 의한 레트로 피트 활동의 활성화

- 고위협 환경에서의 군용 UAV 플릿 확대

- 지상 업무의 전기가 e-APU 채용 촉진

- 마이크로 APU 수요를 낳는 민간 우주기의 출현

- 하이브리드 전기 추진 아키텍처에 APU 통합

- 시장 성장 억제요인

- 발전기 부품에 사용되는 희토류 재료의 가격 불안정성

- 공항용 지상 동력 장치에 대한 기호성에 의해 APU 가동 시간 감소

- 신에너지 APU 기술을 위한 길고 엄격한 인증 프로세스

- 소형 항공기용 APU 설계에서 열 관리 과제

- 밸류체인 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 플랫폼별

- 상업용

- 내로우 바디 항공기

- 와이드 바디 항공기

- 지역 제트

- 군용

- 전투

- 특별 미션

- 수송

- 트레이너

- 무인 항공기(UAVs)

- 일반항공

- 경비행기

- 비즈니스 제트

- 헬리콥터

- 상업용

- 항공기 유형별

- 고정익

- 회전익

- 정격 출력별

- 50kVA 미만

- 50-150kVA

- 150kVA 이상

- 기술별

- 기존 터보샤프트

- 배터리 및 일렉트릭

- 연료전지

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 남미

- 브라질

- 기타 남미

- 중동 및 아프리카

- 중동

- 아랍에미리트(UAE)

- 사우디아라비아

- 카타르

- 기타 중동

- 아프리카

- 남아프리카

- 이집트

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Honeywell International Inc.

- RTX Corporation

- Safran SA

- JSC SPE Aerosila

- Technodinamika(Rostec)

- PBS Group as

- Rolls-Royce plc

- Motor Sich JSC

- Aegis Power Systems, Inc.

- Eaton Corporation plc

- Liebherr Aerospace(Liebherr Group)

- Jakadofsky GmbH

제7장 시장 기회 및 향후 전망

AJY 25.11.12The aircraft auxiliary power unit (APU) market size stands at USD 3.08 billion in 2025 and is forecasted to reach USD 3.69 billion by 2030, advancing at a CAGR of 3.65%.

Moderate expansion stems from airlines shifting toward electrified and hydrogen-ready systems while regulators tighten ground-emissions rules that favor gate-supplied electricity over onboard APUs. Airports enforcing APU-off policies cut ramp emissions up to 50% whenever fixed electrical ground power is available. Commercial airlines command volume through single-aisle deliveries, militaries accelerate technology needs in rotary-wing upgrades, and rising UAV procurement widens demand for micro-rated units. Fuel-cell prototypes gain momentum as Airbus validates hydrogen APUs and Honeywell races to certify 100% sustainable aviation fuel across its conventional line. Meanwhile, supply chain exposure to rare-earth restrictions forces Western OEMs to redesign generators and diversify sourcing.

Global Aircraft Auxiliary Power Unit Market Trends and Insights

Increased Deliveries of Next-Gen Fuel-Efficient Narrowbody Aircraft

China's commercial fleet is expected to double to 9,740 aircraft by 2043, underscoring the sustained demand for APUs optimized for single-aisle operations. Airlines such as Air Arabia selected 131 Honeywell 131-9A units for A320neo aircraft to secure 1-2% fuel savings in High Efficiency Mode. Compact architectures emphasizing rapid starts and minimal thermal loads suit higher-cycle narrowbody schedules. Synergies with LEAP engines enhance dispatch reliability as carriers replace legacy CFM56 fleets. This delivery wave underpins line-fit revenue and a growing spares pipeline for the aircraft auxiliary power unit market.

Rising Retrofit Activity Due to Regulatory APU-Off Mandates

European hubs now enforce electrical ground power use during turnarounds, forcing carriers to upgrade legacy jets with compatible interface kits rather than procure new APUs. Qatar Airways secured the region's first HGT1700 overhaul capacity to cut compliance costs while extending asset life. Assaia's ramp-monitoring analytics enable airports to validate APU-off adherence, converting voluntary eco-measures into compulsory upgrades. As a result, aftermarket margins rise even as original-equipment volumes plateau, offering attractive service income for established suppliers.

Price Instability of Rare-Earth Materials Used in Generator Components

China's export curbs on neodymium and dysprosium inflate magnet costs, creating pricing uncertainty for APU permanent-magnet generators. US Air Force analyses list rare-earth dependence among top aerospace supply vulnerabilities, prompting OEMs to explore recycling and ferrite-based designs that may compromise power density. Contract pricing is now indexed to commodity exposure, affecting long-term maintenance agreements and eroding margins across the aircraft auxiliary power unit market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Military UAV Fleets in High-Threat Environments

- Electrification of Ground Operations Driving Adoption of e-APUs

- Preference for Airport Ground Power Units Reducing APU Operating Hours

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The commercial segment generated 68.21% of 2024 revenue and retains the backbone of the aircraft auxiliary power unit market. Line-fit demand matches Airbus and Boeing production ramps, while airlines pursue APU refurbishments instead of replacements to meet emission rules. Military platforms contribute a smaller base today but accelerate at 4.69% CAGR through 2030 as programs such as US rotary-wing modernization specify higher-output electric systems. This defense tailwind supports technology spillovers into civil variants, sustaining value creation across the aircraft auxiliary power unit industry.

Sustained narrowbody deliveries in Asia and North America anchor volume, whereas widebody jets require higher-rated APUs to power galleys and environmental control packs. On the military side, UAVs and transport aircraft adopt micro-and macro-rated solutions, broadening the application matrix. Business jets form a premium niche valuing rapid spool-up and cabin comfort, generating above-average aftermarket yields.

Fixed-wing deliveries kept an 80.65% hold on 2024 shipments, reflecting single-aisle production cycles and freighter conversions. Rotary-wing upgrades add 3.87% CAGR, propelled by programs that embed digital avionics and electronic warfare packages requiring a cleaner electrical supply. Helicopter APUs must fit constrained bays and tolerate vibration, driving miniaturized heat exchangers and variable-speed architectures.

Emerging eVTOL prototypes rely on auxiliary generation for backup power and system redundancy, injecting new design criteria. Fixed-wing fuel-cell trials on Airbus A330 demonstrate how long-range platforms may pivot toward alternative energy once certification hurdles are cleared, setting future demand patterns for the aircraft auxiliary power unit market.

The Aircraft Auxiliary Power Unit (APU) Market Report is Segmented by Platform (Commercial, Military, and General Aviation), Aircraft Type (Fixed-Wing and Rotary-Wing), Power Rating (Less Than 50 KVA, 50 To 150 KVA, and More Than 150 KVA), Technology (Conventional Turboshaft, Battery-Electric, and Fuel-Cell), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained a 32.78% share in 2024, anchored by Boeing deliveries and sustained Pentagon spending that underwrite R&D for next-generation solutions. Government stimulus for domestic critical minerals processing also intends to reduce rare-earth exposure. The aircraft auxiliary power unit market size is forecasted to grow steadily as GTF and LEAP fleets mature and enter heavy maintenance cycles.

Asia-Pacific is the fastest riser at 5.40% CAGR through 2030, driven by China's C919 rollout and India's forecast for 19,500 new aircraft by 2043. Joint ventures such as Safran-HAL localize parts production, trimming lead times, and aligning with regional offset mandates. Aftermarket revenues will multiply as the regional fleet reaches 129 USD billion service value by 2043, deepening the aircraft auxiliary power unit market footprint.

Europe leverages policy leadership to push low-emission power units under the Clean Aviation umbrella. Hydrogen infrastructure pilots and stringent APU-off enforcement foster innovation in low-NOx combustion and fuel cells. While ground power prevalence tempers unit sales, it pressures suppliers to deliver ultra-efficient products that satisfy airlines facing tight turnaround and environmental compliance.

- Honeywell International Inc.

- RTX Corporation

- Safran SA

- JSC SPE Aerosila

- Technodinamika (Rostec)

- PBS Group a.s.

- Rolls-Royce plc

- Motor Sich JSC

- Aegis Power Systems, Inc.

- Eaton Corporation plc

- Liebherr Aerospace (Liebherr Group)

- Jakadofsky GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased deliveries of next-gen fuel-efficient narrowbody aircraft

- 4.2.2 Rising retrofit activity due to regulatory mandates on APU-off operations

- 4.2.3 Expansion of military UAV fleets in high-threat environments

- 4.2.4 Electrification of ground operations driving adoption of e-APUs

- 4.2.5 Emergence of commercial spaceplanes creating demand for micro-APUs

- 4.2.6 Integration of APUs into hybrid-electric propulsion architectures

- 4.3 Market Restraints

- 4.3.1 Price instability of rare-earth materials used in generator components

- 4.3.2 Preference for airport ground power units reducing APU operating hours

- 4.3.3 Lengthy and rigid certification processes for new-energy APU technologies

- 4.3.4 Thermal management challenges in compact aircraft APU designs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Commercial

- 5.1.1.1 Narrowbody Aircraft

- 5.1.1.2 Widebody Aircraft

- 5.1.1.3 Regional Jets

- 5.1.2 Military

- 5.1.2.1 Combat

- 5.1.2.2 Special Mission

- 5.1.2.3 Transport

- 5.1.2.4 Trainer

- 5.1.2.5 Unmanned Aerial Vehicles (UAVs)

- 5.1.3 General Aviation

- 5.1.3.1 Light Aircraft

- 5.1.3.2 Business Jets

- 5.1.3.3 Helicopters

- 5.1.1 Commercial

- 5.2 By Aircraft Type

- 5.2.1 Fixed-Wing

- 5.2.2 Rotary-Wing

- 5.3 By Power Rating

- 5.3.1 less than 50 kVA

- 5.3.2 50 to 150 kVA

- 5.3.3 more than 150 kVA

- 5.4 By Technology

- 5.4.1 Conventional Turboshaft

- 5.4.2 Battery-Electric

- 5.4.3 Fuel-Cell

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 RTX Corporation

- 6.4.3 Safran SA

- 6.4.4 JSC SPE Aerosila

- 6.4.5 Technodinamika (Rostec)

- 6.4.6 PBS Group a.s.

- 6.4.7 Rolls-Royce plc

- 6.4.8 Motor Sich JSC

- 6.4.9 Aegis Power Systems, Inc.

- 6.4.10 Eaton Corporation plc

- 6.4.11 Liebherr Aerospace (Liebherr Group)

- 6.4.12 Jakadofsky GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment